How Much Is the TAVR Market Worth After a 70% Crash? An Industry Valuation Report

One of the key objectives of in-depth industry research is to guide investment decisions. For such decisions, the valuation of industry sectors is critical.

In industry research, company valuation is common practice, yet sector-level valuation remains largely unexplored. VCBeat’s Sector Pricing Report Series aims to fill this gap by assessing the overall value of market sectors, thereby providing a reference framework for developing more rational investment strategies and more accurately estimating the value of investment targets.

When evaluating industry sectors, relying solely on revenue scale does not yield accurate conclusions; sector valuation is far more critical. Sector valuation differs from sector size: some sectors boast large revenue scales but suffer from weak profitability and extremely low long-term net profit margins, resulting in modest valuations. Conversely, other sectors may have unremarkable revenue scales, yet their strong competitive moats enable them to sustain high net profit margins, leading to potentially higher valuations.

TAVR (Transcatheter Aortic Valve Replacement) is the first report in our sector valuation series. Moving forward, VCBeat will continue to release a series of reports on related sectors.TAVR was chosen as the opening topic for the following three reasons:

First, TAVR was the absolute darling of the capital market before 2021, enjoying immense popularity. However, within less than a year, the market capitalization of the “Three Musketeers” of China’s TAVR sector (Venus Medtech, HeartFlow [Xintong Medical], and Peijia Medical) listed on the Hong Kong Stock Exchange plummeted by 70%. Through in-depth research, we perceive that the market is likely overly pessimistic. The pricing for the TAVR sector clearly lacks an anchoring benchmark, and there is no consensus regarding its intrinsic value.

Second, as a rapidly exploding market within the medical device sector, TAVR is not only an arena where domestically produced medical devices are shining but also one fraught with numerous unresolved controversies. These include bottlenecks in physicians’ learning curves and surgical volume capacity, debates over the effective number of self-paying patients, and concerns about anticipated price reductions due to volume-based procurement by national health insurance. However, these issues can be addressed with greater certainty through further detailed analysis. By conducting in-depth research to clarify market non-consensus and gradually guide consensus formation, this report on sector valuation delivers its core value.

Third, from a more granular perspective, we believe that although the market potential for transcatheter mitral valve replacement and repair (TMVR) in structural heart disease is expected to far exceed that of TAVR, and the technical barriers and complexity of transcatheter tricuspid valve replacement and repair (TTVR) appear to significantly surpass those of TAVR, TAVR remains the cornerstone of the entire transcatheter valve sector. The expansion of the TAVR market has laid a solid foundation for the development of TMVR and TTVR across multiple domains, including physician skill acquisition, patient education, and corporate R&D. In essence, a deep understanding of TAVR is a crucial prerequisite and foundation for comprehending TMVR and TTVR.

Due to space limitations, this article presents selected excerpts from the report. To read the full text, please scan the mini-program QR code at the end of the article to download it.

In early 2021, TAVR was the undisputed darling of the capital markets. In less than a year, the market capitalization of China’s “TAVR Trio” (Venus Medtech, HeartFlow [Xintong Medical], and Peijia Medical) plummeted by 70%. What has happened to the TAVR industry? What is the true valuation of the TAVR sector? Is it currently undervalued? How have industry growth rates and market potential changed? What factors should be prioritized in the short, medium, and long term? Could TAVR be impacted by national medical insurance reimbursement policies? If so, to what extent, and how would this affect industry valuation? Where is the future of TAVR headed? In this report, we provide answers to these questions through in-depth research and field investigations.

1Revisiting the Commercial Essence of TAVR: True Demand + Quality Products, Becoming Friends with Time in a Long-Term, High-Potential Sector

Medical devices represent one of the most dynamic fields for innovation; however, not every innovation can be successfully translated into a commercial product. Transforming an innovation into a viable product requires not only cutting-edge technology with high barriers to entry but also alignment with urgent clinical needs. Transcatheter Aortic Valve Replacement (TAVR) exemplifies a medical device innovation track that perfectly meets genuine clinical demands and constitutes a high-quality product.

1.1 Genuine Needs, Quality Products: TAVR Technological Innovation Drives Significant Value Creation

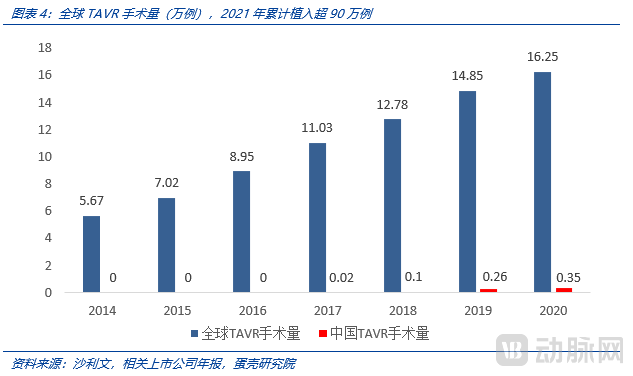

TAVR is a high-value product that delivers substantial clinical benefits, significantly improves patients’ survival and quality of life, and addresses a vast volume of unmet, inelastic real-world demand.Generally speaking, new products resulting from technological innovation do not necessarily address genuine needs or create clinical value. In contrast, TAVR delivers substantial real-world value. From a micro-level individual perspective, TAVR saves the lives of patients who are intolerant to conventional surgical procedures and significantly reduces the physical trauma and suffering associated with open-heart surgery. From a macro-level perspective, TAVR has achieved widespread adoption as a mainstream product, with cumulative global implants exceeding 900,000 cases; the annual global implant volume in 2021 was projected to surpass 180,000 cases.

Currently, the primary indication for TAVR is aortic stenosis (AS), with a smaller proportion of cases involving aortic regurgitation (AR). Aortic stenosis is a common cardiac condition in which the aortic valve functions as a “valve” to ensure unidirectional blood flow within the heart. As the aortic valve gradually becomes calcified with age, the valvular orifice narrows, leading to reduced blood flow. The main symptoms include fatigue, shortness of breath, angina, and syncope.

Prior to the advent of transcatheter aortic valve replacement (TAVR), the primary treatment modality was surgical aortic valve replacement (SAVR) via open-heart surgery. This procedure involves replacing the diseased valve with a prosthetic heart valve to restore normal blood flow through the heart. The conventional surgical approach entails a median sternotomy, cannulation for cardiopulmonary bypass, and induction of cardiac arrest. Under direct visualization, the surgeon makes an incision in the aorta to expose the aortic valve, excises it, implants the prosthetic valve, and sutures it into place. Following this, the heart is restarted, and the procedure is completed.

For patients, the pain associated with surgery is pervasive throughout the entire process. Many frail patients who are elderly, physically weak, or have underlying conditions such as diabetes cannot tolerate such a highly challenging open-chest surgical procedure.Prior to the advent of TAVR, such high-risk surgical patients had no therapeutic options. The emergence of TAVR has changed this landscape.

From a micro-level individual perspective:

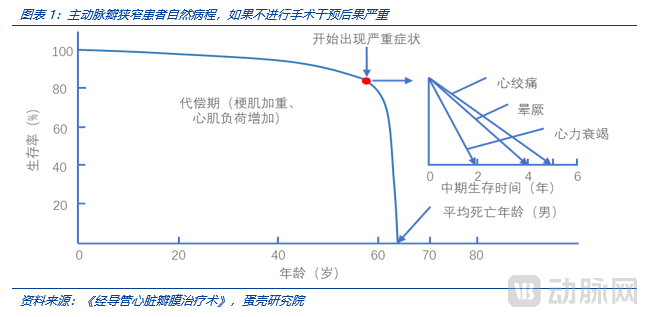

(1) Aortic stenosis carries a high risk; without timely surgical intervention, it severely impacts survival.Aortic stenosis increases the resistance to left ventricular ejection into the aorta, leading to typical clinical manifestations such as dyspnea, angina, and syncope. Without treatment, the condition progresses and can be life-threatening. The prognosis of aortic stenosis is correlated with its severity. In symptomatic patients, if valve replacement is not performed, the median survival is 5 years after the onset of angina, 3 years after the onset of syncope, and only 2 years after the onset of dyspnea. The PARTNER study showed thatFor patients with severe calcific aortic stenosis who are not suitable for surgical intervention, the one-year mortality rate reaches 50.7% following conservative management (without surgery).For asymptomatic patients with severe aortic stenosis, the majority will develop symptoms within 5 years, and the annual rate of sudden death is 1%.

(2) Prior to the advent of TAVR, the primary treatment option was surgical open-heart valve replacement, which is highly invasive (involving a 20 cm incision) and requires a prolonged recovery period (3–6 months). When patients presented with symptoms such as dyspnea and chest pain, and were confirmed to be candidates for valve replacement, open-heart surgery was generally performed in the absence of TAVR as an alternative. The procedure requires sternotomy, cardiac arrest, and direct visual replacement of the valve; even for experienced surgeons, the operation typically lasts more than four hours, posing a significant challenge to patient tolerance. Patients had to endure pain from a 15–20 cm incision, weeks of hospitalization, a lengthy recovery time, and a high risk of infection. Furthermore, patients who were unsuitable for surgery or at high surgical risk often had no surgical options available. For patients with severe calcific aortic stenosis who are not candidates for surgical intervention, the one-year mortality rate without surgery reaches 50.7%—meaning that more than half of these patients do not survive beyond one year.

(3)With TAVR interventional surgery, physicians replace the valve via a 1-cm vascular access incision, significantly reducing patient discomfort.For experienced TAVR operators, the procedure can typically be completed within one hour. Cardiac arrest is not required during the process, and some procedures do not even require general anesthesia. Patients can be discharged within three days after surgery (as early as the next day), with rapid postoperative recovery. It is particularly noteworthy thatPatients who are intolerant of surgical intervention or at high surgical risk can undergo TAVR, creating immense value in saving lives.

From a macro-level population perspective:

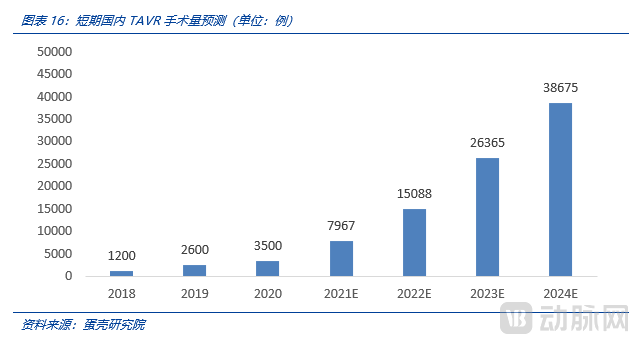

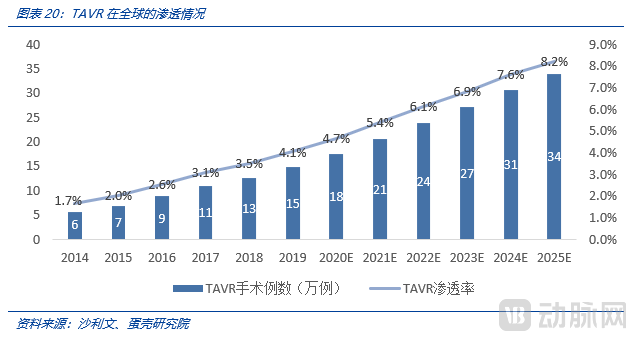

Globally, since the first human implantation of TAVR in 2002, cumulative implants have exceeded 900,000 cases across more than 40 countries. The high value of TAVR has been repeatedly validated; it is a truly superior product and an innovation in medical devices driven by strong clinical demand. In China, TAVR implantation volume has just entered a phase of rapid growth, with 3,500 procedures performed in 2020 and an estimated exceedance of 8,000 in 2021, indicating substantial room for expansion.

1.2 High Barriers, Low Substitutability: The TAVR Sector Exemplifies the Classic “Long Slope, Thick Snow” Investment Thesis

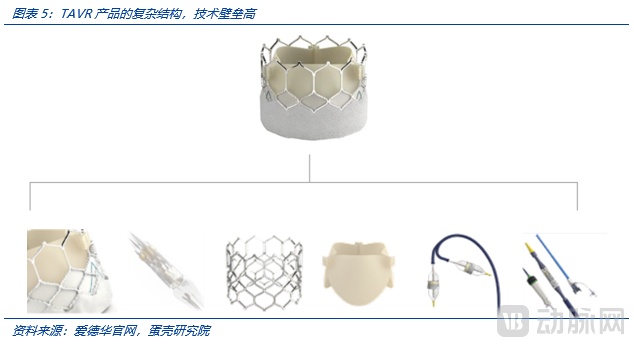

TAVR technology encompasses valve-related and delivery system-related technologies, presenting extremely high barriers to entry. The major overseas players are limited to four industry giants: Edwards, Medtronic, Abbott, and Boston Scientific.During valve design, it is essential to consider the anti-calcification durability of the leaflets as well as relevant hemodynamic parameters; otherwise, the valve is prone to calcific deposition and thrombus formation, thereby accelerating structural deterioration. Furthermore, regarding deployment mechanisms, there are various options including self-expanding, balloon-expandable, and mechanically expandable valves. The selection and trade-offs among these expansion methods reflect a company’s depth of understanding in both valve design and clinical application.The overarching design principles must account for the clinical outcomes following valve deployment, ensure ease of use and reliability for the operator, minimize post-procedural adverse events, and maintain controllable and affordable costs.For instance, adequate anchoring and support are required, imposing extremely high demands on the braiding of the valve stent and material processing techniques, as these factors directly affect radial force. To comprehensively address postoperative concerns, the upper crown section of the valve stent must feature a large-cell design to prevent coronary artery obstruction, thereby ensuring that percutaneous coronary intervention (PCI) remains feasible after transcatheter aortic valve replacement (TAVR). The lower end of the valve typically requires a skirt design (either external wrapping or conformal attachment) to minimize or prevent paravalvular leakage after implantation. The overall length of the valve should not be excessive, so as to enhance navigability through the aortic arch and avoid conduction blockage that could increase the need for permanent pacemaker implantation (PPI). Radial force must be precisely balanced: excessive radial force may cause displacement due to over-recoil during deployment, while insufficient radial force makes anchoring and positioning difficult, and incomplete valve expansion can accelerate structural deterioration. It can be said that behind every intricate design detail lies not only craftsmanship but also valuable experience accumulated at the cost of human life. Such products and technologies cannot undergo “rapid trial-and-error iteration”; instead, they demand rigorous design and testing, resulting in exceptionally high technical barriers.

On the other hand, TAVR has become a primary treatment modality for aortic stenosis (AS), exerting a certain substitutive effect on surgical open-heart valve replacement, owing to its robust clinical evidence regarding efficacy and adverse events (e.g., the PARTNER 3 trial).

Currently, all next-generation innovations in aortic stenosis treatment technologies are centered on transcatheter aortic valve replacement (TAVR) as the core technology (e.g., retrievability and repositionability).And no alternative technologies to TAVR have emerged.(From Pharmaceuticals to Medical Devices),International giant Edwards has been continuously optimizing its TAVR portfolio for over a decade, with its current primary strategy still focused on upgrading its transcatheter heart valve system.Although innovative products such as Leaflex are currently available for aortic valve repair, they are primarily targeted at younger patients for whom early valve implantation is unsuitable. These devices enhance leaflet mobility by disrupting aortic valve calcification through clamping forces. However, they cannot replace Transcatheter Aortic Valve Replacement (TAVR). Similar technologies, such as Valvosoft, which employs acoustic pressure waves to fragment calcified areas of the aortic valve, are also not comparable to TAVR in terms of efficacy. Instead, these repair devices are better positioned as adjuncts to TAVR procedures, particularly for patients with severe calcification. As supporting equipment expands and TAVR technology continues to iterate, TAVR procedures will become increasingly mature and better equipped to meet clinical needs.Therefore, from a medium- to long-term perspective, TAVR will maintain its mainstream position, with a very low likelihood of being replaced.

TAVR demonstrates immense potential for clinical value creation and commercial realization, underpinned by high technological barriers and long-term irreplaceability. Meanwhile, the technology continues to undergo iterative optimization—expanding indications from high-risk to low-risk patients, extending from aortic stenosis to regurgitation, overcoming contraindications for bicuspid aortic valves, and progressively lowering age requirements—thereby continuously enhancing therapeutic outcomes for both aortic stenosis and regurgitation.It can be said that TAVR is a veritable long-slope, thick-snow track.

2TAVR Implant Volume: 5-Fold Growth in 3 Years; Short-Term Surge Depends on Physician Training, Mid-Term Ceiling on Out-of-Pocket Affordability, and Long-Term Potential on Insurance Coverage

In China, TAVR implantation volumes are driven sequentially in the short, medium, and long term by three key factors: physician training progress, patients’ out-of-pocket payment capacity, and the extent of medical insurance coverage.

From a temporal perspective, the volume of TAVR implants in the short term (within three years) is primarily driven by the supply side—namely, the number of hospitals and physicians capable of performing TAVR procedures. It is evident that, in the short term, the effective demand from patients significantly exceeds the available supply. Therefore, the number of hospitals adopting TAVR and the number of physicians qualified to perform TAVR procedures determine the volume of TAVR implants over the next three years.

In the medium term, TAVR adoption is primarily driven by the number of self-pay patients with effective demand. Given the low likelihood of TAVR being included in China’s centralized volume-based procurement (VBP) under the national medical insurance scheme within the next 3–6 years, procedures will remain predominantly self-paid. Currently, the total cost of a TAVR procedure is relatively high, amounting to approximately RMB 300,000 per case (with device costs accounting for RMB 200,000). The size of the patient population in China capable of affording self-paid TAVR procedures determines the upper limit of TAVR implantation volumes during this “insurance coverage gap” period—this remains a major point of contention in current debates over TAVR implantation rates.

In the long term (after seven years), more than 10 domestic companies will have commercialized TAVR products in the Chinese market (with an additional 2–3 overseas companies likely completing product registration and launch in China). At that point, conditions will be ripe for inclusion in centralized volume-based procurement under the national medical insurance scheme, given the relative maturity of TAVR procedures and the sufficient number of suppliers. Consequently, the primary long-term drivers for TAVR will stem from the medical insurance reimbursement system and related policies. Once TAVR procedures are covered by medical insurance, a surge in demand is highly probable, enabling China’s TAVR penetration rate to catch up with those of Germany and the United States. However, volume-based procurement under medical insurance will almost inevitably lead to price reductions. Ultimately, the TAVR industry will be influenced by the combined effects of volume and price resulting from centralized procurement. Although centralized procurement lowers the end-user price of products, its impact on ex-factory pricing and profit margins for TAVR companies requires careful analysis (for instance, the sales expense ratio is expected to decline significantly post-procurement; this aspect will be elaborated in our subsequent analysis of pricing and profit margins).

2.1 Short-Term Growth Driven by Physician Training: Accelerated Coverage of Academic Training, Rapid Adoption of Simplified Surgical Techniques, and Product Innovations Reducing Procedural Complexity

We anticipate a fivefold increase in the volume of transcatheter aortic valve replacement (TAVR) procedures in China over the next three years. This growth is primarily driven by three factors: accelerated training coverage by manufacturers, rapid product adoption facilitated by simplified procedural techniques, and continuous reductions in procedural complexity coupled with improved implantation precision owing to retrievable delivery systems for both balloon-expandable and self-expanding valves.

First,Manufacturers are accelerating the coverage of academic training and promotional efforts, with diligent companies and dedicated physicians rapidly driving the widespread adoption of TAVR procedures.Taking Qiming Medical as an example, by the end of 2020, the company had a professional academic promotion team of over 100 members. It carried out diverse forms of academic promotion, which not only enhanced physicians’ surgical capabilities but also improved patients’ awareness of valvular heart disease, thereby accelerating the adoption of valve replacement surgeries. In 2020, the company conducted more than 2,000 surgical training sessions.

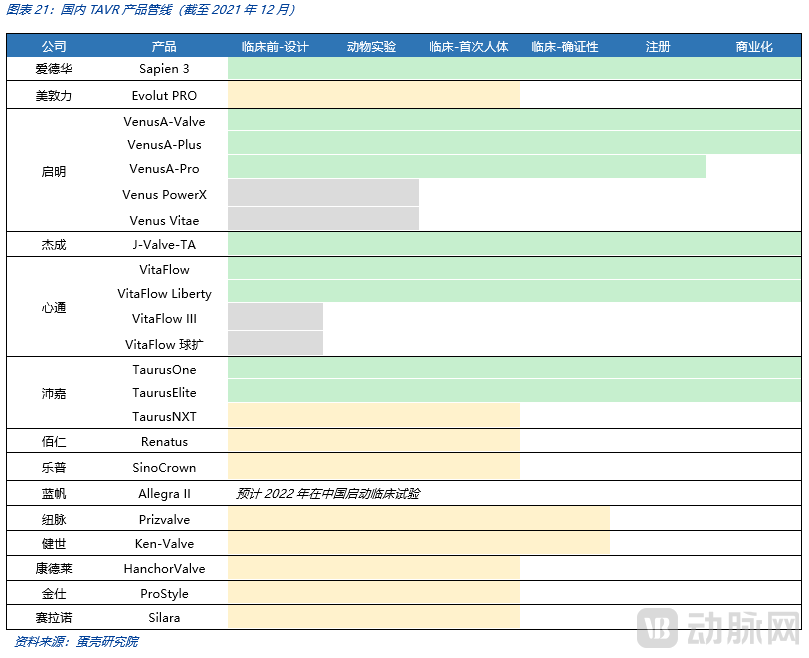

The results indicate that the promotion of TAVR in China has indeed entered a fast track.After VenusA obtained product registration in May 2017, Qiming accelerated the promotion of TAVR adoption in hospitals. The market launches of TAVR products by VitaFlow and Peijia Medical in 2019 and 2021 further accelerated this coverage process.

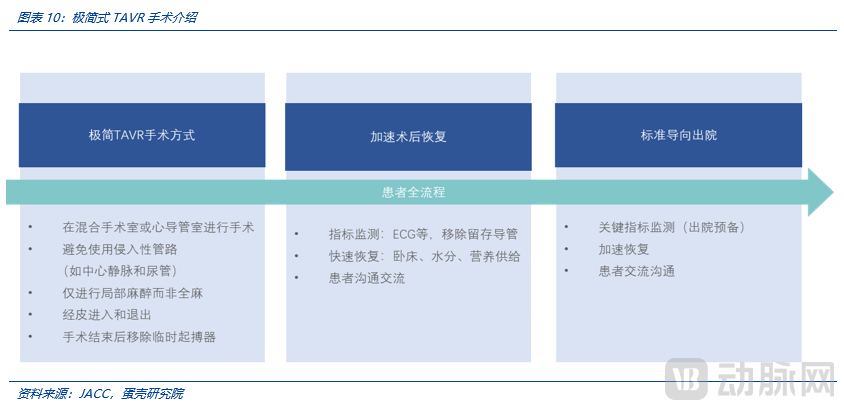

Second, as the technology gradually matures, minimalist TAVR has become an inevitable trend; the reduced complexity of TAVR procedures facilitates broader adoption.Non-minimalist TAVR requires a procedural duration of 2 hours (or longer, depending on the operator’s proficiency), whereas minimalist TAVR can be completed in as little as 30 minutes. Valve implantation itself is no longer the primary challenge; future metrics for assessing an operator’s surgical competence will shift toward procedural time (completion within 1 hour) and the number of valves implanted per procedure (a single valve per case, with no unplanned valve-in-valve procedures). Supply bottlenecks are expected to be resolved rapidly.

Minimalist TAVR refers to the restructuring of the clinical pathway for patients undergoing transcatheter aortic valve replacement (TAVR), guided by the principle of adopting less invasive approaches. It embodies the philosophy of “doing less to achieve more and better outcomes.” The most prominent feature of minimalist TAVR is that physicians avoid general anesthesia during the procedure, shifting from deep sedation under conditions resembling surgical operations to local anesthesia more akin to cardiac catheterization procedures.

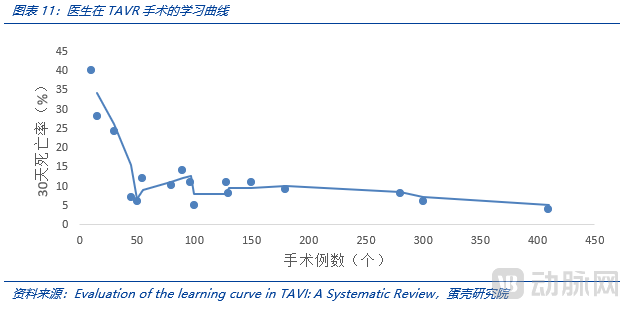

Third, the learning curve is no longer steep. The learning curve for TAVR with the first-generation valve (SAPIEN) was approximately 200 cases; after case number 201, centers demonstrated no further improvement in the composite endpoint of 30-day mortality or stroke. In contrast, the second-generation valve (SAPIEN 3) is easier to position than its predecessor and is associated with less paravalvular leak.

In studies on the Sapien 3, no learning curve or relationship between case volume and surgical outcomes was observed. With this generation of device, "centers should expect to achieve consistently excellent results, even during their early experience with cases."

Technological advancements are continuously reducing the learning curve for TAVR products. Previously, precise valve deployment was challenging; however, with advances in balloon-expandable valve technology, valve deployment has become more accurate and convenient. The development of 3D printing technology enables physicians to simulate the intraoperative anatomical environment preoperatively, thereby improving the success rate of first-attempt valve implantation. Furthermore, the market introduction of second-generation retrievable valves has reduced the need for second valve implantation. If a valve is malpositioned during the procedure, the system allows for repositioning and redeployment, further lowering procedural difficulty.Encouragingly, even Grade II Class A hospitals such as “Taishan People’s Hospital” have begun performing TAVR procedures, suggesting that the number of hospitals offering TAVR may exceed previous expectations, potentially reaching thousands.

Driven by three key factors—accelerated coverage of academic training, rapid promotion of simplified procedural techniques, and product innovations that lower technical barriers—surgical volumes at mature centers have increased significantly. To date, West China Hospital alone has completed over 1,300 TAVR procedures. Meanwhile, surgical capabilities at mid-tier and smaller hospitals, which are less mature in this field, continue to improve.

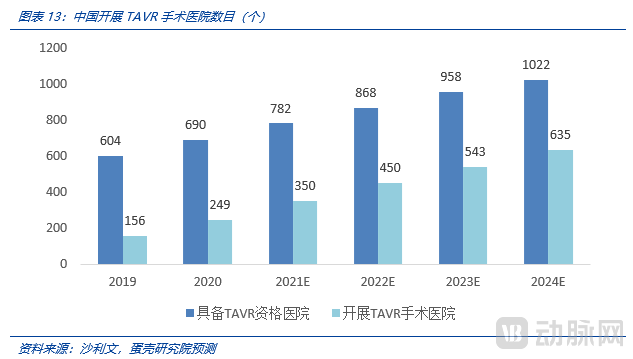

Hospitals performing more than 400 percutaneous coronary intervention (PCI) procedures annually are considered qualified to perform transcatheter aortic valve replacement (TAVR). The number of TAVR-qualified hospitals is projected to increase from 604 in 2019 to 1,022 in 2024.

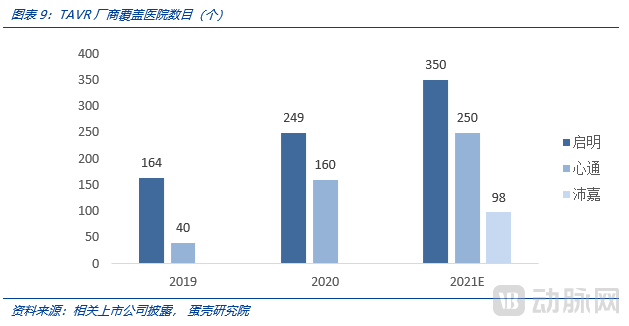

In 2019, the number of hospitals performing TAVR procedures exceeded 164; in 2020, it surpassed 249; and it is projected to reach 350 in 2021, which remains significantly lower than the total number of hospitals capable of performing TAVR. We believe that over the next three years, the number of hospitals conducting TAVR procedures will continue to grow at an annual rate of more than 100.

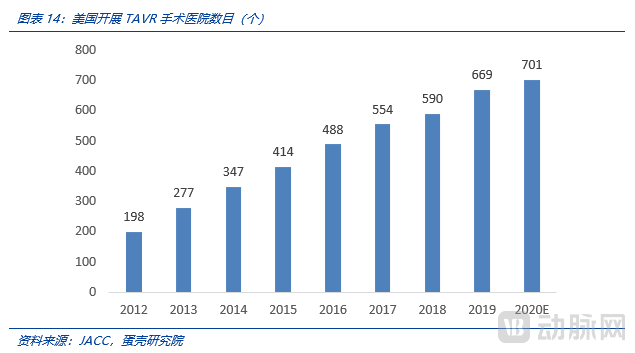

The expansion of hospitals performing TAVR procedures in the United States exhibits similar characteristics. The number of U.S. hospitals conducting TAVR procedures was 156 in 2012, increased to 348 in 2014, and reached 701 by 2020. Considering factors such as the strong enthusiasm among Chinese physicians for learning and the diligent promotional efforts by enterprises, the growth rate of hospitals offering TAVR in China is likely to surpass that of the United States. The number is highly probable to exceed 600 by 2025 and, in the long term, is likely to surpass 1,000.

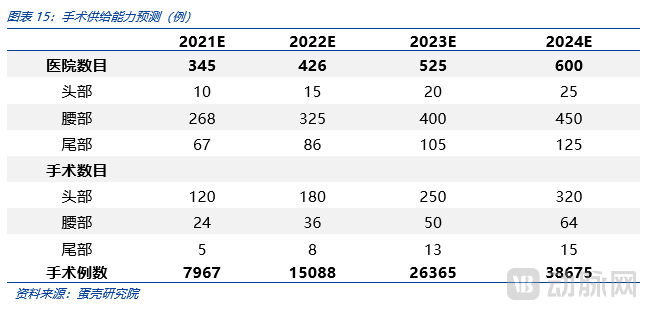

Over 600 hospitals have performed TAVR procedures within the past three years, with the number of cases expected to exceed 38,000 in 2024.In 2018, Fuwai Hospital performed a total of 124 TAVR procedures. By 2021, surgical volumes at the four major centers (Beijing Fuwai Hospital, West China Hospital of Sichuan University, The Second Affiliated Hospital of Zhejiang University School of Medicine, and Zhongshan Hospital Fudan University in Shanghai) began to grow significantly. Meanwhile, TAVR manufacturers are continuously expanding TAVR procedure adoption in other leading hospitals. Currently, there are approximately 20 leading hospitals, with an average annual surgical volume of over 100 cases per hospital. Considering the trend toward simplification of TAVR procedures and the continuous reduction in procedural difficulty (according to Dr. Wu Yongjian, Director at Fuwai Hospital, the difficulty of TAVR procedures during their maturity phase will not exceed that of PCI), the long-term annual surgical volume at leading hospitals could well exceed 1,000 cases. At present, mid-tier hospitals often have their department heads trained by leading centers in TAVR techniques. We assume that over the next three years, the number of mid-tier hospitals will grow rapidly, accounting for a significant proportion, with surgical volumes maintained at one-fifth of those at leading hospitals, ranging from 30 to 60 cases annually. Tail-end hospitals account for 20% of non-leading hospitals, with surgical volumes one-fifth of those at mid-tier hospitals, ranging from 5 to 15 cases annually.

2.2 Mid-term Ceiling Depends on Out-of-Pocket Payment Capacity: One-Fifth of Patients Can Afford Self-Pay, with the 100,000-Case Mark Not Yet Reaching the Ceiling

We believe that the likelihood of TAVR being included in the national volume-based procurement (VBP) program within the medium term (six years) is low; the primary growth driver will stem from the out-of-pocket payment capacity of both existing and new patients. Specifically, for the domestic market, we conduct our analysis across three tiers. The broadest tier, based on the number of incident cases (where timely treatment is required upon the onset of typical symptoms), represents the fundamental patient pool. The second tier is defined by clinical guidelines, indicating the number of patients with indications suitable for TAVR. The third, and most critical, tier concerns the actual base of self-paying patients—specifically, how many households possess the financial capacity to cover the RMB 300,000 out-of-pocket cost required to treat elderly patients aged over 70.

At the primary level, China has a vast patient population with pronounced late-stage symptoms and an urgent need for treatment. According to estimates based on data from Zhongshan Hospital of Fudan University, the prevalence of severe aortic valve disease among individuals aged 70 and above in China is approximately 1%, while the prevalence of severe aortic regurgitation is around 2–3%. The National Health Commission’s “2020 Annual Bulletin on the Development of Aging Causes” reports that the population aged 70 and above totals 116.62 million. The eligible population for TAVR procedures numbers in the millions (annual new cases); if indications are expanded to include regurgitation, the population size would reach two to three million. The total number of patients with severe aortic valve disease amounts to four million.

Second Level: From the perspective of treatment guidelines and expert consensus, the indications for TAVR are continuously expanding. Initially, US guidelines restricted TAVR use to patients at high surgical risk; however, its application has gradually extended to those at intermediate and low surgical risk. Due to initial concerns about valve durability, physicians limited transcatheter heart valve implantation to elderly patients. As clinical evidence increasingly validates the durability of these valves, TAVR is now being performed in relatively younger patients, positioning it as a competitive alternative to SAVR (surgical aortic valve replacement). Anatomically, bicuspid aortic valve (BAV) is highly prevalent among patients in China. Patients with BAV often present with severe and heterogeneous leaflet calcification, asymmetric leaflet size, and concurrent ascending aortic disease, which can lead to complications during the procedure such as valve migration, paravalvular leak, coronary artery obstruction, annular rupture, and aortic dissection. Consequently, BAV was considered a relative contraindication in early TAVR guidelines. However, given the high prevalence of BAV in China and the accumulation of procedural experience, this contraindication has been gradually overcome. BAV is no longer a contraindication for TAVR.

The evolution reflected in Chinese expert consensus statements and international guidelines—shifting “from high-risk to low-risk,” “from older to younger patients,” and “from tricuspid to bicuspid aortic valves”—has already expanded the eligible population for transcatheter aortic valve replacement (TAVR) to several times its initial size. Furthermore, advancements in device technology have enabled TAVR to provide a certain degree of therapeutic benefit for patients with pure aortic regurgitation (for instance, consideration may be given if two out of four anchoring points are suitable, although risks remain). The Qiming TAVR valve has been implanted in 100–200 patients with pure aortic regurgitation to date. Once aortic regurgitation is formally included as an indication for TAVR, the patient volume is expected to reach 2–3 times the current number of cases treated for aortic stenosis. Meanwhile, clinicians retain substantial decision-making authority; even if TAVR for aortic regurgitation is not officially incorporated into guidelines in the short term, off-label use will continue to increase.

Third Dimension: Out-of-Pocket Payment Capacity. Given the low likelihood of nationwide medical insurance coverage for TAVR procedures in the short term, we predict that TAVR surgeries will remain primarily dependent on patients’ out-of-pocket payments over the next six years. Consequently, patients’ ability to pay out-of-pocket has become a significant factor influencing the mid-term ceiling for the scale of TAVR procedures. According to the Hurun Wealth Report and various bank reports, the number of middle-class households in China reached 33.2 million in 2019, covering a population of approximately 100 million. Roughly calculating, if we consider that middle-class households with average assets possess the capacity to pay for TAVR surgery out-of-pocket—implying that 80% of patients lack such capacity—and combine this with the current population of 820,000 patients in China with aortic stenosis eligible for TAVR (assuming a three-year survival period, the annual number of deaths due to untreated AS approaches 300,000, suggesting approximately 300,000 new cases per year), then based on the 20% of households capable of out-of-pocket payment, the annual population with aortic stenosis who have the financial means to pay exceeds 100,000.

2.3 Long-term Outlook: Medical Insurance Coverage; Penetration Rate Benchmarking Against Germany and the US, with Annual Implant Volume Expected to Exceed 300,000 Cases

From a long-term perspective, reimbursement under the national medical insurance scheme is a critical prerequisite for the widespread adoption of transcatheter aortic valve replacement (TAVR). The long-term market potential for TAVR in China is significantly influenced by insurance coverage. If TAVR procedures are included in the national medical insurance reimbursement list, annual TAVR implantations in China could exceed 300,000 cases, benchmarking against Germany and the United States.

The high penetration rates of TAVR in the United States and Germany are primarily driven by insurance reimbursement coverage (mainly TK and AOK in Germany, and Medicare in the United States). The relatively comprehensive insurance coverage in both countries has facilitated the high adoption of TAVR.

In China, some local medical insurance schemes have begun to cover certain TAVR products. Taking the reimbursement policy for Edwards SAPIEN 3 in Henan Province as an example, the negotiated price under medical insurance is RMB 258,000, with patients covering 40% out-of-pocket and the remaining 60% reimbursed through provincial/municipal basic medical insurance or the New Rural Cooperative Medical Scheme (NRCMS). After reimbursement, the out-of-pocket cost for consumables amounts to approximately RMB 130,000 under provincial/municipal medical insurance and RMB 190,000 under NRCMS. MicroPort’s products are priced lower and have been included in medical insurance coverage in Guizhou and Yunnan provinces. In Guizhou, the out-of-pocket expense for employees covered by basic medical insurance after TAVR reimbursement is around RMB 70,000. Although there have been localized attempts to include TAVR in medical insurance coverage in certain regions, the conditions necessary for volume-based procurement are clearly not yet met.

Once covered by medical insurance reimbursement, implantation volumes are expected to increase significantly.Taking the development of percutaneous coronary intervention (PCI) as an example, in 2000, many regions in China had not yet included it in medical insurance coverage, and a total of 11,750 PCI procedures were performed that year. By 2018, as all provinces in China had included coronary stents in their medical insurance schemes, the annual volume of PCI procedures exceeded 910,000.

If covered by national medical insurance, the implantation volume would increase significantly. However, we anticipate that it is unlikely for the procedure to be included in the National Reimbursement Drug List (NRDL) and subject to centralized procurement before reaching an annual implantation volume of 100,000 units (detailed analysis follows).Based on the current status of Edwards and MicroPort’s inclusion in local medical insurance schemes, long-term national medical insurance coverage is inevitable. As out-of-pocket costs drop from RMB 300,000 to under RMB 100,000, TAVR implantation volumes will see a substantial increase. Due to the high gross margins in this sector, volume-based procurement (VBP) will not significantly impact its valuation. Subsequent chapters will discuss the anticipated timeline for VBP implementation and provide detailed calculations on its impact on the sector’s value.

2.4 Overseas Markets Are the Hidden Gem: Fierce Domestic Competition for TAVR in China vs. Persistent Global Shortage of TAVR

The commercialization of TAVR in China began in 2017, whereas the global market has already become a vast and rapidly growing sector, with over 200,000 procedures performed annually and generating $6.5 billion in revenue.

Although the domestic TAVR landscape in China is somewhat saturated and highly competitive, transcatheter aortic valve replacement (TAVR) remains a scarce technology globally and constitutes a critical bottleneck for most countries. Currently, the global commercial TAVR market is dominated by Edwards Lifesciences and Medtronic, which together hold a 90% market share. Other companies offering commercial TAVR solutions include Boston Scientific, Abbott, and NVT (acquired by Blue Sail Medical), while India’s SMT also possesses certain R&D capabilities. Apart from these, no other countries have established TAVR supply capabilities. From a business logic perspective, given the absolute monopoly and rapid market penetration by Edwards and Medtronic, it is unlikely that new TAVR startups will emerge in the global market. The development of China’s own TAVR industry is attributed to unique historical circumstances and the delayed approval of imported valves by the National Medical Products Administration (NMPA), which has been a stroke of luck for the Chinese TAVR sector. Therefore, expanding into the global market is an inevitable path for Chinese TAVR enterprises. It is foreseeable that the current competitive advantage of Chinese companies in the global market lies primarily in pricing, while their main disadvantage is the lack of global patent layout, which is controlled by companies such as Edwards and Medtronic. However, from a longer-term perspective, Chinese TAVR companies may develop distinct advantages in innovations related to bicuspid aortic valves, prevention of paravalvular leak, retrievability, and indications for aortic regurgitation (the incidence of aortic regurgitation is significantly lower in Europe and the United States than in China). Ultimately, their clinical outcomes could well surpass those of the current leading foreign brands.

Given the global market size of $6.5 billion, if Chinese brands can capture 5%-10% of the market, they will achieve an additional $4 billion in global sales. Furthermore, the current global market is primarily concentrated in regions such as the United States, Europe, and Japan, while penetration rates in South Asia, Africa, and South America are relatively low (or even non-existent). Expanding into these underserved regions will provide greater global growth opportunities for domestic TAVR companies.

3TAVR Pricing: Stable with a Slight Decline; Pipeline Products Awaiting Launch Do Not Impact Pricing, and Long-Term Volume-Based Procurement by National Healthcare Security Administration Does Not Affect Industry Profitability

The primary factors influencing TAVR pricing in the medium to long term are the competitive landscape of the industry and the intensity of centralized procurement under national medical insurance. We believe that while implantation volume is undoubtedly the key variable affecting the scale and growth of the TAVR industry, significant fluctuations in pricing could also substantially impact industry size—for instance, in the coronary stent sector, where price reductions driven by centralized procurement led to a contraction in market size. Our analysis of pricing will therefore focus primarily on the likelihood of price reductions, as the possibility of price increases appears limited at present.

3.1 The Queue of Products Under Development for Market Launch Does Not Affect Product Pricing: An Analysis Based on Competitive Strategy

A major factor influencing pricing is competition. We believe that although more than 10 domestic companies have TAVR pipelines in development, leading to a trend of intense internal competition (“involution”), irrational price wars are unlikely to succeed in capturing market share (merely triggering industry-wide retaliatory moves and causing overall harm to the sector). Therefore, a significant price decline driven by competitive pressures is improbable.

An analysis of the current TAVR pipeline reveals that a wave of new product launches is expected in three years. The market generally anticipates that, absent significant improvements in product functionality, technical sophistication, and clinical outcomes, the substantial upfront R&D investments will compel companies to adopt price competition strategies. This applies not only to established players with strong channel coverage such as Lepu Medical and Blue Sail Medical, but also to emerging innovators like Peijia Medical and Jian Shi Technology. However, the reality may prove more complex than anticipated.

A typical example is the TAVR promotion strategy of Venus Medtech. Despite adopting a low-price strategy—with end-user prices significantly lower than those of competitors and ex-factory prices substantially below competitors’, resulting in comparable channel incentive margins—it did not yield the unexpectedly strong results anticipated. Given that Venus Medtech, backed by the robust channel capabilities of the MicroPort system, still found it challenging to achieve desired outcomes through low pricing, it is even less likely for ordinary companies to capture market share by relying solely on price-based strategies.

If a price war fails to capture market share in the short term, subsequent price increases will become even more difficult, rendering such a strategy impractical. The likelihood of successfully using pricing as a disruptive tactic is low. Even if a price war leads to an increase in market share, it is inherently difficult to sustain long-term profitability (as market share may decline once competitors follow suit with price cuts). Therefore, unless there is a substantial pipeline of next-generation products, engaging in a price war holds little strategic value.

In fact, there is a certain degree of habit stickiness in the use of TAVR. Although product parameters do not directly reflect significant differences, clinicians perceive distinct variations during surgery. For instance, while Qiming Medical’s VenusA, VitaFlow Medical’s Vitaflow, and Peijia Medical’s TaurusOne all emphasize their superior radial support force in their product descriptions, our interviews reveal that Qiming’s VenusA feels the “stiffest” with the strongest radial support, VitaFlow’s Vitaflow feels the “softest,” and Peijia’s TaurusOne falls in between. This does not imply that greater radial support is inherently advantageous; however, when addressing specific indications, physicians tend to prefer products they are more familiar with and confident in using. For example, an overly stiff valve stent design combined with oversizing may generate forward elastic recoil during deployment, resulting in a tactile experience significantly different from that of other valves. Furthermore, VitaFlow’s electric delivery system offers a distinct user experience, and once physicians become accustomed to it, this also contributes to habit stickiness. In addition, manufacturers are attempting to further reinforce physician loyalty through training systems and other initiatives. While switching between systems poses little difficulty for leading experts, it remains considerably challenging for mid-tier physicians to master multiple valve delivery systems and adapt to their differing deployment tactile feedback.

From a practical standpoint, the primary strategy for companies with future TAVR pipelines is differentiation, with each seeking its own advantageous market.For instance, companies such as BaiRen and New Pulse primarily develop balloon-expandable valves, distinguishing themselves from the self-expanding valves pioneered by the earlier “Big Three.” Similarly, KangDuoLe’s HanchorValve incorporates a positioning device that enables leaflet anchoring, thereby addressing indications for aortic regurgitation (AR). Additionally, Lepu Medical’s SinoCrown features a shortened self-expanding valve design, which reduces the risk of coronary obstruction and permanent pacemaker implantation (PPI). Consequently, targeting niche markets with differentiated functionalities has become the primary competitive strategy for subsequent TAVR manufacturers, rather than engaging in simple price wars.

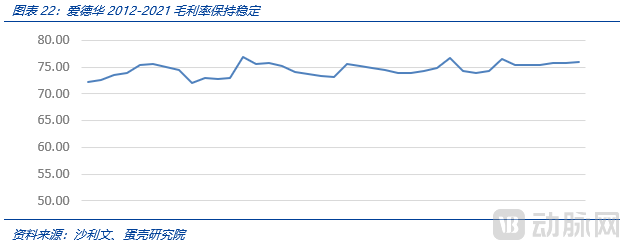

From a global market perspective, long-term market evolution has also established a favorable landscape. Edwards Lifesciences, the leader in the TAVR field, has maintained a high gross profit margin of 70–80% since 2012, demonstrating exceptional profitability. This indicates that the competitive landscape in the TAVR sector will consolidate during its mature stage, with gross profit margins remaining at elevated levels.

3.2 Long-term Volume-Based Procurement for Medical Insurance Does Not Affect Industry Profitability: An Analysis Based on Price Reduction Scenarios

Another factor influencing pricing is the centralized volume-based procurement under the national medical insurance program. However, we believe that while this policy appears to constrain prices at the terminal level, it may not necessarily lead to a substantial decline in ex-factory prices.The true trade-off is that patients’ effective demand will inevitably surge due to price reductions, while the impact on physicians’ motivation warrants careful analysis. On balance, we believe that even with centralized volume-based procurement (VBP), the momentum for TAVR is unlikely to decline significantly. This is because mastering TAVR represents a substantial value-add for interventional cardiologists; greater proficiency in TAVR opens up more opportunities for higher-value procedures such as TMVR and TTVR. If annual TAVR volumes reach 100,000 cases—a relatively optimistic projection based on the distribution of PCI across hospitals—this figure remains an order of magnitude lower than that of PCI. Whereas PCI may have previously offered stronger financial incentives for physicians, TAVR provides more pronounced professional drive through technical skill acquisition, as it serves as the foundational expertise for subsequent structural heart disease interventions. In summary, VBP does not exert a significant negative impact on physicians’ motivation.

Regarding the timing of national centralized volume-based procurement (VBP) for medical insurance, we anticipate that it is unlikely for these products to be covered by national medical insurance and included in VBP before reaching an annual implantation volume of 50,000–100,000 units (approximately within the next six years). Our analysis of the annual usage volumes of major medical consumables at the time of their inclusion in VBP shows that most cardiovascular consumables had already reached an annual usage level of hundreds of thousands, with some varieties exceeding one million units.

From the perspective of industry profit margins, we believe that if the price reduction from centralized volume-based procurement by medical insurance is less than 70%, it would be a significant benefit to the industry as a whole.We believe that during the critical initial years of the centralized volume-based procurement (VBP) program under the national medical insurance scheme, the National Healthcare Security Administration (NHSA) demonstrated an unprecedentedly resolute stance and intensity in driving down prices. Coupled with manufacturers’ lack of experience in bidding, this led to numerous instances of drastic price cuts (“ankle-chopping” reductions). However, as comprehensive evaluations of VBP’s overall impact are conducted and companies adopt more rational bidding strategies, we anticipate that the magnitude of price reductions in VBP six years from now will be smaller than current levels. On the other hand, VBP primarily targets end-user prices, with intermediate distribution channels serving as a buffer; consequently, the ex-factory prices for manufacturers may not necessarily decline significantly. Meanwhile, selling expense ratios are expected to drop substantially, meaning net profit margins may not necessarily decrease (note that current coronary stents do not conform to the above assumptions).

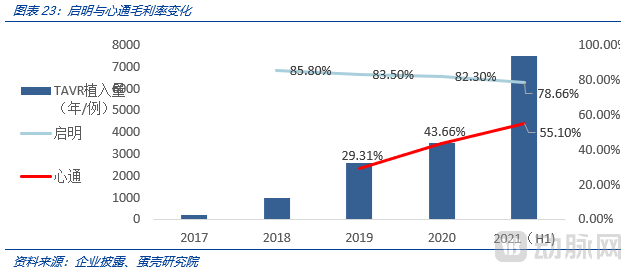

If the medical insurance price reduction reaches 70% of the current average price, the industry scale will still reach RMB 17.9 billion. The industry profit may exceed RMB 10 billion before R&D investment, and under the aggressive R&D investment assumption, the industry profit can reach RMB 4.8 billion.We conducted scenario analysis and stress testing on industry scale and corporate profitability following the implementation of centralized volume-based procurement (VBP) by the national medical insurance system. If VBP leads to a 70% price reduction, patients’ out-of-pocket expenses would decrease from RMB 200,000 to RMB 20,000, potentially enabling near-universal coverage of TAVR procedures across the eligible patient population (assuming an annual procedure volume of 250,000). Under this scenario, the total market size could reach RMB 17.9 billion. Although the industry’s gross profit margin would decline from 83% to 69% (a drop of 14 percentage points), the selling expense ratio would simultaneously decrease from 20% pre-VBP to 5%, thereby offsetting the impact of the reduced gross margin on net profit margins.

4Long-Term Trend Analysis of the TAVR Industry: High Growth + Large Market Potential; Major Oligopolies + High Profitability; Retrievability + Comprehensive Portfolio; Extended Durability + Expanded Indications

Four Major Long-Term Trends in the TAVR Sector: First, regarding industry scale, the TAVR market offers substantial growth potential and is expected to maintain a high growth rate. Second, in terms of competitive landscape, the leading tier is already well-defined; an oligopolistic structure is highly likely to emerge, with pronounced Matthew effects among top players, thereby sustaining high profitability within the sector. Third, concerning technological trends, the focus is on precise valve deployment to improve success rates and reduce adverse events. Balloon-expandable and mechanically expandable valves demonstrate clear advantages in achieving precise deployment, while self-expanding valves offer strong complementary value through their retrievability. Meanwhile, technologies such as 3D printing enable physicians to simulate valve positioning ex vivo, making implantation more precise and reliable. The reduction of adverse events is further supported by cerebral embolic protection devices (primarily reducing stroke incidence) and aortic valve repair and decalcification equipment (e.g., acoustic pressure wave technology). Fourth, regarding major challenges and bottlenecks facing TAVR, valve durability issues are expected to be optimized and improved through dry valve technology and better addressed via polymer materials. The expansion of indications is primarily trending toward pure aortic regurgitation, which requires superior anchoring mechanisms (such as perivalvular positioning designs), while the transfemoral approach remains the mainstream direction for the future. (Due to space constraints, this chapter has been significantly abridged.)

4.1 High Growth + Large Market: Revisiting the TAVR Industry Size

Following the inclusion of TAVR in China’s national medical insurance coverage, TAVR implantation volumes are poised for another surge, with penetration rates approaching those of Europe and the United States, potentially exceeding 300,000 cases (given that the long-term technical difficulty of TAVR implantation will be no greater than that of PCI, there are no supply-side bottlenecks). We anticipate that national medical insurance coverage will likely be implemented when annual domestic valve implantations reach the range of 50,000–100,000 cases (in six years or more). Assuming a 70% price reduction under medical insurance, the long-term market size for TAVR in China could reach RMB 20 billion, indicating substantial growth potential. Prior to medical insurance coverage, we project that TAVR implantations in China will maintain rapid growth: a five-fold increase in three years and a ten-fold increase in six years (similar to the U.S. scenario in 2013; Germany has seen slower growth due to its already having reached the highest global penetration rate).

4.2 Duopoly + High Profitability: Revisiting the Competitive Landscape of TAVR

Due to the accumulation of clinical evidence, the formation of surgical habits, stickiness from corporate training, and economies of scale, the TAVR sector exhibits a Matthew effect where the strong grow stronger. We anticipate that the long-term landscape of China’s TAVR market will be characterized by an oligopoly. As the first three companies to go public, Venus Medtech, MicroPort CardioFlow, and Peijia Medical hold significant leading advantages in promoting their TAVR businesses.International experience offers valuable insights: Edwards Lifesciences and Medtronic simultaneously received CE certification in Europe in 2007. However, Edwards secured FDA approval in 2011, a full three years ahead of Medtronic’s 2014 approval. This head start enabled Edwards to rapidly capture market share and maintain its leadership position. A review of the competition between Edwards and Medtronic reveals that early market entry generates a pronounced Matthew effect. Beyond the stickiness of physicians’ usage habits, being first to market allows for the generation of more extensive clinical evidence. Such evidence enhances the clinical persuasiveness and application value of superior products, thereby driving higher implantation volumes and creating a business flywheel effect. Although Medtronic lagged slightly behind, it has made strenuous efforts to catch up with its two major brands, CoreValve and Evolute. Nevertheless, it has struggled to overturn Edwards’ leading advantage. The intense rivalry between these two giants has left other competitors far behind.

4.3 Recyclable + Fully Supported: Revisiting TAVR Technological Innovation

From the perspective of technological innovation, current efforts are primarily focused on achieving precise drug release, improving success rates, and reducing adverse reactions.

To address the challenge of precise deployment, balloon-expandable and mechanically expanded valves offer distinct advantages, while self-expanding valves provide a strong complement through their retrievability. Meanwhile, technologies such as 3D printing enable physicians to simulate valve positioning ex vivo, thereby making valve implantation more precise and reliable.

In the international market, the two dominant players in TAVR, Edwards and Medtronic, have adopted balloon-expandable and self-expanding technological approaches, respectively. Balloon-expandable valves account for approximately 60% of the global market, while self-expanding valves hold about 40%. Currently, only self-expanding products are commercially available in China, although there are more balloon-expandable products in the development pipeline. Both self-expanding and balloon-expandable valves have their respective advantages, and numerous studies have long discussed their pros, cons, and clinical outcomes. After comparing all-cause mortality, stroke, vascular complications, implantation success rate, postoperative regurgitation, permanent pacemaker implantation, other complications, and valve durability, overall, there is no significant difference between the two. Moreover, self-expanding and balloon-expandable valves each offer advantages for patients with different anatomical structures. VCBeat believes that each technology has a patient profile that is more suitable from an anatomical perspective; therefore, both technological pathways will coexist in the Chinese market for the long term.

Furthermore, it is worth noting that in recent years, entirely new types of expansion mechanisms (non-self-expanding/balloon-expandable) have emerged. Silara is a novel and unique prosthesis featuring a non-metallic valve frame and a flexible, low-profile delivery system, which allows for repositioning and repeated assessment of full hemodynamic performance prior to final implantation.

4.4 Extended Durability + Expanded Indications: Revisiting the Breakthrough of TAVR Bottlenecks

The two major bottlenecks that TAVR urgently needs to overcome are durability issues and the expansion of indications (primarily for pure aortic regurgitation).

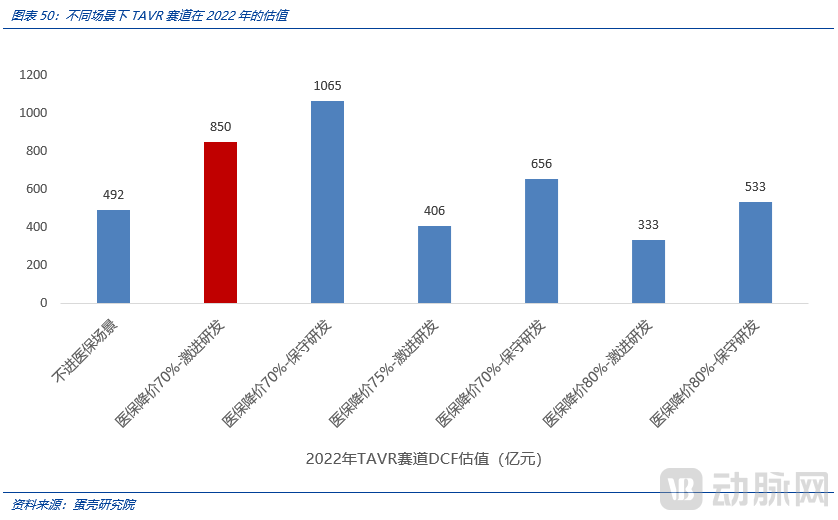

5Market Segment Valuation: The market segment was valued at RMB 85 billion in 2022.

Based on the DCF model, we valued the TAVR sector at RMB 85 billion in 2022.

5.1 Valuation Methods and Tools: Dual Verification Using DCF and P/E

We employed the DCF model to value the TAVR sector, supplemented by P/E ratio valuation for cross-verification.

The Discounted Cash Flow (DCF) model is the fair standard for asset pricing and represents the gold standard aligned with asset pricing logic. However, in practice, applying DCF to corporate valuation presents significant challenges. This is primarily because a company’s cash flows depend not only on the growth rate of its industry—often complicated by the fact that a single enterprise may operate multiple business lines across diverse sectors—but also on the competitive landscape within those industries and changes in market share. Furthermore, regarding the denominator in the DCF model, the risks and uncertainties faced by an individual company during its operations are greater than those affecting the industry as a whole. An industry merely needs to confirm the existence and sustained growth of demand; if one company declines due to internal factors, competitors can quickly fill the gap, generally without significantly impacting the overall development of the industry. Therefore, the industry as a whole exhibits greater stability compared to any specific enterprise. We believe that sector-based valuation offers greater robustness and accuracy than the DCF model applied to individual companies.

However, due to the complexity of its calculation process and lack of intuitiveness, the Discounted Cash Flow (DCF) model makes rapid cross-sectional comparisons difficult and hinders investors’ intuitive judgment. Therefore, we also employ the Price-to-Earnings (P/E) valuation method as a supplementary validation for DCF. If DCF represents the “ultimate truth” of valuation theory, P/E is more akin to its “conventional truth”—a “pragmatic approach” that offers greater intuitiveness and comparability. Meanwhile, we apply the P/E valuation method to verify the reasonableness of the DCF valuation results for the TAVR sector.

5.2 Valuation Premises and Assumptions: Cash Flow and Discount Rate Analysis

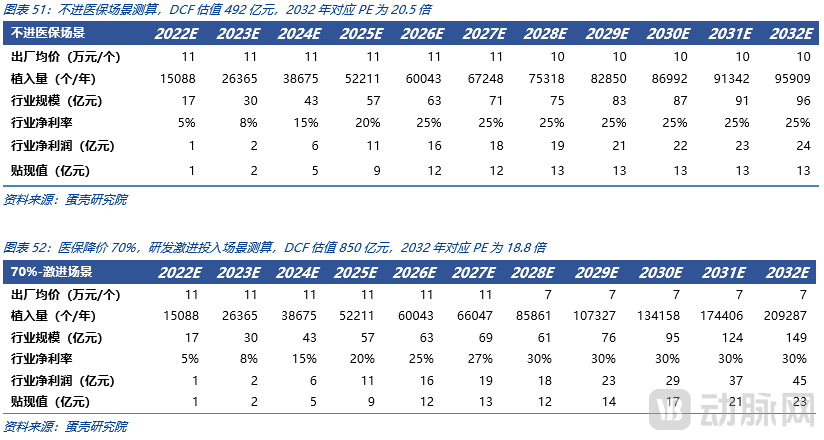

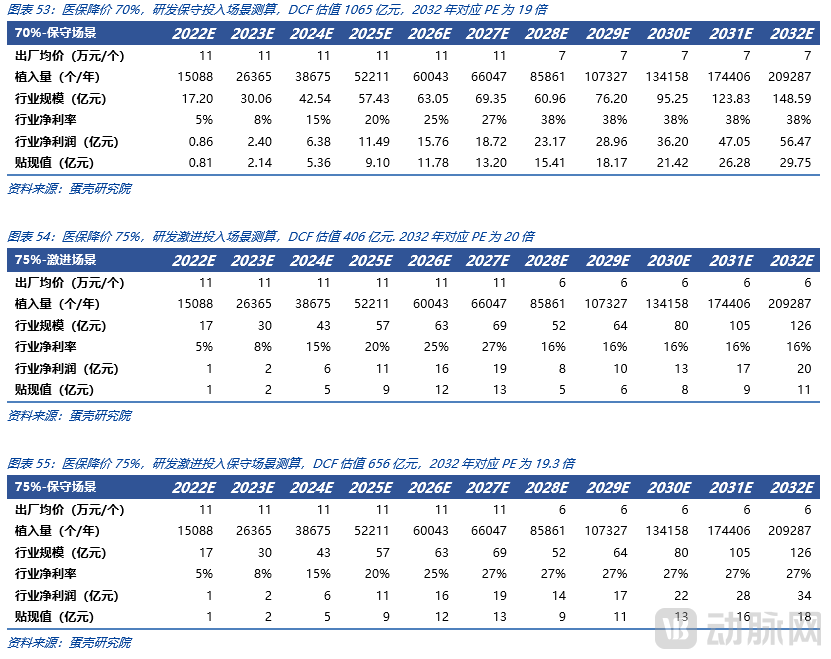

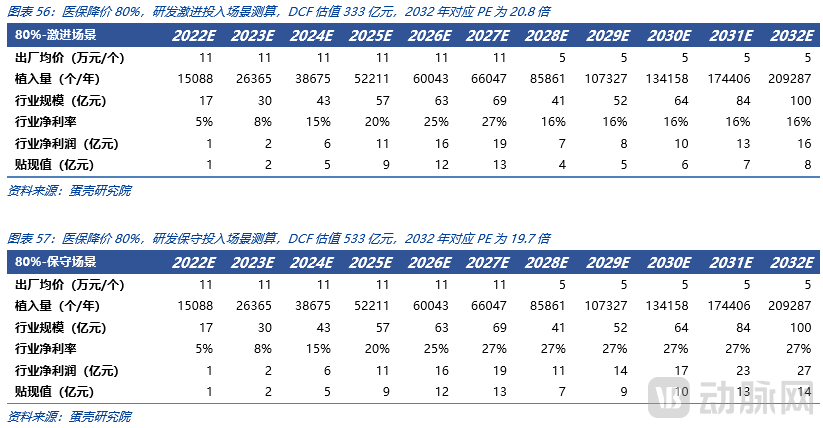

Key assumptions for forecasting cash flows in the DCF valuation of the TAVR sector include implantation volume and its growth, average selling price (ASP) and its trends, timing and intensity of national volume-based procurement (VBP) under medical insurance, R&D investment intensity, and net profit margin. We assume that VBP will be implemented in 2028 (base-case estimate) and conduct scenario analysis based on terminal price reductions of 70%, 75%, and 80%. Furthermore, we perform detailed analyses for both conservative and aggressive R&D investment scenarios under the 75% and 80% price reduction cases, assuming R&D expense ratios of 5% for conservative investment and 20% for aggressive investment. Following inclusion in VBP, we assume a 30% year-over-year increase in implantation volume.

Key assumptions for forecasting the discount rate in the DCF valuation of the TAVR sector are as follows: For the DCF discount rate, individual assets or companies in the pharmaceutical and medical device sectors typically adopt a discount rate of approximately 10% (although WACC calculation is possible, a direct figure is usually applied). Considering that the risks faced by the industry as a whole are significantly lower than those faced by individual companies, and given that (1) mature products have already achieved large-scale commercial sales, eliminating uncertainty regarding business model validation; and (2) Edwards Lifesciences has achieved remarkable success in the global market (validating the long-term stable growth of the TAVR sector), thereby removing uncertainty regarding growth, we apply a 6% discount rate to the denominator of the DCF model.

5.3 Valuation Results and Scenarios: Analysis of Value and Value Drivers

We tend to believe that a 70% price reduction under medical insurance coverage, coupled with aggressive R&D investment, better aligns with future real-world scenarios. Under this scenario, the DCF-based valuation of the TAVR sector in 2022 amounts to RMB 85 billion. This corresponds to a P/E (price-to-earnings) ratio of 18.9x at the initial stage of stable growth (2032).

The key factors influencing industry valuation are as follows:

One of the Key Drivers: Promotion Speed (Primarily Affects Short-Term Industry Scale Growth)

Key Driver #2: Out-of-Pocket Spending Capacity (Primarily Affects Mid-Term Industry Scale)

Key Driver #3: Timing and Magnitude of Volume-Based Procurement under Medical Insurance (Primarily Affecting Long-Term Industry Scale and Net Profit Margin)

Key Driver 4: Industry Competitive Landscape (Primarily Affecting Net Profit Margin)

Key Driver #5: Industry-wide R&D Investment (Primarily Affects Net Profit Margin)

We calculated the industry's discounted cash flow (DCF) valuations under scenarios with no national reimbursement, and 70%, 75%, and 80% price reductions due to national reimbursement, each combined with aggressive or conservative R&D investment strategies. The highest valuation of RMB 106.5 billion was achieved under the scenario of a 70% price reduction with conservative R&D investment, while the lowest valuation of RMB 33.3 billion occurred under the scenario of an 80% price reduction with aggressive R&D investment.

6Related Companies

Due to space limitations, the full text of this report is not displayed here. To read the complete article, please scan the mini-program QR code below.