Gushengtang Lists on HKEX, 'Quiet Monk' of Healthcare Investment Scores Two IPOs in 18 Months

Long Hill Capital

Venture Capital Institution

In June this year, Gushengtang TCM, China’s largest private integrated traditional Chinese medicine (TCM) healthcare service platform, filed its prospectus with the Hong Kong Stock Exchange.

Just five months later, Gushengtang passed the hearing by the Hong Kong Stock Exchange.

On December 10, Gushengtang successfully listed on the Hong Kong Stock Exchange.

On its listing day, Gushengtang’s market capitalization finally settled at HK$6.681 billion. Among companies listed on the Hong Kong Stock Exchange, it became the medical services enterprise with the fourth-largest market capitalization that day, trailing only China’s leading oncology healthcare group Hygeia Healthcare, assisted reproductive services provider Jinxin Fertility Group, and C-MER Eye Care.(See details below)。

Gushengtang’s listing has, to some extent, bolstered confidence in the healthcare sector, breaking the jinx whereby pharmaceutical companies’ stocks would fall below their IPO price on the first day of trading. Over the past few months, the Hong Kong IPO market has been sluggish, with many companies choosing to postpone their offerings. For instance, Baixinan Biology, originally scheduled to list on November 26, announced that “in light of current market conditions and after consulting with the sole global coordinator, it has decided to delay the global offering.” Despite the relatively tepid market sentiment, Gushengtang still achieved an oversubscription rate of more than eight times.

Behind the listing of Gushengtang, we once again see the presence of Long Hill Capital, a consistently low-profile capital promoter. Why Long Hill Capital again? This question has once more been placed before the public.

For Gushengtang, an unavoidable key figure is Jiang Xiaodong, Managing Partner of Long Hill Capital.

According to Gushengtang’s prospectus, in August 2014, Jiang Xiaodong, then Managing Director of NEA China, invested exclusively in Gushengtang’s Series A round as its first institutional investor.

Over the following seven years, Jiang Xiaodong, representing NEA and Long Hill Capital (which he founded in late 2016), increased their stakes in Gushengtang on four separate occasions. Ultimately, Long Hill Capital and NEA held nearly 15% of Gushengtang’s shares at the time of its IPO, making them the company’s largest external institutional investors.

As the sole representative of the company’s early investors, Jiang Xiaodong continued to serve as a director of the listed company Gushengtang in the capacity of Non-Executive Director and member of the Audit Committee, following his seven-year tenure as a director of Gushengtang.

In Gushengtang’s prospectus, we also identified a rather intriguing point. The prospectus reveals that Long Hill Capital was not only Gushengtang’s first institutional investor but also the lead investor in its Pre-IPO financing round prior to listing. This same pattern was observed in Hygeia Healthcare, another company listed with Long Hill Capital’s involvement just a year and a half earlier.

Hygeia Healthcare, the leading oncology medical group that successfully went public in late June 2020, has now become the most valuable healthcare services company listed on the Hong Kong Stock Exchange. Jiang Xiaodong was both the first investor in Hygeia Healthcare at its inception and the last investor before its IPO—in 2019, Long Hill Capital, under his leadership, co-invested with WuXi AppTec in Hygeia Healthcare’s Pre-IPO round.

By examining its investments in Gushengtang Traditional Chinese Medicine and Hygeia Healthcare, one can observe Long Hill Capital’s “long-termism” and perseverance in the healthcare services sector. The value ultimately demonstrated by this steadfast commitment is nothing short of remarkable—

According to Choice, there are currently nearly 50 companies in the Hong Kong stock market classified under “Healthcare Providers & Services.” If we filter these based on the nature of serious medical care—excluding companies in the dental and medical aesthetics sectors, which have stronger consumer healthcare attributes (it may also be worth noting that Jiang Xiaodong has publicly stated that all medicine is inherently serious, with consumer healthcare merely leaning more toward consumer-oriented scenarios)—and further screen for companies that deliver services backed by offline physical hospitals, we can identify approximately 11 Hong Kong-listed companies more focused on the medical services sector.

![CVUS08Z_58@J{PG)$]$R3}X.png](http://cdn.vcbeat.top/upload/image/08/12/11/26/1639211196503569.png/dmw) Serious Healthcare Service Providers Listed on the Hong Kong Stock Exchange, Data as of December 10, 2021, Source: Tiger Brokers

Serious Healthcare Service Providers Listed on the Hong Kong Stock Exchange, Data as of December 10, 2021, Source: Tiger Brokers

As of the market close on December 10, the combined market capitalization of the aforementioned 11 listed healthcare service companies stood at HK$91.994 billion. Among them, Hygeia Healthcare and Gushengtang Traditional Chinese Medicine, both affiliated with Long Hill Capital, had a combined market capitalization of HK$42.861 billion, accounting for nearly half of the total market value of these healthcare service enterprises. This underscores the unique insight of Long Hill Capital in the healthcare services sector.

Left: Tu Zhiliang, Founder of Gushengtang; Right: Zhu Yiwen, Founder of Hygeia Healthcare

In fact, not all capital can achieve success in the healthcare services sector.

According to VCBeat’s “2020 Global Healthcare Industry Capital Report,” the global healthcare industry saw a total of 2,199 financing events in 2020, with the total amount raised reaching an all-time high of $74.9 billion (approximately RMB 516.93 billion). Among these, the biopharmaceutical sector led all subsectors with 786 deals and a total financing amount of $36.9 billion (approximately RMB 254.7 billion). In contrast, the healthcare services sector completed only 66 transactions, with a cumulative total of just RMB 10 billion, ranking last.

In the healthcare services sector, where most investors hesitate to tread, why has Long Hill Capital, as the sole Series A investor, backed half of the Hong Kong-listed healthcare services companies? What drove them to make substantial bets at the startup stage and continuously increase their investments until these companies grew into industry leaders?

Perhaps, we have to return to the investment logic of Long Hill Capital.

"Do the Hard but Right Thing"

The "Sweeping Monk" of Healthcare Investment Stuns the World

"Jiang Xiaodong declined the interview due to his special status as a director of a listed company."

However, by reviewing his reflections posted on WeChat Moments after Gushengtang’s IPO, we can perhaps gain some insight into Jiang Xiaodong’s determination to go “all in” on the healthcare services sector.

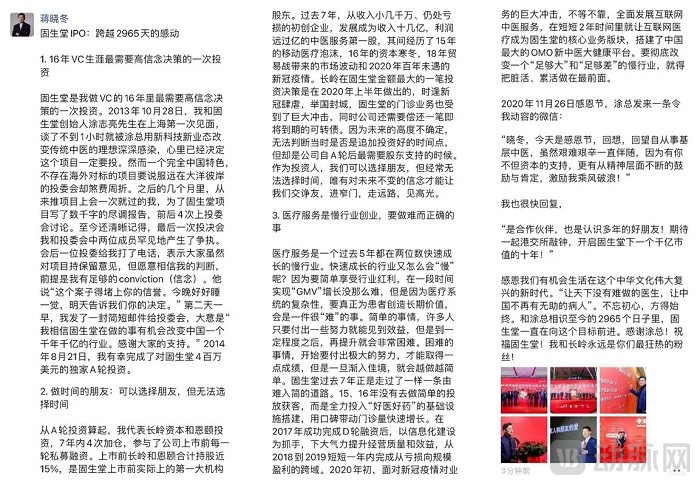

Screenshot from Jiang Xiaodong’s WeChat Moments post at 4:08 PM on December 10

In fact, for a long period, Long Hill Capital maintained a notably low profile, bordering on mystique. Despite its frequent investments in innovative healthcare services and medical technologies, its founder, Jiang Xiaodong, rarely made public appearances or participated in mainstream venture capital community events.

By reviewing the few public speeches he has delivered over the past five years, we may gain insight into his thinking on the healthcare services industry.

He has repeatedly described the healthcare services sector as a “slow industry with rapid growth.” This appears to be a contradictory “combination.” According to Jiang Xiaodong, this is because “it is not particularly difficult to achieve GMV growth over a certain period by simply capitalizing on industry tailwinds. However, due to the systemic complexity of the healthcare sector, creating genuine long-term value for customers is a truly ‘challenging’ endeavor. With easy tasks, many people can see results with modest effort, but further improvement becomes exceedingly difficult after a certain point. In contrast, challenging tasks require substantial initial effort to yield even modest gains; yet once momentum builds and operations mature, they become progressively easier.”

Is embracing simplicity and humility, and doing the difficult yet right things in a slowly growing industry, the secret behind Jiang Xiaodong’s seemingly magical success in investing in healthcare services?

At the VCBeat Future Healthcare Top 100 Conference held this April, Jiang Xiaodong delivered a keynote speech titled “Seeing Because We Believe: Reconstructing the Future of Healthcare with Innovative Services.” He pointed out that Long Hill Capital’s investment strategy is based on the most significant “gray rhino” facing China’s economic and social development over the next two decades—the shift in demographic structure toward an aging population—which could lead to a doubling of medical insurance expenditures. To address the challenges posed by rising healthcare costs, Long Hill Capital has proposed a third solution beyond the conventional approaches of “increasing revenue” and “cutting costs”: investing in innovative medical services and technologies to improve the input-output ratio of healthcare delivery, thereby “achieving more with less.” In his view, one of the key innovation opportunities in the healthcare services sector lies in OMO (Online-Merge-Offline), the integration of online and offline services. This rationale partly explains why the firm chose to invest in Gushengtang Traditional Chinese Medicine and Hygeia Healthcare.

Long Hill Capital’s project screening capabilities have also been validated. By steadfastly committing to the tracks of innovative medical services and innovative medical technologies, Long Hill Capital has ensured that its portfolio companies often successfully secure subsequent rounds of financing. Over a period of four and a half years, it also successfully raised three US dollar funds and one RMB fund, with a total fundraising scale reaching RMB 6 billion. This to some extent reflects the market’s confidence in Long Hill Capital.

By maintaining a low profile and only investing in industry leaders such as Hygeia Healthcare and Gushengtang, Long Hill Capital inevitably invites speculation.

In Jin Yong’s novel *Demi-Gods and Semi-Devils*, a sweeping monk is depicted. Seemingly unremarkable, perhaps even lacking any sense of presence, his martial arts mastery nonetheless reaches the pinnacle of perfection, stunning everyone present with his very first move.

Where will Jiang Xiaodong, the “sweeping monk” of investment in China’s healthcare services sector, lead Long Hill Capital? And who will be the next healthcare services unicorn from the Long Hill Capital ecosystem to go public? Only time will tell.