Commercial Health Insurers Navigate Opportunities and Challenges Amid DRG/DIP Reimbursement Reform

China’s commercial health insurance market has expanded rapidly in recent years, with its size growing from RMB 67.7 billion in 2010 to RMB 817.3 billion in 2020, representing a compound annual growth rate (CAGR) of 28%. In January 2020, the China Banking and Insurance Regulatory Commission (CBIRC) and other relevant departments jointly issued the “Opinions on Promoting the Development of Commercial Insurance in the Social Services Sector,” which set a target to exceed RMB 2 trillion in the health insurance market size by 2025.

Looking ahead, the market size of commercial health insurance continues to expand, with its coverage scope constantly broadening, positioning it as an increasingly important solution for medical payments. Meanwhile, a wave of DRG/DIP payment method reforms is sweeping through the sector, bringing about significant changes to healthcare reimbursement mechanisms. This will undoubtedly have a profound impact on China’s healthcare and medical insurance systems. While commercial health insurance faces challenges amid these payment system reforms, it can still stand out by seizing the emerging opportunities.

This article is byShao Xiaojun, Chief Medical Officer of China Pacific Life Insurance Co., Ltd.andJiang Yishi, Data Analysis Manager, Health Insurance Division, China Pacific Life Insurance Co., Ltd.Completed through collaboration, this study aims to explore the impact of DRG/DIP payment system reforms on commercial health insurance and how the industry can respond.

The views expressed in this article are solely those of the author and do not represent the views of VCBeat. The intellectual property rights to the content published by VCBeat are exclusively owned or held by VCBeat and/or the relevant rightsholders. Without prior permission, any use, including but not limited to reprinting, excerpting, copying, or creating mirror images, is strictly prohibited.

Health insurance payment is a critical component of health insurance management and the deepening of healthcare reform, serving as an important lever to regulate medical service behavior and guide the allocation of medical resources. Therefore, reforms in the health insurance payment system will have a significant impact on both basic medical insurance and commercial health insurance. For a long time, China’s health insurance payment model has primarily been fee-for-service. While this approach has promoted the development of medical technologies and healthcare institutions, it has also tended to induce over-treatment, placing substantial pressure on health insurance funds.

In 2017, the State Council issued important documents requiring the comprehensive implementation of a diversified and composite medical insurance payment system dominated by case-based payment. Subsequently, the National Healthcare Security Administration launched two reform pilots for case-based payment: Diagnosis-Related Groups (DRG) and Global Budgeting with Regional Points and Big Data Diagnosis-Intervention Packet (DIP). This marked a significant reform in medical insurance payment methods.

DRG, short for Diagnosis Related Groups, refers to a payment system developed in the United States in the 1970s for application within the Medicare program. Subsequently, this payment model was adopted by Europe, Australia, and certain Asian countries, and is now widely recognized as one of the more advanced healthcare payment systems globally.

Based on factors such as patient age, gender, length of stay, clinical diagnosis, procedures/surgeries, disease severity, comorbidities and complications, and outcomes, Diagnosis-Related Groups (DRG) classify patients into several diagnostic-related groups. DRG possesses the capacity for self-improvement and development, allowing for continuous optimization of grouping by integrating clinical practice and advances in medical technology. In contrast, Big Data Diagnosis-Intervention Packet (DIP) is a big data-based case-mix index payment model. As a healthcare reimbursement method with distinct local characteristics, DIP is suitable for regions where the implementation of DRG is temporarily hindered by inadequate data infrastructure.

Based on these groups, basic medical insurance further establishes corresponding payment standards in accordance with Diagnosis-Related Groups (DRG) or Big Data Diagnosis-Intervention Packet (DIP), thereby achieving the goal of standardizing the utilization of medical resources. Given that patients will no longer receive itemized billing statements under the diagnosis-based payment model, this change in the payment process will directly impact the claims administration of commercial health insurance. Insurers will be unable to allocate liability across individual line items when processing claims, resulting in reimbursement based solely on the total cost.

For health insurance policies that cover only benefits within the scope of basic medical insurance or specific sub-categories, if exclusions or benefit segmentation cannot be applied, insurers are required to pay claims exceeding their actual liability. This will lead to underpricing of health insurance products, thereby affecting the sustainability of the health insurance sector, particularly long-term medical insurance.

For example, an insurer recently received a claim for commercial health insurance. The insured was hospitalized for “medical treatment of Henoch-Schönlein purpura.” This condition is covered under the diagnosis-related group (DRG) payment system; regardless of the specific medical treatments provided, the hospital charges a fixed DRG rate of RMB 4,790. As hospitals no longer provide itemized billing statements under the DRG payment model, the inpatient receipt submitted by the insured only shows a lump-sum “other inpatient charges” of RMB 4,790 and an out-of-pocket amount of RMB 2,205, without breaking down costs for bed fees, Western medicines, laboratory tests, etc. Consequently, the insurer cannot apply itemized billing according to the coverage responsibilities stipulated in the prior contract and must instead use the total out-of-pocket expense as the basis for claims calculation and reimbursement.

If changes in claims processing represent the most direct impact of the DRG/DIP health insurance payment reform, then more importantly, it will usher in new concepts and transformations for commercial health insurance products, particularly presenting both opportunities and challenges for traditional health insurance offerings such as critical illness insurance, million-yuan medical insurance, and Huiminbao.

First, DRG/DIP grouping is based on disease severity and medical resource consumption. This grouping method provides a new classification approach for insurance products covering specific disease liabilities, enabling the design of innovative commercial health insurance products.

For instance, based on DRG/DIP disease group weights, scientifically define mild, moderate, and severe disease groups to design specific-disease insurance products with fixed benefits; or, in accordance with DRG/DIP disease group weights, design tiered allowance levels to develop reimbursement-based or allowance-based medical insurance plans that feature disease-specific tiers and equitable subsidies.

Upgrading of Inpatient Allowance Insurance Following the Reform of DRG/DIP-Based Medical Insurance Payment Methods

Secondly, the primary objective of implementing DRG/DIP prospective payment is to incentivize hospitals to shift from pursuing revenue maximization to profit maximization, thereby enabling reasonable control over commercial health insurance claim expenditures.

Since the payment standards for each DRG/DIP group are relatively fixed, if the actual cost of diagnosis and treatment exceeds the predetermined payment standard, the hospital must bear the excess; conversely, the hospital may retain any resulting surplus. Pharmaceuticals, medical consumables, and diagnostic tests have become costs of care delivery rather than sources of hospital revenue. Consequently, in most countries implementing DRG-based payment, after government health insurance programs adopt DRG payments, commercial health insurers also tend to use DRG-based methods to settle inpatient expenses with healthcare providers.

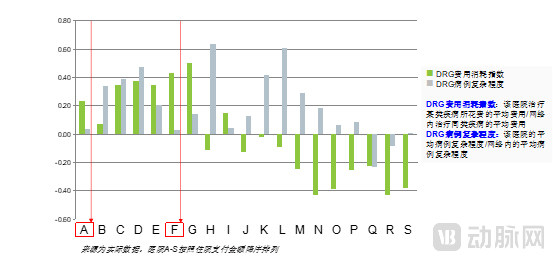

The core competitive element of commercial health insurance is the medical service network. The implementation of Diagnosis-Related Groups (DRG) provides a set of scientific evaluation metrics for healthcare institution performance and service capabilities, which can be used for the analysis and assessment of medical service networks (Provider Profiling). As commercial insurance companies in China prepare to build their own medical networks, DRG/Diagnosis-Intervention Packet (DIP) payment methods have become an optional payment model. This approach facilitates the establishment of a cooperative mechanism between commercial health insurers and healthcare institutions that features profit-sharing and risk-sharing, thereby promoting the coordinated development of the healthcare system and commercial insurance.

Case Study of Medical Network Analysis Based on DRG Evaluation Metrics: Hospitals A and F, marked in red, are medical institutions that treat simple cases but charge higher medical fees, requiring intensive follow-up attention and management.

Furthermore, the DRG/DIP system enhances the transparency of medical activities and promotes transparent clinical workflows. It facilitates the standardization and normalization of medical record quality, thereby providing high-quality medical data. Through comprehensive medical cost accounting, it helps build a new healthcare ecosystem based on DRG/DIP, achieving rational allocation of medical resources and improved efficiency.

This has significantly enhanced commercial health insurers’ understanding of medical practices and related data, laying a solid foundation for the end-to-end implementation of innovative health insurance products—including design, pricing, and claims processing. DRG/DIP data are characterized by their broadest dimensionality and high degree of structuring, providing more detailed information on medical care and patient visits.

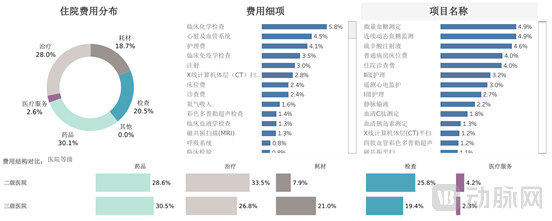

For instance, DRG/DIP data contain detailed inpatient cost information, making it possible to disaggregate the structure of hospitalization expenses. Setting caps based on specific cost categories and pricing high-cost drugs and consumables separately facilitates actuarial pricing and risk control for commercial health insurance. Furthermore, commercial insurers can conduct big data analytics on metrics such as average cost per case and length of stay for each DRG/DIP group, thereby establishing reasonable cost ranges for DRG groups and mapping disease-specific cost profiles. This enables the identification of unreasonable charges and triggers manual claims adjudication, thereby precisely controlling claims risks.

DRG Cost Fingerprint Chart

In summary, the reform of medical insurance payment methods based on Diagnosis-Related Groups (DRG) and Big Data Diagnosis-Intervention Packet (DIP) has built a bridge for mutual understanding and collaboration between the healthcare industry and commercial insurance companies, deepening their mutual understanding and further facilitating their cooperation.

With the development of the health insurance market, innovative operations in health insurance have entered a new stage of growth. Insurance companies are actively positioning themselves, and product design and innovation that integrate health management have become a major trend in market development. The reform of DRG/DIP payment methods facilitates commercial insurers’ deeper integration into the healthcare service system, enabling them to master medical insurance payment technologies and healthcare management systems. This truly bridges “insurance products + health services,” providing the public with more comprehensive economic and health protection.

It is crucial not to overlook the potential adverse effects of DRG/DIP payment models, including case selection, upcoding, overtreatment, and frequent readmissions. Hospitals may prioritize cases with lower costs and higher profit margins while shifting or refusing unprofitable cases. To increase revenue, hospitals may engage in upcoding by assigning higher-level diagnosis or procedure codes, thereby moving medical records into DRG/DIP groups with higher reimbursement rates. Furthermore, hospitals might provide more complex or expensive treatments to qualify for higher-paying DRG/DIP groups, or boost revenue by increasing the frequency of patient admissions.

Therefore, the DRG/DIP payment model imposes more refined claims adjudication requirements on commercial health insurers, necessitating the establishment of big data-based audit mechanisms and systems grounded in DRG/DIP to ensure reasonable reimbursement of medical expenses.

It is thus evident that the reform of medical insurance payment methods based on diagnosis-related groups (DRGs) presents both opportunities and challenges for commercial health insurance.

The reform of DRG/DIP-based medical insurance payment methods, through global budgeting and the establishment of payment standards for disease groups, encourages hospitals to focus more on medical costs and clinical workflows, thereby helping to curb unreasonable growth in healthcare expenditures. From a management perspective, it supports performance evaluation and enhances transparency in clinical processes, facilitating the rational allocation of medical resources and improving efficiency. In terms of data, it contributes to better medical record quality and the provision of high-quality data, offering a more accurate actuarial basis for commercial health insurance.

Meanwhile, the reform of DRG/DIP payment methods will also face challenges. Under the influence of new payment models, hospitals may alter their medical practices, such as shifting costs and increasing claims against commercial health insurance. Consequently, commercial health insurers will need to adjust their product design logic and strategies. In the future, aspects such as payees, design philosophies, and claims settlement mechanisms in commercial health insurance will all be impacted by this reform.

Commercial insurance companies should proactively respond to and participate in the national reform of DRG/DIP-based medical insurance payment methods, assist the government in implementing corresponding DRG/DIP-supported management controls and assessment measures, and accumulate experience in the implementation of DRG/DIP payment systems. Meanwhile, they should apply the insights gained from in-depth study of DRG/DIP payment mechanisms to commercial health insurance, laying the foundation for future healthcare network development and the provision of “insurance + services” products, while safeguarding against increased commercial insurance claims resulting from cost shifting by hospitals.

In the initial phase, commercial insurance companies can select a subset of high-utilization healthcare institutions and DRG/DIP disease groups for pilot programs. Using the DRG/DIP payment standards as a benchmark, they should set reimbursement rates based on the specific circumstances of the hospitals where patients receive care and their own negotiation leverage, and then negotiate pricing and sign contracts with these hospitals.

Furthermore,Commercial health insurers can also conduct in-depth research on DRG/DIP payment methodologies, applying the data and principles of DRG/DIP to essential components of health insurance, such as product design and risk control.Design insurance products based on DRG/DIP payment models to appropriately transfer cost risks and effectively control medical expense costs; utilize DRG/DIP case-mix groups for claims settlement to improve processing efficiency, while implementing real-time intelligent DRG/DIP audits and medical reviews to effectively identify fraud, waste, and abuse.

As China’s healthcare system reforms deepen, reforms to health insurance payment methods will also be further advanced. Drawing on international experience and aligning with China’s national conditions, value-based integrated healthcare delivery systems will become the mainstream direction for future development. Diagnosis-related group (DRG)-based payment is a key stage in this reform, driving health insurance payments to focus on the actual value of healthcare services.

Commercial health insurance is a vital component of the nation’s multi-tiered medical security system. Commercial insurers should proactively leverage their role as payers by establishing collaborative mechanisms that integrate with basic medical insurance and connect to healthcare services, thereby supporting national reforms in medical insurance payment methods. Playing an indispensable role in the implementation of the national healthcare reform strategy, commercial health insurance will contribute to the sustainable development of both the national medical security system and healthcare services.

The Curtain Has Risen on DRG/DIP: Are Commercial Insurers Ready to Embrace the New Era of Health Insurance Development?