How Deep-Water Internet Healthcare Companies Are Selling Drugs: Business Models, Product Portfolios, and Recent IPO Filings

As 2022 began, the internet healthcare industry, which had been developing for over two decades, entered its “deep-water zone.”

From the earliest attempts at medical literature retrieval and online lightweight consultations, to the increased investment in pharmaceutical e-commerce and medical science popularization, and now to the booming sectors of internet-based chronic disease management and internet hospitals, the exploration of business models in digital healthcare has never ceased.

To this day, internet healthcare is still defined by many industry insiders as merely “drug sellers.”

The reason is that, after internet healthcare companies have successively listed on secondary markets in recent years, it has become evident from their financial statements that core revenues are predominantly concentrated in “pharmaceutical e-commerce” or “pharmacy” income.It seems that, apart from the “drug sales” business, other initiatives in internet healthcare have yet to identify a viable commercial model.

From the current perspective, “drug sales” indeed constitute a major revenue source for internet healthcare companies. However, industry pioneers are gradually expanding into digital health and medical services sectors, though this path is challenging and cannot yield significant results overnight.

In this process, companies need to rely on sufficient cash flow to support their development, so the mature “drug sales” model naturally becomes the preferred path. After all,From the perspective of business fundamentals, profitability is one of the essential factors determining whether an enterprise can achieve long-term sustainability.

At this current juncture, how are digital health companies strategically positioning themselves within the now-established “online pharmacy” model? How are their drug sales performing? What challenges do they still face? And in their pursuit of profitability, what new “remedies” have they discovered? To address these questions, VCBeat has analyzed industry trends and conducted interviews with experts to shed light on the answers.

Next, you will learn about:

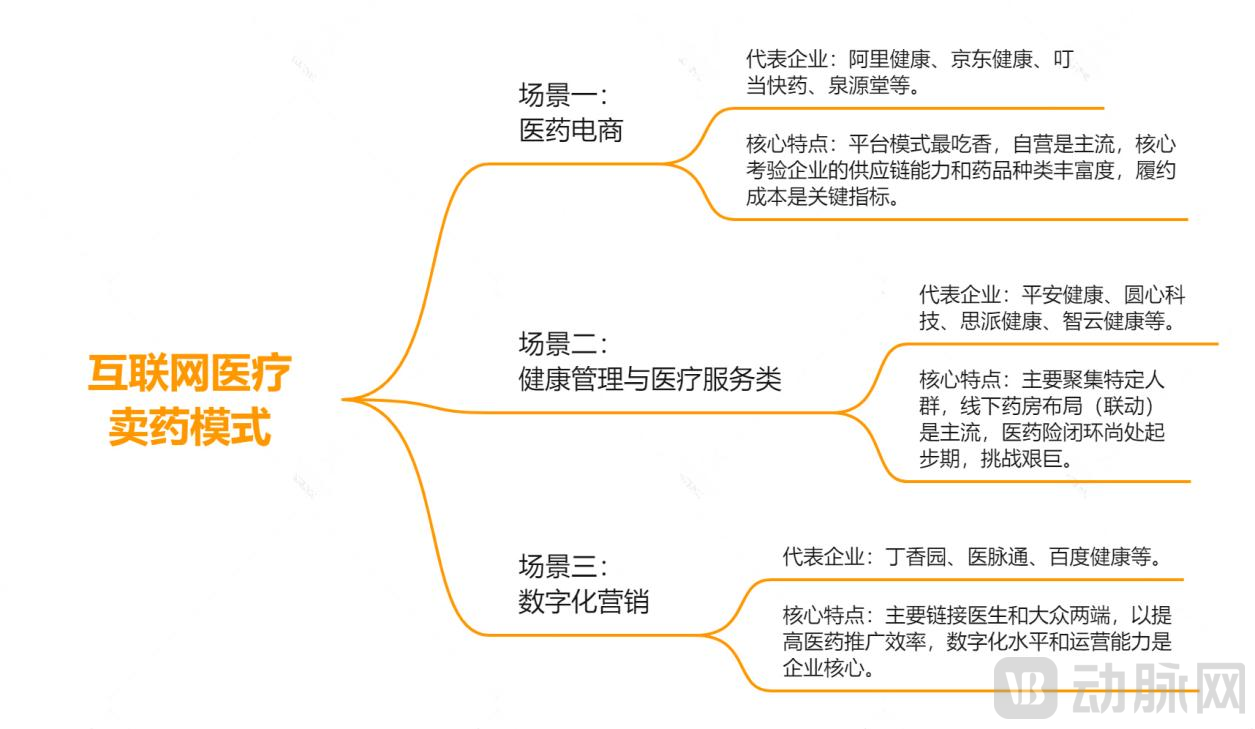

1. Currently, there are three major pharmaceutical sales scenarios in the industry: pharmaceutical e-commerce, health management and medical services, and digital marketing;

2. Pharmaceutical E-commerce Scenario: The platform model is the most favored, while self-operated models remain mainstream. The core challenges lie in a company’s supply chain capabilities and the diversity of its pharmaceutical product offerings, with fulfillment costs serving as a key performance indicator;

3. Health Management and Medical Service Scenarios: Primarily targeting specific populations, with offline pharmacy layouts (integration) being the mainstream approach; the closed-loop integration of pharmaceuticals, healthcare, and insurance is still in its infancy, presenting significant challenges;

4. Digital Marketing Scenarios: Primarily connecting physicians and the general public to enhance the efficiency of pharmaceutical promotion, with digitalization level and operational capability being the core competencies of enterprises.

“From the perspective of corporate financing moving into the late stage and the final sprint toward an IPO, internet healthcare companies that are currently profitable or have the potential for profitability are either already selling drugs or are in the process of building drug-selling scenarios to achieve a substantial increase in revenue.“A senior investor who has long observed the internet healthcare industry told VCBeat.”

Currently, internet healthcare enterprises can be broadly categorized into three types of pharmaceutical sales scenarios: e-pharmacy, health management and medical services, and digital marketing.

Due to the different scenarios in which companies specialize, pharmaceutical sales methods also vary.

Centered on pharmaceutical e-commerce: The platform model is most favored, while self-operated models remain mainstream. The core challenges lie in a company’s supply chain capabilities and the breadth of its drug portfolio, with fulfillment costs serving as a key performance indicator.

As one of the channels for pharmaceutical distribution, pharmaceutical e-commerce has seen rapid growth since 2013, with an average annual market size increase of around 10%, making it the most direct "online drug sales" channel currently.

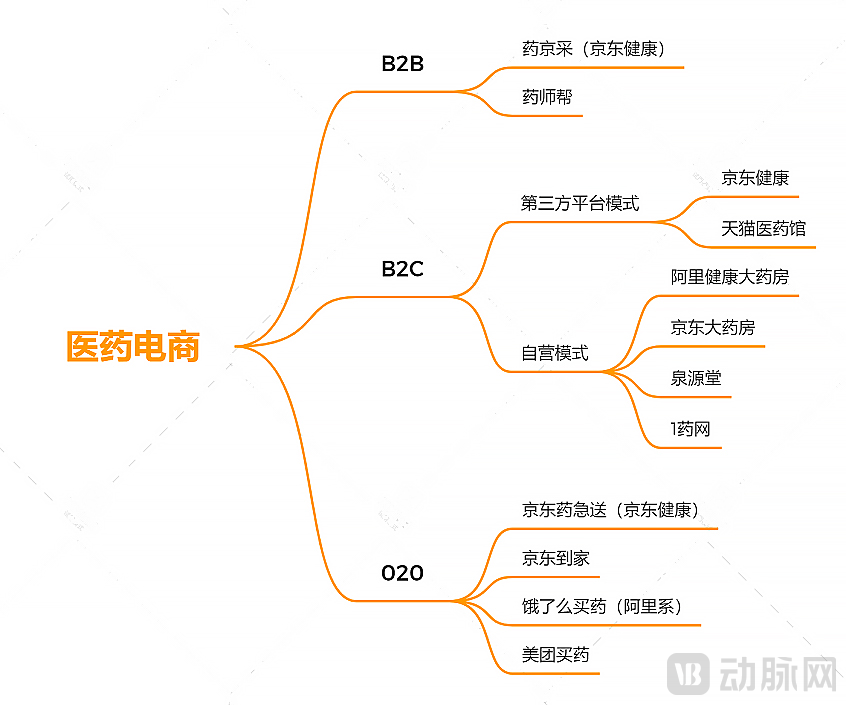

In terms of specific models, pharmaceutical e-commerce is primarily categorized into three types: B2B, B2C, and O2O.

In the early stages of the industry, innovative enterprises typically enter the market through a single focal point. As the industry matures into its mid-to-late stages, leading companies tend to adopt an integrated approach by simultaneously developing B2B and B2C channels (including third-party platforms and direct-to-consumer models) and establishing a presence in the “last-mile” O2O sector. This strategy optimizes the platform model to maximize economies of scale.

(Pharmaceutical E-commerce Types and Corporate Layouts, Chart by VCBeat)

In the current market landscape, active players in the pharmaceutical e-commerce sector include Alibaba Health, JD Health, Meituan Medicine, Dingdang Kuaiyao, Quanyuantang, 111.com, and Yaoshibang. Among these, Alibaba Health and JD Health are already publicly listed, while Dingdang Kuaiyao and Quanyuantang filed their prospectuses in 2021. The following analysis deconstructs how such companies strategize their layouts, based on the prospectuses or financial reports of four selected enterprises, as well as public media coverage and app-based observations.

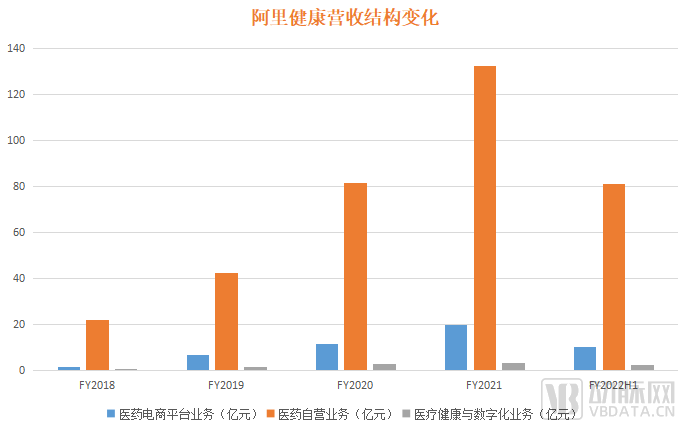

First, let’s look at Alibaba Health: its self-operated pharmaceutical business is the main driver of its revenue.According to the interim results announcement for fiscal year 2022 released in late November, Alibaba Health’s self-operated pharmaceutical business generated revenue of approximately RMB 8.1 billion, a year-on-year increase of 34.5%, accounting for nearly 87% of total revenue; platform business revenue reached RMB 1.01 billion, up 9.2% year on year, representing about 10.8% of total revenue.

Notably, within the proprietary pharmaceutical business, drug sales from self-operated pharmacies under the “AliHealth” brand accounted for 64% of revenue, while prescription drug business revenue grew by 127.3%.From this perspective, Alibaba Health is driving the expansion of its prescription drug business.

(Data source: Alibaba Health financial report; chart by VCBeat)

On the other hand, Alibaba Health encompasses the pharmaceutical e-commerce platform businesses of Tmall Pharmacy and its new retail model, generating a combined revenue of approximately RMB 1 billion during the period, representing a year-on-year increase of 9.2%. In terms of partner merchant scale, as of the end of the reporting period, the company had served over 25,000 merchants, an increase of 3,000 from six months earlier, with inventory exceeding 40 million SKUs, an increase of 7 million from six months earlier.This indicates that Alibaba Health is continuously intensifying its efforts to expand the number of merchants and pharmaceutical SKUs.

Leveraging its “self-operated + platform” model, Alibaba Health currently offers a comprehensive range of pharmaceutical products covering major chronic disease areas, including cardiovascular and cerebrovascular diseases, respiratory conditions, hepatobiliary disorders, gout, and diabetes. Meanwhile, commonly used medications in categories such as tonics and sedatives, gynecology, rheumatology and orthopedics, otolaryngology and ophthalmology, and dermatology are also available online. Furthermore, with the supplementary role played by numerous distributors on the Tmall Pharmaceutical Platform for specific drugs, Alibaba Health is well-positioned to meet the needs of the vast majority of patients with common and chronic diseases for online follow-up consultations and medication purchases.

It can be observed that Alibaba Health is continuously advancing its strategy of “focusing on pharmaceutical services through self-operated drug sales, while enriching the supply of medical and health products via platform merchants.”

However, beyond factors such as self-operated models and drug categories, pharmaceutical sellers must also consider fulfillment costs—namely, the total cost across the entire supply chain from procurement and warehousing to final delivery to consumers. This is often the key determinant of whether e-pharmacy companies can sustain their drug sales operations.

According to the financial report, Ali Health’s fulfillment expenses during the reporting period amounted to RMB 970 million, representing a 30.7% year-on-year increase from the same period in 2020. This rise was primarily driven by revenue growth in its direct pharmaceutical sales business. However, fulfillment costs as a percentage of revenue from direct pharmaceutical sales stood at 12.1%, a 0.3 percentage point decrease compared to the same period in 2020, indicating improved operational efficiency in warehousing, logistics, and customer service.

Furthermore, in bridging the “last mile” of pharmaceutical care, Alibaba Health launched the “Medicine Without Leaving Home” service on Taobao and Alipay in 2020. By adopting an internet-based medical approach that combines “online consultation and prescription” with “home delivery of medications,” this initiative enables patients with chronic diseases to purchase their required medicines from home.

Overall, Alibaba Health has adopted a hybrid strategy combining “direct sales” and “platform” models. Direct sales account for the largest proportion and are growing at a faster rate, with continuous efforts to drive growth in prescription drug sales through this channel. In terms of fulfillment, costs have decreased, and last-mile delivery capabilities are being continuously enhanced to cover various scenarios, including daily medication needs and urgent medical supplies.

Another giant, JD Health, has enriched its pharmaceutical ecosystem through the integration of online and offline services.According to the 2021 interim report, JD Health achieved product revenue (pharmaceuticals and health products) of RMB 11.762 billion in the first half of 2021, accounting for 86.2% of total revenue, with a year-on-year increase of 52.88%.

In terms of specific layout for pharmaceutical sales, JD Health's retail pharmacy business includes three operational models: self-operated, online platform, and omni-channel layout.From this perspective, a key feature of JD Health is its integration of online and offline services.

Specifically,The self-operated business is conducted through JD Health Pharmacy., and gradually establish a supply chain network encompassing industry-leading pharmaceutical companies and health product suppliers. For instance, JD Health has entered into strategic partnerships with domestic and international pharmaceutical enterprises such as Sanofi China and Guilong Pharmaceutical.

The online platform business primarily focuses on onboarding third-party merchants., which complements its self-operated business, with the core objective of offering users a more diverse range of product categories. The onboarded merchants include chain pharmacies, independent pharmacies, and health product vendors. As of June 30, 2021, JD Health’s online platform hosted approximately 14,000 third-party merchants.

The omnichannel strategy refers to JD Health’s partnerships with offline pharmacies across various regions., to meet the urgent medication needs of users, it has established a presence in over 300 cities across China, providing same-day delivery, next-day delivery, 30-minute delivery, and 24/7 rapid delivery services.

In addition to its online JD Pharmacy and Alliance Pharmacies, JD Health has also established offline hospital-adjacent stores and DTP (Direct-to-Patient) pharmacies in multiple regions. Furthermore, JD Health collaborates with global pharmaceutical companies to support their market expansion and maintenance in China.

In terms of drug categories, as the interim report does not break down the sales proportion by product subcategories (prescription drugs, over-the-counter drugs, health products, medical supplies and devices, etc.), it is not possible to determine the structure of JD Health’s pharmaceutical sales. However, in terms of product variety, JD Health’s SKU count has exceeded 40 million, nearly doubling from the end of 2020.

(JD Health App Interface | Screenshot from VCBeat)

Supply chain management capability is one of JD Health’s core competencies and a key differentiator in its pharmaceutical sales.According to the 2021 Interim Report, as of June 30, 2020, JD Health utilized 17 pharmaceutical warehouses and over 350 non-pharmaceutical warehouses across China from JD.com, effectively enhancing the efficiency of pharmaceutical inventory turnover.

Furthermore, certain specialty medications impose stringent requirements on the supply chain. To address this, JD Health and JD Logistics have established a proprietary cold-chain distribution capability for pharmaceuticals, covering 100 cities across 12 provincial-level administrative regions in China.Leveraging this capability, JD Health Pharmacy has been able to accelerate the expansion of its portfolio of specialty medications, such as those for rare diseases.Multiple cold-chain products from brands including Eli Lilly, Novartis, and Sanofi have been launched.

In terms of fulfillment costs, according to the interim report, JD Health’s inventory turnover days decreased by 5.2 days year-on-year from 2020, reaching 39.8 days. Meanwhile, the percentage of fulfillment expenses to total revenue declined from 10.4% in the first half of 2020 to 10% in the first half of 2021, showing a downward trend.

In summary, JD Health’s pharmaceutical sales strategy emphasizes online-offline integration, with supply chain management as its core competency. This has enabled the company to gradually expand its coverage to include special medications such as those for rare diseases, continuously reduce fulfillment costs, and extend into scenarios involving urgent medication needs.

Dingdang Kuaiyao submitted its prospectus last June. Its core business is pharmaceutical O2O services, and it currently relies entirely on self-operated “smart pharmacies” for delivery.According to the prospectus, as of March 31, Dingdang Kuaiyao had established 286 smart pharmacies, covering 14 cities including Beijing, Shanghai, Guangzhou, Shenzhen, and Tianjin.

Relying on the capital-intensive model of self-operated pharmacies, Dingdang Kuaiyao faces profitability challenges. Based on its overall performance, the company recorded net losses of RMB 103 million, RMB 274 million, and RMB 920 million from 2018 to 2020, respectively, due to changes in the fair value of preferred shares. In terms of adjusted losses, the figures for 2018 to 2020 were RMB 70 million, RMB 123 million, and RMB 149 million, respectively, indicating a year-on-year increase in losses.

However, judging from the trend of fulfillment costs as a percentage of revenue, which stood at 16.7%, 15.7%, and 12.7% from 2018 to 2020 respectively, the marked decline indicates a significant improvement in operational efficiency.

It can be seen that,Dingdang Medicine focuses on the O2O model and has adopted a capital-intensive, self-operated pharmacy strategy. While this places significant pressure on profitability, it has enabled continuous and stable improvements in fulfillment capabilities.

Quanyuantang, which submitted its prospectus in December, primarily operates omni-channel retail pharmacies.Specifically, omnichannel retail pharmacies operate through three distribution channels: offline retail, O2O (Online-to-Offline) retail, and online B2C (Business-to-Consumer) retail. Offline retail is conducted through sales at physical pharmacy stores; O2O retail fulfills online orders placed by customers located near physical pharmacies; and B2C retail involves merchants operating online stores on e-commerce platforms and delivering products to customers across China via express courier services.

According to the prospectus, Quanyuantang's total revenue for the first nine months of 2021 was RMB 1.28 billion. Among them,Omni-channel retail pharmacies generated RMB 1.023 billion in revenue, accounting for 79.9% of the total and representing the largest share of revenue.

Upon analysis, it was found that the B2C retail business, as the initial driver of Quanyuantang’s online operations, contributed the most to revenue in the company’s early stages, accounting for 65.9% of total revenue in 2018. However, with the rise of new retail businesses, the share of B2C retail in total revenue dropped to 26.3% in the first nine months of 2021, while the proportion of new retail revenue rose to 53.6%, exceeding half of the total.

That is to say,New retail has become the fastest-growing business segment of Quanyuantang in recent years and now serves as the pillar supporting its total annual revenue of over RMB 1.2 billion.

Omni-channel retail pharmacies have diversified drug purchasing channels and optimized the buying experience, thereby expanding business scope and meeting the needs of consumers across different age groups and with varying preferences. However, whether offline retail pharmacies, B2C, or O2O, these remain fragmented business lines. If omni-channel strategy merely amounts to a simple aggregation of these elements, it may instead increase operational risks.

Therefore, in practical operations, to achieve significant synergies in omnichannel retail pharmacies, it is essential to leverage data analytics capabilities and intelligent technologies. During the reporting period, QuanYuanTang’s R&D investment increased rapidly from RMB 2.073 million in 2018 to RMB 9.137 million in the first nine months of 2021.

Due to the continuous expansion of its offline retail pharmacy network, coupled with employee costs and fulfillment expenses, Quanyuantang has also faced losses. According to the prospectus, Quanyuantang’s net losses from 2018 to the first nine months of 2021 were RMB 93.431 million, RMB 166 million, RMB 155 million, and RMB 222 million, respectively.

Quanyuantang has pioneered the new model of omnichannel pharmacies, enabling it to cover the vast majority of medication purchase scenarios. Its core competitive barriers are digital capabilities and operational expertise. Nevertheless, it will also face long-term operational challenges.

Overall, in the context of pharmaceutical e-commerce, the platform model is most favored, with its core competitiveness hinging on the breadth of drug offerings and supply chain capabilities.An analysis of representative companies such as Alibaba Health, JD Health, Dingdang Kuaiyao, and Quanyuantang reveals that establishing proprietary self-operated businesses has become the mainstream strategy. Leveraging their respective parent companies, Alibaba and JD.com, Alibaba Health and JD Health hold significant advantages in pharmaceutical supply chains. They are also rapidly expanding their portfolios of prescription drugs and specialty medications, thereby achieving pronounced economies of scale.

From this perspective,On the business path of pharmaceutical e-commerce, such internet healthcare companies will compete on optimizing their supply chain systems and improving overall operational efficiency; going forward, particular attention must be paid to changes in fulfillment costs across different players.

Supported by Health Management and Medical Services: Aggregating Specific Populations with Offline Pharmacy Layouts (Integration) as the Mainstream, While the Closed-Loop of Medicine-Insurance Integration Is Still in Its Early Stages.

Among companies in the health management and medical services sector, Ping An Health, WeDoctor, Yuanxin Technology, SiPi Health, and Zhiyun Health are typical representatives. Ping An Health went public in 2018, while the latter companies all filed their prospectuses in 2021.

From a business layout perspective, Ping An Health, WeDoctor, Yuanxin Technology, Si Pai Health, and Zhiyun Health all started with healthcare services before expanding into diversified businesses. However, WeDoctor does not engage in specific drug sales operations.

From a strategic deployment perspective,For such internet healthcare companies, pharmaceutical marketing is a key component of their integrated strategy linking pharmaceuticals with health insurance products.

In other words, within the entire process chain, users (patients) purchasing medications are referred from online consultation services or payment benefits; therefore,Significantly different from pharmaceutical e-commerce: while traffic volume may be a relative disadvantage, the target audience is more segmented, and user stickiness is relatively stronger.

Next, we will examine how Ping An Health, Yuanxin Technology, Si Pai Health, and Zhi Yun Health achieve pharmaceutical marketing through their strategic layouts.

Ping An Good Doctor's competitive advantage lies in its access to 220 million Ping An financial services users.Ping An Health provides value-added services to Ping An Group’s insurance users through health and medical membership products: from a strategic perspective, Ping An Health first secured the payer (insurance) and then expanded into niche services such as pharmaceutical sales.Within this ecosystem, pharmacies are akin to hospital networks and health examination institutions, serving as an integral component of the overall service system.

Based on this logic, in addition to the two major categories of Chinese and Western medicines and nutritional supplements, the Health Mall within the Ping An Good Doctor app also offers products such as food, beauty cosmetics, personal care items, and household goods.Additionally, best-selling pharmaceuticals are primarily concentrated in commonly used medications and health supplements, generating substantial revenue., the financial report shows that Ping An Health's revenue in the first half of last year was RMB 3.818 billion, of which the online mall contributed RMB 1.909 billion, accounting for 50%.

(Ping An Health APP interface, screenshot from VCBeat)

In terms of drug supply, Ping An Health primarily collaborates with third-party pharmacies. As of June 30 last year, Ping An Health had partnered with 163,000 pharmacies, covering more than 25% of all pharmacies across China.

Yuanxin Technology primarily focuses on prescription drugs.The prospectus shows that its revenue for the first eight months of 2021 was RMB 3.612 billion. Of this, income from out-of-hospital comprehensive patient services (out-of-hospital pharmacies and out-of-hospital medical care) amounted to RMB 3.5371 billion, accounting for 97.9% of total revenue.

Unlike community pharmacies that primarily focus on over-the-counter (OTC) drugs and standard prescription medications,Approximately 83% of Yuanxin Technology's sales revenue comes from prescription drugs, most of which are not covered by the National Medical Insurance., which is the biggest differentiator between Yuanxin Technology and its competitors.

For example, as of August 31, 2021, Yuanxin Technology’s drug portfolio included 59 of the 78 innovative oncology therapeutics approved by the National Medical Products Administration (NMPA) since 2015, and its prescription drug inventory for cardiovascular diseases alone exceeded 1,600 items.

According to Frost & Sullivan, in terms of revenue in 2020, Yuanxin Technology was China’s largest comprehensive healthcare delivery platform focused on prescription drugs.

In terms of specific layout,Most of Yuanxin Technology’s pharmacies are strategically located near hospitals., thereby being closest to the prescription and the patient, and serving as a supplement to in-hospital treatment. In terms of coverage, Yuanxin Technology’s Yuanxin Pharmacy brand operates 251 pharmacies across 30 provinces and 91 cities in China (as of August 31 last year).

SiPi Health focuses on specialty drugs.From the perspective of its development history, Sipei Health initially laid out its strategy in the field of oncology big data, and later expanded into three major business segments: Physician Research Solutions (PRS), Pharmacy Benefit Management (PBM), and Provider and Payer Solutions (PPS). Among them,Pharmacy Benefit Management (PBM) is currently the largest revenue contributor.。

Since a significant portion of customers in the PBM business are cancer patients,SiPi Health primarily focuses on cancer patients who regard specialty drugs as life-saving medications.

According to the prospectus, Sipei Health reported revenue of RMB 2.7 billion in 2020, with PBM revenue amounting to RMB 2.48 billion, accounting for 91.8% of total revenue. As of June 30, 2021, Sipei Health operated 81 specialty drug pharmacies across 29 provincial-level administrative regions in China, excluding Tibet and Qinghai.Its business volume is equivalent to that of China's largest private specialty pharmacy.。

Medication alone is insufficient for the ongoing care of cancer patients; Si Pai Health has also implemented numerous initiatives across the service continuum. For instance, it established China’s first and only national platform for managing specialty medications, providing follow-up assessment services within a unified system.

In addition, SiPai’s 30 specialty pharmacies have obtained “dual-channel medical insurance accreditation” from local healthcare security administrations, enabling patients to seek reimbursement for medications that were previously reimbursable only when purchased at public hospitals. Furthermore, the company has established direct-billing arrangements with major insurers to provide patients with additional payment solutions.

Meanwhile, Zhiyun Health has been deeply engaged in the field of digital chronic disease management., currently, three major business lines have been established: in-hospital solutions, pharmacy solutions, and personal chronic disease management solutions.

The prospectus shows that Zhiyun Health’s revenue in 2020 was RMB 839 million. Of this, revenue from pharmacy solutions amounted to RMB 340 million, representing a year-on-year increase of 41.2%,Revenue from the supply of medical supplies to pharmacies amounted to RMB 330 million, representing its largest revenue source.。

As one of its core products, the Zhiyun Health Pharmacy SaaS system is designed to enhance operational efficiency and prescription rationality in pharmacies, delivering more professional and compliant 24/7 pharmaceutical care services to patients with chronic diseases through offline pharmacy channels. As of June last year, over 150,000 pharmacies across China had installed the Zhiyun Health Pharmacy SaaS system, representing a market penetration rate of 29%.In terms of the number of pharmacy installations and the number of patients served, Zhiyun Health has become China’s largest provider of pharmacy SaaS solutions.

From the perspective of revenue structure, digital marketing services driven by pharmaceutical company payments also showed significant growth: rapidly increasing from RMB 35 million in 2019 to RMB 149 million. This indirectly reflects the importance of digital marketing services within hospital settings and positions them as a new growth engine for Zhiyun Health’s future in-hospital solutions. Data shows that in 2020, “Zhiyun Health Pharmacy SaaS” was integrated with approximately 110,000 pharmacies across China, an increase of nearly 100,000 compared to 2019.

Therefore, in the context of health management and medical services, the integration of offline pharmacies has become mainstream. Companies are targeting specific populations—either starting from the payment side (insurance customers) or focusing on particular groups such as patients with chronic diseases or cancer—to implement refined operational strategies.

Moreover, judging by current market trends, such companies are actively building a closed-loop ecosystem integrating pharmaceuticals and insurance to connect the entire service chain, thereby enhancing user stickiness and medication adherence. However, this model is still in its nascent stage and requires further exploration.

Leveraging Digital Marketing as a Vehicle: Bridging Physicians and the General Public to Enhance Pharmaceutical Promotion Efficiency, with Digitalization and Operational Capabilities as the Core.

In the digital marketing sector, benchmark companies such as Baidu Health, DXY, and Medlive have already emerged. Since most of these companies (with the exception of Medlive) have not filed prospectuses, we primarily rely on publicly available information to analyze how each facilitates pharmaceutical marketing.

Medlive and DXY primarily acquire physician users by providing professional medical information and services, and then generate revenue by charging physicians subscription fees and offering digital marketing services to pharmaceutical companies. Therefore,Physician coverage, engagement, and retention are the core competitive advantages of such enterprises.

According to the prospectus, Medlive has approximately 3.5 million registered users, of whom about 2.4 million are licensed physicians, representing approximately 58% of all licensed physicians in China. According to Frost & Sullivan data, Medlive is the largest professional physician community in China. In the fourth quarter of 2020, Medlive’s average monthly active users (MAU) exceeded 1 million, with a monthly activity rate surpassing 28%, achieving a relatively high level of user engagement.

Leveraging the effective operation of its physician community, Medlive has expanded into the field of digital pharmaceutical marketing. According to its prospectus, pharmaceutical companies have consistently been Medlive’s largest payers, with its top five customers all being pharmaceutical firms.

In terms of monetization capability, Medlive ranked first among digital healthcare marketing service providers for physician platforms in China in 2020, with a market share of 21.4%. This was reflected in its revenue, which reached RMB 213.5 million in 2020.

Baidu Health, backed by Baidu, has established a content ecosystem centered on Baidu Health Medical Encyclopedia and a service ecosystem anchored by Baidu Health Ask-a-Doctor.

Baidu Health Medical Encyclopedia is an authoritative public welfare initiative for popularizing health knowledge, launched by Baidu Health. It collaborates with top-tier medical resources both in China and abroad to build an authoritative platform for medical and health science communication. Baidu Health Ask-a-Doctor is a 24/7 online consultation service platform introduced by Baidu Health.

Leveraging its accumulated expertise in content and services, Baidu Health joined forces with pharmaceutical giants GlaxoSmithKline (GSK) and AstraZeneca at the 2021 China International Import Expo (CIIE) to engage in in-depth collaboration in areas such as digital pharmaceutical marketing. Baidu Health partnered with GSK to launch precise disease science education initiatives, using herpes zoster prevention as a pilot program, and collaborated with AstraZeneca to establish a Chronic Disease Management Center, providing users with integrated online-to-offline chronic disease management services.

In other words, Baidu Health has introduced a new approach to digital marketing for pharmaceutical companies through its proprietary technology platform and its “content + services” model.

As can be seen, digital marketing-driven pharmaceutical sales primarily target B-end clients, testing companies’ digitalization and operational capabilities. In terms of revenue scale, digital marketing-based pharmaceutical marketing still lags behind both pharmaceutical e-commerce and health management and medical service scenarios.

In summary, the pharmaceutical e-commerce model is the most direct approach, characterized by a comprehensive range of drug products and extensive scenario coverage, with advantages in traffic acquisition and supply chain management. The health management and medical services model focuses on targeted populations, achieving deep operational engagement through the deployment of offline pharmacies and the integration of pharmaceuticals with insurance. The digital marketing model is more indirect, primarily targeting B-end clients to enhance the efficiency of pharmaceutical promotion.

It is not difficult to see that pharmaceutical marketing is indeed a critically important monetization strategy for current internet healthcare enterprises. However, this path is not one that any company can easily embark on at will, as it involves numerous factors of uncertainty.

First, the company requires substantial financing, as scaled growth demands significant capital.For internet healthcare companies, whether establishing offline pharmacies or building online platforms, the capital requirements often reach hundreds of millions.

Pharmaceutical sales is ultimately a scale-driven business. Only with sufficient volume can companies leverage economies of scale to negotiate better pricing and reduce costs, thereby offering more choices to end users, enhancing customer stickiness, and maintaining strategic flexibility to navigate industry changes.

Since 2013, the total financing volume of the entire internet healthcare industry has reached approximately RMB 200 billion. However, even with current development, few companies are profitable. If the industry’s overall profitability remains low, it will need to continue raising funds for financial support.

Second, the pharmaceutical marketing scenarios differ, posing distinct tests on core competencies.For example, DTP and O2O represent two entirely different operational models, each imposing distinct requirements on a company’s core competencies.

Specifically, DTP pharmacies focus on long-term operations, requiring them to provide patients with ongoing follow-up care and medical services; in contrast, O2O pharmacy sales prioritize speed and offer everyday, privacy-sensitive product selections. These are two fundamentally distinct business models.

Therefore, the success or failure of pharmaceutical O2O hinges primarily on service capability; without delivering exceptional service, the model is doomed to fail. Behind the “28-minute home delivery” promise offered by O2O enterprises lie persistently high costs associated with store operations, order fulfillment, and marketing promotion. In contrast, the core of DTP (Direct-to-Patient) pharmacies lies in the professionalism of their pharmaceutical care services. Given that specialty drugs are not ordinary medications, there are stringent requirements for building robust professional service capabilities, making the recruitment and training of specialized talent critical.

Third, the gross profit margin of pharmaceutical products is relatively low, making it difficult to translate revenue growth into profit growth.In the past two years, the internet healthcare sector has experienced a surge in IPOs. However, the financial data of many companies reveal characteristics such as low gross profit margins and high sales expenses. In particular, the gross profit margin for pharmaceuticals generally remains below 15%, diluting net profit margins and resulting in revenue growth without corresponding profit growth. This poses challenges to the sustainable development of these enterprises.

Generally, when companies experience revenue growth without corresponding profit growth, it is primarily attributable to two factors. First, increased R&D and administrative expenses; the capital invested in these areas can generate potential returns for the company’s future development, and the resulting decline in gross margin is only temporary. Second, expansion into businesses with lower gross margins, such as pharmaceutical sales, which falls into the latter category. This reduces the company’s risk resilience and exacerbates challenges during market downturns. Therefore, companies need to continue promoting scale economies, improving operational efficiency, and reducing fulfillment costs to continuously enhance their gross margin levels.

The internet healthcare sector has long been held in high regard by the industry. However, despite the influx of massive capital and rapid development to date, only the pharmaceutical marketing segment has achieved a viable business model within the internet healthcare space.

“From a medium- to long-term perspective,If internet healthcare companies wish to secure new revenue streams, they must subsequently develop targeted business initiatives aimed at payers such as upstream pharmaceutical manufacturers, basic medical insurance programs, patients, and commercial insurance providers.“A senior investor stated.”

The development of the industry also requires policy guidance and regulation. In late October 2021, the National Health Commission released the Detailed Rules for the Supervision of Internet-Based Diagnosis and Treatment (Draft for Comments). This policy clearly delineates the red lines between multiple relationships, such as those between medical services and pharmaceuticals, providing internet healthcare enterprises with a stronger policy basis for their business model exploration and user service delivery.

Notably, the release of the Detailed Rules,This signifies a higher barrier to entry for the industry and encourages innovative enterprises.For instance, the “Detailed Rules” implement digital oversight across the entire process of internet-based diagnosis and treatment, aiming to foster industry-wide development in China under a unified regulatory framework. This is undoubtedly beneficial for large-scale internet diagnosis and treatment platforms that boast robust technical infrastructure and mature operational capabilities.

In addition, the Detailed Rules set forth multiple requirements for the information technology platforms of internet hospitals. For instance, institutions providing internet-based diagnosis and treatment services must establish dedicated departments to manage medical quality, medical safety, pharmaceutical services, information technology, and other related operations. The Rules require that electronic medical record (EMR) data generated during internet-based diagnosis and treatment be shared with the EMR system of the affiliated physical medical institution, thereby achieving integrated online-offline quality control. Furthermore, the Rules mandate the implementation of cybersecurity measures and compliance with Level 3 or higher of the Multi-Level Protection Scheme (MLPS) for platform information security.

It is not difficult to find that,The industry’s future requirements for the digital capabilities of entities providing internet-based diagnosis and treatment services mean that possessing appropriate digital health infrastructure, along with related technical capabilities and operational management experience, will become a critical prerequisite for compliant operations.

For example, as major internet healthcare platforms continue to advance the accumulation of “physician resources” through specialized disease and specialty-focused platform models, the “internet hospital + medication purchase” model may become a primary revenue stream in the future.

For another example, driven by the maturation of both software and hardware, internet healthcare is gradually shifting from an information and connectivity platform to one grounded in “professionalism” and “clinical evidence-based practice,” directly engaging in critical aspects of disease treatment and boosting overall industry efficiency. This signifies that the value of internet healthcare will be further unlocked, with greater potential for revenue growth.

Looking ahead, the internet healthcare industry still has many hurdles to overcome. This requires every stakeholder to engage in continuous trial-and-error and exploration, thereby realizing the vision held at its inception.: Leveraging the power of digital technology, internet healthcare has broken through the barriers of public hospitals, enabling medical resources such as physicians, treatment plans, and pharmaceuticals to transcend geographical constraints and reach patients across diverse locations, thereby enhancing the overall efficiency of the healthcare and wellness industry.

This is the mission undertaken by the entire internet healthcare industry, and also the shared expectation of all people for technology to be universally accessible and serve the public.