STAAR Surgical: Global Leader in ICL for Vision Correction

STAAR

Ophthalmic Equipment R&D Company

STAAR Surgical (STAAR), a specialized global manufacturer of ophthalmic surgical devices.

With over 30 years of focus on the manufacturing of implantable lenses for ophthalmic surgery, particularly in the field of ICL (Implantable Collamer Lens), the company has nearly monopolized the global market as the industry leader. In 2019, STAAR announced that global ICL implants had surpassed one million. In 2020, its annual net sales reached $163.5 million, a 9% increase from 2019, with ICL sales accounting for more than 85% of the total.

So, what is ICL? What are the market prospects? How has STAAR managed to become the leader in this field? This article will seek answers to the aforementioned questions by examining STAAR’s business development.

ICL May Become the Mainstream Approach for Myopic Refractive Surgery

With the rising global prevalence of myopia, refractive surgery has accelerated over the past decade.

From early Radial Keratotomy (RK) to Excimer Laser Photorefractive Keratectomy (PRK), then evolving to Femtosecond Laser-Assisted In Situ Keratomileusis (LASIK), followed by Small Incision Lenticule Extraction (SMILE) and Implantable Collamer Lens (ICL) implantation, myopia refractive surgery has been progressing toward greater safety, minimal invasiveness, and the pursuit of higher visual quality.

Currently, mainstream refractive surgeries for myopia fall into two categories: corneal refractive surgery and phakic intraocular lens (IOL) implantation, which operate on fundamentally different principles. Corneal refractive surgery follows a “subtractive” approach, whereas phakic IOL implantation adopts an “additive” approach:

Corneal Refractive Surgery, by removing part of the corneal tissue to achieve corrective treatment effects, mainly including SMILE (Small Incision Lenticule Extraction), LASIK (Laser-Assisted In Situ Keratomileusis), and TPRK (Transepithelial Photorefractive Keratectomy).

Intraocular Lens Implantation, without damaging corneal tissue, refractive correction is achieved by implanting an artificial intraocular lens; currently, the mainstream approach is ICL implantation.

ICL (Implantable Collamer Lens) is a phakic intraocular lens, more commonly known as an implantable contact lens.ICL implantation is a surgical procedure that corrects vision by implanting an ultra-thin, refractive artificial lens between the iris and the natural crystalline lens.

ICL implantation is currently in a phase of rapid adoption and is even considered poised to replace the more mainstream laser surgeries of today. What accounts for such high expectations for ICL?

In terms of treatment, ICL offers the following prominent advantages:

First, ICL implantation does not involve corneal ablation and is reversible. The intraocular lens can be explanted when no longer needed. Furthermore, it yields superior postoperative outcomes and is associated with a low incidence of complications such as corneal endothelial damage.

Second, ICL implantation has relatively low requirements for corneal conditions. It is suitable for patients with thin corneas and those requiring refractive correction after corneal refractive surgery.

Third, ICL offers a wider range of corrective diopters. While laser surgery typically corrects myopia within the range of 3.00 to 8.00 diopters, ICL implantation can correct vision from 0.50 to 18.00 diopters.

Additionally, ICL can also be used to treat astigmatism, hyperopia, and presbyopia.

Although ICL implantation is currently more expensive for consumers than laser surgery, it represents a more cost-effective surgical option from the perspective of hospitals and clinics.First, compared with laser surgery, which requires greater upfront investment in surgical instruments, ICL surgery involves relatively simpler equipment; second, for surgeons experienced in intraocular procedures (such as cataract surgery), the learning curve for ICL implantation is short.

ICL is considered poised to become a mainstream surgical procedure, owing to its broad applicability, therapeutic efficacy, and low dependence on equipment.

It has been over 20 years since the world’s first ICL product was launched in 1996. During this period, the safety and efficacy of ICL have been extensively validated in clinical practice, helping more than one million eyes worldwide regain clear “vision.”

As the pioneer of ICL, STAAR launched the world’s first ICL product. Currently, the mainstream ICL product in the global market is its EVO ICL (Vision ICL V4c).

Over 30 Years of Focus on Ophthalmic Surgery: How STAAR Rose to Prominence

1982, STAAR was established.The company focuses on the design, development, manufacturing, and sales of implantable lenses and delivery systems for inserting lenses into the eye. Its sales revenue is 100% derived from its ophthalmic surgical products division, with main products including implantable collamer lenses (ICL) for refractive surgery, intraocular lenses (IOL) for cataract surgery, and injector components used to deliver artificial lenses during surgeries.

Source: STAAR Official Website, Soochow Securities Research Institute

In 1990, eight years after its establishment, STAAR was listed on the NASDAQ in the United States.Judging from the trend in STAAR’s stock price, its early performance was lackluster. This was mainly due to limitations in product performance, which restricted clinical applications and slowed market promotion. Consequently, STAAR has been continuously refining and upgrading its products.

STAAR's stock price fluctuates with the continuous upgrades and iterations of its products.For example, whether it was the FDA approval of Vision ICL V4 in 2005 or the CE certification of the upgraded EVO ICL (Vision ICL V4c) in 2011, the company’s business has consistently grown alongside improvements in product performance and regulatory approvals, with corresponding upticks in its stock price chart at these key milestones.

With the global promotion and development of EVO ICL, particularly since its entry into the Chinese market, STAAR entered a phase of rapid growth in 2016.

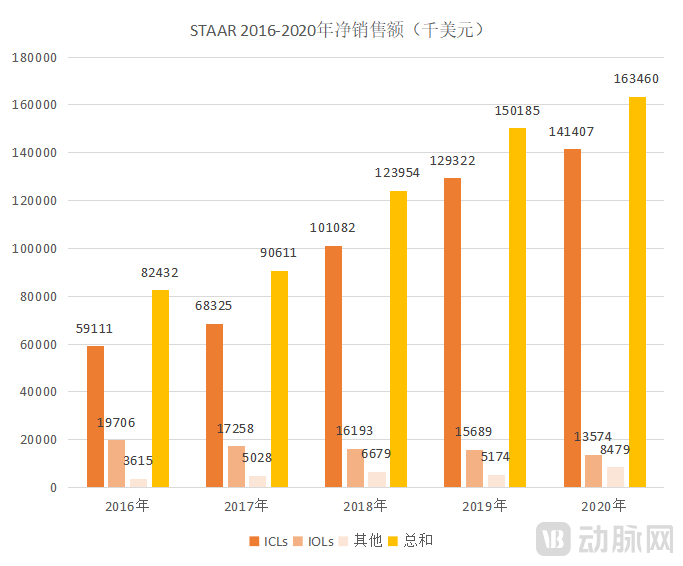

In recent years, the STAAR business has maintained rapid growth.According to its 2020 annual report, net sales in 2020 were approximately $163.5 million, representing a 9% increase from the $150.2 million reported for fiscal year 2019. Net sales in 2019 increased by 21% compared with the $124 million reported for fiscal year 2018.

Among these, total sales of ICLs in 2020 amounted to $141.4 million, representing a 9% increase from $129.3 million in fiscal year 2019. Sales of other products, including IOLs, were approximately $22.1 million, a 6% increase from $20.9 million in fiscal year 2019.

Source: STAAR official website, 2020 and 2018 Annual Reports

1Product Portfolio: Early Market Entry, Focusing on Solutions for Refractive Errors and Cataracts

Impressive data must ultimately be grounded in the product.

STAAR has been deeply engaged in the field of ophthalmic surgery for 35 years. From developing intraocular lenses (IOLs) for cataract treatment to becoming a pioneer and leader in Implantable Collamer Lenses (ICLs), its products are now sold worldwide.However, as a global company, it has not pursued a path of broad scale and comprehensive coverage, but has instead chosen to climb the ladder of specialized expertise.

In terms of product portfolio, STAAR launched its first intraocular lens (IOL) for cataract treatment in the early 1990s. In 1996, the company introduced its first Implantable Collamer Lens (ICL) product, which received CE marking approval in 1997 and was subsequently marketed in Europe. Since then, STAAR has been deeply engaged in the two ophthalmic surgical fields of cataract and refractive correction.

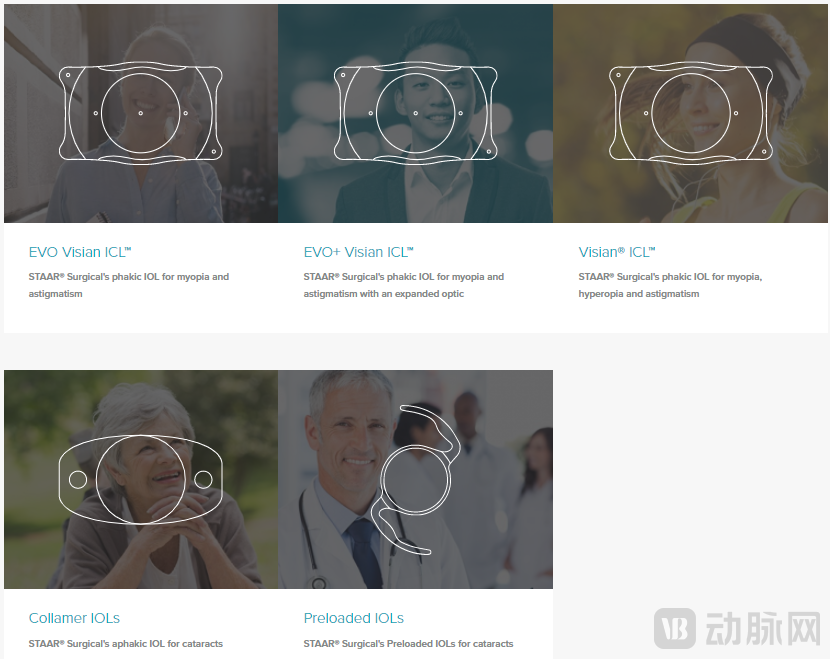

Major Products (ICL, IOL) Source: STAAR Official Website

In the Field of Cataract SurgerySTAAR’s representative IOL products include Collamer IOLs and the Preloaded IOLs series. In the IOL market, STAAR primarily competes based on its technological quality and value. However, the global cataract intraocular lens market is highly concentrated, and STAAR’s competitive advantages are limited beneath the dominance of the top four major ophthalmic medical device giants.

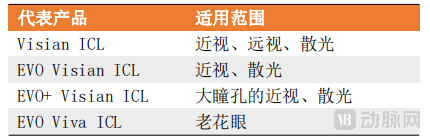

In the field of refractive correctionSTAAR can be regarded as the leader in ICL. Its ICL products are the best-selling worldwide, with cumulative sales exceeding one million units in 2019. Currently, its flagship products mainly include the EVO Visian ICL, EVO+ Visian ICL, and Visian ICL series, each designed for different indications.

Source: STAAR Official Website

STAAR’s product is the only FDA-approved posterior chamber phakic intraocular lens (PIOL) marketed in the United States.Although there are other ICL products on the market, STAAR stated that its primary competitor in the refractive surgery market is laser vision correction. This underscores STAAR’s dominant position in the global ICL sector.

In terms of product sales proportion, ICL is STAAR’s core business, with its share of sales increasing year over year.ICL accounted for the largest share of the company’s business segments, contributing over 85% of sales revenue in 2020. Between 2016 and 2020, its proportion increased by 14.8 percentage points.

Proportion of Net Product Sales, 2018–2020 Source: STAAR 2020 Annual Report

2R&D Barriers: Synergistic Advancements in Patented Materials and Product Design

Superior products are born from advanced technology.

STAAR’s ICL products hold a monopolistic position in the global market, primarily due to the manufacturing materials and structural design underlying the product.

Under the definition of STAAR, ICL stands for: Implantable Collamer Lens. Collamer is a collagen copolymer used to manufacture implantable lenses, with its name being a combination of “collagen” and “polymer.”

Collamer offers high biocompatibility and flexibility, ensuring harmonious integration of the implanted lens with the patient’s eye. Additionally, Collamer material provides UV protection without compromising normal visual acuity.Currently, STAAR holds the international patent for Collamer, and it is the sole global manufacturer of this material.

In addition to the material used for lens fabrication, implantation position is another critical factor in the development of Implantable Collamer Lens (ICL) surgery. The implantation site of ICLs has evolved from the anterior chamber to angle-supported designs, and then to iris-fixated models; currently, posterior chamber implantation has become the mainstream approach and is widely recognized in clinical practice. Posterior chamber implantation refers to placing the lens behind the iris and in front of the natural crystalline lens. STAAR’s ICL is a posterior chamber implantable lens.

Furthermore, in terms of specific product design, STAAR’s most prominent feature is the application of CentralFLOW technology.

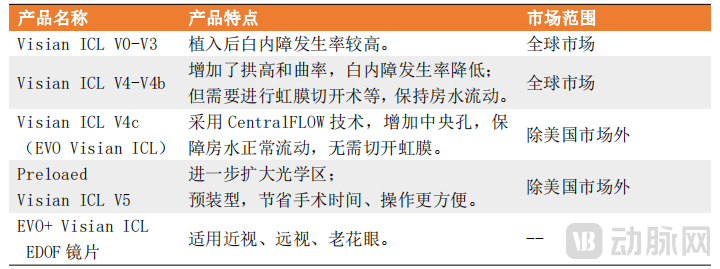

In fact, the early STAAR ICL had many shortcomings in terms of stability and optical zone, leading to an increased incidence of cataracts after implantation, which hindered its widespread adoption. It was not until 2005, when the ICL V4 further increased vault height and curvature, significantly reducing the incidence of cataracts, that it also received FDA approval in the same year.

ButSTAAR’s first truly global product was the EVO ICL (Visian ICL V4c), launched in 2011.The product was first launched in markets outside the United States, entered the Chinese market in 2014, and is currently a mainstream product in the global market.

EVO ICL (Visian ICL V4c) utilizes Central FLOW technology, which incorporates a central port in the center of the ICL’s optical zone. This central port restores the natural circulation of aqueous humor without compromising visual quality, thereby reducing the incidence of cataracts. Furthermore, this design eliminates the need for preoperative peripheral iridotomy, minimizing tissue trauma, while also ensuring stable intraocular pressure.

Overall, STAAR’s products have undergone five major iterations, as shown in the figure:

Source: STAAR Official Website, Soochow Securities Research Institute

Even as a leader in the ICL field, STAAR has never halted its pace of product updates and iterations to sustain its competitive edge.STAAR prioritizes R&D, with its annual report data indicating an overall upward trend in R&D expenditures. Over the past five years, annual R&D spending has consistently remained above $20 million. Currently, its R&D focus is on medical devices for presbyopia correction, pre-loaded injector systems, and the development of next-generation ophthalmic medical devices and materials.

In August 2019, the FDA approved STAAR to initiate clinical studies in the United States for the EVO/EVO+ Visian and EVO/EVO+ Visian Toric Implantable Collamer Lenses (ICLs). To date, recruitment of 300 subjects has been completed, and follow-up is being conducted in accordance with the clinical trial protocol. In July 2020, the EVO Viva ICL, designed to provide vision correction for patients with presbyopia, received CE marking and is being marketed in the European Union.

From prototype to mass production, and from mass production to more mature products, STAAR has consistently upgraded its products based on clinical feedback, thereby ensuring superior product quality and establishing a competitive moat.

3Market Development: From Clinics to Physicians, Sales Coverage Worldwide

Even a product with “the fragrance of fine wine” needs the wind of the market to blow it “out of the alley.”

It is reported that the global number of ICL implants over the past four years has exceeded the total from the previous 15 years, underscoring the rapid growth of ICL in recent years.

Throughout the continuous updating and iteration of ICL products, STAAR has also been actively engaged in market development and education. STAAR’s ophthalmic product, the ICL, has been available in the global market for over 20 years and in the Chinese market for more than 10 years, with a patient satisfaction rate exceeding 95%.

During this period, STAAR cultivated the market by participating in major ophthalmology conferences worldwide and actively conducting training for healthcare professionals and patient outreach.

For example, STAAR is a partner of ophthalmic surgery-related international conferences such as the ASCRS Foundation (American Society of Cataract and Refractive Surgery), the International Society of Refractive Surgery (ISRS), the ICO Foundation’s “Teach the Teachers” program, the Congress of European Ophthalmic Surgeons, and Beyond Blindness.

For many years, STAAR has also maintained close collaborations with leading refractive clinics in the areas of training, product awareness, and practice development.For example, in 2016, STAAR announced a strategic partnership with Aier Eye Hospital; in 2017, it announced a collaboration with South Korea’s BalGeunSeSang Eye Clinic; and since 2019, it has continued to forge strategic partnerships with eye clinics in Japan, the Philippines, Germany, the United States, and other countries.

Furthermore, STAAR provides professional certification to ophthalmologists, incorporating them into its own certified network of ICL/TICL surgical experts. As a result, STAAR has maintained a strong reputation and brand presence across multiple global markets.

Selected Partner Clinics Source: STAAR Official Website

STAAR’s products are sold in more than 75 countries and regions worldwide. The company has a substantial global presence, with its 2020 annual report indicating that markets outside the United States accounted for 96% of its total sales.

STAAR maintains operational and management entities in the United States, Switzerland, and Japan. The company distributes its products through direct sales or distributor networks in over 75 countries. Direct sales are implemented in Japan, Germany, Spain, the United States, Canada, the United Kingdom, and Singapore; a combination of direct sales and distribution is adopted in China, South Korea, India, France, the Benelux region, and Italy; while distributor-based sales are employed in all other countries.

China is STAAR’s largest overseas market, accounting for approximately 44% of its consolidated net sales in fiscal year 2020. Shanghai Lansheng serves as STAAR’s distributor in China. From 2018 to 2020, the Chinese market generated approximately $71.69 million, $64.82 million, and $46.07 million in sales for STAAR, respectively.

Low ICL Penetration Rate Leaves Huge Potential for the Future Market

Myopic refractive surgery is the second most frequently performed ophthalmic surgical procedure. According to estimates by the World Health Organization, the global myopic population is projected to reach 4.9 billion by 2050, with the number of individuals with high myopia increasing to 925 million during the same period. ICL implantation holds a distinct advantage in the treatment of moderate to high myopia; however, its overall penetration rate remains low.

Taking China as an example, according to Frost & Sullivan data, 44,000 ICL implantation procedures were performed in China in 2018. However, this figure corresponds to a population of over 70 million individuals aged 18–45 with high myopia, resulting in a penetration rate of only 618 cases per million people. This also indicates substantial future growth potential for ICL.

Caren Mason, President and Chief Executive Officer of STAAR, stated, “While the refractive surgery industry as a whole saw a 21% decline, ICL procedures grew by 11% throughout 2020. The Company’s positive growth confirms the increasing adoption of the EVO ICL implantable lens portfolio and demonstrates that our lenses continue to expand their share of the refractive market.”

Meanwhile, STAAR also stated that competitors from Asia have begun launching low-cost posterior chamber implantable collamer lenses on the market, intensifying competition within the ICL industry. Currently, ICL products under development in the Chinese market have entered clinical trial stages.

References:

[1] jogalaco. A Side View of iCare Medical’s Prolens PR via ICL/PRL. Xueqiu. 2021-11-07

[2] Zhu Guoguang, Quan Ming. Investment Strategy for the Ophthalmology Industry from an International Perspective: A Golden Track and the Rise of China. Soochow Securities. 2020-08-24

[3] Pharmaceutical Industry: The Ophthalmology Arena – Who Will Prevail? Haitong International. 2020-09-21

[4] ICL Volume Growth Exceeds Expectations, Offering Insights for the Domestic Market. Soochow Securities Pharmaceutical Team Led by Zhu Guoguang | Weekly Report Dated August 6. 2021-08-08