Gushengtang: The First TCM Healthcare Stock — What It Got Right in 11 Years

Long Hill Capital

Venture Capital Institution

Gushengtang Listing Ceremony, Image: Long Hill Capital Official WeChat Account

China’s TCM medical services industry welcomes its first publicly listed company!

Despite the recent sluggish performance of Hong Kong stocks, Gushengtang’s global IPO still attracted subscriptions exceeding eight times the offering and drew in several cornerstone investors, including Huiyuan Capital, Boyu Capital, and UBS. Gushengtang issued 27.878 million shares for its HKEX listing, which took place on December 10. The offering price was HK$29 per share; it opened at HK$33.4 and closed at HK$29, resulting in a market capitalization of HK$6.681 billion.

Based on current business needs, Gushengtang intends to use the proceeds from its global offering to expand its online and offline operations, as well as to strengthen its research and development capabilities and supply chain capabilities.

The prospectus shows that Gushengtang has secured multiple rounds of financing since 2014. In March 2021, prior to its listing, Gushengtang completed a $37.7 million Series E financing round, with major investors including New Enterprise Associates (NEA) and Long Hill Capital. Long Hill Capital, the exclusive investor in Gushengtang’s Series A round, increased its stake four times and participated in every round of private financing before the company’s IPO.

Gushengtang, founded in 2010, is a technology-enabled “OMO” (Online-Merge-Offline) New TCM platform that focuses on primary care, integrates traditional Chinese medicine with modern medical approaches, and combines offline operations with an online presence to provide comprehensive, full-lifecycle, all-scenario health management services.

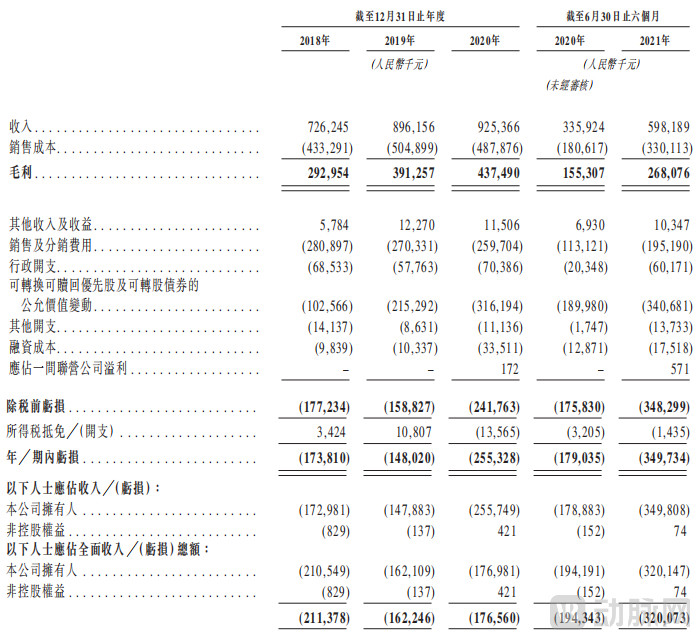

In terms of revenue, Gushengtang has achieved substantial growth over the past three years. According to the prospectus, for the years ended December 31, 2018, 2019, and 2020, the Company generated revenues of approximately RMB726.2 million, RMB896.2 million, and RMB925.4 million, respectively, representing a compound annual growth rate (CAGR) of 12.9%. The Company’s revenue increased by 78.1% from RMB335.9 million for the six months ended June 30, 2020, to RMB598.2 million for the six months ended June 30, 2021.

In the high-barrier TCM big health market, why has Gushengtang stood out?

A company’s aspirations are closely tied to the founder’s sense of mission. Before founding Gushengtang, Tu Zhiliang worked at iKang Guobin, a chain health examination provider, where he rose from head of sales to assistant to the group president and deputy general manager for East China within six years, participating in the integration of iKang and Guobin and the establishment of the group’s marketing center.

At first glance, Tu Zhiliang seemed to have little connection with Traditional Chinese Medicine (TCM). It was actually health warnings that emerged after periods of intense work that prompted him to truly enter the field of TCM. Since both his wife and father-in-law are engaged in clinical practice and research in TCM, and his father-in-law, Li Zhengmu, holds a doctorate from Guangdong University of Chinese Medicine, illnesses in the family have always been treated with TCM. After taking the herbal prescriptions provided by his father-in-law, all of Tu Zhiliang’s physical indicators returned to normal.

Tu Zhiliang began to re-examine the field of Traditional Chinese Medicine (TCM) from his own perspective. His years of experience in Western medicine-based health management at iKang Guobin made him recognize the commercial value and immense market potential of TCM health preservation and wellness—why couldn’t TCM healthcare be operated with the same level of standardization as Western medical check-ups?

Tu Zhiliang’s vision aligned perfectly with his father-in-law’s initial ambition to scale Gushengtang Clinic to the stature of Tongrentang. Consequently, at the earnest invitation of his father-in-law and wife, Tu formally joined Gushengtang, ushering in new changes for this traditional Chinese medicine clinic. He is committed to standardizing and scaling the family’s TCM practice.

In the early stages of his venture, Tu Zhiliang also took some detours. Initially, he designed a B2B development strategy for Gushengtang, under which the company provided VIP services to large corporations and established physical clinics to deliver these offerings. This model was similar to iKang Guobin’s health checkup model, with the advantage of yielding quick results. After implementing this approach, Gushengtang achieved RMB 1 million in membership card sales revenue in its second month of operation.

However, traditional Chinese medicine (TCM) services are non-standardized products, making it difficult to rapidly replicate them in a productized manner like health checkups. As a result, the conversion rate for Gushengtang’s membership cards remained below 40%. After recognizing this reality, the founding team conducted a review and discussion, and in the third quarter of 2012, decided to adopt a business model centered on outpatient clinics led by renowned TCM practitioners.

Once the business model was established, Tu Zhiliang began engaging with investors. He positioned Gushengtang as a traditional Chinese medicine (TCM) enterprise leveraging capital to drive growth. In 2014, Gushengtang secured angel funding, followed by Series A financing within less than a year. The successful fundraising was attributable not only to Tu Zhiliang’s strategic decisions but also to favorable policy conditions.

Around the time of Gushengtang’s first two rounds of financing, the State Council successively issued the “Several Opinions on Promoting the Development of the Health Service Industry” and the “Notice on Printing and Distributing the Summary of Work in 2014 and Key Tasks for 2015 in Deepening the Reform of the Medical and Healthcare System,” which explicitly expressed support for the development of Traditional Chinese Medicine (TCM), particularly for social capital entering the TCM health service industry at the grassroots community level.

Benefiting from favorable national policies supporting the development of grassroots traditional Chinese medicine, Gushengtang has also gained favor among investors.

There is a saying in the healthcare industry: “Western medicine relies on the institution, while Traditional Chinese Medicine (TCM) relies on the practitioner.” This means that patients of Western medicine prioritize the reputation of the hospital, such as seeking care at local Grade 3A hospitals, whereas TCM patients place greater emphasis on the renown of the individual physician.

Large hospitals offer advanced equipment and an ideal research environment, making doctors willing to work for leading public hospitals with strong brands. The term “veteran TCM practitioners” commonly refers to experienced traditional Chinese medicine (TCM) doctors. These doctors attract patients who seek them out by reputation, whether they practice in large hospitals, run their own clinics, or provide consultations at well-known TCM institutions such as Tongrentang and Gushengtang. Consequently, large hospitals hold limited appeal for these TCM practitioners.

If Gushengtang aims to pursue a strategy centered on renowned physicians, it must establish a system capable of attracting such top-tier medical experts. Tu Zhiliang is clearly aware of this imperative. To this end, Gushengtang has built a standardized platform for Traditional Chinese Medicine (TCM) diagnosis and treatment, positioning itself as a “TCM agent.”

Gushengtang adopts a model in which physicians hold equity stakes in individual clinics, partnering with renowned TCM practitioners to establish traditional Chinese medicine (TCM) clinics. Gushengtang holds a 70% equity stake, while the physician holds 30%. As the “agent,” Gushengtang is responsible for operational management. Physicians are solely responsible for clinical consultations, allowing them to focus on patients without distraction from administrative matters, thereby practicing as traditional doctors. Furthermore, provided that contractual terms are not violated, physicians are guaranteed an exit option regardless of the clinic’s profitability or losses, and their equity can be liquidated at any time. Additionally, TCM practitioners are entitled to receive dividends based on a proportional share of the clinic’s revenue.

In this way, renowned physicians effectively gain a comprehensive assistant and are eligible for profit sharing, leaving them with no concerns. Under this model, Gushengtang has successfully recruited a large number of distinguished physicians. The prospectus shows that as of the end of June 2021, Gushengtang’s leading physician team was headed by four National TCM Masters (out of a total of 56 nationwide). The company had more than 19,000 physicians across China, with extensive business coverage including TCM internal medicine, gynecology, dermatology, hepatology, otolaryngology, and gastroenterology.

Leveraging its extensive pool of physicians and broad geographic coverage, Gushengtang has accumulated nearly 1.9 million customers, with total patient visits exceeding 8.4 million.

Gushengtang’s highly scalable business model has attracted significant attention from the capital markets. Between 2014 and 2017, the company completed four rounds of financing, raising a total of RMB 1.7 billion. Each round set a new record for the largest single financing transaction in China’s traditional Chinese medicine (TCM) sector at the time.

With capital support, Gushengtang entered a period of rapid growth. According to its prospectus, the company’s revenue from 2018 to 2020 was RMB 726 million, RMB 896 million, and RMB 925 million, respectively, representing a compound annual growth rate (CAGR) of nearly 13%. Despite irregular operations at offline clinics due to the pandemic over the past year, Gushengtang’s annual revenue still approached RMB 1 billion. Having generated RMB 2.547 billion in revenue over three years, this veteran TCM provider has indeed proven its capability.

In terms of business model, Gushengtang’s revenue structure is primarily divided into two parts: first, the provision of healthcare solutions, which accounts for over 90% of total revenue; and second, the sales of healthcare products. The so-called “healthcare solutions” mainly refer to revenue generated from Traditional Chinese Medicine (TCM) consultations.

According to the prospectus, Gushengtang generated RMB 668.1 million, RMB 865.9 million, and RMB 891.8 million in revenue from healthcare solutions in 2018, 2019, and 2020, respectively, accounting for 92.0%, 96.6%, and 96.4% of its total revenue during the same periods.

The prospectus states that Gushengtang’s revenue-sharing model compensates physicians on a per-visit basis, allowing them to retain 80% of the registration fee for each consultation. In addition to substantial consultation fees, physicians also benefit from profit sharing from their exclusive studios, revenue sharing from proprietary prescription products, and preferential equity interests and free option plans offered by the group.

Such a substantial revenue-sharing ratio is indeed worthy of the “TCM Agent” model established by founder Tu Zhiliang.

In addition to its TCM outpatient services, Gushengtang generates another stream of revenue from the sales of pharmaceutical and health products, which amounted to RMB 58 million, RMB 30 million, and RMB 34 million in 2018, 2019, and 2020, respectively. This segment accounted for a relatively small proportion of total revenue, representing 8%, 3.4%, and 3.6% of the company’s total income in those years.

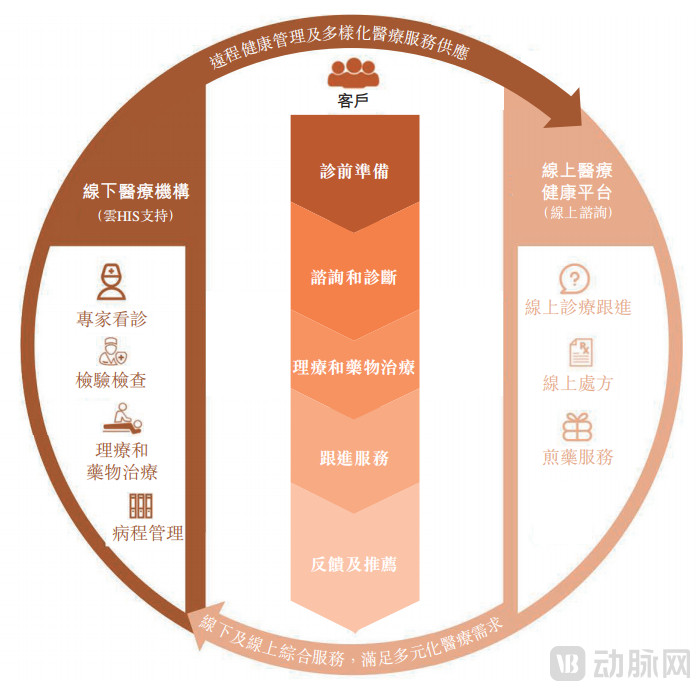

Gushengtang is also seeking transformation by prioritizing online development and proposing the creation of a new OMO (Online-Merge-Offline) model for Traditional Chinese Medicine (TCM) healthcare. The so-called OMO new TCM healthcare model refers to leveraging internet technologies to integrate offline and online TCM resources, thereby providing patients with digitalized and standardized TCM medical services and breaking the temporal and spatial limitations inherent in traditional TCM diagnosis and treatment models.

For a long time, Traditional Chinese Medicine (TCM) has emphasized the four diagnostic methods: inspection, auscultation and olfaction, inquiry, and palpation. The internet enables TCM practitioners to perform “pulse diagnosis via a suspended thread,” but this is difficult to achieve with current technology. Therefore, at the present stage, Gushengtang places greater emphasis on leveraging online platforms to support follow-up care after offline consultations.Health Management FeaturesFrom a fundamental logic perspective, the objective is to extend the product lifecycle. Gushengtang follows the same approach. By providing comprehensive medical management services that cover the entire traditional Chinese medicine (TCM) care cycle and all health management scenarios, it transforms brief, ten-minute offline TCM consultations into long-term health management services.

Secondly, it was the first to adopt“OMO” Business Model. Benefiting from favorable government policies that encourage the development of online healthcare services, Gushengtang has gained a first-mover advantage among new TCM healthcare providers in China in building an online medical platform, and has achieved synergies by leveraging its extensive network of offline medical institutions. On one hand, the development of the company’s online healthcare services enables more efficient utilization of medical resources and expands customer reach; on the other hand, the company can strategically select cities for expanding its offline coverage based on metrics of online physician and customer activity.

Finally,Standardization, Digitalization, and IntelligenceIn the field of Traditional Chinese Medicine (TCM), the saying “one prescription per individual” has long prevailed, reflecting a lack of standardization in traditional TCM practices. However, this absence of standardization is fatal for enterprises, adversely affecting operations, business expansion, and cost reduction. Gushengtang has developed a standardized and scalable operating model for its offline business.

Gushengtang developed and implemented a cloud-based Hospital Information System (HIS) in 2017, aiming to achieve full supply chain management from upstream procurement to downstream distribution while expanding its business scale and maintaining quality control capabilities. Additionally, Gushengtang leverages information technology systems to enhance customer experience and satisfaction, enabling clients to check physician availability and schedule appointments through their preferred channels, as well as facilitate timely communication.

Gushengtang has established a standardized and scalable operating model for its offline business. Meanwhile, the Company is a pioneer in the traditional Chinese medicine (TCM) industry in developing and implementing an integrated cloud Hospital Information System (HIS), striving to achieve digitalization of the entire supply chain management from upstream procurement to downstream distribution. Leveraging its cloud HIS, the Company has enhanced its operational capabilities and quality control.

Not only operations, but also herbal medicines have been standardized. Gushengtang is also improving its layout of the traditional Chinese medicine (TCM) industry chain. Since 2015, Gushengtang has launched a quality assurance system for TCM decoction pieces, participated in establishing GMP-compliant herbal material processing plants, and took equity stakes in large-scale GAP-certified cultivation bases for major TCM varieties. This has enabled the company to provide one-stop services ranging from herbal cultivation, processing, and sales to home delivery, thereby forming a complete TCM ecological chain.

With the aforementioned measures in place and financing secured, Gushengtang has obtained the capital necessary for rapid expansion. As of the end of June 2021, Gushengtang owned and operated 42 medical institutions in Beijing, Shanghai, Guangzhou, Shenzhen, Foshan, Zhongshan, Fuzhou, Nanjing, Suzhou, Ningbo, and Wuxi, among which 10 were self-built and 32 were acquired.

According to the prospectus, for self-built institutions, the break-even period and payback period are approximately 5 months and 18 months, respectively. Following standardized renovations by Gushengtang and integration with the cloud HIS system, the operating performance of newly acquired medical institutions is expected to improve over the next one to two years. Based on existing cases, the break-even point and investment payback period are approximately 35 months.

For medical institutions that fail to achieve the annual revenue target of RMB 10 million within a specified period (typically the first full year following acquisition or establishment), Gushengtang’s management will review their operational and financial performance metrics as well as their built-up area. The company will then assess their future growth prospects by considering factors such as local demand for traditional Chinese medicine (TCM) healthcare solutions, growth trends in patient visit volumes and average spending per visit, and the strategic advantages of offline medical facilities, thereby determining whether it is necessary to close the institution.

If the initial phase of TCM practitioners marked Gushengtang’s “1.0” era, the company is currently in its “2.0” era, characterized by the integration of online and offline resources through an OMO model and ongoing standardization initiatives. To achieve its “3.0” vision of building China’s largest new TCM healthcare ecosystem, Gushengtang will continue to upgrade its existing business models and services.

First, strengthen OMO integration to cover the entire patient journey and all customer scenarios, expand the reach of medical resources, deepen “OMO” integration, and increase market penetration. To this end, Gushengtang will develop family doctor services and chronic disease management services through its membership program to meet diverse customer needs, provide health management across the full life cycle, and further strengthen long-term relationships with customers and affiliated physicians. The Company will continue to expand its offline business, focusing on tier-1 and tier-2 cities where medical resources are concentrated, to increase market penetration and reinforce its leading market position in these cities, while implementing a steady expansion strategy to enter new cities each year. Finally, it will consolidate its online healthcare business, enhance the synergies between offline and online operations, and focus on integrating its online platforms to deliver high-quality medical services to customers in lower-tier cities.

Second, we will continuously improve the cloud-based HIS system to drive the digitalization of diagnostic processes, standardization of health solutions, and standardization of traditional Chinese medicine (TCM) formulas. The system covers all customer health management scenarios and empowers small and medium-sized TCM clinics by providing standardized operational expertise and an integrated supply chain management system.

Third, we will continue to invest in R&D to deliver superior specialized TCM nursing care. Gushengtang plans to continuously develop a more diverse portfolio of TCM healthcare products, develop in-house hospital preparations with the assistance of CROs, and allocate additional resources to researching and developing new TCM solutions for chronic disease management. Furthermore, Gushengtang will fully leverage its technology platform, devote substantial efforts, and collaborate with leading national universities of Chinese medicine to develop smart medical devices such as smart wristbands and four-diagnostic instruments.

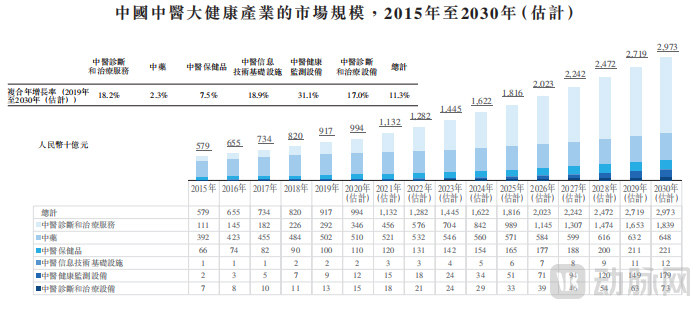

In recent years, driven by proactive national policy guidance and accelerated by the COVID-19 pandemic, China’s traditional Chinese medicine (TCM) health industry has expanded significantly. According to Frost & Sullivan analysis, the market size of China’s TCM health industry is projected to grow at a compound annual growth rate (CAGR) of 11% from 2019 to 2030. The market size officially surpassed the RMB 1 trillion mark in 2021 and is expected to reach approximately RMB 3 trillion by 2030.

With the increasing proportion of the aging population, rising per capita disposable income, and growing health awareness among residents, per capita healthcare expenditure has continued to rise, making healthcare consumption an important component of personal spending. According to data from the National Bureau of Statistics and forecasts by Frost & Sullivan, China’s per capita healthcare expenditure is expected to increase from RMB 1,843 in 2020 to RMB 4,359 in 2030, accounting for 8.7% and 9.8% of total per capita consumption expenditure in 2020 and 2030, respectively.

Traditional Chinese Medicine (TCM) medical services constitute a vital component of healthcare services. Providers of TCM healthcare primarily include TCM hospitals, TCM clinics, TCM centers, and other major medical institutions offering TCM services. Within the broader healthcare services market, TCM medical services serve as a complement to other types of medical services.

The market share of private healthcare providers within the TCM diagnosis and treatment services segment of China’s TCM big health industry increased from 29.0% in 2015 to 41.2% in 2019, and is projected to reach 51.2% by 2030. The private TCM diagnosis and treatment services segment of China’s TCM big health industry features numerous market participants and is highly fragmented. Measured by revenue generated from providing healthcare solutions in 2020, Gushengtang held a 0.6% market share in the private TCM diagnosis and treatment services segment.

It is foreseeable that China’s TCM health and wellness industry will still have enormous room for growth over the next decade, and early entrants will undoubtedly gain a first-mover advantage. Traditional Chinese medicine (TCM) represents a vast yet fragmented market, and participants providing TCM medical services need to earn the recognition of doctors, patients, and investors. Following the successful IPO of Guangdong Gushengtang Traditional Chinese Medicine Health Science And Technology Co.,Ltd., more such innovative enterprises are expected to emerge in the future.