Orthopedic Robotics Surge Amid National Volume-Based Procurement: Capital Inflows and Strategic Layouts by Hillhouse and Sequoia

2021: A Year of Qualitative Transformation for Orthopedics

With the implementation of volume-based procurement (VBP) for traditional orthopedic consumables, the previously high gross profit margins of premium medical devices have been significantly compressed. According to the results of the government-organized centralized procurement negotiations in 2021, the average price of artificial joints under national-level VBP decreased by 82%, while the average price reduction for orthopedic trauma consumables across twelve provinces reached nearly 90%. The traditional market for high-value orthopedic consumables, once valued at tens of billions of yuan, has been substantially shrunk.

Facing the winter chill, leading domestic orthopedic companies have successively undertaken technological upgrades, forged supply chain partnerships, and pursued mergers and acquisitions to weather the downturn together. As the orthopedics market undergoes structural transformation, astute investors are strategically focusing on the digitalization of orthopedic surgery, heavily backing technology-driven innovators represented by orthopedic surgical robots.

Global giants are actively positioning themselves in this sector through acquisitions exceeding $1 billion and intensifying their promotional efforts in the Chinese market. Notable systems already approved for sale in China include Stryker’s Mako RIO, Medtronic’s Mazor X, and Zimmer Biomet’s MEDTECH ROSA ONE.

Domestic giants are also vying to capitalize on this sector. MicroPort Scientific and Weigao Medical have both established a presence in orthopedic surgical robotics, with MicroPort’s robotics subsidiary recently going public and achieving a market capitalization exceeding RMB 50 billion. Recently, medical imaging company United Imaging Healthcare has also entered this arena.

According to statistics from VCBeat (WeChat ID: vcbeat), multiple companies in the digital orthopedic surgery sector have completed new rounds of financing, with amounts reaching the hundred-million-yuan level. Participating investors include well-known firms such as Hillhouse, Sequoia, and CDH Investments.

However, in stark contrast to the fervor in the primary market, the commercialization of orthopedic surgical robots in China is far from optimistic.

The penetration rate of orthopedic surgical robots in China is relatively low,As of December 31, 2020, only 17 joint replacement surgical robots had been installed in China, with a penetration rate of robot-assisted joint replacement surgeries at 0.1%. In comparison, the United States had installed 1,060 joint replacement surgical robots, with a penetration rate of 7.6%. (Data source: Frost & Sullivan)

Not many orthopedic surgical robots that have been launched in the Chinese market have truly gained widespread clinical recognition.Clinicians remain cautious in their perception of orthopedic surgical robots. Industry experts believe that current digital orthopedic solutions are limited to a narrow range of surgical procedures and are prohibitively expensive, preventing their widespread adoption in China’s complex orthopedic market.

As the orthopedics market turns a new page with volume-based procurement, digital platforms in orthopedics are ushering in unprecedented development opportunities. Why have intelligent orthopedic surgical products attracted hundreds of billions of yuan in investment? Which companies and products will emerge as winners in this sector? VCBeat (WeChat ID: vcbeat) has conducted a comprehensive review of this landscape.

The digital empowerment of physicians is commonly metaphorized as comprising three components: the “hand” (robotic arm), the “eye” (navigation), and the “brain” (AI).

Among these, the key focus of laparoscopic surgical robots is to empower the surgeon’s “hands.” The da Vinci laparoscopic surgical robot primarily assists surgeons in performing procedures within confined spaces, thus imposing stringent requirements on the design and control of robotic arms to minimize hand tremors.

The key focus of digital orthopedic surgery systems is to empower the surgeon’s “brain” and “eyes.”

In the specialized field of orthopedic surgery, the primary requirements for trauma surgery are precise reduction and fixation; the core requirement for joint surgery is accurate osteotomy; and the central need for spinal surgery is also fixation. For clinicians, the “brain” refers to exceptional proficiency in interpreting two-dimensional X-ray images—specifically, the ability to reconstruct three-dimensional spatial relationships mentally, identify bony landmarks, plan surgical procedures, and treat patients. The “eye” denotes navigational capabilities that integrate intuition with tactile feedback (often referred to as “hand feel”). For instance, during screw placement, senior surgeons typically require more than a decade of clinical experience to accurately determine the position of a Kirschner wire within the bone by perceiving the subtle vibrations transmitted through the high-speed rotating wire.

Under traditional conditions, surgeons could only enhance their cognitive and visual capabilities by repeatedly performing intraoperative fluoroscopy and relying heavily on extensive clinical experience.

Whether for orthopedic surgical navigation or orthopedic surgical robots, the core value lies in providing real-time 3D models of patients’ bones and planning surgical pathways for surgeons in real time. This reduces repeated intraoperative fluoroscopy, significantly shortens operation time, markedly lowers surgical risks, and alleviates patient pain, thereby empowering surgeons’ “brains” and “eyes” through technology.

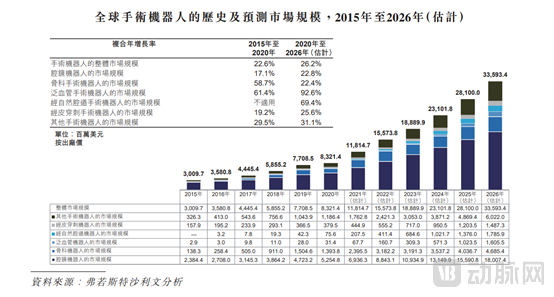

In terms of market value, digital products for orthopedic surgery have vast market potential.

According to Frost & Sullivan statistics, orthopedic surgical robots are regarded as the second-largest market segment, trailing only laparoscopic surgical robots, with the market size projected to reach $4.04 billion by 2025.

In the future, the digital orthopedic surgery products market with the most potential for growth lies in tapping into the incremental market at the grassroots level.

An orthopedic surgeon with extensive experience in using surgical robots once told VCBeat, “The dexterity of existing orthopedic surgical robots actually falls short of that of a surgeon’s hands, and certain mechanical deviations are observed in clinical practice. Digital orthopedic surgical products offer limited benefit to top-tier surgeons; however, for junior physicians, tools such as surgical navigation systems and surgical robots help reduce the learning curve, enable more physicians to master complex procedures, and improve the consistency of medical services.”

From the perspective of development trends in the orthopedics market, although China’s primary-care market is fragmented, it exhibits strong growth momentum.

In contrast to the slowing growth in admissions at tertiary hospitals, grassroots hospitals have experienced relatively rapid growth in admissions, with a notable increase in orthopedic admissions at county-level hospitals in recent years. Statistics show that from 2011 to 2016, the compound annual growth rate (CAGR) of admissions for traumatic fracture surgeries at county-level hospitals was 14.30%, compared with -8.71% at urban hospitals; the CAGR of admissions for spinal disc diseases at county-level hospitals was 37.30%, versus 6.07% at urban hospitals.

However, existing primary care hospitals lack clinical surgical capabilities, particularly in complex orthopedic procedures, and thus fail to meet the rapidly growing patient demand. Taking pelvic fracture reduction—the most complex procedure in trauma care—as an example, senior surgeons capable of performing minimally invasive reduction are concentrated in a limited number of Tier 1 cities’ tertiary Grade A hospitals across China.

Empowered by digital orthopedic surgical products, physicians’ cognitive and visual capabilities are significantly enhanced, the learning curve for mastering complex procedures is markedly shortened, and the professional expertise of senior surgeons is standardized and disseminated to primary care settings through digital means, thereby further stimulating growth in the primary orthopedic market.

However, the currently available surgical robot systems on the market come with exorbitant price tags often reaching tens of millions of yuan, far exceeding the purchasing capacity of primary-care hospitals, thereby resulting in slow market adoption.

During the period when digital orthopedic surgery systems had not yet entered the Chinese market, their core competitiveness lay in productization and commercialization capabilities. Today, the assessment of core competitiveness for orthopedic surgical robots and digital orthopedic surgery solutions has become more multidimensional.

Currently, the three major technical barriers facing digital orthopedic surgery systems are optical navigation technology, collaborative robots, and artificial intelligence technology.

In fact, few companies in China can master all core technologies.

Optical navigation technology represents a critical and challenging area requiring breakthroughs in China. In clinical surgical applications, optical navigation systems must deliver ultra-high precision and sustained stability, posing significant challenges to the quality of fundamental components, manufacturing processes, and core algorithm capabilities.

Currently, the optical navigation devices used in orthopedic surgical robots are largely monopolized by Canada’s Northern Digital Inc. (NDI). Tinavi Medical Technologies, a domestic manufacturer of orthopedic surgical robots, sources its optical tracking cameras from NDI. Tinavi is also independently developing its own optical tracking systems.

Collaborative robots are a critical component of digital orthopedic surgical systems. The high-precision cooperative control algorithms, component selection, and configuration design of robotic arms present significant R&D challenges.

Regarding the two major technical challenges of optical navigation equipment and collaborative robots, most domestic enterprises currently rely on imports.According to Tinavi’s prospectus, optical navigation equipment and collaborative robots are key raw materials for orthopedic surgical navigation and positioning robots. In 2017, 2018, and 2019, the procurement amounts for these two categories accounted for 35.75%, 32.61%, and 35.74% of the total raw material procurement, respectively. The robotic arms were purchased from Universal Robots.

AI technology is the ultimate driving force behind the intelligent evolution of digital orthopedic surgical systems. In key areas of orthopedic surgical navigation—including intelligent image recognition, automatic segmentation, data fusion, precise registration, 3D reconstruction, and intelligent planning—multiple Chinese manufacturers have achieved breakthroughs.

Currently, digital systems for orthopedic surgery are entering a golden age of development.

On one hand, after years of market education, domestic orthopedic surgeons have gained a basic understanding of digital systems for orthopedic surgery. On the other hand, a growing number of orthopedic surgical robot companies have emerged in China, bringing truly high-quality products to the market.

According to VCBeat, there are currently dozens of companies in China focusing on the field of orthopedic surgical robots. Among them, only a few hold medical device sales qualifications: foreign companies such as Medtronic (MAZOR X), Stryker (MAKO), and Zimmer Biomet (ROSA), as well as domestic companies including Tinavi (Tiandi), Xinjunte (ORTHBOT), and Noitom (HOLOSIGHT).

As a well-known technological innovation enterprise in China, Liu Haoyang, founder of Beijing Noitom Technology Ltd., told VCBeat, “True digital products for orthopedic surgery should return to clinical needs, rely on the integration of medicine and engineering, build open platforms through independent innovation, and empower primary-care hospitals.”

The “Transparent Orthopedics” Minimally Invasive Intelligent Visualization System is an autonomous, controllable, and open solution designed to adhere to this philosophy and meet the needs of all orthopedic specialties.

Divergent R&D philosophies are profoundly reflected in product differentiation. Noitom’s digital orthopedic surgery system focuses on empowering the surgeon’s “brain” and “eyes,” while preserving the dexterity of their hands, thereby enabling precise surgical navigation without reliance on robotic arms.

Noitom, in collaboration with the team of Professor Tang Peifu and Professor Chen Hua from the Department of Orthopedics at the Chinese PLA General Hospital, has achieved 3D dynamic real-time navigation for pelvic fracture surgery, filling the gap in intelligent navigation for pelvic fracture reduction. According to the published paper “A Case of Closed Reduction Treatment for Complex Pelvic Fracture Assisted by an Intelligent Monitoring System,” this technology enables precise, real-time 3D dynamic monitoring of fracture reduction while reducing radiation exposure. The system boasts a spatial resolution accuracy of 0.2 mm/500 mm and an angular accuracy of 0.2°.

Noitom's "Transparent Orthopedics" Minimally Invasive Intelligent Visualization System

Liu Haoyang stated, “In fact, many developers of orthopedic surgical robots aim to increase procedural fees. However, we believe the significance of 3D dynamic navigation in orthopedics lies not in making orthopedic surgery appear more sophisticated, but in enabling ordinary hospitals and physicians to perform surgeries with high quality. Therefore, digital products for orthopedic surgery should not be limited to top-tier tertiary hospitals in first-tier cities, but should serve the vast number of general hospitals.”

Amidst the inflection point in the orthopedics sector, the digital orthopedics industry is accelerating its development. The landscape is rife with opportunities, yet it also presents significant challenges. Nothing is truly unknown; it is merely obscured. The current market for digital orthopedic surgery is far from reaching its endgame, leaving ample room for opportunity. We remain optimistic about enterprises that genuinely master core technologies and deeply understand the needs of physicians.