Navigating the Second Growth Curve: How Chinese Pharmaceutical Enterprises Are Adapting in an Era of Medical Innovation

National centralized procurement of proprietary Chinese medicines is all but a foregone conclusion.

In August, the National Healthcare Security Administration (NHSA), in its response to the “Proposal on Accelerating the Inclusion of Traditional Chinese Medicine (TCM) and Formula Granules into Centralized Procurement,” explicitly stated that, on the basis of improving quality evaluation standards for proprietary Chinese medicines and formula granules, the NHSA will work with relevant departments to scientifically and steadily advance the reform of centralized procurement for proprietary Chinese medicines and formula granules.

In September, the Hubei Provincial Medical Service Price and Centralized Drug Procurement Management Network released the “Announcement on Inter-Provincial Alliance Centralized Volume-Based Procurement of Chinese Proprietary Medicines (No. 1).” The inter-provincial alliance for centralized procurement of Chinese proprietary medicines, led by Hubei Province and comprising 19 provinces and regions, selected 76 Chinese proprietary medicine products from 17 product groups characterized by high clinical usage volume and substantial procurement expenditure.

The procurement by this inter-provincial alliance will have a significant impact on the market for proprietary Chinese medicines.

It is evident that competition among pharmaceutical companies will further intensify. Proprietary Chinese medicines that cannot guarantee efficacy and safety will lose their profit margins under the volume-based procurement (VBP) program. For winning bidders, however, this does not necessarily mean they can rapidly scale up volume to capture market share.

On one hand, hospitals are placing greater emphasis on the rational clinical use of medications, with some institutions beginning to explore optimal utilization strategies for traditional Chinese medicine (TCM) products to maximize their therapeutic efficacy. On the other hand, the emergence of scenarios involving “price caps coupled with volume limits” during pilot programs could impose significant constraints on manufacturers of proprietary Chinese medicines if such measures are replicated.

Pharmaceutical companies must contemplate, within the broader context of policy reforms, how to identify their own second growth curve.

Centralized Procurement of Proprietary Chinese Medicines and Restrictions on Adjuvant Drugs: Chinese Pharmaceutical Companies Have Begun Their Transformation

“Volume-based procurement, as a major national policy, aims to help the public address the difficulties and high costs of accessing medical care, while also tackling the issue of inflated drug prices. For pharmaceutical companies, volume-based procurement presents both challenges and opportunities for innovative and high-quality development,” said Fang Tonghua, Chairman of Zhenbaodao.

Zhenbaodao, founded in 1996, was listed on the A-share market in 2015 as “a traditional Chinese medicine (TCM) enterprise engaged in the R&D, production, and sales of multi-formulation, multi-product TCM, with a focus on high-end TCM preparations,” and has ranked among China’s Top 100 Pharmaceutical Industries for consecutive years. The company primarily focuses on advantageous therapeutic areas such as cardiovascular and cerebrovascular diseases, respiratory system disorders, and oncology, emphasizing full-cycle disease management and continuously enriching its product pipeline. As a renowned enterprise in the TCM industry, Zhenbaodao’s brand recognition is somewhat representative.

From a factual perspective, centralized procurement is not merely a crisis; it also presents an opportunity for enterprises.

On one hand, the normalization of centralized volume-based procurement has led to a restructuring of the competitive landscape for pharmaceuticals—as the overall market size shrinks, competition among pharmaceutical companies intensifies.

On the other hand, centralized procurement itself is playing a role in promoting the structural adjustment of the pharmaceutical industry, encouraging pharmaceutical companies to innovate while ensuring drug quality.

For example: Pharmaceutical companies' drugs only need to pass the consistency evaluation, and even generic drugs can compete fairly and justly with original research drugs.

The “Opinions on Carrying Out the Quality and Efficacy Consistency Evaluation of Generic Drugs” (Guo Ban Fa [2016] No. 8) issued by the General Office of the State Council explicitly stipulated that if more than three manufacturers have passed the consistency evaluation for the same drug variety, varieties that have not passed the evaluation shall no longer be selected in centralized drug procurement and other related processes. Requirements from the National Medical Products Administration also indicate that for generic drugs approved for marketing before the implementation of the new chemical drug registration classification—including those listed as essential medicines—other manufacturers producing the same variety shall, in principle, complete the consistency evaluation within three years after the first manufacturer’s product passes the evaluation.

This also means that pharmaceutical companies should not only conduct consistency evaluations but do so more rapidly. Otherwise, they face not only the loss of the hospital market but also risks to their ability to obtain drug approval documents. Stricter requirements for drug product quality mean that capable enterprises can stand out more quickly.

According to Fang Tonghua, Zhenbaodao has also placed significant emphasis on the research and development of high-end formulations and products with high technical barriers in the field of generic chemical drugs. In addition to approved products, several of its generic chemical drug candidates have entered the preclinical preparation and regulatory submission stages. Furthermore, Zhenbaodao has built a pipeline of nearly 100 generic chemical drug products, structured in a tiered reserve, with plans for phased market launches over the next two to three years.

For the centralized procurement of proprietary Chinese medicines, the overarching logic is similar to that of chemical drugs. However, there are some differences.

Currently, there is a lack of quality assessment tools for proprietary Chinese medicines (PCMs), such as consistency evaluations. The key issue may lie in the fact that volume-based procurement (VBP) for generic drugs is built upon the existing market scale established by originator drugs. Post-VBP, pharmaceutical companies are essentially competing for a relatively well-defined market segment: namely, the share previously held by manufacturers whose products failed consistency evaluations, as well as the market space occupied by off-patent originator drugs unwilling to reduce prices. However, PCMs differ in two main aspects. First, there is an absence of robust quality evaluation standards. Second, the PCM market is more heavily driven by corporate promotion efforts. Therefore, it remains to be seen whether VBP can deliver the anticipated market expansion for these enterprises.

Furthermore, in practice, drugs with particularly broad indications, insignificant clinical efficacy, and potential risks are commonly referred to as “adjuvant medications.” However, such products often have a certain market demand. To ensure the public’s medication needs, the General Office of the State Council previously proposed “key monitoring and surveillance of adjuvant medications and drugs abnormally used in hospitals, and clarifying physicians’ prescribing privileges.”

Although many traditional Chinese medicine (TCM) products are classified as “adjunctive therapies,” they still hold a significant share in disease treatment. As it becomes increasingly difficult for adjunctive therapies to gain hospital access, this trend inevitably imposes a burden on TCM pharmaceutical companies. In this challenging landscape, TCM manufacturers such as Zhenbaodao clearly cannot simply “go with the flow.” While strategically prioritizing the R&D of innovative TCM drugs, in-hospital preparations, formula granules, and the development of classical prescriptions, Zhenbaodao is also approaching healthcare policy reforms from another perspective. Its core stance is clear: to encourage pharmaceutical enterprises to pursue innovation.

The national government and various local authorities have also successively introduced a range of policies to encourage innovation. For instance, provinces such as Shanxi and Shandong began emphasizing the advancement of traditional Chinese medicine (TCM) at an early stage. In March 2020, the Shanxi Provincial Committee of the Communist Party of China and the Shanxi Provincial People’s Government issued the Implementation Plan for Building Shanxi into a Leading Province in Traditional Chinese Medicine, with the goal of establishing Shanxi as a TCM powerhouse by 2030. In 2021, six departments—including the Shanxi Provincial Department of Science and Technology, Department of Education, Department of Agriculture and Rural Affairs, Health Commission, Market Supervision Administration, and Medical Products Administration—jointly released the Traditional Chinese Medicine Technological Innovation Engineering Plan, aiming to strengthen the development of TCM technological innovation bases in Shanxi Province. Earlier this year, Shandong Province also enacted the Shandong Province Traditional Chinese Medicine Regulations to further promote the development of the TCM sector.

In the realm of innovative drugs, national initiatives such as the “863 Program,” the “973 Program,” the National Natural Science Foundation, and the Major New Drug Creation Project demonstrate the government’s strong support and commitment to fostering innovation. With comprehensive reforms in national new drug policies now covering multiple aspects of the industry—including review and approval systems, clinical trial management, intellectual property protection, the Marketing Authorization Holder (MAH) system, and the inclusion of innovative drugs in the National Reimbursement Drug List—the policy environment for enterprises engaged in new drug development has been fundamentally improved. Seizing this historical opportunity in innovative drug R&D, Zhenbaodao is vigorously promoting research and development innovation and accelerating its R&D layout. Currently, in the field of innovative drugs, Zhenbaodao has focused on completing the construction of a new drug R&D platform and establishing a drug screening and evaluation platform. By concentrating on antiviral and antitumor therapeutics, the company has launched a series of innovative drug projects.

Amidst the broader environment of centralized procurement, restrictions on auxiliary drug use, and reforms supporting innovation, how should traditional Chinese medicine enterprises transform to identify a second growth curve?

How Can Traditional Chinese Medicine Enterprises Find Their Second Growth Curve?

The pressure faced by traditional Chinese medicine enterprises is not centralized procurement.

According to data from Menet, hospital terminal sales of chemical drugs and biologics reached RMB 1.0946 trillion in 2019, while those of traditional Chinese medicine (TCM) proprietary medicines amounted to RMB 281.4 billion. The share of TCM proprietary medicines in hospital sales declined to 20.5%. In terms of overall market size, sales of TCM proprietary medicines nearly peaked in 2018 at RMB 286.1 billion, followed by a year-on-year decline thereafter. The growth of TCM proprietary medicines in the hospital sector has reached a bottleneck.

Furthermore, the further price reductions driven by centralized procurement have exerted additional impact on market size. In a scenario where the existing competitive landscape cannot be broken through, Chinese proprietary medicine enterprises are in urgent need of identifying new growth drivers.

In this process, numerous pharmaceutical companies—including Zhenbaodao, Tasly, Jiuzhitang, Pien Tze Huang, Tongrentang, and Baiyunshan—are undergoing cross-industry transformations. For traditional Chinese medicine (TCM) manufacturers to achieve sustainable growth, the longstanding business model of “heavy marketing, light R&D” has become increasingly obsolete. Under policies such as centralized volume-based procurement and restrictions on “adjuvant drugs,” companies adhering to this approach face a heightened risk of being eliminated from the market.

From the perspective of pharmaceutical companies themselves, a straightforward logic for achieving better growth may be to “increase revenue and reduce costs.”

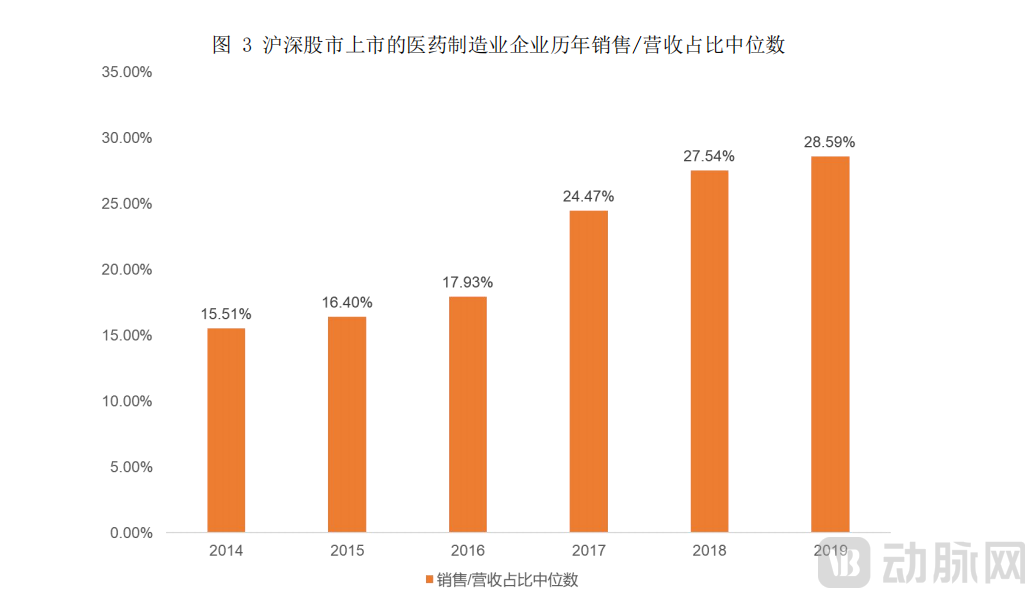

From the perspective of “cost reduction,” the historical model of “prioritizing marketing over R&D” has resulted in marketing accounting for a substantial portion of corporate costs. According to data from VCBeat’s “Innovation Report on Digital Marketing Services in the Pharmaceutical Industry,” it is evident that the median ratio of sales expenses to revenue for pharmaceutical manufacturers has remained persistently high, with an upward trend observed year after year.

Source: VCBeat's "Innovation Report on the Digital Marketing Services Industry in Pharmaceuticals"

Source: VCBeat's "Innovation Report on the Digital Marketing Services Industry in Pharmaceuticals"

Marketing costs represent a significant burden for enterprises. To boost profitability, pharmaceutical companies need to further control marketing expenses—either by cutting these costs or by improving personnel efficiency.

Digital marketing represents a viable strategy for pharmaceutical companies, enabling them to conduct marketing campaigns with lower costs and greater scalability, thereby reaching a broader audience of physicians and patients. While reducing expenses, digital marketing also facilitates the accumulation of user feedback on medications, which in turn informs and drives product updates and iterations.

In terms of improving personnel efficiency, Zhenbaodao has adopted different models for pharmaceutical sales and Chinese herbal medicine sales. In pharmaceutical sales, Zhenbaodao “vigorously expands retail terminal sales on the basis of stabilizing and enhancing sales at medical terminals, establishes a comprehensive commercial system and distribution network, leverages its academic leadership, and improves the quality of sales services.” In Chinese herbal medicine sales, it conducts targeted sales to pharmaceutical companies and professional herbal medicine market customers across China by leveraging its advantages in the entire traditional Chinese medicine industry chain, thereby further reducing sales costs.

From the “open source” perspective, pharmaceutical companies—especially those specializing in traditional Chinese medicine (TCM)—have made extensive attempts and explorations.

First, traditional Chinese medicine (TCM) enterprises are adjusting their innovation strategies. For instance, Tasly, which focuses on three major therapeutic areas—cardiovascular and cerebrovascular diseases, digestive and metabolic disorders, and oncology—has pursued coordinated development across its three core segments: modern TCM, biologics, and chemical drugs. Subsequently, it spun off and divested Tasly Biopharmaceuticals. The strategy of spinning off subsidiaries for independent listing presents both advantages and disadvantages for the parent company. On one hand, such spin-offs can provide subsidiaries with greater access to development capital, thereby supporting the growth of companies within the Tasly group. On the other hand, the impact on the parent company may be either negative or positive, introducing a certain degree of uncertainty.

In June 2021, Zhenbaodao also decided to invest in Taurus, accelerating the company’s strategic transformation and international integration through deep engagement in the biologics sector. Notably, Taurus boasts a top-tier, large-scale commercial biologics manufacturing facility in China, having overcome technical bottlenecks in process scale-up and mass production of monoclonal antibodies. This capability provides a cost advantage and enables Taurus to offer CDMO services to both domestic and international partners. Taurus maintains a high-value product pipeline comprising 11 innovative drugs and biosimilars under development, with three products approved for clinical trials (Phase I/III). Its technological expertise spans targeted therapy, antibody-drug conjugates (ADCs), cancer immunotherapy, bispecific antibodies, and nanobodies, demonstrating strong core competitiveness.

Secondly, some traditional Chinese medicine (TCM) enterprises are undergoing cross-industry transformations, leveraging brand premium to create new growth opportunities. Perhaps the most prominent example is Yunnan Baiyao, whose toothpaste has consistently maintained a dominant market share. Yunnan Baiyao’s initiatives extend beyond oral care, with explorations into product categories such as facial masks and sanitary napkins. Ma Yinglong has advanced even further into the consumer goods sector, exemplified by its launch of products including Babao eye cream, lipstick, diapers, and digestive health biscuits. This expansion from the traditional medical domain into the consumer market represents an innovative strategy currently being pursued by pharmaceutical companies.

As a “time-honored” traditional Chinese medicine (TCM) enterprise founded in 1996, Zhenbaodao has been in development for 25 years. Having weathered pharmaceutical industry reforms, it continues to maintain innovation and vitality, making it a case worthy of in-depth exploration. How did the company embark on its own journey of exploration during this process?

How Is Zhenbaodao Seeking a Second Growth Curve?

Fang Tonghua stated, “The key to addressing challenges lies in finding new momentum during the process to achieve iterative product upgrades and new breakthroughs. In this process, Zhenbaodao has chosen technological innovation, management innovation, and industrial innovation and upgrading as its entry points.”

It may be helpful to briefly review the historical evolution of Zhenbaodao. Founded by Fang Tonghua in 1996, Zhenbaodao accelerated its development after obtaining the Good Manufacturing Practice (GMP) certification for pharmaceuticals in 2001. Since 2018, Zhenbaodao has further expedited its expansion, establishing a diversified product portfolio and layout featuring multiple varieties, dosage forms, and specifications, with traditional Chinese medicine (TCM) products as the foundation and encompassing chemical drugs and biologics.

Innovative products are the lifeblood of pharmaceutical companies’ growth. In terms of technological innovation, Zhenbaodao has established a comprehensive product hierarchy and R&D pipeline by continuously developing a multi-tiered product portfolio. For different product pipelines, it has proposed distinct development strategies:

First, regarding traditional Chinese medicine (TCM). In the area of formula granules, Zhenbaodao opted to participate in the formulation of national standards and established a platform for consistency evaluation between formula granules and decoctions. It successfully filed 550 commonly used TCM formula granules, thereby gaining market access. For Zhenbaodao’s existing product portfolio, the company has collaborated with renowned universities and research institutions to conduct secondary development. For instance, the secondary development of Shuxuening Injection has expanded its clinical application scope and enhanced product competitiveness. Additionally, the company has intensified R&D efforts on in-house hospital preparations. Among the 49 in-house preparations completed, 39 varieties have been approved for dispensing and use across all Tier-II-and-above hospitals in Heilongjiang Province, and have qualified for reimbursement under the medical insurance scheme, enabling them to replace similar proprietary Chinese medicines available on the market.

Secondly, regarding chemical drugs. In terms of generic drugs, in addition to multiple products entering the pre-clinical preparation and marketing application review stages, certain drugs such as Clindamycin Hydrochloride Capsules and Metformin Hydrochloride Tablets have been approved through the Consistency Evaluation of Generic Drugs. Furthermore, it has reserved nearly 100 generic chemical drug projects. In terms of innovative drugs, it has focused on completing the construction of a new drug R&D platform and establishing a drug screening and evaluation platform. Multiple anti-tumor drugs, including the Class 1 innovative anti-tumor drug AKT kinase inhibitor HZB0071 and the Class 1 innovative anti-liver cancer drug pan-FGFR inhibitor HZB1006, have successively received approval and obtained patents in Europe and the United States.

Subsequently, with regard to biologics, strategic partnerships have been established with multiple renowned domestic biopharmaceutical R&D and manufacturing enterprises, including Tureis, to concurrently advance the development of the Biologics Research Institute at Hangzhou Medical Port. It is anticipated that a pipeline of 15–20 biologic products, structured in a tiered manner, will be established within three years, with a focus on major oncology indications such as breast cancer and lung cancer.

Notably, Zhenbaodao Investment has strategically positioned itself in the antibody-drug conjugate (ADC) sector by investing in Teruisi Pharmaceutical. The ADC sector has rapidly gained momentum following the approval of the first domestically produced ADC product. Zhenbaodao’s significant investment at this juncture reflects more than just a response to current industry trends; in fact, prior to its investment in Teruisi Pharmaceutical, Zhenbaodao had already conducted extensive long-term research on the ADC sector and participated in investments in multiple ADC companies, including Duoxi Biologics.

Ultimately, positioning Teruisi as its bridgehead in the field of ADC innovation aligns with Zhenbaodao’s own characteristics and future corporate development. In addition to its differentially positioned ADC products, Teruisi’s product pipeline includes several biosimilar products. These biosimilars will rapidly complement Zhenbaodao’s current product portfolio in the coming years. Furthermore, Teruisi’s established commercial-scale manufacturing capabilities can synergize with other biopharmaceutical companies invested in by Zhenbaodao, thereby accelerating the efficiency of industrial translation for innovative products.

A multi-pipeline product portfolio relies on organizational innovation.

Previously, Zhenbaodao’s management structure was relatively flat, with departments operating on a parallel basis. As the company deepened its R&D efforts across multiple product pipelines, it dynamically adjusted its organizational structure. While the third-quarter financial report earlier this year still reflected a “One Center, Three Institutes” framework, the company’s official website has since been updated to reflect a “One Center, Four Institutes” structure.

Image source: Zhenbaodao official website

The increasingly clear division of responsibilities within the organizational structure has also provided Zhenbaodao with a well-defined direction for development. Currently, its Beijing R&D Center is primarily dedicated to scientific and technological research, project coordination, and strategic oversight. Under this center, four specialized institutes operate with distinct R&D functions: the Beijing Institute of Pharmaceutical Research, the Harbin Institute of Pharmaceutical Research, the Bozhou Institute of Pharmaceutical Research (a minority-owned affiliate), and the Hangzhou Institute of Biopharmaceutical Research. Specifically, the Bozhou Institute of Pharmaceutical Research focuses on traditional Chinese medicine (TCM) formula granules, hospital preparations, and secondary development, while the Hangzhou Institute of Biopharmaceutical Research is responsible for the research and development of antibody-drug conjugates (ADCs), monoclonal antibodies, and bispecific antibodies.

Fang Tonghua emphasized that Zhenbaodao remains unwaveringly committed to R&D rooted in traditional Chinese medicine (TCM). Adhering to the principle of advancing both chemical drugs and biologics in parallel, the company will deepen and refine innovation in TCM products, “raise product quality standards and develop new indications, fully unlock the clinical and market value of traditional Chinese medicine, and enhance the company’s core value and competitiveness.”

The inherent emphasis of Traditional Chinese Medicine (TCM) on authentic, geo-specific medicinal materials and raw material quality has driven Zhenbaodao to strategically deploy across the entire TCM industry chain. Currently, Zhenbaodao has established a deep presence in major TCM herb-producing regions across China, integrating upstream, midstream, and downstream segments to promote comprehensive industrial upgrading from cultivation to distribution. This has resulted in a modernized “N+50” industrial layout for TCM medicinal materials, covering 95% of TCM production areas nationwide. By establishing industry standards, Zhenbaodao has achieved standardized, regulated, and traceable processing of TCM medicinal materials at their source.

The Shennong Valley·Bozhou Chinese Herbal Medicine Commodity Trading Center, a key project developed and implemented, is a global spot trading platform for bulk Chinese herbal medicines approved by the People’s Government of Anhui Province. It has established a comprehensive, one-stop smart trading and health city for Chinese herbal medicines covering all business formats. The trading center features several dedicated zones, including a cultural and tourism area, an e-commerce demonstration and interaction zone, a bulk wholesale zone (Shennong Warehouse), a decoction pieces display zone (Decoction Pieces Warehouse), and a specialized zone for distinctive varieties (Daily Chemicals Warehouse). In addition to offline display and sales, the Shennong Warehouse also conducts online sales through “Shennong Cai,” a third-party e-commerce platform innovatively developed within the trading center, further driving the “Internet Plus” upgrade of the Chinese herbal medicine industry.

Through a multi-pipeline product portfolio and organizational innovation, coupled with the renewal, iteration, and upgrading of the traditional Chinese medicine (TCM) industry, Zhenbaodao is accelerating its exploration of the “second growth curve.”

How Will Pharmaceutical Companies Develop in the Future Under an Innovative Environment?

With the further implementation of the Two-Invoice System and volume-based procurement, Chinese pharmaceutical companies are ushering in new development opportunities. As these enterprises, particularly manufacturers of traditional Chinese medicine (TCM) proprietary medicines, are driven to embrace reform, it is evident that the overall market may undergo certain new changes in the future:

① Some companies will be eliminated. Pharmaceutical companies that fail to win bids may further withdraw from the hospital market and shift their focus to the OTC and e-commerce markets;

② Large enterprises with substantial strength have more opportunities. For instance, large companies with advantages such as GAP certification, intelligent manufacturing, and professional promotion are expected to experience rapid development;

③ Accelerated transformation of pharmaceutical companies. Whether expanding from traditional Chinese medicine pipelines into innovative fields such as novel chemical drugs and biologics, or gradually shifting from the serious medical sector to the consumer health market, pharmaceutical companies will undertake more explorations in search of a second growth curve.

Change is the only constant. This holds true for the current wave of innovation among traditional Chinese medicine (TCM) enterprises. It remains to be seen what transformative advancements companies like Zhenbaodao will bring to the industry in the future, a prospect that continues to warrant anticipation.