The Dawn of China's Domestic Surgical Robotics Era: Market Outlook and Product Landscape of Laparoscopic Surgical Robots

Author: Research Team of Haitong International Research Co., Ltd.Shu Yinglan,Hahn Zhang、Zhuang Jiexian JasonPublished with authorization from VCBeat; content has been abridged from the original report.

In 2021, which we consider the inaugural year for laparoscopic surgical robots in China, MicroPort MedBot went public as the first listed company specializing in laparoscopic surgical robots, with its products having submitted for registration. Shanghai included four types of laparoscopic robotic surgeries in its medical insurance coverage. Weigao Surgical Robot became the first domestic manufacturer to obtain regulatory approval, while Jingfeng, Kangduo, and Shurui surgical robots are undergoing clinical trials. Thus, China has entered a new era of domestically produced surgical robots. As one of the most technologically advanced medical devices, the localization of laparoscopic surgical robots marks a new phase in indigenous medical device innovation. Therefore, at this juncture, we are releasing an industry report to present our outlook on the future of China’s laparoscopic surgical robot industry.

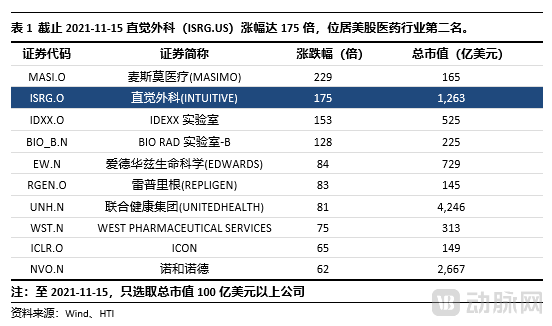

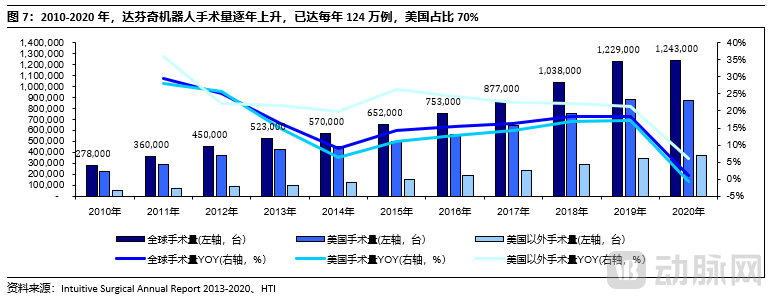

Since 2000, the stock price of Intuitive Surgical, the maker of the da Vinci Surgical System, has surged by 175-fold.Since its IPO in 2000, Intuitive Surgical (ISRG) has seen its stock price surge by 175-fold, ranking second among U.S. pharmaceutical and healthcare stocks. Its market capitalization reached $126.3 billion on November 16, 2021. The da Vinci Surgical System is Intuitive Surgical’s flagship product, with 5,989 units installed globally, performing 1.24 million procedures annually, generating $4.3 billion in annual revenue and $1 billion in net profit. Within the surgical robotics sector, laparoscopic surgical robots offer particularly compelling investment value, as blockbuster products often give rise to large-cap companies. We believe that China’s laparoscopic robotics industry will produce high-quality investment opportunities.

The market potential for domestically produced surgical robots in China is as high as RMB 48.7 billion, pioneering a business model tailored to China’s national conditions.The Da Vinci Surgical System sells for approximately $3.5 million per unit in China, with an average cost of RMB 30,000–50,000 per procedure. These high costs deter many patients. In the United States, robotic surgery fees are reimbursable alongside standard laparoscopic instruments, thanks to generous insurance coverage. In Japan, however, the development of robotic surgery lags significantly behind the U.S. due to limited insurance reimbursement capacity, high prices for imported products, and a lack of competition from domestic manufacturers. The “China model” focuses on achieving higher market penetration through localized production and competitive pricing—trading lower unit prices for greater volume. We anticipate that, under ideal conditions, laparoscopic robots will penetrate Tier-2 hospitals, meaning any hospital performing minimally invasive surgeries could potentially be equipped with such systems.

We forecast the market size of laparoscopic surgical robots based on a revenue structure comprising equipment, consumables, and service fees. Under an optimistic scenario, we project that in 5–10 years, the selling price of domestically produced robots will reach RMB 6 million, with average consumable costs per procedure at RMB 10,000. At this price level, we assume that Grade A tertiary hospitals will have an average of 2.5 laparoscopic robots each, other tertiary hospitals 1.5 units each, and secondary Grade A hospitals 0.8 units each. Based on the number of hospitals in China in 2020, the Chinese market can accommodate 9,531 robots. With a seven-year depreciation period, the steady-state annual addition of new equipment will be 1,362 units, resulting in an equipment market size of RMB 8.2 billion. In terms of surgical volume, assuming a 50% penetration rate for target procedures, China will perform 3.955 million laparoscopic robotic surgeries annually, equivalent to 415 procedures per robot per year, yielding a consumables market size of RMB 39.6 billion. We estimate annual service fees per robot at approximately RMB 100,000, leading to a service fee market size of around RMB 1 billion. Combined, the total market size for domestically produced surgical robots in China reaches RMB 48.7 billion.

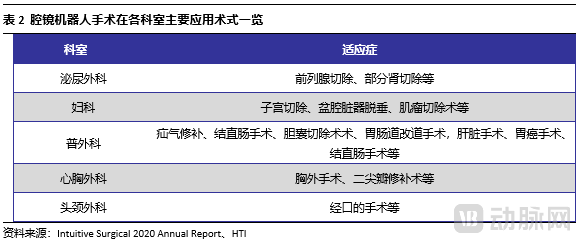

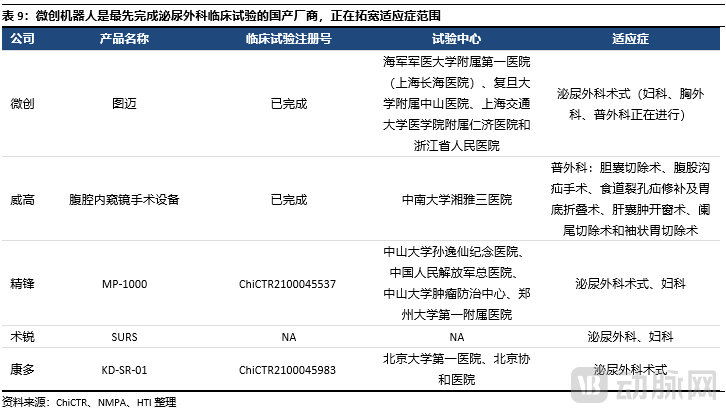

Urological surgery is a classic application for endoscopic robotic systems, and minimally invasive surgical robots were the first to complete clinical trials in urology.We consider urological procedures such as radical prostatectomy and partial nephrectomy to be classic indications for surgical robots. Entering clinical practice through these procedures facilitates acceptance by hospitals and physicians. Various Chinese-made surgical robots have conducted clinical trials for different indications. MicroPort MedBot has taken the lead in completing urological clinical trials and has begun patient enrollment in gynecology, thoracic surgery, and general surgery. Edge Medical has completed patient enrollment in urology and entered clinical trials in gynecology. Shurui and Kangduo have initiated urological clinical trials, while Weigao’s surgical robot has been approved for certain general surgical procedures.

Laparoscopic surgical robots are not merely a product, but rather a standardized platform, with AI, VR, 5G, and other technologies unlocking the platform’s value.The Da Vinci Surgical Robot System was originally invented to address the challenge of performing remote surgeries on soldiers injured at the front lines, with advanced communication technologies such as 5G making telesurgery feasible. Surgical robots represent a step toward standardizing complex surgical procedures, thereby reducing the technical demands placed on surgeons. The integration of surgical robots with AI, VR, and other technologies will further lower the skill threshold for physicians, making high-difficulty surgeries more accessible. It is conceivable that in the future, AI-driven autonomous surgeries or the performance of highly complex procedures by junior surgeons may become reality, leading to higher penetration rates and greater growth potential for surgical robots. Although the current requirement for regulatory certification will limit the pace of market expansion, endoscopic surgical robots, as a standardized platform, offer broad application prospects and high platform value.

120 Years, 175-Fold Growth: Laparoscopic Surgical Robots Create a U.S. Healthcare Stock Legend

Since its IPO in 2000, Intuitive Surgical has surged 175-fold, ranking second in the U.S. healthcare sector.Intuitive Surgical’s flagship product is the da Vinci surgical system, a laparoscopic surgical robot. The system received FDA approval for performing surgeries independently in 2000 and has since been updated to its fourth generation. With 5,989 units installed globally, it facilitates 1.24 million procedures annually, generating $4.3 billion in annual revenue and $1 billion in net profit. Blockbuster products often give rise to companies with substantial market capitalizations; we believe that China’s laparoscopic surgical robot industry will produce high-quality investment opportunities.

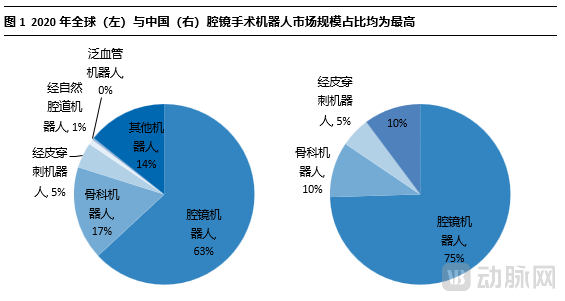

Laparoscopic surgical robots hold the greatest market potential among all surgical robot categories. According to Frost & Sullivan statistics cited in MicroPort MedBot’s prospectus, the global surgical robot market was valued at approximately $8.3 billion in 2020, with laparoscopic surgical robots accounting for $5.25 billion, or 63% of the total. Orthopedic surgical robots ranked second, with a market size of approximately $1.39 billion, representing 17%. In China, the national surgical robot market reached approximately $425 million in 2020, with laparoscopic surgical robots comprising 75% of this figure.

2Endoscopic Robots Can Be Viewed as a Comprehensive Upgrade to Minimally Invasive Surgery

Robot-assisted surgery (RAS) can be regarded as a comprehensive upgrade of minimally invasive surgery and represents the third generation of surgical techniques.From first-generation open surgery and second-generation minimally invasive surgery to third-generation robotic-assisted surgery (RAS), the evolution of surgical techniques has continuously emphasized patient outcomes, striving for advantages such as minimal invasiveness, precision, fewer complications, and faster recovery. While second-generation minimally invasive surgery significantly reduced incision size and improved prognosis, it is less capable of handling complex procedures, particularly those requiring delicate dissection in confined spaces, such as urological and pelvic floor surgeries.

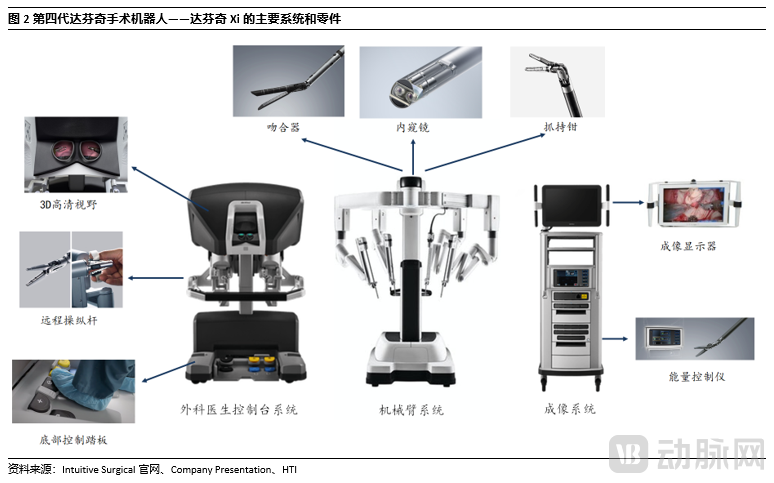

The da Vinci Surgical System primarily consists of three components: the surgeon console, the imaging system, and the patient-side manipulator arms.Taking the latest Da Vinci Xi system as an example, the robot is mainly divided into three parts:

(1) Console:It consists of two master controllers and a foot pedal. The console and computing system translate the surgeon’s movements into robotic arm motions. Key technical parameters include force feedback from the master controllers, motion latency between the robotic arms and the controllers, and safety mechanisms to prevent inadvertent operations.

(2) Imaging System:The system includes a 3D endoscope, camera, processor, display system, and other components. The 3D endoscope is mounted on the scope-holding arm of the robotic manipulator, while the display screen is located at the surgeon’s console. Key technical features include image clarity, positioning systems, and intraoperative fluorescence imaging. The surgical team can also monitor the procedure in real time through the imaging system, thereby enhancing safety.

(3) Robotic Arm:Arguably the most critical component of a surgical robot, it consists of four robotic arms mounted on a mobile base, typically comprising a camera-holding arm, left and right instrument arms, and an energy device arm. By equipping different surgical instruments—such as graspers (Endowrist series), staplers (SureForm series), and energy platforms—it can perform nearly all laparoscopic surgical procedures. Single-port robotic systems utilize a single highly integrated robotic arm with four embedded manipulators, corresponding to the four-arm design of multi-port robotic systems.

Laparoscopic surgical robots are high-tech products that integrate medicine, mechanics, biomechanics, and computer science. They address the challenge of anatomical precision in minimally invasive surgery and enable the performance of complex procedures that are difficult to accomplish with conventional laparoscopy.Robotic laparoscopic surgery utilizes a master-slave teleoperation system to scale down the surgeon’s gross hand movements into precise, minute motions at the robotic arm’s end-effector, while simultaneously eliminating physiological tremor. Coupled with a 3D laparoscopic view offering more than 10x magnification, this technology enables highly delicate surgical dissection.

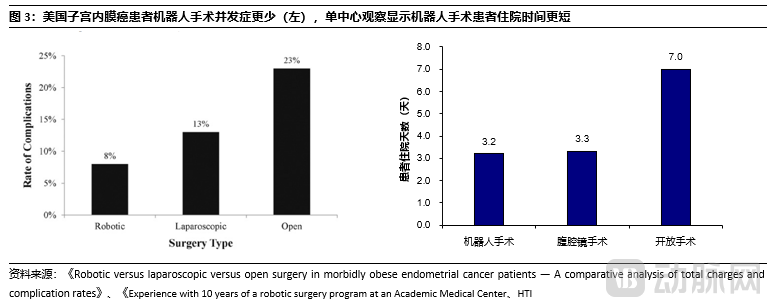

In the United States, the penetration rate of robot-assisted radical prostatectomy has exceeded 70%, making radical prostatectomy a classic procedure for robotic surgery.Prior to the advent of robotic laparoscopic surgery, radical prostatectomy performed via conventional laparoscopy required 4–5 hours of operative time, resulted in approximately 400 mL of blood loss, and necessitated a hospital stay of around seven days. It has been reported that even for the most experienced surgeons, laparoscopic radical prostatectomy remains highly challenging; the limited visual field and constraints of minimally invasive instruments make precise dissection of the neurovascular bundles difficult, leading to frequent postoperative complications such as urinary incontinence and sexual dysfunction. Following the introduction of the da Vinci Surgical System, robotic-assisted laparoscopic surgery has been widely adopted in urological procedures, including radical prostatectomy. A single-center study evaluating 2,766 cases of robot-assisted radical prostatectomy (RARP) demonstrated an average operative time of only 154 minutes, with approximately 96% of patients discharged within 24 hours postoperatively and a significant reduction in complication rates.

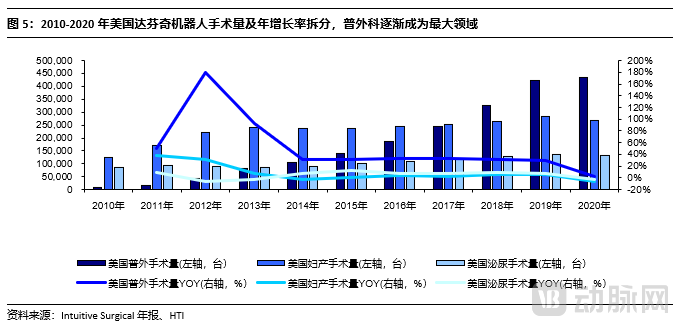

Reviewing the commercialization journey of the da Vinci Surgical System in the United States, we believe that the development trend of laparoscopic robotic surgery has progressed from urology to gynecology and then to general surgery.Prior to 2008, urological surgery was the leading indication for da Vinci surgical procedures. In 2009, gynecology became the largest specialty, primarily driven by hysterectomies. By 2018, general surgery emerged as the dominant field, mainly comprising cholecystectomies and bariatric surgeries. The overall development trend of robotic laparoscopic surgery demonstrates a pattern originating from oncologic procedures and gradually expanding to benign conditions.

We believe that urologic oncology surgeries are characterized by urgency and high willingness to pay. The clinical superiority of laparoscopic robotic surgery in the field of urologic cancer procedures will serve as the initial step for laparoscopic robots to penetrate the market.For complex procedures such as radical prostatectomy, laparoscopic robotic surgery represents a significant leap in surgical quality and efficiency. Due to the absolute advantages of laparoscopic robotic surgery in these areas, hospitals are motivated to invest millions of dollars in equipment, and surgeons are incentivized to learn laparoscopic robotic surgery from scratch. As laparoscopic robotic surgery becomes more widespread, the number of hospitals equipped with robotic systems has increased, and the number of surgeons proficient in these techniques has grown accordingly. Consequently, the marginal cost of expanding indications for laparoscopic robotic surgery has decreased significantly, leading to its extensive application in gynecological surgeries. Most robotic gynecological procedures are performed near the pelvic floor, retaining the primary advantages of robotic surgery; however, approximately 80% of these procedures are benign hysterectomies. With further adoption of laparoscopic robotic surgery, indications in general surgery have gradually emerged, with representative procedures including hernia repair and bariatric surgery (gastric bypass). Many major general surgery procedures are benign, and the clinical advantages of using robots compared to traditional minimally invasive surgery are not as pronounced as they are in urology and gynecology. Thus, as laparoscopic robotic surgery becomes more prevalent, the marginal cost of broadening its indications continues to decline, shifting the rationale for acceptance among doctors, hospitals, and patients from “Why” to “Why not.” The most critical step in this evolution has been the volume surge during the urology phase.

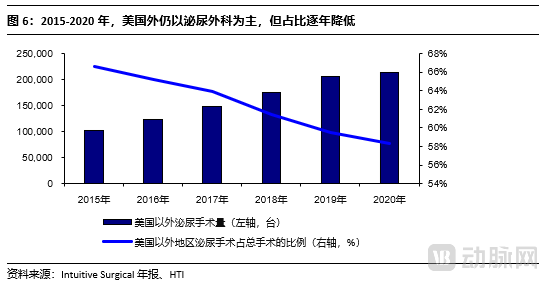

In markets outside the United States, robotic laparoscopic surgery remains in its introductory phase, primarily concentrated in urology.In 2020, the global volume of da Vinci robotic surgeries reached 1.24 million cases, with the United States accounting for approximately 70%. In China, the volume of laparoscopic robotic surgeries was only 47,000 cases in 2020, representing about 3.7% of the global total, indicating that the market is still in its early stages. Outside the United States, urological procedures accounted for more than 50% of all robotic surgeries, meaning that the majority of these procedures were concentrated in the field of urology.

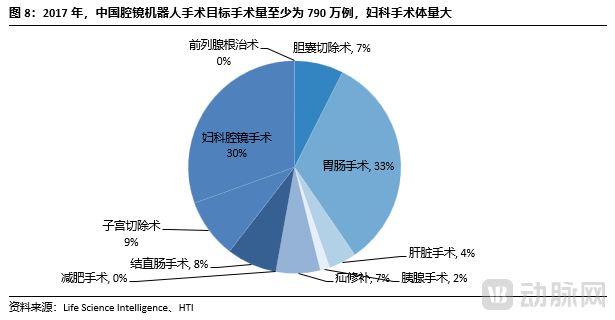

The target volume for robotic laparoscopic surgeries in China is at least 7.9 million cases. According to a report by Life Science Intelligence, there were a total of 60.69 million surgical procedures of various types performed in China in 2017. Among these, the procedures with near-term potential for robotic laparoscopic surgery include, but are not limited to: prostatectomy, gynecological laparoscopic surgery, open hysterectomy, colorectal surgery, bariatric surgery, hernia repair, and cholecystectomy. The combined volume of these procedures totals 7.9 million cases.

3The Market for Domestically Produced Surgical Robots Reaches RMB 48.7 Billion, Pioneering a Business Model Aligned with National Conditions

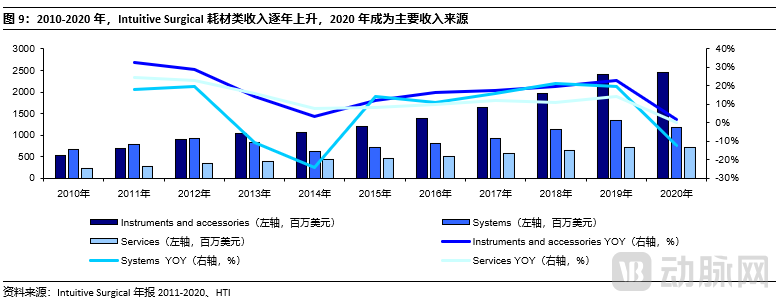

The surgical robot market is mainly divided into three parts: equipment, service fees, and consumables.During the product introduction phase, equipment revenue accounts for the majority of the market; as robotic surgery becomes more widespread and the volume of procedures per unit increases, consumables revenue becomes the primary driver of profitability, while service fees, which are tied to the number of installed devices and charged as a fixed annual amount, represent a relatively stable component. In 2020, consumables revenue accounted for 56% of Intuitive Surgical’s total revenue, equipment revenue for 27%, and service fees for 17%.

3.1 High Reimbursement Levels in the U.S. Healthcare System Provide a Payment Foundation for the Da Vinci System’s High Price

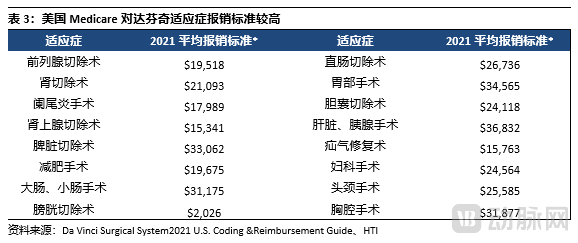

U.S. Medicare’s reimbursement standards for laparoscopic surgery are significantly higher than those in China and Japan, allowing it to cover the costs of robotic surgery without any adjustments.According to data compiled by Intuitive Surgical, the average Medicare reimbursement for laparoscopic surgery in the United States reached approximately $20,000–$30,000 in 2021. This high level of reimbursement has created significant growth opportunities for robotic surgery. In the U.S., the cost of traditional laparoscopic surgery is comparable to that of da Vinci robotic surgery; therefore, Medicare does not require separate insurance coverage policies for robotic procedures, substantially reducing the administrative burden on hospitals and physicians when adopting robotic surgery as an alternative to traditional laparoscopy.

The structure of U.S. commercial insurance favors coverage for high-value medical consumables and equipment.Unlike the strong bargaining power of China’s single-payer healthcare system, a significant portion of healthcare costs in the United States is covered by commercial insurance. Commercial insurers face competitive pressures among themselves. Robotic surgery, as the latest surgical trend favored by patients, has become a tool for commercial insurers to attract customers. Many commercial insurance plans under Medicare Part D and Medicare Advantage promote coverage of robotic surgery systems as a key selling point.

3.2 Japan’s lower affordability compared to the United States led to slow adoption of robotic surgery, which accelerated significantly after its inclusion in national health insurance coverage

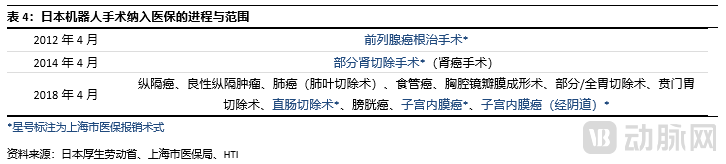

Based on Japan’s experience, the adoption of robotic surgery grew slowly before it was covered by national health insurance, but accelerated significantly after coverage was introduced.Japan only included radical prostatectomy in its public health insurance coverage in 2012, added partial nephrectomy in 2014, and further expanded coverage to include 12 additional surgical procedures—such as those for gastric cancer and lung cancer—in April 2018. Following inclusion in the national health insurance scheme, the cost of robotic surgery in Japan is approximately ¥2 million (RMB 113,000), with 70% covered by insurance, leaving patients to pay around RMB 30,000 out-of-pocket. Low-income individuals can benefit from Japan’s unique “High-Cost Medical Care Benefit” system, which provides additional reimbursement based on income levels, reducing their out-of-pocket expenses to as low as ¥100,000 (RMB 5,600).

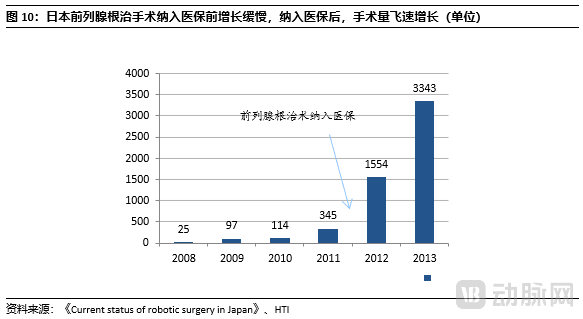

Since the inclusion of radical prostatectomy in Japan’s national health insurance coverage in 2012, the volume of robot-assisted procedures has accelerated rapidly. The annual growth rates for surgical volumes in 2012 and 2013 reached 350% and 115%, respectively.

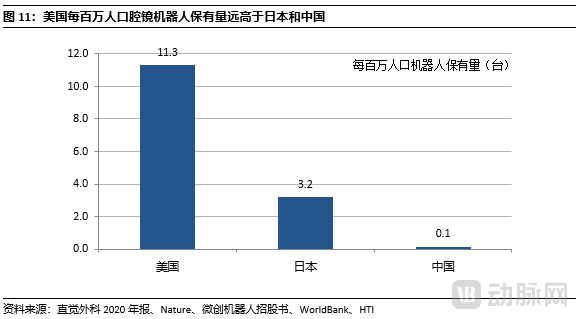

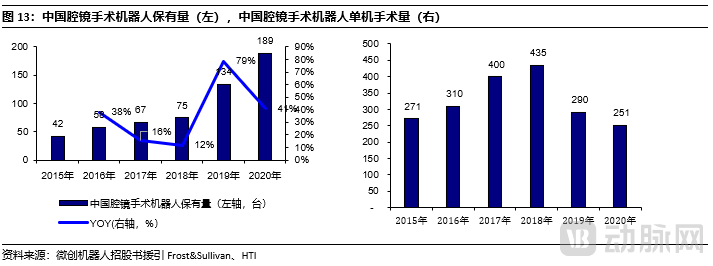

According to Intuitive Surgical’s 2020 annual report, there were approximately 3,720 da Vinci surgical robots in the United States. Nature Communications reported that Japan currently has around 400 surgical robots. Data from MicroPort MedBot’s prospectus indicates that China had 189 surgical robots installed. Based on the 2020 population figures for these three countries, the United States had 11.3 laparoscopic robots per million people, Japan had 3.2 per million, while China had only 0.1 per million.

3.3 Price Reduction and Increased Penetration Rate: The Business Model Most Aligned with China’s National Conditions

In China, laparoscopic robots have the potential to penetrate all medical institutions that perform minimally invasive laparoscopic surgery.As a third-generation surgical technology, robotic laparoscopic surgery can replace a significant proportion of open surgeries and minimally invasive laparoscopic procedures.

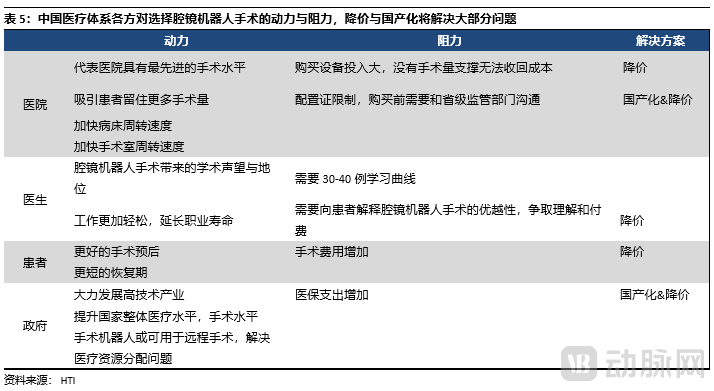

We believe that, excluding price considerations and regulatory certification constraints, robotic surgery holds appeal for all hospitals and physicians performing minimally invasive laparoscopic procedures.We have summarized the driving forces and barriers influencing the adoption of robotic laparoscopic surgery among four key stakeholders: hospitals, physicians, patients, and the government. Price reduction emerges as the solution to most challenges. Assuming the price of domestically produced robotic laparoscopic surgical systems drops to RMB 6 million per unit, their cost would become comparable to that of common large-scale hospital equipment such as CT scanners, which have already become standard configurations in Chinese hospitals. Regarding consumables, we estimate that the current cost of disposables for a conventional laparoscopic procedure ranges from several thousand to approximately RMB 10,000. If the cost of consumables for robotic laparoscopic surgery were reduced to RMB 10,000 per procedure, its adoption rate should reach levels comparable to those of conventional laparoscopic surgery.Therefore, we believe that under ideal circumstances, with the complete liberalization of configuration permits, robotic laparoscopic surgery should penetrate to the county level, while tertiary A hospitals should be equipped with multiple units.

3.4 Following the “price-for-volume” strategy, the market size of China’s laparoscopic surgical robot sector could reach RMB 48.7 billion

We forecast the market size for laparoscopic surgical robots based on a revenue structure comprising equipment, consumables, and service fees.Data on the number of hospitals and the annual volume of target surgical procedures are sourced as follows:

1) According to the 2020 Statistical Bulletin on the Development of China’s Health and Wellness Undertakings, there were 2,996 tertiary hospitals nationwide, including 1,580 Grade A tertiary hospitals.

2) According to the 2020 China Health Statistics Yearbook, there were a total of 4,321 Grade II Class A hospitals in China.

3) Based on Life Science Intelligence’s 2017 estimates of the number of various surgical procedures in China, we believe that the target procedures potentially amenable to robotic laparoscopic surgery total at least 7.91 million cases annually.

Under an optimistic scenario, we project that in 5–10 years, the selling price of domestically produced robots will be RMB 6 million, with average consumables costs per surgery at RMB 10,000. At this price level, we believe Grade A tertiary hospitals will own an average of 2.5 laparoscopic robots each, other tertiary hospitals 1.5 units each, and Grade II Class A hospitals 0.8 units each. Based on the number of hospitals in China in 2020, the Chinese market can accommodate 9,531 robots. Assuming a 7-year depreciation period, 1,362 new units will be added annually under steady-state conditions, resulting in an equipment market size of RMB 8.2 billion. In terms of surgical volume, assuming a 50% penetration rate for target procedures, China will perform 3.955 million laparoscopic robot-assisted surgeries annually, equivalent to 415 surgeries per robot per year, yielding a consumables market size of RMB 39.6 billion. We estimate annual service fees per robot at approximately RMB 100,000, leading to a service fee market size of around RMB 1 billion. Combined, the total market size for domestically produced surgical robots in China reaches RMB 48.7 billion.

In a pessimistic scenario, we estimate the selling price of domestically produced robots at RMB 14 million, with an average consumable cost of RMB 20,000 per surgery. The average installed base is one unit per Grade A tertiary hospital and 0.1 units per other tertiary hospital, while hospitals below the tertiary level do not adopt these systems. Assuming a seven-year depreciation period, the steady-state annual addition of new equipment amounts to 246 units. The penetration rate for target procedures in laparoscopic robotic surgery is approximately 10%, translating to 790,000 laparoscopic robotic surgeries performed annually, with each device conducting an average of 459 procedures per year. The consumables market size reaches RMB 15.8 billion, bringing the total addressable market to RMB 19.4 billion.

We use the annual number of surgeries per robot as an indicator to assess the model’s validity. Under three scenarios, the annual surgical volume per robot remains stable at approximately 400–500 procedures. Based on calculations from MicroPort MedBot’s prospectus, the pre-pandemic (2018) annual number of laparoscopic robotic surgeries per unit in China was 435 cases.

4In the New Era of Chinese-Made Robots, MicroPort MedBot Takes the Lead in Completing Urology Clinical Trials, While WEGO Has Obtained Certification

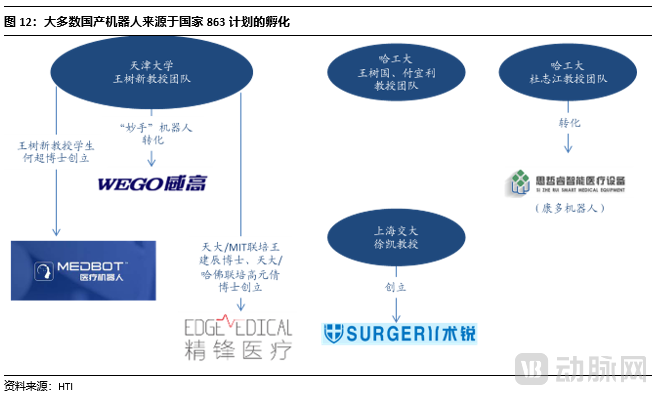

The 863 Program has accelerated the development of domestically produced surgical robots.The Intelligent Robotics Theme of the National High-Tech R&D Program (863 Program) funded surgical robot projects at Tianjin University and Harbin Institute of Technology, among others. In December 2013, Harbin Institute of Technology announced the completion of a laparoscopic surgical robot with independent intellectual property rights, which was subsequently commercialized as the Kangduo Robot project. Professor Wang Shuxin’s robotic project at Tianjin University was transformed into the Miaoshou series of robots by Weigao Group. Dr. He Chao, specializing in electronic and mechanical engineering at Tianjin University, later founded MicroPort MedBot. Dr. Wang Jianchen (Tianjin University, MIT) and Dr. Gao Yuanqian (Tianjin University, Harvard) are the founders of Shenzhen Jingfeng Medical, which has deployed both single-port and multi-port robotic systems. Additionally, Dr. Xu Kai, founder of Beijing Surgerii, developed a domestically produced single- and multi-port compatible laparoscopic robot using continuous dual-body design.

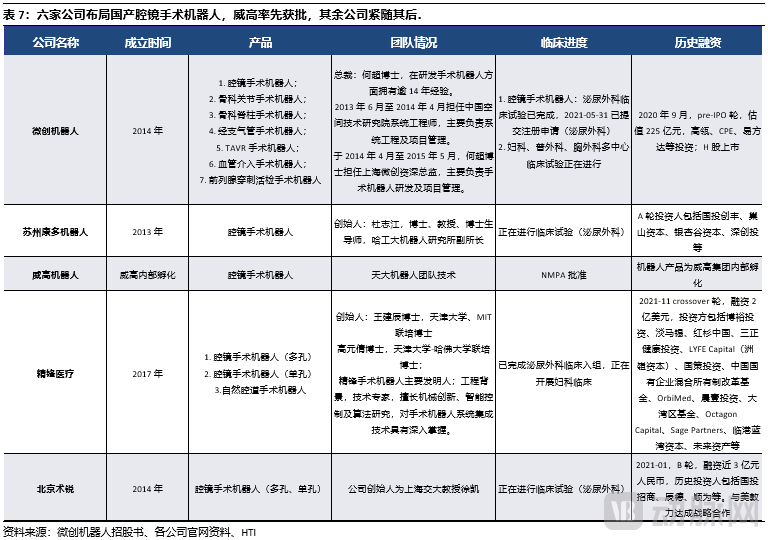

The first domestically produced laparoscopic surgical robot has been approved.On October 27, 2021, the National Medical Products Administration (NMPA) approved the registration application for the innovative product “Laparoscopic Endoscopic Surgical System” manufactured by Shandong Weigao Surgical Robot Co., Ltd. In addition to Weigao, MicroPort MedBot is currently in the registration application phase in China; Edge Medical has completed clinical enrollment in urology; and Kangduo Robotics and Shurui are undergoing clinical trials. We anticipate that by 2025, six domestically produced surgical robots will have completed clinical trials and received approval, ushering in a new era for Chinese-made laparoscopic robotic systems.

Domestic surgical robot technologies follow complex development pathways, with diverse product forms.Diversification in technological architectures facilitates differentiated competition, thereby preventing the industry from becoming mired in price wars. We observe that domestically produced laparoscopic robots predominantly adopt an integrated four-arm design similar to the da Vinci Surgical System, with seven degrees of freedom and 3D visualization becoming standard features.

In addition to Weigao Robotics, MicroPort, Jingfeng Medical, ShuRui, and Kangduo have all publicly completed radical prostatectomies. MicroPort Robotics has completed urological clinical trials, demonstrating reliable product performance.Radical prostatectomy, as the most representative procedure in robotic surgery, serves as a “touchstone” for evaluating the performance of surgical robots. According to incomplete statistics, products that have completed urological clinical trials worldwide include the da Vinci system (Intuitive Surgical, USA), Versius (CMR Surgical, UK), Toumai (MicroPort MedBot, China), Hinotori (Medicaroid, Japan), and Hugo (Medtronic, USA). These products are all leading players in the field of laparoscopic surgical robots globally. It can be considered that MicroPort MedBot has secured a leading position among domestically produced laparoscopic surgical robots by leveraging its first-mover advantage. Currently, the Toumai laparoscopic robot has completed urological surgeries and is conducting multi-center, multidisciplinary clinical trials across China, covering gynecological, general surgical, and thoracic surgical procedures. It is the domestic robot with the fastest clinical progress and the widest range of covered surgical procedures.

5China's Endoscopic Robot Market Is Currently Constrained by Pricing and Configuration Certificates

We believe that the widespread adoption of laparoscopic surgical robots in China is an inevitable trend, although the pace of volume growth will not be rapid in the near term.It took Intuitive Surgical 20 years to achieve global installations of 5,989 units since its initial approval. As one of the most complex medical devices, laparoscopic robotic systems require substantial time for manufacturing, after-sales service, market education, policy formulation, and inclusion in medical insurance coverage. We believe that procurement permits will not be fully deregulated within the next 3–5 years, with the installation volume likely ranging from 300 to 500 units.We believe that the factors hindering the near-term volume growth of laparoscopic robots are as follows:

1) In the vast majority of regions and provinces, robotic laparoscopic surgery has not yet been included in medical insurance coverage.

2) Endoscopic surgical robots are expensive, and their purchase still requires a provincial-level allocation permit.

In the long run, price reductions driven by domestic production will effectively address the aforementioned issues, while in the short term, the market may remain in a phase of adjustment and exploration.

5.1 Robotic surgery is significantly more expensive than laparoscopic surgery

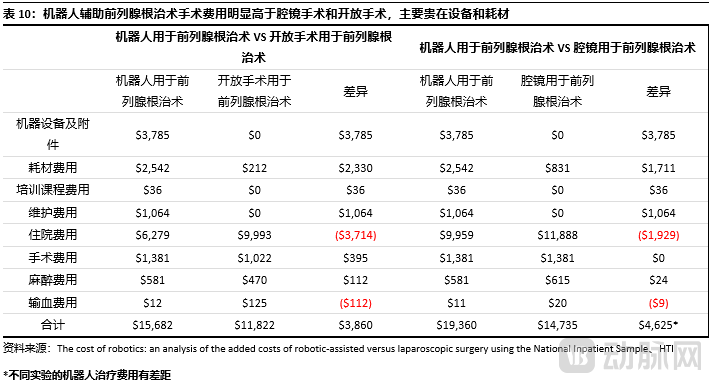

According to medical economic calculations, the high cost of robotic surgery is mainly attributed to equipment depreciation and consumables.A U.S. nationwide study of inpatient data indicates that robotic surgery can reduce certain costs, such as hospitalization and blood transfusion expenses, but incurs significantly higher costs for equipment and consumables compared with laparoscopic and open surgeries.

The price of the da Vinci surgical robot in China, as well as the cost of consumables, is higher than that in the United States.According to Intuitive Surgical’s 2020 annual report, the price of a single da Vinci surgical robot system ranges from $500,000 to $2.5 million. However, in China, public data indicate that the fourth-generation da Vinci robot distributed by Fosun Pharma is priced at approximately $3.5 million. Meanwhile, the cost of consumables per da Vinci robot-assisted surgery in China, ranging from RMB 30,000 to 50,000, is also higher than that in the United States. These factors have hindered the development of laparoscopic robots in China.

5.2 Domestic production will accelerate the inclusion of robotic surgery in medical insurance, further unleashing demand

Shanghai has taken the lead in including laparoscopic surgical robots in its medical insurance reimbursement coverage.On April 6, 2021, the Shanghai Municipal Healthcare Security Administration issued the "Notice on Matters Concerning the Inclusion of Certain Newly Added Medical Service Items in the Basic Medical Insurance Reimbursement Scope of This City," incorporating robotic laparoscopic surgery under the category of "Artificial Intelligence-Assisted Therapeutic Technology" into Class B medical insurance coverage, with patients bearing 20% of the cost. The reimbursable procedures include: "radical prostatectomy, partial nephrectomy, total hysterectomy, and radical resection for rectal cancer." These four procedures initially covered by reimbursement are those for which robotic surgery has demonstrated significant advantages, as validated by years of clinical practice abroad. We believe that the subsequent expansion of indications will be guided by the clinical advantages of robotic surgery; procedures likely to be included in medical insurance coverage in the future may include "hernia repair, cholecystectomy, and mitral valve repair," among others.

5.3 Configuration Certificates and Pricing Hinder Hospitals from Purchasing Laparoscopic Robots

Strong Demand for Surgical Robots in China, but High Import Prices Hinder Industry Development.Compared with the United States and Japan, China has an extremely low penetration rate of laparoscopic surgical robots, yet the number of procedures performed per unit is relatively high. However, in terms of procedures per unit, a total of 1.24 million da Vinci robotic surgeries were performed globally in 2020, with an average of 218 procedures completed per robot annually. According to calculations based on MicroPort MedBot’s prospectus, the number of laparoscopic robotic surgeries per unit in China reached 435 in 2018. The average annual number of surgeries per robot in China is nearly twice the global average. We believe this indicates suppressed demand for surgical robots in China, which may be met by domestically produced robots.

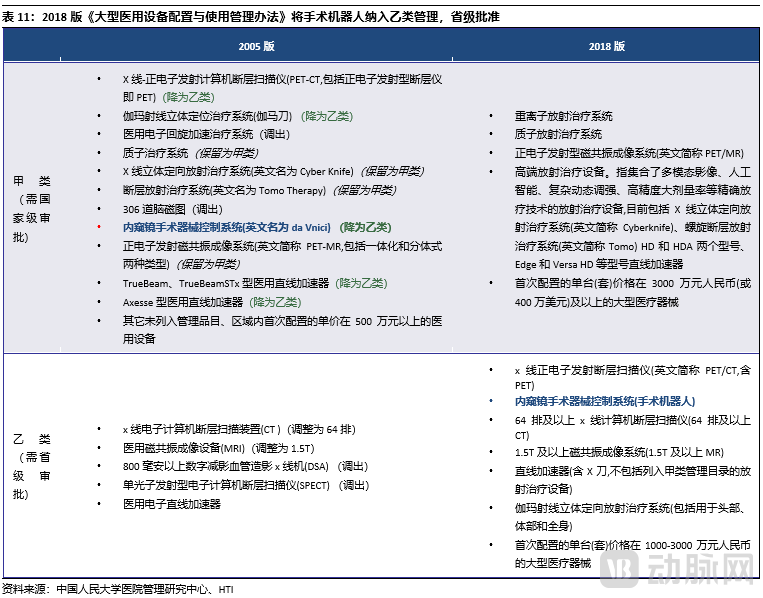

Currently, hospitals must obtain provincial-level approval to purchase surgical robots, with configuration controls primarily targeting high-unit-price medical equipment.When the da Vinci Surgical System was first introduced, it was classified as a Class A medical device under the “Administrative Measures for the Configuration and Use of Large-Scale Medical Equipment” issued by the National Development and Reform Commission (NDRC), requiring national-level approval for its purchase and introduction. In 2018, surgical robots were reclassified as Class B devices, with procurement subject to provincial-level approval. This policy relaxation in 2018 directly led to a substantial increase in the installed base of surgical robots in China in 2019 and 2020, with annual growth rates of 79% and 41%, respectively. Given the ongoing trends toward domestic production and price reductions for surgical robots in the coming years, we anticipate that their installation volume will continue to rise.

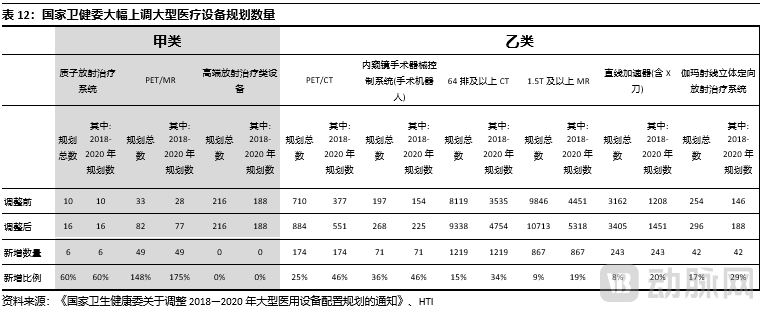

The national plan for 2018–2020 increased the allocated number of surgical robots from 154 to 225 units; we project that the annual upper limit for new installations will be approximately 100 units over the next five years.On July 31, 2020, the National Health Commission (NHC) issued the “Notice of the National Health Commission on Adjusting the Configuration Plan for Large Medical Equipment from 2018 to 2020,” substantially increasing the approved quotas for Class A and Class B large medical equipment. The planned configuration quotas for PET/CT scanners and surgical robots, both classified as Class B equipment, were each raised by 46%. According to Frost & Sullivan statistics, the installed base of surgical robots in China increased by 114 units from 2018 to 2020, falling short of the originally planned target of 154 units. Therefore, we believe that in addition to policy restrictions, economic considerations are also a key factor limiting the purchase of da Vinci surgical systems by hospitals in China.

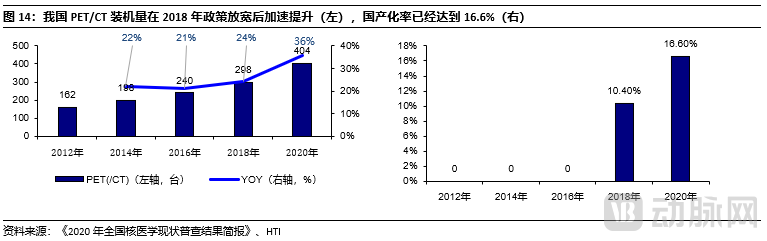

PET-CT Perspective on the Commercialization of Domestic Surgical Robots: 16.6% Localization Rate Four Years After ApprovalSince 2016, domestically produced PET(/CT) systems have gradually received regulatory approval. As of July 10, 2021, a query of the National Medical Products Administration (NMPA) database revealed approvals for Jiangsu Sinogrand (2016), Shanghai United Imaging (2016), Shenyang Neusoft (2016), Beijing Ruisikang (2017), and Hubei Ruishi Digital (2020). With the approval of domestically produced PET(/CT) systems, the year-on-year growth rate of PET(/CT) installations in hospitals across China has increased significantly. Meanwhile, the market share of domestically produced PET(/CT) systems has risen rapidly, reaching 16.6% by 2020.

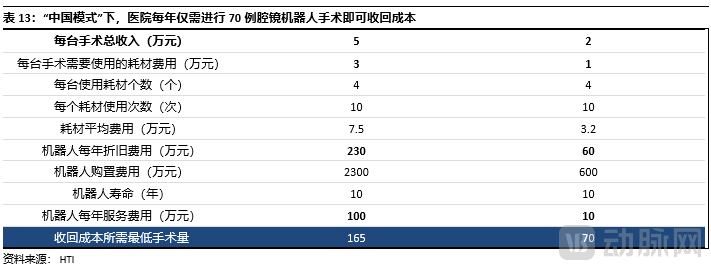

Da Vinci’s high pricing restricts non-tier-3 hospitals from purchasing robotic systems, while the price reduction of domestically produced alternatives will lower the threshold for hospitals to acquire laparoscopic surgical robots.Given the current high price of the da Vinci system, hospitals need to perform at least 165 robotic surgeries annually to break even. Based on our optimistic projections for the pricing of domestically produced robots in China, hospitals would only need to conduct 70 procedures per year to recoup their costs, significantly lowering the threshold for adopting laparoscopic robotic surgery. The logical relationships between other barriers and their corresponding solutions are now clearer. Overall, we believe that with large-scale domestic production and subsequent price reductions, laparoscopic robotic surgery will be more rapidly deployed across China.

6Endoscopic Robotic Platforms: High Value and Wide Application Range

Although surgical robots cannot perform surgeries autonomously, they have taken the first step toward standardizing surgical procedures.Unequal distribution of medical resources has long been a persistent issue in China’s healthcare system, with the varying levels of physician competence being one of its primary manifestations. In 2020, there were 2,996 tertiary hospitals in China, accounting for 8.5% of the total number of hospitals; however, these institutions handled 1.8 billion patient visits annually, representing 54.2% of all hospital visits. This disparity may stem from the public’s lack of confidence in the competence of physicians at primary care facilities. For open and laparoscopic surgeries, surgical quality depends on physicians’ clinical experience and technical operative skills. In contrast, with Robot-Assisted Surgery (RAS), robotic systems compensate for deficiencies in manual operative skills among some surgeons, thereby narrowing the gap in surgical capabilities among physicians across different hospitals.

AI+AR Technology Enables Less Experienced Physicians to Accurately Identify Anatomical Landmarks, Significantly Reducing Surgical Complexity.Da Vinci Iris is a 3D modeling software based on CT scans, enabling physicians to formulate surgical plans using anatomical models. The application of augmented reality (AR) technology allows for the real-time overlay of anatomical structures, such as blood vessels, onto the surgical field, thereby assisting physicians in more accurately locating and identifying anatomical landmarks.

Surgical robots were originally designed for use on the battlefield and in space.From the 1970s to the 1990s, multiple surgical robot projects emerged in the United States, Canada, and Europe. The original design intent behind surgical robots was to enable physicians to perform remote surgeries on astronauts in space and injured soldiers on the battlefield from within hospitals. NASA and the U.S. military funded numerous unsuccessful projects, which failed due to factors such as excessive signal transmission latency, insufficient precision of robotic movements, and inadequate product reliability.

China’s First Domestically Produced Remote Radical Prostatectomy Completed; Advancements in 5G Technology Make Remote Surgery PossibleAccording to a report by China News Service, in March 2021, Shanghai Changhai Hospital and Jiaxing No. 1 People’s Hospital performed the first remote radical prostatectomy in China using the Shurui single-port laparoscopic surgical robot. Early studies in the United States have indicated that surgeons can successfully perform procedures using laparoscopic robots with latency of up to 200 milliseconds. Typically, master-slave control systems in surgical robots exhibit inherent latency, which is further compounded by signal transmission delays in remote surgery; therefore, remote surgery imposes stricter requirements on the robotic system itself. The refinement of 5G technology has significantly reduced signal latency and improved data transmission quality. If the intrinsic latency of the robots themselves can be further reduced in the future, the feasible distance for remote surgery will increase substantially. The distance between Shanghai and Jiaxing is 100 kilometers, whereas the International Space Station orbits at an altitude of 400 kilometers. With continued technological advancements, space-based surgery may also become possible.

Compared with traditional laparoscopic surgery, robotic surgery utilizing VR is not difficult to learn.Enhanced by VR technology, surgeons can perform multiple surgical simulations on robotic platforms, with an experience akin to “playing video games.” Taking radical prostatectomy as an example, studies indicate that the learning curve for laparoscopic radical prostatectomy is approximately 200–250 cases, whereas the learning curve for robotic surgery is shorter, with proficiency typically achieved after 30–40 cases. According to continuous observations at UC San Diego from 2005 to 2016, the average operative time for robotic surgeries at this center was approximately 453 minutes per case when first introduced in 2005; however, by 2007, it had decreased by 46% to 246 minutes, after which it stabilized.

Author

Linda Shu, PhD

linda.yl.shu@htisec.com

Hahn Zhang

Hahn.h.zhang@htisec.com

Jason Zhuang Jiexian

Jason.Zhuang@us.htisec.com