RMB 47 Billion, 136 Deals: Trends in China's Healthcare M&A Landscape – 2021 Annual Review

Big fish eat small fish, and small fish eat shrimp; the biological world has its own specific ecological chain.

Similarly, in the healthcare sector, mergers and acquisitions have become a key driver of market consolidation and industry ecosystem evolution.

According to Deloitte’s “White Paper on M&A Market in China’s Life Sciences and Healthcare Industry 2021,” both cross-border M&A transactions and domestic M&A activities increased in 2020. The “2021 iCapital China Health Industry White Paper – M&A Section” also noted that, with the emergence of new industry regulations and policy evolution—such as adjustments to China’s medical insurance payment structure and reimbursement list, the consistency evaluation of generic drugs, and the normalization of centralized procurement—the need for companies in China’s health industry to further diversify their product portfolios and extend their industrial chains through M&A and integration has become increasingly prominent. Wu You, Managing Director of iCapital and Head of the Health Industry M&A Group, stated that enterprises across all major segments of the broader healthcare sector—including pharmaceuticals, medical devices, healthcare services, and digital health—have clear rationales for growth through M&A and strong incentives for mergers and restructurings.

So, what are the characteristics of the “big fish eating small fish” phenomenon in each sub-sector? How will M&A transactions evolve in the future? Focusing on these active sectors, VCBeat has compiled 136 M&A deals involving domestic companies and Chinese enterprises acquiring overseas targets in 2021, with a total disclosed transaction value of RMB 47 billion, to analyze and interpret the features of market consolidation and trends in ecosystem evolution.

Due to differences in growth logic, business synergy models, and policy orientation, M&A transactions in pharmaceuticals, medical devices, healthcare services, and digital health exhibit significant variations (this section includes statistics where both the targets and acquirers are domestic enterprises).

Pharmaceuticals: Mergers or Collaborations Between Innovative and Traditional Pharmaceutical Companies Are the Prevailing Trend

Mergers and acquisitions in the pharmaceutical sector are primarily driven by several key rationales: at the strategic level, they involve integration between traditional pharmaceutical companies and innovative drug developers; at the operational level, they include complementary product portfolio integration or capacity expansion, as well as the combination of R&D, manufacturing, and sales across the business value chain.

According to incomplete statistics, as of November 29, 2021, a total of 52 mergers and acquisitions (M&A) transactions occurred in China’s pharmaceutical sector, with the total transaction amount reaching RMB 21.9 billion (excluding deals with undisclosed values). Many of these transactions reflected the aforementioned logic.

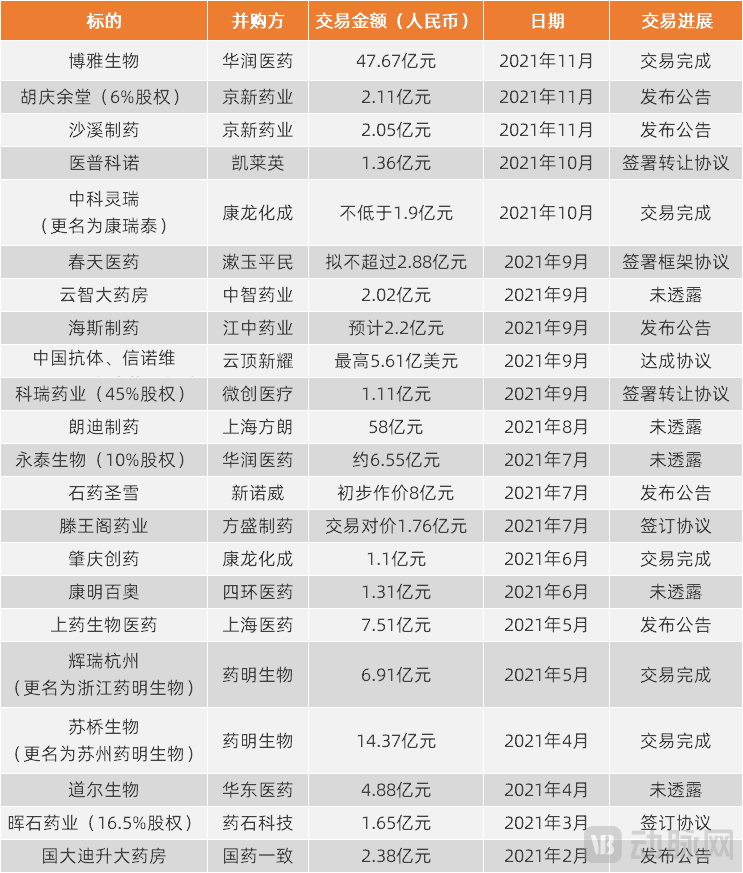

M&A Transactions in the Pharmaceutical Sector with Deal Values Exceeding RMB 100 Million Since 2021; Data Sources: Arterial Orange, Qichacha, and Listed Company Announcements; Chart Compiled by VCBeat

For instance, transactions such as Huadong Medicine’s acquisition of Daol Biologics and Sihuan Pharmaceutical’s acquisition of Kangming Bio all represent the integration of traditional pharmaceuticals with innovative drugs, reflecting the enrichment and strategic combination of product pipelines. Daol Biologics focuses on oncology, metabolism, ophthalmology, and other therapeutic areas, having developed multiple multi-specific fusion protein drugs based on multi-domain structures as well as innovative single-domain antibody drugs. Upon completion of the acquisition, Daol Biologics will become a key biopharmaceutical R&D platform for Huadong Medicine, supporting its innovative transformation. Kangming Bio possesses two major antibody technology platforms: “Mab Edit” (antibody editing) and “Mebs-Ig” (antibody-edited bispecific antibodies). Following the transaction, Kangming Bio will contribute a biopharmaceutical R&D pipeline to Sihuan Pharmaceutical’s innovative research efforts, while also complementing Sihuan’s existing small-molecule innovative drug R&D platform, thereby forming a combined portfolio of small-molecule and large-molecule products. After being acquired, such innovative pharmaceutical companies can leverage their parent companies’ mature manufacturing and commercialization capabilities to achieve a faster return on R&D investment.

In terms of CXO M&A, WuXi Biologics (a CDMO) invested RMB 1.437 billion and RMB 691 million to acquire Suqiao Bio and Pfizer Hangzhou, respectively. Following the acquisitions, WuXi Biologics’ R&D capabilities will be further strengthened, while its urgently needed bulk drug substance and drug product manufacturing capacity for biologics will see a significant increase.

“The rise of innovative drugs and the recent downward adjustment in valuations have accelerated the pace of M&A and consolidation in the pharmaceutical sector.” Wu You believes that their future growth paths will be as follows: either being acquired or acquiring Contract Sales Organizations (CSOs) to bolster marketing and sales departments, thereby becoming comprehensive pharmaceutical companies like Pfizer and AstraZeneca, which possess both strong R&D capabilities and excellent marketing and sales prowess; or becoming companies focused solely on R&D, without building in-house marketing and sales teams, by licensing out the rights to mature products to pharmaceutical companies with established sales and marketing capabilities. Both paths present opportunities for M&A and consolidation. The first scenario typically occurs between innovative pharmaceutical companies and traditional pharmaceutical companies, particularly those with mature marketing and sales teams. The second involves innovative pharmaceutical companies further expanding their R&D capabilities, diversifying their product portfolios, and even considering mergers with medical device companies in the same therapeutic area to share sales teams and distribution channels.

Moreover, the overall process for innovative drugs—from R&D and clinical trials to process development and manufacturing, and finally to commercialization—is lengthy. There is often overlap across various aspects, ranging from customer bases and procurement to talent training, which makes it easy to generate synergies post-merger. Consequently, consolidation among CXO companies is particularly common in the industry.

“The consolidated entity will see enhancements in both scale and recognition in the capital markets, thereby exerting significant pressure on industry competitors. If a target company is acquired by a competitor, the enterprise may find itself at a disadvantage. Such mergers and acquisitions often carry substantial strategic significance.” Wu You cited as an example the merger between Biostar and Sundia in 2020, which held prominent strategic value. Prior to the merger, Biostar and Sundia Pharma were preclinical CRO companies with respective areas of expertise. The merged entity became a CRDMO, providing comprehensive services covering drug discovery, research and development, and manufacturing for active pharmaceutical ingredients (APIs) and finished drugs, thus offering more competitive solutions.

Medical Devices: Accelerating the Development of Platform Companies Through M&A

For medical device companies, supplementing product lines or technologies and expanding revenue scale are two key drivers of mergers and acquisitions. From the perspective of product characteristics, the medical device industry is characterized by fragmentation and discrete manufacturing, with significant segmentation across various sub-sectors. Product technologies are undergoing rapid iteration, and new technologies often have a disruptive impact on older ones. From a market standpoint, growth ceilings in specific medical device sub-sectors are clearly defined; if companies fail to further expand their market share, intense external competition will quickly erode their existing share.

M&A Transactions in the Medical Device Sector with Deal Values Exceeding RMB 100 Million Since 2021. Data sources: Artery Orange, Qichacha, and announcements from listed companies; chart compiled by VCBeat.

Since 2021, there have been 43 mergers and acquisitions in China's medical device sector, with a total transaction value of RMB 6.2 billion (excluding deals with undisclosed amounts).

In October 2021, Venus Medtech entered into an agreement with Nuocheng Medical to acquire 100% of the equity interests and corresponding rights in Nuocheng Medical for a maximum consideration of RMB 493 million. The completion of the acquisition marked another significant milestone in Venus Medtech’s transformation into a comprehensive platform for the treatment of structural heart disease.

In September 2021, Yuwell Medical acquired Kailite Medical for RMB 366 million. Kailite Medical’s product portfolio includes continuous glucose monitoring (CGM) systems, blood gas and electrolyte analyzers, and other point-of-care testing (POCT) products. Diabetes care and POCT are among the three key strategic sectors for Yuwell Medical’s future development. This acquisition will complete Yuwell Medical’s comprehensive business layout in the diabetes care sector and drive overall corporate performance growth.

Therefore, both platform companies within specific disease areas and comprehensive platform companies are strengthening their capabilities through acquisitions.

“When a company has only a single product, achieving sales of tens or even hundreds of millions of yuan after obtaining product registration certification is not difficult. However, achieving further multiplicative growth becomes challenging, and this scale is insufficient to support an initial public offering (IPO),” said Li Gang, Partner and Co-Head of the Healthcare Group at China Renaissance Capital. This situation compels companies to transform into platform enterprises through acquisitions. Multinational corporations such as Medtronic, Danaher, and Johnson & Johnson have also become platform-type companies with dozens or even hundreds of product lines by continuously acquiring businesses and expanding their product portfolios.

Wu You also cited rehabilitation equipment as an example, noting that while the market for such devices is valued at tens of billions of yuan, very few companies hold a 5% market share. “Rehabilitation equipment spans numerous clinical departments, including orthopedics, neurology, audiology, speech therapy, and other neurological specialties, resulting in a diverse product portfolio. Building a dominant player in this sector requires substantial capital and effort, presenting ample opportunities for mergers, acquisitions, and consolidation.”

Healthcare Services: M&A Drives Revenue Growth and Cost Reduction

Mergers and acquisitions (M&A) in the healthcare services sector are primarily driven by horizontal expansion and vertical integration. Horizontal expansion involves healthcare service groups acquiring physical medical institutions such as hospitals and clinics, while vertical integration entails online entities acquiring offline counterparts or vice versa. Another key driver for M&A among healthcare service groups is the acquisition of qualifications required for specialized medical services.

“Similar to the medical device sector, platform-based companies in the healthcare services industry also pursue acquisitions to support their growth. Hospital management groups, building on an existing portfolio of general and specialized hospitals, further acquire healthcare service institutions that feature distinctive specialties, possess high barriers to entry in terms of medical technology and expertise, and demonstrate strong profitability,” said Li Gang.

M&A Deals in the Healthcare Services Sector with Transaction Values Exceeding RMB 100 Million Since 2021. Data sources: Artery Orange, Qichacha, and announcements from listed companies. Chart compiled by VCBeat.

Since 2021, a total of 23 mergers and acquisitions (M&A) transactions have occurred in the healthcare services sector, with a cumulative value of RMB 9.1 billion (excluding deals with undisclosed amounts). Jinxin Fertility and Hygeia Healthcare demonstrated high M&A activity and accounted for the two largest single transactions by value.

In October 2021, Jinxin Fertility issued an announcement stating its intention to acquire three target assets, including Sichuan Jinxin Women and Children’s Hospital, for RMB 3 billion. The announcement revealed that Sichuan Jinxin Women and Children’s Hospital is a Grade 3A hospital with an average annual outpatient volume of 600,000 visits. In the first half of 2021, the hospital reported revenue of RMB 225 million and net profit of RMB 47 million, with 549 deliveries resulting from Jinxin Fertility’s IVF treatments. Currently, Sichuan Jinxin Women and Children’s Hospital has 303 beds in use out of a total capacity of 602, indicating room for further growth.

In April 2021, Hygeia Healthcare announced the acquisition of a 98% equity stake in Suzhou Yongding Hospital. Suzhou Yongding Hospital is a Grade II general hospital that recorded 20,000 inpatient visits and 482,000 outpatient visits in 2020, with revenue of RMB 492 million and net profit of RMB 61 million. As the largest private hospital in the local area, it demonstrates strong profitability. Hygeia already operates Suzhou Canglang Hospital, which has a high patient volume in Suzhou. Following the completion of the acquisition, the two hospitals in Suzhou will achieve synergistic development. On May 26, Hygeia issued another announcement regarding the acquisition of Hezhou Guangji Hospital in Guangxi. Within two months, Hygeia’s stock price surged from HKD 61 at the time of the transaction announcement to HKD 101, representing an increase of up to 60%. It is expected that Suzhou Yongding Hospital will make a significant contribution to the revenue growth of Hygeia’s hospital business segment in the future.

Recently, Gushengtang, a chain of traditional Chinese medicine (TCM) outpatient clinics that has passed the hearing by the Hong Kong Stock Exchange, acquired 32 offline medical institutions for a total consideration of approximately RMB 645 million over the past few years. In 2020, Gushengtang also acquired the internet healthcare platforms Bailu TCM and Wanjia TCM to strengthen its “New TCM OMO” model, which integrates online and offline operations.

If healthcare service providers rely on traditional expansion through opening new stores or facilities, the payback period for individual units is long. In addition to capital expenditure on fixed assets, significant costs are also required for human resource development and management. In contrast, mergers and acquisitions (M&A) can rapidly achieve economies of scale, as well as boost revenue and profits. In the aforementioned M&A cases, besides expanding their service networks through acquisitions, healthcare service groups have also enhanced their own performance by leveraging the target companies’ strong and stable revenue or profitability. Gu Shengtang’s M&A strategy further reflects an approach integrating online and offline operations, maximizing synergies between these channels and reducing customer acquisition costs.

In addition, the fact that the targets of Jinxin Fertility’s two other acquisitions—Yunnan Jiuzhou Hospital and Kunming Hewanjia Maternity Hospital—both hold IVF licenses was also a key factor in Jinxin Fertility’s decision.

Digital Health: Companies Explore More Application Scenarios Through M&A

M&A activity in the digital health sector is generally less robust than in the three aforementioned fields, which is attributable to the industry’s nascent stage and the relatively smaller number of publicly listed companies.

M&A Deals in the Digital Health Sector in 2021; Data Sources: Artery Orange, Qichacha, and Public Announcements of Listed Companies; Chart Compiled by VCBeat

Alibaba Health’s acquisition of Xiaolu TCM was a major transaction in the digital healthcare sector in 2021. Prior to the acquisition, Alibaba Health had already established an integrated online-to-offline medical and health service system. By leveraging Xiaolu TCM’s strengths in internet-based traditional Chinese medicine (TCM), Alibaba Health was able to take the lead in providing users with internet healthcare services that integrate traditional Chinese and Western medicine, and even develop more innovative business models.

Mergers and acquisitions arising from the strategic expansion of internet giants into online healthcare, AI, and other sectors are a common occurrence in the digital health industry; previously, BATJ have all undertaken similar initiatives.

Furthermore, some acquirers are not internet giants, and the companies are still in their growth stage. For example, Deepwise Healthcare acquired Yitu Healthcare to enrich its product portfolio and share or expand its customer base. Yuanxin Technology acquired Yiku, rapidly increasing the number of registered physicians, thereby enhancing medical service capabilities, and providing an integrated medical platform and compliant digital marketing services.

“The industry has high expectations for digital health, believing that these companies will have a disruptive impact in the future, and therefore assigns them higher valuations. High valuations and strong fundraising capabilities drive these companies to pursue mergers and acquisitions as a means of identifying more application scenarios or data sources,” said Wu You.

It is worth noting that many digital health companies are either still exploring their business models or have yet to achieve large-scale commercialization of their products; therefore, both acquisition targets and acquirers may not yet be profitable.

In Li Gang’s view, in response to this situation, the dimensions of M&A and integration in digital health can be considered from three aspects:

First, large internet healthcare platforms are consolidating small and medium-sized companies in vertical niches.

Second, cross-sector integration—for example, traditional pharmaceutical distribution companies acquiring internet healthcare platforms—is a process that enhances efficiency. Even if the platform itself is not profitable, it holds significant value by helping traditional distributors improve operational efficiency. Furthermore, with the rise of digital therapeutics, traditional pharmaceutical companies may also acquire such firms to pursue cross-industry combinations.

Third, mergers and reorganizations among small and medium-sized innovative companies can facilitate complementary strengths and collective resilience, thereby establishing deeper moats or higher technical barriers.

The inherent characteristics of the aforementioned sectors are correlated with the level of M&A integration activity. Changes in the external environment also influence M&A activity, thereby reshaping the market landscape. Overall, there are five primary external factors.

The Globalization of Domestic Enterprises Is Accelerating, with More Industry Leaders Becoming Multinational Corporations

With China's economic development, R&D capabilities in the fields of innovative drugs and innovative medical devices have been steadily improving, and industry leaders are increasingly participating in the global market.

Wu You stated that there are four main reasons for the frequent overseas mergers and acquisitions in recent years: First, domestically developed technologies can no longer fully meet domestic market demands; second, the existing market landscape fails to support companies’ expansion along the upstream and downstream segments of the industrial chain, prompting some enterprises to acquire technology, production capacity, or distribution channels through overseas “buying sprees”; third, some Chinese companies have already acquired the capabilities to become multinational or even global corporations and need to expand their markets through M&A; fourth, in certain overseas countries with smaller market sizes, companies possessing strong technologies often have more reasonable valuations than their Chinese counterparts due to sluggish growth.

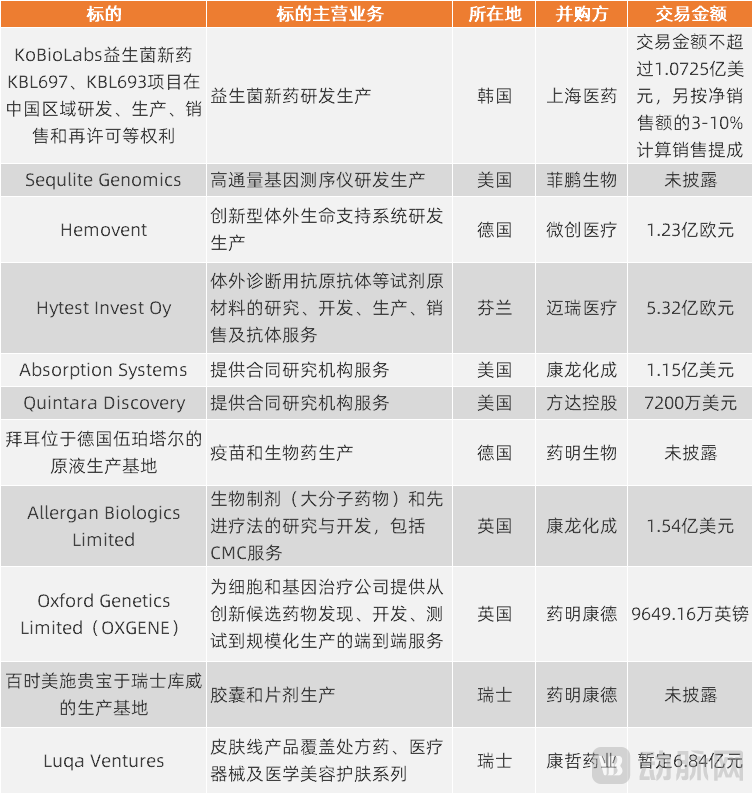

2021 Overseas M&A Projects by Chinese Enterprises. Data sources: Arterial Orange, Qichacha, and announcements from listed companies. Chart compiled by VCBeat.

In 2021, medical device companies such as Mindray and MicroPort, as well as innovative drug companies including Pharmaron, WuXi Biologics, and WuXi AppTec, continued to expand their overseas operations.

In September 2021, Mindray completed the acquisition of Finland’s Hytest Invest Oy for €532 million. Through this transaction, Mindray will strengthen its in-house R&D and manufacturing capabilities for core raw materials, increase the proportion of self-produced core materials, further drive technological breakthroughs and performance enhancements in its chemiluminescence products, and optimize the global layout of its upstream and downstream supply chain to ensure supply security. Since embarking on its global M&A journey in 2008, Mindray has acquired multiple overseas targets, such as U.S.-based ultrasound diagnostics company Zonare and Australian distributor Ulco in 2013, and the patient monitoring business of U.S.-based Datascope in 2008.

In March 2021, WuXi AppTec completed the acquisition of OXGENE, a UK-based gene therapy technology company. This acquisition will further expand the technical capabilities of WuXi AppTec’s cell and gene therapy platform, enabling the company to provide integrated, end-to-end development and manufacturing services for cell and gene therapy products.

“Leading enterprises in certain niche sectors within China are gradually evolving into multinational corporations, and even global giants. Companies such as Mindray and WuXi AppTec have already demonstrated this trend,” said Wu You. He believes that multiple drivers underpin this phenomenon, the most significant being China’s rapid economic development, large population, and substantial market demand. The rapid growth of these companies has attracted significant social capital; high growth leads to high valuations, which in turn deliver high returns to shareholders, creating a “positive feedback” loop. As the industry expands rapidly and capital accumulates quickly, dominant firms naturally engage in consolidation—“the big fish eating the small fish”—thereby swiftly meeting shareholder expectations for corporate growth through mergers and acquisitions.

Centralized Procurement of Drugs and Medical Consumables Drives Industry Transformation

The “4+7” drug centralized procurement program, launched at the end of 2018, was gradually expanded in scope until it covered the entire country. As of June 2021, five rounds of national centralized volume-based drug procurement had been conducted, covering 218 drugs, with the average price reduction for selected products reaching 54%. In 2020, centralized procurement was extended from drugs to high-value medical consumables. To date, two rounds of national centralized procurement for high-value medical consumables have been carried out, resulting in an average price reduction of 93% for selected coronary stents and 82% for selected artificial joints.

The “14th Five-Year Plan” for National Healthcare Security stipulates the regular and institutionalized implementation of national centralized volume-based procurement of pharmaceuticals, while continuously expanding the scope of national centralized volume-based procurement of high-value medical consumables. By 2025, each province shall have procured more than 500 varieties of pharmaceuticals through national and provincial centralized volume-based procurement, with high-value medical consumables covering more than five major categories.

Therefore, the industry impact of normalized centralized procurement on pharmaceuticals and medical devices will persist. The Joint Procurement Office for Pharmaceuticals has pointed out that the room for price reductions in centralized procurement mainly stems from three aspects: reducing marketing costs through direct supply to hospitals, lowering financial costs via timely payments, and decreasing production costs through high-volume, low-margin sales. This process eliminates unreasonable expenses that have long existed in the distribution sector.

“Under the broader context of centralized volume-based procurement, channel expenses will be significantly compressed. Within manufacturing enterprises, cost structures related to sales and medical affairs personnel will face substantial reductions, leading to a surplus of talent entering the job market and intensifying cost pressures on these companies. Consequently, many firms are inclined toward collaboration or mergers to diversify their product portfolios and integrate distribution channels.” Li Gang believes that small companies with cost and pricing advantages are driven to expand rapidly, while larger companies are motivated to enrich their product lines, both of which will further spur merger and acquisition activities.

The Pandemic Has Driven Rapid Growth in Certain Niche Sectors

Epidemic prevention and control have driven rapid growth in several niche sectors, such as in vitro diagnostics (IVD), third-party medical testing, and vaccines.

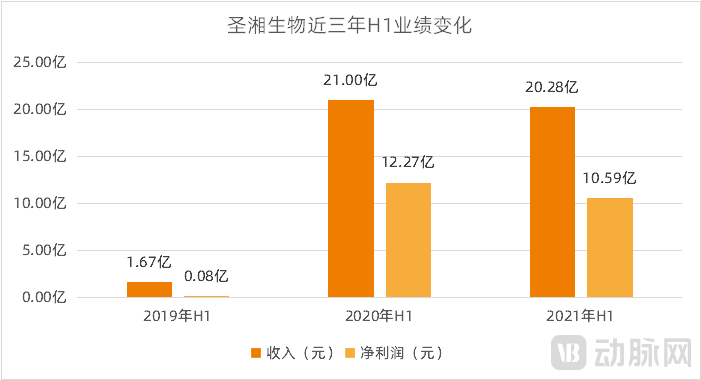

The rapid growth of the IVD industry became evident during the 2020 pandemic. In early January 2020, Sansure Biotech’s COVID-19 nucleic acid diagnostic kit received regulatory approval, after which the company undertook large-scale production of these tests. In August, Sansure Biotech successfully completed its initial public offering (IPO) on the STAR Market. Driven by revenue from COVID-19 nucleic acid testing kits, Sansure Biotech’s performance surged in the first half of 2020: it reported revenue of RMB 2.1 billion, a year-on-year increase of 1,159.39%, and net profit of RMB 1.227 billion, a year-on-year increase of 14,687.20%.

Performance Growth of Sansure Biotech, Data Source: Prospectus and 2021 Semi-Annual Report, Compiled and Charted by VCBeat

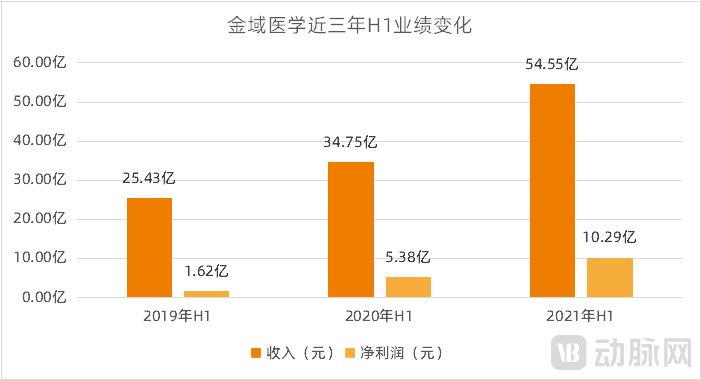

Third-party medical testing laboratories also began to play a significant role from the early stages of the pandemic. Taking KingMed Diagnostics as an example, its performance experienced continuous growth from 2020 to 2021. In the first half of 2021, its revenue reached RMB 5.455 billion, twice that of the same period in 2019; net profit amounted to RMB 1.029 billion, six times that of the first half of 2019.

According to KingMed Diagnostics’ 2021 semi-annual report, revenue from COVID-19 nucleic acid testing expanded, while routine testing services (non-COVID-19) recovered robustly, driving a substantial increase in revenue scale. This led to a pronounced dilution effect on fixed costs and expenses, thereby further boosting profits.

KingMed Diagnostics’ Performance Growth; Data Source: 2020 and 2021 Semi-Annual Reports, Compiled and Charted by VCBeat

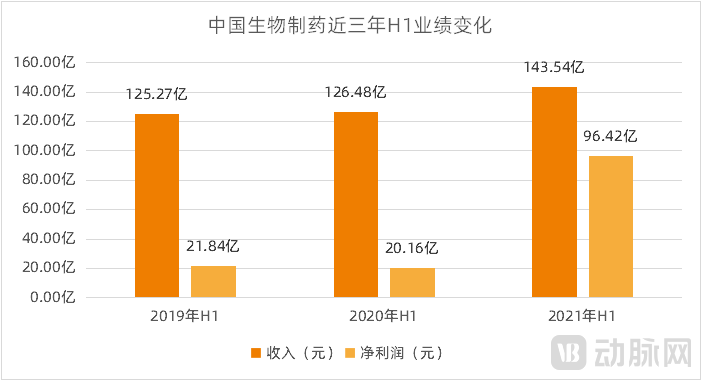

In terms of vaccines, due to the longer R&D cycle, the revenue growth driven by production and vaccination began to materialize in 2021. In the first half of 2021, China Biopharmaceutical achieved revenue of RMB 14.354 billion, a year-on-year increase of 13.49%; net profit reached RMB 9.642 billion, a year-on-year surge of 378.27%. China Biopharmaceutical holds a 15.03% stake in Sinovac Life Sciences. According to its 2021 semi-annual report, Sinovac’s COVID-19 vaccine has been approved for emergency use or conditional marketing authorization in more than 50 countries. Associates and joint ventures, including Sinovac Life Sciences, contributed a total profit of RMB 7.585 billion.

Furthermore, CanSino Biologics, which had previously listed on the Hong Kong Stock Exchange as an unprofitable technology company, achieved profitability for the first time in the first half of 2021, driven by sales of its COVID-19 vaccine, with a net profit of RMB 973 million.

The current epidemic has had a profound impact on various industries. Wu You believes that supplies related to infectious disease control may be stockpiled for emergency response purposes, similar to strategic war reserves. This also implies that the market size for these products may not shrink rapidly as the epidemic subsides. Consequently, mergers and acquisitions in this sector may need to consider factors related to national security and will be significantly influenced by policy regulations.

Performance Growth of Sino Biopharmaceutical; Data Source: 2020 and 2021 Semi-Annual Reports, Chart Compiled by VCBeat

Li Gang stated that the pandemic brought about significant changes in the market landscape. Some companies that were previously unable to go public or were hovering around the break-even point rapidly developed into industry leaders with ample cash flow, thus creating a demand for mergers and acquisitions to facilitate further expansion.

Sansure Biotech is one of the companies experiencing rapid growth and seeking further expansion through mergers and acquisitions. In 2021, Sansure Biotech acquired a 14.77% equity stake in Zhenmai Biotechnology for RMB 255 million and proposed to acquire an 18.63% equity stake in Kehua Bio-Engineering for RMB 1.95 billion. Although the transaction to acquire Kehua Bio-Engineering was temporarily terminated due to issues with transfer procedures, it still demonstrates Sansure Biotech’s strategy of deepening its industrial chain layout through mergers, acquisitions, and integration.

The Impact of Changes in Capital Exit Pathways

Initial public offerings (IPOs) and mergers and acquisitions (M&A) are two common exit routes for capital. While the two exhibit a certain degree of inverse relationship, a higher volume of IPOs may also stimulate increased M&A activity.

Both the Chapter 18A listing rules of the Hong Kong Stock Exchange and the fifth set of listing criteria of the STAR Market allow pre-profit companies to go public, providing a listing pathway for firms with technological innovation capabilities that are not yet profitable, while also offering investors more exit options. “Without these channels, when a fund reaches maturity, its portfolio companies would become targets for mergers and acquisitions,” said Wu You.

On November 15, 2021, the Beijing Stock Exchange (BSE) commenced operations. Among the first batch of 81 listed companies, 10 were from the healthcare sector, including Nuosheng Lande, Deyuan Pharmaceutical, Sanyuan Gene, and Senxuan Medicine. Dominated by small and medium-sized enterprises (SMEs), the BSE has added another channel for capital exit.

However, there is another side to this impact. Wu You noted that an initial public offering (IPO) serves not only as an exit route for investors but also as one of the channels for companies to raise capital. With financial support gained after going public, companies can achieve growth through mergers and acquisitions much faster than by building teams and expanding operations organically. “Therefore, more companies being able to go public also means that more enterprises have access to funding channels for further consolidation of other businesses.”

M&A integration with capital as the buyer is on the rise

Historically, acquirers in M&A integrations were predominantly strategic industry players, aiming to optimize their business portfolios and drive revenue growth.

However, the "2021 iKang Capital China Health Industry White Paper—Mergers and Acquisitions in the Health Industry" notes that due to the lack of liquidity in the primary market, the exit of minority shareholders is constrained by numerous factors, such as the company’s financing or IPO plans and the investment intentions of new-round investors. Consequently, exit pathways for early-stage minority equity stakes are often unclear, and funds with specific investment horizons frequently face the dilemma of having to sell at a discount. In contrast, acquiring controlling interest in a company significantly enhances a fund’s strategic initiative. By participating in internal operational management, engaging in external M&A integration, and designing capitalization pathways, funds can continuously optimize the enterprise’s business and capital structure, thereby reducing investment risks and achieving asset appreciation.

Consequently, fund-led M&A integration, with the fund acting as the buyer, is becoming a trend. “After acquiring controlling interest in a company, funds typically have a 3–5 year window to execute rapid integration or value enhancement and to consider exit strategies,” said Wu You. Compared with strategic investors, funds face stricter requirements regarding time horizons and the pace of industrial integration.

Representative firms such as Songbo Investment have extensively participated in the development of various sectors within the dental industry across Asia, North America, and Europe through controlling stakes and minority investments. With a presence spanning the upstream, midstream, and downstream segments of the value chain, they assume the role of builders advancing both the dental discipline and its associated industries.

CB Capital also falls into this category, focusing on platform development, controlling acquisitions, and alternative investments in three core areas: pharmaceuticals and biotechnology, medical technology, and healthcare services. Unlike traditional investment firms, CB Capital operates more like an industrial incubation platform, providing capital and resource support to projects in specialized healthcare sectors to help them grow and expand. In August 2021, CB Capital made a controlling investment in Anhe Galil, a company specializing in ultrasonic scalpels, further extending its presence in the field of minimally invasive therapy.

How Will M&A Transactions Shape the Industry Landscape in the Future?

Li Gang believes that, considering the aforementioned multidimensional influencing factors, mergers and acquisitions (M&A) are expected to account for approximately one-third of all transactions in the healthcare industry over the next three to five years. “This projection is based on Capital Alpha’s observations of industry data and its coverage of enterprises within the sector.”

In its previous article, “By Analyzing Capital Data from 5,000 Companies, We Have Gained Insights into the Current Status and Future of 12 Healthcare Subsectors,” VCBeat compiled and analyzed investment and financing data across specialized fields such as innovative drugs, medical devices, healthcare services, and artificial intelligence. Most of these sectors entered their peak funding periods between 2013 and 2015.

“From 2013 to 2018, equity financing in the primary market was booming. However, after several years of development, some companies struggled and began to show signs of fatigue around 2018–2019. Of course, financing for innovative drugs and biotechnology remained robust and did not wane,” said Li Gang. He noted that in the future, M&A will serve as a pathway for further growth for companies with rapid expansion and IPO readiness. Meanwhile, for some companies whose IPO plans face setbacks, achieving capital exit through acquisition is a pragmatic option.

However, unlike the "survival of the fittest" dynamic seen in the natural world, mergers and acquisitions (M&A) integration is a multi-party strategic game that requires the perfect alignment of timing, favorable conditions, and human harmony. For instance, in July 2021, Winning Health and B-Soft announced plans to merge, quickly making the announcement an industry hotspot. Yet, just four days later, a dramatic turn of events occurred: both parties announced the termination of the merger due to their "inability to reach agreement on core terms."

Wu You stated that, typically, three key factors facilitate smooth post-merger integration: strong certainty on the seller’s part to close the deal, a sufficient number of potential buyers to foster competitive bidding, and a strong strategic fit between the target’s quality and the acquirer.

Taking Hygeia’s acquisition of Suzhou Yongding Hospital as an example, iCapital served as the exclusive financial advisor to Suzhou Yongding Hospital. According to Wu You, from the seller’s perspective, the controlling shareholder of Suzhou Yongding Hospital is Shangda Capital, which faced an urgent need to exit due to the approaching maturity of its fund, resulting in a high degree of certainty for the sale. From the buyer’s perspective, there are numerous listed healthcare service groups as well as fund-backed healthcare service groups, ensuring a sufficient pool of potential buyers. In terms of the target itself, Suzhou Yongding Hospital generated nearly RMB 500 million in revenue and RMB 61 million in net profit in 2020, demonstrating solid financial performance. Moreover, with only half of its beds currently operational, the hospital has significant room for growth. Additionally, the project exhibits a high level of regulatory compliance, having previously been part of two listed companies, China Automation Group and Yongding Shares. Overall, it represents a scarce and attractive investment target.

Precisely because M&A transactions are the result of multi-party trade-offs and strategic gaming, comprehensive due diligence, and protracted negotiations, all relevant stakeholders can only maximize their benefits after the integration is completed. As M&A integration activity intensifies within the industry, the beneficiaries extend far beyond acquirers seeking to expand their product portfolios and service networks or achieve performance growth. Capital investors also benefit by recycling funds into innovative fields after exiting their investments, thereby enhancing industrial vitality. Moreover, acquisition targets realize their own value through access to larger platforms and richer resources.