Surgical Robots Emerge as the Hottest MedTech Segment in 2021: $7.5B IPO and $4.3B in Funding Highlight Sector Boom

Which medical device sector was the hottest in 2021? The answer is undoubtedly surgical robots.

In 2021, the surgical robotics industry delivered an impressive performance in response to prior market skepticism about its value. Affirmation from the capital markets exceeded earlier expectations, with surgical robots demonstrating through tangible results that this sector was not overvalued.

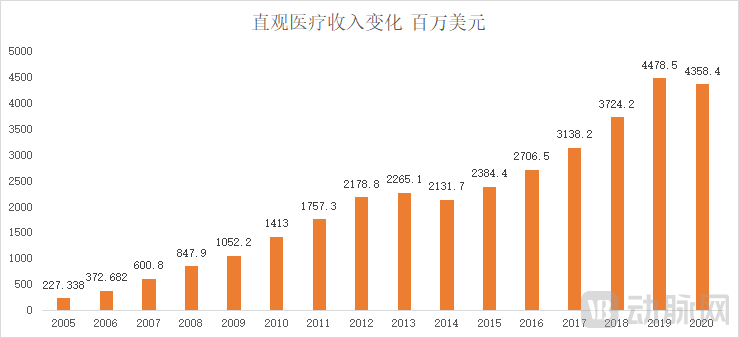

In the secondary market, surgical robots achieved the highest-market-cap IPO in the medical device industry in 2021.: MicroPort MedBot. Although MicroPort MedBot is a spin-off subsidiary of MicroPort Scientific, its market capitalization has surpassed that of its parent company, once exceeding RMB 60 billion. Across the ocean, Intuitive Surgical has continued its growth legend, with a market capitalization exceeding USD 120 billion and a post-IPO gain of more than 175-fold.

In the primary market, the surgical robotics sector has remained the hottest track in the medical device industry for two consecutive years, leading in both the number of financing deals and the total amount raised.In China, more than 10 companies have secured financing exceeding RMB 100 million each, with four individual deals surpassing RMB 500 million. The total financing amount across the entire sector has exceeded RMB 3 billion. Laparoscopic surgical robots, orthopedic surgical robots, and vascular interventional surgical robots are all flourishing.

Major Financing Events for Surgical Robots in China in 2021

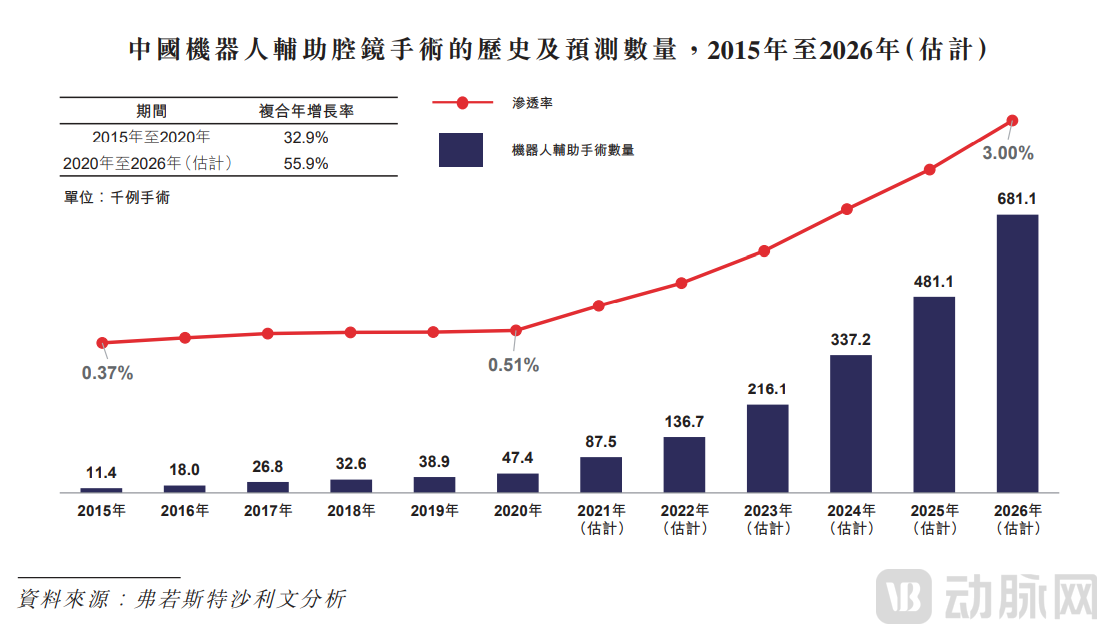

In clinical practice, the installed base and surgical volume of surgical robots are growing rapidly.Globally, more than 6,500 da Vinci surgical robots have been installed, assisting in over 10 million procedures. In China, the total installed base of da Vinci surgical robots exceeds 260 units, with nearly 300,000 surgeries performed, marking a rapid growth in surgical volume.

In terms of commercialization, Chinese companies have taken a significant step toward regulatory approval. Weigao has secured approval for China’s first domestically produced laparoscopic surgical robot. Additionally, several other domestically made surgical robots are currently in the clinical trial phase. In the laparoscopic segment, MicroPort’s Toumai surgical robot, Jingfeng Medical’s MP surgical system, and Kangduo’s laparoscopic surgical robot have all completed patient enrollment for clinical trials. In the orthopedic segment, joint replacement robots from Yuanhua Intelligence, Jianjia, and MicroPort Robotics have also entered the clinical trial stage.

"Building on existing achievements, domestically produced surgical robots have reached the stage of facing large-scale clinical application."

What Is the Value of Surgical Robots from the Physician’s Perspective? To better reflect clinical needs, VCBeat conducted interviews with physicians in orthopedics and laparoscopy in China for its year-end review, examining the development of domestic laparoscopic and orthopedic surgical robots from the physician’s perspective.

For a long time, laparoscopic surgical robots in China were synonymous with the da Vinci Surgical System, as it was previously the only laparoscopic surgical robot approved for use in the country.

In the past, although the da Vinci Surgical System had been in the Chinese market for more than five years, surgical volume did not experience significant growth. The primary reason was that its high initial cost limited the size of the domestic market.

A da Vinci robotic surgery costs approximately RMB 40,000 more than traditional laparoscopic surgery. The high cost of the da Vinci system is primarily driven by equipment procurement expenses, with purchase prices ranging from RMB 20 million to RMB 30 million. Based on an eight-year depreciation schedule, the annual depreciation expense amounts to approximately RMB 3 million. Secondly, maintenance costs are significant, with annual maintenance fees for the da Vinci surgical robot exceeding RMB 1.5 million. Another major expense involves specialized consumables, which include both single-use and multi-use (up to 10 uses) specialized items. Single-use specialized consumables for the surgical robot cost USD 533 per set (including arm covers, camera arm covers, monitor covers, and trocar seal caps), while multi-use specialized instruments cost USD 400–1,000 per use and can be reused up to ten times. On average, the combined cost of multi-use specialized instruments and single-use specialized consumables per procedure is approximately RMB 30,000. Overall, the total cost per procedure performed using the da Vinci surgical robot amounts to RMB 44,000.

The high price once limited most hospitals from purchasing the da Vinci surgical robot.However, changes in surgical volume over the past two years and market feedback demonstrate that Chinese hospitals have great enthusiasm for surgical robots and are willing to pay for innovative products.

A representative from Fosun Intuitive stated that, as of the third quarter of 2021, more than 55 da Vinci surgical robot systems had been installed in China that year, with over 65,000 procedures performed. This figure has already surpassed the full-year total of 47,000 procedures recorded in 2020. In terms of cumulative numbers, more than 260 da Vinci surgical robot systems have been installed in China, and nearly 270,000 procedures have been completed.

Domestic physicians also hold the da Vinci Surgical System in high regard, with many expressing their desire for their respective hospitals to acquire the system.

A chief physician in the Department of Urology told VCBeat, “The greatest value of the da Vinci Surgical System lies in freeing surgeons’ hands and reducing fatigue. Furthermore, it expands the scope of surgical procedures; in urological surgeries, the robotic system achieves deeper access to the operative field. The robotic arms can maneuver flexibly, performing actions such as rotation, translation, articulation, and firm grasping with greater dexterity than human hands. Equipped with stabilizers, the robotic arms prevent tremors that may occur with manual operation, thereby avoiding accidental injury to nerves and blood vessels caused by hand tremors during surgery.”

The value of da Vinci surgical robot-assisted procedures is widely recognized, but why has it only begun to experience rapid growth in the past two years?

Before experiencing explosive growth, the da Vinci surgical robot underwent a prolonged period of market education.An industry insider stated, “The da Vinci Surgical System was approved for market launch in the United States in 2000. It took a considerable amount of time to promote it among medical professionals, and only after a prolonged period of market cultivation did surgical volumes achieve rapid growth. The same holds true in China. In recent years, the da Vinci Surgical System has been focused on training Chinese surgeons, helping them become accustomed to robotic surgical techniques. Through repeated simulations and trials, it has gained physicians’ recognition of the safety and efficacy of robotic surgery.”

The development trajectory of the da Vinci Surgical System demonstrates to latecomers that only through prior periods of arduous perseverance can subsequent explosive growth be achieved; the large-scale adoption of surgical robots is by no means an overnight accomplishment.

The growth of the da Vinci Surgical System in recent years has also been driven by its inclusion in medical insurance coverage and the relaxation of procurement permit regulations.

The liberalization of medical insurance coverage has significantly reduced the financial burden on patients. In April 2021, Shanghai included certain robot-assisted laparoscopic procedures—namely partial nephrectomy, radical prostatectomy, total hysterectomy, and pelvic autologous preservation—in its list of reimbursable surgeries, covering 80% of the medical costs. The scope of reimbursement may be expanded in the future based on patient demand and the adequacy of medical insurance funds. Under Shanghai’s policy, patients’ out-of-pocket expense ratio is only 20%.

It is expected that more cities will include surgical robots in their medical insurance coverage in the future. According to the 14th Five-Year Plan for the Development of the Medical Equipment Industry, issued by the Ministry of Industry and Information Technology in February 2021, local governments are encouraged to include robot-assisted surgeries within the scope of medical insurance reimbursement.

The issuance of allocation permits is also being gradually liberalized,Surgical robots are expensive and require substantial capital investment. As large-scale medical equipment, their procurement by hospitals requires a configuration permit. The Catalogue for the Configuration Management of Large-Scale Medical Equipment is divided into Class A and Class B. Applications for the configuration of Class A large-scale medical equipment shall be submitted to the National Health Commission, while applications for Class B equipment shall be submitted to the provincial-level health administrative authorities where the applicant is located.

In 2018, surgical robots were reclassified from Class A to Class B large-scale medical equipment, lowering the configuration threshold and significantly relaxing limits on the number of units allowed. According to the "Notice of the National Health Commission on Adjusting the Configuration Plan for Large-Scale Medical Equipment for 2018–2020" issued by the National Health Commission, a total of 225 laparoscopic surgical robots were planned to be sold to medical institutions in China between 2018 and 2020.

Patients’ acceptance of surgical robots is also gradually increasing.Minimally Invasive Surgery Replacing Open Surgery as the TrendIn China, open surgery remains the most common surgical approach; however, it is limited by the depth of incision access, resulting in prolonged patient recovery times and significant blood loss. Traditional laparoscopic minimally invasive surgery involves small incisions but lacks robotic assistance, which can impair surgeons’ hand-eye coordination. Because the shafts of traditional laparoscopic instruments pivot around the entry port, the distal movement of the instrument tips is opposite to the direction of the surgeon’s hand movements. Consequently, surgeons must adjust their hand-eye coordination to accommodate this counterintuitive operation. Additionally, traditional laparoscopic surgery is associated with hand tremors and limited degrees of freedom for the instruments.

Compared with open surgery and laparoscopic minimally invasive surgery, surgical robots demonstrate superior capability in performing complex procedures; they offer greater stability in surgical outcomes, as well as higher operational precision and flexibility; additionally, they result in smaller incisions and shorter recovery times, thereby reducing blood loss and complications.

Taking radical prostatectomy as a representative procedure, this surgery is performed in a very narrow and deep operative field, making it unavoidable for open surgery and laparoscopic radical prostatectomy to cause damage to adjacent healthy tissues and nerves. The high precision of surgical robots allows for better performance of radical prostatectomy; currently, more than 80% of radical prostatectomies in the United States are performed using the da Vinci Surgical System.

Although the introduction of robot-assisted laparoscopic surgery in China occurred later than in the United States, its adoption is increasingly widespread in China, primarily driven by the growing prioritization of minimally invasive techniques and their unique advantages in treating conditions such as early-stage prostate cancer.

As robotic laparoscopic surgery experiences explosive growth, the number of market participants is also increasing. Currently, there are four domestically developed laparoscopic surgical robots in China undergoing clinical trials, with market launch expected in the near future.

Major Domestic Laparoscopic Surgical Robot Products

The logic behind domestically produced laparoscopic surgical robots entering the market is low-cost import substitution. However, some physicians have expressed concerns about the stability of domestic surgical robot products. The surgical robotics industry demands high precision; although domestic manufacturers emphasize differentiated performance, product stability is, in fact, more critical.

Undoubtedly, the demand for laparoscopic surgical robots in the Chinese market is clear. After a prolonged period of market cultivation, domestically produced laparoscopic surgical robots have finally reached a tipping point of rapid growth. By the end of 2020, Intuitive Surgical had installed 3,720 da Vinci systems in the United States; by comparison, the Chinese market still holds substantial room for expansion.

Five years ago, the challenges for the da Vinci Surgical Robot in entering the Chinese market were restricted allocation permits and a prolonged market cultivation period. Today, although the restrictions on allocation permits have been lifted, the core challenge for domestic companies is to demonstrate clinical performance comparable to that of the da Vinci Surgical Robot.

The orthopedic surgical robotics segment has witnessed the highest number of financing events among all surgical robotics sectors. This trend is associated with the implementation of centralized volume-based procurement (VBP) for artificial orthopedic joints in 2021. Some investors believe that as the gross profit margins of traditional high-value orthopedic consumables decline, orthopedic surgical robotic systems will emerge as new high-value products.

With the implementation of centralized procurement, traditional orthopedic consumables manufacturers and surgical robot developers have flocked to the orthopedic surgical robotics sector, resulting in a number of domestic participants in this field that is no smaller than that in the laparoscopic surgical robotics market.

In 2021, the most significant change in the field of orthopedic surgical robots was a more rational market perception, with the market updating its understanding of two key aspects of orthopedic surgical robots.

First, some people previously believed that the commercialization of orthopedic surgical robots had cooled down, and that orthopedic surgical robots represented a fabricated demand.However, the commercialization of different types of orthopedic surgical robots has been uneven. The commercial performance of trauma and spine orthopedic surgical robots has fallen short of expectations, while joint surgery robots have demonstrated remarkable commercial success.

The representative of joint surgery robots is Stryker's Mako surgical robot, whose sales and surgical volumes far outpace those of other orthopedic surgical robots.VCBeat has compiled an overview of the global commercialization status of orthopedic surgical robots. According to data from Stryker’s official website, over 1,000 Mako Systems had been installed worldwide by 2021, with more than 500,000 procedures performed to date. These figures far exceed those of any other type of orthopedic surgical robot globally, which explains why joint replacement surgical robots are the most prominent segment within the orthopedic robotics field and have attracted the largest number of companies.

Why Are Orthopedic Surgical Robots Experiencing a Tale of Two Extremes? Joint Surgery Robots Are Booming, While Trauma and Spine Robots Face a Cold Reception.

In terms of the problems addressed, the osteotomy issues resolved by joint surgical robots are more practical than the screw placement issues addressed in spinal and trauma surgeries.

"An industry insider stated, 'Spine and trauma surgical robots can only address the issue of screw placement. For surgeons, mastering screw placement skills is not a challenge. Furthermore, existing trauma/spine surgical robots still exhibit certain mechanical errors and involve relatively complex operations. These factors have resulted in low utilization rates of spine/trauma surgical robots in hospitals.'"

“Knee osteotomy generally involves cutting bone across six planes, with the robotic arm participating throughout the entire process. This workload actually accounts for 60% of the total effort in joint replacement surgery, and joint surgical robots help surgeons undertake a significant portion of this work. This is why joint surgical robots are more popular.”

The second major market insight concerns technological barriers. While some argue that the orthopedic surgical robotics sector is crowded with low entry barriers and severe product homogenization, the reality is that while the barrier to entry is low, the threshold for achieving excellence is exceptionally high.

Indeed, the entry barrier for orthopedic surgical robots is not high, particularly for those used in trauma and spine surgeries; however, the entry barrier for joint-related orthopedic surgical robots is relatively higher.

Even in the field of articulated robots, which has high entry barriers, there are varying levels of technical difficulty across different technological approaches. Mako is an active orthopedic surgical robot, while Rosa is a collaborative robot; from a technical perspective, active surgical robots entail greater complexity.

An orthopedic surgeon told VCBeat, “There is substantial demand among orthopedic surgeons for intelligent solutions in orthopedic surgery. However, existing orthopedic surgical robots are still in their early stages, with considerable room for product improvement. Currently, some functionalities of orthopedic surgical robots are similar to those of navigation software. Navigation products have been available in China for over two decades, and most hospitals that could afford them have already made purchases. If orthopedic surgical robots only improve operational precision without being able to participate throughout the entire surgical procedure, their potential impact will be limited.”

The surge in surgical robotics continues to spread. Beyond laparoscopic and orthopedic surgical robots, companies have already embarked on the research and development of robotic systems for vascular intervention, pulmonary intervention, and TAVR procedures.

In the field of vascular interventional surgical robots, Siemens Healthineers was previously the sole participant; however, in 2021, multiple manufacturers of high-value vascular consumables recognized the potential of this sector and began to establish their presence.

Current vascular interventional surgical robots are primarily designed for coronary interventions and generally consist of robotic arms and a control console, allowing physicians to guide catheters through patients’ blood vessels. With the assistance of these robotic systems, physicians can avoid radiation exposure.

Companies in China with a presence in the vascular intervention sector

Natural orifice surgical robots are also a hotly contested sector. These robots are applied in natural orifice endoscopic surgeries, such as bronchoscopy (lung examination), colonoscopy (intestinal examination), and gastroscopy (stomach examination). Natural orifice surgical robots provide a clearer view of the target area, enabling surgeons to manipulate instruments with greater dexterity.

There are only three FDA-approved natural orifice surgical robots worldwide, including the Ion bronchial robot developed by Intuitive Surgical, the Monarch bronchial robot developed by Johnson & Johnson, and the Flex gastrointestinal robot developed by MedRobotics.

Pulmonary interventional surgical robots have garnered favorable outlooks from Intuitive Surgical and Johnson & Johnson. Intuitive Surgical developed Ion, a robotic system for pulmonary interventional diagnostic procedures, which received FDA approval in 2019 and has been installed in over 90 units across the United States to date.

In terms of domestic enterprises, MicroPort MedBot has also proactively laid out its presence in the field of pulmonary intervention.

Final Thoughts

It is foreseeable that R&D and design capabilities for surgical robots will become the core technological competency of domestic medical device companies.

The surgical robotics sector has attracted a multitude of players. However, the more heated the market becomes, the greater the need for sober reflection—particularly in a field like surgical robotics, where many unknown issues have yet to surface.

Surgical robots are entering a golden age of development, but alongside the industry’s fervor, signs of overcrowded competition are emerging. Drawing on the trajectory of the da Vinci Surgical System, surgical robot products can only achieve substantial clinical adoption through precision mechanical design, superior clinical outcomes, and prolonged market cultivation. Within China’s medical device industry, there is no shortage of products that were overly hyped prior to launch but subsequently encountered lukewarm commercial reception.

The development of China’s surgical robotics industry must directly confront its challenges and difficulties. By tackling the most arduous tasks, the easier ones will be resolved effortlessly and correctly; by addressing weaknesses, strengths will naturally flourish without additional effort. We believe that by choosing to tackle the most difficult challenges from the outset, all subsequent endeavors will become simpler.