Is Global Expansion the Ultimate Antidote to Domestic 'Involution' in China's Pharma Industry? BeiGene Secures $2.9B TIGIT Antibody Deal with Novartis

On December 20, BeiGene announced that it had entered into a collaboration agreement with Novartis, licensing the primary overseas rights to its TIGIT antibody to Novartis for $2.9 billion. Novartis will pay a $300 million upfront payment, additional payments of $600–700 million, $1.895 billion in regulatory approval and sales milestone payments, as well as tiered royalties of 20–25% on net sales.

TIGIT antibodies are one of the core products in BeiGene’s combination therapy portfolio. Clinical trials of PD-1 plus TIGIT inhibition have been conducted across multiple solid tumors, including non-small cell lung cancer, small cell lung cancer, cervical cancer, esophageal cancer, and liver cancer. Meanwhile, triplet regimens combining PD-1 inhibitors, TIGIT inhibitors, and chemotherapy are also being explored.

This marks another blockbuster collaboration between BeiGene and Novartis, following the PD-1 antibody tislelizumab.

In recent years, domestically developed innovative drugs have increasingly expanded into overseas markets, covering a wide range of therapeutic modalities, including immune checkpoint antibodies targeting PD-1, TIGIT, and CD47, SARS-CoV-2 neutralizing antibodies, antibody-drug conjugates (ADCs), CAR-T therapies, fusion proteins, and novel small-molecule drugs.

In January this year, Novartis licensed BeiGene’s PD-1 antibody tislelizumab for $2.2 billion, with an upfront payment of up to $650 million and a total transaction value exceeding $2.2 billion. This deal set two domestic records at the time: the highest upfront payment and the highest licensing transaction value for a single product. Additionally, several other Chinese biopharmaceutical companies, including RemeGen, Junshi Biosciences, Jacobio Pharmaceuticals, and Sino Biopharm, have expanded into global markets through overseas licensing and other strategies.

2020 is regarded as the inaugural year for domestic license-out deals in China. This year has continued the strong momentum from last year, with a steady increase in both the number and value of license-out transactions. According to incomplete statistics, a total of 40 domestic drug projects were licensed out overseas in 2021, among which 16 deals exceeded USD 100 million in transaction value.

License-out deals serve as a stepping stone for Chinese innovative pharmaceutical companies to successfully expand overseas and achieve internationalization. However, as these companies accelerate their global expansion, they face numerous challenges. In the face of fierce competition in overseas markets, how should domestic innovative pharmaceutical companies strengthen their independent R&D capabilities and promote commercialization in the global market to establish a firm foothold internationally?

Why is “going global” necessary? First, the era of windfall profits from license-in deals has passed, as centralized procurement has compressed profit margins and costs continue to rise. Second, intense domestic competition in innovative drugs is forcing companies to seek new revenue growth opportunities overseas, making global expansion increasingly urgent and an imperative choice for innovative pharmaceutical enterprises.

The licensing model has passed its period of high growth.

New drug development is one of the most risky, complex, and time-consuming areas of technological research in human advancement. Data shows that bringing an innovative drug from early discovery to commercial launch costs approximately $2.6 billion, takes more than 10 years, and has a success rate of less than one in ten. High R&D costs, long development cycles, and low success rates have long been the “three major burdens” weighing on pharmaceutical companies.

China’s pharmaceutical industry started relatively late, with R&D lagging behind. Coupled with historical neglect, this resulted in a prolonged growth phase characterized by the export of low-end active pharmaceutical ingredients (APIs) and the expansion of generic chemical drugs. In the face of intensifying global competition, as well as policy pressures such as volume-based procurement and adjustments to the National Reimbursement Drug List, the industry has begun to look toward biopharmaceutical innovation as the new pathway for transformation and breakthrough.

Since 2015, the Chinese government has introduced a series of favorable policies to encourage the research, development, and market launch of innovative drugs. Meanwhile, Chapter 18A of the Hong Kong Stock Exchange (HKEX) Listing Rules and the fifth set of listing criteria on the Shanghai Stock Exchange’s STAR Market have successively opened the doors of the capital markets to emerging biotechnology companies. Unprofitable biotech firms have flocked to list in Hong Kong, bolstering their R&D and commercialization efforts. In 2021, 18 unprofitable biotechnology companies completed initial public offerings (IPOs) on the HKEX, bringing the cumulative total to 46. Among them, four companies successfully removed the “B” marker from their stock tickers, marking a successful transition to commercialization.

Amid a series of favorable developments, Chinese innovative pharmaceutical companies are embarking on new paths for commercialization, with various innovative models emerging, including License-in, License-out, and the VIC model.

License-in, also known as inbound licensing, involves obtaining commercialization rights for a product in specific countries or regions—including development, manufacturing, and sales—by paying an upfront fee to the licensor, along with agreed-upon milestone payments and future sales royalties.

The most prominent feature of in-licensing is “speed.” On one hand, it enables companies to bypass the lengthy early-stage development process for new drugs, thereby enriching their R&D pipelines at a relatively low cost and accelerating subsequent market launch. On the other hand, it facilitates the rapid introduction of advanced foreign products into the domestic market, unlocking its potential, while also enhancing the company’s capabilities in secondary development. This approach helps maintain a product lifecycle nearly identical to that of the original foreign products and saves time on regulatory approval.

License-in has emerged as a favorable business model for the development of domestic biopharmaceutical enterprises, attracting intense competition among Chinese pharmaceutical companies. In 2021, there were over 130 license-in transactions, with transaction amounts continuing to rise. However, as China’s pharmaceutical ecosystem enters the 2.0 era, the license-in model is facing challenges.

First, as license-in prices continue to rise, the profits generated by in-licensed products are increasingly insufficient to cover costs, resulting in shrinking profit margins. Prior to 2019, domestic innovative drug in-licensing deals were predominantly valued at under $100 million, with an average upfront payment of approximately $15 million in that year. However, over the past three years, total deal values have surged, with 17 transactions exceeding $100 million, accounting for 60% of the total number of deals.

Secondly, under the backdrop of centralized procurement, the state will strictly control the scope of application and impose price caps on drugs that lack innovation and heavily consume medical insurance resources, thereby further squeezing profit margins.

Some industry observers argue that pharmaceutical companies’ choice to license in pipelines is essentially “borrowing” external innovations. By skipping preclinical R&D and directly bridging to clinical trials in China, the market tends to view this approach as a variant of the CSO (Contract Sales Organization) model. This perception stems not only from the lack of demonstrated R&D capabilities but also from the forfeiture of the core value proposition for biotech firms—namely, licensing out their assets.

The new regulations for the STAR Market released in March this year marked a turning point. In the “Guidelines for Evaluating Sci-Tech Innovation Attributes (Trial)” issued by the STAR Market in March, as well as in the latest revisions made by the China Securities Regulatory Commission (CSRC) to the Guidelines in April, new provisions were introduced to restrict companies based on “business model innovation” from going public. Meanwhile, applicants seeking listing on the STAR Market are now required to simultaneously meet four key criteria: “R&D expenditure as a percentage of revenue,” “number of invention patents,” “revenue thresholds,” and “proportion of R&D personnel.”

Meanwhile, the failed IPO attempts of some pharmaceutical companies in 2021 sent a signal to the industry that China’s sci-tech innovation market is no longer readily embracing “license-in”-based follow-on innovation.

Intense Competition Among Domestic Innovative Drugs Makes Global Expansion “Imminent”

Although some pharmaceutical companies in China are now capable of independently developing certain innovative products, the country is at a critical stage of transitioning from generic drugs to innovative drugs. The prevailing strategy is fast-following, focusing primarily on the development of Me-too or Me-better drugs, which subsequently leads to significant homogenization.

For instance, PD-1/PD-L1 immune checkpoint inhibitors are novel anticancer therapies that have emerged in recent years, offering a new lifeline for cancer patients. Since the launch of Opdivo, the first PD-1 monoclonal antibody, in China in June 2018, major pharmaceutical companies and national regulatory authorities have intensified their efforts. Currently, eight PD-1 inhibitors and four PD-L1 inhibitors have been approved for marketing in China.

This has led to a concentration of biological drug targets and significant redundancy. The PD-1/PD-L1 space is overcrowded, and price competition for innovative drugs has reached a fever pitch. In this highly competitive market, companies entering the PD-1 sector now face limited remaining market share.

According to statistics from Southwest Securities, 85 Chinese companies are engaged in the independent or collaborative development of PD-1 products, and the number of domestic PD-1 products is expected to reach 15 within the next two to three years. Previously, an expert noted that Chinese pharmaceutical companies are clustering around “innovation”; however, how can such Fast Follow or me-better drugs compete globally with First-in-Class therapies from other countries?

In recent years, the Chinese government has successively introduced multiple policies that emphasize patient-centered clinical needs across both R&D and reimbursement sectors. These measures aim to curb low-level duplication of generic drugs and homogeneous competition among innovative medicines, thereby compelling enterprises to pursue drug innovation and differentiation. Going forward, differentiated innovation will become the dominant trend in the biopharmaceutical industry.

Meanwhile, a growing number of industry professionals recognize that accelerating globalization is crucial for innovative pharmaceutical companies currently trapped in intense “involution.” Compared to the domestic market, which is characterized by fierce homogeneous competition, the international market represents a promising blue ocean for these enterprises. Data shows that by 2024, the global pharmaceutical market reached $1.64 trillion, with the innovative drug market accounting for $1.13 trillion, or nearly 70% of the total. “Going global” has become an urgent imperative.

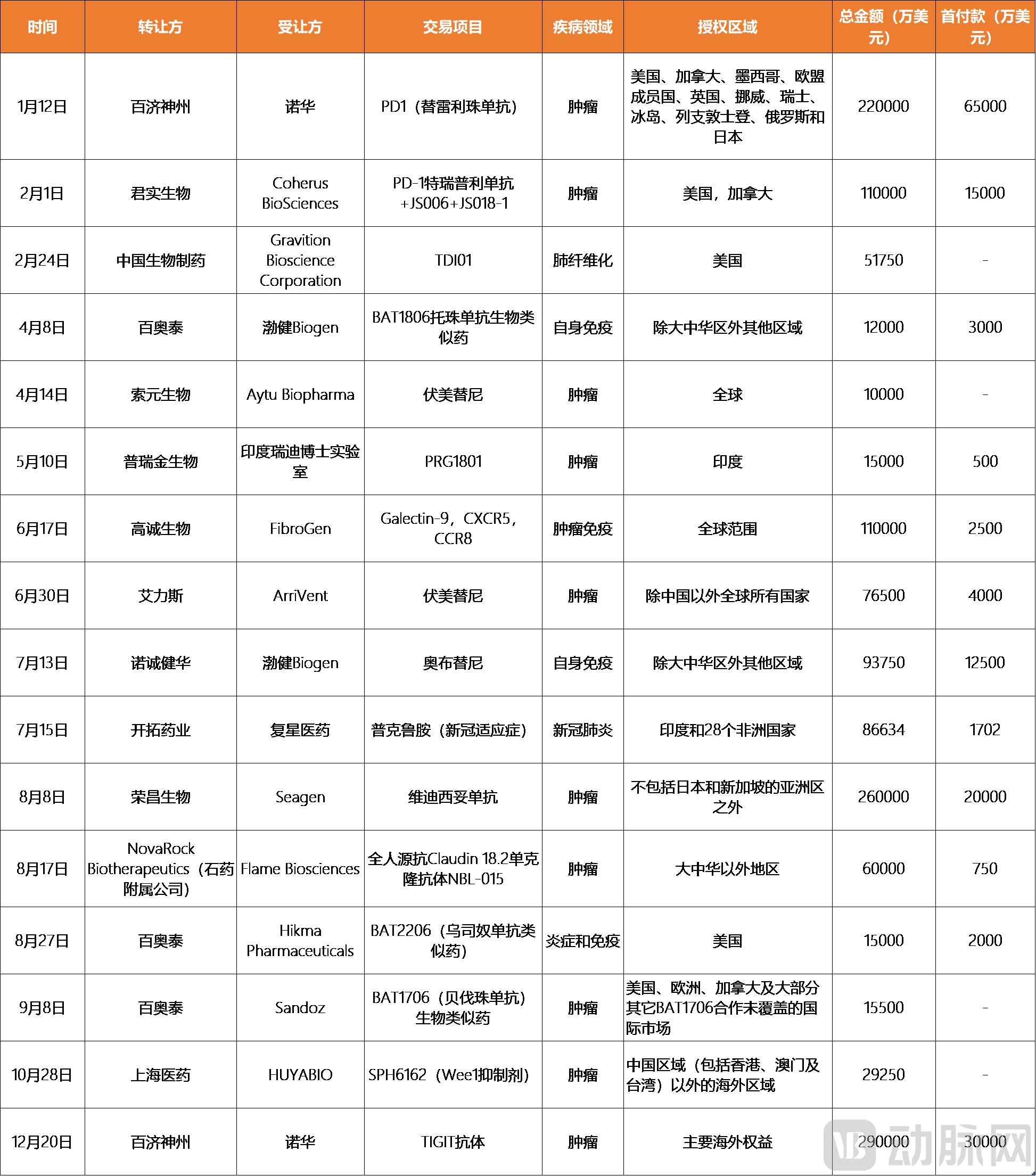

The licensing model is gradually shifting from in-licensing to out-licensing for overseas authorization. Collaborating with overseas pharmaceutical companies through out-licensing not only enables complementary advantages and reduces the risks of new drug development on the R&D side, but also leverages the sales networks of international large pharmaceutical companies on the commercialization side, allowing Chinese-made innovative drugs to enter the global market more rapidly and generate substantial cash flow returns. According to incomplete statistics, a total of 40 domestic drug projects were licensed out overseas in 2021, among which 16 deals exceeded USD 100 million in transaction value.

2021 License-Out Deals by Chinese Pharmaceutical Companies Valued at Over $100 Million (Source: Compiled from Public Information)

An increasing number of innovative pharmaceutical companies, along with traditional pharmaceutical firms transitioning toward innovation, are turning their attention to overseas markets, aiming to expand their global footprint through out-licensing agreements.

"Must be able to walk out, and stand firm."

The frequent license-out deals by domestic pharmaceutical companies signify that the R&D capabilities of Chinese new drugs are gradually gaining recognition in overseas markets. Underpinning these license-out transactions is the establishment of China’s innovative drug ecosystem, which no longer relies solely on in-licensing innovative drugs from foreign companies. Instead, it emphasizes accelerating the development of innovative technology platforms and differentiated products, enhancing new drug development efficiency, building overseas commercialization teams, and tapping into larger international markets.

However, it is undeniable that the overseas market is more challenging than the domestic market.

Liu Yi, Chief Medical Officer of Dimed Biopharmaceutical Technology in China, categorizes the global expansion of innovative drugs from China into four stages: first, licensing innovative drugs to multinational pharmaceutical companies for global development; second, internationalizing clinical trial operations, such as establishing overseas clinical teams and recruiting patients for international multicenter clinical trials; third, internationalizing R&D, such as recruiting R&D talent abroad and building early-stage R&D teams; and finally, internationalizing commercialization by establishing proprietary overseas commercial teams.

So, how can domestic innovative pharmaceutical companies take the first step toward going global?

Wang Yinxiang, Chairman and CEO of Jacobio Pharmaceuticals, stated that to gain recognition from multinational pharmaceutical companies, a project must first be based on a novel target with a solid scientific foundation; targets in highly competitive “red ocean” markets are unlikely to secure substantial out-licensing deals. Second, all data must meet international standards, and patent protection must be comprehensive. Third, the project’s progress in filing an Investigational New Drug (IND) application in the United States must rank among the top three globally. Even if a project is promising, if more than a dozen companies worldwide are pursuing similar efforts, there is virtually no opportunity for out-licensing. Once these hard criteria are met, effective communication between the two parties’ teams is also essential.

It is reported that Jacobio’s SHP2 inhibitor was licensed to AbbVie last year for an upfront payment of $45 million, milestone payments totaling $811 million, and a double-digit percentage share of global sales. This deal positions Jacobio to potentially generate over $855 million (approximately RMB 5.5 billion) in license-out revenue.

Chinese innovative drug companies must not only go global, but also establish a firm foothold.

An executive at a multinational pharmaceutical company stated that overseas markets have their own requirements for clinical trial design and clinical data processing. Companies must possess the capability to conduct global clinical trials, ensure high drug efficacy, and provide comprehensive clinical trial data.

Recently, an overseas report noted that Dr. Pazduer, an FDA expert, stated at a “Biopharmaceutical Conference” that approving new drugs based solely on clinical data from a single country is problematic—for instance, relying exclusively on clinical data from China. This approach runs counter to the U.S. principle of striving to enhance patient diversity in clinical trials. The report interpreted Dr. Pazduer’s remarks as indicative of the FDA’s future direction, suggesting that the agency is imposing increasingly stringent requirements for clinical trials, thereby further raising the bar for Chinese companies seeking to expand into global markets.

The aforementioned executives also stated that the ability to rapidly establish local sales teams, integrate into local markets, and form strategic partnerships with local enterprises is also a critical capability.

Beigene and Novartis have joined forces to pave the way for the global commercialization of tislelizumab. Under the licensing agreement, the two parties will co-develop tislelizumab in the United States, Canada, Mexico, EU member states, and other regions. Novartis will be responsible for regulatory filings after a transition period and will carry out commercialization activities upon approval.

BeiGene has also deployed its own commercialization team in overseas markets. According to the company’s prospectus, as of March this year, BeiGene’s commercialization team in the United States comprised more than 100 members.

In addition to BeiGene, innovative pharmaceutical companies such as CStone Pharmaceuticals, InnoCare Pharma, and Innovent Biologics have all chosen to partner with industry giants to advance the global commercialization of their innovative drugs.

“Independent R&D” of innovative drugs is destined to be a thorny path. Securing cash flow through overseas licensing and achieving commercialization of one’s own products is merely the first step for innovative pharmaceutical companies in expanding their international market presence. “Leveraging partners to go global” means, to some extent, that fate remains in the hands of collaborators. Only by cultivating in-house commercialization capabilities in the global market, thereby feeding back into R&D and operations, can companies ensure long-term sustainability. Among the new wave of innovative drug companies going global, only those that actively build their own R&D and commercialization teams, independently drive new drug development, and efficiently conduct large-scale, multi-center clinical trials worldwide—ultimately bringing drugs to market—can firmly take their destiny into their own hands.

References:

1. Does the “License-in” Model for Innovative Drugs Still Have a Future? — Shanghai Municipal Commission of Science and Technology

2. Accelerated Global Expansion of Innovative Drugs: From $28 Million to $2.6 Billion, the Out-Licensing Model Has Proven Successful! — Times Weekly

3. BeiGene Licenses Antibody to Novartis for $2.9 Billion, Accelerating the Global Expansion of China’s Biopharma Sector — 21st Century Business Herald

4. From “Chokehold” to “Going Global”: Can Chinese Innovative Drugs Really Deliver?