Who Will Lead the Next Half of China's Billion-Dollar Neurointervention Market Amid Surging Growth?

The neurointerventional sector, once dominated by imports and crowded with numerous participants, is now seeing its market landscape truly take shape, with the gap between market players gradually widening.

The neurointerventional sector has transitioned from an era focused on product and technological prowess to the second half, where commercialization and monetization capabilities are put to the test.

The neurointerventional sector in China has a relatively short development history. In the past two years, the surge in demand within this field has attracted numerous participants, with many believing that neurointervention will become the next coronary intervention.

However, after more than 20 years of industry consolidation and development, the coronary intervention sector has ultimately accommodated no more than three leading domestic manufacturers.The neurointerventional sector is undergoing industrial consolidation at a faster pace.

This rapidly expanding industry has left standing only those players that have weathered market cycles. Companies such as Acandis Medical, JuiChuang Tongqiao, and Peijia Medical have conducted IPOs on the Hong Kong Stock Exchange, rapidly expanded their product portfolios, and entered a phase of aggressive market penetration. Within less than a year of its product launch, Acandis Medical achieved a market share exceeding 5%.

Neurointervention has emerged as a phenomenal niche within China’s medical device industry. Domestic players have leveraged technological innovation to penetrate the market, rapidly achieve import substitution, and list on capital markets, thereby compressing into a few years an industrial development trajectory that previously took companies a decade or longer to complete.

However, this is not the endgame for the industry. Against the backdrop of centralized procurement compressing the market space for single-track high-value medical consumables, the landscape of the high-value medical consumables sector has become complex. There is no predetermined path for industrial development, nor is there a perfect model for industrial transformation. Furthermore, the valuation logic for individual market segments has undergone significant changes.

How to Kick Off the Second Half of the Game? Domestic Neurointerventional Players Have Provided the Answer.

What is the current market landscape of the neurointerventional sector?

From the perspective of market development stages, China's neurointerventional market is in an early phase of rapid growth.

Although the neurointerventional sector is widely perceived as overheated, it is undeniable that it remains one of the fastest-growing segments in China. Its market expansion rate far surpasses that of other emerging sectors, and clinical demand for high-quality neurointerventional devices continues to surge.

An investor once described such a scene to VCBeat: in the hospital’s interventional suite, you can see a large number of opened neurointerventional packaging boxes—piled high like mountains.

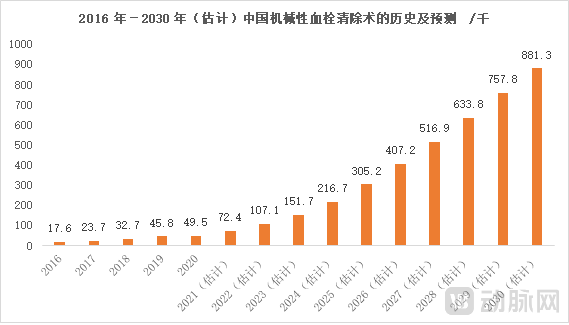

The Growth Momentum of Neurointerventional Procedures: Data show that the total number of neurointerventional procedures in China reached 120,000 in 2019 and rose to 160,000 in 2020, despite the impact of the pandemic. In 2019, the number of discharged patients with ischemic stroke exceeded 4.4 million, while those with hemorrhagic stroke approached 800,000. Supported by this substantial patient base, the volume of neurointerventional procedures is rapidly expanding, as market expectations had predicted.

Among the two major categories of neurointerventional procedures—ischemic and hemorrhagic—neurointerventional surgeries for ischemic stroke have developed rapidly, with a significant increase in surgical volume.

This is partly due to the increasing clinical recognition of neurointerventional therapy,Taking the treatment of ischemic stroke as an example, mechanical thrombectomy combining intracranial stent retrievers with catheter aspiration has gradually become a powerful tool for treating acute cerebral infarction, as demonstrated by multiple cohort clinical studies in recent years.

On the other hand, it is also related to the rapid market launch of domestically produced products.Companies with approved core products will be the first to reap the benefits of unleashed market potential. Currently, in the field of thrombectomy stents, Mindray Medical, GuiChuang TongQiao, and RuiKangTong have already received approval for their thrombectomy stents in China.

In terms of market structure, neurointerventional procedures are not confined to central hospitals in first-tier cities, unlike high-complexity interventions such as TAVR and electrophysiological ablation; the grassroots market has already become a primary growth driver. Currently, some county-level hospitals in China are capable of performing neurointerventional surgeries for patients with ischemic stroke. In 2021, the Chinese Medical Association released the "Primary Care Diagnosis and Treatment Guidelines for Ischemic Stroke (2021)."

Compared to the transcatheter valve market, where physician education is still in its early stages, the neurointerventional market is achieving faster adoption and volume growth. In contrast to the cardiovascular intervention market, whose competitive landscape has largely stabilized, China’s neurointerventional sector is poised to unlock greater potential as market acceptance rises and multiple products reach commercialization.

However, at this stage, most domestic players enter the market with individual products and lack competitiveness.

Single-product offerings have significant disadvantages. With the advent of the volume-based procurement (VBP) era, single products not only have limited resilience against VBP-related risks but also fall short in meeting clinical needs, as surgeons require a variety of products during procedures. Integrated solutions offer greater advantages in the intraoperative setting.

During a neurointerventional procedure, physicians utilize a variety of products, including access devices and therapeutic devices. A high-quality access catheter can enhance the success rate of the procedure. The precise coordination among various surgical instruments makes an integrated solution more competitive.

For domestic neurointerventional companies, expanding from single-product breakthroughs to a full product portfolio is both an industry consensus and a significant challenge.

Taking ischemic stroke as an example, products for the treatment of ischemic stroke include thrombectomy stents, access catheters, microcatheters, and occlusion balloon catheters.

An integrated solution requires mastery of underlying polymer material technologies and suction technology platforms; in China, only a few companies possess expertise across these core technology platforms simultaneously.

Currently, in terms of product approvals, Mindray Medical can provide a complete suite of thrombectomy solutions.

Drawing on the development trajectory of the coronary intervention market, the domestic market will ultimately accommodate no more than three leading Chinese manufacturers. The key to widening the gap between the top-tier players and the second tier lies in multiple dimensions: independent R&D capability serves as the foundation for sustained innovation, a diverse product portfolio constitutes a critical moat, and localized commercialization capability is essential for future cash flow generation. For leading enterprises, the crux lies in delivering tangible performance, with all these factors being pivotal.

From the perspective of the current competitive landscape, the financial reports of several leading domestic neurointerventional companies have shown impressive performance.

Xinwei Medical’s thrombectomy stent was launched in December 2020, becoming the first commercially available complete set of stent retriever devices in China. This product serves as Xinwei Medical’s core offering. In terms of financial performance, the company reported revenue of RMB 30.12 million and gross profit of RMB 19.05 million in the first half of 2021, representing a year-on-year revenue growth of 1,287%.

In the first half of 2021, Peijia Medical generated RMB 42.31 million in sales revenue from neurointerventional products, representing a 197.1% increase compared to the approximately RMB 14.24 million recorded during the same period in 2020. In the first half of 2021, TransMedics’ neurovascular intervention revenue amounted to RMB 42.91 million.

As several leading domestic companies accelerate high-speed commercial monetization, China’s neurointerventional sector enters the second half of its journey, marked by extensive market expansion.

While both neurointervention and interventional valve procedures are experiencing significant growth, their underlying growth logics within the interventional sector differ. The unique characteristics of neurointervention dictate that its market will evolve into a decentralized, networked structure rather than a centralized one.

The “nodes” that constitute the neurointerventional network market are precisely China’s primary healthcare institutions. Professor Liu Jianmin, a leading domestic expert in neurointervention, often states in interviews: “Every second counts for stroke patients; each one is as precious as gold.”

Stroke patients experience acute onset and have a narrow therapeutic window for treatment, making long-distance transfer impractical. Rapid intervention must be administered at the best-equipped local hospital, which is typically the county-level hospital. The grassroots market represents a key future growth driver for the neurointerventional market.

In the past, as an emerging therapeutic approach, neurointerventional procedures were primarily performed in large hospitals, with relatively low penetration rates. With the promotion and upgrading of neurointerventional devices, numerous neurointerventional products have been adopted by hospitals and physicians across China, leading to a continuous increase in the penetration rate of neurointerventional surgeries.

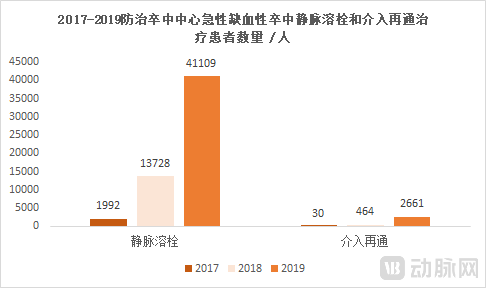

In China, there are over one million new stroke cases annually, yet only 49,000 mechanical thrombectomy procedures were performed in 2020, indicating a very low penetration rate.

To achieve higher market share and realize genuine domestic substitution, Chinese neurointerventional companies must strive for greater competitiveness in the future.The market development trend involves both securing influence at central hospitals and expanding into the primary care market.。

The deployment of neurointerventional services at the primary care level is a key focus of the tiered diagnosis and treatment policy and stroke prevention and control. Liu Jianmin, Director of the Clinical Neuroscience Center at Changhai Hospital Affiliated to Naval Medical University, once pointed out: “While coronary intervention has been widely adopted in county-level medical institutions, neurointervention has not yet become commonplace even at the prefecture-level. The most important task for the nation and the industry over the next five years is to ensure that 60% to 80% of county-level hospitals master the basic techniques of neurointervention.”

Both multinational corporations and emerging players have recognized the potential of grassroots markets. The aggressive expansion of emerging market teams by multinational medical device companies in recent years is evident from the hiring activities of firms such as Medtronic and Boston Scientific.

In fact, the primary healthcare market is one where domestic products hold a competitive advantage. This segment exhibits low dependence on imported brands, prioritizes manufacturer services, and involves patients who are more price-sensitive. Domestic medical device manufacturers offer more affordable pricing and possess a deeper understanding of the needs of Chinese physicians, all of which enhance the competitiveness of local enterprises in vying for share in the primary healthcare market.

Taking Xinwei Medical as an example, the company has expanded its presence in the primary healthcare market through initiatives such as educational training and channel penetration into lower-tier markets. Xinwei Medical established a special fund for stroke care to help primary-care physicians better master neurointerventional procedures, thereby facilitating the adoption of these techniques at the grassroots level.

In terms of channel layout, Xinwei Medical is increasing its penetration into the primary hospital market. On the basis of consolidating its existing market advantages, it is exploring new market demands and extending its products to the grassroots market, with the goal of covering 80% of the market.

In the Second Half of Neurointervention, Leading Companies Continuously Evolve; Their Influence Extends Beyond Individual Segments, and the Competition and Struggles in This Phase Resonate in Sync with the Entire Medical Device Sector.

If we view the landscape of China’s medical device industry as a jigsaw puzzle, its pieces were once distinctly separated. Today, however, this industrial landscape has undergone profound changes beneath the surface.

First, there has been a rapid proliferation of specialized segments in recent years. China’s demographic dividend has created multiple high-value tracks within the interventional medical device industry, giving rise to numerous sectors such as neurointerventional devices, transcatheter heart valves, cardiac electrophysiology, surgical robots, pulmonary intervention, cardiac rhythm management, and continuous glucose monitoring (CGM).

Numerous innovative companies have emerged in these niche sectors. With the introduction of Chapter 18A of the Hong Kong Stock Exchange Listing Rules and the launch of the STAR Market, the golden age of China’s medical device industry has officially begun.

However, reliance on a single innovation track can no longer sustain continued rapid growth. In particular, the nationwide implementation of volume-based procurement has cast a shadow over innovation in individual sectors, resulting in a scenario where innovations are critically acclaimed but commercially unsuccessful. While these innovation tracks have been highly sought after in the primary market, they have performed poorly in the secondary market, with domestic innovative medical device companies experiencing significant stock declines recently.

This change has also led to another major shift in the landscape of the medical device industry,Traditional business boundaries have been broken. Over the past two years, a clear trend in the medical device industry has been integration and platformization.Multiple enterprises are positioning themselves as platform-based companies, widening the gap with those focused on vertical sectors.

In the field of cardiovascular intervention, the most representative players are the Donord Medical group and the MicroPort group. Both have established portfolios in structural heart disease, peripheral intervention, renal denervation, surgical robotics, and electrophysiology, resulting in a high degree of overlap in their strategic layouts.

In the field of neurointervention, MicroPort NeuroTech recently announced capital increases for three subsidiaries, stepping up investments in electrophysiology, pulmonary intervention, surgical robotics, and other sectors.

Pulmonary intervention represents an extension of Vessel Medical’s neurointerventional technology platform. In the field of pulmonary intervention, Vessel Medical has deployed thrombectomy stents, aspiration thrombectomy systems, and balloon catheters for pulmonary embolism, as well as endobronchial valve (EBV) products.

Pulmonary interventions represent a market valued at hundreds of billions. In terms of disease mortality, pulmonary embolism ranks as the third most common vascular disease globally, alongside ischemic heart disease and stroke. The treatment of myocardial infarction and stroke has already spawned markets worth hundreds of billions, whereas the treatment of pulmonary embolism remains in its early stages of development. Interventional therapy for pulmonary embolism is regarded as one of the most valuable new frontiers in the interventional field over the next decade.

Bronchial valves offer a novel therapeutic strategy for patients with refractory pneumothorax. Compared with conventional surgical interventions, this procedure imposes relatively lower demands on cardiopulmonary function, making it tolerable even for patients with debilitated physical conditions.

In the electrophysiology sector, Xinwei’s strategic approach focuses on cryoablation for atrial fibrillation treatment, which, together with its left atrial appendage occluder, creates a one-stop solution for preventing cardioembolic stroke.

Xinwei Medical is also building a computer-aided technology platform to consolidate its advantages in existing fields by developing vascular interventional robots, while simultaneously researching and developing neurosurgical navigation systems.

Through a platform-based strategy, companies can transcend the limitations of a single track and widen the gap with vertically focused enterprises.

Amid gradually shifting market dynamics, niche segments of the industry chain will continue to consolidate and evolve. The transition from a single-segment player to a platform-based enterprise places greater demands on a company’s comprehensive competitiveness. To grow into a true platform-based enterprise, a company must possess sustained innovation and product output capabilities, localized commercialization channel capabilities, and a forward-looking global perspective.

To successfully make the daring leap from a single-track business to a platform-based enterprise, Chinese companies must first position themselves around globally forward-looking innovative technologies. While underlying technologies driving medical innovation continue to surge, high-level redundant development should be avoided. Vertical-sector companies seeking to transform into platform enterprises need to build composite, multi-dimensional technology platforms.

Meanwhile, evolving into a platform-based enterprise also requires ensuring robust local commercialization capabilities and strong product promotion capabilities.

The medical device industry represents hard-core technological innovation, with high-end medical equipment being one of the key development areas for the sector during China’s 14th Five-Year Plan period. Enhancing core technologies is crucial to achieving import substitution in the domestic high-end medical device industry. The global manufacturing hub for high-end medical devices is continuously shifting toward China. It is foreseeable that China will give rise to globally competitive medical device enterprises; indeed, the platform-based strategies adopted by domestic companies indicate that the first steps toward building global platform enterprises have already been taken.

Those who walk on frost know that severe cold and freezing are imminent; enterprises that sense market changes in advance and make strategic layouts are believed to welcome spring sooner.