With China's First Domestic Certificate, Bmdevice Takes on J&J and Medtronic as Dual-Business Medical Firm Eyes Beijing Stock Exchange

Bmdevice

R&D and Manufacturing of Medical Devices and Peptide Pharmaceutical Equipment

When medical consumables companies choose to deepen their focus on pharmaceutical equipment: a risk hedging experiment planned more than a decade in advance.

On June 12, Hainan Biomedical Device Co., Ltd. will undergo review at the Beijing Stock Exchange.

Its signature achievement is an absorbable knotless suture, the first domestically produced product of its kind to receive registration certification, breaking the monopoly held by three foreign giants: Johnson & Johnson, Corza Medical, and Medtronic.

Prospectus data shows:

In 2025, Bmdevice reported revenue of RMB 214 million and net profit of RMB 70.8087 million, with a gross margin exceeding 75%;

Annual product sales exceeded 2.01 million units, covering nearly 3,000 hospitals across China and reaching over 50% of the top 100 hospitals nationwide by surgical volume;

Ranked by sales revenue, it holds an 8.9% market share in China's knotless suture market, ranking fourth in the industry and first among domestic brands, currently enjoying the peak benefits of domestic substitution.

Corporate Revenue Performance, Source: Prospectus

If the story ended here, this would just be an unremarkable tale of domestic substitution.

However, according to the information disclosed in the prospectus, this company, which is primarily identified by its surgical sutures, had already established its subsidiary, Hainan Jianbang Pharmaceutical Science Co., Ltd., in February 2006. This subsidiary focuses on the research and development and production of peptide pharmaceutical equipment, such as peptide synthesizers and peptide cleavage instruments, and holds approximately a 10% market share in China's market for peptide synthesizers and cleavage instruments.

This indicates that within Bmdevice's core business scope, the two major segments of medical consumables and pharmaceutical equipment have been developing in parallel for 19 years.

Bmdevice's decision was not a passive foray into new sectors driven by operational difficulties, but rather a strategic approach encompassing risk hedging and long-term development.

In 2007, Yang Dingjian, who held a Ph.D. in Biochemistry and Molecular Biology from Lanzhou University, launched his entrepreneurial venture in Hainan. At that time, the domestic market for absorbable knotless sutures was entirely dominated by foreign brands. After eight years of intensive technological research and development, the product achieved a qualitative leap in performance, quality, and functionality in 2015, becoming comparable to similar products from abroad.

In 2019, the product obtained a Class III medical device registration certificate from the National Medical Products Administration (NMPA), becoming the first registered absorbable knotless suture produced in China and filling a gap in the domestic market.

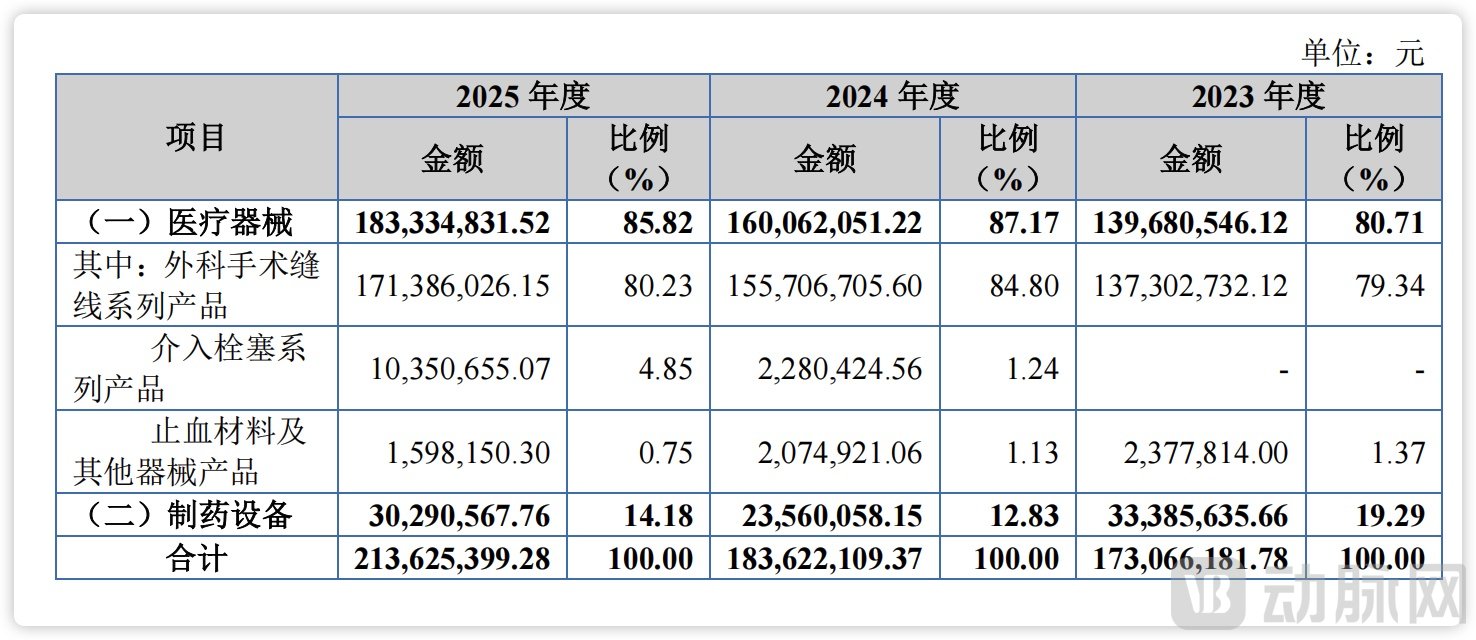

According to the data disclosed in the prospectus, in 2025, absorbable surgical sutures generated revenue of RMB 165.7466 million, with annual sales volume reaching 2.0137 million units, representing a year-on-year increase of 21.11%.

In the domestic knotless suture market, the overall market share reached 8.9%, ranking fourth in the entire industry and firmly holding the top position among all Chinese brands.

The explosive growth in market demand has directly led to tight production capacity, with the current capacity utilization rate surging to 114.66%, and production lines operating under long-term overload conditions.

Behind the impressive performance lies proof that its products are entering a dividend period. Based on industry experience, when a company is at this stage, it must either choose to continue increasing investment or actively lay out plans to prepare for the second growth curve in the future.

Bmdevice's dual-core business strategy was already in place as early as 2006, at a time when absorbable knotless sutures were still in the early stages of R&D, more than a decade away from regulatory approval and market launch. This move was not a forced transformation driven by operational difficulties, but rather a proactive response to recognized systemic industry risks, made just as the core business was on the verge of breakthrough success. This underlying philosophy of preparing for potential crises even in times of stability has permeated Bmdevice's development journey over the years.

Examining Bmdevice's development trajectory, a clear timeline reveals the forward-looking nature of its strategic decisions.

In February 2006, Yang Dingjian established Hainan Jianbang Pharmaceutical Science Co., Ltd. focusing on the research and development and production of peptide pharmaceutical equipment. In June 2007, he founded Jianke Limited (the predecessor of Bmdevice) to explore the field of clinical medical devices. In 2009, Hainan Jianbang successfully developed China's first fully automated large-scale peptide synthesizer with independent intellectual property rights, achieving a critical transition in peptide drug production from laboratory research to large-scale industrial manufacturing.

Bmdevice's second growth track took off even earlier than the boom in its core consumables business. When Hainan Jianbang was established in 2006, key instruments and equipment required for peptide drug synthesis in China relied mainly on imports, were expensive, and had few domestic manufacturers. Leveraging his professional background in biomedicine and experience in the peptide drug industry, Yang Dingjian identified this market gap. By the time Jianke Limited was founded in 2007 and began expanding into the clinical medical device sector, its peptide pharmaceutical equipment business had already accumulated a certain level of technical expertise.

This strategic approach of prioritizing equipment before consumables is extremely rare among domestic medical consumable companies.

Bmdevice's peptide pharmaceutical equipment business, cultivated over many years, has become an independent cornerstone of its performance. The prospectus reveals that the company's major clients for peptide pharmaceutical equipment include leading domestic pharmaceutical companies such as Sinopep, WuXi AppTec, Hengrui Medicine, and Qilu Pharmaceutical. In the domestic niche market for peptide synthesis equipment, Bmdevice also holds a significant market share.

In 2023, the pharmaceutical equipment segment achieved an operating revenue of RMB 38.1728 million. Although this accounted for only 19.29% of the company's total revenue, its share dropped to 12.83% in 2024 due to the base effect resulting from the volume surge in the medical device segment driven by centralized procurement. This precisely underscores the complementarity between the two business segments.

From a policy perspective, peptide pharmaceutical equipment falls under the category of pharmaceutical industrial equipment. Its regulatory rules, pricing systems, and procurement models are entirely independent from those of medical consumables, remaining unaffected by centralized volume-based procurement (VBP) policies for consumables and thus completely avoiding the impact of price reductions associated with such initiatives. From a customer structure perspective, downstream clients for this equipment primarily consist of leading domestic pharmaceutical companies such as Hengrui Medicine, WuXi AppTec, and Sinopep. These customers exhibit rigorous procurement decision-making processes, long-term cooperation cycles, and strong customer stickiness, unlike hospital end-users who are frequently impacted by VBP policies.

From the perspective of the operating cycle, pharmaceutical equipment is classified as corporate fixed assets, characterized by high single-purchase amounts and stable payment collection rhythms. Consequently, its performance volatility is significantly lower than that of the consumables business, which is subject to the dual influences of end-user demand and medical insurance policies. Therefore, even if the consumables business faces revenue pressure, the pharmaceutical equipment segment can stabilize the company's core operations, thereby enhancing the overall resilience against risks.

More critically, these two business lines are not mere examples of unrelated diversification, but rather extensions based on the company's own technological capabilities. This fundamentally distinguishes them from cases of blind cross-industry expansion that ultimately failed due to technological fragmentation.

Bmdevice's adoption of a dual-core business model focusing on medical devices and peptide pharmaceutical equipment is not a capital-driven trend-following expansion. Both surgical suture production and pharmaceutical equipment manufacturing belong to technology-intensive industries characterized by the intersection of multidisciplinary knowledge, featuring complex manufacturing processes and stringent production quality control requirements. Their core competencies are built upon foundational technologies such as precision machining, automated control systems, aseptic processing techniques, and biomaterial compatibility technologies.

Taking the thread-cutting machine, a core production equipment for surgical suture products, as an example, it leverages the extensive R&D and manufacturing experience of its subsidiary, Hainan Jianbang, in the field of pharmaceutical equipment. Through continuous research and development, the company has mastered automation technology for thread-cutting machines, achieving full automation in the entire surgical suture production process. This has significantly improved production efficiency and enhanced the consistency of product quality.

This technology-driven natural extension distinguishes Bmdevice's dual-core business model from the traditional concept of a second growth curve. Rather than building a new technical team and accumulating patents from scratch, the company leveraged its foresight in making early strategic moves, completing over a decade of technological cultivation, accumulation, and validation. This process has established its competitive moat.

More than a decade of dual-core business drive has ultimately pointed to a clear goal: continuously optimizing the revenue structure.

Currently, the revenue structure dominated by absorbable surgical sutures has not undergone any fundamental change. The prospectus indicates that over the past three years, sales revenue from absorbable surgical sutures has accounted for approximately 80% of the company's total operating revenue.

Over the next few years, optimizing its revenue structure from being driven by a single business line to a more balanced model is the core objective of Bmdevice's initial public offering (IPO) fundraising.

In this IPO, Bmdevice plans to raise RMB 306 million, with all proceeds allocated to the Hainan Bmdevice Advanced Medical Devices Project. The capacity planning for this fundraising investment project clearly outlines the company's three-pronged strategy for tiered optimization.

In the short term, expanding production capacity for existing core consumables is a key measure to consolidate the fundamental business. Upon completion of the project, an additional annual production capacity of 3.25 million units of absorbable knotless sutures will be added. Given the current ultra-high capacity utilization rate of 114.66%, the new capacity will effectively alleviate production bottlenecks. Leveraging the mature sales network established through centralized procurement programs in multiple provinces across China, sales volume of core products is expected to further increase, thereby continuously consolidating market share and providing sufficient cash flow support for subsequent new product development and technological upgrades in the second growth track.

In the medium term, the commercial scale-up of new consumable products will enrich the product portfolio, fundamentally addressing the challenge of reliance on a single product. Currently, gelatin sponge embolic microspheres have successfully received market approval and officially entered the commercial promotion phase, beginning to gradually contribute to revenue. Another core product under development, absorbable medical adhesive for sealing, is steadily advancing through clinical trials and is approaching market launch. As these two new products are successively launched, the company's consumables business will shift from dominance by a single product to synergistic development across multiple categories, effectively mitigating risks associated with dependence on a single product.

The long-term goal is to scale the peptide pharmaceutical equipment business into a second growth curve. The prospectus discloses that the company's R&D portfolio includes high-throughput peptide synthesizers, peptide post-processing equipment, supporting consumables, and technical services, covering the entire equipment industry chain. Of greater strategic significance is the oligonucleotide synthesizer project under development, which targets the cutting-edge field of nucleic acid therapeutics. With the explosive growth of GLP-1 peptide drugs and the rapid rise of nucleic acid-based medicines, market demand for peptide and oligonucleotide synthesis equipment will continue to expand.

Bmdevice aims to consolidate its market share in peptide equipment while expanding into new fields to continuously increase revenue from its equipment business.

These three pathways are not pursued in isolation; rather, they mutually reinforce and synergize with one another. Furthermore, new products included in the fundraising investment projects, such as antibacterial fishbone sutures and antibacterial barbed sutures, leverage the company's core competencies, including precision machining technology transferred from its pharmaceutical equipment sector. Meanwhile, the expansion of the equipment segment into the field of oligonucleotide synthesis benefits from the medical device segment's technical expertise in biomaterial compatibility.

Dual-engine drive is not a simple addition of two businesses, but rather the deep integration of one's own full value chain encompassing technology, R&D, and production.

From the establishment of Hainan Jianbang in 2006 to the listing review in 2026, over a span of 19 years, Bmdevice has executed a rare reverse strategic layout: at the peak of consumables dividends, it built a second line of defense with pharmaceutical equipment; as centralized procurement pressures gradually emerged, it aimed to unlock new growth opportunities.