Who Will Disrupt the Endoscopy Industry? Innovations in 4K, 3D, Disposable, and Special Light Imaging Technologies

Since their introduction in the 19th century, medical endoscopes have undergone continuous development and are now widely used in general surgery, urology, gastroenterology, pulmonology, orthopedics, otolaryngology, gynecology, and other specialties, becoming one of the most commonly employed medical devices in modern medicine.

In recent years, technologies such as 4K, 3D, single-use systems, special light imaging (e.g., fluorescence), ultra-thin medical endoscopes, big data, and artificial intelligence have rapidly advanced and been progressively applied in the field of endoscopy. Meanwhile, China’s endoscopy industry is characterized by numerous pain points, abundant opportunities, and a fragmented competitive landscape. The overall industrial structure of endoscopy is being disrupted and reshaped by multiple factors, including technology, policy, and clinical practice.

To help industry professionals keenly capture innovation trends and gain insights into the direction of transformation, VCBeat Research Institute will launch the "2021 Endoscopy Innovation Trends Report," starting from detailed perspectives and targeting different needs and innovation directions. This report focuses on exploring the driving forces behind innovations in the field of endoscopy, analyzing the innovative opportunities brought by emerging technologies such as 4K, 3D, artificial intelligence, and big data applied to endoscopy.

Key Points:

Breakthroughs in CMOS, 4K, 3D, and computer technologies have been achieved and are gradually being applied in the field of endoscopy.

Olympus and other giants monopolize the domestic endoscope market, while Chinese companies are poised to overtake them by breaking through technological blockades.

The disposable endoscope sector is one of the few endoscopy subfields in China that holds a globally leading position.

4K Ultra-HD Endoscopes and 3D Endoscopes Are Moving Toward Integration, with “4K+3D” Set to Become the Mainstream in the Future.

Endoscopic AI-Assisted Diagnostic Systems Focus on the Gastrointestinal Tract, with a Vast Future Market in Primary Care Settings.

Financing in China's endoscopy sector is heating up, with single-use endoscopes and 4K ultra-high-definition endoscopes drawing significant attention.

Medical endoscopes are commonly used medical devices in modern medicine. In terms of categories, there is a wide variety of endoscopes, including gastroscope, colonoscope, laryngoscope, esophagoscope, laparoscope, thoracoscope, cholangioscope, cystoscope, ureteroscope, nephroscope, hysteroscope, intravascular endoscope, and arthroscope. From a functional perspective, endoscopes have diverse application scenarios; they can be introduced into the human body through natural orifices such as the mouth or through surgically created ports to assist physicians in disease screening and diagnosis. At present, they also support physicians in performing minimally invasive surgeries.

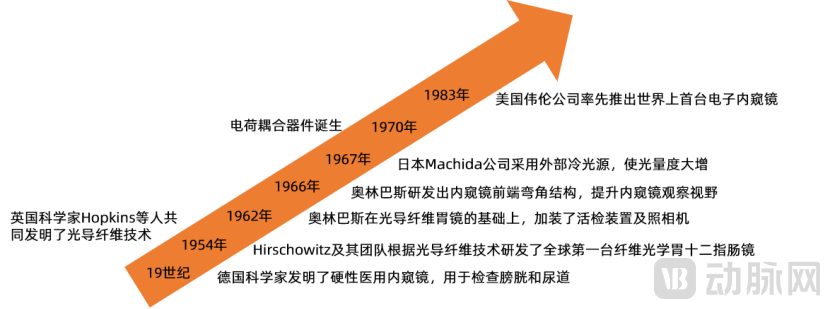

In the 19th century, German scientists invented rigid medical endoscopes for examining the bladder and urethra. Early rigid medical endoscopes consisted of a metal tube housing, optical components, and a light source. The optical components included prisms, lenses, and mirrors; light sources comprised candlelight, tungsten-filament external reflection lights, or small internal incandescent bulbs.

Rigid medical endoscopes, due to their rigid materials, structural limitations, and technical constraints, are not only difficult to insert into body cavities but also cause significant patient discomfort. Furthermore, their low illumination intensity results in unclear images, numerous blind spots, and suboptimal diagnostic performance.

In 1954, British scientists including Hopkins co-invented optical fiber technology. Hirschowitz and his team subsequently developed the world’s first fiberoptic gastroduodenoscope based on this technology, which is widely recognized as the first flexible medical device globally. This device utilized optical fibers as light-guiding and image-transmitting components, employed an external high-intensity cold light source for illumination, and enabled imaging. Since optical fibers are flexible elements (flexibility refers to the property of an object that deforms under force and does not return to its original shape after the force is removed), Hirschowitz’s team incorporated a bending mechanism at the distal tip, allowing controlled deflection of the flexible endoscope to facilitate insertion into the human body and reduce patient discomfort. In 1960, the American company ACMI commercialized this technology.

Japanese companies entered the endoscopy field relatively late but demonstrated rapid innovation. In 1962, Olympus of Japan enhanced fiber-optic gastroscopes by integrating biopsy devices and cameras, significantly improving their diagnostic capabilities. In 1966, Olympus pioneered the development of an angulated tip structure for endoscopes, further expanding the field of view. In 1967, Machida Endoscope Co., Ltd. adopted external cold light sources, substantially increasing light intensity. Driven by technological breakthroughs and continuous innovation, Japanese companies have secured a pivotal position in the global endoscopy market. Currently, Olympus holds a 34% share of the global endoscopy market.

In 1970, the charge-coupled device (CCD) was invented. Due to its dual capabilities of photoelectric conversion and scanning, CCDs rapidly gained prominence in the field of medical endoscopy. In 1983, Welch Allyn, a US company, pioneered the world’s first electronic endoscope. Subsequently, enterprises in Western Europe and Japan quickly followed suit, increasing their R&D investment in electronic endoscopes and sparking a surge in the development and application of electronic endoscopy that continues to this day. Compared with fiber-optic endoscopes, electronic endoscopes offer numerous advantages, including clearer images, more realistic colors, higher resolution, and the ability for multiple observers to view simultaneously. As a result, they have become the mainstream in the market.

Figure 1. History of Endoscopy and Underlying Technology Development

Source: Public data statistics, compiled by VCBeat.

Throughout the history of medical endoscopes, from rigid endoscopes to fiberoptic endoscopes and then to electronic endoscopes, the appearance and structure of endoscopes have undergone tremendous changes, and their image quality has steadily improved with product iterations.

Meanwhile, it is evident that each leapfrog development in endoscopic products has stemmed from fundamental technological innovations. For instance, leveraging optical fiber technology, endoscopy companies pioneered flexible and fiberoptic endoscopes; based on charge-coupled device (CCD) technology, they developed electronic endoscopes, which have gradually replaced fiberoptic models. On the other hand, innovations in structure, materials, and surgical techniques have expanded the application scenarios of endoscopes, saved more patients, and spurred the growth of a larger endoscopy market.

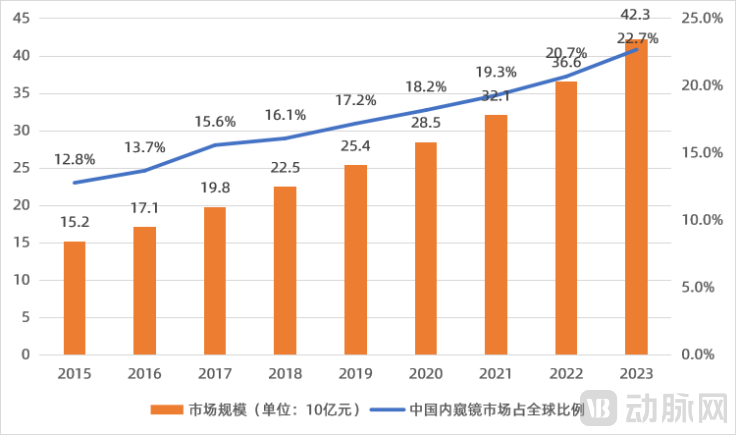

Driven by multiple factors including policies, enterprises, technology, and patient demands, China’s endoscopy industry is accelerating its development. In 2019, the market size of endoscopy in China was RMB 22.5 billion, and it is projected to grow to RMB 42.3 billion by 2024.

Figure 2. China's Endoscopy Market Size and Forecast, 2015–2024E

Source: Frost & Sullivan; prepared by VCBeat

According to "China's Endoscope Market Size and Forecast 2015-2024," China's share of the global endoscope market has been steadily increasing. In 2015, China's endoscopic device market accounted for 12.7% of the global market; this figure rose to 16.1% in 2019 and is projected to reach 22.7% by 2024.

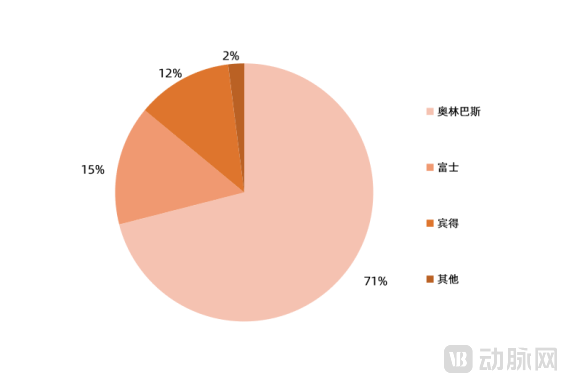

On the other hand, as a major country with a population of 1.4 billion, China is one of the fastest-growing markets for endoscopes, with a growth rate significantly higher than the global average. From 2015 to 2019, the compound annual growth rate (CAGR) of the global endoscope market was only 5.4%, while the CAGR of the Chinese endoscope market during the same period reached as high as 14.5%. The vast market potential and rapid growth have brought development opportunities for domestically produced endoscope enterprises. However, at present, the domestic endoscope market is still dominated by multinational giants. In the competitive landscape of flexible endoscopes in China, three Japanese companies hold a dominant position, with all other brands accounting for less than 2% of the market. Among them, Olympus holds a 71% share, Fujifilm holds 15%, and Pentax holds 12%.

Figure 3 Competitive Landscape of China's Flexible Endoscope Market in 2018

Source: Frost & Sullivan, prepared by VCBeat.

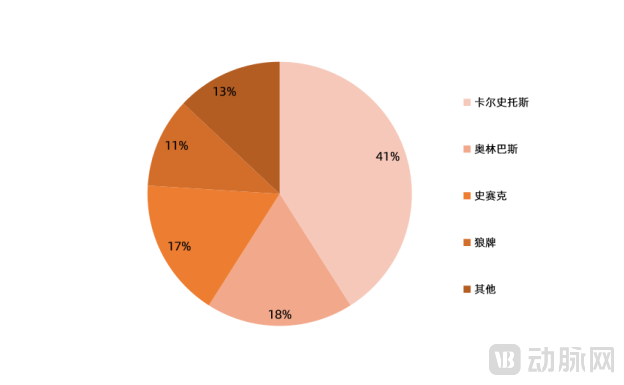

In the rigid endoscopy sector, companies from Germany, Japan, and the United States dominate, accounting for over 80% of the market. Among them, Karl Storz, Olympus, Stryker, and Richard Wolf occupy the top four positions in China’s rigid endoscope market.

Figure 4 Competitive Landscape of China's Rigid Endoscope Market in 2019

Source: Frost & Sullivan, prepared by VCBeat.

Both rigid and flexible endoscopes present exceptionally high technical barriers. For domestic enterprises, key pain points include talent, technology, patents, manufacturing processes, and brand recognition. Overseas giants do not establish R&D centers in China, resulting in a shortage of relevant local talent. Furthermore, their early strategic deployment of patent barriers has significantly increased the difficulty for Chinese companies to overcome these intellectual property hurdles.

Currently, domestic manufacturers have achieved breakthroughs in core components. The core components of an endoscope include the lens, image sensor, image processor, and light source. In terms of cold light sources, 116 products have been approved by the National Medical Products Administration (NMPA) in China; for image processors, 47 products have received approval.

As for image sensors, Chinese companies have also developed solutions. Endoscopic image sensors can be divided into charge-coupled devices (CCD) and complementary metal-oxide-semiconductor (CMOS) devices. Among them, CCD technology is monopolized by a few foreign companies, while CMOS technology is gaining momentum globally. From a technical perspective, CMOS offers advantages such as small size, low power consumption, low cost, and high system integration, making it highly likely to become the mainstream technology for endoscopic sensors. Currently, many companies worldwide have applied CMOS technology to medical endoscopes and launched various innovative endoscopic products. Meanwhile, Chinese companies are making rapid progress in CMOS technology, with a narrow gap compared to overseas technologies, presenting significant opportunities to achieve technological breakthroughs through CMOS image sensors.

From the perspective of domestic endoscope manufacturers, the industry is relatively fragmented, with no leading enterprise emerging that can challenge foreign giants. Meanwhile, domestically produced endoscopes currently compete primarily in the mid-to-low-end market, while the high-end segment remains dominated by imported brands. In the field of flexible endoscopy, key Chinese players include Shenzhen Sonoscape and Shanghai Aohua; in rigid endoscopy, major companies include New Optical Dimension Medical, Shenyang Shenda, Tiansong Medical, Mindray Medical, and Haitai Optoelectronics.

From the perspective of the localization history of individual medical devices, there is significant room for domestic substitution in the endoscopy field. In particular, with the emergence of new technologies, the pace of endoscope localization in China is expected to accelerate substantially. For instance, in optical imaging technology, the rise of CMOS image sensors has broken the Japanese monopoly on CCD sensors; in staining techniques, beyond Olympus’ NBI technology, various brands have developed their own proprietary staining technologies, such as Pentax’s i-Scan and Sonoscape’s VIST; and in terms of scope manufacturing, the trend toward treating endoscopes as consumables is becoming increasingly pronounced, with notable breakthroughs achieved in single-use endoscopes.

Currently, leveraging multiple technological innovations, the market has seen the emergence of various innovative products, including disposable endoscopes, hybrid endoscopes (such as endoscopic ultrasound [EUS], optical coherence tomography [OCT] endoscopes, fluorescence endoscopes, and confocal laser endomicroscopes), endoscopic robots, AI-assisted endoscopic diagnostic systems, 4K ultra-high-definition endoscopes, 3D endoscopes, and capsule endoscopes.

In the traditional endoscopy sector, domestic companies have had to devote substantial efforts to catching up technologically. However, with the emergence of new technologies and the stagnation of conventional ones, Chinese firms and multinational giants now stand on the same starting line in innovative endoscopy—a rare opportunity for domestic endoscope manufacturers to overtake their competitors on a bend.。

From the perspective of endoscopy’s development history, its leapfrog iterations have stemmed from fundamental technological breakthroughs. Today, a range of cutting-edge technologies—including CMOS, 4K, 3D, artificial intelligence, big data, and deep learning—are becoming increasingly mature and are gradually being applied in the field of endoscopy, laying the technical foundation for innovation in this domain.

On the other hand, the continuous growth of the endoscopy market size provides ample space for endoscopy companies to seize market share, generate profits, and create wealth. The pursuit of profit and wealth creation drives these companies to continuously innovate their products, enabling them to gain a competitive advantage in the market.

Meanwhile, multiple factors—including shifts in consumer behavior, escalating clinical demands, capital investment, policy support, and corporate competition—are jointly driving endoscopy companies to pursue continuous innovation.

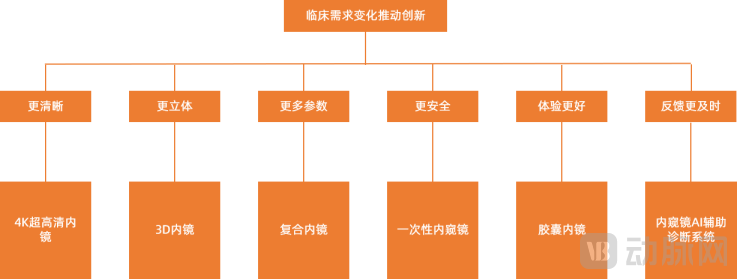

Compared to two decades ago, clinical needs have undergone significant changes. For physicians, there is a demand for imaging with greater clarity, three-dimensionality, and more parameters; for patients, there is a need for safe, painless endoscopic diagnosis and treatment with real-time feedback.

Figure 5. Evolving Clinical Needs Drive Endoscopic Innovation

Data source: Frost & Sullivan, prepared by VCBeat.

To meet the demand for greater clarity, companies both in China and abroad have been developing or have already developed 4K ultra-high-definition endoscopes. For instance, New Optical Dimension Medical has launched a 4K medical endoscopic camera system; Tuge Medical’s AIENDO-4K ultra-high-definition endoscopy system is the first domestically produced 4K endoscope to be procured by hospitals in China. Furthermore, fluorescence endoscopes (operating spectrum: 400–900 nm) feature a broader working spectrum compared to traditional white-light endoscopes (operating spectrum: 400–700 nm), enabling them to display images of superficial human tissues as well as fluorescence imaging of sub-surface structures, such as the cystic duct, lymphatic vessels, and blood vessels. In contrast, white-light endoscopes primarily visualize superficial tissue structures. Consequently, fluorescence endoscopes are being increasingly widely adopted in clinical practice. Currently, OptoMedix has broken the long-standing dominance of foreign companies by launching the world’s first 4K fluorescence laparoscopy system. Other domestic enterprises have also introduced related products; for example, Meirunda showcased its 4K ultra-high-definition fluorescence endoscopy system at the China International Medical Equipment Fair (CMEF).

To address the demand for more immersive visualization, 3D endoscopes can provide physicians with three-dimensional stereoscopic images. Currently, SinoMicro Medical has launched a 3D electronic thoraco-laparoscopic system, and Surui Medical’s 3D electronic laparoscope has received approval from the National Medical Products Administration (NMPA). However, 3D endoscopes still face challenges in image clarity, making the integration of 3D with 4K resolution the next key hurdle for companies in this sector to overcome.

To meet the demand for more parameters, Sonoscape has launched China’s first endoscopic ultrasound system, which provides both endoscopic and ultrasound images. Micro-Tech has developed an Endoscopic Optical Coherence Tomography (EOCT) system, the first product in China to apply optical coherence tomography technology to the early diagnosis of digestive tract cancers, and also the second commercially available EOCT system worldwide. Jingwei Shida pioneered the confocal laser endomicroscope for the pancreatic and bile ducts, providing clinicians with real-time, in vivo pathology-level image information and enabling doctors to view cellular-level microscopic images of strictures in real time during surgical procedures.

To meet the demand for greater safety, multiple companies have developed single-use endoscopes, addressing the issue of cross-infection during endoscopic examination and treatment and thereby enhancing safety. For instance, Ruipai Medical’s single-use electronic cystoscope and single-use electronic ureterorenoscope catheter were approved in 2020, with its product line planned to cover urology, gynecology, otolaryngology, pulmonology, general surgery, and other specialties. Meanwhile, companies such as Xin Guangwei Medical, Pusheng Medical, Anqing Medical, Happy Factory, and Beifang Tengda have also received approval for marketing their single-use endoscope products. For manufacturers of single-use endoscopes, the key innovation challenge remains ensuring imaging quality and functionality comparable to those of conventional reusable endoscopes while maintaining low costs.

In response to the demand for painless endoscopy, the advent of capsule endoscopy has brought hope to patients. Currently, companies such as Ankon Medical, Jinshan Science & Technology, and Zifu Medical have launched multiple capsule endoscopy systems for gastrointestinal disease examination and early cancer screening. Shaped like a capsule, the device begins imaging once swallowed by the patient. With a one-patient-one-capsule approach, it eliminates the risk of cross-infection. For capsule endoscopy manufacturers, key areas of innovation include expanding indications, ensuring diagnostic accuracy, and providing AI-assisted image interpretation.

To meet the demand for timely feedback, AI-assisted diagnostic systems can help physicians make diagnoses more efficiently, rapidly, and accurately. Given the uneven distribution of medical resources in China and the scarcity of endoscopy image interpretation specialists, AI-assisted diagnostic systems can enable less experienced physicians to achieve “expert-level” performance, while reducing image reading time and accelerating the issuance of diagnostic reports.

In addition, the trend toward domestic substitution and supportive national policies have, to a certain extent, driven innovation in the endoscopy industry. Financial backing from numerous investment institutions has further bolstered corporate innovation. It is believed that, under the combined forces of technology, market dynamics, policy support, and capital, the endoscopy industry will usher in a new wave of innovation.

Disposable endoscopes address the common risk of cross-infection associated with traditional endoscopes.

As precision instruments inserted deep into human body cavities, endoscopes are highly prone to causing cross-infection. For instance, in the annual "Top 10 Health Technology Hazards" report published by the ECRI Institute in the United States, cross-infections associated with endoscopes have consistently been listed. In 2016, the number one hazard was: inadequate cleaning of flexible endoscopes prior to disinfection, which can transmit fatal pathogens; in 2017, the number two hazard was: inadequate cleaning of complex reusable medical devices, leading to patient infections; in 2018, the number two hazard was: inadequate cleaning and disinfection of endoscopes, exposing patients to infection risks; and in 2019, the number five hazard was: improper handling of soft endoscopes after disinfection, resulting in patient infections. Among these, flexible endoscopes with multiple narrow and long channels, such as cystoscopes, ureteroscopes, colonoscopes, and gastroscopes, are more difficult to clean and disinfect, thereby posing a higher risk of cross-infection.

To address the issue of cross-infection, single-use endoscopes were developed. In 2009, Ambu launched the world’s first single-use bronchoscope and gradually expanded its portfolio to include single-use laryngoscopes, cystoscopes, gastroduodenoscopes, colonoscopes, and duodenoscopes.

As of now, at least 12 companies in China have entered the single-use endoscope market. Among them, Ruipai Medical, Huaxin Medical, New Guangwei Medical, Pusheng Medical, Anqing Medical, Lancesert, and Youkang Technology have already initiated globalization strategies.

Table 1 List of Domestic Single-Use Endoscope Manufacturers

Source: Public information; prepared by VCBeat.

Chinese and overseas enterprises have nearly simultaneously embarked on innovation in single-use endoscopes, with Chinese manufacturers demonstrating considerable competitiveness in technological innovation, product development, and pace of commercialization. For instance, the majority of single-use endoscope products currently marketed by companies such as Ambu, Boston Scientific, Pentax, and Olympus were approved between 2019 and 2021. Similarly, single-use endoscope products from domestic companies—including Ruipai Medical, Pusun Medical, Anqing Medical, Xingfu Factory, Beifang Tengda, and New Guangwei Medical—received approval from China’s National Medical Products Administration (NMPA) during the same period. Furthermore, products from Ruipai Medical, Huaxin Medical, New Guangwei Medical, Pusun Medical, Anqing Medical, Lainsert, and Youkang Technology have obtained CE certification, while those from Huaxin Medical, New Guangwei Medical, and Pusun Medical have secured FDA clearance.

According to statistics from the China Association for Medical Devices Industry, the annual growth rate of China’s endoscopy market is expected to remain at approximately 20%. Benefiting from supportive industry policies, increasing downstream market demand, and accelerated adoption rates, the market size of medical endoscopes in China has been expanding year by year. Furthermore, as patients’ living standards and economic capacity improve, there is a growing demand for safe and effective single-use endoscopes.

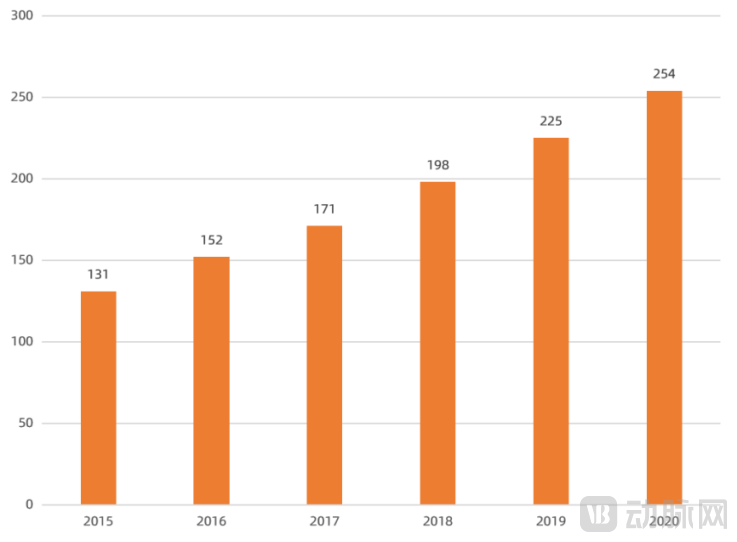

According to Frost & Sullivan data, the market size of endoscopes in China reached RMB 25.4 billion in 2020, with a compound annual growth rate (CAGR) of approximately 11.67% from 2015 to 2020. During the same period, the global endoscope market size grew from USD 16.4 billion to USD 21.5 billion, at a CAGR of approximately 5.5%.

Figure 6 Market Size of Endoscopes in China (CNY 100 million)

Data Source: Frost & Sullivan, VCBeat.

Disposable endoscopes, as high-value consumables that reduce the risk of cross-infection, will occupy an increasingly important position in the endoscopy market. In terms of product supply, manufacturers will develop and produce disposable endoscopes to replace or partially replace traditional endoscopes based on various factors such as the production, maintenance, facility usage, and sterilization costs of conventional endoscopes, as well as their utilization and turnover rates; alternatively, they will develop disposable endoscopes with certain performance advantages over traditional models.

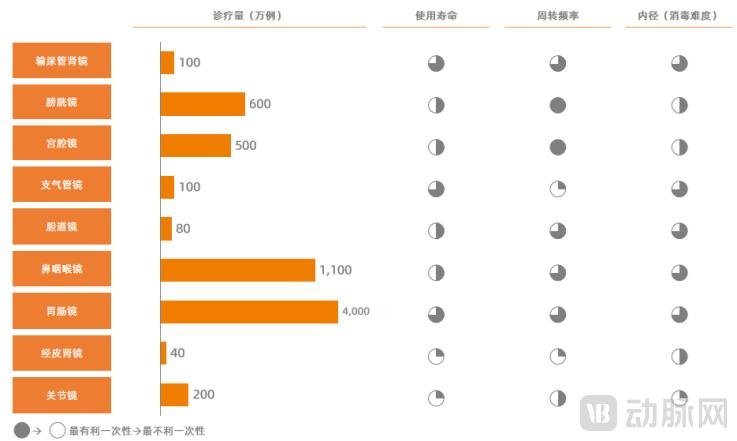

DotStone Capital believes that endoscopes characterized by high procurement, maintenance, and disinfection costs, short single-use durations, and rapid turnover rates all have the potential to become “single-use” devices. Such endoscopes, which have the potential to be transformed into disposable consumables, correspond to a potential diagnostic and treatment volume of nearly 70 million cases in China. Based on this substantial volume, the market size for single-use endoscopes exceeds RMB 10 billion.

Figure 7 Analysis of the Potential for Traditional Endoscopes to Become Disposable Consumables

Data Source: Dianshi Capital

At present, products developed or approved by domestic companies are primarily single-use cystoscopes and single-use ureteroscopes, with limited progress in single-use laryngoscopes, single-use gastroscopes, single-use colonoscopes, and single-use duodenoscopes. This is because relevant enterprises have taken into account factors such as clinical necessity, market adoption, market prospects, and cost-effectiveness.

Traditional cystoscopes and ureteroscopes entail relatively high potential costs, have short single-use durations, and require rapid turnover, making them the most suitable for a “disposable” model. The cost of using endoscopes includes not only the product itself but also expenses such as maintenance, facility usage, and sterilization. Considering factors such as service life, maintenance costs, sterilization costs, and facility usage costs, cystoscopes and ureteroscopes are the most amenable to substitution.

Traditional cystoscopy and ureteroscopy carry relatively high fee schedules, which facilitates market acceptance of the pricing for single-use endoscopes. Currently, gastroscopy costs RMB 200–300, bronchoscopy ranges from RMB 300 to 800, laryngoscopy is priced at RMB 100–300, cystoscopy costs approximately RMB 1,000, and ureteroscopy costs around RMB 2,000. Furthermore, the use of endoscopes during surgical procedures incurs even higher costs. Given the existing pricing structure for cystoscopy and ureteroscopy, the market is more receptive to the pricing of single-use cystoscopes and single-use ureteroscopes, thereby facilitating product promotion by manufacturers and enabling greater financial benefits for patients, relevant enterprises, and hospitals.

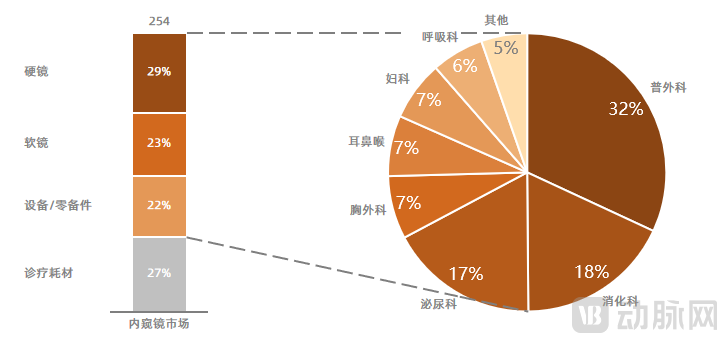

Cystoscopy and ureteroscopy account for 17% of the endoscopy market within urology, representing a substantial market size. For instance, there are 6 million cystoscopic procedures performed annually, and as the population ages and the number of patients increases, the utilization of cystoscopes is expected to rise further.

Figure 8 Endoscopy Market Distribution

Source: Dianshi Capital

Compared with traditional cystoscopes and ureteroscopes, single-use endoscopes offer greater cost-effectiveness and safety. For instance, in traditional flexible ureteroscopy, the cost per procedure exceeds RMB 12,000 due to factors such as the limited lifespan of the flexible scope and frequent maintenance requirements; in contrast, the use of a single-use ureteroscope costs no more than RMB 10,000. Furthermore, traditional ureteroscopes require cleaning and disinfection, and their performance gradually deteriorates with repeated reprocessing, which can compromise surgical safety. Single-use ureteroscopes follow a “one patient, one scope” principle, ensuring optimal quality for each procedure and eliminating the risk of cross-infection, thereby enhancing surgical safety.

VCBeat’s research indicates that although domestically developed or approved products are primarily single-use cystoscopes and single-use ureteroscopes, relevant companies have begun to expand their portfolios to include a broader range of single-use endoscopes. For instance, Ruipai Medical has developed various single-use endoscopes covering multiple specialties, including urology, gynecology, otolaryngology, pulmonology, and general surgery. Ruipai Medical is currently the manufacturer holding the largest number of Class III registration certificates for single-use endoscopic products in China.

Compared with traditional endoscopes, single-use endoscopes adhere to the “one patient, one scope” principle, thereby eliminating the risk of cross-infection and offering greater health economic value.

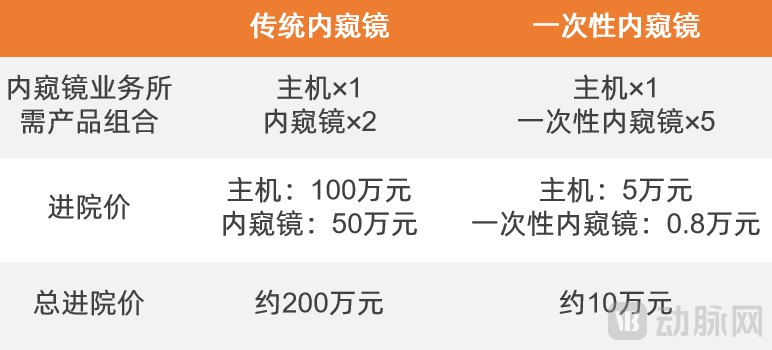

At the hospital level, launching endoscopy examination and treatment services previously required at least two flexible endoscopes and one processor unit, with a total cost of approximately RMB 2 million. Today, however, only several single-use endoscopes and one processor unit are needed, reducing the total cost to merely around RMB 100,000. By comparison, single-use endoscopes are more conducive to enabling primary-care hospitals to establish endoscopy services.

Table 2 Hospital Procurement Prices of Traditional Endoscopes vs. Single-Use Endoscopes

Source: Public information; compiled by VCBeat.

Furthermore, traditional endoscopes require consideration of post-procedural matters such as maintenance, cleaning, and sterilization, whereas single-use endoscopes are “ready-to-use out of the box,” eliminating costs associated with maintenance, cleaning, and sterilization, thereby significantly reducing the financial burden on hospitals. Data indicates that the cost per procedure for a traditional reusable flexible ureteroscope in China exceeds RMB 12,000, with daily disinfection, sterilization, and operational maintenance accounting for 43% of the total cost. In contrast, single-use endoscopes eliminate concerns regarding service life and repairability, leading to a substantial reduction in costs. When considering both equipment and consumables, the initial procedural cost of using a single-use flexible ureteroscope is only 5% of that for a reusable flexible ureteroscope.

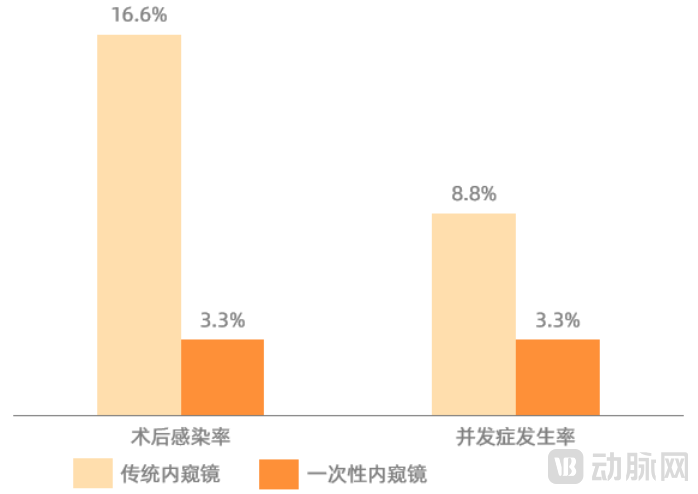

From the patient’s perspective, traditional endoscopes are prone to causing cross-infection, whereas disposable endoscopes eliminate this risk. When calculating the total cost of care throughout the patient’s entire clinical journey, expenses associated with traditional endoscopic surgery—including complication management and hospitalization—far exceed those of using disposable endoscope products. Furthermore, the performance of traditional endoscopes deteriorates with repeated reprocessing and maintenance, which can compromise surgical safety. In contrast, disposable endoscopes adhere to a “single-use per patient” model, ensuring optimal quality for every procedure and thereby enhancing surgical safety. The latest clinical research published in January 2021 demonstrated that, compared with traditional ureteroscopes, disposable ureteroscopes were associated with shorter hospital stays and reduced duration of antibiotic therapy, as well as lower overall complication rates and postoperative infection rates. These findings indicate that the use of disposable endoscopes can significantly reduce postoperative complications and infection rates, thereby safeguarding patient safety.

Figure 9. Disposable endoscopes reduce the postoperative infection rate of flexible ureteroscopy

Data Source: Dianshi Capital

The rise of single-use endoscopes presents a rare opportunity for Chinese manufacturers to overtake their competitors in the endoscopy field, and also serves as a catalyst for the development of domestic single-use endoscope enterprises.

Previously, China’s endoscopy market was largely monopolized by companies such as Olympus, Fujifilm, Karl Storz, Stryker, and Richard Wolf. However, with the continued expansion of the single-use endoscope market, the existing landscape of the endoscopy industry is set to be disrupted. Meanwhile, significant differences between single-use and traditional endoscopes in terms of design philosophy, scaled mass production, and cost control mean that established players like Olympus do not hold a clear leading advantage in exploring the single-use endoscope market.

In contrast to the overseas monopoly held by giants in the traditional endoscopy market, Chinese companies demonstrate strong competitiveness in the nascent field of single-use endoscopes. For instance, leading overseas players in the single-use endoscope sector, such as Ambu and Boston Scientific, obtained regulatory approvals for most of their products between 2019 and 2021. During the same period, Chinese enterprises also achieved breakthrough progress. For example, Ruipai Medical obtained Class III medical device registration certificates for its “Single-Use Electronic Cystoscope” and “Single-Use Electronic Ureterorenoscope Catheter” in July and August 2020, respectively. Additionally, Xin Guangwei Medical received CE certification for its “Single-Use Electronic Hysteroscope” in 2021.

As for traditional endoscopy giants such as Olympus, they also began to enter the field of single-use endoscopes around 2019. However, as of now, Olympus has only launched a single-use bronchoscope, which was developed and manufactured by the Chinese company Huaxin Medical, with Olympus serving as the exclusive U.S. distributor to introduce the product to the American market.

Thus, it is evident that in the field of single-use endoscopes, domestic companies such as Ruipai Medical and Huaxin Medical are on par with global leaders like Ambu and Boston Scientific. Meanwhile, it is foreseeable that Chinese single-use endoscope manufacturers will experience rapid growth as the market matures, and the landscape of China’s endoscopy market will be reshaped by the rise of these domestic players.

Currently, the disposable endoscope industry is still in its early stages of development, with numerous pain points that require continuous innovation to address. Through interviews with disposable endoscope manufacturers, we have found that innovation in this field will center on the requirements of various surgical procedures, usage scenarios, and market demands.

First, companies will innovate and develop dedicated single-use endoscopes tailored to specific procedural requirements. For instance, Lancesight has developed a single-use electronic ERCP endoscope for Endoscopic Retrograde Cholangiopancreatography (ERCP). Such products highly integrate various consumables required during surgery onto the endoscope body, eliminating the need for physicians to repeatedly manipulate instruments through the instrument channel, thereby reducing procedural complexity and enhancing surgical safety.

Second, companies will innovate and develop products based on the application scenarios of single-use endoscopes. Due to their lightweight and portable design, single-use endoscopes can be deployed in diverse settings such as bedside care, emergency departments, and primary healthcare facilities. Unlike traditional endoscopes, single-use endoscopes will undergo iterative upgrades tailored to these innovative application scenarios.

Third, driven by market demand, companies will continuously innovate to enhance the performance of single-use endoscopes, such as image clarity, while reducing production costs.

4K Ultra-High-Definition Endoscopy: A 4K ultra-high-definition endoscope is an endoscopic system with a resolution reaching the 4K level, in which all components—including the light source, optical lenses, sensor, transmission system, image processing unit, and display—are 4K-grade.

In 2015, SOMED, a joint venture between Sony and Olympus, launched the world’s first 4K ultra-high-resolution surgical endoscopy system. Featuring 4K-level resolution, this product provides surgeons with clear visualization of minute blood vessels, nerves, and fascial layers during procedures, thereby facilitating precise surgical interventions. In the development of this 4K ultra-high-definition endoscope, Sony primarily contributed image processing, color reproduction, and transmission technologies, while Olympus provided endoscopic expertise. The collaboration between Sony and Olympus accelerated the market entry of the 4K ultra-high-definition endoscope. Despite the substantial data load associated with 4K resolution, the system achieves lag-free display of high-precision images.

The differences between 4K ultra-high-definition endoscopy and conventional high-definition endoscopy are limited to soft characteristics such as image resolution and color fidelity. Therefore, the indications for 4K ultra-high-definition endoscopy are consistent with those for conventional high-definition endoscopy; however, in specific scenarios where conventional high-definition endoscopy fails to meet current clinical demands, 4K ultra-high-definition endoscopy plays an irreplaceable role.

The resolution of images generated by 4K ultra-high-definition endoscopes is four times that of traditional high-definition endoscopic images. Based on the higher resolution, 4K ultra-high-definition endoscopes can visualize subtle blood vessels, nerves, and fascial layers, as well as details of lesion areas and biopsy sites that are difficult to examine with traditional high-definition endoscopes.

4K Ultra-High-Definition Endoscopy Accurately Reproduces Image Colors. Compared with traditional high-definition endoscopes, 4K ultra-high-definition endoscopes feature a wider color gamut, enabling faithful reproduction of images captured by the endoscopic system. Relative to conventional endoscopes, 4K ultra-high-definition endoscopes provide enhanced depth perception and intraoperative operational awareness, owing to their superior resolution, visual acuity, and color resolution. For instance, in laparoscopic surgery, where the visual field exhibits rich color gradations, 4K laparoscopy facilitates the differentiation of subtle distinctions between pancreatic tissue and adipose tissue based on true-to-life color representation.

4K Ultra-High-Definition Endoscopy Offers Superior Recognition of Anatomical Planes and Vasculature. Leveraging comprehensive advantages in image resolution, color differentiation, and visual detail, 4K ultra-high-definition endoscopy enables the identification of minute structures such as lymph nodes, fascia, blood vessels, and nerves. For instance, 4K laparoscopy allows for clearer identification and preoperative assessment of the anterior superior pancreaticoduodenal vein branches located posterior to the right gastroepiploic vein and on the pancreatic surface, thereby avoiding unnecessary injury to these venous branches during manipulation of the right gastroepiploic vein. Furthermore, during transhiatal dissection of lower mediastinal lymph nodes, it facilitates the recognition and identification of vital organs and fascial layers within this anatomical region.

4K Ultra-High-Definition Endoscopy Enhances Surgical Precision. Clinically, 4K ultra-high-definition endoscopy provides surgeons with clearer surgical fields and visual displays. The ultra-high-definition images enhance depth perception, and when combined with image magnification capabilities, offer improved localization and orientation for surgeons, thereby increasing surgical precision. For instance, compared to conventional high-definition laparoscopy, 4K laparoscopy offers superior recognition accuracy and a lower probability of intraoperative errors. It assists clinicians in identifying the relationships between critical anatomical structures and surrounding tissues, helping to avoid injury to nerves, blood vessels, lymphatics, and other vital areas.

4K Ultra-High-Definition Endoscopy Can Be Applied to a Wider Range of Clinical Scenarios. Leveraging the superior image quality and clarity of 4K ultra-high-definition endoscopy, it can be utilized for delicate procedures that are challenging to perform with conventional endoscopes, such as neurovascular surgery. Furthermore, due to its ability to clearly visualize or identify membranous anatomical planes, minute blood vessels, nerves, and the boundaries of lymph node dissection, 4K ultra-high-definition endoscopy offers greater practical value in surgeries involving the stomach, colorectum, pancreas, thyroid, bariatrics, and hernia repair.

According to Frost & Sullivan data, the global market size for 4K ultra-high-definition endoscopes reached USD 1 billion in 2020, accounting for 4.7% of the total global medical endoscope market that year. The global 4K ultra-high-definition endoscope market is projected to reach USD 9.4 billion by 2030, representing 23.8% of the total global medical endoscope market in 2030. In China, the market size for 4K ultra-high-definition endoscopes amounted to RMB 300 million in 2020 and is expected to grow to RMB 12.4 billion by 2030.

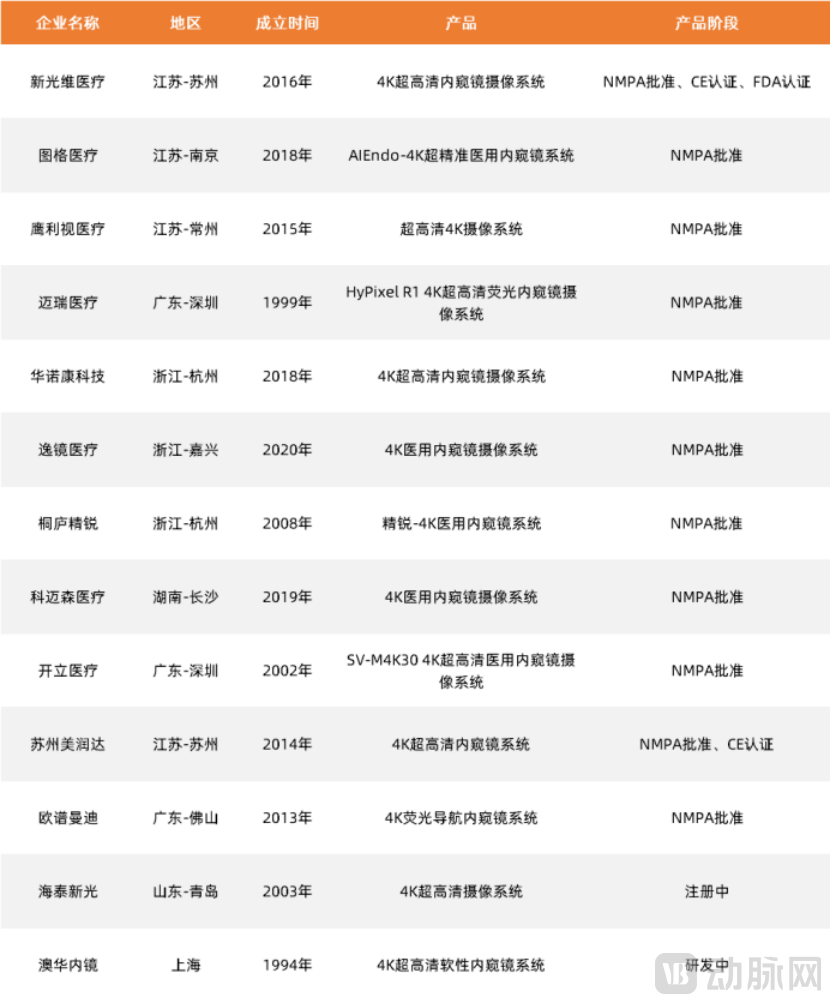

In China, a total of 20 medical device companies have received approval from the National Medical Products Administration (NMPA) for their 4K imaging (camera) systems, including Tuge Medical, Newopto Medical, Mindray, SonoScape, and Eagle Vision Medical.

Table 9 Representative Enterprises of Domestic 4K Ultra-High-Definition Endoscopes

Source: Public information; prepared by VCBeat.

Among them, companies such as Mindray Medical, Suzhou Meirunda, and OptoMedic have combined fluorescence endoscopy with 4K technology to launch 4K ultra-high-definition fluorescence endoscopes. New Vision Medical is also scheduled to introduce its 4K endoscopic fluorescence imaging system in early 2022.

Currently, the domestic 4K endoscopy market in China remains predominantly occupied by international medical device companies such as Olympus. However, supported by multiple factors, Chinese manufacturers have significant opportunities to catch up. In 2020, the penetration rate of domestic brands was only 5.6%, with an even lower penetration rate for 4K ultra-high-definition endoscopes, which are classified as high-end medical devices. Nevertheless, benefiting from continuously improving technical capabilities, increasing talent and capital resources, and industry-supportive policies advocating the substitution of imports with domestically produced alternatives, the penetration rate of domestic endoscopes is projected to reach 27.7% by 2030, accompanied by substantial growth in the adoption of 4K ultra-high-definition endoscopes.

In terms of technology, Chinese companies have broken through technological blockades and independently developed core components for 4K ultra-high-definition endoscopes. For instance, numerous enterprises such as Tuge Medical, New Optical Dimension Medical, and Sonoscape Medical have achieved breakthroughs in camera systems, with 20 models of 4K-grade endoscopic camera systems already approved in China. Additionally, companies like Hisense Medical have launched 4K ultra-high-definition endoscopic monitors.

Meanwhile, Chinese enterprises have resolved key hardware and software challenges associated with 4K ultra-high-definition endoscopy, including large data volumes, data transmission, and color reproduction. To date, companies such as Tuge Medical, Sinovation Medical, Mindray Medical, and Eagle Vision Medical have launched 4K ultra-high-definition endoscopes. It is expected that more domestically produced 4K ultra-high-definition endoscopes will enter clinical use in China over the next three years.

In terms of capital, numerous state-owned funds and prominent institutions, including CAS Star, CAS Venture Capital, SDIC Merchants, Fortune Capital, and Tsinghua Holdings Ginkgo, have actively invested in the 4K ultra-high-definition endoscopy sector, accelerating the development of enterprises in this field. For instance, Tuge Medical completed its angel and Series A financing rounds in 2018 and 2020, respectively, with investments from CAS Venture Capital, CAS Star, Nanjing Xinyuliu Equity Investment, Nanjing Innovation Investment Group, Shanghai United Investment, and Nanjing Qilin Industrial Investment. Opmedi completed four rounds of financing between 2016 and 2021; its Series B and C rounds each raised nearly RMB 100 million, while its Series D round secured several hundred million RMB. Investors included Fortune Capital, Tsinghua Holdings Ginkgo, Leaguer Venture Capital, Xiyu Investment, Hetang Venture Capital, Maorong Investment, Guangdong Guoke, Chunhua Capital, and SDIC Merchants.

In terms of policy, the Chinese government has introduced multiple measures to encourage domestic enterprises to independently develop high-end medical devices and to prioritize the procurement of domestically produced devices by healthcare institutions. In March 2021, the Health Commission of Guangdong Province released the "Public Notice on the 2021 List of Imported Products for Provincial Health Institutions." Compared with the 2019 list, the number of imported products eligible for procurement was reduced from 132 to 46. Notably, endoscopic products such as hysteroscopes, laparoscopes, and arthroscopes were removed from the imported product list, requiring healthcare institutions in Guangdong Province to prioritize the procurement of domestically produced endoscopes, thereby promoting the substitution of imports with domestic products. Meanwhile, several other provinces, including Sichuan and Zhejiang, have adopted similar policies to support the development of China’s medical device industry.

In terms of products, the quality of domestically produced 4K ultra-high-definition (UHD) endoscopes has reached an internationally leading level. For instance, Tuge Medical’s 4K UHD imaging system captures front-end video input and processes the raw footage through an FPGA module to perform noise reduction, dead pixel correction, color restoration, and edge enhancement, thereby improving video clarity. Meanwhile, it leverages high-speed DDR memory chipsets to enable local zooming and freeze-frame storage of specified images, with output available in multiple formats, demonstrating strong compatibility.

For another example, the 4K thoracoabdominal endoscopes, 4K nasal endoscopes, and 4K arthroscopes launched by Xin Guang Wei Medical can be used in conjunction with 3D technology, enabling physicians to obtain more comprehensive information. Compared with other 4K ultra-high-definition (UHD) endoscopes on the market, Xin Guang Wei Medical’s 4K UHD endoscopes feature six functions: smoke removal and defogging, vessel enhancement, wide dynamic range (WDR), low-light correction, exposure correction, and special imaging (compatible with fluorescence imaging). Among these, the wide dynamic range function refers to achieving uniform brightness and clear contours in images by suppressing overexposure and enhancing signals in shadowed areas.

Overall, although China's 4K ultra-high-definition endoscopy started late, it has attracted numerous participants and developed rapidly, breaking through technological blockades. Currently, several domestic companies have launched 4K ultra-high-definition endoscope products. It is expected that more such devices will be introduced to the market in the future, meeting clinical needs, replacing imported products, and increasing the localization rate.

It is foreseeable that, with technological advancements, continuous innovation, and product iterations by domestic enterprises, Chinese-made 4K ultra-high-definition endoscopes will capture the majority of the domestic market and expand internationally, ushering in an era of global competition.

The above is an excerpt from the report. The table of contents is listed below. Scan the mini-program QR code at the end of the article to read the full report for free:

I. The Development History of Endoscopes

II. Landscape and Opportunities in Endoscopy

III. Innovation Drivers in Endoscopy

(I) Technological Breakthroughs Lay the Foundation for Innovation

(II) Market Scale Growth Stimulates Innovation Momentum

(3) Changes in Clinical Needs Drive Corporate Innovation

IV. Six Major Innovation Directions for Endoscopes

(1) Disposable Endoscope

(2) Compound Endoscope

(3) Endoscopic Interventional Surgical Robots

(4) Endoscopic AI-Assisted Diagnostic System

(5) 4K Ultra-High-Definition Endoscopy System

(6) 3D Endoscope

V. Investment and Financing in the Endoscopy Industry

VI. Case Studies of Innovative Endoscopy Companies

(1) Ruipai Medical: Innovative Platform for Disposable Endoscopes

(2) Xin Guangwei Medical: A Provider of Comprehensive Endoscopy and Innovative Product Solutions

(3) Tuge Medical: R&D Platform for 4K Endoscopic Imaging Systems and Digital Intelligent Operating Rooms

(4) OptoMedix: A Platform Enterprise for Endoscopic Minimally Invasive Diagnosis and Treatment

(V) Hisi Yigou: A Service Provider for AI Technology and Equipment Applications in Digestive Endoscopy