Billions in Capital Inflows Drive Five Profitable Scenarios in Healthcare Big Data | 2021 Year-End Review

On November 30, 2021, the Ministry of Industry and Information Technology issued the “14th Five-Year Plan for the Development of the Big Data Industry,” which not only set a growth target of “breaking through 3 trillion yuan in estimated scale of the big data industry by the end of 2025,” but also proposed new objectives such as establishing a data element value system and a modernized big data industrial system. Among these development goals is the need toCultivating the Big Data Trading Market。

Looking back, the development of the medical big data industry can be traced to the “46312” project formulated by the National Health and Family Planning Commission seven years ago. Its fundamental purpose was to standardize medical data infrastructure and transform “vast amounts of medical data” into usable “medical big data.”

At that time, riding the wave of policy support, a large cohort of next-generation healthcare IT companies branded as “medical big data” emerged. Their objectives were twofold: first, to help hospitals establish the foundational infrastructure for big data analytics; and second, to unlock the potential value of big data by developing medical big data applications tailored to specific scenarios.

After several years of development, this cohort of big data enterprises born out of policy support has reached the stage of initial public offerings (IPOs) or pre-IPO phases. Data from the VCBeat Orange Database shows that among the 948 informatics-related companies established between 2014 and 2016, 24 have advanced to Series C funding rounds or beyond.

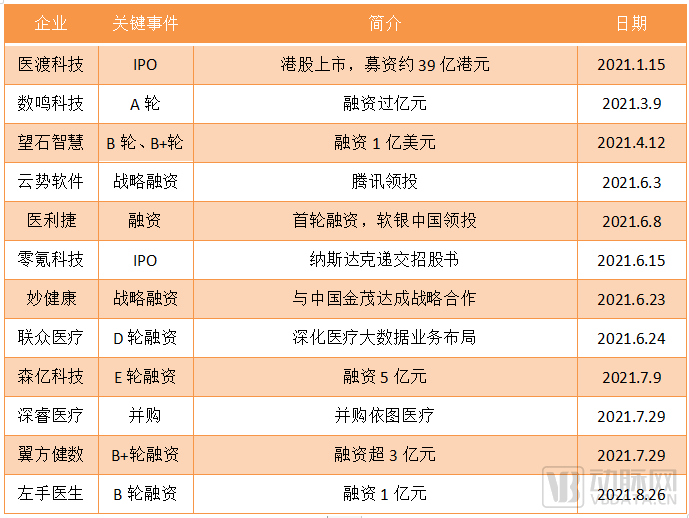

New capital continues to flow into this sector. In the first ten months of 2021 alone, the medical big data sector witnessed 10 financing rounds, eight of which exceeded RMB 100 million.

2021 Healthcare Big Data Financing Overview

2021 Healthcare Big Data Financing Overview

Five Years into the Boom: How Well-Prepared Is Medical Big Data? Has Adoption of Related Applications Become Widespread? What Opportunities Lie Within Each Segment? To Address These Questions, VCBeat Conducted a Survey of Nearly 20 Companies in the Big Data Sector and Attempts to Provide Answers.

The essence of medical big data lies in the organization and reuse of healthcare data; therefore, the first step is to establish a data center within healthcare institutions to store vast amounts of medical data.

General hospitals, due to their limited data storage capacity, typically establish server rooms within the hospital premises, primarily adopting a self-built infrastructure model. In contrast, provincial-level regional data centers need to aggregate data from various locations and usually opt for leased facilities or cloud services for data storage.

According to the data from the “National Health Informatics Survey Report” released by the Statistical Information Center of the National Health Commission in 2021, in terms of hospital informatization, 98.8% of tertiary hospitals and 96.1% of secondary hospitals in China have established data center server rooms; in regional medical informatization, all provincial-level health commissions possess data and central server rooms, and 82.3% of municipal-level data centers have server rooms.It can be said that the “framework” of China’s medical big data has been largely established.

So, has the market for big data infrastructure development entered a red ocean? The answer is no.

Three Key Pathways to Choose From.First, as data storage volumes continue to accumulate over time, the physical footprint required for server rooms will inevitably increase; therefore, institutions that already possess data centers still face the need for capacity expansion.

The value of this business segment can be gleaned from Wanda Information’s public health orders this year. On April 23, Wanda Information won the bid for the “National Healthcare Security Administration Data Center Server Room and Communication Infrastructure Leasing Project,” with a winning bid price of RMB 38.66 million. On April 25, it secured the “Construction Project of the Public Service Zone A in the Data Center of Tianjin Municipal Healthcare Security Administration’s Healthcare Security Information Platform,” with a winning bid price of RMB 38.8558 million. For county- and city-level data centers, as well as capacity expansion projects at tertiary hospitals, the average transaction value is relatively lower, with tender prices generally ranging from several million to RMB 10 million.

Second, the existing market still requires time to be absorbed.The “Basic Standards for Medical Service Capacity of County Hospitals” and the “Recommended Standards for Medical Service Capacity of County Hospitals,” issued by the General Office of the National Health and Family Planning Commission in 2016, explicitly identified data center construction as a key component of county-level hospitals’ service capabilities. Data indicate that while data center infrastructure has largely taken shape at county hospitals (secondary level or above), only 59.0% of county health commissions have their own data centers. Among hospitals, excluding secondary and tertiary institutions, 24.5% still lack data centers. From initial establishment to subsequent expansion, there remains untapped market potential in data center construction.

Third, cloud leasing may become a new source of market growth.According to data from the “National Health Informatics Survey Report,” over 90% of hospitals included in the statistics have self-built data centers, with less than 10% having migrated to the cloud. In contrast, among regional health commissions, nearly 60% at the provincial level, nearly 40% at the municipal level, and nearly 20% at the county level have adopted cloud-based solutions.

Xu Xiangdong, Deputy Director of the Information Technology Division at the Statistical Information Center of the National Health Commission, once stated that the center has structured its next-generation data center into three tiers: first, the infrastructure tier, which supports cloud data center construction and corresponds to the IaaS layer; second, the support tier, encompassing concepts such as business middle platforms and data middle platforms; and third, the application tier, focused primarily on integrating existing applications and developing new ones.

In short, the future direction of data center construction will shift from physical server rooms to virtual cloud spaces to cope with the growing pressure of data storage. More importantly, the value of medical data storage lies in its potential future applications. From this perspective, leased cloud services will unlock an immeasurable market space.

Data centers are established to store data in a complete and comprehensive manner; however, storage is merely a tool, while data mining and ultimate application constitute the final objectives of informatization development. To this end, hospitals must overcome the two major constraints of data quality and data mining.

Over two decades of unbridled growth in healthcare IT have driven digital transformation in hospitals, while also leaving behind numerous persistent challenges. From a macro perspective, the pain points associated with medical data generally includeThe proliferation of IT vendors and systems has led to severe data silos, making data governance highly challenging; low levels of data standardization result in inefficient data governance for hospital administrators; high pressure on clinical research is coupled with low efficiency in producing research outcomes.Three aspects.

Next is data mining. Traditional data mining primarily integrates data from common hospital information systems, such as the Hospital Information System (HIS), Laboratory Information System (LIS), Picture Archiving and Communication System (PACS), Radiology Information System (RIS), and pathology systems, to establish common databases like Electronic Medical Record (EMR) systems, Clinical Data Repositories (CDR), and electronic Medication Administration Records (eMAR). However, in practice, these databases often fail to meet the diverse needs of researchers.

Wang Minhui, Senior Vice President of Huazhuo Technology, told VCBeat: “Traditional big data applications are driven by business needs. One day a doctor has an idea, and the next day another department raises a request. Without platform support, every request that exceeds the capabilities of conventional databases requires the IT department or the enterprise to undergo time-consuming and labor-intensive processes of data collection and cleaning. In contrast, a platform-based approach enables unified data governance processes and addresses ad-hoc, non-systematic demands through a systematic mindset.”

Theoretically,Medical Big Data PlatformIt can to some extent address the aforementioned two issues.

The essence of a platform is service. A so-called medical big data platform can be viewed as a suite of services provided throughout the entire lifecycle of medical big data utilization, including data acquisition, integration, processing, modeling and analysis, and visualization. In practice, health IT vendors typically integrate multiple big data processing tools into a single system, which is what we commonly refer to as a big data platform.

The medical big data platform, established in accordance with hospital requirements and organizational structure, incorporates SSD storage technology, integrates the Hadoop platform, utilizes data warehouses such as Oracle and Sybase, and employs parallel processing database technologies including MPP and MapReduce.Hospitals can leverage the platform’s engine and models to process stored data at scale, thereby addressing the issues of information silos and low data standardization prevalent in Chinese hospitals. Based on this platform, developers can directly access data to build disease-specific databases according to hospital requirements, thus resolving the challenges of high research investment and low efficiency in hospital-based scientific research.。

Meanwhile, as data storage continues to migrate to the cloud, some healthcare IT companies are also promoting cloud deployment of big data platforms. For instance, Huazhuo Technology has adopted an internet-based cloud computing architecture to build its big data platform, meeting hospitals’ needs for either on-premises or cloud deployment through parallel support for public, private, and hybrid clouds.

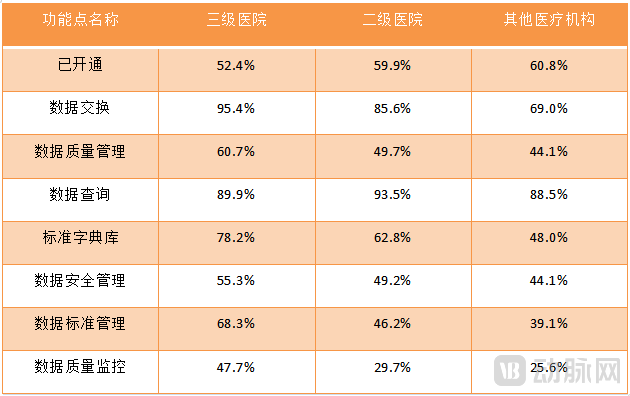

Due to the inherent technological convergence characteristics of medical big data platforms, there are currently no clear statistical data available on the deployment status of such platforms across hospitals. However, market trends can be inferred from statistics on the basic functionalities of hospital information systems presented in the “National Health Informatization Survey Report,” as detailed in the table below.

Construction Status of Basic Functional Points for Hospital Information Platforms (Data Source: National Health Informatization Survey Report)

Statistics on the implementation of basic functional modules of hospital information platforms reveal significant disparities in medical big data processing capabilities across hospitals, although more than half have deployed certain functionalities. To address deficiencies in various areas (which are typically scattered across different business systems), some hospitals have begun seeking comprehensive, one-step solutions by directly procuring medical big data platforms.

According to estimates by Collibra, a medical big data enterprise, the contract value for a single hospital-based big data platform construction project ranges from RMB 5 million to RMB 8 million, with some large-scale projects exceeding RMB 15 million per contract. The total market size exceeds RMB 20 billion.

Notably, the tender amounts for certain in-hospital big data platforms can reach as high as RMB 20–30 million. This is because hospitals often require the deployment of specific applications alongside platform construction, thereby further enhancing the value delivered by the platform vendors.

However, the significance of large-scale healthcare data platforms to the industry extends beyond mere data management. As data infrastructure continues to mature, the “Ark” naturally sails toward the vast frontier of big data applications in healthcare.

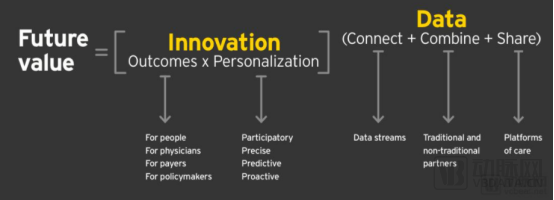

EY’s “Life Sciences 4.0 Report” once used FV=IDDescribe the Future Value of life sciences, where future value equals “innovation” raised to the power of “data.”

In simple terms, if an “invisible hand” could collect, organize, and share data from patients, physicians, payers, and policymakers, and then apply it to precision medicine, disease prediction, healthcare cost containment, and other medical services, the value of such data would be immeasurable.

The Future Value of Life Sciences Equals “Innovation” to the Power of “Data”

It is no easy task to classify applications of medical big data. Operational, clinical, research, health-related, and vast amounts of hard-to-categorize data each conceal enormous market potential.

The most frequently utilized data in hospitals currently isClinical DataApproximately 21.9% of tertiary hospitals have initiated application research and development based on such data, presenting significant opportunities for corporate involvement. For instance, AI-assisted diagnosis for imaging and knowledge graph-based Clinical Decision Support Systems (CDSS) for text analysis have been widely implemented in hospitals. In the realm of Real-World Studies (RWS), regulatory authorities have incorporated real-world evidence into approval submissions.

Taking Ping An Intelligent Auxiliary Diagnosis and Treatment Information System, under Ping An Smart Healthcare of Ping An Smart City, as an example, the system leverages a comprehensive knowledge base encompassing diseases, drugs, prescription treatments, and clinical guidelines. This knowledge base is built upon more than 100,000 clinical practice guidelines, hundreds of thousands of drug knowledge entries, tens of millions of medical literature articles, millions of real-world data records, and thousands of classic case studies. By integrating diagnostic models, treatment models, disease prediction models, and clinical experience rules developed through big data and artificial intelligence technologies, the system supports multi-level application scenarios across the entire healthcare process.

In terms of application, the system centers on supporting clinical diagnosis and treatment workflows, seamlessly integrating into physician workstations to provide intelligent information assistance across the entire process—from consultation, diagnosis, and examinations to laboratory testing and treatment. It features functions such as intelligent clinical decision support recommendations, real-time clinical alerts, clinical knowledge retrieval, and disease risk prediction, thereby enhancing healthcare management and service capabilities.

Currently, Ping An’s Intelligent Auxiliary Diagnosis and Treatment Information System has been deployed across 10 provincial-level administrative regions and more than 20 cities throughout China, covering nearly 40,000 healthcare institutions at all levels, including hospitals, community health service centers, township health centers, village clinics, general clinics, and infirmaries. Ping An Smart Healthcare’s AskBob Doctor Station serves over 1 million physicians, providing a professional medical search engine, industry platforms, clinical decision support tools, as well as medical education resources and consultation services.

In addition to intelligent assisted diagnosis and treatment, Ping An Smart City has made significant achievements in medical supervision. The Ping An Smart Healthcare Clinic Supervision and Service Integrated Platform has extended its supervisory coverage to over 5,000 clinics in Shenzhen. During its first year of operation, the platform monitored more than one million patient visits, issued over 13,000 risk alerts, and facilitated corrective actions in more than 2,000 clinics. In early 2021, the Guangdong Provincial Health Commission and Ping An Smart Healthcare jointly developed the Guangdong Province “Epidemic Sentinel Information Management System.” This system covers all 21 prefecture-level cities in Guangdong Province, encompassing 18,000 healthcare institutions and a registration system for 25,000 physicians. By leveraging information technology, the system not only integrates private clinics into the epidemic prevention and control network—highlighting their importance in primary healthcare and as epidemic sentinel points—but also enables tracking and management of febrile patients identified through sentinel monitoring, thereby fulfilling the critical sentinel role of private clinics.

In the specialty sector, companies such as Huimei Technology and Senyi Intelligence have developed relatively mature applications. Huimei Technology’s intelligent VTE prevention and control system effectively enhances hospital-based assessments of VTE risk and bleeding risk, facilitates single-disease data reporting, and has been successfully implemented in more than 300 hospitals. Its rated version of the Clinical Decision Support System (CDSS) has also helped over 100 hospitals achieve high-level accreditation in “Electronic Medical Records” and “Interconnectivity” evaluations.

Four Major Categories of Stakeholders in the CDSS Product Landscape

Four Major Categories of Stakeholders in the CDSS Product Landscape

Hospital'sOperational DataIt can effectively facilitate collaborative decision-making among hospitals, regional health systems, and public health agencies. For instance, DRG-based payment serves as an incentive mechanism established around hospital operations, while hospital dashboards enable self-optimization by hospitals leveraging big data.

Hospitals typically do not need to generate separate orders for the management of operational data. Companies such as Yilianzhong and Heyu Health integrate this function into the development of medical consortia and medical alliances, assisting hospital administrators in managing information related to personnel, consumables, performance metrics, patient disease profiles, and geographic distribution of cases.

Health DataIt represents the largest and most promising data asset, yet it remains the area with the most limited current application; fewer than 10% of hospitals have developed applications leveraging health data.

An analysis of the underlying reasons reveals that while Internet of Things (IoT) devices have enhanced hospitals’ collection of patient health data, there is limited research integrating health data with clinical data, thereby undermining the persuasiveness of health data.

Fortunately, as the world’s largest market for chronic disease management, the rise of “Internet + Chronic Disease Management” is reshaping the value of this sector. At this juncture, new entrants include internet giants such as Baidu, JD.com, and Alibaba.

Fusion of Multimodal DataIt also possesses its unique value, with big data epidemic prevention platforms being an increasingly popular application in the past two years.

The Zhuhai Public Health Emergency Management Platform, which recently won the “Anping Award” in the China region of the 2021 World Smart City Awards, is a prefecture-level public health monitoring and early warning platform built by Ping An Smart City and the first of its kind to go live in Guangdong Province. Tailored to Zhuhai’s local characteristics, the platform fully integrates four major monitoring channels—municipal hospitals, the disease control system, the 120 emergency center, and nucleic acid testing—and has established seven early warning systems, including syndrome surveillance, multi-point trigger reporting for COVID-19, and pharmaceutical monitoring, thereby leveraging technological capabilities to achieve precise epidemic prevention and control.

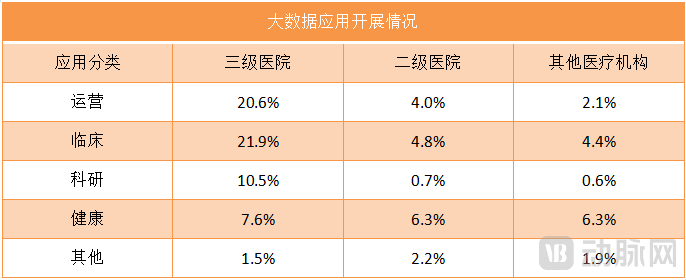

Overall, although data constitutes the most valuable component of the entire medical big data chain, its value has not been fully tapped from the perspective of application development.

Status of Big Data Applications in Various Hospitals (Data Source: "National Health Informatization Survey Report")

However, from another perspective, health and scientific research big data, which have not yet been fully utilized, present certain barriers to entry while also offering a vast market potential that is difficult to estimate.

Although the value extraction from medical big data follows three processes—storage, governance, and application—from the perspective of its usage workflow, in practical applications, governance and application can exist independently or be combined to directly serve the main entities.It is worth noting that enterprises focused on applications may not necessarily transition to building platforms, whereas platform-centric enterprises are increasingly expanding into the application space.

“The development of our medical big data platform will proceed in three steps. The first step is to promote digital transformation in hospitals and leverage the big data platform to optimize hospital management. With accumulated data, we will develop AI solutions for specific diseases on the platform, thereby advancing specialization in clinical departments and disease-specific care,” said Wang Minhui from Huazhuo Technology. “Once these foundations are established, we will extend our applications to patients, using big data to optimize their disease management.”

Meanwhile, hospitals and enterprises must establish a mutually beneficial partnership. For hospitals, the platform offers not only stability and scalability but also supports “hot-swapping” of various applications. Under this arrangement, hospitals possess both the capability to utilize applications and the autonomy to select them. For enterprises, leveraging the platform as a foundation facilitates subsequent application development, ensuring that the final products are better integrated with the platform and deliver an enhanced experience for hospitals.

However, from the perspective of the Information Technology Department, the medical big data platform ensures the effective development of applications by platform providers, facilitating clinical research for physicians. Nevertheless, for other vendors within the hospital, these data remain opaque and unshared, meaning that developers still face the issue of re-cleaning data when processing applications.

Amid these complex challenges, the concept of the “data middle platform” has begun to extend from the financial and e-commerce sectors into healthcare informatics as a new approach to addressing longstanding issues.

A Data Middle Platform is a sustainable mechanism designed to “put enterprise data to work.” It represents a strategic choice and organizational model that, tailored to an enterprise’s unique business model and organizational structure, establishes a continuous process for transforming data into assets that serve business operations, supported by tangible products and implementation methodologies. This concept was initially proposed by Alibaba for application in e-commerce and, due to its effectiveness, has gradually become a standard component in this field.

Unlike data middle platforms in the e-commerce and financial sectors, Huimei Technology’s data middle platform allows hospitals to import various types of raw data. The platform automatically standardizes these data, generating a data map to facilitate subsequent applications and retrieval.

However, the innovation of a data middle platform lies not only in its functionality. Wang Shi, CTO of Huimei Technology and a former Alibaba employee, stated, “Hospital data middle platforms emphasize real-time data management and application, as well as centralized governance and internal data transparency. In many cases, medical data is stored within vendors’ proprietary architectures after collection, leading to hospitals being ‘held hostage’ by healthcare IT vendors. The role of the data middle platform is to reclaim control over data management,”Return to the Information Technology Department.”

The transformation of the information management role is critically important. Although hospitals possess big data platforms, they still need to engage corresponding IT vendors for research purposes, specifying their data requirements and relying on these vendors to execute data extraction and processing. However, if data management authority is vested in the Hospital Information Department, the department can provide APIs and deliver the specific data requested by vendors as needed. This approach offers three key benefits: first, it reduces the costs associated with repetitive data cleaning; second, it resolves the problem of data silos caused by incompatible interfaces; and third, it enhances the development efficiency of healthcare applications.

Huimei's Big Data Middle-Platform Solution

Currently, the average transaction value for hospital procurement of data middle platforms stands at approximately RMB 10 million, indicating that the market is still in its early stages. However, from the perspective of healthcare informatization development, as hospitals progressively meet national accreditation standards and strive for higher ratings, the application of data middle platforms becomes increasingly critical.

“Lower-level ratings focus only on the overall compliance of data quality, whereas higher-level ratings, as well as current data reporting requirements, demand that hospitals isolate data quality for dedicated review and implement more refined management,” said Wang Shi.

The key to winning in the healthcare informatization sector lies in grasping the future trajectory of policy development. From the current perspective, middle-platform-related companies such as Huimei Technology and Winning Health have already played a strong hand in the early stage of the market.

To maximize the value extracted from clinical data, it can, on one hand, help physicians optimize clinical pathways and select superior treatment modalities; on the other hand, it can foster collaboration between hospitals and pharmaceutical/medical device manufacturers as well as insurance companies, thereby facilitating the development of new drugs and medical devices and promoting commercial insurance coverage for conditions excluded from basic medical insurance.

Cancers with persistently high incidence rates are a key focus of collaboration between hospitals and pharmaceutical and medical device companies. Currently, there is an urgent clinical demand for innovative drugs and treatment regimens represented by precision medicine. However, the reality is that precision medicine has made traditional research increasingly challenging, R&D costs for new drugs continue to rise, and market approval processes remain slow, leading to the current problems of high drug prices and limited patient access. These challenges have driven AI and big data companies to intervene, serving as a bridge between pharmaceutical/medical device enterprises and hospitals.

LinkDoc, a healthcare technology enterprise, is among the pioneers in exploring commercialization within this sector. Taking its LinkSolutions precision life sciences solution as an example, the real-world studies (RWS), clinical trial recruitment, and data insights included in the solution can, to a certain extent, address the aforementioned challenges.

Powered by AI, LinkDoc Technology leverages its data integration and analytics capabilities to conduct in-depth mining of structured knowledge graphs. By analyzing corporate market conditions and drug efficacy, it helps enterprises identify the most suitable clinical scenarios for their pharmaceuticals, thereby facilitating effective post-marketing development and ultimately benefiting patients. This approach minimizes marketing costs for enterprises, redirecting investments toward the generation of clinical evidence. Based on high-level evidence, it further supports the continuous development of new indications for drugs, uncovering more “aspirin-like” opportunities.

Patient recruitment has long been a bottleneck in clinical trials, with the pace of clinical research largely dependent on the speed of patient enrollment. As oncology drug therapies become increasingly precise, the pool of suitable candidates for each medication shrinks, making patient screening more challenging. Therefore, measures must be taken to accurately identify and match eligible patients. Traditional recruitment channels are inefficient and have limited reach, making it difficult to quickly connect new drug development projects with truly needy, well-matched patients. Leveraging healthcare big data to achieve precise project-patient matching is currently the most efficient and viable pathway for development, which constitutes the core value of LinkDoc Technology.

Collinbrew is also actively exploring commercial pathways within insurance companies and pharmaceutical and medical device enterprises. In its collaborations with insurers, the company can assist in the design of commercial health insurance coverage, actuarial pricing, claims operations management, healthcare provider network management, as well as market and sales expansion. For pharmaceutical companies, Collinbrew helps analyze drug efficacy, enabling R&D-focused pharmaceutical firms to obtain broad, real-world data on patient treatment outcomes, thereby assessing directions for new drug research and investment.

By providing B2B services to pharmaceutical companies and insurance firms, medical big data enterprises can generate annual revenues of up to RMB 4 million from digital analysis reports purchased by a single pharmaceutical manufacturer, and up to RMB 10 million from those purchased by a single insurance company. Roughly calculated, this points to an underlying market worth nearly RMB 100 billion per year.

Despite its substantial value, the development of medical big data has not been smooth. In many contexts, medical big data is even regarded as a sensitive term.

Data security and cybersecurity are the primary challenges facing medical big data. The inherent value of medical big data often attracts intense interest from various parties. Hangzhou Meichuang Technology told VCBeat:“Level Protection 2.0” has promoted the development of data security, but information security is a game between intruders and defenders; there is no absolute security, only continuously evolving defensive measures.

Cybersecurity is also a key area of focus for hospital development. A well-known hospital was attacked after migrating its information systems to the cloud, sparking distrust in cloud storage within the industry.

However, from the perspective of technological development, every approach has its limitations and requires growth through exploration. Rather than succumbing to fear, relevant authorities should establish robust crisis response mechanisms to prevent potential risks and foster the healthy development of technology.

Next are the issues of privacy and ownership. Compared to the previous issue, this one has a lower technical threshold, primarily requiring managers to establish protective mechanisms and users to enhance their awareness of protection.

In specific patient medical records, basic information such as the patient’s name and ID number is often used as a unique identifier. However, this information also falls under the category of data that requires protection. Therefore, the correct approach is to anonymize the data to ensure privacy without compromising its accuracy.

Meanwhile, different types of information hold varying value in privacy protection. Therefore, applying high-level protection measures uniformly to all medical information would impair the efficiency of practical applications and result in resource waste. Hence,Hospitals should establish a robust data classification system and implement differentiated protective measures for different categories of personal information and data.

Finally, there is the issue of ownership. The current legal system is not yet able to adequately explain and define the ownership rights of health and medical data, particularly the ownership of medical data. In practice,There is a controversy over whether the ownership of medical big data belongs to individual patients or hospitals.

Some argue that medical big data reflects an individual’s health status and should therefore belong to the patient. Others contend that since medical big data is generated through collection and entry by hospitals, and stored and maintained within healthcare institutions, it should rightfully belong to these institutions. A third perspective holds that ownership of medical data lies with the individual patient, control rests with the hospital, and management authority resides with the government; third-party entities can only commercialize and utilize such data with government support and hospital cooperation.

In practical applications, ownership of medical big data essentially resides with hospitals. The ambiguity surrounding the ownership of medical data not only hinders the authorized use of health and medical data but also poses challenges and creates hidden risks for the protection of patients’ personal information rights.

The convergence of these three issues has resulted in the current state of the medical big data industry, characterized by rapid infrastructure development but slow application. Although the National Health and Medical Big Data Northern Center was established years ago, data access is restricted to authorized use under the National Health Commission due to security concerns.

Nevertheless, the construction of big data trading markets, as outlined in the “14th Five-Year Plan for the Development of the Big Data Industry,” will inevitably drive the improvement of trading infrastructure. In this light, the ultimate goal of data infrastructure development must be application; once critical thresholds are crossed, medical big data may usher in a new era within five years.