Venous Intervention: The Final Billion-Dollar Frontier in Endovascular Therapy

The treatment of venous vascular diseases has become a new growth point for the global vascular intervention industry.

In the financial reports of numerous multinational corporations worldwide, venous intervention products have emerged as a new growth engine.

In Medtronic’s financial report for the first quarter of fiscal year 2022 (May–July 2021), the Coronary & Peripheral segment saw an 11% year-over-year growth. While the coronary business was significantly impacted by China’s volume-based procurement program, the venous business achieved robust growth with a rate exceeding 25%.The primary growth drivers are the VenaSeal endovenous closure system for varicose veins, the ClosureFast radiofrequency ablation system, and the Abre venous stent.。

Although the venous intervention sector in China started later than the global market, it has been experiencing rapid growth. The compound annual growth rate (CAGR) of the volume of radiofrequency ablation procedures for varicose veins from 2015 to 2019 reached 76.9%.

Interventional therapy for venous vascular diseases has given rise to multiple high-value segments. In the treatment of venous vascular diseases, products such as deep vein thrombosis aspiration devices, pulmonary embolism aspiration devices, and iliac vein stents have become key areas of focus for global medical device companies. Several domestic companies have also entered the venous intervention market. VCBeat (WeChat ID: vcbeat) has compiled an overview of two major segments within the venous intervention market—radiofrequency ablation and thrombus aspiration—mapping out the key players and their distribution landscape.

As can be seen from the chart, nearly seven companies have entered these two market segments. What trends are emerging in the competitive landscape? VCBeat provides an analysis.

In the history of the global medical device industry, vascular diseases have always been a key area for investment. In the field of cardiovascular disease, stents represent a market worth tens of billions; in cerebrovascular disease, there are thrombectomy devices and coils. As important vessels in the human body, veins are also prone to pathological changes, yet venous diseases are often overlooked.

Clinically common venous diseases include varicose veins (VV), venous thromboembolism (VTE), and iliac vein compression syndrome (IVCS), with the total number of patients in China reaching hundreds of millions.

Among these three major categories of venous diseases, interventional therapy for venous thromboembolism (VTE) is regarded as the most valuable new frontier over the next decade, due to its high mortality rate and high in-hospital incidence.

Why is VTE a Worthwhile Investment Sector?

VTE includes pulmonary embolism (PE) and deep vein thrombosis (DVT).

In terms of case fatality rate, pulmonary embolism (PE) within venous thromboembolism (VTE) ranks as the third leading vascular disease worldwide, alongside ischemic heart disease and stroke.The treatment markets for myocardial infarction and stroke have already spawned industries worth hundreds of billions, while the treatment of venous thromboembolism (VTE) remains in its early stages of development.

Deep vein thrombosis (DVT) is a condition characterized by impaired venous return due to abnormal blood clot formation within the deep veins. When a thrombus dislodges and obstructs the pulmonary arteries, it results in pulmonary embolism (PE). PE is associated with an extremely high case fatality rate and is distinguished by its high incidence, high disability rate, and high mortality, making it a critical and acute condition of the respiratory system.

Globally, there are nearly 10 million cases of venous thromboembolism (VTE) annually, with up to 60% of VTE events occurring during hospitalization or after discharge, making it a leading cause of preventable in-hospital death.In China, the prevalence of VTE is 27% among ICU patients, 12.4%–21.7% among stroke patients, and reaches as high as 40% in orthopedic patients.

From the perspective of hospital prioritization, the prevention and treatment of venous thromboembolism (VTE) have become a key focus in China’s efforts to improve healthcare quality and patient safety in recent years.In February 2021, the National Health Commission issued the "Notice on the 2021 National Goals for Improving Medical Quality and Safety." This notice, for the first time at the national level, proposed ten major goals for improving national medical treatment safety, including "increasing the standardized prevention rate of venous thromboembolism" as one of the targets.

From the perspective of diagnostic and treatment capacity building, in 2018, China launched a nationwide project to build capabilities for the prevention and treatment of pulmonary embolism (PE) and deep vein thrombosis (DVT). The VTE prevention and control capabilities of hospitals across China have been significantly enhanced. As of September 2021, nearly 30% of county-level regions had achieved coverage under this VTE prevention and control capacity-building project, laying the foundation for the market penetration of VTE therapeutic products.

Three major factors—high case fatality rate, heightened in-hospital attention to the disease, and improved hospital diagnostic and therapeutic capabilities—position VTE to become the next growth pole in the field of vascular intervention, following stroke and ischemic heart disease.

However, the expansion of the VTE treatment market faces a major constraint: the lack of mature therapeutic products.

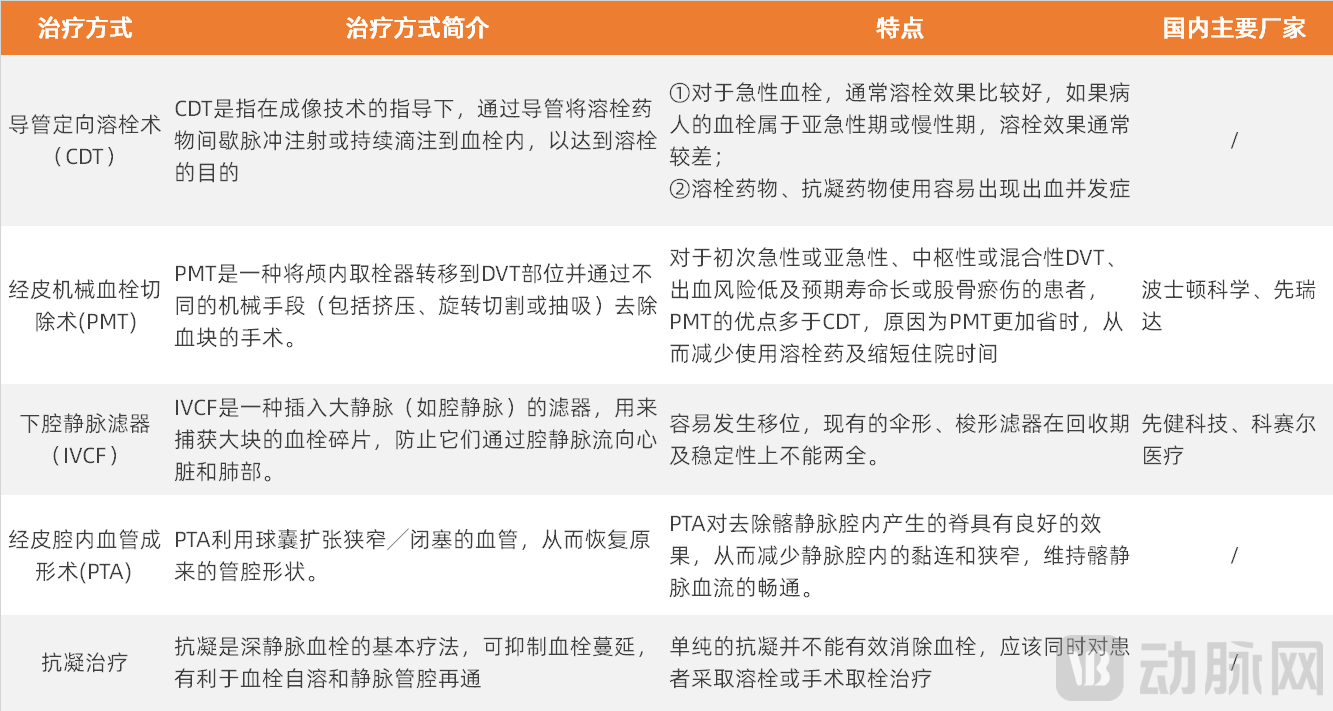

VTE can be managed with various treatment modalities, including basic anticoagulation therapy, catheter-directed thrombolysis (CDT), percutaneous mechanical thrombectomy (PMT), inferior vena cava filters, and percutaneous transluminal angioplasty.

VCBeat has summarized the characteristics of different major treatment modalities for venous thromboembolism (VTE). In clinical practice, catheter-directed thrombolysis (CDT) is the primary thrombolytic approach employed by hospitals, with the most commonly used CDT catheters being UniFuse (AngioDynamics, Inc.) and Cragg-McNamara (EV3, Inc.). However, CDT has its limitations: treatment may need to continue for up to seven days, its main complication is bleeding at various sites, and there is a significant risk of thrombus embolization during the thrombolytic process.

# Main Treatment Modalities for VTE

For CDT, the primary direction of innovation is to reduce the use of thrombolytic agents.Boston Scientific has launched EkoSonic in this field. EkoSonic is a specialized dual-lumen catheter. One lumen houses a wire equipped with multiple ultrasound transducers that emit high-frequency, low-intensity ultrasound waves, while the other lumen features multiple ports for localized thrombolysis. The ultrasound energy facilitates the penetration of thrombolytic agents into the thrombus, thereby reducing the required dosage of thrombolytic drugs. Boston Scientific aims to leverage this product to pioneer advancements in thrombolytic therapy for pulmonary embolism.

In the treatment of VTE, PMT products are also held in high regard.Currently, two thrombectomy devices have been approved in China: Boston Scientific’s AngioJet Thrombectomy System and Straub Medical’s Aspirex Mechanical Thrombectomy Device. However, neither product has yet received approval for use in the aspiration treatment of pulmonary embolism.

Due to the previous lack of specialized devices for mechanical peripheral thrombectomy in China, clinical management of deep vein thrombosis (DVT) has been relatively passive. To address the absence of dedicated peripheral aspiration systems in clinical practice,Mechanical thrombectomy devices specifically designed for venous vessels will become the prevailing trend.

Currently, the market for mechanical aspiration of deep vein thrombosis (DVT) in the United States is predominantly dominated by Penumbra’s product portfolio. Prior to the launch of Penumbra’s products in 2013, the U.S. faced a situation similar to what China is experiencing today. Following its introduction, Penumbra’s mechanical thrombectomy aspiration devices were rapidly adopted in clinical practice and have remained the mainstream standard in this field ever since.

Penumbra, the global leader in aspiration thrombectomy, has reaped substantial profits by developing dedicated aspiration products for the peripheral vascular field.

Penumbra, the global leader in aspiration technology, built its foundation on neurointerventional aspiration products. In 2014, Penumbra launched the Indigo® Aspiration System for peripheral thrombectomy, designed to remove clots from arteries and veins in the peripheral vascular system and to treat pulmonary embolism.

In Penumbra’s latest Q3 2021 financial report, revenue from its peripheral product portfolio surpassed that of its neurovascular portfolio, with a faster growth rate as well. In Q3 2021, Penumbra’s peripheral product portfolio generated $105 million in revenue, a year-on-year increase of 40.3%, with the Indigo Aspiration System being the primary driver of growth in the vascular segment. Meanwhile, revenue from neurovascular aspiration products amounted to $84.65 million, representing an 11.5% year-on-year increase.

After recognizing the opportunity in peripheral thrombectomy products, Penumbra also developed its next-generation vascular aspiration product, Lightning. The Lightning aspiration catheter, designed for pulmonary embolism, features a large lumen and circumferential sweeping aspiration.

Who Can Replicate Penumbra’s Success in the Peripheral Intervention Field in China?

Acandis, a leading domestic player in peripheral interventions, has also developed a product for peripheral thrombus aspiration, which is expected to receive approval and hit the market in the near future.

Acandis’s thrombectomy aspiration devices incorporate numerous targeted design features tailored to the characteristics of peripheral vascular thrombi.

It is understood that, in terms of flexibility, Spectranetics catheter walls adopt a multi-stage gradient hardness design, enabling the catheter to navigate smoothly through tortuous vascular pathways or stenotic lesion segments. In terms of support strength, Spectranetics employs a metal coil structure, ensuring that the catheter does not kink even after traversing sharply angled vascular paths. This maintains the maximum cross-sectional area of the lumen, facilitating smoother thrombus aspiration. Additionally, the metal braided structure provides excellent pushability and torque control, allowing precise execution of the operator’s maneuvers and accurate feedback of various intraoperative tactile sensations.

Notably, Acandis’ thrombectomy products account for the important application scenario of pulmonary embolism (PE) thrombectomy. A dedicated shaped catheter has been designed specifically for patients with acute PE, making it one of the few domestically developed original products in China indicated for both deep vein thrombosis (DVT) and PE. The aspiration pump of Acandis’ peripheral aspiration system received approval from the National Medical Products Administration (NMPA) on August 5, 2021.

Currently, the domestic thrombectomy aspiration market in China is still in its early stages, but the volume of procedures is growing at a rapid pace.

According to data presented by Professor Liu Jianlong, approximately 1–2 individuals per 1,000 adults develop lower extremity deep vein thrombosis (DVT) annually. Venous thromboembolism (VTE), which includes deep vein thrombosis and pulmonary embolism, has a postoperative incidence rate exceeding 1.5%, with pulmonary embolism ranking as the third leading cause of clinical death.

The number of thrombectomy procedures in China increased from 29,000 cases in 2015 to 60,000 cases in 2019, representing a compound annual growth rate (CAGR) of 19.9%. The figure is estimated to reach 142,000 cases in 2024, with a CAGR of 18.7% from 2019 to 2024, and further increase to 527,000 cases by 2030, corresponding to a CAGR of 24.4% from 2024 to 2030.

It is expected that with the market launch of SinoMed’s products, which will fill the domestic gap in this field, the price of PMT devices will decrease relative to imported products, leading to a significant expansion of the domestic PMT market. Furthermore, given the high incidence of pulmonary embolism in obstetrics and orthopedics, it is foreseeable that growth drivers for the thrombectomy market will extend beyond vascular surgery.

The second largest growth driver in venous vascular diseases is varicose veins. Unlike VTE, which has an acute onset, varicose veins follow a prolonged clinical course.

Varicose veins are one of the most common chronic venous diseases, affecting 25%–33% of adult women and 10%–40% of adult men. In 2019, the number of patients with varicose veins in China reached 399.4 million, accounting for 28.5% of the total population, and is projected to reach 476.6 million by 2030.

As a common condition, the number of patients undergoing surgical treatment for varicose veins continues to rise.

According to data from the Zhongwei Cloud Medical Big Data Platform, between 2015 and 2017, a total of 109,000 inpatient records for varicose veins and 90,368 surgical cases were reported across 511 hospitals in 30 provinces, municipalities, and autonomous regions nationwide. Among these, 208 secondary-level hospitals accounted for 15,602 cases, while 303 tertiary-level hospitals accounted for 93,517 cases.

For severe varicose veins, treatment options include open surgery, foam sclerotherapy, and ablation therapy.

The American Venous Forum (AVF) and the UK National Institute for Health and Care Excellence (NICE) both recommend ablation therapy as the first-line treatment for varicose veins, due to its superior efficacy and lower recurrence rates compared with other treatments.

Although the number of varicose vein treatment surgeries in China has exceeded 100,000 cases,However, due to variations in the development levels of hospitals across different regions, traditional ligation and stripping procedures, which are more invasive, remain the most widely used surgical approach.Ligation and stripping surgery involves higher blood loss than minimally invasive treatment, and the average hospital stay is longer than that for minimally invasive surgery.

However, the volume of minimally invasive surgeries in tertiary hospitals is increasing year by year.The number of radiofrequency ablation procedures for varicose veins in China increased from 2,700 in 2015 to 26,300 in 2019, representing a compound annual growth rate (CAGR) of 76.9%.

With the standardization of minimally invasive procedures for varicose veins, minimally invasive therapies will replace traditional surgery, leading to a further rapid increase in surgical volume.

In minimally invasive therapy, radiofrequency ablation (RFA) and endovenous laser ablation (EVLA) are two evidence-based treatments for ablation therapy., with RFA accounting for more than 70% of endovenous thermal ablation procedures in China in 2019.

Currently, there are two radiofrequency ablation systems approved in China. There are mainly three peripheral radiofrequency ablation catheters available on the Chinese market, all manufactured by foreign companies: Medtronic’s ClosureFast and Closure RFS, and F Care Systems NV’s EVRF Endovenous Radiofrequency Closure System.

Innovation in radiofrequency ablation products is focused on reducing complications.Complications associated with existing radiofrequency ablation products primarily include skin burns, vein rupture, subcutaneous ecchymosis and swelling, and saphenous nerve injury. Controlling energy delivery, administering subcutaneous tumescent fluid, and applying continuous pressure therapy can effectively reduce the incidence of these complications. Thermal ablation techniques require tumescent anesthesia prior to energy delivery, which may cause patient discomfort and potentially prolong procedural time.

To this end, Medtronic has focused on its room-temperature closure product, VenaSeal. This closure system works by using a catheter to inject adhesive into the vein to achieve venous occlusion. VenaSeal received FDA approval for market launch in 2015 and has become a major growth driver for Medtronic’s peripheral business in recent years. The product is not yet available in China.

Domestic companies are currently focusing on the localization of radiofrequency ablation products for varicose veins and reducing complications associated with thermal ablation products.The adjustable, controllable, and intelligent features of radiofrequency ablation systems will significantly reduce the complexity of surgical procedures, representing a key direction for product improvement.

Domestic companies developing radiofrequency ablation products include Acotec and Genius Medtech.

Siruida’s radiofrequency generator can autonomously adjust output power to achieve rapid heating and automatically correct overheating, thereby maintaining temperature stability within the operational range. Considering that primary-care physicians in China have limited proficiency in radiofrequency ablation techniques, Siruida has incorporated automation features into its adjustable radiofrequency system, thereby facilitating surgical procedures for clinicians.

Xianruida’s radiofrequency ablation technology platform for great saphenous vein treatment is poised to make the company one of the few domestic manufacturers to offer both radiofrequency ablation catheters and generator systems. This achievement will break the monopoly held by imported products in the field of great saphenous vein radiofrequency ablation therapy, pioneering the substitution of imports with domestically produced alternatives.

Iliac vein compression syndrome in venous vascular diseases has also garnered significant attention. In 2019 alone, there were 700,000 patients with iliac vein compression syndrome in China. Until early 2019, there were no dedicated venous stents available in China, and arterial stents were commonly used as substitutes in interventional procedures. However, due to the substantial structural differences between arteries and veins, there is an urgent need for dedicated venous stents in China.

Unmet market demand has driven multiple companies to converge on this track, with more than eight domestic enterprises having iliac vein stents either under development or approved. In the future, competition in the iliac vein stent sector is expected to intensify.

An analysis of the key products offered by major players in the global venous disease market reveals that,There is a huge unmet demand for the treatment of venous diseases in China, requiring more mature products to penetrate the market.

Among the participants, the venous intervention market has attracted numerous companies worldwide. Global medical device giants entered the venous intervention market early; however, overall, neither aspiration products nor radiofrequency ablation products have achieved large-scale volume growth in China. Moreover, their superior next-generation products have not yet entered the Chinese market, making it difficult to meet the growing domestic demand for disease treatment. This leaves substantial market space for domestic brands, particularly in the currently underserved segments of venous thrombus aspiration and varicose vein radiofrequency ablation.

Drawing on the development of the peripheral arterial market, which preceded that of the peripheral venous intervention sector, Acotec has emerged as the leading domestic player in China’s peripheral arterial market. In the first half of 2021, Acotec reported revenue of RMB 140 million, representing a year-on-year increase of 106.0%, thereby demonstrating the growth potential of the peripheral vascular market.

Venous diseases account for half of all vascular surgery cases. Clinically, they constitute approximately 60% of vascular surgery conditions, predominantly affecting the lower extremities, with an incidence rate roughly six times that of arterial diseases. As vascular surgery departments are established in hospitals across China, the volume of venous interventional procedures has rapidly increased, with its market potential expected to be no less than that of coronary interventions.

The venous intervention market is poised to become another strong growth driver for the peripheral vascular market. According to forecasts by Industrial Securities, the size of China’s venous intervention market is projected to grow from RMB 890 million in 2017 to RMB 3.1 billion in 2022, representing a compound annual growth rate (CAGR) of 28.4%.

It is foreseeable that with the improvement of medical infrastructure, rising health awareness among residents, and increasing consumption levels, the demand for treatment of venous vascular diseases in China will begin to experience rapid growth. The domestic venous intervention market will inevitably give rise to leading Chinese manufacturers.

From the perspective of domestic participants, the competitive landscape of China’s venous intervention market is beginning to take shape. Key players include multinational corporations such as Medtronic, Boston Scientific, and BD (Becton, Dickinson and Company); leading Chinese companies such as Acotec and MicroPort Endovastec; and a cohort of emerging startups.

To stand out in fierce competition, it is essential to secure a leading position in the field of venous intervention by breaking through the market gaps for domestically produced thrombus aspiration systems and radiofrequency ablation systems, possessing core proprietary technologies in this area; furthermore, there must be stable pipeline advancement capabilities and sustained innovative R&D capacity.

Breaking the stronghold of import monopoly is also the strategy of leading domestic players.Taking Acotec as an example, the company holds a dominant position in the peripheral artery sector and leads the peripheral drug-coated balloon (DCB) market. How can Acotec replicate its success in peripheral arteries within the peripheral vein space?

Based on the pipeline progress of Acotec, all products in its peripheral aspiration platform are expected to receive regulatory approval imminently. This will position Acotec as a rare Chinese enterprise in this field that possesses proprietary technology and can provide comprehensive solutions.SinoRad’s radiofrequency ablation system also completed clinical trial enrollment in the second half of the year and is expected to receive regulatory approval next year. This demonstrates that SinoRad’s strategy in the peripheral venous market is to target high-barrier, high-demand segments where domestic alternatives are lacking, leveraging its advanced technology platform and superior manufacturing processes to develop the nascent domestic market.

If we trace the path of blood circulation in the human body, blood first flows through the aorta, then passes into smaller vessels, reaching the narrowest capillaries. It subsequently transitions into thin-walled, low-pressure venous tributaries. As the veins gradually increase in diameter, their number decreases, ultimately converging into the large vena cavae, through which blood returns to the heart.

Veins play a vital role in the human circulatory system. Today, both physicians and patients are paying greater attention to venous diseases. We believe that companies with proprietary technology platforms and mastery of core technologies will reap the benefits of the rapid growth in the venous intervention market in the years ahead.

Reference: National Conference on Varicose Veins and Microcirculation 2019 | Zheng Yuehong: Vascular Surgery—A Rising Sun Discipline

Jiacai Mei: Interpretation of the Expert Consensus on the Diagnosis and Treatment of Microcirculation in Lower Extremity Superficial Varicose Veins