Will 80,000 Independent Pharmacies Be Eliminated in Three Years? Industry Consolidation Accelerates Amid Intensifying Market Shakeout

Jianzhijia Acquires Another Pharmacy.

On November 30 and December 1, Yunnan Jianzhijia Chain Health Pharmacy Co., Ltd., a wholly-owned subsidiary of Jianzhijia, successively issued announcements regarding the acquisition of 100% equity interest in 81 directly-operated pharmacies of Pu'er Baicaotang Youxuan Pharmaceutical Co., Ltd. (hereinafter referred to as “Pu'er Baicaotang”) and 100% equity interest in Chengdu Haoyaoshi Guangshengtang Grand Pharmacy Chain Co., Ltd. In addition, with respect to store acquisitions, Jianzhijia completed a total of eight acquisition projects from January to September this year, including seven in Yunnan Province and one in the Guangxi Zhuang Autonomous Region.

It is evident how rapidly it has expanded into lower-tier markets. Jianzhijia aims to quickly capture regional market share through continuous acquisitions, establishing a dense network of outlets to enhance its industry competitiveness and brand influence. Since its listing, Jianzhijia has aggressively pursued both mergers and acquisitions and organic growth, with each move drawing significant attention from the outside world. Yet what underlying shifts in the industry landscape have enabled such “cheat-code”-like maneuvers?

A new industry landscape takes shape only after undergoing multiple phases of decline, turbulence, competition, and resurgence. The enterprises that survive this competitive reshuffling will go on to dominate the industry and market. Currently, industry consolidation has become an irresistible trend. If the theme of the pharmaceutical commercial sector over the next four years is mergers and acquisitions, then faced with immense pressure for transformation and upgrading driven by rising industry concentration, the pace of elimination within the pharmaceutical industry must continue to accelerate, further speeding up the terminal-level reshuffling. This also means that a batch of small and medium-sized pharmacies will be acceleratedly eliminated or undergo mergers and restructurings, while the market share of chain pharmacy giants will increase even further. As the tides wash away, large boulders remain steadfast, whereas small pebbles may vanish without a trace...

On October 28, the Ministry of Commerce released the “Guiding Opinions on Promoting High-Quality Development of the Pharmaceutical Distribution Industry During the 14th Five-Year Plan Period” (hereinafter referred to as the “Opinions”), which explicitly sets forth requirements for increasing industry concentration. Notably, the “Opinions” state that by 2025, China aims to cultivate and establish 5–10 specialized and diversified pharmaceutical retail chain enterprises with annual revenues exceeding RMB 50 billion each; the annual sales revenue of the top 100 pharmaceutical retail enterprises should account for more than 65% of the total pharmaceutical retail market, and the pharmaceutical retail chain rate should approach 70%.

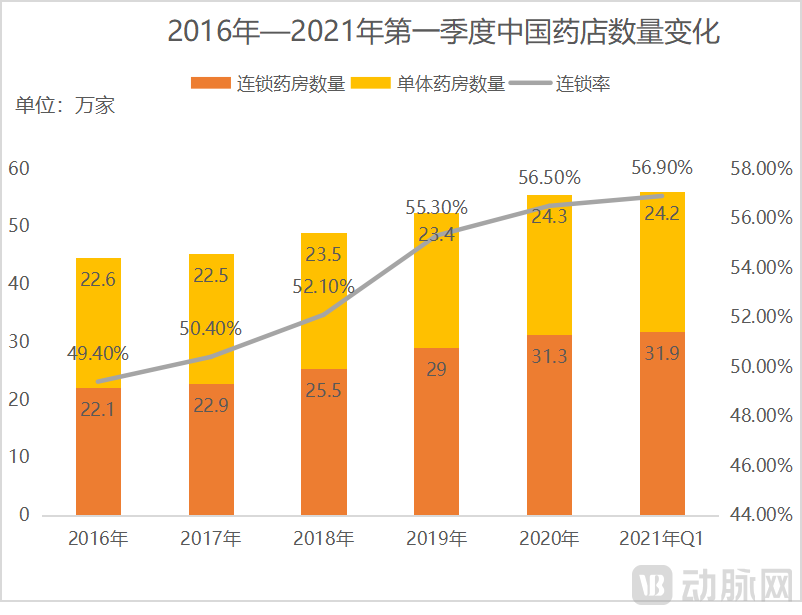

Data Source: National Medical Products Administration; Chart compiled by VCBeat

According to statistics from the National Medical Products Administration, as of the end of March 2021, the total number of retail pharmacy outlets in China reached 561,000. Among these, 241,900 were independent pharmacies, and 319,100 belonged to chain enterprises, with the chain affiliation rate rising to 56.88%. Compared with the end of 2020, the total number of outlets increased by 1.26% over the three-month period, while the chain affiliation rate rose by 0.67 percentage points.

To achieve the 2025 development target of “a retail chain affiliation rate approaching 70%,” the industry may witness a wave of mergers and acquisitions.

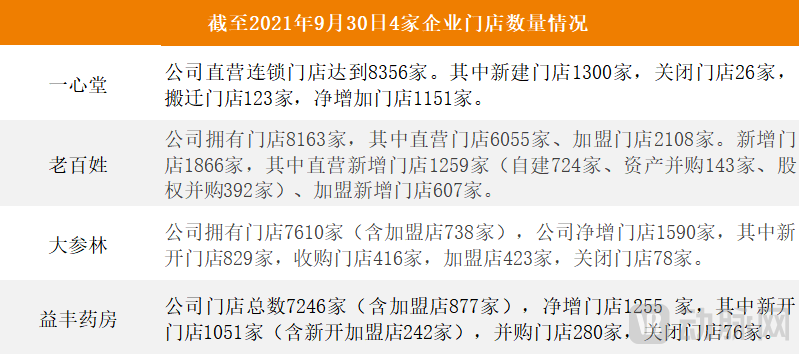

Currently, the four core listed companies in China’s retail chain pharmacy sector are Yixintang, Yifeng Pharmacy, Dashenlin, and Laobaixing. An analysis of the performance of these listed chains during the first three quarters reveals that major chain giants have been accelerating their market expansion in recent years, continuously increasing their chain store ratios. As of the third quarter of 2021, the number of stores operated by the four listed chains—Yixintang, Dashenlin, Laobaixing, and Yifeng Pharmacy—had become relatively comparable. Yixintang and Laobaixing formed the first tier, competing for the top spot, while the total store counts of Yifeng Pharmacy and Dashenlin had both surpassed the 7,000-store threshold. By reviewing the financial reports of these four leading listed enterprises for the first three quarters of 2021, VCBeat has identified the current operational status of the pharmaceutical retail chain pharmacy market.

1Store Count Continues to Expand

According to the quarterly reports of each company, all four enterprises showed positive growth in the number of stores. In terms of store count, Yixintang had the highest number with 8,356 stores, followed by Laobaixing, Dashenlin, and Yifeng Pharmacy.

Source: VCBeat, compiled from annual reports of various companies.

Fierce competition for store resources has accelerated the expansion of store networks by the four major retail pharmacy chains through a combination of organic growth and mergers and acquisitions (M&A). In the first half of this year alone, Laobaixing Pharmacy and Yifeng Pharmacy each completed 11 M&A deals, spending RMB 573 million and RMB 312 million respectively, and incorporating 309 and 264 stores into their networks. Dashenlin completed 14 M&A transactions in the first quarter alone, involving 371 stores at a cost of RMB 533 million.

In August this year, Laobaixing Pharmaceutical Chain Co., Ltd. announced that it plans to acquire a 51% equity stake in Hebei Huatuo Pharmacy Chain Co., Ltd. for RMB 1.428 billion (including loans) using its own funds. The “11x” valuation premium even triggered an inquiry from the Shanghai Stock Exchange, undoubtedly reflecting the intense momentum of mergers and acquisitions aimed at consolidating industry resources.

2Distinct Market Positioning

Behind the Fierce Competition Among Chain Pharmacies: Companies Rely on Clear Market Positioning, with Distinct Development Strategies Tailored to Their Respective Positionings. The Four Companies Each Possess Unique Core Competencies, Which Overall Manifest in Standardization, Diversification, Specialization, Intelligent Efficiency, Omnichannel Operations, and Talent Support.

· Yixintang

Yixintang is actively exploring specialized and digital development pathways to enhance its service capabilities, continuing to innovate its business models by developing specialized pharmacies for chronic diseases, dermo-cosmetic specialty stores, and other formats. It provides services such as health monitoring, device-based rehabilitation, extended medical care, and chronic disease management to meet the diverse health service needs of consumers. Meanwhile, reforms in medical insurance payment methods, the entry of cross-industry capital, and the growth of pharmaceutical e-commerce have intensified competition in the drug retail industry.

In terms of regional market focus, Yixintang continued to deepen its presence in the Sichuan-Chongqing region by further expanding its chain of directly operated stores and optimizing its network layout. By the end of the reporting period, the number of stores had exceeded 1,400. In the Sichuan-Chongqing area, the company pursued in-depth expansion through self-built outlets and fragmented acquisitions, continuously optimizing store distribution and product mix. These efforts enhanced Yixintang’s brand influence, strengthened sales capabilities and profitability, and increased its market share in the local market.

· The General Public

During the reporting period, Laobaixing steadily expanded into lower-tier markets. In response to the characteristics of different market segments, the company pioneered a unique M&A strategy: acquiring controlling stakes in regional leading pharmaceutical retail chains while retaining partial equity for the original founders (referred to as the “Spark” model). The franchise model has also been continuously refined and strategically deployed. Regarding “Spark”-style acquisitions, expansion into third-, fourth-, and fifth-tier cities was achieved in the third quarter, with county- and city-level stores accounting for approximately 70% of the Group’s total, reflecting a rapid pace of market penetration. In terms of franchising, Laobaixing ensures the quality, efficiency, and productivity of franchise stores through high-standard management based on the “Seven Unifications” and 100% product distribution. Digitalization and new retail are also key areas of strategic focus for the company. Laobaixing has continued to strengthen its dual-speed IT organizational structure, which is now well-established, with relevant teams fully in place. Aligned with its digital transformation objectives, the company consistently leverages business digitalization to optimize its overall operational system.

Furthermore, the development of pharmaceutical care service systems is also a key initiative advanced by LBX Pharmacy. Currently, the company has trained 5,163 chronic disease management specialists and installed Bluetooth-enabled testing devices in 5,016 stores. All data are uploaded in real time, allowing customers to access their chronic disease records via the “LBX Medication Consultant” feature on LBX Pharmacy’s WeChat platform.

· Dashenlin

Dasenlin continues to penetrate the secondary and tertiary markets in its established regions while simultaneously exploring new markets in key areas by opening new stores, pursuing mergers and acquisitions, and expanding its franchise network. The company is constantly expanding the scale of its retail channel brand to enhance competitiveness and maintain its scale advantage. Meanwhile, Dasenlin has been deepening its development in the wholesale sector, cultivating clients across various levels of the pharmaceutical industry. It focuses on distributing general agency products and private-label brands, complementing its business with circulating product lines to meet clients’ operational needs. Furthermore, the company is making in-depth strides into the big health industry as a core strategic priority for its operations.

Regionally, Dashenlin has deeply cultivated the South China market and achieved high growth rates in Northeast, North, Northwest, and Southwest China, with revenue growth reaching 71.37%. Overall, the company’s development across various regions is largely balanced. It has actively implemented an expansion strategy outside its home province, sustaining growth in Northeast, North, Northwest, and Southwest China, primarily driven by sales contributions from store acquisitions.

· Yifeng Pharmacy

Yifeng Pharmacy has adopted an expansion model centered on “new store openings, mergers and acquisitions, and franchising,” focusing on growth to continuously enhance the breadth and depth of its store network coverage. By implementing a controlled premium product strategy and optimizing its product mix, the company has built a supply chain system with controllable online and offline channels and pricing. Through the integration of business operations with IT systems and the digitization of core processes, Yifeng has established an efficient and agile digital operational framework. Leveraging intelligent omnichannel service transactions, the company is capturing outpatient prescription outflows from hospitals and driving innovation in the broader health and wellness sector, thereby achieving a comprehensive upgrade of its business model.

As the competitive landscape evolves, the era when a single advantage could guarantee widespread success is gone; only enterprises with strong comprehensive competitiveness can secure a foothold amidst intense market consolidation. Beyond the strategic moves already undertaken by dominant chain giants, competition among small and medium-sized pharmacy chains is also intensifying.

In 2021, the capital market remained turbulent. To date, six pharmacy chains, including Dingdang Kuaiyao, Quanyuantang, Huaren Health, Sipay Health, Yuanxin Technology, and Dajiaweikang, have publicly filed their prospectuses, with IPOs scheduled. From the current perspective, this undoubtedly marks a new wave of listings in the pharmaceutical retail sector. Why are these pharmacy chains rushing to go public? “For some small and medium-sized pharmacy chains, the path forward is clear: to achieve growth and scale, they must either pursue specialization to strengthen and expand or face acquisition,” an anonymous source from Haoyaoshi Pharmacy told VCBeat. This suggests that joining forces to increase scale, leveraging the listing wave to align with larger companies on the capital market journey, and then breaking through independently may be the only way to build sufficient resilience against shocks and volatility in the pharmaceutical industry.

Currently, regional competition among chain pharmacies remains pronounced. For retail pharmacies, in the internet era, customers can compare prices and make purchases across various online channels anytime and anywhere, making it nearly impossible to build customer loyalty through price competition alone. However, a differentiated brand image ensures that customers think of the pharmacy first when needs arise, thereby helping enterprises establish customer loyalty and constituting a true core competitive advantage. “At present, some regional pharmacies enjoy greater brand advantages, with higher public trust in their brands; thus, implementing regional monopolies has become an existing developmental advantage for these enterprises. Nevertheless, the impact posed by online pharmacies cannot be overlooked,” said the aforementioned industry insider.

It is worth noting that, against this backdrop, independent pharmacies may face increasingly difficult conditions. Based on the high-quality development target of achieving a retail chain affiliation rate close to 70% by 2025, and using the current base of 561,000 pharmacies for projection, the number of independent pharmacy outlets is expected to shrink to 168,300 over the next three years. This represents a sharp decline of nearly 80,000 stores compared to the current figure of approximately 250,000.

In recent years, independent pharmacies have long been on the path to obsolescence, with this trend only accelerating. Data shows that in Guangdong Province, the number of pharmacies having their Drug Operation Licenses revoked has grown rapidly over the past three years: a total of 450 licenses were revoked in 2019, 1,229 in 2020, and 2,163 by September 2021. Beyond Guangdong, announcements regarding the revocation of Drug Operation Licenses were issued in Henan, Sichuan, Shaanxi, Yunnan, and other regions during the first half of this year, marking the exit of a large number of pharmacies from the market. What harsh realities are the current 250,000-plus independent pharmacies facing?

From the perspective of both internal and external environments, independent pharmacies are experiencing significant anxiety due to aggressive expansion by large and medium-sized chain competitors, stringent national policies regulating business operations, and inherent deficiencies in their own soft and hard capabilities.

In terms of external competition, the penetration of products and services into grassroots markets has become a trend. Major listed pharmacy chains are leveraging capital to accelerate mergers, acquisitions, and franchising, actively vying for market share in fourth- and fifth-tier cities. Furthermore, cross-regional and local chains are also making strides in grassroots markets to expand their spheres of influence. Meanwhile, pharmaceutical e-commerce platforms and cross-industry competitors are entering the fray, seeking to capture a share of the drug retail market.

In terms of national policy, regulatory oversight by the National Healthcare Security Administration and the National Medical Products Administration over pharmacy operations has become increasingly stringent. Measures such as the implementation of the revised Drug Administration Law, the institutionalization of unannounced inspections and targeted rectification campaigns for pharmacies, and the continuous regulation of licensed pharmacists have all heightened the compliance pressures on independent retail pharmacies.

In terms of their own capabilities, due to their small scale, single-store pharmacies are more commonly found in county, township, and rural markets, and they tend to be lacking in professional service quality, operational standardization, customer attraction and sales promotion effectiveness, and channel bargaining power.

Amid the overarching trend of pharmacy chain consolidation, the survival prospects of independent pharmacies are a cause for concern. It has been suggested that independent pharmacies face only three options: closing down, being acquired, or joining a franchise. According to industry insiders, some independent pharmacies have become target candidates for chain pharmacies. These chains initially provide financial support, software solutions, and various services to help independents reduce costs. After nurturing their growth to a certain stage, the chains further expand their business models by merging with or acquiring these pharmacies.

However, independent pharmacies that have survived to this day may surpass chain stores in certain aspects, such as specialized services and on-site Traditional Chinese Medicine (TCM) consultations. Although their market share continues to shrink, those with distinctive expertise have already established strong local brands. Most of them attract a loyal customer base through business models like on-site TCM consultations and outpatient services, achieving considerable sales revenue and gross profit margins. Suzhou Yuehai Pharmacy and Shanghai Qunli Herbal Medicine Store are undoubtedly representative examples in this regard.

If a model could enable independent stores to retain their own brands while securing support from industry leaders to navigate policy changes, it would be an ideal solution with strong potential for long-term sustainability.

Independent pharmacies lack both the dense distribution network of chain pharmacies and the low drug prices offered by discount pharmacies. Faced with such intense competition from numerous pharmacies, what innovations should independent pharmacies implement to secure a foothold in the pharmaceutical industry? In a market environment where overall disadvantages outweigh advantages, how can independent pharmacies enhance their competitiveness and avoid being easily eliminated?

In this regard, we can make the following assumption:

I: Independent pharmacies choose to join pharmacy chains to gain support in sales channels, product procurement, and enterprise management, thereby securing fundamental survival guarantees and building capacity for long-term development.

II: Independent pharmacies will position themselves as specialty pharmacies by strengthening internal capabilities, leveraging their inherent advantages, and identifying unique characteristics to achieve long-term, stable, and sustainable growth.

III. Independent pharmacies are attempting to leverage the internet to explore new development models. In short, they must either continue to expand and develop into chains, undergo transformation and upgrading, or seek external partnerships and form alliances.

Overall, driven by policy incentives and market development trends, the pharmacy industry is entering a phase of transformation and upgrading. As policies governing mergers, acquisitions, and restructuring continue to be simplified, optimized, and normalized, chain consolidation among pharmacies will become an inevitable trend. Consequently, the number of independent pharmacies will continue to decline, with mounting pressure on their survival.