China's Answer to Da Vinci: MicroPort Medical Robotics Launches $5.4B IPO After Five Years in Stealth

On November 2, the Hong Kong Stock Exchange welcomed its first surgical robotics company: MicroPort MedBot.

The surgical robotics sector once produced the renowned high-performing stock Intuitive Surgical. When Intuitive Surgical went public in 2000, its share price was merely $9; today, it exceeds $350, with a market capitalization reaching hundreds of billions of dollars.

MicroPort MedBot, given its high degree of business similarity to Intuitive Surgical, is regarded as China’s Intuitive Surgical. Can MicroPort MedBot replicate Intuitive Surgical’s growth myth?

In terms of share price, MicroPort MedBot issued 36.2 million shares at an offering price of HK$43.20 per share. In the grey market trading on November 1, MicroPort MedBot opened at HK$44.00, representing a 1.85% premium over the offering price of HK$43.20 per share, but closed down 7.29% at HK$40.05. Based on the offering price, MicroPort MedBot’s market capitalization will reach HK$41.777 billion.

From a product line perspective, MicroPort MedBot and Intuitive Surgical have highly overlapping businesses.Backed by MicroPort Scientific Corporation, MicroPort MedBot has adopted an all-encompassing product strategy, covering five major sectors: laparoscopic surgery, orthopedic joint replacement, natural orifice surgery, vascular intervention, and percutaneous puncture. Its pipeline even surpasses that of Intuitive Surgical.

Although MicroPort MedBot has a rich product pipeline, its commercialization is still in the early stages, with no surgical robots approved yet. Furthermore, MicroPort MedBot’s competitors extend beyond Intuitive Surgical; medical device giants such as Medtronic, Johnson & Johnson, and Siemens are also focusing heavily on this market, while several domestic companies are poised to enter.

Surgical robots have been on the market for over 20 years, yet their global penetration rate remains at only 3%; in the Chinese market, this figure is even lower.

Can the joint efforts of multiple global companies unlock China’s surgical robot market? What core products support MicroPort MedBot’s market capitalization? VCBeat (WeChat ID: vcbeat) has compiled an analysis on these questions.

MicroPort is a leading domestic medical device company. Starting with drug-eluting stents, it has grown into a group with eight major business segments: cardiovascular interventional products, orthopedic medical devices, rhythm management, aortic and peripheral vascular interventional products, neurointerventional products, heart valve therapies, surgical robotics, and general surgical medical devices.

MicroPort Medical reported operating revenue of RMB 2.485 billion and a net loss of RMB 583 million in the first half of 2021. However, for MicroPort Medical, the primary focus has not been on its financial figures, but rather on its listed subsidiaries.

MicroPort Medical has earned the nickname “the company that produces publicly listed medical companies.” In 2019, MicroPort Medical spun off its subsidiary MicroPort Endovascular for listing on the STAR Market; in 2021, it spun off MicroPort CardioFlow for listing on the Hong Kong Stock Exchange. MicroPort MedBot is the third listed company spun off by MicroPort Medical. Additionally, MicroPort Medical has several other subsidiaries.

As the third listed subsidiary of MicroPort, its surgical robotics business had long been kept under wraps. According to the prospectus, MicroPort actually began developing laparoscopic surgical robots as early as 2014, incubating it as an internal project. In 2015, MicroPort MedBot was incorporated in China and commenced the development of joint replacement surgical robots.

In 2020, MicroPort MedBot entered a period of rapid development.

The high speed is first reflected in product advancement: MicroPort MedBot’s core laparoscopic surgical robot, Toumai, has begun clinical trials, while its joint replacement robot, Honghu, has entered the green approval channel.

Meanwhile, MicroPort MedBot also began external fundraising, completing its Series A and Series B financing rounds in August and November 2020, respectively, and introducing several prominent strategic investors, including Hillhouse Capital, CPE, Bailin Capital, Yuanyi Investment, and E Fund Capital.

Following the infusion of investment, MicroPort MedBot began actively pursuing external acquisitions.Through collaborations with overseas medical robotics companies Robocath, NDR, and Biobot, the company has established a presence in pan-vascular interventional robots, percutaneous puncture surgical robots, and natural orifice transluminal endoscopic surgical robots, thereby enriching its product portfolio and laying the foundation for its 2021 IPO.

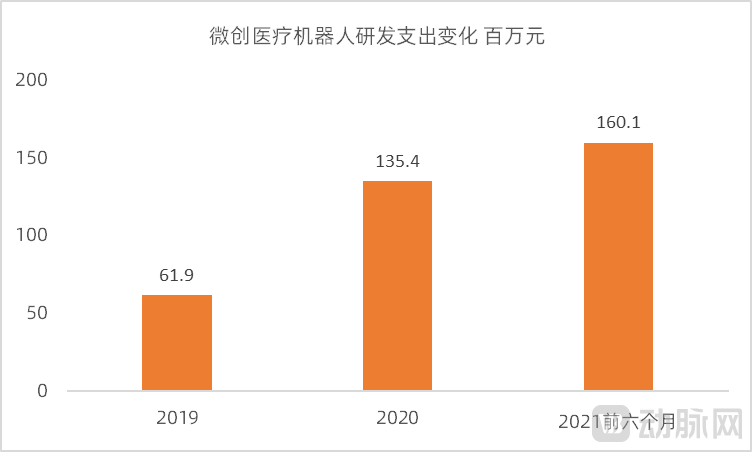

The clinical advancement of products and aggressive external acquisitions have also driven up the R&D expenditures of MicroPort MedBot. In the first half of 2021, R&D spending reached RMB 160 million, surpassing the total R&D investment for the entire year of 2020. Meanwhile, MicroPort MedBot’s losses have continued to widen. The net losses for 2019, 2020, and the first half of 2021 were RMB 69.8 million, RMB 209 million, and RMB 242 million, respectively.

In the future, MicroPort MedBot’s revenue pillars will primarily rest on its laparoscopic surgical robots and orthopedic joint replacement robots. However, achieving commercial returns in these two major markets is no easy feat.

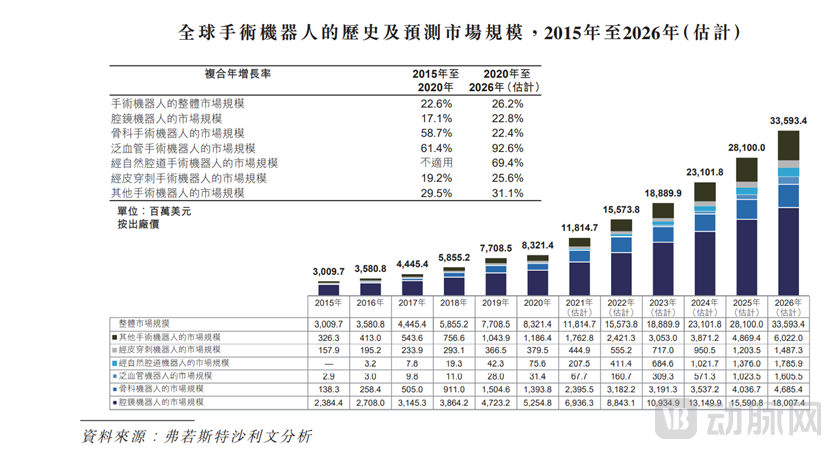

According to Frost & Sullivan data cited in the prospectus, the global surgical robot market can be segmented into five major markets by market size: laparoscopic surgical robots, orthopedic robots, pan-vascular robots, percutaneous puncture robots, and other surgical robots.

The laparoscopic surgical robot market is the largest and most competitive segment.

The market size of laparoscopic surgical robots is supported by two major factors. On one hand, there are extensive application scenarios; laparoscopic surgical robots can be used in urological, gynecological, thoracic, and general surgical procedures, replacing traditional surgical workflows. On the other hand, laparoscopic robotic products are the most mature.

It has been over 20 years since Intuitive Surgical launched its first-generation da Vinci surgical robot. As of March 2020, the global installed base of da Vinci robots had reached 5,669 units, with a cumulative total of approximately 7.2 million procedures performed. Currently, there are 3,581 da Vinci robots installed in the United States and 800 across Asia.

Although many believe that the high cost of laparoscopic surgical robots has constrained the domestic market size, in reality, the growth of China’s laparoscopic surgical robot market has exceeded expectations.

First, from the perspective of market demand, there is an undersupply of laparoscopic surgical robots in clinical practice. According to data from MicroPort MedBot’s prospectus, during the three-year period from 2018 to 2020,In the United States, an average of 240 surgeries are performed annually with the assistance of a laparoscopic surgical robot, whereas in China, the annual average number of such procedures is 299.

Tang Hao, a partner at Tianfeng Capital, stated, “In terms of surgical volume, the average number of procedures performed per da Vinci surgical system in China is approximately twice that in the United States. In 2018, The First Affiliated Hospital of Zhengzhou University completed 1,198 robotic surgeries, setting the world record for the highest annual surgical volume by a single unit. Therefore, while clinical adoption of robotic systems can scale up rapidly, their installation base remains limited due to constraints such as high costs, configuration permits, and a shortage of proficient surgeons.”

From the perspective of individual hospitals in China, there is strong demand for surgical robots among large-scale hospitals.. Taking the First Affiliated Hospital of Zhengzhou University as an example, the hospital has already been equipped with three da Vinci surgical robots, and the volume of robot-assisted laparoscopic surgeries had exceeded 3,000 cases by 2019.

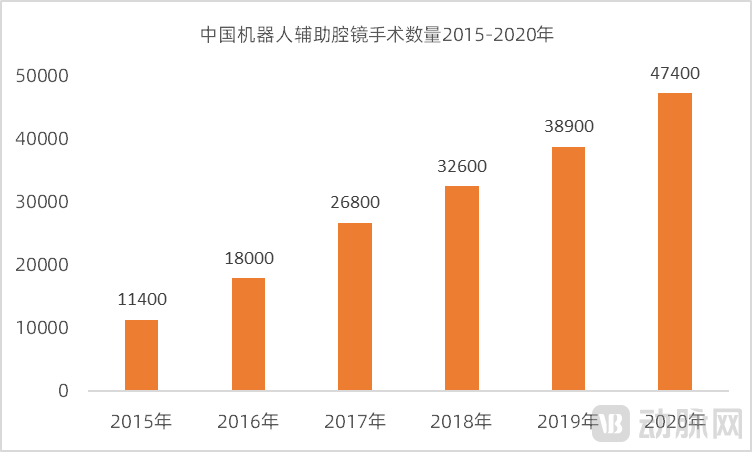

Driven by robust demand, the volume of laparoscopic robotic surgeries in China is expected to continue growing. The number of robot-assisted laparoscopic procedures performed annually in China increased from approximately 11,445 cases in 2015 to 47,379 cases in 2020.The compound annual growth rate is 32.9%, and it is expected to further increase to 681,098 cases in 2026.

Data source: MicroPort® Robot Prospectus

On the payment side, China’s national medical insurance is gradually expanding reimbursement coverage for laparoscopic surgical robots, a policy that will further drive the expansion of the laparoscopic surgery market.

The da Vinci Surgical System has long been considered expensive. In reality, its costs consist of two components: equipment procurement and maintenance, plus the cost of specialized consumables. Laparoscopic surgeries assisted by the da Vinci Surgical System are typically 20,000 to 40,000 RMB more expensive than traditional laparoscopic procedures.

Medical insurance reimbursement for surgical robots is gradually expanding. In April 2021, Shanghai included certain AI-assisted therapeutic technologies in the basic medical insurance coverage, with reimbursement limited to radical prostatectomy, partial nephrectomy, total hysterectomy, and radical resection of rectal cancer.

The vast market for laparoscopic surgical robots and Intuitive Surgical’s continuously rising stock price have driven global medical device companies to enter this market.

Global companies in the laparoscopic surgical robot industry can be divided into two major tiers.

The first tier consists of industry giants, including Medtronic and Johnson & Johnson, both of which are deploying laparoscopic surgical robots. Medtronic’s Hugo surgical robot and Johnson & Johnson’s Ottava are regarded as strong competitors to Intuitive Surgical’s da Vinci surgical robot.

The second tier consists of emerging companies. In China, the total financing raised by enterprises developing laparoscopic surgical robots has exceeded RMB 1 billion. VCBeat has compiled a list of the major global players in laparoscopic surgical robots and the commercialization status of their core products.

Major Laparoscopic Surgical Robots Worldwide

The laparoscopic surgical robot market is a stronghold of Intuitive Surgical, posing significant commercialization challenges for new entrants.

From the perspective of the current market landscape, the da Vinci surgical robot series has installed over 3,500 units in the United States and 250 units in China. Although there is still a significant gap in terms of numbers, the da Vinci surgical robots have achieved high coverage among top-tier hospitals in China. Given the high cost of configuring surgical robots, how new entrants can expand into new hospital markets remains a major challenge.

The most basic thresholds are the commercial access license and the allocation permit.In China, apart from the da Vinci Surgical Robot System, only Weigao’s laparoscopic surgical robot has received regulatory approval. Other major domestic laparoscopic surgical robots are still in the clinical trial phase.

The second major hurdle is differentiated innovation.Differentiating from the da Vinci Surgical System is a core competitive dimension for laparoscopic surgical robots.In terms of pathway selection, technological superiority and cost breakthroughs are the primary approaches.

The current da Vinci system is not perfect; from a clinical perspective, there is still room for improvement in terms of controllability and degrees of freedom. For example, unlike the four-arm design of the da Vinci system, Johnson & Johnson’s Ottava surgical robot system employs a six-arm configuration to achieve greater controllability and higher degrees of freedom.

Another major “weakness” of the da Vinci Surgical System lies in its high cost, which limits its rapid expansion in clinical settings. To address this shortcoming, several domestic companies are reducing costs through independent research and development and supply chain optimization.

Shurui, a Chinese surgical robotics company, reduces costs through an integrated single- and dual-port design and in-house production of core components, while expanding procedural capabilities with its snake-like arm design to establish differentiated competition against the da Vinci Surgical System.

The third major challenge stems from market education.Market training can only be conducted after approval, and capturing physicians’ mindshare through such training is critical for market expansion. The da Vinci Surgical System has been in the Chinese market for over a decade, with the first six years focused on training Chinese physicians.

Tang Hao, a partner at Tianfeng Capital, stated, “The entire healthcare system is relatively conservative and cautious; both physicians and hospitals require substantial data and case studies for support, which constitutes one of the challenges in the clinical adoption of surgical robots.”

Beyond the laparoscopic surgical robot market, orthopedics is also a key battleground for surgical robots.

The limited field of view for surgeons and the high precision requirements in orthopedic surgeries create fertile ground for the adoption of surgical robots in orthopedics. Orthopedic surgical robots provide enhanced imaging of the surgical site, cause less damage to healthy bone, and facilitate faster recovery.

Existing orthopedic surgical robots are primarily joint replacement robots and spinal robots.。

Orthopedic robots for joint replacement are primarily used in total knee arthroplasty (TKA), unicompartmental knee arthroplasty (UKA), and total hip arthroplasty (THA).

# Minimally Invasive Spinal Orthopedic RobotThe spine is a complex motion system within the human body, characterized by intricate anatomical structures and close proximity to critical neural and vascular tissues, such as the spinal cord, vertebral arteries, and venous plexuses. Minimally invasive spinal orthopedic robots can significantly shorten the surgical learning curve and overcome the limitations associated with both traditional open spinal surgery and conventional minimally invasive spinal procedures.

In China, orthopedic surgical robots were introduced relatively early, yet their penetration rate remains low.

In 2020, the number of robot-assisted joint replacement surgeries performed in China was 243, with a penetration rate of less than 0.1%.

Tinavi was the first company in China to launch an orthopedic surgical robot for spine and trauma surgeries. From 2017 to 2019, Tinavi recognized revenue from 16, 20, and 41 units of its orthopedic surgical navigation and positioning robots, respectively. In 2020, the sales volume of Tinavi’s orthopedic surgical navigation and positioning robots reached 30 units.

Although Tinavi’s orthopedic surgical robots were commercialized at an earlier stage, the company remains unprofitable. Data for this year show that in the first three quarters of 2021, Tinavi generated RMB 105 million in revenue, a year-on-year increase of 37.09%, while posting a net loss of RMB 64 million.

The commercialization challenges for orthopedic surgical robots are greater than those for laparoscopic surgical robots.

Like laparoscopic surgical robots, orthopedic surgical robots have also been included in urban medical insurance reimbursement. According to regulations issued in September 2021, starting from October 2021, robot-assisted orthopedic surgeries in Beijing are eligible for 100% medical insurance reimbursement, while disposable supplies used in robot-assisted orthopedic surgeries are partially covered by medical insurance.

The main shortcomings of orthopedic surgical robots lie in the technical aspect.Previously, orthopedic surgeons pointed out that large-scale surgical robots better address all issues encountered during surgery, whereas orthopedic surgical robots can only resolve one or several key problems in the procedure. Moreover, the relatively segmented nature of the orthopedic robot market has also limited its overall size.

For instance, spinal surgical robots primarily assist in the placement of screws such as pedicle screws, but they do not provide assistance in procedures involving spinal exposure, decompression, or fusion. Joint surgical robots mainly perform femoral and tibial osteotomies, but they do not assist with joint exposure, prosthesis implantation, or soft tissue balancing.

Unlike Tianzhihang, MicroPort’s orthopedic surgical robots are primarily designed for joint replacement procedures. The domestic market for orthopedic joint surgery robots in China also has no shortage of participants.

Competitive Landscape of Joint Replacement Surgical Robots in China

Orthopedic artificial joints are one of MicroPort’s core businesses. With the launch of its joint surgery robot, MicroPort can offer an integrated solution, thereby tapping into the domestic market for orthopedic surgical robots.

The third most prominent area for surgical robots is the vascular intervention market, where the volume of vascular intervention procedures, like laparoscopic and orthopedic surgeries, reaches millions.

Pan-vascular surgical robots are used to treat diseases of the circulatory system or organs related to the cardiac, cerebral, or peripheral vascular systems. The greatest clinical benefit of vascular interventional surgical robots is the reduction of radiation exposure to physicians, while also enhancing the precision of surgical manipulation.

The new product category of pan-vascular interventional surgical robots is also facing significant competition. The most advanced vascular interventional robot globally is Siemens’ Corindus Vascular Robotics system, which has currently entered China’s innovative medical device approval pathway.

Major players in China's vascular interventional robotics sector also include Weimai Medical, Aopen Medical, and Aibo Medical.

MicroPort MedBot’s vascular interventional robot is not entirely independently developed; instead, it has established a joint venture with the French medical robotics company Robocath (Shanghai Zhimai) to manufacture and sell certain Robocath robots and accessories in the Greater China region. These robots and accessories have already received regulatory approval outside of Greater China.

Vascular intervention is a key strength of MicroPort MedBot. MicroPort holds advantages in both physician resource accumulation and market channel development, which may facilitate the commercialization of its pan-vascular interventional surgical robots.

In terms of R&D layout, MicroPort Medical attaches great importance to vascular interventional robots. In addition to the pan-vascular interventional robot for PCI procedures, MicroPort is also developing a TAVR robot.

Before genuine commercial outcomes are realized, the surgical robotics industry has attracted substantial capital and high expectations. However, the true measure of this industry’s success is not its level of capitalization, but rather its clinical value and performance in each individual surgery. The Chinese medical device market has long anticipated the emergence of a “Chinese da Vinci” surgical robot and a “Chinese Intuitive Surgical.” In reality, what China lacks is not products similar to the da Vinci surgical system, but rather truly disruptive innovation.

Reference: Why Did Orthopedic Robots and General Surgical Robots Start at Almost the Same Time, Yet General Surgical Robots Achieved Greater Commercial Success? Firsthand Insights from Physicians at Tier 3A Hospitals – MedRobot