Navigating the Challenges of Medical Device Technology Translation: Insights from Zhou Mi of Puhua Capital

Abstract: The core proposition of venture capital in the medical device sector lies in the clinical and commercial translation of intellectual property or scientific and technological achievements. Such translation requires close collaboration among industry, academia, research institutions, and healthcare providers, with venture capital firms and government agencies serving as key driving forces behind it. This article uses representative domestic and international investment cases by Puhua Medical—Oxford Nanopore Technologies and Micro-Tech (Nanjing) Co., Ltd.—to illustrate how medical device technology translation can bridge the two “valleys of death.”

Author | Zhou Mi, Managing Partner of Healthcare Investment at Puhua Capital

Recently, the 2021 China Biotechnology Innovation Conference (3rd Edition), a national-level flagship event in the biotechnology sector, opened in Chengdu. This year’s conference featured the largest number of academicians and experts in its history, bringing together nearly 30 academicians, more than 300 leading authorities, over 1,000 scholars and professionals, as well as representatives from nearly 20 Fortune Global 500 multinational pharmaceutical companies and more than 50 renowned domestic and international pharmaceutical enterprises, all convening in Chengdu to discuss the innovative development of China’s biotechnology industry.

Zhang Yudong, Vice Minister of the Ministry of Science and Technology, and Wang Fengchao, Deputy Secretary of the Chengdu Municipal Committee of the Communist Party of China and Mayor of Chengdu, attended the opening ceremony and delivered speeches. Chen Zhu, Vice Chairperson of the Standing Committee of the 13th National People’s Congress, Chairperson of the Central Committee of the Chinese Peasants and Workers Democratic Party, and Academician of the Chinese Academy of Sciences, delivered a speech via video link. Zhou Mi, Managing Partner of Medical Investment Management at Puhua Capital, was invited to attend and presented a report titled “Translation of Medical Devices.”

Zhou Mi, Managing Partner of Healthcare Investment Management at Puhua Capital

The following is the content of Zhou Mi’s report on “Medical Device Translation” at the 2021 China Biotechnology Innovation Conference (3rd Edition) – “Seminar on Achievements of National Key R&D Programs in the Field of Biology”.

Medical devices refer to instruments, equipment, appliances, in vitro diagnostic reagents and calibrators, materials, and other similar or related articles, including the required computer software, that are used directly or indirectly on the human body. Their intended primary action is obtained by physical or other means, rather than by pharmacological, immunological, or metabolic means, although such means may be involved but only play an auxiliary role.

Current Status of the Medical Device Industry

The medical device market is currently experiencing a golden period of growth,By the end of 2020, the market size of medical devices in China reached RMB 734.1 billion, representing a year-on-year growth of 18.3%, which was nearly four times the global growth rate for medical devices. China has become the world’s second-largest medical device market, after the United States.

Large Number of Medical Device Companies,Low Industry Concentration, the number of medical device manufacturers in China reached 26,500, representing a 46.7% increase from the end of 2019, while the number of distributors stood at 898,600. The medical device market in China is characterized by intense competition, a fragmented landscape, and low industry concentration.

The Scale of Medical Device Products Continues to Rise Year by Year, in 2020, the total number of medical device product registrations in China reached 44,964, a year-on-year increase of 66.8%.

Driving Forces Behind Medical Device Commercialization: Significant Potential for Import Substitution of High-End Domestically Produced Medical Devices

Medical devices constitute a strategic emerging industry characterized by multidisciplinary integration, knowledge intensity, and high value-added. Technological innovation serves as the key driver for the sustainable development of this industry, while industry-academia-research collaboration has become a strategic measure to accelerate industrial innovation and the commercialization of scientific achievements, thereby enhancing the competitiveness of both products and enterprises.

Internal and External Factors Drive the Rise of Domestically Produced Medical Devices, underpinned by internal factors such as technological advancements and the maturation of the industrial chain, and bolstered by external factors including policies accelerating import substitution and capital inflows.

High-end medical devices urgently need to address their shortcomings,The total volume of medical device patents in China is on an upward trend, with continuous improvement in quality and certain breakthroughs achieved in the mid-to-high-end medical device sector. However, the high-end medical equipment market has long been monopolized by foreign enterprises. Multinational corporations represented by GE from the United States and Siemens from Germany firmly control key technologies and core components, capturing over 90% of the market share for high-end medical devices in China. Overcoming challenges in technological R&D and the commercialization of research achievements has become a critical pathway to enhancing the overall level of domestically produced high-end medical devices.

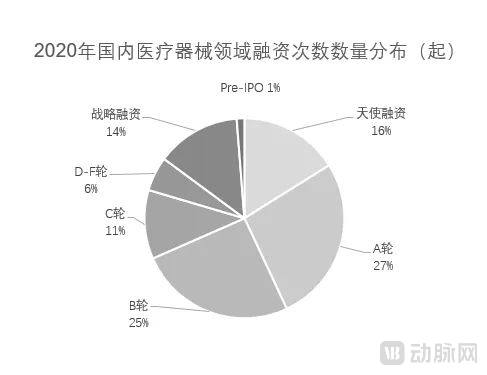

Financing Landscape for the Commercialization of Medical Devices: In 2020, there were 330 financing events in China's medical device sector, with a total financing volume of RMB 48 billion; 52% of these occurred at Series A and Series B stages. Interest in IVD (In Vitro Diagnostics) and cardiovascular sectors remained strong, while AI and robotics emerged as new favorites. In terms of the number of financing deals, the IVD and genetic testing sectors recorded 121 events, while the cardiovascular and AI-assisted healthcare sectors saw 33 events. Regarding financing volume, the IVD and genetic testing sectors raised over RMB 24.5 billion, the cardiovascular sector exceeded RMB 6.5 billion, and medical robotics surpassed RMB 4 billion.

The IVD sector has long been favored by investors.While the biochemical and immunological sectors are relatively mature, there remains significant potential for domestic substitution in molecular diagnostics and point-of-care testing (POCT).

High-value medical consumables are gradually drawing attention across various sectors.Driven by the national volume-based procurement policy and capital investment, the localization of cardiovascular interventional devices has accelerated significantly, while sectors such as orthopedic interventional devices, neurointerventional devices, dental devices, and ophthalmic devices are also gradually gaining attention.

Artificial Intelligence Wins Capital Favor. The integration of artificial intelligence with medical imaging has become a trend. For instance, Keya Medical received the first Class III medical AI device approval issued by China’s National Medical Products Administration (NMPA) and secured strategic financing in the hundreds of millions in February. Shukun Technology and Yizhun Intelligence have also each obtained financing in the hundreds of millions.

Medical Robots Experienced a Boom in 2020.In 2020, there were over 20 financing events in the medical robotics sector. Among them, Tinavi Medical Technologies was listed on the STAR Market, and MicroPort MedBot secured RMB 3 billion in strategic investment.

Policies for the Commercialization of Medical Devices: Opportunities and Challenges Coexist

During the 14th Five-Year Plan period, the medical device sector will focus on development in the following areas:Establish national laboratories; build major design innovation platforms; develop high-end medical equipment; create 5G application scenarios; provide policy incentives for corporate R&D and innovation; streamline domestic listing and financing channels for medical device companies.

The Outline of the 14th Five-Year Plan emphasizes,Promote the reform of centralized volume-based procurement and use of drugs and medical consumables organized at the national level.Driven by volume-based procurement, domestically produced high-value medical consumables will continue to strengthen their capabilities in talent development and R&D technology, thereby achieving price reductions alongside quality improvements.

The Medical Device Registrant System was piloted in 2017 and rolled out nationwide in April 2020.Decoupling registration from manufacturing unlocks idle industry resources; innovators can focus on product R&D, while production can be outsourced to qualified enterprises.

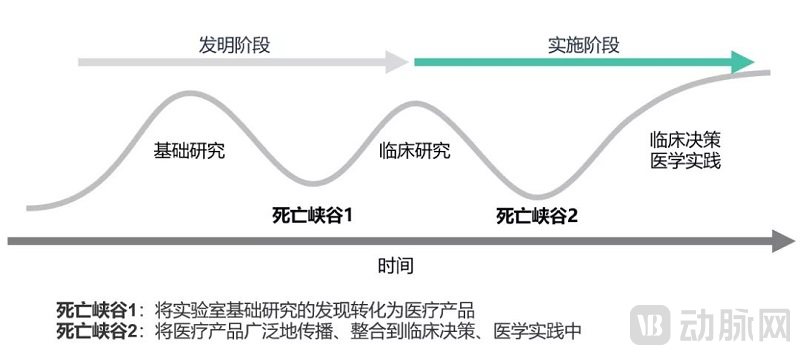

The momentum of technological development is strong, but the conversion rate of scientific and technological achievements remains low.

The commercialization rate of scientific and technological achievements in universities has long hovered between 4% and 5%.. In 2020, patents for medical devices granted to universities and research institutes in China accounted for 43% of the national total. However, the R&D outcomes from these institutions were primarily oriented toward academic research, with project initiation emphasizing theoretical and technological advancement rather than market demand due to a lack of market research. This disconnect has resulted in many developed products failing to gain market acceptance, and very few “hard patents” have successfully achieved industrialization and generated practical benefits.

The medical community has not truly integrated into the mainstream of translating scientific and technological achievements into practical applications.Physicians are not only users of medical device products but also drivers of innovation in this field, and even developers of new technologies. In the current environment, however, it is difficult for physicians to collaborate with universities, research institutes, and enterprises on technological R&D activities. Physicians who possess technical expertise or have innovative R&D ideas also face significant challenges in successfully translating their scientific and technological achievements into commercial products.

Enterprises lack strong motivation to engage in industry-university-research collaboration.China has over 17,000 medical device manufacturers, yet few possess substantial long-term technological expertise and hold independent intellectual property rights. The difficulty in commercializing technological achievements dampens enterprises’ enthusiasm for R&D, which in turn further reduces the pool of convertible technologies, creating a vicious cycle. Mechanisms for enterprises to adopt outcomes from universities and research institutes are inadequate, and profit-sharing models fail to accurately reflect each party’s contribution to the overall profitability of collaborative projects.

The foundation of medical device translation originates from clinical needs and their assessment,Key factors include: the identification of unmet or partially met clinical needs; new insights into pathophysiology; novel understanding of diagnostic or therapeutic approaches; emerging technologies capable of improving existing diagnostic or treatment methods; changes within healthcare systems that necessitate modifications to diagnostic or therapeutic strategies; or a combination of the above.

Medical Device Commercialization Path – Scaling Mountains and Overcoming Obstacles

Medical Device Translation – Linear Inductive Translation Process (Theory)

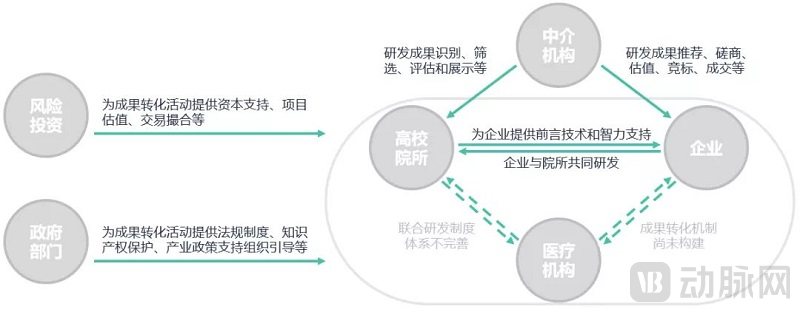

It is important to note that the actual translation process is not linear; conducting health technology assessments in advance, centering everything on clinical needs, and requiring close collaboration among industry, academia, research institutions, and healthcare providers.

Collaborative Models for the Translation of Medical Devices – Industry-Academia-Research-Medicine Collaboration

Establishing a Company

Medical Device Commercialization – Corporate Fundraising Channels

The funds raised will be primarily used for daily operational expenses and major R&D expenditures.

Establishing a company involves the following processes:

▶Internal due diligence, including assessment of freedom to operate (non-infringement of third-party patents) and patent eligibility (patentability).

▶Building a Business Case: Market Reports, Market Penetration, Available Seed Funding, and Identification of Strengths, Weaknesses, Opportunities, and Threats;

▶Technical Status: Is there a prototype or proof of concept? Is further research required? Are additional IP rights needed?

▶Draft an equity allocation plan mutually agreed upon by the prospective CEO and the academic founder, and establish a holding company;

▶The CEO began to steer the technological development process, engage in business management, prepare the business plan, and conduct the first round of roadshows for investors.

Oxford Nanopore Technologies has created a gene sequencing tool,By unzipping the double-helix structure, penetrating DNA, and utilizing unique electrical current signals to determine base-pair sequences, this approach differs from existing solutions.This technology is rapid and cost-effective, providing real-time sequencing results, and has already been applied in precision medicine.

UK universities have long prioritized basic research over applied research, resulting in limited industry-academia-research collaboration and a disconnect between research outcomes and industrial practice. Consequently, the rate of commercialization of university technological achievements remains low, making it difficult to translate scientific findings into industrial profits, with patent outputs significantly lagging behind those of the United States and Japan.

Against this backdrop, IP Group was founded in the United Kingdom in 2000, focusing on the commercialization of intellectual property (IP) from higher education institutions. It provides seed funding and professional IP commercialization services to university-affiliated companies, ultimately generating returns through equity stakes.

The company has established collaborations with 32 top universities and research institutions in the UK, US, and Australia, invested in over 300 enterprises globally, and holds net assets exceeding £1.49 billion (approximately RMB 12.97 billion). IP Group plc holds a 10.3% stake in Oxford Nanopore Technologies.

IP Group’s core business is to create value for its shareholders and partners by commercializing intellectual property (IP) from research-intensive institutions. Typically entering at the seed stage, it provides companies built on advanced technology IP with support in areas such as capital, strategic consulting, and corporate management.

▶ Selection Phase, leveraging deep technical and industry expertise to identify promising research and technologies among university, research institution, and corporate partners, and building businesses around them.

▶ Incubation Phase, universities and other founders establish startups, which are invested in by IP Group to help the founding teams conduct early-stage commercial and technical validation.

▶ Seed Stage, helping companies identify and engage with potential customers, and leveraging their feedback to guide the subsequent development of startups.

▶ Scale Expansion and Active Management, proactively expand investment sources through other channels, allocate more resources to business models, licensing information, industry collaborations or mergers and acquisitions, and IPO development strategies, and exit at the appropriate time.

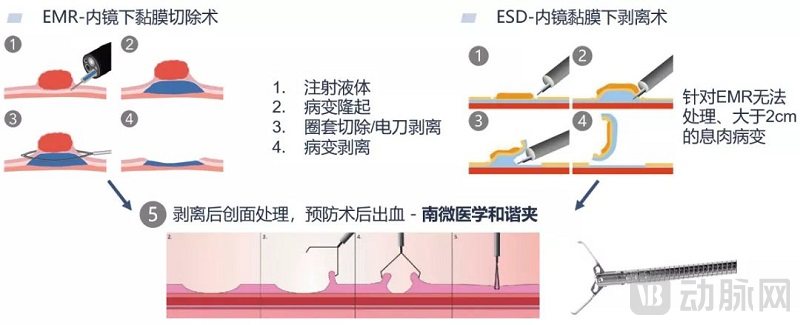

Micro-Tech Medical has developed a disposable soft tissue clip designed for endoscopy-guided wound management in clinical settings,Application innovation driven by clinical needs achieves international technical standards while offering significant price advantages, enabling wound management at the resection site after endoscopic mucosal resection (EMR) or endoscopic submucosal dissection (ESD) to prevent postoperative bleeding.

Nanwei Medical Harmony Clip – Minimally Invasive EMR/ESD Treatment for Early Gastrointestinal Cancer and Precancerous Lesions.

While Nanwei Medical’s Harmony Clip technology has reached international standards,Superior performance with a distinct price advantage.

Since the product's market launch, salesSales volume grew rapidly, achieving fast growth in both the United States and Europe.

Micro-Tech Medical Harmony Clip - Analysis of Success Factors

Medical devices undergo continuous improvement and refinement. Upon its initial market launch, Nanwei Medical’s hemostatic closure products had numerous issues; however, the product iteration speed was rapid., through the strong relationships established between the R&D team and clinicians, continuously communicateObtain Clinical Feedback, to understand the true clinical needs and extreme use scenariosand use this to improve the productOver the course of one year, product issues were largely resolved, resulting in the creation of the star hemostatic closure product, “Harmony Clip,” which was enthusiastically embraced by clinicians upon its launch.

Its technical advantages include:

▶The all-in-one design for single use reduces the workload of cleaning and disinfection for medical staff;

▶Capable of precise 360-degree rotation;

▶"Reusable with multiple open-close cycles, featuring a wide aperture and strong gripping force."

While ensuring that its technical performance meets international standards, the Harmony Clip has reduced its price from RMB 600–700 to RMB 199–299.Previously, the high cost of hemostatic closure devices limited their use in surgeries. Following price reductions, usage surged rapidly as clinicians could afford to apply multiple clips from safety and prophylactic hemostasis perspectives. This also opened up the EMR market, whose volume is a geometric multiple of that for ESD.