GuShengTang Passes HKEX Listing Hearing: Which Medical Specialties Are Set to Rise?

Yesterday, Gushengtang, a chain of traditional Chinese medicine outpatient clinics, passed the hearing by the Hong Kong Stock Exchange, marking another significant step forward in its IPO journey.

Since 2021, ten companies in the medical services sector have either filed for initial public offerings (IPOs) or made significant progress in their listing processes. Among the specialized fields represented by these ten companies, four are in ophthalmology, three in dentistry, and one is in traditional Chinese medicine (TCM), as exemplified by Gushengtang.

Indeed, ophthalmology and dentistry are widely recognized as highly market-driven specialties. Their high consumer demand and scalability have fostered a cohort of industry leaders, including numerous listed and pre-IPO companies, many of which have achieved profitability. Traditional Chinese Medicine (TCM) serves a broad population, encompassing both patients and health-conscious individuals, while digitalization is providing new growth momentum for the sector.

IPO Rush in the Healthcare Services Sector in 2021; Source: Public Information, Compiled and Charted by VCBeat

So, apart from the aforementioned fields, which other specialties hold significant market potential? To better understand shifts in demand, we compared changes in specialty medical service volumes over a five-year period (Due to the impact of the pandemic in 2020, healthcare service volumes did not reflect normal conditions; therefore, this article does not use 2020 data as a reference.)。

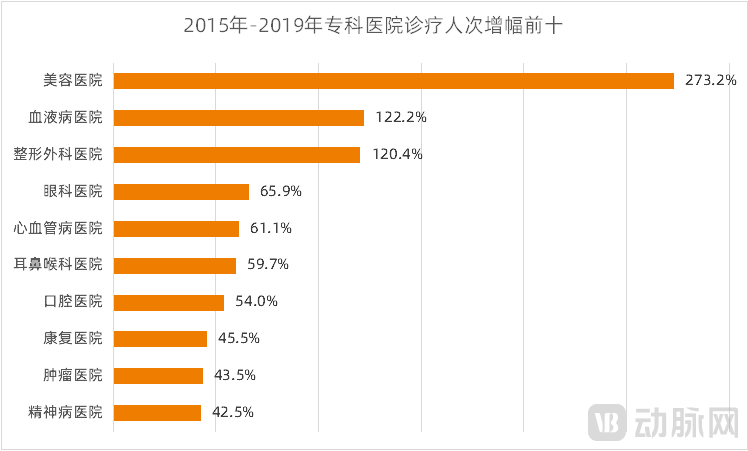

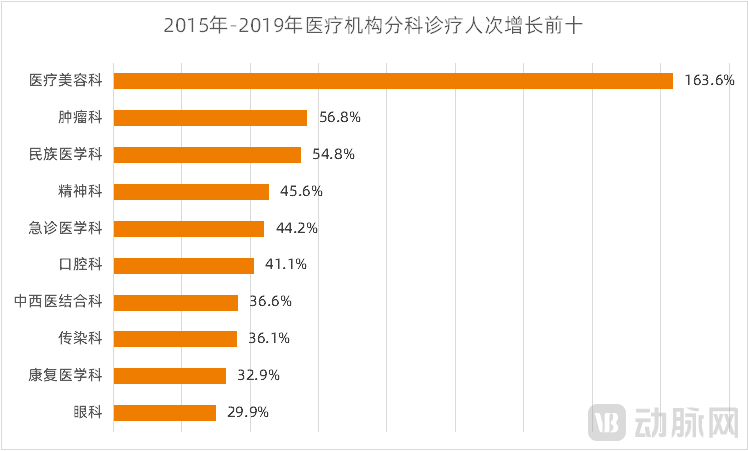

Data shows that oncology, rehabilitation, and psychiatry rank among the top ten specialties in terms of growth in outpatient visits, both for specialized hospitals and across all medical institutions by department. Although the volume of medical aesthetic services has also seen significant growth, its development logic differs substantially from that of disease-focused specialties; therefore, it is not covered in this article.

Growth in the Number of Specialist Medical Service Visits in 2019 Compared with 2015. Data Source: China Health and Health Statistical Yearbook; Chart compiled by VCBeat.

The above data largely represent the specialty fields with the fastest-growing patient demand in recent years. However, beyond demand, factors influencing industry development also include policy, technology, and payers. Taking these into account, which specialty fields are poised to gain further prominence? VCBeat offers a forward-looking analysis based on multi-source data and insights from investment institutions.

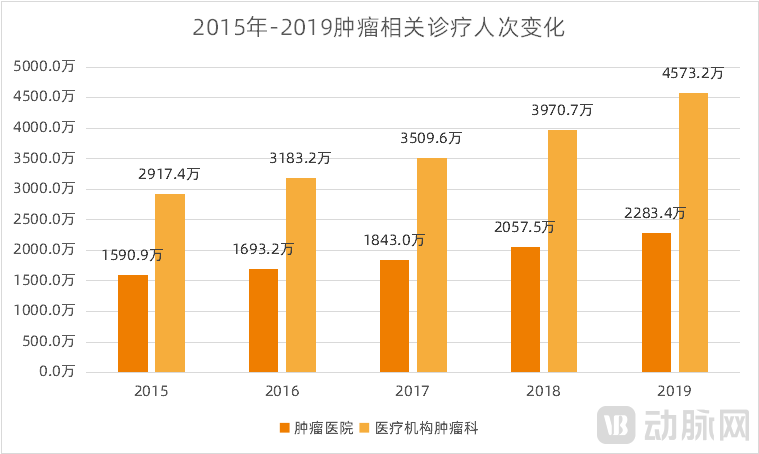

The analysis of the prevalence of malignant tumors in China, released by the National Cancer Center in 2019, shows that over the past decade or more, the incidence rate of malignant tumors has maintained an annual increase of approximately 3.9%, and the mortality rate has maintained an annual increase of 2.5%. The burden of cancer continues to rise, presenting a severe situation for prevention and control.

The analysis further indicates that the current increase in cancer burden is primarily driven by population aging. In terms of age distribution, the incidence of malignant tumors rises with advancing age. The incidence rate remains low among young people under 40 years old, begins to rise rapidly after age 40, and is predominantly concentrated in individuals aged 60 and above, peaking in the 80-year-old age group.

Changes in the Number of Oncology Visits and Treatments, 2015–2019. Data source: China Health Statistics Yearbook; chart compiled by VCBeat.

According to the *2021 China Health and Health Statistical Yearbook*, there were a total of 150 oncology hospitals in China in 2020, including 78 public and 72 non-public hospitals.

“Oncology diagnosis and treatment is a capital-, talent-, and technology-intensive industry with high barriers to entry,” said Jiang Xiaodong, Managing Partner at Changling Capital. He noted that outstanding private hospitals can establish a virtuous cycle among these three elements and foster a relationship with public hospitals that involves both competition and collaboration. Technological and model innovations—such as precision medicine, data-driven approaches, and robotic surgery—are gradually reducing the reliance of diagnostic and treatment protocols on expert experience while enhancing standardization. This trend presents new development opportunities for the private healthcare sector.

Amid the persistent rise in the incidence and prevalence of malignant tumors, oncology treatment resources are generally insufficient in total volume and unevenly distributed, with medical resources predominantly concentrated in first- and second-tier cities and large Grade 3A hospitals. Consequently, market opportunities in the field of oncology treatment fall into two models: one focuses on specific segments of the cancer care continuum to promote a more balanced distribution of resources; the other involves comprehensive cancer hospitals that integrate the entire diagnostic and therapeutic process, thereby serving as an overall supplement to existing medical resources.

For example, Hygeia and Yingkang Life have adopted the first model, establishing oncology hospitals with radiotherapy as the entry point. Specifically, Hygeia has focused its expansion in third-tier cities to address the scarcity of oncology treatment resources in these areas, thereby providing complementary services.

“Radiotherapy equipment penetration in China is relatively low and unevenly distributed. While availability is adequate in first-tier cities, it remains scarce in lower-tier markets, presenting a significant market opportunity,” said Miao Yiqing, Vice President of Investment at STOA Capital. In recent years, institutions primarily focused on chemotherapy have also emerged in first-tier cities. These entities operate through collaborations between private hospitals and public hospitals, such as medical consortiums, implementing chemotherapy regimens developed by public hospitals. This model helps public hospitals improve bed turnover rates while generating revenue for the private partners, representing another market opportunity. “However, we are more keen to see improvements in oncology treatment outcomes driven by the optimization of the entire diagnosis and treatment system and care models.”

According to data from the National Cancer Center, the current 5-year relative survival rate for malignant tumors in China is approximately 40.5%, representing an overall increase of about 10 percentage points compared to a decade ago. However, a significant gap remains between China and developed countries. This disparity is primarily attributed to differences in cancer spectra: China has a high incidence of digestive system tumors with poorer prognoses, such as liver, gastric, and esophageal cancers, whereas developed countries in Europe and America predominantly see higher rates of tumors with more favorable outcomes, such as thyroid, breast, and prostate cancers.

However, the 5-year survival rates for cancers with a relatively favorable prognosis in China, such as breast cancer (82.0%), thyroid cancer (84.3%), and prostate cancer (66.4%), still lag behind those in developed countries like the United States (90.9%, 98%, and 99.5%, respectively). This disparity is primarily attributed to the low proportion of cases diagnosed at an early stage, low rates of early diagnosis, and non-standardized clinical management of advanced-stage cases. Therefore, China should make concerted efforts in two key areas: expanding the coverage of screening, early diagnosis, and early treatment for relevant cancers, and promoting the standardized and homogeneous application of clinical cancer diagnosis and treatment protocols, so as to reduce mortality from malignant tumors.

It is evident that opportunities in the oncology sector extend beyond niche therapeutic interventions to encompass comprehensive, end-to-end diagnosis and treatment pathways, beginning with early screening and diagnosis. Previously, Guizhou Cancer Hospital under Sinopharm Holding (Xinbang Pharmaceutical) and Hainan Cancer Hospital under Chengmei Medical had already established themselves as integrated oncology care institutions. Beijing Meizhong Airui Cancer Hospital, which commenced operations in 2021, not only provides full-process diagnostic and therapeutic services but also delivers more systematic patient care through a Multidisciplinary Team (MDT) model.

Wang Bin, Managing Director of China Renaissance Capital, stated that oncology diagnosis and treatment involve multiple disciplines, including surgery, internal medicine, cardiology, pulmonology, gastroenterology, as well as pathology, clinical laboratory science, and radiology. “Establishing an oncology hospital requires not only strong capabilities in these relevant specialties but also leadership across all stages of cancer care—such as staffing with top-tier specialists and equipping the facility with the most advanced medical technologies, equipment, and therapeutic drugs. This ‘specialty-focused, general-support’ model is bound to attract significant investor interest.”

Wang Bin also believes that although public hospitals currently dominate cancer diagnosis and treatment, in the long run, as cancer becomes more like a chronic disease, more cancer patients can extend their lives through radiotherapy, chemotherapy, innovative drugs, etc., and private healthcare will definitely have greater room for development.

“Oncology is increasingly driven by technological advancements, and the emergence of new technologies may disrupt traditional healthcare service models.” A representative from BlueRun Ventures noted that new technologies facilitating the management of cancer as a chronic disease also warrant attention.

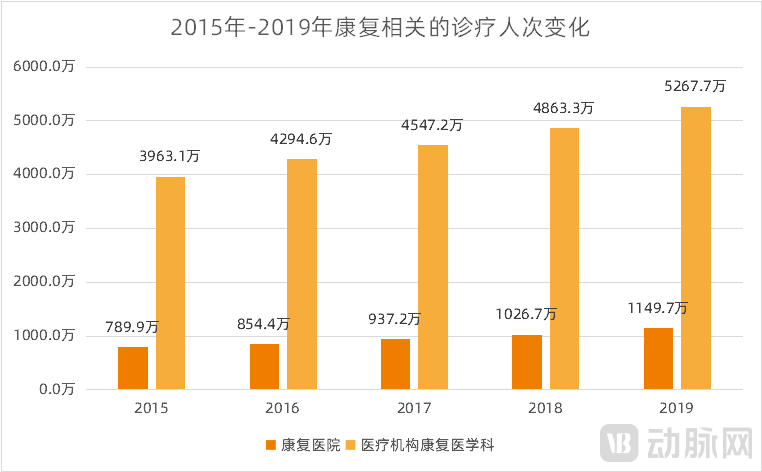

The field of rehabilitation covers multiple population groups. In addition to overlapping with the health and wellness sector (such as the elderly), it also includes individuals with disabilities, those with sports-related injuries, post-surgical patients, and postpartum women. Overall, there is significant market potential. In recent years, the volume of diagnoses and treatments in rehabilitation hospitals and rehabilitation departments has risen rapidly.

Changes in the Number of Rehabilitation Visits, 2015–2019. Data source: China Health and Family Planning Statistical Yearbook; chart compiled by VCBeat.

Jiang Xiaodong believes that rehabilitation, much like the field of mental health and psychology, is a blue-ocean market with significantly unmet demand. “Higher-quality rehabilitation following disease or surgery will directly enhance patient benefits, including improved quality of life, reduced complications, and cost savings throughout the entire treatment process.”

However, the penetration rate of rehabilitation medicine remains low across various subpopulations.

In June 2021, the National Health Commission and seven other departments jointly issued the “Opinions on Accelerating the Development of Rehabilitation Medical Services,” proposing to actively promote the development of subspecialties in rehabilitation medicine—including neurological, orthopedic, cardiopulmonary, oncological, pediatric, geriatric, pain, critical care, traditional Chinese medicine (TCM), and psychological rehabilitation—based on the disease characteristics and urgent rehabilitation service needs of different population groups. These efforts aim to provide refined services in rehabilitation assessment, treatment, guidance, and follow-up within each subspecialty.

The rehabilitation subfields prioritized for key development above, to a certain extent, reflect the current areas of weakness.

Miu Yiqing believes that pain management departments independently established within hospitals in recent years, as well as pediatric speech rehabilitation and autism care institutions such as Dongfang Qiyin, all fall under the broad category of “comprehensive rehabilitation.” “In the past, the demand across various branches of the rehabilitation sector was not fully tapped, and diagnostic and therapeutic technologies had not yet reached a level sufficient to support a viable market. Currently, with emerging demand and technological advancements, the convergence of several key subfields has created a substantially larger market size.”

In August 2021, the "Pilot Plan for Deepening the Reform of Medical Service Prices," issued by eight departments including the National Healthcare Security Administration (NHSA) and the National Health Commission (NHC), proposed that policy incentives should be provided for weak disciplines with historically low prices and insufficient medical supply, such as nursing. In January 2021, the NHSA's "Interim Measures for the Designated Management of Medical Insurance in Medical Institutions" added "rehabilitation hospitals" to the scope of "medical institutions eligible to apply for designated medical insurance status." Recently, certain cities in Anhui Province have adjusted the prices of selected medical services. Notably, hyperbaric oxygen therapy and single-patient chamber therapy—key treatment modalities in rehabilitation, particularly in critical care rehabilitation—have undergone tiered price increases based on the classification of medical institutions (Levels I, II, and III), with an overall price increase of approximately 50–80%.

In the future, medical service items that reflect the technical expertise and labor value of healthcare professionals will become a key focus of support in medical service pricing, with rehabilitation medicine featuring a substantial number of such items. The preferential orientation of medical service pricing and health insurance payment policies has also created opportunities for the rehabilitation sector.

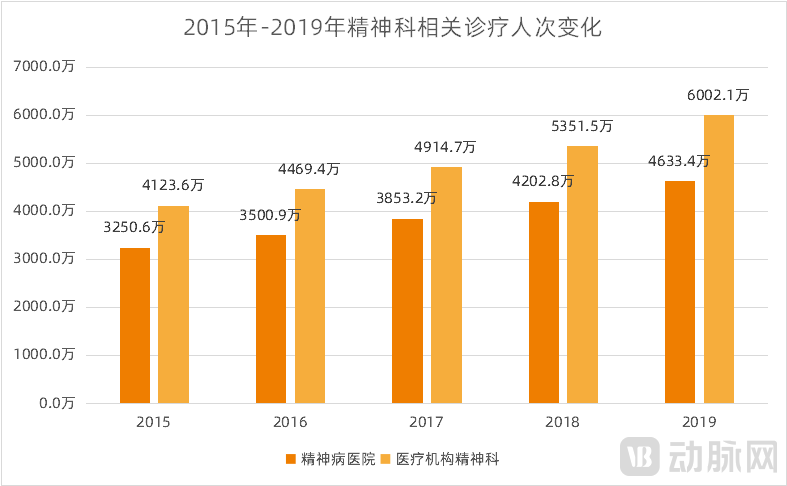

According to authoritative statistical data, 16%–17% of the population in China suffers from various mental and psychological disorders. The disease burden attributable to mental and psychological conditions accounts for 13% of the total burden of non-communicable diseases, making it a major public health, social, and livelihood issue.

Wang Bin noted that in the past, social capital represented by Kangning Hospital entered the mental health field, serving as a supplement to resources; today, platforms such as Haoxinqing, Zhaoyang Doctor, and Xiaodong Health have leveraged information technology to enhance the efficiency of doctor-patient connectivity through their technological capabilities.

Changes in the Number of Psychiatric Outpatient Visits from 2015 to 2019. Data Source: China Health Statistics Yearbook; Chart compiled by VCBeat

However, experiencing mental and psychological distress is not equivalent to having a “disorder.” According to statistics, the prevalence of major depressive disorder in the field of mental health is 2.1%, and the prevalence of anxiety disorders is 4.98%. Although the prevalence rates of these two conditions are not low, they still differ significantly from the aforementioned figure of 16%–17%.

According to statistics, psychiatric hospitals and psychiatric departments in medical institutions collectively handle tens of millions of patient visits annually, a figure that continues to grow year by year. However, some individuals with psychological issues do not seek hospital care, indicating varying degrees of severity in mental and psychological problems and, consequently, a diversity of corresponding intervention strategies.

In Jiang Xiaodong’s view, there is a substantial unmet need in the field of mental and psychological health. Theoretically, this gap indeed requires significant supplementation by private healthcare providers. “However, what this sector lacks most is high-quality services and patient management, rather than merely ‘selling medications.’ Users with mental and psychological concerns require long-term, continuous, and comprehensive management. For individuals who do not yet meet the diagnostic criteria for mental disorders, greater emphasis should be placed on preventive interventions. We are optimistic about platforms offering such front-end services. We also see promise in full-course patient management and digital therapeutics. Only by integrating these two approaches and serving patients based on quantifiable outcomes can we ensure that patients truly benefit.”

Miao Yiqing noted that the population with mental and psychological issues is substantial, with a large segment requiring highly accessible services, such as science-based prevention education and psychological exercises. Institutions of this kind can not only deliver more universally applicable services but also minimize exposure to medical risks.

“As material living standards become increasingly affluent, choices multiply and human desires expand; however, the ability to resist various urges remains insufficient, leading to greater awareness of psychological suffering. Therefore, we believe that the mental health sector will inevitably become a high-growth area,” said a representative from BlueRun Ventures. Currently, the insufficient supply of qualified psychotherapists under professional supervision in China is a major constraint on industry development. Two types of solutions warrant attention: technology-assisted diagnosis and treatment, and self-management interventions.

The reality is that public awareness of common mental disorders and psychological-behavioral issues remains insufficient. There is a widespread lack of knowledge about prevention and treatment, as well as limited initiative in seeking help or medical care, while stigma persists among some patients and their families. Consequently, opportunities in the field of mental health lie in both improving the quality and efficiency of diagnosis and treatment, and implementing preventive interventions. Regardless of the stage focused on, technology-driven solutions, particularly digitalization, serve as a critical approach and will become a key driver in this domain.

In addition to the three specialty services mentioned above that have already seen substantial data growth, there are other areas showing market potential due to various factors.

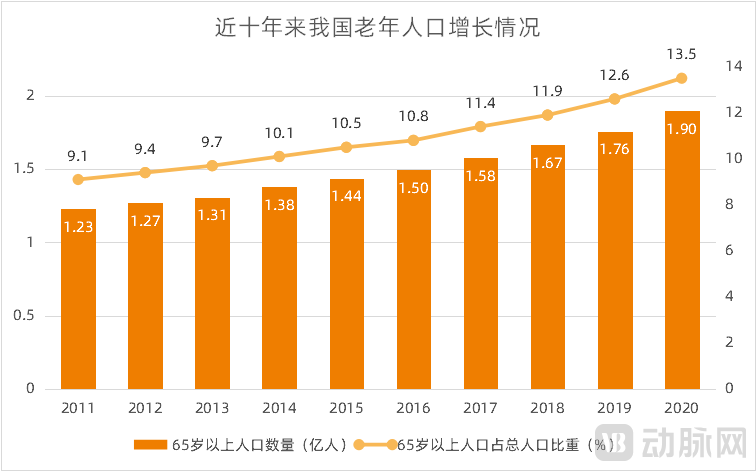

For example, another niche sector closely tied to demographic shifts is health and elderly care. According to the Seventh National Population Census, China’s population aged 60 and above reached 264 million in 2020, accounting for 18.7% of the total population, with those aged 65 and above comprising 13.5%.

Trend of Population Aging in China; Data Source: National Bureau of Statistics; Chart Compiled by VCBeat

To meet the substantial demand for elderly care, the state has repeatedly introduced policies to encourage non-governmental entities to establish health and elderly care institutions. In June 2021, the National Development and Reform Commission, the Ministry of Civil Affairs, and the National Health Commission jointly issued the Implementation Plan for Actively Responding to Population Aging and Childcare Services Construction during the 14th Five-Year Plan Period, which stated that support should be provided for non-governmental entities to build specialized, large-scale elderly care institutions with prominent capabilities in integrating medical and elderly care services; improve standards and norms for long-term care services; strengthen the training and reserve of professional nursing personnel; enhance the level of informatized and intelligent management services; promote the application of rehabilitation assistive devices; and reinforce long-term care services for elderly individuals with disabilities and dementia.

In recent years, stakeholders such as real estate developers and insurance companies have explored the health and elderly care sector, primarily by establishing large-scale elderly care institutions.

“Over the next decade, more social capital will flow into the sector, with greater funding availability in the health and elderly care space, a larger number of market participants, and products and services that better align with market demand,” Wang Bin noted. “Ninety percent of older adults choose to age at home or within their communities, where a significant volume of recurring, consumption-based services also takes place. The capital markets have begun to focus on chain institutions in the health and elderly care sector and ‘Internet + nursing’ platforms, strategically positioning themselves early in leading enterprises.”

As the needs of elderly individuals vary across different age stages, the services provided by health and wellness care institutions must also differ. For seniors with limited mobility who rely on assistive devices but remain in relatively good health, the focus is on assisted living services, which are primarily domestic care-oriented. For seniors who depend on others for daily care and suffer from severe disabilities, the focus is on skilled nursing services, whereby medical professionals deliver specialized healthcare and wellness support.

Wang Bin believes that in the future, companies with outstanding capabilities in assisted living and nursing care, highly standardized services, high service quality, and strong risk control capabilities will surely stand out with the support of capital.

A robust health and wellness ecosystem also requires a well-developed payment framework. Due to the accelerating trend of population aging, China’s basic old-age insurance system currently faces two major challenges: limited benefit levels under the basic old-age insurance scheme for urban and rural residents, and substantial fiscal pressure. Previously, large insurance companies had already explored various initiatives under the “insurance + health and wellness” model, such as Taikang’s retirement communities integrated with its insurance products. Currently, chain health and wellness providers are also integrating with long-term care insurance (LTCI). For instance, E-DeCare, under New Frontier Group, has launched home-based care, nursing services, hospital companionship, and LTCI-covered services. Supported by LTCI, beneficiaries need only cover a small portion of the costs for 42 types of daily living assistance and clinical nursing services.

Therefore, in the development of the health and wellness sector, establishing a diversified payment system is also an indispensable component.

While demand in most other medical specialties is relatively low-frequency, the maternal and child health sector (specifically referring to obstetrics and pediatrics, excluding gynecology) is characterized by relatively high-frequency demand. Consequently, substantial private capital has flowed into maternity hospitals, children’s hospitals, and pediatric clinics.

A representative from BlueRun Ventures noted that while the maternal and child health sector enjoyed high popularity in previous years, interest has waned over the past two years. Although many institutions achieved leapfrog development after securing capital injections, certain issues have come to light, such as an insufficient supply of high-quality services and overall profit margins that lag behind those of specialties like ophthalmology and dentistry. In the maternal and child health sector, service quality is a critical factor; enhancing it requires sustained commitment to the industry and meticulous attention to detail.

Miao Yiqing noted that obstetrics and gynecology was an early sector to undergo marketization, with competition in first-tier cities already reaching a fever pitch. Pediatrics attracted significant capital interest in recent years, giving rise to numerous chain clinics; however, many pediatric clinics are currently seeking transformation due to several development bottlenecks: difficulty in recruiting and retaining pediatricians, intense competition despite strong consumer payment capacity in first-tier cities, low revenue ceilings for individual outlets, and insufficient management capabilities and market space to support large-scale expansion or unlimited outlet deployment. “Children’s specialized hospitals or obstetrics and gynecology hospitals, backed by the scale of a full-fledged hospital, are in a relatively better position. In the future, this sector is likely to see more mergers and acquisitions, particularly through complementary integration of hospital and clinic resources within the same city, forming higher-quality entities that can accelerate their entry into the secondary market.”

In October 2021, Jinxin Fertility issued an announcement regarding the acquisition of Sichuan Jinxin Women and Children’s Hospital. This marks another major acquisition by Jinxin Fertility, following its purchase of Yunnan Jiuzhou Hospital and Hewanjia Hospital in June of the same year, and represents a significant strategic move to enhance its full-lifecycle service offerings.

Wang Bin stated that the women’s and children’s healthcare sector can encompass a series of services spanning preconception, pregnancy, and postpartum periods. “With the national implementation of the three-child policy, the women’s and children’s health sector is showing signs of recovery. However, it is essential to establish a full-cycle service ecosystem—namely, building an integrated service system ranging from assisted reproductive technologies and maternity care to pediatric diagnosis and treatment—rather than merely operating standalone hospitals. Currently, industry consolidation is already exhibiting these trends. In the future, capital will favor medical groups that have established such comprehensive service ecosystems.”

It is evident that, under the combined influence of birth rates, fertility policies, and industry-specific business characteristics, a “new maternal and child health” sector—characterized by a full-process service ecosystem—is taking shape, creating new opportunities for innovation and growth.

After decades of accumulation, brain science is entering a period of explosive application.

In the 14th Five-Year Plan, artificial intelligence and brain science were designated as national strategic scientific and technological forces. The recent rollout of a series of supporting policies signals that the next 5–10 years will witness the rapid expansion of brain science from basic research to clinical applications, making the present a critical juncture for its development.

In 2021, the “China Brain” Project entered its implementation phase. The Ministry of Science and Technology officially released the “Guidelines for Project Applications in 2021 under the Major Project ‘Science and Technology Innovation 2030—Brain Science and Brain-Inspired Research,’” which established a five-year cycle for the major project on brain science and brain-inspired research. In 2021, the project focused on 59 research directions across five areas: elucidation of the principles of brain cognition; pathogenesis and intervention technologies for major brain disorders associated with cognitive impairment; brain-inspired computing and brain-machine intelligence technologies and applications; brain and intellectual development in children and adolescents; and technical platform construction. The estimated national funding allocated for these initiatives amounted to RMB 3.148 billion.

2020–2021 Financing Events in the Field of Functional Neurosurgery. Data source: Artery Orange; graphic by VCBeat.

Brain science focuses on upstream research, while closely linked to it are downstream brain health-related services.

Wang Bin noted that brain science and brain health have been a highly watched sector in the broader healthcare industry since 2021. Brain-computer interface (BCI) technology has made certain progress abroad, while China’s capital markets have also begun to focus on domestic tech companies involved in brain science and institutions providing medical services in the field of brain health.

In September 2021, Sanbo Brain Hospital’s IPO application was approved by the Listing Committee of the ChiNext board, with its technical prowess emerging as its core competitive advantage. Additionally, Donglei Brain Hospital, founded by a physician group, is also experiencing rapid growth. These institutions have set a benchmark for private healthcare providers entering the brain health sector.

As life expectancy continues to rise, the incidence of various neurological and chronic diseases is also increasing. Against this backdrop, public demand for high-quality brain health services is steadily growing. Currently, the government is providing financial support for brain science research, while social capital and market entities are actively investing in brain science technologies. In the future, as research findings are produced, translated into applications, and integrated into service delivery, the field of brain health will seize new development opportunities.

Certainly, in addition to the aforementioned specialties, there are also areas such as day surgery centers that enhance the efficiency of the healthcare service system, and "small but beautiful" fields like otolaryngology, which also hold significant potential.

In Miao Yiqing’s view, the development of private healthcare has entered a new phase, with consumers becoming more mature and no longer relying solely on payment considerations when making choices. “It is no longer the case that patients automatically choose public hospitals for services covered by medical insurance and turn to other providers only for non-reimbursable care. An increasing number of factors will influence consumer decision-making.”

Nevertheless, the supply side of healthcare services still adheres to fundamental underlying principles. For a considerable period, the top-level design of China’s healthcare system has been guided by the dual objectives of enhancing quality and improving accessibility. Within the public sector, these goals are pursued through comprehensive reforms of public hospitals, initiatives promoting high-quality development of public hospitals, and the establishment of national-level regional medical centers. The private healthcare sector, across all specialties, likewise follows this strategic direction.

During the interview, Jiang Xiaodong repeatedly emphasized “patient benefit,” which he regards as the primary criterion for assessing the value of medical services.

Jiang Xiaodong stated that China’s healthcare service system is undergoing profound changes along two dimensions: first, demonstrable patient benefits, particularly those verifiable through data; and second, the return on investment. Combined, these two aspects refer to how many resources and funds healthcare institutions invest to achieve quantifiable, evidence-based patient benefits. “We believe this will be the main development trajectory for innovative healthcare services in China for a considerable period. Currently, our healthcare service system still suffers from significant inefficiencies. The greater opportunity for professionals in the healthcare industry lies in improving efficiency—specifically, how to deliver more proven patient benefits within limited resources.”

Furthermore, a representative from BlueRun Ventures stated that investors also focus on the payer perspective—specifically, whether entrepreneurs can take into account the needs of various payers when structuring their business models, designing product formats, and exploring service models, and whether they can address some of these payers’ needs when delivering their services or products.

Driven by demand, empowered by technology, fueled by capital, and supported by policy, specialized medical institutions that better deliver patient benefits, empower payers, and enhance the quality and efficiency of healthcare delivery are poised to generate more outstanding projects and even enter the secondary market in the near future.