The Capital Battle Behind a Counseling Session: Over $1.5 Billion Poured In Within a Year—Is the Mental Health Industry on the Verge of Explosion? | 2021 Annual Review

The mental health industry seems to have suddenly heated up.

According to the VCBeat database, since March 2021, a total of 14 companies in the mental health industry have completed 17 financing rounds, with the total amount exceeding RMB 1 billion (calculation rules: exchange rate conversion based on 1 USD = 6.37 RMB; amounts described as "tens of millions" are calculated as RMB 10 million; amounts described as "hundreds of millions" or "over 100 million" are calculated as RMB 100 million). Among them, Haixinqing, Zhaoyang Health, Jiandan Xinli, and Yidianling each secured single-round financing exceeding RMB 100 million, marking a significant departure from the industry’s previously lukewarm state.

Amid heavy capital investment, has the industry ushered in a window of opportunity? What are the emerging trends? In this article, VCBeat seeks to answer these questions by examining a series of events and changes in the field of mental health and psychological well-being in 2021.

I. Decades of Ordinariness, Gradually Heating Up

A mental health practitioner once noted that two decades ago, some experts believed the industry’s “spring” was imminent; yet ten years on, that spring remains distant.

Although this is largely just an inside joke about the industry’s development over the past few years, it also underscores the tortuous path forward for the mental health sector.

It appears that this is a forgotten industry.

Not so. China has been actively promoting the development of the mental health industry; although progress was slow in the early stages, it has been steady and robust.

The reason it is described as slow is that China did not officially promulgate the Mental Health Law until 2012, whereas countries with well-developed psychological services, such as the United States and the United Kingdom, passed their National Mental Health Act and Mental Health Act in 1946 and 1983, respectively. By comparison, China’s mental health sector had a relatively late start.

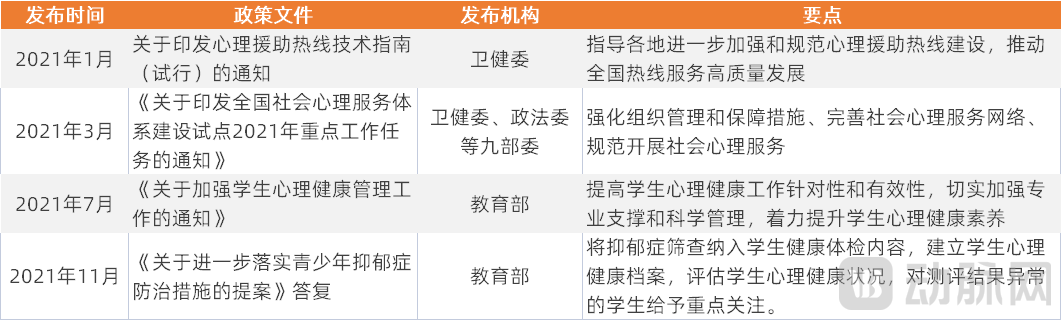

However, since 2015, China has seen a continuous stream of policies and guidelines related to mental health and psychology, with their content becoming increasingly detailed. Correspondingly, public awareness and understanding of mental health have been steadily improving.

In 2021, the issuance of policies such as the inclusion of psychotherapy in medical insurance coverage and the implementation of depression screening for students all constituted significant tailwinds for industry development. Furthermore, the Outline of the 14th Five-Year Plan for National Economic and Social Development and the Long-Range Objectives Through the Year 2035 explicitly called for improving the social psychological service system and crisis intervention mechanisms.

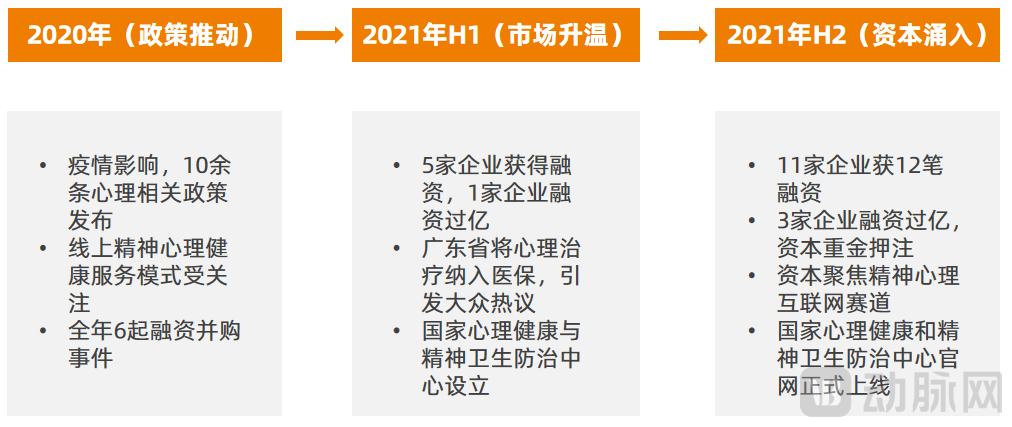

Driven by policy support, the capital market has responded swiftly, bringing the mental health and psychological well-being industry—long dormant for several years—back into the public spotlight. Compared with the number of financing and M&A transactions in 2020, the number of financing deals in the industry in 2021 not only more than doubled, but also occurred at later funding stages.

In fact, due to the impact of the epidemic at the beginning of 2020, public attention to the mental health industry reached an unprecedented height. According to incomplete statistics from VCBeat, there were more than 10 policies related to mental health in 2020, most of which were also related to the epidemic. Although only six financing and M&A transactions occurred in the industry that year, the favorable policies undoubtedly laid the foundation for subsequent heavy capital investment.

At that time, VCBeat conducted in-depth analyses of this sector on multiple occasions and posited that online mental health service platforms, diagnosis and treatment service enterprises, and technology-driven companies would be more favored by the market and capital in the industry’s future development. These insights were gradually validated by the market financing landscape in 2021.

Overview of Industry Events in 2020-2021

II. Continued Rise in Heat of the Internet Sector for Mental and Psychological Health

By examining the businesses of companies that secured successive rounds of financing in 2021, it becomes evident that nearly all of them focused on the online mental health sector. This trend is closely linked to both the inherent suitability of mental health conditions for digital care models and the scarcity of supply-side resources within the industry.

First, in terms of service content, conventional mental health services (such as psychological counseling and mental health education) generally place greater emphasis on the quality of communication between providers and clients, making them inherently well-suited for online delivery; this also applies to diagnostic and therapeutic services for psychiatric and psychological disorders.

Compared with other diseases, the diagnosis and treatment services for mental and psychological disorders rely less on physical equipment, with most current diagnostic and therapeutic devices serving primarily as adjunctive tools. Consequently, it is understandable that transitioning these services to an online model is feasible.

Secondly, from the perspective of service supply, the insufficient supply of medical resources has long been a perennial issue in China, which has provided room for growth for online platforms. This situation has also continued in the mental health industry.

Data show that China currently has approximately 40,000 psychiatrists and fewer than 100,000 licensed psychological counselors, while an estimated 16%–17% of the population suffers from various mental and psychological disorders. This highlights a significant imbalance between supply and demand in China’s mental health sector.

The emergence of online services has clearly been effective in improving this situation. As a result, both investors and market entrants have shown strong interest in the internet-based mental health sector, with frequent financing events. Companies such as Haixinqing and Yidianling, each with different business focuses, have also deeply engaged in this field. Building on previous online initiatives, they continue to explore the digitalization and intelligent enhancement of their services, with digital therapeutics being a typical example of such service models.

In simple terms, digital therapeutics leverage digital interventions to modify patients’ behaviors and lifestyles, thereby achieving therapeutic effects for mental and psychological disorders. Extensive clinical trials have demonstrated that digital therapeutics offer significant advantages in the personalized treatment of patients with mental and psychological conditions. Furthermore, from a feasibility standpoint, mental health represents one of the most accessible entry points for the application of digital therapeutics.

Among the companies that secured financing in 2021, Zheng’an Health and Lingxin Intelligence were focused on the research and development of digital therapeutics. Meanwhile, enterprises such as Zhaoyang Health and Yidianling also placed significant bets on this sector, attempting to develop digital therapeutics and digital diagnosis and treatment solutions through in-house R&D and collaborations with industry partners.

III. Strengthening Multi-Link Connectivity and Pursuing Full-Spectrum Layout to Identify New Growth Drivers

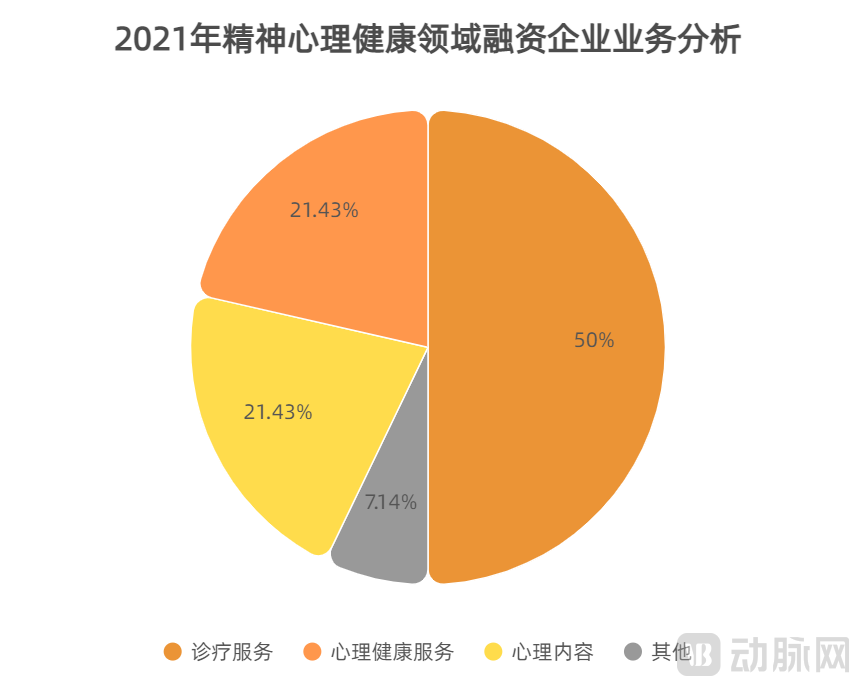

Mental health services can be broadly categorized by service type into three segments: diagnosis and treatment of mental disorders, professional psychological counseling services, and lightweight psychological content services (or general wellness psychology services). From the perspective of user base size, none of these three sectors constitutes a niche market, a fact corroborated by the financing landscape in 2021. An analysis of the business operations of more than ten companies that secured funding in 2021 reveals that representative enterprises in each respective domain successfully attracted investment. This demonstrates that the capital markets have shown substantial recognition for both lightweight psychological content and clinical diagnostic and therapeutic services.

However, the chart above also reveals that capital is currently more inclined toward enterprises focused on diagnostic and therapeutic services. This trend is largely driven by the high prevalence of mental and psychological disorders in China and the substantial size of the patient population. Taking depression as an example, data from the World Health Organization indicates that over 350 million people worldwide suffer from depression, with the number of patients increasing by approximately 18% over the past decade. Currently, China has a population of 180 million individuals experiencing depressive symptoms, among whom 95 million are diagnosed with depression.

Corresponding to the continuously growing patient population is an insufficient supply of medical resources, with market demand far from being met. Therefore, it is not difficult to understand why Zhaoyang Health and Haoxinqing, both focusing on diagnostic and treatment services, were able to secure over RMB 100 million in financing one after another in 2021.

Ideally, although the three major sub-sectors—diagnosis and treatment services for mental and psychological disorders, professional mental health services, and lightweight psychological content services—differ in their target audiences and service focuses, there should inherently be a relationship of continuity and overlap among them. Taking diagnostic and therapeutic services as an example, patients with mental and psychological disorders typically require appropriate psychotherapy and psychological counseling interventions alongside specialized medical treatment. This underscores the need for a holistic solution that spans from diagnosis and treatment to rehabilitation and subsequent reinforcement.

However, the reality is that close coordination across various fields has not yet become the norm; psychiatrists and psychological counselors often operate in silos, and a significant gap remains between clinical diagnosis and treatment services for mental and psychological disorders and routine mental health services.

To address this issue, many companies in the industry have made significant efforts and begun to continuously explore the integration of psychiatry and mental health services on the basis of their existing businesses, with the aim of providing users with one-stop services.

For example, Zhaoyang Health, which initially focused on moving psychiatric diagnosis and treatment services online, is now vigorously expanding its service chain and diversity to meet users’ multi-level needs, ranging from severe to mild conditions and from disease treatment to mental health services.

Meanwhile, Yidianling and Jiandan Xinli, which previously focused on mental health services, have also expanded their offerings into the diagnosis and treatment of psychiatric and psychological disorders, establishing online internet hospitals and opening offline clinics.

By achieving comprehensive coverage across the entire spectrum of mental health and psychological services, users benefit from more effective fulfillment of their individual needs and significantly improved accessibility to various services. Meanwhile, enterprises can continuously generate new growth drivers for their development through a complete strategic layout within this sector.

IV. Exploring the B2B Market, Focusing on the Construction of Social Psychological Service Systems

For a long time, the B2B market for mental health and psychological well-being (hereinafter referred to as the “B2B segment,” encompassing enterprise and education sectors) has remained like an underwater iceberg, largely overlooked by the public in contrast to the highly visible B2C market. However, driven by policy support, this segment has also experienced rapid growth over the past two years.

In November 2018, the National Health Commission and nine other ministries and commissions issued the Work Plan for Pilot Programs on the Construction of a National Social Psychological Service System. The plan required pilot regions to gradually establish a social psychological service system, build social service platforms, incorporate mental health services into the evaluation index system for Healthy Cities, and ultimately explore models and working mechanisms for social psychological services that could be promoted nationwide.

Over the following three years, multiple departments jointly launched new pilot initiatives for the construction of social psychological service systems each year, based on the implementation status of previous pilot tasks, to further advance and guide the standardized implementation of service system construction across various regions.

In November 2021, the Ministry of Education responded to the Chinese People’s Political Consultative Conference’s “Proposal on Further Implementing Prevention and Control Measures for Adolescent Depression,” explicitly incorporating depression screening into student health examinations, establishing mental health records for students, assessing their mental health status, and providing focused attention to students with abnormal assessment results.

Policy guidance has significantly increased the demand for mental health services among government and public institutions, educational entities, and enterprises, thereby creating substantial market growth opportunities. As a result, a growing number of mental health service providers are actively expanding their presence in the B2B sector.

Generally, for B2B clients, the services provided by enterprises mainly include supplying software and hardware products, establishing SaaS platforms for businesses, and directly providing psychological counseling and assessment services for psychological intervention.

It is reported that companies such as Yidianling and Jiandan Xinli, which previously focused more on the consumer (C-end) market, have begun to offer scaled business-to-business (B-end) services to enterprises. Notably, Yidianling’s approach involves building a SaaS platform for psychological services tailored to B-end clients, a model that enhances client engagement in the service delivery process.

While both Haixinqing and Zhaoyang Health offer SaaS platforms, their approaches differ slightly. Both companies provide SaaS services tailored to psychiatric hospitals and physicians, facilitating patient management through a B2B2C model. This model not only helps expand the business-to-business (B-end) market but also builds a bridge for companies to strengthen their presence in the consumer (C-end) market.

In fact, although China’s B2B market for mental health and psychological well-being has only come into public view in the past two years, numerous companies have long been establishing their presence in this sector. For example, Liuhe Xicheng, a company with state-owned equity participation, has focused since its inception on the B2B market for intelligent, digital psychological services. Addressing the mental health service needs of government agencies, enterprises, and other organizations, it leverages artificial intelligence to meet emerging psychological needs, extracts complex and multifaceted psychological signals from users, constructs holistic psychological profiles, and drives a shift among users from “passively seeking help after psychological issues arise” to “proactively managing mental health.” To date, it has segmented its services across four key populations—employees, primary and secondary school students, veterans, and domestic workers—serving approximately 3,000 institutional clients and reaching 6.3 million users.

Although the B2B market for mental health is not expected to experience explosive growth in the short term, this niche segment will gradually become a crucial component of the overall mental and psychological health market as efforts to strengthen the social psychological service system continue to intensify.

V. Technology Empowerment: Continuous Industry Renewal

Amidst the rapid and constant evolution of technology, service models in the healthcare industry are undergoing continuous transformation. Over the past two years, the integration of mental health care with intelligent technologies has been further strengthened. Along the path of tech-enabled services, a growing number of enterprises have achieved their respective breakthroughs.

For instance, in the VR + mental health sector, Xinjing Technology and Xuzhishi leverage technologies such as VR, big data, and AI to provide comprehensive VR digital therapeutic solutions for mental health rehabilitation training. Notably, the cognitive function rehabilitation system developed by Xuzhishi successfully obtained NMPA certification at the end of 2020, marking it as the first VR-based mental health rehabilitation training system approved by the NMPA in China.

In addition to VR-based mental health services, psychological service robots represent another key area of intensive development for industry players. Lianxin Technology, for instance, began in-depth R&D into digital and intelligent applications for psychological services as early as 2018, launching its AI-powered mental health service robot, “Lian Xiaoxin.”

Unlike robots in other medical subfields, psychological service robots focus more on semantic recognition and language interaction. Therefore, innovation in this product requires continuous breakthroughs in big data, AI technology, and algorithms as support.

Nowadays, with the iteration of technology and the accumulation of data, psychological service robots have become more intelligent in semantic understanding and interaction, and their functional coverage has become more comprehensive. Whether it is front-end prevention and diagnosis, or mid-to-back-end intervention and treatment, all can be implemented through the platform of psychological service robots.

VI. How Will It Develop in the Future?

Driven by policies and diverse market demands, an increasing number of innovative mental health service solutions are entering the market, with capital markets maintaining a positive outlook. What development trends will the industry exhibit in the future?

First, standardization. Although the industry is currently viewed favorably by multiple stakeholders, it still faces the challenge of a lack of standardized mental health services. This not only hinders the stable development of the sector but also creates certain difficulties in achieving inclusive and scalable service delivery.

In response to this issue, numerous industry players are continuously promoting the standardization of the sector by regulating their own practices and establishing corresponding service systems. Furthermore, the 14th Five-Year Plan explicitly calls for the improvement of the social psychological service system. In light of this, the industry is inevitably poised to develop in directions that enhance the accessibility, inclusiveness, and scalability of mental health services—all of which clearly require standardized services as a critical foundation.

Against this backdrop, once the industry truly clears the hurdle of standardization, it will usher in a genuine golden age of development.

Second, the integration of technology with mental health services will be further strengthened. Industry insiders believe that the convergence of AI, big data, and smart hardware with mental health services can help—and even partially replace—certain aspects of service delivery in the future. This not only effectively meets user demand but also promotes the professionalization and standardization of these services.

Third, online and digital service models will continue to be a key focus of capital investment in the future. The core of this service model lies in addressing the imbalance between medical resources and patient demand. On this basis, digital intervention solutions, such as digital therapeutics, will increasingly enter the market.

2021 was an extraordinary year for the mental health industry, and we will wait and see whether the industry can continue the existing trends in 2022.