Shandong's Hyaluronic Acid Industry Powers Global Beauty Economy as Tech Giants Enter the Fray

In the current era where the "beauty economy" is prevalent, the medical aesthetics industry has seized the momentum, attracting a large number of enterprises and capital investors. According to data from the VCBeat Orange Database, since 2016, there have been over 100 primary market financing deals in China's medical aesthetics industry, with the total financing amount reaching tens of billions of RMB.

Amid the surging momentum, the medical aesthetics industry has seen the emergence of numerous niche segments with market potentials reaching tens of billions, or even hundreds of billions, of yuan.Among them, sodium hyaluronate (commonly known as "hyaluronic acid," hereinafter referred to as hyaluronic acid) is the most prominent one.

Why? First, leading companies boast ultra-high gross profit margins of up to 90%, comparable to Kweichow Moutai. Second, the industry has spawned multiple enterprises with market capitalizations exceeding RMB 10 billion, and the market continues to expand.This indicates that hyaluronic acid companies not only possess ample cash flow and profit margins, but also demonstrate high growth potential.

Reflected in the capital markets, the market capitalizations of the “big three” hyaluronic acid companies—Imeik, Bloomage Biotech, and Haohai Biological Technology—have all reached tens of billions, or even hundreds of billions, of yuan. Meanwhile, the primary market remains hot: Tencent and Fortune Capital have recently invested in Shandong-based hyaluronic acid enterprises Freda Biotechnology and Meiye Biotechnology, respectively.

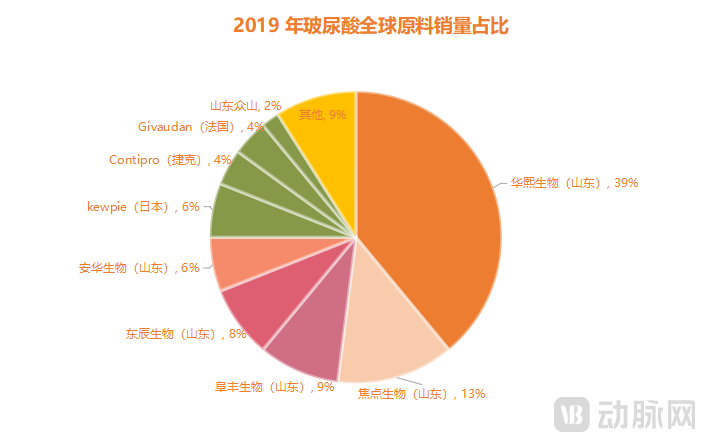

However,Little known is the fact that the vast majority of hyaluronic acid raw materials in the global market originate from China.According to the "China Hyaluronic Acid Industry Market Research Report" released by Frost & Sullivan in 2020, China's total sales volume of hyaluronic acid raw materials accounted for 81% of the global total in 2019, meaning that the raw materials for eight out of every ten hyaluronic acid products originated from China.

(Data source: Orient Securities; Chart by VCBeat)

(Data source: Orient Securities; Chart by VCBeat)

What is even more surprising is that the top five companies by sales volume of hyaluronic acid raw materials (Bloomage Biotech, Focus Biotech, Fufeng Biotech, Dongchen Biotech, and Anhua Biotech) are all located in Shandong Province, with a combined global market share as high as 75%, virtually “monopolizing” the entire market.

Why Has Shandong Taken a Clear Lead in the Hyaluronic Acid Industry? What Challenges and Hidden Concerns Remain, and What Is the Future Evolutionary Path? Next, VCBeat seeks to uncover the answers by interviewing multiple industry insiders and conducting a comprehensive industry review.

Although hyaluronic acid has a history of nearly a century, the entire industry has only become highly active in the past 20 years or so. Why? The core challenge lies in the industrialization of the technology.

Back in 1934, Karl Meyer, a professor of ophthalmology at Columbia University, extracted a polysaccharide from the vitreous humor of bovine eyes during an experiment and named it uronic acid (hyaluronic acid). He discovered that this substance could lubricate joints, regulate the permeability of blood vessel walls, modulate the diffusion and transport of proteins and water-electrolytes, and promote wound healing. As a result, hyaluronic acid garnered widespread attention from the industry upon its introduction.

However, in the following decades, hyaluronic acid failed to achieve widespread application. This was because each cow has only two eyes, resulting in limited extraction yields, and due to technological limitations at the time, the quality was also poor.Therefore, the challenge of industrializing hyaluronic acid technology lies before researchers.

To achieve industrialization, mass production must first be addressed. Consequently, researchers focused on overcoming technical challenges related to the source and processing of hyaluronic acid, successfully extracting it from chicken combs. Compared with bovine eye extraction, the chicken comb method enabled the mass production of hyaluronic acid, facilitating its application across numerous fields.

However, the problem is that the rooster comb extraction method still suffers from extremely low extraction yields, complex separation processes, and limited production capacity. This has led to the high cost of hyaluronic acid; for instance, low-purity hyaluronic acid used in cosmetics costs $5,000 per kilogram, while medical-grade high-purity hyaluronic acid costs $100,000 per kilogram, making it as expensive as gold.At that time, although hyaluronic acid was already available in substantial volumes, it remained a high-end consumer product for the wealthy, still quite distant from mass-market adoption.

It was not until 1964 that Shiro Kobayashi’s team in Japan successfully synthesized hyaluronic acid using monomeric enzyme catalysis, officially launching the industrialization of hyaluronic acid.

In China, the industrialization of hyaluronic acid was not successfully achieved until the 1980s. At that time, Guo Xueping and Ling Pei, both students of Zhang Tianmin—one of the founders of biochemical pharmaceutical sciences in China—joined the Shandong Academy of Pharmaceutical Sciences and began researching hyaluronic acid with their team.

To address the technical challenges in hyaluronic acid fermentation production, Guo Xueping’s team undertook China’s national key scientific and technological research projects during the “Eighth Five-Year Plan” and “Ninth Five-Year Plan” periods. After two years of countless experiments, they successfully mastered the microbial fermentation technology for producing hyaluronic acid in 1992, filling a technological gap in China.This fermentation method enabled the production and mass manufacturing of hyaluronic acid via Streptococcus fermentation, whereas it had previously been extractable only from bovine eyes and rooster combs. This breakthrough significantly reduced costs, directly accelerating the industrialization and scaling of hyaluronic acid, and transformed China’s reliance on imports for this key ingredient.

Once mass production is confirmed to be problem-free, the second step in industrialization is commercialization.In 1992, Ling Peixue’s team founded Shandong Freda Pharmaceutical Group by contributing technology from the Academy of Pharmaceutical Sciences as equity investment (from which Bloomage Biotech was later spun off), making it one of the first enterprises in China’s hyaluronic acid industry. Subsequently, Shandong-based hyaluronic acid companies such as Focus Bio, Fufeng Bio, and Dongchen Bio were established one after another, thereby accelerating the commercialization process of hyaluronic acid.

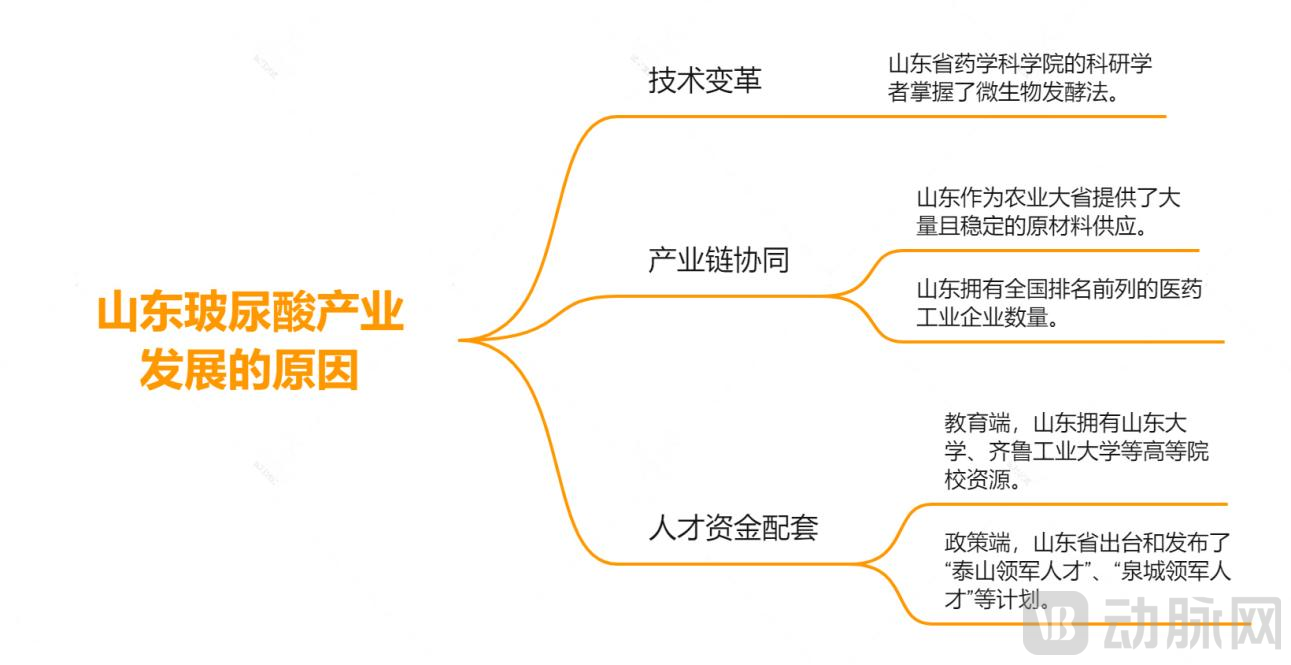

As can be seen from the above course of industrial development,The clustering of hyaluronic acid enterprises in Shandong is not unrelated to the fact that scientific researchers such as Ling Peizhang and Zhang Tianmin hail from the Shandong Academy of Pharmaceutical Sciences, thus endowing the region with a natural historical “foundation.”

On the other hand, whether an industry can achieve agglomeration in a given location must also be evaluated from the perspective of maximizing commercial efficiency, such as supply chain synergy and the availability of supporting talent and capital.

First, let us examine the synergy within the industrial chain.As a major agricultural province, Shandong provides a substantial and stable supply of raw materials for hyaluronic acid production. On the other hand, Shandong is home to numerous pharmaceutical companies. According to data released by the Information Office of the Shandong Provincial People's Government, as of 2020, there were 616 pharmaceutical industrial enterprises above designated size in Shandong Province, with the scale of its pharmaceutical industry accounting for approximately one-tenth of the national total. This has endowed the hyaluronic acid industry with advantages in upstream and downstream collaboration, rapidly fostering a network of industrial synergy.

Next, let's look at the matching funds for talent.In terms of education, Shandong Province boasts higher education resources such as Shandong University and Qilu University of Technology, which provide a steady stream of graduates to the pharmaceutical industry. Coupled with the clustering of pharmaceutical companies, this has also fostered the development of numerous technical and research professionals within the industrial sector. Furthermore, the Shandong Provincial Government has consistently prioritized the biopharmaceutical field, introducing initiatives such as the “Taishan Leading Talent” and “Quancheng Leading Talent” programs, supported by financial incentives and policy measures to attract talent from across China and around the world.

Driven by the aforementioned factors, Shandong has established a complete hyaluronic acid industrial cluster, giving rise to major hyaluronic acid raw material manufacturers such as Bloomage Biotech, Focus Biotech, Fufeng Biotech, Dongchen Biotech, and Anhua Biotech, thereby achieving a commercial footprint that extends from Shandong to China and then to the global market.

It is worth noting that, leveraging its advantages in the hyaluronic acid industry, Shandong has gradually formed a large-scale medical aesthetics industrial cluster.A search for “medical aesthetics” on Tianyancha reveals over 40,000 currently active related enterprises in Shandong Province, ranking first nationwide.

Undoubtedly, Shandong has become one of the important industrial clusters for medical aesthetics raw materials in China and even worldwide.

Since the industrialization of hyaluronic acid raw materials entered an accelerated phase, the supply of hyaluronic acid-related products has rapidly increased, gradually expanding into fields such as orthopedics and ophthalmology.

However, it was the rapid development of the medical aesthetics industry after 2000 that truly propelled hyaluronic acid to fame and enabled Shandong’s hyaluronic acid raw materials to dominate the global market.

It is worth noting that since the beginning of the 21st century, China’s medical aesthetics industry has experienced vigorous growth, with public hospitals establishing plastic surgery departments and private institutions emerging in large numbers. Amidst the rising demand for and supply of medical aesthetic services, hyaluronic acid has been widely adopted. This is largely due to its exceptional hydrating capacity, as a single hyaluronic acid molecule can bind more than 500 times its weight in water. Consequently, relevant companies have developed hyaluronic acid-based products to help combat aging.

On one hand, it has the potential to attract attention; on the other hand, hyaluronic acid also possesses strong water-absorbing properties.

This is primarily because minimally invasive aesthetic procedures involving injectable fillers mainly use hyaluronic acid as the raw material. Compared with surgical aesthetic procedures, they offer higher safety, lower operational complexity, lower unit prices, and greater user acceptance, particularly resulting in higher repurchase rates. These factors collectively lead to lower promotion and customer acquisition costs for medical aesthetic institutions.Therefore, from a business perspective, hyaluronic acid is undoubtedly a lucrative venture.

According to Frost & Sullivan data, among pharmaceutical-grade hyaluronic acid end-use products (medical aesthetics, orthopedic treatment, and ophthalmic treatment), medical aesthetics accounts for a significant share and exhibits the highest compound annual growth rate (CAGR). In 2014, medical aesthetic products accounted for 33.3% of the overall pharmaceutical-grade hyaluronic acid market; this proportion rose to 53.8% in 2018. From 2014 to 2018, the CAGR of the market size for pharmaceutical-grade hyaluronic acid end-use products was 32.2%.

(Medical aesthetics drives significant surge in hyaluronic acid raw material market; Image source: Shenwan Hongyuan)

(Medical aesthetics drives significant surge in hyaluronic acid raw material market; Image source: Shenwan Hongyuan)

From the perspective of product extension in pharmaceutical-grade hyaluronic acid, there are many categories that can be expanded. If classified by function, they can be divided into three types: first, rapid hydration products, such as skin boosters; second, filling and shaping products, such as rhinoplasty, chin and forehead augmentation, cheek enhancement, and lip augmentation; third, wrinkle-reducing products, such as treatments for nasolabial folds, marionette lines, and forehead wrinkles.

On the other hand, with the industrialization and technological advancements of hyaluronic acid, hyaluronic acid and its derivatives with diverse physical and biological properties have gradually entered the skincare and color cosmetics markets. They are now widely used in products such as serums, lipsticks, lotions, creams, facial masks, and facial mists. It is evident that the expanded versatility of these products has led to richer user scenarios and greater commercial potential.

From medical aesthetics to cosmetics, hyaluronic acid is holding up the faces of women worldwide: from beauty enhancements and skincare to daily grooming, hyaluronic acid has become ubiquitous.Leveraging the synergistic advantages of a concentrated cluster of hyaluronic acid raw material manufacturers and its cost competitiveness, Shandong has secured a significant share of the international market.

According to Bloomage Biotechnology’s prospectus, in 2018, the average export price of pharmaceutical-grade and other grades of hyaluronic acid raw materials from Chinese companies was nearly less than half of the average export price from overseas companies. In 2018, China’s export volume of hyaluronic acid raw materials was approximately 292 tons, with a compound annual growth rate (CAGR) of 35.2% from 2014 to 2018. Among exporting enterprises, Bloomage Biotechnology accounted for 34.0%, and Focus Biochemistry accounted for 16.6%.As can be seen, the hyaluronic acid raw material industry exhibits a high degree of market concentration.

However, it is important to recognize that although Shandong-based enterprises “dominate globally” in the field of hyaluronic acid raw materials, Allergan, Imeik, Q-Med AB, LG Life Sciences, Ltd., Bloomage Biotechnology, and Haohai Biological Technology hold the major shares of the overall medical aesthetic hyaluronic acid market. In other words, among the top-ranking companies, only Bloomage Biotechnology is from Shandong, indicating that Shandong-based enterprises account for a relatively small proportion of the entire market.

What are the underlying reasons?

Theoretically, possessing a production advantage in raw materials often implies that a company also enjoys cost and industrial synergy advantages in the research and development of high-value-added end products.

For example, in 2012, China saw the launch of its first domestically produced hyaluronic acid dermal filler, “Runbaiyan” (developed by Bloomage Biotech). The introduction of this product accelerated the trend among young people in China to receive injections of domestically produced hyaluronic acid. Nine years after its market debut, the product continues to demonstrate strong sales performance: during this year’s June 18 Shopping Festival, Runbaiyan achieved total cross-platform sales exceeding RMB 230 million, a year-on-year increase of 232%. Sales on its Tmall flagship store surpassed RMB 100 million, marking the third consecutive year of doubled growth, and securing the top position among emerging domestic skincare brands on Tmall throughout the entire June 18 promotional period.

The underlying reason is that, building on its deep expertise in hyaluronic acid raw materials, Bloomage Biotech is better positioned to align technical processes and manufacturing techniques with the development of end-user products. “Compared with its peers, this has given Bloomage Biotech a more favorable time window,” said Dai Yao (pseudonym), an industry insider close to Bloomage Biotech, in an interview with VCBeat.

Yet behind the glamour, Shandong’s hyaluronic acid raw material industry cannot conceal an awkward reality: raw materials struggle to command high prices, and competition is becoming increasingly fierce. According to data provided by Ling Peixue in a previous media interview,Hyaluronic acid raw material prices have been declining for the past decade, with an average annual decrease of approximately 5%, suggesting that production capacity may have begun to exceed demand.

Data from leading companies indicate that the unit price of sodium hyaluronate has been declining year by year, according to figures disclosed in Imeik’s prospectus. Specifically, the average selling price of Bloomage Biotech’s injection-grade raw materials decreased from RMB 122.62 per gram in 2017 to RMB 111.69 per gram in 2019, while Haohai Biological Technology’s procurement price for refined hyaluronic acid powder also fell from RMB 170.94 per gram in 2017 to RMB 150.37 per gram in 2019.

In other words, relying solely on the raw material business is no longer sufficient to sustain the long-term growth of hyaluronic acid companies.“Most hyaluronic acid raw material manufacturers in Shandong have made limited efforts in developing end-user products, relying primarily on trend-driven tailwinds for growth, with few notable successes in creating blockbuster products,” said Dai Yao.

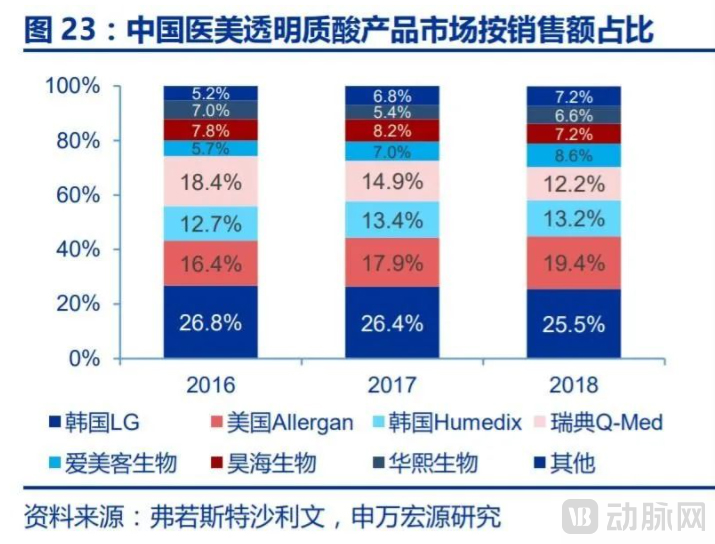

According to Frost & Sullivan data, in terms of market sales share (2018) of medical aesthetic hyaluronic acid products in China, the leading brands were foreign companies such as LG Chem (South Korea), Allergan, Humedix (South Korea), and Q-Med (Sweden). Among Chinese manufacturers, only Bloomage Biotechnology from Shandong Province ranked among the top players, but its market share was merely 6.6%, significantly lower than LG Chem’s 25.5%.

(Image source: Shenwan Hongyuan)

(Image source: Shenwan Hongyuan)

“For hyaluronic acid companies, it is not enough to remain confined to the role of raw material suppliers; they need to continuously deepen their presence downstream and diversify their business portfolios,” said Dai Yao. She noted that these end products enjoy high gross profit margins, bolstered by the low cost of hyaluronic acid, with medical aesthetic products achieving gross margins of approximately 80%.

Taking Freda Biopharm, which received investment from Tencent, as an example, in addition to businesses such as the research and development, production, and sales of raw materials, it currently owns 11 brands, including “Rellet,” specializing in hyaluronic acid-based skincare, and “Dr. Alva,” focused on microbiome science-based skincare. Among these, both “Rellet” and “Dr. Alva” achieved sales exceeding RMB 100 million each during this year’s “Double 11” shopping festival.

Similarly, looking at Bloomage Biotech, its 2020 financial report showed that in the revenue structure, the income from “functional skincare” reached RMB 1.346 billion, surpassing for the first time the RMB 703 million from product raw materials and the RMB 576 million from medical terminal products.

Interestingly, Meiyi Biologics, a portfolio company of Fortune Capital invested in recently, was founded in 2016 by Ling Peixue, the founder of Freda Biotechnology. The company focuses on the skincare sector and primarily operates three brands: Dr. Ling (skincare), FMFM (body care), and Natural Rhythm (skincare and personal care). Among these, Dr. Ling’s core ingredient is full-molecular-weight hyaluronic acid (Gaussian HA). Launched in 2021, the brand achieved sales of nearly RMB 200 million within its first five months on the market. This demonstrates that functional skincare has become a key area for hyaluronic acid companies to extend their value chain downstream.

Notably, the functional food sector has also opened up new potential pathways for hyaluronic acid companies.Earlier this year, the National Health Commission officially approved Bloomage Biotechnology Corp., Ltd.’s application to list hyaluronic acid as a new food raw material, marking the commencement of Bloomage Biotechnology’s commercial journey into functional foods.

Meanwhile, the internet-famous brand Hankou Erchang has launched “Ha Shui,” a hyaluronic acid-infused sparkling water, emphasizing in its marketing that it contains an amount of hyaluronic acid equivalent to four facial masks and three beauty serums, with benefits such as enhancing skin hydration, promoting supple and radiant skin, and improving complexion. Furthermore, WonderLab, a nutritional meal-replacement brand, introduced its first oral hyaluronic acid gummies, while SMEAL launched a hyaluronic acid blood orange drink, among other products. The functional food sector featuring hyaluronic acid is experiencing significant growth and enthusiasm.

According to the “2020 White Paper on Hyaluronic Acid Application Scenarios,” the market size of terminal pharmaceutical-grade hyaluronic acid products in China reached RMB 12.6 billion in 2024, while the global market size for food-grade hyaluronic acid terminal products amounted to RMB 3.2 billion.It is evident that, building on hyaluronic acid as a raw material, the development of end-use products has opened up an increasing number of niche market segments, creating opportunities for hyaluronic acid companies.

“Raw materials are no longer Bloomage Biotech’s largest source of revenue, but it is important to recognize that the company’s R&D investment ratio is relatively low. For a biotechnology firm, this necessitates a reevaluation of its competitive barrier structure,” said Dai Yao. Currently, the ratio of R&D expenses to revenue for hyaluronic acid companies such as Bloomage Biotech, Focus Bio, and Fufeng Bio is below the 15% threshold generally required by the STAR Market for listed companies. In other words,As the current technological barriers for these companies gradually erode, future competition may hinge more on distribution channels, marketing, branding, and other factors.

However, the challenge lies in the fact that channels, marketing, and branding are areas where consumer-grade companies excel. For enterprises on Shandong’s hyaluronic acid industry chain, which originated from pharmaceutical manufacturing, this path is far from easy: building sales teams, creating products favored by end consumers, and establishing consumer brands are, in reality, commercial blind spots for manufacturers of hyaluronic acid active pharmaceutical ingredients (APIs).

“Simply put, companies that originally produced raw materials like hyaluronic acid powder are now seeking to manufacture end-user products such as facial serums and dermal fillers. This requires not only catching up on product development and R&D but also mastering the shift from B2B to B2C marketing,” said Dai Yao. “These are fundamentally different business models with significant disparities. While Bloomage Biotech has performed relatively well in this transition, it does not mean that all hyaluronic acid companies in Shandong Province can successfully transform.”Of course, the long-term survival dilemma faced by hyaluronic acid raw material manufacturers necessitates a strategic pivot. If they fail to transform and break through, they must return to the technological core, ramp up R&D efforts, and evolve into high-value biotechnology enterprises, thereby securing greater pricing power.”

This may be a positive signal, after all, the development history of the hyaluronic acid industry has proven that it is precisely technological innovation that has enabled more people to achieve their desire for beauty by using more affordable hyaluronic acid products.

Therefore, for hyaluronic acid raw material manufacturers in Shandong Province, only by continuously prioritizing research and development can they ensure the long-term “beauty” and sustainability of their medical aesthetics business.