Quanyuantang Pharmacy, a New Retail Dark Horse with Nearly 500 Stores and Over RMB 1.2 Billion in Annual Revenue, Files for IPO

In 2021, chain pharmacies witnessed a surge in IPO rushes.

According to incomplete statistics from VCBeat, several chain pharmacy companies, including Dingdang Kuaiyao, Chinese People’s Health, Sifang Health, Yuanxin Technology, and Dajia Weikang, have filed prospectuses this year. Among them, Dajia Weikang, known as the “first stock” of professional pharmacies, successfully went public on December 7.

On the evening of December 22, another unicorn company made a sprint toward its IPO: Chengdu Quanyuantang Pharmacy Chain Joint Stock Co., Ltd. (hereinafter referred to as “Quanyuantang”) filed an application with the Main Board of the Hong Kong Stock Exchange, with Citigroup and Haitong International serving as joint sponsors.

Since its establishment in 2012, Quanyuantang has demonstrated the potential of a dark horse.As of the latest practicable date in the prospectus, Quanyuantang has established 471 offline retail pharmacies across 15 cities in China, including first-tier and new first-tier pharmaceutical consumer markets such as Chengdu, Chongqing, Guangzhou, Shanghai, Shenzhen, Zhengzhou, and Xi’an. According to Frost & Sullivan,Based on the average number of orders per pharmacy per month (2020 data), Quanyuantang ranked first among all self-operated O2O and offline retail pharmacies in China.It is worth mentioning that during its development, Quanyuantang has garnered favor from over 15 capital firms.

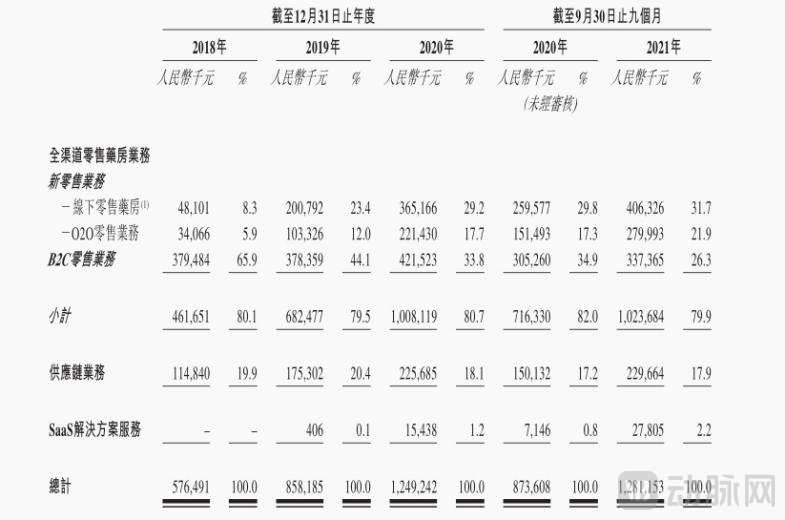

In terms of revenue, the prospectus shows that,Chengdu Quanyuantang Pharmacy Chain Joint Stock Co.,Ltd. recorded rapid revenue growth, with figures of RMB 576 million, RMB 858 million, RMB 1.249 billion, and RMB 1.281 billion in 2018, 2019, 2020, and the first nine months of 2021, respectively.

(Image source: Quanyuantang’s prospectus)

(Image source: Quanyuantang’s prospectus)

In terms of business operations, Quanyuantang primarily operates omnichannel retail pharmacies and provides SaaS solutions and supply chain services to customers.

Specifically:

· The omnichannel retail pharmacy business primarily includes: new retail operations (comprising offline retail pharmacies and O2O retail services) and B2C retail operations (operating online pharmacies on B2C e-commerce platforms);

·SaaS solution services include providing SaaS solutions to retail pharmacy customers and upstream pharmaceutical companies, empowering participants in the retail pharmacy industry to achieve online operations;

· Supply chain services refer to Quanyuantang, as a pharmaceutical wholesaler, selling pharmaceutical products to clients in other industries (including retail pharmacy clients, medical institutions, and pharmaceutical wholesalers).

As a rapidly growing omnichannel retail pharmacy in China,Quanyuantang has pioneered a new sales channel by operating online pharmacies on e-commerce platforms, integrating online and offline retail pharmacies with online prescription drug sales.According to Frost & Sullivan, Quanyuantang held a market share of approximately 0.8% in 2020 by revenue.

What does Quanyuantang’s “report card” look like as it makes its IPO push? How is its omnichannel retail pharmacy model performing? What are its core competitive moats? What challenges remain unresolved? In what direction will the industry evolve in the future? Answers to these questions may be gleaned from Quanyuantang’s development trajectory, business layout, and financial performance.

Quanyuantang’s brand journey has spanned over a century.: In 1902, Li Xichen, a renowned physician in Sichuan, founded Quanyuantang and opened his clinic for medical practice, marking the beginning of Quanyuantang's long-term development journey.

In 2012, marking the 110th anniversary of the clinic’s founding, Li Can, the fourth-generation heir of Quanyuantang, established Chengdu Quanyuantang Pharmacy Chain Joint Stock Co., Ltd. in Sichuan Province, formally entering the pharmaceutical retail sector. Within just two years, Quanyuantang opened 17 stores in Chengdu and Pujiang County, achieving sales revenue exceeding RMB 20 million.

In 2014, riding the wave of mobile internet, Quanyuantang set its sights on the then-booming pharmaceutical e-commerce sector and launched its Tmall flagship store, entering the B2C business.

According to Chen Zhouhua, CEO of Quanyuantang, as previously stated to VCBeat, there were three main reasons for entering the pharmaceutical e-commerce sector at that time.

· First, policies governing pharmaceutical e-commerce are becoming increasingly clear, with the state beginning to encourage the integration of "Internet Plus" into pharmaceutical distribution;

· Second, traditional pharmaceutical distribution companies and major internet firms have entered the pharmaceutical e-commerce sector. At that time, Jointown Pharmaceutical Group and Kangmei Pharmaceutical began launching their pharmaceutical e-commerce projects, while Alibaba had just acquired CITIC 21st Century, which owned the “95095” platform, to establish its presence in online pharmaceutical retail.

· Third, pharmaceutical e-commerce has demonstrated high growth potential, with a market growth rate consistently exceeding 200%, and the future market size is expected to be substantial.

Riding the industry tailwinds, Quanyuantang rapidly established an independent pharmaceutical e-commerce team in Guangzhou and gradually built out its warehousing, logistics, and other operational systems.Guangzhou was chosen because it is the national hub for pharmaceutical e-commerce: at the time, the top three pharmaceutical e-commerce companies in China were all based in Guangzhou. The local pharmaceutical e-commerce ecosystem and talent pool were relatively well-developed, facilitating Quanyuantang’s rapid market entry.

The results were evident: Quanyuantang’s e-commerce business achieved significant growth within a year. E-commerce revenue surged from less than RMB 1 million to over RMB 70 million (2015 data), with its share of total revenue rising from 2% to more than 75%. Notably, on Singles’ Day 2015, Quanyuantang’s online sales exceeded RMB 15 million, earning it the Tmall “Singles’ Day Sales Progress Award.”

Having tasted the benefits,Quanyuantang subsequently seized the opportunities presented by O2O retail pharmacies, taking the lead in developing an integrated online-to-offline retail pharmacy business model,It also operated pilot pharmacies for O2O retail in Chengdu. In 2018, Quanyuantang expanded the scope of its new retail business, gradually extending from Sichuan and Chongqing to more first-tier and new first-tier cities across China by replicating its proven single-store operational model.

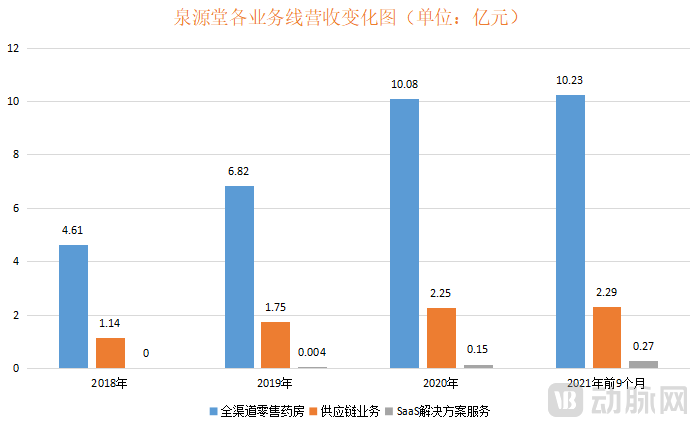

The prospectus shows that Quanyuantang’s offline retail pharmacies grew continuously from 24 stores at the beginning of 2018 to 471 offline retail pharmacies as of the Latest Practicable Date. Meanwhile, the proportion of revenue from new retail business in total revenue increased steadily from 14.3% in 2018 to 53.6% for the nine months ended September 30, 2021.

In this process, Quanyuantang has continuously expanded its supply chain business (selling pharmaceutical products to industry clients) and empowerment business (providing proprietary SaaS solutions to participants in the retail pharmacy industry) based on market demand.This has driven Quanyuantang to continuously evolve toward multi-business synergy, emerging as another dark horse among regional pharmacy chains, culminating in its current push for an initial public offering.

As one of the earliest enterprises to enter the pharmaceutical e-commerce sector, Chengdu Quanyuantang Pharmacy Chain Joint Stock Co., Ltd. has reaped the benefits from the development and transformation of the new retail consumer market in the pharmaceutical industry.

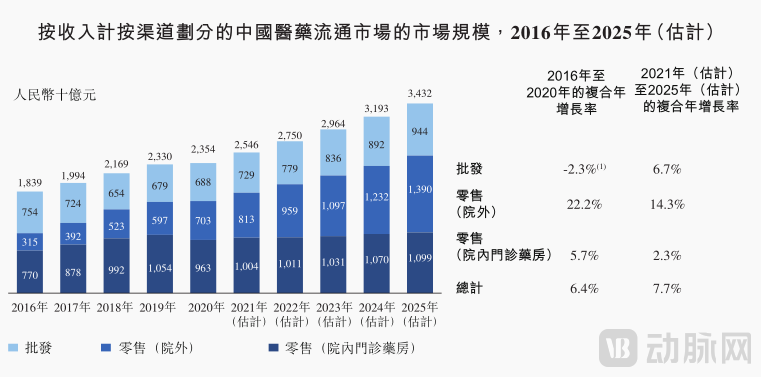

How should this be understood? Here, it is necessary to mention an industry background: in the pharmaceutical distribution sector, the market can be primarily divided into three segments: wholesale, in-hospital, and out-of-hospital. The wholesale segment is relatively traditional and accounts for a smaller share; the in-hospital market, needless to say, is predominantly dominated by hospitals. AndThe traditional out-of-hospital market is primarily composed of various retail pharmacies, characterized by a large number of participants, fragmented market share, and high operational costs., and since retail pharmacies are at the downstream end of the pharmaceutical distribution industry, they have weak bargaining power and generally face higher procurement costs.

(Image source: Quanyuantang’s prospectus)

With the digital transformation of the entire industry, offline out-of-hospital retail pharmacies are beginning to face intense competition from online out-of-hospital retail pharmacies and e-commerce platforms, due to the latter’s convenient purchasing processes, lower operating costs, and high efficiency in directly reaching target consumers.

In this context, how to better adopt strategies to respond and improve operational efficiency has become a topic that every traditional retail pharmacy needs to consider. In response to this, Quanyuantang’s solution is: to build an omnichannel retail pharmacy.

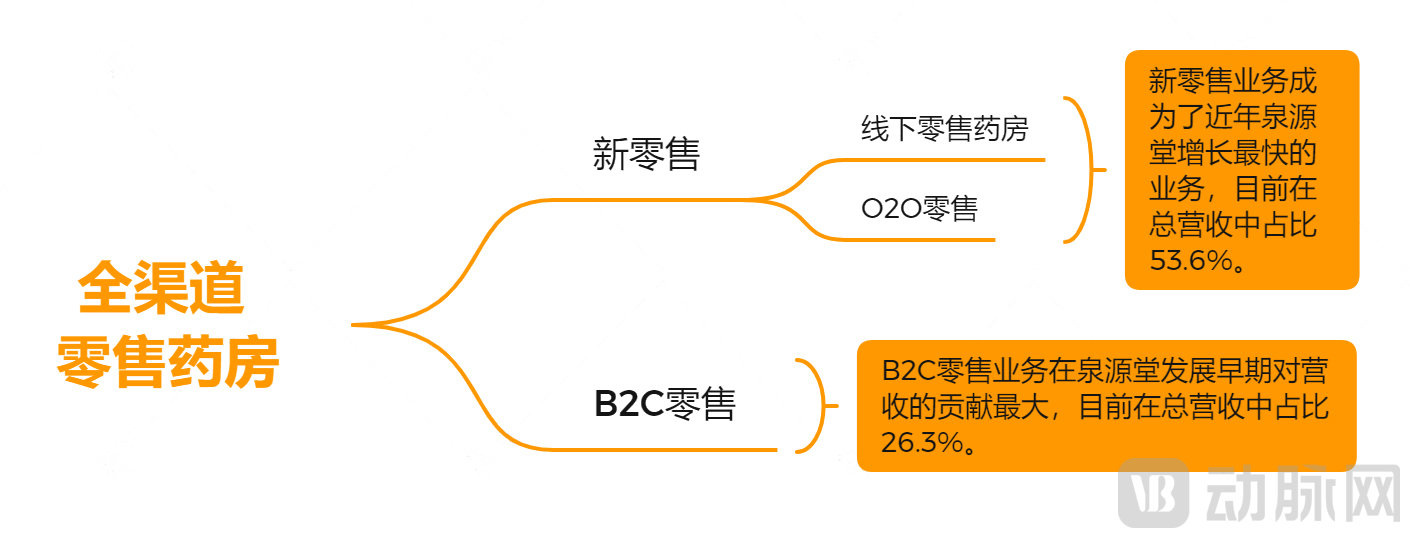

Specifically, omnichannel retail pharmacies operate through three distribution channels: offline retail, O2O (Online-to-Offline) retail, and online B2C (Business-to-Consumer) retail. Offline retail is conducted through sales at physical pharmacy stores; O2O retail fulfills online orders placed by customers located near physical pharmacies; and B2C retail involves merchants operating online stores on e-commerce platforms and delivering products to customers across China via express courier services.

In response to this logic, Quanyuantang willOmni-channel retail pharmacies are divided into new retail operations (offline retail pharmacies and O2O retail services) and B2C retail operations.

According to the prospectus, Quanyuantang's total revenue for the first nine months of 2021 was RMB 1.28 billion. Of this,Omni-channel retail pharmacy revenue amounted to RMB 1.023 billion, accounting for 79.9% of total revenue and representing the largest share.

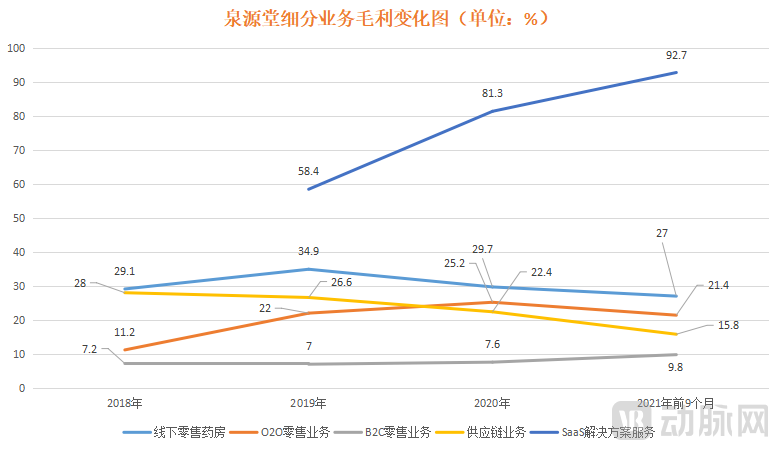

Let us now examine the various sub-segments of omnichannel retail pharmacy. As the earliest online business initiative, B2C retail contributed the most to revenue during the early development stage of Chengdu Quanyuantang Pharmacy Chain Joint Stock Co., Ltd., accounting for 65.9% of total revenue in 2018. However, with the rise of new retail operations, the share of B2C retail in total revenue declined to 26.3% in the first nine months of 2021, while the proportion of new retail revenue increased to 53.6%, exceeding half of the total.In other words, the new retail business has become Quanyuantang’s fastest-growing segment in recent years and now serves as the pillar supporting its total annual revenue of over RMB 1.2 billion.

From a strategic perspective, compared with single-channel or multi-channel retail pharmacies, the advantage of omnichannel retail pharmacies lies in providing comprehensive pharmaceutical products to patients and consumers: offline channels offer traditional face-to-face communication services; O2O channels cover scenarios for urgent medication needs, typically enabling instant delivery within one hour, thereby bringing great convenience to patients and consumers; B2C channels cover scenarios such as daily medications and health supplements, characterized by convenience, wide selection, and competitive pricing.

In short, omnichannel retail pharmacies have diversified drug purchasing channels and optimized the buying experience, thereby expanding their business scope and meeting the needs of consumers across different age groups and with varying preferences.

Furthermore, omnichannel retail pharmacies can sustain balanced and flexible growth by leveraging diverse sales and distribution channels. Additionally, these pharmacies can utilize cross-channel data to optimize their business strategies; the economies of scale derived from cross-channel operations also reduce procurement costs and improve inventory turnover.

However, it is important to recognize that offline retail pharmacies, B2C, and O2O are in fact fragmented business lines. If omnichannel strategy merely amounts to a simple aggregation of these elements, it may instead increase operational risks. Therefore, in practical implementation,To achieve significant synergies in omnichannel retail pharmacies, it is essential to leverage data analytics capabilities and intelligent technologies.. As can be seen, during the reporting period, Quanyuantang’s R&D investment increased rapidly from RMB 2.073 million in 2018 to RMB 9.137 million in the first nine months of 2021.

Interestingly, Quanyuantang is transforming its digital capabilities—originally developed to enhance internal efficiency—into a new business line that empowers traditional retail pharmacies. From a market perspective, small and medium-sized retail pharmacies lacking centralized management systems can acquire SaaS solutions at costs significantly lower than those associated with in-house development. Furthermore, these SaaS offerings can be delivered on demand and customized to meet the specific needs of small and medium-sized retail pharmacies. Moreover, leveraging its own omnichannel retail pharmacy operational expertise, Quanyuantang provides clients with operational guidance.

According to the prospectus, Quanyuantang’s SaaS solution services surged from RMB 406,000 in 2019 to RMB 27.805 million in the first nine months of 2021. Most notably, the gross profit margin of this business has steadily increased, rising from 58.4% in 2019 to 92.7% in the first nine months of 2021.Driven by rapid market expansion and exceptionally high gross margins, SaaS solution services are poised to become a new growth engine for Quanyuantang.

Specifically, Quanyuantang’s supply chain business involves selling certain well-known pharmaceutical products to industry clients—such as retail pharmacies, healthcare institutions, and pharmaceutical wholesalers, particularly those subscribed to its SaaS solutions—after securing regional agency rights (including both exclusive and non-exclusive regional distribution rights) for these products. In terms of proportion, revenue from exclusive regional distribution rights accounted for over 40% of the supply chain business income in each year from 2018 to 2020. Given that this segment is heavily influenced by exclusive regional distribution rights and its share of total revenue has been gradually declining (from 28% in 2018 to 15.8% in the first nine months of 2021), its growth ceiling appears relatively limited.

As can be seen, the logic behind Quanyuantang’s omnichannel retail pharmacy model is to leverage digital technologies and data analytics capabilities to foster stronger synergy among its offline pharmacies, O2O, and B2C operations. This approach enhances sales and operational efficiency at individual store levels, while also productizing its own supply chain and digital capabilities to achieve commercial monetization by empowering relevant clients.

Changes in gross profit can corroborate the actual effects achieved. From 2018 to the first nine months of 2021, Quanyuantang’s gross profit margins were 13.4%, 19.4%, 20.8%, and 20.7%, respectively.

In summary, Quanyuantang has achieved sustained growth in its overall business through its omnichannel retail pharmacies, marked by a steady increase in gross profit. The company has successfully expanded from the Sichuan-Chongqing region to numerous first-tier and new first-tier cities, establishing a unique differentiated position in the pharmaceutical retail sector. Moving forward, attention should be paid to controlling fulfillment costs and continuously strengthening digital capabilities.

From the perspective of current market evolution, the entire pharmacy industry is presenting a situation of “one rejoicing while another worries.”

“What worries” are single-store pharmacies.Due to their small scale, independent pharmacies have weak bargaining power with upstream suppliers, low levels of informatization, and poor risk resilience. Consequently, a large number of independent pharmacies have been deregistered and exited the market in recent years.

Taking Guangdong Province as an example, the number of pharmacies with their Drug Operation Permits revoked has shown a rapid growth trend. A total of 450 permits were revoked in 2019, 1,229 in 2020, and 2,163 by September 2021. In addition, during the first half of this year, Henan Province, Sichuan Province, Shaanxi Province, Yunnan Province, and other regions all issued announcements regarding the revocation of Drug Operation Permits.

This trend is set to continue. Based on the high-quality development target of achieving a retail chain affiliation rate close to 70% by 2025, and using the baseline of 561,000 pharmacies, the number of independent pharmacy outlets is projected to shrink to 168,300 over the next three years. Compared with the current figure of approximately 250,000, this represents a reduction of nearly 80,000 stores.

"Happy" are the chain pharmacies.As small, independent pharmacies accelerate their exit from the market, chain pharmacies will gradually capture a larger market share.However, this does not mean that combining multiple pharmacies offers a one-time solution for all future challenges; chain pharmacies also face immense competitive pressure.

From an internal perspective, the expansion in the number of stores also means a larger management radius, placing higher demands on corporate governance and daily operations. Meanwhile, regional breakthroughs are a significant challenge faced by the entire industry. As chain institutions scale up to hundreds, thousands, or even tens of thousands of stores in the future, the pressure on their teams’ financing capabilities becomes increasingly severe.

From an external perspective, China’s retail chain pharmacy sector is dominated by four core listed companies: Yixintang, Yifeng Pharmacy, Dashenlin, and Laobaixing. According to their latest quarterly reports, both Yixintang and Yifeng Pharmacy operate more than 8,000 stores each, while Dashenlin and Laobaixing each have over 7,000 stores, with all four continuing to accelerate their market expansion. For instance, in the first half of this year, Laobaixing and Yifeng Pharmacy each completed 11 mergers and acquisitions, spending RMB 573 million and RMB 312 million respectively, and incorporating 309 and 264 stores into their networks.

On the other hand, Quanyuantang, which has recently filed its prospectus; Dajiaweikang, which has just gone public; and companies such as Dingdang Kuaiyao, Huaren Health, Sipay Health, and Yuanxin Technology, which are currently striving for IPOs, are all gaining strong momentum. With continued capital support, these enterprises may evolve into large-scale chain operators with thousands of stores. Moreover, the entry of pharmaceutical e-commerce platforms and cross-industry competitors has further intensified market competition.

Policies are also propelling chain pharmacies into an era of massive expansion.In late 2020, the “Plan for the Division of Key Tasks from the National Teleconference on Deepening the ‘Streamline Administration, Delegate Power, Improve Regulation, and Upgrade Services’ Reform to Optimize the Business Environment,” issued by the General Office of the State Council, stated that restrictions on the distance between pharmacies would be abolished nationwide, which will further promote the expansion of chain pharmacies.

Regarding the future evolution and development direction of the industry, an investor who wished to remain anonymous told VCBeat that during the process of commercial implementation, the amount of cash flow will be the key to the development of chain pharmacies in a period of rapid expansion.Cash flow determines a pharmacy’s inventory stocking capacity and influences its expansion speed. Therefore, for chain pharmacies, two factors are critical: first, maintaining the ability to secure continuous financing; second, achieving cost reduction and efficiency improvement through technological and business model innovation. These elements are key to determining whether an enterprise can successfully emerge as a market leader.”

In terms of specific pathways, whether by laying out DTP (Direct-to-Patient) pharmacies that directly serve patients and differentiating through the provision of higher-value professional services, or by covering the full spectrum of patient medication scenarios via an omnichannel retail approach,The core lies in delivering greater added value: Amid the broader trend of chain expansion, relying solely on scale and price wars to capture market share is destined to become a “red ocean” struggle, whereas focusing on specific demographic segments or diversifying business offerings can help unlock new “blue ocean” markets.

It is important to recognize that, in this process, capital scale and the short-term number of pharmacies are not the key dimensions for assessing the success of a pharmacy chain; time is the only valid benchmark for evaluation:Only by earning users’ enduring trust and confidence can one emerge as true gold amid the industry’s rigorous trials.

Because a company’s true value often lies not in what it has achieved, but in what it contributes to society and the market.