Private Hospitals Face a Tale of Two Extremes: Over 600 Closures vs. 10 IPOs — Pathways to Survival and Growth

At the end of 2021, Guangzhou Nanyang Cancer Hospital, once one of the most renowned specialized oncology hospitals in Asia, declared bankruptcy.

Notably, this is not the first private hospital to declare bankruptcy. Shandong Xinhua Medical, Liupanshui Liangdu Hospital, and Sichuan Muchuan Traditional Chinese Medicine Hospital have also successively declared bankruptcy.

Private healthcare, having weathered the “cold winter” of the pandemic, now appears to be entering a tale of two extremes: some players are going public while others are filing for bankruptcy.

While numerous private hospitals have declared bankruptcy, others such as Hygeia Healthcare and Hongli Medical have successfully listed on stock exchanges. Sanbo Brain Hospital has passed the regulatory review, with its listing imminent. Meanwhile, several leading medical institutions, including Lu Daopei Medical Group, Shulan Healthcare, and Wuhan Asia Heart Hospital, have begun preparations to list on China’s A-share market.

(Data Source: Compiled from public media reports)

Compared with public medical institutions supported by fiscal funds, private medical institutions face greater operational pressures and cash flow constraints.

As the public healthcare system extends its reach downward and high-quality medical resources become increasingly accessible at the grassroots level, small and medium-sized private hospitals that lack specialized medical services or strong physician support will find their survival space increasingly squeezed.Such competitive pressure is not due to a small market, but rather because healthcare service capabilities fail to keep pace with development demands and cannot effectively complement public hospitals. As a result, these entities struggle to achieve market and capital competitiveness, hinder further growth, and may even face elimination.

Under such industry conditions, what path have private hospitals taken? By examining the development of successful cases such as Sanbo Brain Hospital, Longcheng Hospital, and Wuhan Asia Heart Hospital, we may gain some insights.

According to relevant data from Tianyancha, a total of 347 private hospitals were deregistered in 2019, and this figure surged to 685 in 2020.

(Data source: compiled from public media reports)

(Data source: compiled from public media reports)

The underlying cause may be related to a broken capital chain.

According to a previous report by Securities Daily, analysts have stated that tight capital chains are the key factor putting most private medical institutions to a life-or-death test.

Unlike public hospitals, private medical institutions operate more like restaurants, generating cash flow only when they are open to patients. During the pandemic, some private medical facilities were unable to operate normally, leading to tight cash flows and forcing their operators to seek buyers or financial support.

In stark contrast to the urgent financing needs of private hospital operators, investors remain cautious.

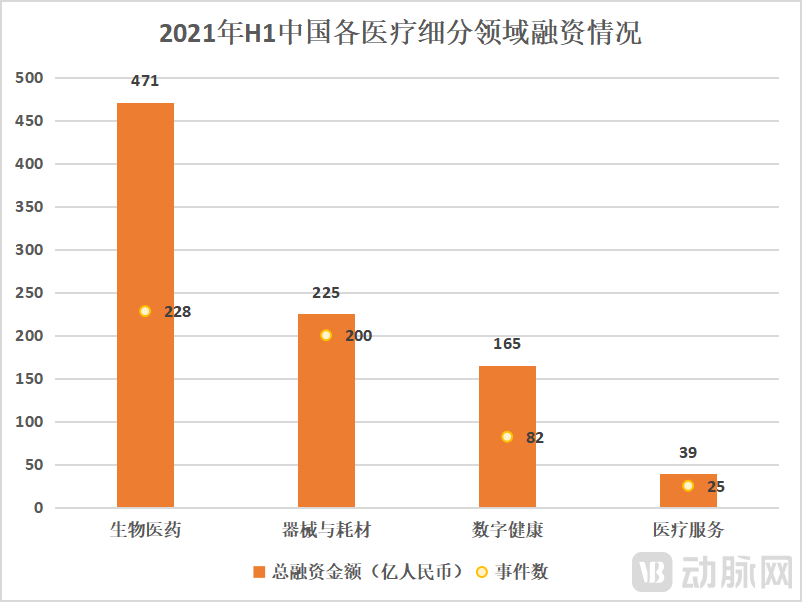

According to the "Global Healthcare Investment and Financing Report for H1 2021" released by VCBeat, China's biomedical sector topped the list with 228 transactions totaling RMB 47.1 billion, followed closely by the medical devices and consumables sector with 200 transactions, while digital health ranked third.Medical services ranked fourth with 25 transactions and a total financing amount of RMB 3.9 billion, slightly higher than pharmaceutical commerce.

(Data source: Arterial Orange)

(Data source: Arterial Orange)

It is worth noting that although private hospitals constitute a major component of the healthcare services industry, they represent only a part of it; therefore, their share of investment and financing data is relatively smaller.There is a significant gap between the number of financing events and the amount of capital raised by private hospitals and those in hot sectors such as biopharmaceuticals and digital health.

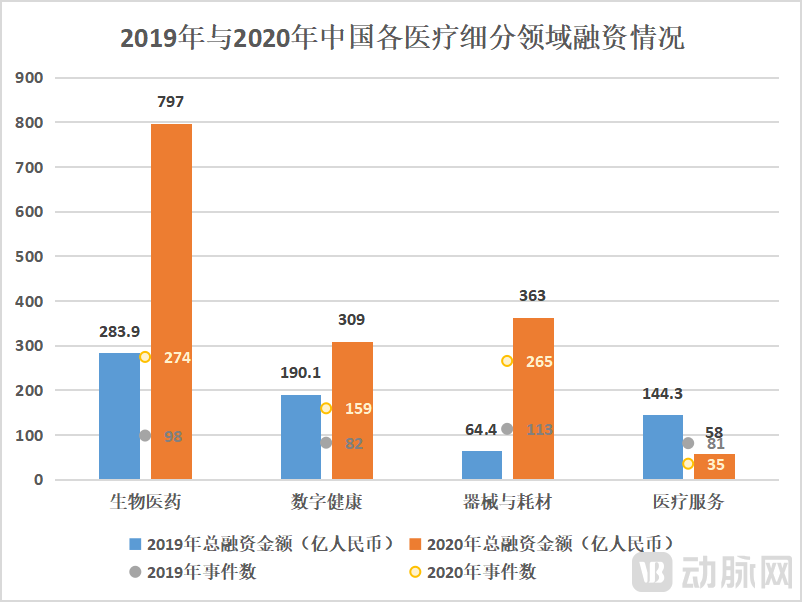

This trend is not solely attributable to the pandemic. According to VCBeat’s investment and financing reports for 2019 and 2020, China’s healthcare services sector ranked third in 2019 with RMB 14.43 billion raised across 81 financing deals. By 2020, however, investment enthusiasm in this sector had declined sharply compared with 2019, with total financing amounting to RMB 5.8 billion across only 35 deals.

(Data source: Artery Orange)

(Data source: Artery Orange)

This is driven by profound historical factors and the inherent characteristics of the industry, as well as by the dominance of public healthcare, the difficulties in attracting top-tier physicians to private hospitals, insufficient credibility of private medical institutions, and a complex and ever-changing social regulatory landscape.

Healthcare providers today can be categorized into three types: public hospitals operated by the government, hospitals run by large state-owned enterprises or state-owned assets, and hospitals established by private individuals or private enterprises.

Public hospitals have served as the cornerstone of China’s healthcare system for decades, holding an irreplaceable monopolistic position in the medical market. Despite policy restrictions on their expansion, they have continued to exhibit significant growth momentum.As the state promotes the modern hospital management system, future reforms in public hospitals across medical care, management, operations, and services will divert a portion of patient volume from private hospitals, while also attracting some patient flow.

The latter two categories consist largely of new entrants to the healthcare market. The earlier entrants were collectively owned hospitals established by large state-owned enterprises, public institutions, or universities, such as university infirmaries and numerous hospitals under the aerospace industry system. In recent years, medical institutions invested by state-owned capital, represented by China Resources, CITIC, Peking University Healthcare, and Sunshine Insurance, have emerged.

Private capital or foreign investment entered the healthcare industry in its early stages through private groups such as the Putian network; subsequently, private pharmaceutical companies and enterprises from other sectors, such as real estate, became involved in the healthcare industry, including Fosun, Taikang, and even Wanda and Evergrande; a small number were medical projects or hospitals established by foreign investors, such as United Family Healthcare in Shanghai, Raffles Medical in Chongqing, and Park Regis in Chengdu.

Overall, the latter two are both in relatively difficult situations.ExhaustedWhile China’s policy support for privately-run healthcare has remained consistent, the state has always positioned such providers as a supplement to public hospitals. Policies have been continuously rolled out to foster the development of private hospitals, encouraging them to deliver multi-tiered, differentiated, and specialized medical services.While private hospitals have surpassed public hospitals in number, most still lag significantly behind their public counterparts in terms of patient volume, quality of care, medical revenue, talent, technology, equipment, capital, and brand reputation. The pressures of operations and cash flow compel many private hospitals to focus on short-term survival, leaving them unable to make long-term strategic plans and layouts.

However, as the public healthcare system extends its reach downward and high-quality medical resources become increasingly accessible at the primary care level, small and medium-sized private hospitals lacking distinctive medical services or strong physician support will see their operational space further squeezed. Such institutions will struggle to maintain market and capital competitiveness, hindering further development and potentially leading to elimination, thereby creating a vicious cycle. With insufficient internal revenue-generating capacity, these hospitals have almost no resilience when confronted with “black swan” events such as the pandemic, making business suspensions, closures, and bankruptcies unsurprising.

On the other side of the wave of bankruptcies, numerous private hospitals have been successively listing or preparing to list on stock exchanges.From an internal perspective, the self-sustaining capabilities of private hospitals—encompassing talent, management, technology, equipment, service, and brand—constitute both their “moat” and their “stepping stone.”。This can be gleaned from the development of successful private hospitals such as Sanbo Brain Hospital, Longcheng Hospital, Wuhan Asia Heart Hospital, and Hygeia Healthcare.

On September 15, according to disclosures by the Shenzhen Stock Exchange, Sanbo Brain Hospital Management Group passed the Listing Committee meeting, bringing its initial public offering closer to realization.

Sanbo Brain Hospital’s successful breakthrough is inextricably linked to its “medical-educational-research” system. In addressing the issue of physician talent, Sanbo Brain Hospital adheres to an integrated strategy of “medicine, education, and research,” namely “Bo Yi (extensive medical practice), Bo Jiao (comprehensive teaching), and Bo Yan (in-depth research),” which also gives rise to the name “Sanbo.”

Specifically,Sanbo Brain Hospital has successfully expanded its presence in regions such as Yunnan, Chongqing, and Fujian through self-establishment, joint ventures, and restructuring, leveraging the technical expertise, talent pipeline, management capabilities, and service experience of its flagship campus, Beijing Sanbo (now a hospital directly affiliated with Capital Medical University).

Within this “medical care, education, and research” framework, Sanbo Brain Hospital has resolved challenges that plague many private hospitals, such as scientific research, teaching, and professional title promotion. The prospectus reveals that more than 75% of clinical physicians at Beijing Sanbo hold a master’s degree or higher, a performance metric that is also excellent compared to the public hospital system.

At the special session on medical devices held during the “High-Quality Development of Private Healthcare (Salon)” hosted by the National Multidisciplinary Medical Collaboration Cloud Platform,Professor Wang Baoguo, Party Secretary and Vice President of Sanbo Brain Hospital, Capital Medical University, stated that, leveraging Sanbo Brain Hospital’s integrated “medical care, teaching, and research” system, the institution maintains a stable talent pool and is capable of training master’s and doctoral students as a strategic talent reserve.

According to a report by Kaiyuan Securities, the key factors that public hospital physicians consider when evaluating private hospitals primarily include: compensation and benefits incentives, talent development systems, hands-on clinical opportunities, research capabilities, promotion mechanisms, and available resources (including training, technology, and equipment).

A comparison with leading large-scale private medical institutions in China reveals that while most of the aforementioned elements are commonly present across these organizations, each institution also exhibits innovative models. For instance, Topchoice Medical’s team-based patient consultation model and Sinopharm Xinbang Pharmaceutical’s chief expert responsibility system provide younger physicians with greater hands-on clinical opportunities, while Jinxin Fertility’s Medical Quality Control and Research Development Committee helps enhance its research capabilities.

Based on the 2021 semi-annual report, private medical institutions have accelerated the recruitment of high-quality physicians by leveraging their aforementioned advantages in physician acquisition.Taking Hygeia Healthcare as an example, the company recruited 844 new medical professionals in the first half of 2021, representing a 33% year-over-year increase compared to the end of 2020. Among these new hires, 128 were chief and associate chief physicians, marking a 43% year-over-year increase from the end of 2020, thereby significantly expanding its high-quality medical team. Jinxin Fertility introduced four renowned experts in the first half of 2021; their extensive clinical experience has strengthened Jinxin Fertility’s medical service capabilities and competitiveness.

In addition to recruiting high-caliber physicians, private healthcare institutions are also accelerating the process of talent development.For instance, Hygeia Healthcare cultivates interdisciplinary talent through its Teaching and Research Institute, while Aier Eye Hospital established the Aier Optometry Industry College and signed a “Cooperative Agreement on Joint Postdoctoral Talent Development” with the Institute of Computing Technology, Chinese Academy of Sciences, to expand its future talent reserve.

Amid the broader healthcare reform landscape, the marketization of physicians is gaining momentum. Private hospitals are striving to refine their mechanisms for talent acquisition, management, training, and promotion. The ability to attract and retain top talent is the key to sustainable long-term development.

Clear positioning and a focus on specialization and distinctive services constitute another key condition for the development of private hospitals. Some investors believe that opportunities for comprehensive private hospitals are now scarce. This underscores the critical importance for private hospitals to accurately define their strategic positioning.

The source revealed that current investments in private hospitals are primarily driven by the large size of the private healthcare market, its low penetration rate, and rapid growth. The core investment thesis rests on four pillars: first, establishing differentiation from public medical institutions or offering superior infrastructure; second, strong independence of specialized departments with low reliance on inter-departmental consultations; third, high standardization and replicability, which facilitate chain expansion, lead to increased market concentration, and offer strong growth potential; and fourth, the ability to extend along the value chain to upstream and downstream departments—for example, assisted reproductive technology institutions can expand into obstetrics and pediatrics.。

Shenzhen Longcheng Hospital, after 18 years of development, has grown from a Tier-1 hospital with a daily outpatient volume of only 200 visits into a large-scale, fully equipped Tier-3 Grade-A specialized rehabilitation hospital in Shenzhen.

This achievement is primarily attributable to Shenzhen Longcheng Hospital’s strategic decision in 2006 to specialize in rehabilitative medicine. At the conference, Zhang Zhiling, Vice President of Shenzhen Longcheng Hospital and the Rehabilitation Medical Consortium Center, shared insights into the hospital’s strategic positioning.

Dean Zhang Zhiling stated,The positioning of Longcheng Hospital was primarily established based on the practical insights of Wang Yulin, President of Shenzhen Longcheng Hospital. At that time, only a few Grade 3A hospitals in Shenzhen had rehabilitation departments, and their bed capacity was extremely limited. While there was substantial demand for rehabilitation services among the general population, the availability of such medical services provided by hospitals was severely inadequate.Meanwhile, looking at the situation from a broader perspective, both national policies and the development trends in rehabilitation medicine clearly indicate that this sector represents a promising area of opportunity.

““To a certain extent, choice is more important than effort. Our differentiated development strategy relative to public hospitals has directly enabled us to stand out in Shenzhen and Guangdong Province,” stated President Zhang Zhiling.

Similarly, Sanbo Brain Hospital has a highly precise positioning, specializing in neurology. According to reports, Sanbo Brain Hospital ranks among the top in China for the cumulative volume of neurosurgical procedures, with 80% being Level 4 surgeries—the most complex category. Its technical expertise is leading nationwide. In 2011, its neurosurgery department was among the first batch in Beijing to be designated as a National Key Clinical Specialty by the former Ministry of Health, alongside those of Tiantan Hospital and Xuanwu Hospital. It successfully retained this designation after reassessment in 2017.

Wuhan Asia Heart Hospital has long been dedicated to technical research in the field of cardiac care and has now developed into a Grade 3A specialized heart hospital with 750 open beds and an annual surgical volume exceeding 29,000 cases. By the end of 2020, the hospital had successfully performed more than 357,000 various types of cardiac surgeries.

Hygeia Healthcare focuses on oncology care. Public information shows that Hygeia Healthcare operates and manages a network of 10 hospitals, with oncology as the core specialty, across seven cities. In 2020, Hygeia Healthcare was listed on the Hong Kong Stock Exchange with an IPO price of HK$18.5 per share; it opened at HK$22.8, and its stock price has risen steadily since listing.

The development of specialized departments has become a crucial pathway for private hospitals to establish differentiated competition and complement public hospitals.

National policies also indicate that private hospitals or non-public medical institutions are an indispensable complement to China’s healthcare services.

On September 29, 2021, the General Office of the State Council issued the “14th Five-Year Plan for National Healthcare Security,” a key programmatic document outlining healthcare insurance priorities for the coming years. The plan specifies that by 2025, inpatient expenses reimbursed under Diagnosis-Related Groups (DRG) and per-disease payment models are expected to account for 70% of total inpatient costs.

CITIC Securities’ report points out that in recent years, the state has introduced multiple policies to accelerate the implementation of Diagnosis-Related Groups (DRGs). It is expected that the rollout of DRGs will drive adjustments on the supply side of public healthcare (such as shifting preoperative and postoperative examinations from inpatient to outpatient settings) and promote the development of outpatient services (which are not subject to DRG controls). Consequently, demand for differentiated medical services is likely to accelerate its shift toward high-quality private hospitals.

Regarding how to establish one’s strategic positioning, experts offer the following recommendations: First, identify your target patient population and develop precise patient personas. Second, consider what health issues these populations need addressed and what challenges they may encounter. Third, assess whether the services provided by the hospital can meet their needs, alleviate their suffering, and help them overcome these difficulties. Fourth, evaluate whether the hospital holds a unique position within its service area; if not, determine which strategies should be employed to enhance competitiveness. Throughout this process, it is also essential to monitor industry development trends and stay aligned with policy directions.

As essential tools in healthcare delivery, medical devices serve as a key indicator for evaluating hospitals. Effective management of these devices not only reflects a hospital’s administrative capabilities but is also an imperative requirement for enhancing the quality of its medical services. At the conference, Dr. Zhang Zhiling, President of Longcheng Hospital, shared insights and recommendations on medical device management at Longcheng Hospital.

At the conference, President Zhang Zhiling highlighted three major pain points in medical device management for private hospitals.First, the procurement process prioritizes low prices, leading to inadequate follow-up maintenance and support.

Private hospitals differ from public hospitals in their positioning of medical devices. Private hospitals tend to prioritize meeting basic clinical needs, developing specialized services, and ensuring cost-effectiveness with high quality at affordable prices. This orientation makes private hospitals more sensitive to return on investment (ROI). They commonly employ multi-vendor price comparisons and have actual controllers engage directly in negotiations to suppress costs. As a result, bids for post-warranty maintenance services are often low, leading to inadequate manufacturer response and even compelling hospitals to handle equipment maintenance independently.

Second, high physician turnover and frequent equipment replacement have led to severe waste.Different experts have varying requirements for equipment brands and models. Coupled with the high turnover rate of physicians in private hospitals, this leads to excessively frequent equipment replacement, resulting in unnecessary financial waste. It also necessitates frequent user training, which often gives rise to avoidable friction with equipment manufacturers.

Third, there is a lack of systematic management philosophy, and regular equipment maintenance is not performed in a timely manner.In many small medical institutions, functions such as information technology, equipment management, and procurement are consolidated into a single department. These institutions rely primarily on manufacturers for maintenance and lack dedicated personnel, resulting in disorganized equipment maintenance logs. This often leads to irregular and untimely maintenance, posing significant safety hazards. Conversely, while larger institutions with dedicated staff and departments exist, they rarely utilize information systems for scientific management.

Addressing Pain Points, President Zhang Zhiling Proposes Four Solutions.Regarding equipment procurement pricing, Zhang Zhiling recommended strengthening communication among private healthcare institutions, with associations organizing volume-based procurement to reduce costs, enabling manufacturers to adopt a strategy of small profits and quick returns.

In terms of equipment maintenance, Zhang Zhiling recommends engaging third-party service providers to address the issue., organized by the Equipment Management Branch, through member nominations and expert evaluations, recommend third-party equipment maintenance providers with strong capabilities and high proficiency to undertake maintenance services for various devices. Manufacturers may also participate to address the shortage of specialized engineers.

Regarding equipment upgrade training,First, hospitals or association branches shall upload training materials provided by manufacturers and experts to online platforms, enabling staff to complete training directly online upon job rotation; personnel who fail to meet competency standards are not permitted to assume their posts. Second, emphasis shall be placed on employee handover processes, with checklists and precautionary reminders established to mitigate risks associated with equipment use. Third, regular exchanges and training sessions shall be conducted in collaboration with manufacturers.

In the management of device consumables using information systems, with designated personnel assigned, procure a cost-effective equipment and consumables management system. First, promptly monitor the current status of equipment; second, timely perform maintenance, repair, and decommissioning of various medical devices and instruments; third, maintain clear records of consumables inventory, including procurement, sales, and stock levels.

In recent years, the state and government have provided policy support at the macro level, lowered entry barriers, and improved the environment for private healthcare provision. However, deep-seated issues at the micro level of hospitals—such as how to attract patients, retain talent, enhance technical capabilities, improve service delivery, and promote sustainable development—cannot be easily resolved merely by introducing policies. Instead, investors in private healthcare, hospital administrators, and healthcare professionals need to work together, drawing on practical experience, to explore solutions step by step.

At the conference, Professor Wang Baoguo also remarked with emotion, “The voice of private hospitals has been growing in recent years. Whether it is applying for national research projects or accessing medical and academic platforms, the situation has improved significantly compared to the past. The influence of private hospitals is continuously increasing, and national policies actively encourage non-public medical institutions and social organizations to participate in certain national scientific research projects.” Active participation by private hospitals in national research projects and diligent implementation of national policies are important measures to enhance the influence of socially run healthcare institutions.

President Zhang Zhiling also stated that private hospitals should actively offer advice and suggestions, participating in government medical services.Taking Longcheng Hospital as an example, through proactive policy recommendations, the hospital collaborated with the government to pioneer an expert appraisal model for work-related injury rehabilitation. Additionally, in terms of medical insurance reimbursement, Longcheng Hospital secured substantial government support through its advisory contributions.

Even during the pandemic, a period marked by significant fundraising challenges, Sanbo Brain Hospital successfully completed over RMB 800 million in Series B equity financing, making it one of the largest transactions in the healthcare services sector in recent years.

Moreover, in previous media reports, Zhang Yang, Chairman of Sanbo Brain Hospital, revealed that even without this round of financing, Sanbo Brain Hospital would still be able to pay its employees’ salaries for two to three years, even if it ceased all operations and all its affiliated hospitals were shut down.

As disclosed in the prospectus, Sanbo Brain Hospital Group Co., Ltd. recorded operating revenues of RMB 800 million, RMB 940 million, and RMB 1.02 billion from 2017 to 2019, respectively, reflecting steady growth in operational performance. In 2020, despite the impact of the COVID-19 pandemic, the company still achieved an operating revenue of RMB 990 million.

Hospital management is a systematic engineering endeavor. In their development, private hospitals must not only focus on primary factors but also pay attention to secondary ones, while placing greater emphasis on the interconnections among these factors. Each hospital possesses its own unique characteristics; only by fully understanding the opportunities and challenges it faces can a hospital chart a course suited to its specific needs, drawing from self-reflection, the experiences of others, and advanced management theories.In general, for private hospitals, the optimal strategy is to focus on internal development by strengthening their self-sustaining capabilities and enhancing their resilience to pressure; only by becoming stronger first can they achieve larger scale.