Oral Healthcare Chain Sector Accelerates with Over 10 Companies Securing Funding: Who Is the Top Dark Horse? | 2021 Year-End Review

As 2021 draws to a close, the fervor in the dental chain industry shows no signs of abating.

As of December 23, a total of 14 financing deals (involving 13 companies) occurred in the dental chain industry this year, averaging one deal per month, with the total financing amount exceeding RMB 3 billion.It is worth noting that Meiwai Dental secured two rounds of financing within a year, with a single round exceeding RMB 1 billion, while Arrail Dental completed its Series E financing of nearly USD 200 million, representing some of the largest financing amounts in the industry in recent years. Additionally, Arrail Group, China Dental Care Group, and Yaboshi Dental have all filed their prospectuses.

In addition to the high frequency of financing,This year, investors making substantial financial bets on the dental chain sector are also highly diverse.This includes internationally backed institutions such as SoftBank China, OrbiMed, and Temasek; renowned domestic firms and enterprises such as Fortune Capital, Cypress Capital, and New Hope Group; as well as numerous industrial capital entities including Yizhuang State-owned Investment and Hubei Zhongyuan Jiupai.

The Capital Rush Reflects Renewed Confidence in the Dental Chain Healthcare Industry: In the consumer healthcare segment of dentistry, China has produced Topchoice Medical, a standout stock that surged 28-fold over ten years. Its share price performance has not only outperformed the vast majority of listed companies but also ranked among the top in the pharmaceutical industry.

However, it is important to note thatDespite the industry’s promising outlook, it is also a sector where high-quality investment targets are extremely scarce.There are three core reasons: first, private hospitals (clinics) are subject to strict government regulations, making it difficult to recruit high-quality physicians; second, hospitals (clinics) cannot operate solely for profit, as they bear significant social responsibilities and face high public opinion risks; third, due to the unique nature of medical care, any medical accidents or disputes not only endanger patients’ lives but also deal a severe blow to investors.

Thus, within the venture capital landscape over the years, investor interest in dental chain clinics has fluctuated, fundamentally reflecting an assessment of whether the industry’s myriad challenges have been addressed. ThereforeThe emergence of new technologies and business model variables often attracts active bets from investors. Dark horse companies at the forefront of industry waves are inevitably prime targets sought after by capital.

So this year, has the dental chain sector, which has strongly attracted over RMB 3 billion in funding, unveiled any new narratives?

The dental industry has always been a golden track that investors flock to. Why?

This is due to the deepening aging population in China, which has led to a gradual rise in demand for oral health services. Additionally, given the strong “consumer-driven” nature of the dental care sector, users’ willingness and frequency to spend on dental services have increased.Driven by China’s vast population base and high prevalence of dental diseases, along with growing acceptance of high-ticket orthodontic, implant, and restorative procedures, the potential demand market is being further unleashed. According to a report by Zhiyan Consulting, China’s oral healthcare services market is projected to reach approximately RMB 200 billion in 2024.

Faced with vast market potential, a surge of capital has flooded into the sector, driving rapid growth in the dental industry.“We also co-invested in a dental chain clinic in 2017, riding the wave of market enthusiasm at the time, and its valuation doubled by 2018,” an investor who wished to remain anonymous told VCBeat. “The sudden surge in industry hype was indeed somewhat unexpected.”

However, dental chain organizations quickly hit the “brakes”: Affected by the pandemic and related policies, many patients in first- and second-tier cities have returned to public hospitals over the past two years. Dental hospitals (clinics) that rely on high-cost customer acquisition strategies, such as prime locations and advertising marketing, are facing increased operational pressure:This directly exposes the numerous challenges faced by dental service providers in achieving profitability.

Specifically, under compliant operations, the net profit margin of a dental service provider typically accounts for approximately 15% of its revenue, which is far from the exorbitant profits rumored in public discourse. “As more players enter the market, maintaining a net profit margin of 10% would be considered quite respectable,” said the aforementioned investor.

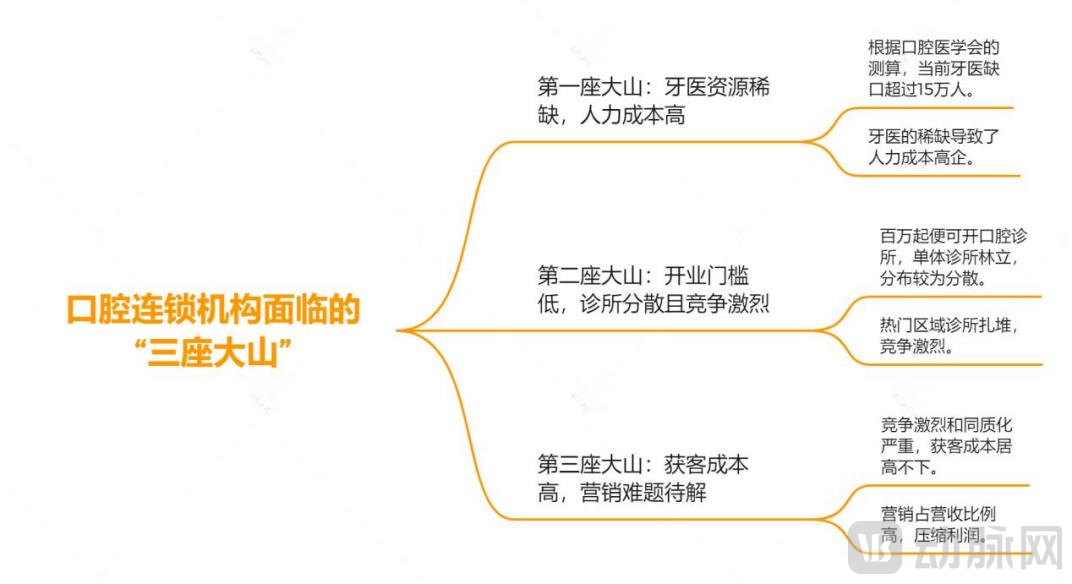

The underlying reason lies in the fact that,Dental healthcare service providers face various challenges in talent, technology, market, marketing, and management during their chain expansion, which dilute profits and prevent the effective realization of economies of scale.In summary, there are roughly “three major hurdles” to overcome.

The first major challenge is the scarcity of dental professionals and high labor costs.According to the Health Statistical Yearbook, the number of registered dentists in China was only about 200,000 in 2018, meaning there were 150 dentists per million people, whereas most developed countries abroad have between 500 and 2,000. According to estimates by the Chinese Stomatological Association, the current shortage of dentists exceeds 150,000. The scarcity of dentists has led to high labor costs.

The second major challenge is the low barrier to entry, resulting in a fragmented clinic landscape and intense competition.Opening a dental clinic requires an initial investment of approximately RMB 1 million, while investing in a medium-sized clinic ranges between RMB 2 million and RMB 3 million. As a result, there is a proliferation of standalone clinics with relatively dispersed distribution. In some high-demand areas, the growth rate of clinics has outpaced both the covered population and the number of dentists, leading to increasingly fierce competition.

The third major challenge is the high cost of customer acquisition, with marketing difficulties yet to be resolved.Due to intense competition and severe homogenization, customer acquisition costs for dental service providers have remained persistently high. According to the prospectus of Dr. Ya, its marketing and promotional expenses amounted to RMB 133 million, RMB 172 million, and RMB 140 million in 2018, 2019, and 2020, respectively, accounting for approximately 21%, 19.54%, and 16.79% of its revenue. Even leading industry platforms maintain marketing expense ratios around the 20% mark; therefore, smaller, fragmented independent dental clinics face even greater pressure from marketing costs if they seek to acquire customers.

Based on the above factors, in an interview with VCBeatMost investors have stated that although dental chain groups appear promising, it is extremely difficult to identify high-quality investment targets.The core logic is that the dental chain business is capital-intensive, as each store expansion requires substantial funding, compounded by the difficulty of standardization and elevated risks.

Investment also requires consideration of returns. According to past research, the expected investment cycle for dental chains is generally 5 to 10 years, with some even longer, so short-term losses are inevitable.

From a long-term perspective, risks are also difficult to control. Constrained by the “three major burdens,” dental healthcare service providers face significant challenges in expansion, making it difficult to rapidly extend their service coverage radius. Once they expand across regions, maintaining consistent medical quality among geographically dispersed facilities becomes challenging. Any medical malpractice incidents or negative publicity could severely damage the brand reputation built over many years.

Therefore, an observation of the market landscape reveals that,Leading dental chain enterprises in China share a common characteristic: regional concentration.For instance, Topchoice Medical is primarily concentrated within Zhejiang Province, Dazhong Stomatology focuses on Central China, and More Dental is mainly based in the Jiangsu-Zhejiang-Shanghai region... Clearly, market participants are maintaining a cautious approach toward expansion beyond their home provinces and nationwide growth.

In light of this current situation, what new explorations has the dental chain industry undertaken?

What explorations has the industry undertaken to address the challenges of scaling in chain operations? What new changes have emerged this year, and why have they attracted a surge of capital investment? Next,This article examines the market conditions and strategic layouts of leading dental chain enterprises in China and the United States to identify where the transformation opportunities lie for the dental chain industry.

First, let’s examine the overall landscape of the U.S. dental care services market.

According to a report by China Research Intelligence, the U.S. dental services market is valued at approximately $120 billion, with a compound annual growth rate (CAGR) of around 3%. Dental clinics and dental hospitals account for a ratio of 9:1, with clinics serving as the dominant force.

Why? This is because, after years of practice, most dentists aspire to own their own clinics and choose to start their own businesses. Therefore, in terms of the fundamental market structure, there are significant similarities between the United States and the Chinese domestic market:In the private market, small and scattered dental clinics are the mainstream.However, the issue is that although dentists possess extensive clinical experience and strong professional competence, they lack expertise in non-clinical areas such as clinic operations, legal affairs, finance, and management.

In response to this, a large number of Dental Service Organizations (DSOs) have emerged in the United States. TheirThe core is to provide non-clinical business support services for dentists and dental clinics., thereby enabling dentists to devote more energy to advancing clinical techniques and treating patients.

In the United States, dental clinics affiliated with Dental Support Organizations (DSOs) account for more than 10% of all practices. The top three DSO companies in the U.S. are currently Heartland Dental, Aspen Dental, and Pacific Services, which operate over 1,000, more than 800, and over 600 clinics, respectively. In terms of growth, the U.S. DSO market expanded at a compound annual growth rate of 19% from 2015 to 2020, significantly outpacing the average annual growth rate of 4% seen in the broader dental market.

Take Heartland Dental as an example. Founded in 1997 by Dr. Rick Workman, Heartland Dental originated from two dental clinics in Illinois, USA. Currently, Heartland Dental provides services to 1,400 dentists across 37 states and has entered into a strategic partnership with American Dental Partners Incorporated, another leading U.S. dental support organization (DSO), this year, resulting in a certain degree of resource integration between the two parties. It is evident that the path of chain expansion is accelerating.

Since acquiring its first dental group, MidSouth Dental Partners, in 2000, Heartland Dental has been on its M&A journey for 21 years. A key milestone occurred in 2017 when the globally renowned private equity firm KKR entered the scene and provided strategic support, bolstering Heartland Dental’s capital reserves and enabling it to double its number of clinics over the following four years.

What Did Heartland Dental Do Right to Achieve Rapid Scaling?

After sorting out its business logic,Beyond the aggregation effect brought by the DSO model, what is more important is the underlying logic behind this model: the continuous deepening of efforts in digitalization and dentist empowerment.

For example, to advance digitalization, Heartland Dental has built the largest Invisalign provider network, completing over 50,000 collaborative cases to date. Moreover, Heartland Dental has undertaken the largest-scale deployment of intraoral scanners within its organization, providing thousands of scanners to its supported practices. These seemingly asset-heavy initiatives have significantly enhanced standardization and efficiency across its clinics.

In terms of dentist empowerment, Heartland Dental has been deeply exploring dentists' needs. For instance, it launched the “A Company of More” campaign to understand and address the support dentists require in their daily practice. Additionally, Heartland Dental collaborates with leading dental product and technology companies to facilitate dentists’ access to new equipment and technologies. Furthermore, Heartland Dental operates a dedicated Management Information System (MIS). The MIS team assumes full financial responsibility and provides dentists with comprehensive financial reports, including monthly and quarterly financial statements, monthly and quarterly bonus calculations, daily tracking sheets, and performance metrics.

It is on this basis that the chain expansion model for dental clinics has been successfully validated. The official website shows that 82% of dentists supported by Heartland Dental expressed satisfaction with the services provided by Heartland Dental, and 15% of the clinics achieved revenue growth within their first year alone.

Let us now examine the overall situation of China's dental medical services market.

According to data from iiMedia Research, China currently has more than 90,000 dental medical institutions, which can be broadly categorized into three types: dental departments in general hospitals, specialized dental hospitals, and dental clinics. In 2019, dental clinics accounted for 88% of all categories, dental departments in general hospitals made up 11%, and specialized dental hospitals comprised only 1%.

From the perspective of leading enterprises’ development strategies, the focus is primarily on establishing a presence in both dental clinics and dental hospitals. Most of these companies operate both types of facilities, albeit with varying proportions.In terms of specific explorations, companies vary in their approaches.

For example, Arrail Group, which filed its prospectus this year, positions itself as a mid-to-high-end brand in the private dental clinic sector and has accumulated an extensive medical case database over more than two decades of development. Happy Dental, which garnered interest from industrial investors such as Yizhuang State-owned Capital Investment this year, is advancing the productization of diagnostic and treatment services, the digitization of consultation plans, and the standardization of business processes.

Meiwei Dental, which secured two rounds of financing this year, is continuing to exert strong efforts in the “healthcare + technology” sector.It adopts a distinctive “DSO” model to aggregate dental entrepreneurs and medical institutions, continuously providing these entities with comprehensive empowerment spanning strategic investment, standardization, clinical technology enhancement, brand management, and digital transformation, thereby facilitating their rapid, personalized development.

In terms of medical services, Meiwei Dental prioritizes the cultivation of outstanding dental professionals. Initiatives such as the Meiwei DSO Empowerment 2.0 Advanced Management Course and the M-Wei Sharing Session held this year, along with the strategic goal of establishing an “Industry-Academia-Research Innovation Alliance” at its inception, demonstrate this commitment. By collaborating extensively with numerous prestigious domestic and international dental schools, Meiwei Dental engages in deep cooperation across academic forums, clinical teaching, scientific research innovation, and medical technologies. This approach facilitates the establishment of a scientific research innovation system and a physician group, thereby enhancing the clinical skills, service philosophies, and overall service standards of talent within dental institutions. Leveraging resources from renowned medical experts both domestically and abroad, Meiwei Dental has gradually built a diversified, international talent development platform that includes the “2017 Meiwei Implantology Forum,” the “Meiwei Dental Medical Case Competition,” the “China MaxiCourse® Implantology Training Program,” and overseas visiting scholar programs.

In terms of technology, Meiwu Dental has partnered with Weixin Technology this year to jointly develop a standardized and intelligent hospital infection management system centered on the “Meiwu Site Safety Code.” The methodology underpinning the “Site Safety Code” is derived from DNV’s approach to hospital infection risk management. It integrates DNV’s healthcare standards, best practices in risk management, HSE and quality management systems, and maturity-based safety rating criteria. This initiative not only standardizes public health management within outpatient clinics but also establishes an updated standard system implemented after adhering to DNV-related standards, thereby empowering the digital and intelligent upgrading of dental healthcare institution management through technology.

As of now, Meiwei Dental has established nearly 200 dental clinics and hospitals across core urban clusters in China. Its self-developed Wei Xiaomei Medical Cloud Intelligent Management Platform covers 95% of its own clinics and hospitals. Backed by a high-quality team of business partners, the company has reported positive operating cash flow and profits for the past two consecutive years. This demonstrates that Meiwei’s distinctive “DSO” model has been successfully validated and has gained strong market recognition.

Under Meiwei Dental’s business partner mechanism, dentist-owners become the managers of new clinics. Empowered by Meiwei’s distinctive “DSO” model and the continuous advancement of its “technology + healthcare” strategy, the company not only helps dental institutions resolve operational challenges but also enables them to scale up and strengthen their market position, facilitating their growth into regional leaders.

In summary, although there are differences between the Chinese and U.S. markets, the core objectives remain consistent:Reduce costs and increase efficiency by enhancing digital capabilities, while making sustained efforts in the training and empowerment of dentists to improve the quality of medical services and maximize standardization, thereby facilitating scalability.

Leveraging the unprecedented enthusiasm in the primary market this year, dental chain enterprises that have secured funding are ramping up investments in both software and hardware infrastructure. They are either initiating or preparing to launch a new round of aggressive market expansion, while also striving for initial public offerings (IPOs).

During this process, the concentration of the entire oral healthcare industry will also rise significantly, and in the next 3 to 10 years, super dark horse enterprises with more than 500, or even over 1,000 clinics, will gradually emerge.

Looking ahead, how should the dental chain industry strengthen its core competencies? How will industry trends evolve? In response to these questions, Wang Xianzheng, Investment Director at Fortune Capital (Dachen Caizhi), shared the following insights with VCBeat, which can be summarized as follows:

First, the advancement of information technology accelerates the process of chain expansion.In healthcare service institutions, whether chain organizations or standalone clinics, the management of personnel, finances, and materials is essential; therefore, informatization construction has become critically important. Dental chain institutions equipped with comprehensive Hospital Information Systems (HIS) or Software-as-a-Service (SaaS) systems will significantly enhance management efficiency.

Furthermore, as institutions expand, informatization and chain-scale operations are mutually reinforcing. From a scalability perspective, informatization signifies enhanced replicability and synergy, which holds greater appeal for capital investors. It is worth noting that a newly opened chain store, empowered by the group headquarters, can attract customers and even achieve profitability in a shorter timeframe, with the information system serving as a key enabler of this empowerment. This is because an information system is not merely a tool, but also the digital embodiment of the group’s proven business processes.

Second, the rise of large chain groups will become an irreversible trend, further increasing industry concentration and reinforcing the dominance of leading players.Looking at the overall market, the vast majority of dental clinics are currently single-location practices or small chains with two to five locations. These enterprises exhibit weak operational consolidation, poor financing capabilities, and low risk resilience, leaving them utterly vulnerable in the face of sudden crises such as the COVID-19 pandemic. In the early stages of the outbreak last year, news of closures among small, fragmented dental clinics was frequently reported in the media.

Due to their strong advantages in financing and brand expansion, large chain groups can raise funds through equity financing, debt financing, and internal capital allocation within the group when facing unexpected situations. Therefore, they have strong risk resistance capabilities and can achieve resource synergy.

Third, enterprises that achieve better localization of the DSO model are more likely to emerge as leaders.The core function of a Dental Support Organization (DSO) is to provide clinics with support for non-clinical operations, including management, operations, finance, legal affairs, and training. This enables dentists to devote more energy to enhancing their clinical skills and treating patients. Essentially, this model serves to empower dentists.

Therefore, for enterprises adopting the DSO model, the key to gaining a first-mover advantage lies in how deeply and thoroughly they can integrate China’s national conditions with local realities. “Meiwei’s DSO model has achieved substantial localization and developed its own distinctive features,” said Wang Xianzheng, Investment Director at Fortune Capital (Fortune Smart Investment).

More importantly, in the healthcare services industry, the quality of care is a critical metric. The localization of Dental Support Organizations (DSOs) helps to gain insights into users’ differentiated needs, thereby ensuring that the quality of healthcare services is tangible and perceptible, ultimately delivering a superior service experience.

According to the "2020 White Paper on Oral Healthcare" released by VCBeat, China's total population grew from 1.34 billion in 2010 to 1.39 billion in 2017. With this expanding population base, the number of individuals requiring oral healthcare services also rose to 694 million. Overall, approximately 50% of Chinese residents suffer from various oral diseases, keeping demand consistently high. However, due to varying degrees of severity, most patients do not attach sufficient importance to their conditions. Consequently, a significant portion of the population remains untreated for oral diseases due to various reasons.The dental healthcare consumer market still has significant room for growth.

However, it is important to clearly recognize that there are significant differences between China’s oral care market and that of the United States.China’s doctor-patient demands, distribution structures, decision-making factors, payment systems, regulatory environments, patient acquisition channels, and other aspects all operate under distinct logics.Therefore, the team's understanding of the Chinese market is crucial in evaluating projects based on such new models.

As we stand at the end of 2021, we anticipate that the dental chain industry in 2022 will continue this year’s financing pace, with capital increasingly concentrated among leading enterprises as they move toward final pushes for initial public offerings.

However, in the process of rapid scaling up, issues such as profitability, level of informatization, and control over the quality of medical services will inevitably arise.

Therefore, looking ahead, every enterprise must strengthen its core competencies, proactively innovate, and embrace long-term value.