Why Is a Healthcare IT Company Worth $28.3 Billion? The Cerner Corporation Story

Philips Healthcare

Integrated service provider in healthcare, quality living, and lighting fields

Recently, Oracle announced the acquisition of U.S. healthcare IT company Cerner Corporation. The acquisition agreement was ultimately executed at a price of $95 per share, with Cerner selling itself for a staggering $28.3 billion (approximately RMB 180.3 billion).

This can be hailed as the century’s most significant acquisition in the healthcare sector. On both sides of the deal, one is the world's largest software vendor, and the other is an epic enterprise in the field of U.S. healthcare IT.

In rigid sectors such as healthcare IT, market share is one of the most critical indicators, capable of delivering sustained value to enterprises. In April 2021, Microsoft acquired Nuance Communications, a voice and image AI company, for $16 billion. Oracle, which also places significant emphasis on life sciences, naturally followed suit; its nearly $30 billion investment secured a vast base of hospital clients and a diverse portfolio of clinical information systems.

However, compared to Oracle’s yet-to-begin adventure, Cerner’s valuation is far more captivating.

A Comparison of the Operational Performance of Domestic Medical IT Enterprises,The revenue of leading listed companies is typically in the range of RMB 1 billion, which pales in comparison to Cerner’s staggering RMB 30 billion in annual income.So, can China give rise to a healthcare IT giant like Cerner? What insights can Cerner’s development journey offer for the growth of China’s domestic healthcare IT sector?

Cerner was founded in 1979. It entered the healthcare sector through laboratory informatics and later primarily provided EMR-related equipment and hardware to hospitals.

Cerner’s journey has been remarkably smooth. In 1986, it listed on the NASDAQ with $17 million in revenue. However, over the following decade, Cerner’s performance was lackluster, with its stock price showing virtually no fluctuation.

Between 2000 and 2005, investors reassessed Cerner’s value, driving its stock price up by approximately 500%. Over a 15-year period, Cerner capitalized on the surge in EHR development, with its customer base growing from 250 in 1990 to 5,000 in 2005.

In February 2009, President Obama signed the American Recovery and Reinvestment Act (ARRA), which included the HITECH Act (Health Information Technology for Economic and Clinical Health Act). The HITECH Act earmarked over $20 billion to promote the adoption of health information technology nationwide, aiming to reduce healthcare expenditures through informatization. Coupled with the “Medicare and Medicaid EHR Incentive Program,” which mandated financial incentives for physicians and hospitals adopting electronic health records (EHRs) and penalties for those failing to do so, Cerner seized another significant growth opportunity.

Cerner's Stock Price Changes Since 1997 (Data Source: Futu NiuNiu)

When the federal legislation was first enacted, Cerner served a total of 2,300 hospitals. By 2013, as the foundational build-out of electronic health records (EHR) systems neared completion, its hospital client base had exceeded 3,000. During the same period, with approximately 5,000 hospitals in the United States, Cerner captured a significant share of the market from Epic, reaching a market capitalization of $15 billion.

Subsequently, direct collaborations with government entities became a new pillar of Cerner’s electronic health record (EHR) business. In 2015, the U.S. Department of Defense signed a $9 billion EHR contract with Cerner, Leidos, and Accenture, under which Cerner was responsible for modernizing the EHR systems across military hospitals, propelling Cerner to the peak of its market valuation.

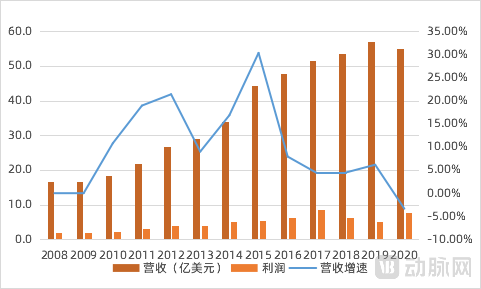

2016 marked a critical turning point. With a limited total customer base, the ceiling for the standalone electronic medical record (EMR) market became clearly visible. As the U.S. healthcare IT infrastructure market was fully carved up by four companies—Cerner, Epic, Allscripts, and MEDITECH—with the top four collectively accounting for over 85% of the market share (Cerner ranked second in 2020), revenue growth across these enterprises slowed significantly. Under this pressure, they were compelled to seek new growth drivers.

Changes in Net Profit and Revenue, 2008–2020: The Turning Point Began in 2016 (Data Source: Compiled from Cerner’s Annual Prospectuses)

To break out of its niche, Cerner chose three directions.

As one of the largest healthcare IT vendors in the United States, Cerner’s capture of more than 20% of the EHR market share signifies its efficient distribution channels and extensive experience in medical data processing. Consequently, transitioning from hospital IT infrastructure to clinical IT systems became Cerner’s primary strategic focus. After the turn of the millennium, it launched a series of clinical decision support and quality control products tailored to specialty-specific needs, driving the U.S. healthcare industry from a reactive to a proactive approach in IT adoption.

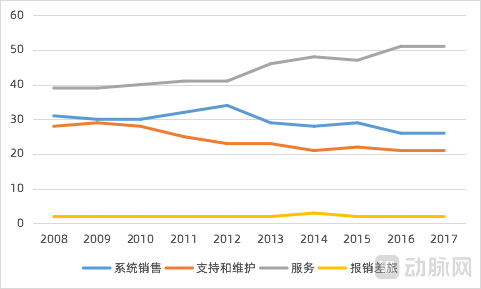

Clinical Specialty Solutions and Big Data Solutions (On-Premises) are Cerner’s key focus areas for expanding new business within hospitals. An analysis of the changes in the proportion of each business segment from 2008 to 2017 shows that the share of Cerner’s services segment continued to rise, while the share of maintenance and support declined gradually.

Analyzed in two time periods: From 2008 to 2012, the electronic medical record (EMR) market experienced a construction boom supported by policies, and sales of Cerner systems began to grow.If other conditions remain unchanged, the support and maintenance segment, which should trend in line with system sales, would be expected to change accordingly; however, the actual outcome contradicts expectations, with the proportion of support and maintenance decreasing rather than increasing.The most likely cause of this change isThe growth in clinical specialty solutions within the System Sales segment and the growth in big data solutions (in-hospital) within the Services segment have generated additional revenue for the enterprise, but have not immediately produced corresponding maintenance income.This is for Cerner's business transformationKey Points.

Percentage Change in Cerner’s Business Segments, 2008–2017 (Data Source: Compiled from Cerner’s Annual Prospectuses)

After the completion of primary electronic health record (EHR) implementation in the United States in 2013, Cerner’s system sales experienced significant fluctuations. Since then, big data solutions (both within and outside hospitals) have gradually become the main driver of Cerner’s incremental revenue growth, exceeding 50% by 2017. During this period, Cerner actively expanded its B-to-B big data applications, seekingPharmacies, pharmaceutical companies, emergency centers, government agencies, etc.By assuming the role of a new payer, Cerner is pursuing its second strategic avenue to break through existing growth ceilings.

Within Cerner’s business framework, clinical solutions are comprised of two main pillars. The first encompasses specialized domains such as intensive care, device management, emergency medicine, and pharmacy, with a core focus on leveraging data to build models that optimize departmental operational efficiency. The second targets specific clinical departments—including radiology, oncology, pediatrics, and cardiology—aiming to assist physicians in auxiliary diagnosis through artificial intelligence and other technologies, thereby addressing gaps in quality control.

Cerner’s Comprehensive Business Layout (Data Source: Compiled and Organized by VCBeat Based on Official Website Data)

Cerner’s Comprehensive Business Layout (Data Source: Compiled and Organized by VCBeat Based on Official Website Data)

Out-of-hospital business operations comprise two segments: real-world data solutions and population health management, targeting physicians/pharmaceutical companies and government entities, respectively. This aligns with the current focus of big data research among enterprises in China. The key difference is that domestic companies are smaller in scale; delivering these two service areas typically requires collaboration between at least one medical big data company and one public health informatics company.

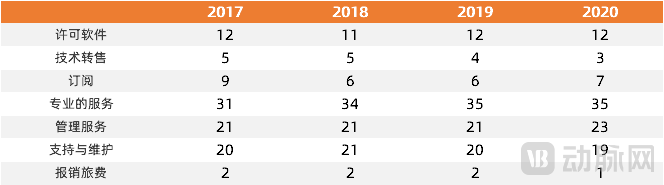

The leap in both directions has continued to the present. Starting in 2017, Cerner’s financial report business segmentation changed from four categories to seven, with professional services revenue showing growth, while the proportion of subscription revenue declined slightly.This also demonstrates the decisive role of clinical specialty solutions and big data solutions in Cerner’s development, accounting for half of its market capitalization.

Percentage of Revenue by Business Segment for Cerner, 2017–2020 (Data Source: Compiled from Cerner’s Annual Prospectuses)

Returning to Cerner’s core business, EHR, this is a market with clearly visible limits. With 5,000 hospitals in the United States, the maximum potential customer base for Cerner’s EHR business is capped at 5,000. For such a system characterized by deep stickiness, it is extremely difficult to capture competitors’ market share once the market has been segmented. Therefore,Building a commercial empire with a market capitalization of 100 billion yuan does not require crossing oceans, but finding a new foothold worth another 100 billion yuan does., Cerner, Epic, Allscripts, and even every major player in healthcare IT must expand overseas.

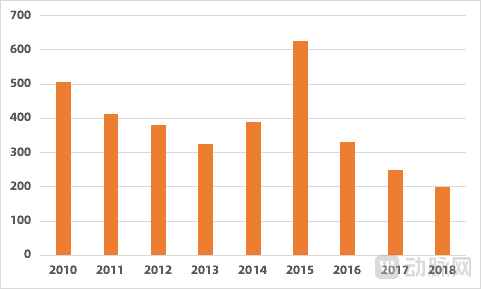

U.S. EMR Equipment Procurement Volume (Data Source: China Business Industry Research Institute)

Cerner is among the first wave of U.S. healthcare IT companies to expand overseas. According to HIT data, the top six regions for Cerner’s international business in 2020 were the Middle East, the UK and Ireland, Oceania, Canada, the DACH region, and Spain, with its geographic coverage expanding year by year. Furthermore, Cerner is the only company with a market share exceeding 10% in the EMEA (Europe, the Middle East, and Africa) region.

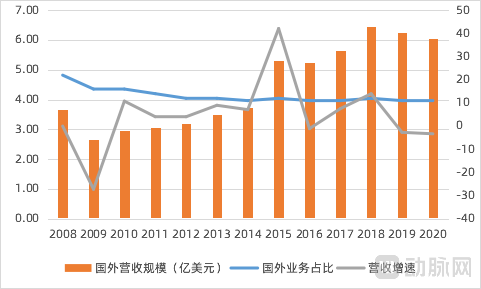

EHR vendors typically enter new countries through two primary approaches: partnering with local enterprises to localize their proprietary solutions, or acquiring local EHR suppliers to directly gain market share using the suppliers’ existing EHR systems. During its expansion, Cerner did not favor any single model, yet it failed to achieve notable results over more than a decade of development. Between 2008 and 2020, Cerner’s overseas business as a proportion of total revenue declined from 22% in 2008 to 11% in 2020, with little change in absolute terms.

Cerner’s Revenue Changes from 2008 to 2021 (Data Source: Compiled from Cerner’s Annual Prospectuses)

Over more than a decade of overseas expansion, Cerner’s M&A strategy has become increasingly aggressive. In 2014, Cerner embarked on its largest and most well-known acquisition, spending $1.3 billion to acquire Siemens’ Health Information Technology division.

This may not have been a cost-effective deal. As shown in the chart above, although Cerner’s revenue surged in 2015 thanks to the inclusion of Siemens’ financial statements, the overall revenue growth rate of the company declined after the acquisition, even turning negative. This indicates that no significant synergies emerged between the acquired business and the original operations.

Behind the predicament lies the fiercely competitive landscape of the German EMR market, where Cerner’s cross-border business expansion has struggled to gain traction. Moreover, native EMR systems exhibit strong user stickiness; once physicians become accustomed to them, switching becomes inconvenient. To this day, Cerner has failed to migrate all of Siemens’ German clients to its own Millennium platform.

In 2020, the outbreak of the COVID-19 pandemic further hindered international travel for medical IT companies, leaving them with few alternatives. According to the EHR report released by Signify Research, the United States accounts for two-thirds of global EHR sales volume. However, over the next five years, the U.S. is projected to become one of the regions with the slowest growth in the EHR market. Consequently, EHR vendors must devise more effective strategies to identify new growth engines in overseas markets, which are characterized by high fragmentation and limited investment.

Returning to the initial question: Can China give rise to a healthcare IT giant akin to Cerner? As of now,The answer is likely no.。

Numerous factors have contributed to this outcome; scale, awareness, product morphology, and product form have constrained the ability of domestic medical IT enterprises to “grow bigger and stronger.”

First is the scale. In 2020, the U.S. healthcare IT market size was conservatively estimated at approximately RMB 720 billion, while China’s healthcare IT market size was around RMB 200 billion (data from AskCI Consulting), indicating a significant gap in market scale. On the other hand, China’s healthcare informatization market is highly fragmented, with different enterprises adopting varying technical standards. While establishing their own competitive barriers, these companies have also created data silos, making the integration of China’s healthcare IT market considerably more challenging.

Next is cognition. The original intention of introducing EHR in the United States was to optimize the efficiency of medical data use to improve hospital efficiency and reduce medical insurance expenditures, a purpose jointly recognized by the government and hospitals. In contrast,The promotion of the domestic medical IT market is largely government-led, with hospitals adopting a passive role; many hospitals have yet to develop an awareness of leveraging informatization to improve operational efficiency and optimize expenditures.

Next is the product form. Since the United States completed its basic healthcare informatization infrastructure around 2012, subsequent business development has focused on providing application-oriented solutions based on medical data for hospitals, insurance institutions, and pharmaceutical companies, thereby opening up a larger market for healthcare IT enterprises. In contrast, the revenue of leading domestic healthcare IT companies in China primarily relies on multimillion-yuan large-scale contracts for public health initiatives and comprehensive hospital construction projects. During the construction phase,Application-oriented products, such as data analytics solutions, are typically bundled within them, leading to a certain degree of undervaluation of this component.。

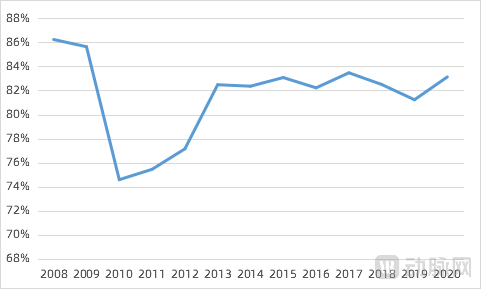

Finally, there is the product format. Judging from Cerner’s business composition, cloud platform-based services account for half of its revenue, even providing managed services for the information management of some hospitals. Under this model, the productLow deployment costs and easy maintenance result in a high gross profit margin.. As the data shows, Cerner’s gross margin stabilized at the 80% level after its business shifted toward the application end.

Cerner’s Gross Margin Trends (2008–2021) (Data Source: Compiled from Cerner’s annual prospectuses)

In contrast, domestic hospitals in China tend to favor on-premise installations, keeping data within the hospital premises, which results in relatively higher costs. The gross profit margins of listed companies generally range from 30% to 50%, with only specialized healthcare IT firms like Medical System Technology Co., Ltd. (Meditech) achieving gross profit margins as high as 70%. Meanwhile, the domestic medical IT market is divided into “general-purpose” and “customized” approaches. While the customized approach provides better services to hospitals, it also somewhat reduces gross profit margins.

Four factors have contributed to the informatization gap between China and the United States, offering significant insights for the next phase of development in China’s healthcare IT sector.

First: Following the completion of infrastructure development, application deployment is the inevitable direction for the growth of healthcare IT. As the construction of informational infrastructure, such as hospital electronic medical records (EMR) and interoperability systems, draws to a close, optimizing clinical workflows through data will become the central theme of healthcare IT initiatives. During this process, the focus of medical system construction will shift toward smart hospital applications, enterprise-wide EMR systems will transition into specialty-specific EMR systems, and intelligence will gradually permeate every aspect of healthcare services.

Second: Expanding into new domestic markets and exploring new business tracks is far more advantageous than going overseas. As evidenced by Cerner’s international expansion, adapting to local policies and launching differentiated competitive products is extremely challenging; neither acquisitions nor in-house R&D have proven effective in gaining market traction. Moreover, Chinese companies are currently unable to replicate Cerner’s high-margin operational model. Consequently, few enterprises are currently attempting overseas expansion, and establishing a viable path for such endeavors will require considerable time and accumulation of experience.

Third: The fragmented market will gradually consolidate. For leading listed medical IT companies, a larger market share means easier promotion of new products and higher standardization, which in turn leads to higher gross profit margins.Economies of scale are enabling leading enterprises to expand their dominance, inevitably squeezing the survival space of small and medium-sized enterprises.

Furthermore, although leading listed medical IT companies currently focus on infrastructure development while emerging medical IT firms concentrate on intelligent application development, in the long run, listed medical IT companies that establish foundational infrastructure can more easily build platform ecosystems, thereby hindering the market deployment of products from emerging medical IT companies. These various advantages are driving medical IT enterprises to capture a larger share of the infrastructure market.

Overall, China and the United States have developed along two distinct paths of informatization, yet both are pursuing industrial integration and the specialization of information infrastructure.

In July 2021, Winning Health extended an olive branch for a merger to B-Soft. Although the final negotiations broke down, this move brought into the open the previously covert merger intentions of healthcare IT companies. In fact, several medical IT firms signaled the possibility of mergers in 2021, with concrete actions likely to materialize over the following two years.

From the current perspective, industry consolidation may better promote the standardization of healthcare informatization and accelerate interoperability. However, it is more likely that the global healthcare IT industry will converge toward a common path to achieve greater scale effects.