Ryan Partners: Policy Insights and Competitive Strategies in China's Volume-Based Procurement

In recent years, Ryan Partners has closely monitored the progress of centralized procurement policies and changes in corporate bidding strategies. This report summarizes the evolution of these policies, development trends in national and local centralized procurement, the impacts of winning or losing bids on enterprises, and case studies of corporate responses. As biologics and medical consumables are progressively included in centralized procurement in phases, it is imperative for companies to respond swiftly. We will continue to update our insights from various perspectives.

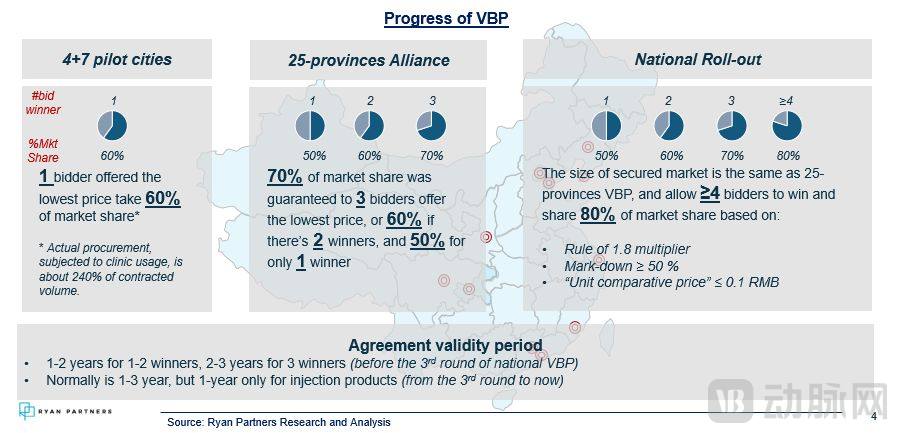

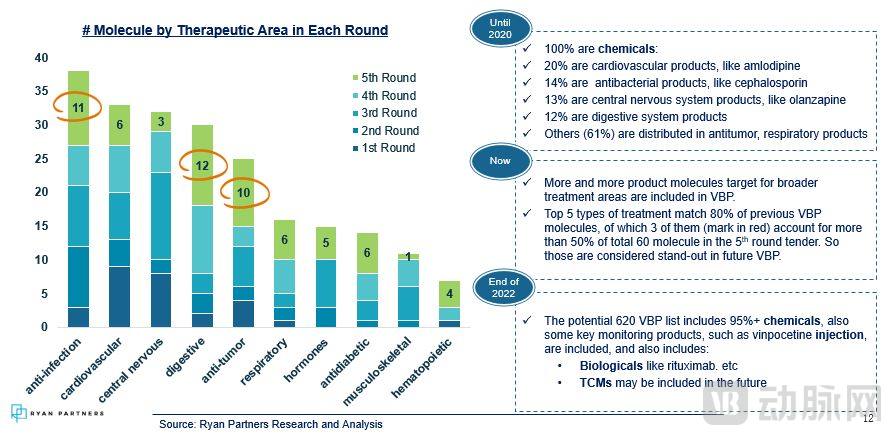

In recent years, the bidding rules for volume-based procurement have been continuously refined, and the policy coverage has been adjusted in each round of bidding.

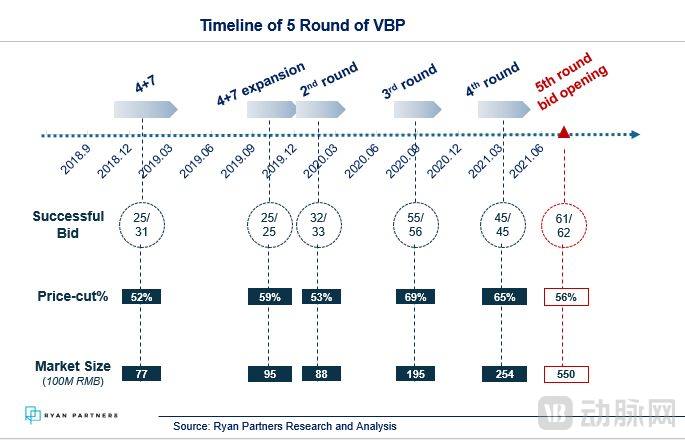

Nowadays, volume-based procurement (VBP) is no longer a novelty in the healthcare industry. The pace of issuing VBP announcements has accelerated, and so has the speed of policy implementation. The time interval from policy release to execution, as well as between successive rounds of centralized procurement, has significantly shortened. Companies have become increasingly adept at adjusting their pricing strategies in response to VBP policies, with a success rate approaching 100%. During bidding, prices typically drop by 50%, after which manufacturers are reluctant to make further concessions, as they gain market share but sacrifice profits. The market size covered by products included in VBP continues to expand, with total sales rising from an initial RMB 7.7 billion to over RMB 50 billion by the fifth round.

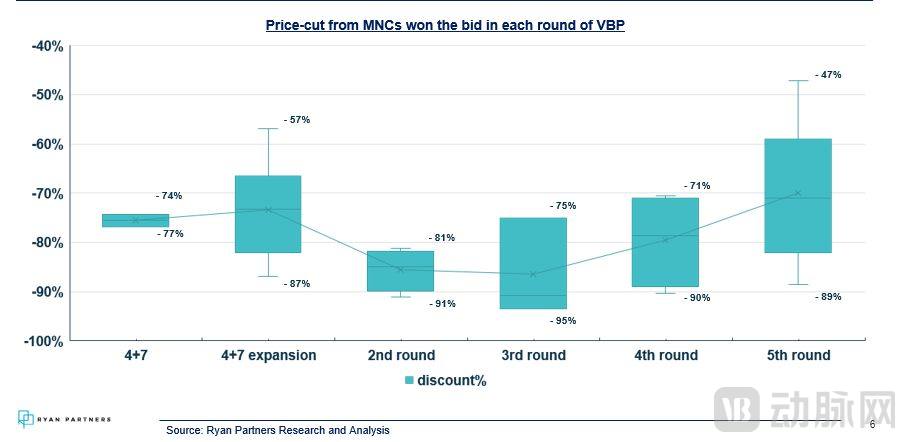

Centralized procurement bidding results show that initiators had to significantly reduce prices to win bids, but in the most recent round of bidding, the average price reduction has rebounded.

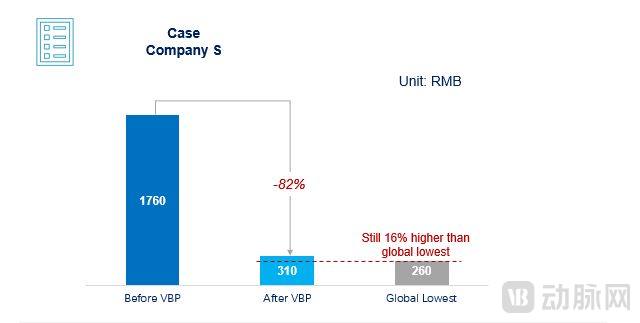

Taking a platinum-based anticancer drug from Company S as an example, its price after the volume-based procurement, despite an 82% reduction, remains higher than the global lowest price.

In the fifth round of centralized procurement bidding, Company S won the bid in the June public tender at a price of RMB 310.51. Compared with the ceiling price of RMB 1,760, Company S secured and maintained its market share by offering an 82% price reduction. Nevertheless, Company S’s final price remained higher than its lowest global selling price, indicating that the decision to reduce prices was still driven by considerations of cost of goods sold.

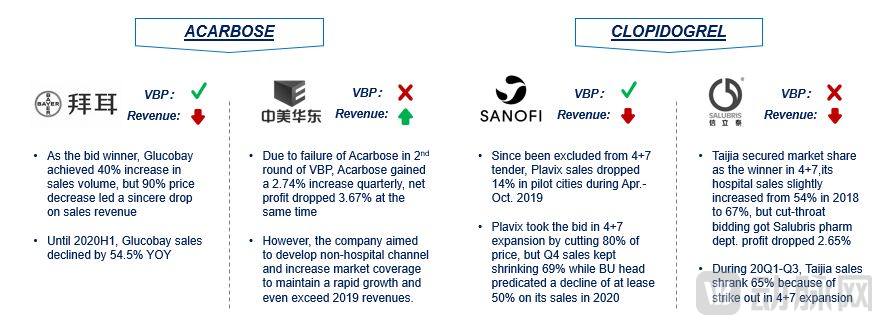

Under the influence of volume-based procurement, market performance varies significantly among different products within the same category. However, regardless of whether they win the bid, the profitability of all products has been affected to varying degrees due to the substantial price reductions in procured categories.

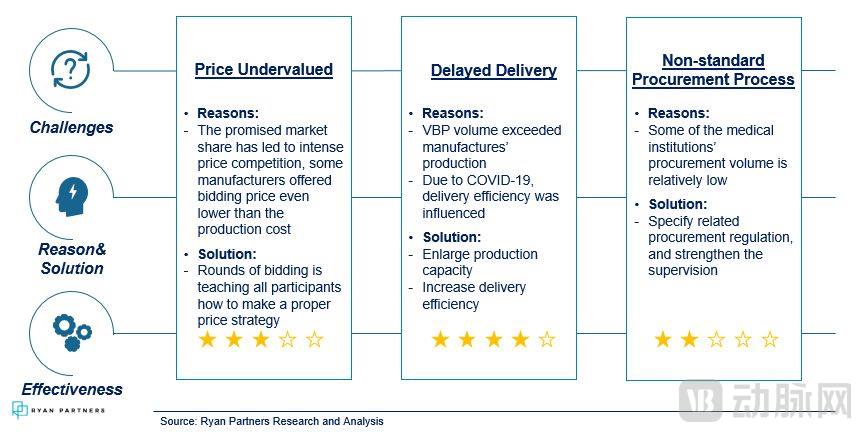

The implementation of the centralized procurement policy has brought some new challenges.

The contracted procurement volumes have triggered intense price competition, with some manufacturers submitting bid prices even below production costs. Bidding enterprises should draw lessons from previous rounds of centralized volume-based procurement (VBP) to learn how to set reasonable bid prices, rather than blindly lowering them to the minimum. On the other hand, as VBP quantities sometimes exceed manufacturers’ production capacity, and delivery efficiency has been impacted by the COVID-19 pandemic, delayed deliveries have occurred. Companies need to expand production capacity and improve delivery efficiency to address these challenges. In addition, some medical institutions have relatively low procurement volumes and non-standardized procurement processes. There is an expectation for further clarification of procurement-related regulations and strengthened oversight.

In light of the adjustments made in previous rounds of centralized procurement policies, the coverage of product categories, regions, and institutions under centralized procurement has been expanding.

In recent years, centralized procurement policies have gradually become standardized. Based on the rules of previous rounds of national and provincial centralized procurement, we anticipate that policy changes will follow several key trends:

1Further Expansion of Product Categories

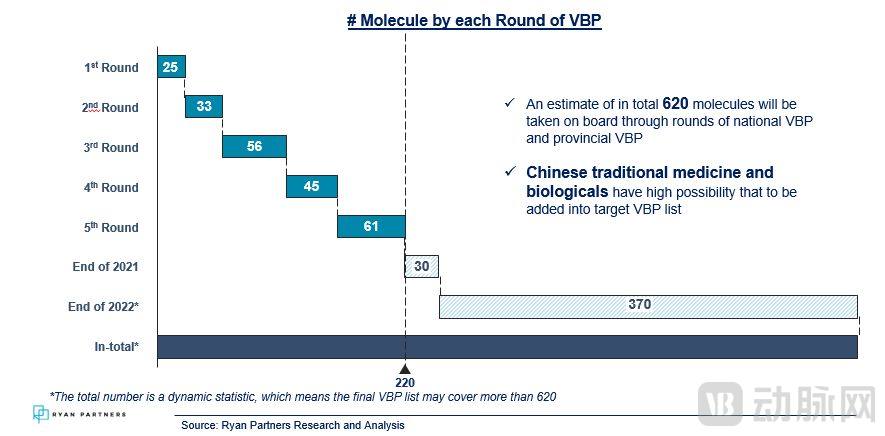

To date, China’s national centralized procurement program has included only 220 out of 620 product categories, accounting for the top 80% by purchase volume. It is projected that approximately 620 product categories will participate in centralized procurement by 2022.

Under the current trend, products with high sales volume and a high proportion of reimbursement through medical insurance are more likely to be included in the centralized procurement list.

At the same time, the therapeutic areas included in the catalog are more diverse.

2Geographic coverage further expanded, with rules becoming more comprehensive and diversified

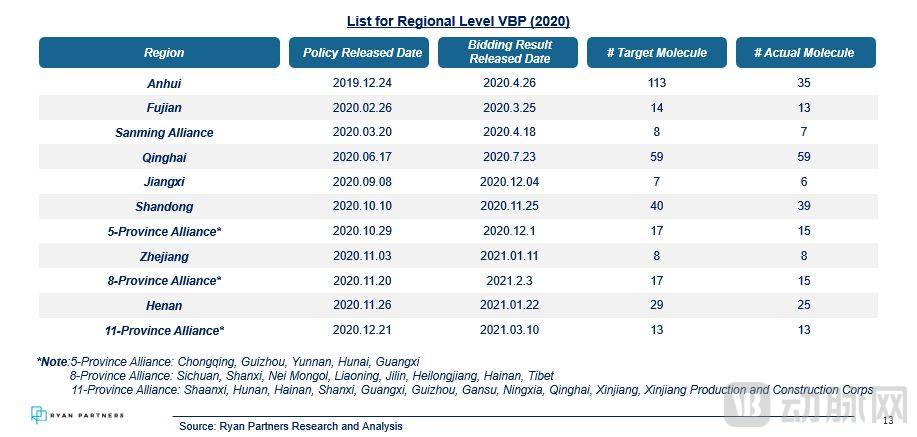

An increasing number of regions have participated in the previous rounds of national centralized procurement. Some provinces and municipalities have independently formulated their own centralized procurement rules and adjusted bidding regulations according to local conditions. To ensure the regional coverage and implementation effectiveness of centralized procurement, many regions have formed alliances for implementing centralized procurement.

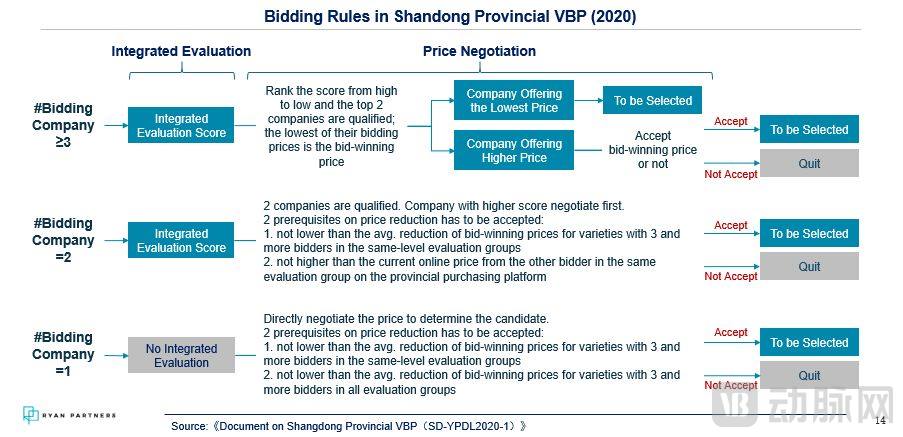

Taking Shandong Province as an example, the province has established bidding rules applicable to regional volume-based procurement.

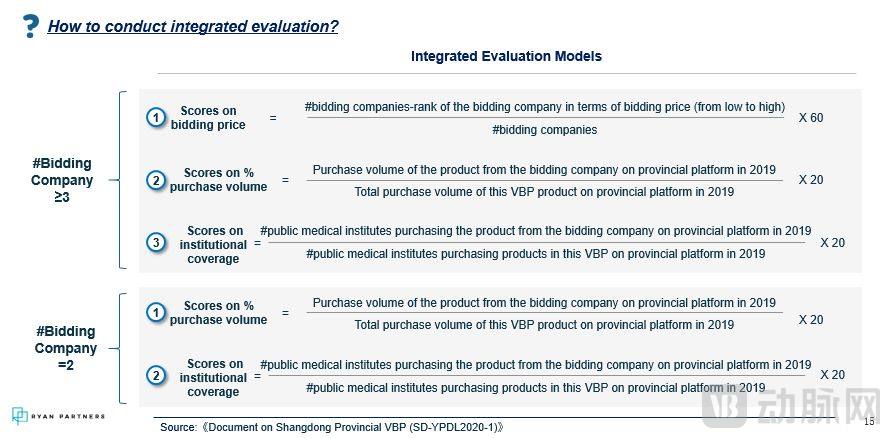

Shandong employs multiple evaluation models to select candidates under varying numbers of bidders.

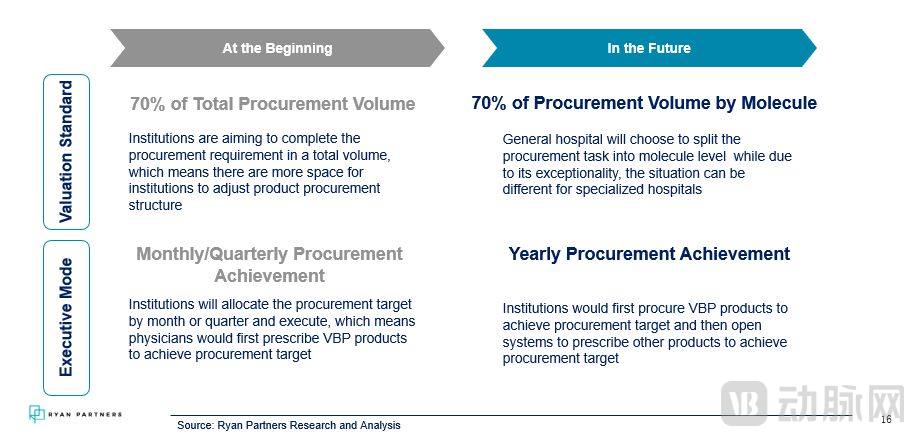

3Rigorous Implementation at the Institutional Level

During the initial phase of the “4+7” centralized procurement policy, healthcare institutions exhibited deficiencies in implementation. However, as regulations became more standardized, these institutions have accumulated extensive experience and enforced the policy with increasing rigor.Compliance with National Regulations. With the standardization of VBP and the introduction of more detailed regulatory provisions, regulatory efficiency will be further enhanced.

Under regulatory pressure, hospitals have implemented various measures to meet procurement and prescription quotas for volume-based procurement (VBP) products.

On January 28, 2021, the State Council issued Document No. 2, which requires medical institutions to implement protocols within their prescription information systems to prioritize the sales volume of enterprises that have won bids in centralized procurement. The purchase and use of bid-winning products serve as key performance indicators for public medical institutions and their heads, and constitute an important consideration in determining the overall health insurance budget.

Therefore, in terms of procurement, hospitals prioritize the acquisition of bid-winning products. Once the procurement volume targets for these products are met, non-bid-winning products may be purchased based on clinical needs. During procurement, hospitals are required to establish a ratio between bid-winning and other products, with the stipulation that the quantity of other products must not exceed that of bid-winning products.

On prescriptions, the Hospital Information System (HIS) monitors the prescription volume of bid-winning products; if the volume reaches the set target, prescribing other products is permitted. In some cases, only physicians with senior or higher professional titles are authorized to prescribe non-bid-winning products. Some hospitals allow only the prescription of bid-winning products but require that the reasons be explained to patients.

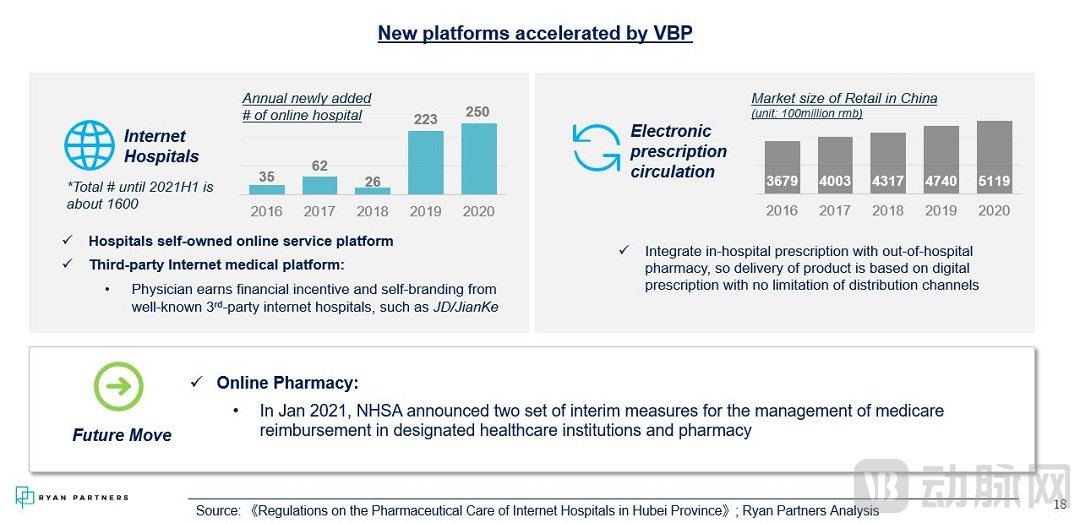

Exploring the potential of the out-of-hospital market and prescription outflow will provide new opportunities for products that failed to win bids in centralized procurement.

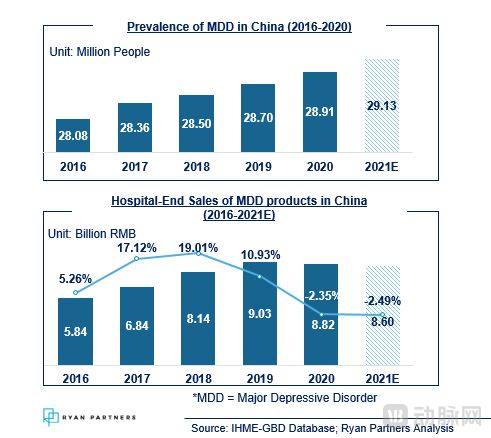

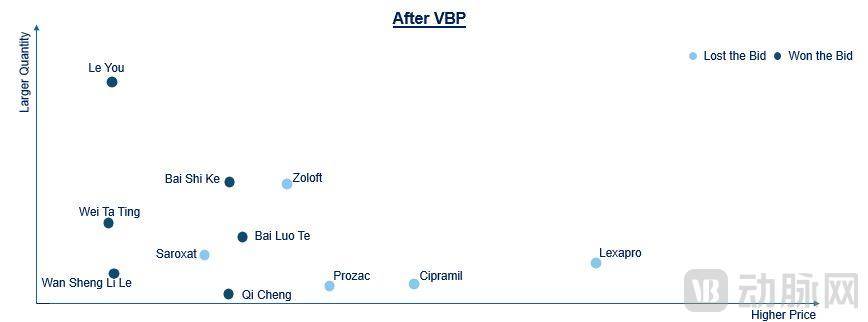

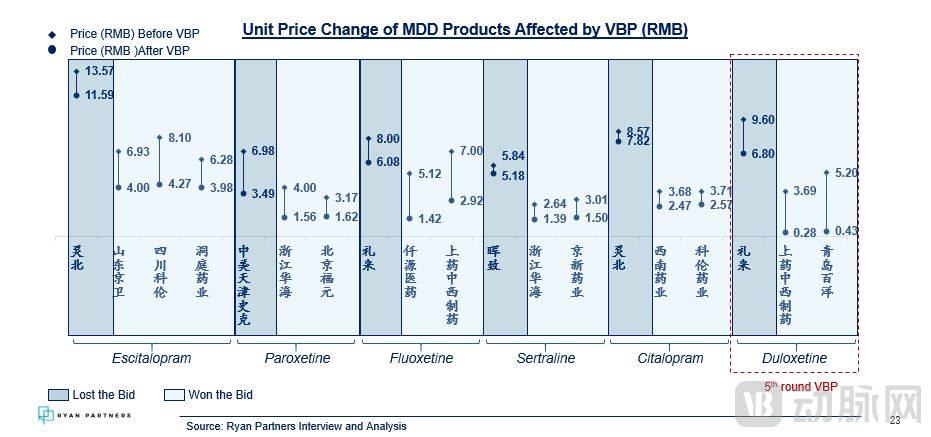

Taking the antidepressant drug market as an example, the number of patients with depression has steadily increased since 2019, but the growth in product sales has gradually slowed down.

The prevalence of depression in China has remained stable at approximately 2.1% annually. The typical duration of treatment for patients with depression ranges from 6 to 36 months. As the patient population gradually increases and long-term medication use becomes more common, market demand for antidepressant products continues to expand.

In the past few years, sales of antidepressant products grew rapidly, but since 2019, the growth rate has shown a downward trend. Although the fact that hospitals were not open to general patients due to the COVID-19 pandemic is also an important reason for the decline in sales, the significant price reductions under the centralized procurement policy have also hindered market growth.

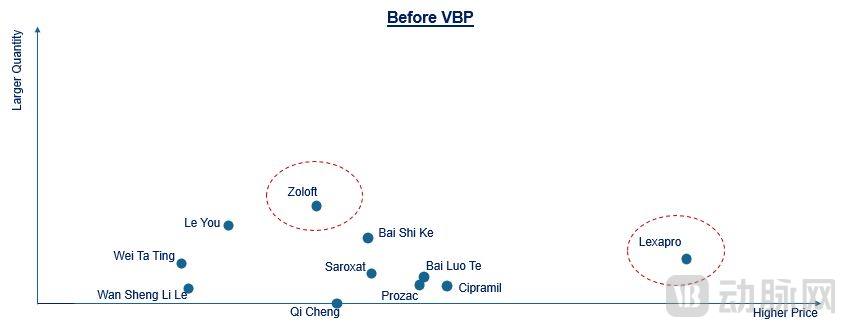

Centralized procurement has shifted the market strategy for antidepressant products toward exchanging lower prices for higher sales volumes.

Prior to centralized procurement, originator drugs were generally priced higher than their domestic competitors, yet most still captured the vast majority of market share. For a long time, the top two players in the antidepressant market have been Zoloft and Lexapro, whose dominance has relied respectively on high market penetration and high selling prices.

Since the essence of centralized volume-based procurement (VBP) is competitive bidding, pharmaceutical companies aiming to win bids have no choice but to lower their product prices. Even for drugs that are not included in the bidding, price reductions may still be pressured when procurement platforms require price linkage. Therefore, compared with maintaining high prices, it is more feasible to sustain sales performance by expanding sales volume. Out-of-hospital markets, such as retail pharmacies and online pharmaceutical e-commerce platforms, as well as lower-tier markets in suburban and rural areas, may offer further growth opportunities.

The decline in prices of antidepressant products within the scope of previous rounds of centralized procurement has led to a slowdown in market growth.

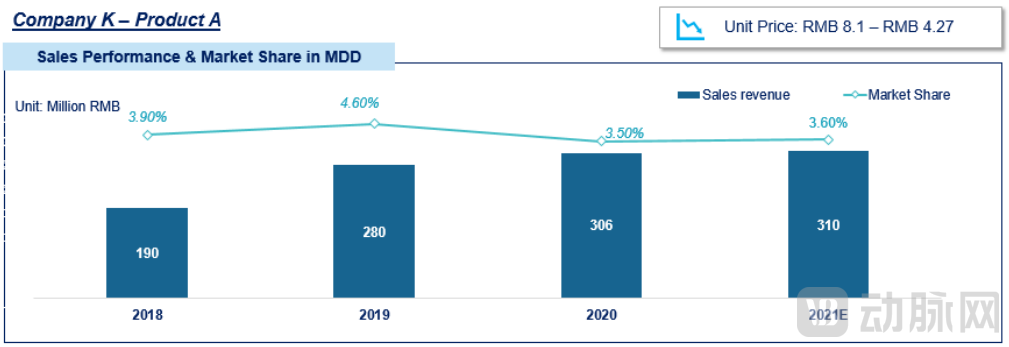

Company K's Product A"As one of the winners in the centralized procurement, we better promoted our products by adjusting the sales team and quickly gained a larger market share."

Following the "4+7" centralized volume-based procurement (VBP) program, Company K established its own sales team to enhance its information dissemination capabilities. By thoroughly interpreting policy requirements, the sales team facilitated hospitals’ compliant implementation, ensuring the fulfillment of agreed-upon procurement volumes. Meanwhile, by actively demonstrating the efficacy and safety of the winning bid products, the company encouraged hospitals to continue prescribing Product A even after meeting their contractual procurement obligations. Additionally, Company K actively pursued academic promotion, organizing more academic conferences in the provinces where its products won the bids.

Company K expanded its hospital coverage by continuously enlarging its in-house sales team.

During the transitional period, branch offices retain limited authority to distribute any of Company K’s products. For branches with established sales teams for successfully bid products, Company K permits them to maintain independent sales teams. In provinces where bidding was unsuccessful, distribution responsibilities remain with distributors.

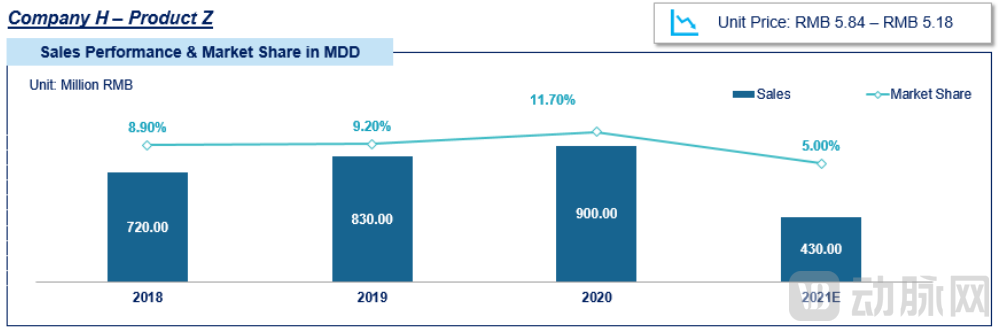

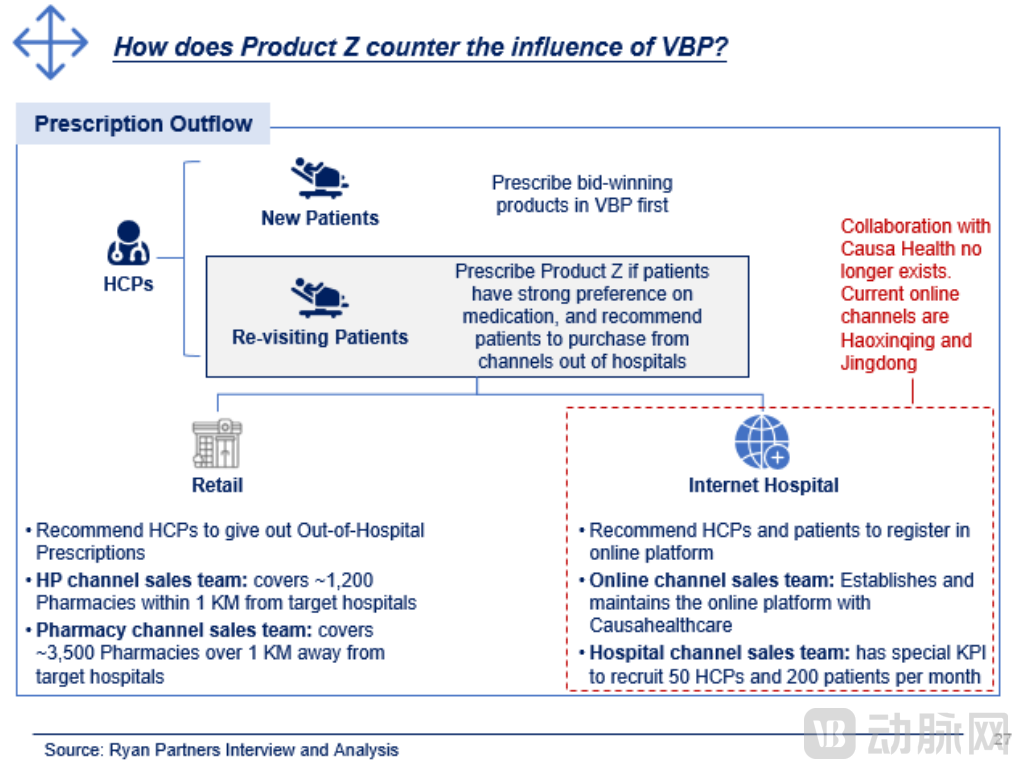

On the other hand, due to the failed bid, the importance of Product Z at Company H declined significantly, and the company’s restructuring further delayed the implementation of its new strategy.

It is reported that following the conclusion of this bidding process, the sales performance of Product Z is expected to decline, prompting the company to lower its 2021 sales targets. At the end of 2020, Company H underwent restructuring, and Product Z was ranked last in importance among all products managed by Company H, resulting in only limited resources being allocated to it. The company’s next strategic objective is to penetrate markets outside hospitals; retail revenue for 2021 is projected to grow by 25%, while online revenue is expected to increase by 15%. However, to date, retail channels have contributed only 15% of Product Z’s revenue, and online sales have accounted for merely 5%. Achieving the target of having non-hospital sales contribute 40% of total revenue appears to require a longer timeframe.

Company H leverages prescription outflow to seek opportunities for selling products that failed in hospital tenders within the out-of-hospital market.

Since failing to win bids in the centralized procurement, Company A has lost more than half of its market share in China within its niche segment.

Taking a business unit of Company A as an example, although the sales team was downsized, the digital marketing team was expanded to enhance online promotion. After the second round of volume-based procurement (VBP), when its key products failed to win bids in the VBP, the business unit of Company A did not change its team size. During the third round of VBP, Company A secured its position by significantly reducing product prices, thereby maintaining its market share. The team, which originally consisted of more than 800 employees, was subsequently reduced to over 500, with 150 medical representatives (MRs) primarily responsible for the sales of Product Y in key cities.

Subsequently, Product Y devoted significant efforts to digital marketing in 2021:

● Promotional/discount campaigns received positive feedback on JD.com, achieving a repurchase rate of >50% and sustaining an average treatment duration of 3 months.

● Conduct patient education on Douyin once every quarter

● #MedicationGuidanceExplained# Explaining the Differences Between Originator Drugs and Generic Drugs

● Collaborate with physicians to provide point-based rewards/kickbacks

At the same time, Company A has also established strategic partnerships with commercial insurance providers and e-commerce platforms.

Ryan Partners provides clients with comprehensive solutions, including global market research, market access strategies, and market potential assessment, among other business intelligence offerings. We address the diverse challenges clients encounter at different stages of the business cycle, helping them evaluate and understand market dynamics and potential opportunities to compete more effectively in the global marketplace. Our mission is to provide the strongest possible assistance and support to ensure our clients’ success in global markets.

Ryan Partners is composed of professionals dedicated to management consulting and research, specializing in vertical industries such as pharmaceuticals and healthcare, fast-moving consumer goods (FMCG), manufacturing, and digital new media, with expert skills and services. Currently, it has branches in Shanghai (China), France, Malaysia, and Singapore, serving multinational corporations and rapidly growing innovative enterprises worldwide.

Scan the QR code below to follow Ryan Partners and gain more industry insights. Thank you!