Why These Three Niche Women's Health Startups Secured Major Funding Amid IPO Filings

In late 2021, the first players specializing in breast health entered China’s internet hospital sector, as Zhenru Network and Hanwei Intelligent Medical successively announced the launch of their internet hospitals, adding a new piece to the puzzle of the women’s health market.

In 2015, the State Council successively issued the “Guiding Opinions on Actively Promoting the ‘Internet Plus’ Action” and the “Guiding Opinions on Advancing the Construction of a Tiered Diagnosis and Treatment System,” both of which proposed the development of internet-based healthcare services. As a result, internet hospitals in China have gradually proliferated across the country. Currently, China’s internet healthcare industry is dominated by general practice internet hospitals and pharmaceutical e-commerce platforms, while specialized internet hospitals remain a minority. In the niche market focused on women’s health, although entities such as WeDoctor Beilian, Guohui Investment Holding Group, and Meiyou have established internet hospitals specializing in obstetrics, gynecology, and pediatrics—alongside some public maternal and child health hospitals or healthcare institutions—internet medical services dedicated exclusively to women’s health have not yet achieved scale.

Women face many unique health issues, including menstrual cycles, pregnancy, contraception, and menopause. According to the World Health Organization (WHO), breast cancer and cervical cancer are the two most common cancers in women; one-third of health problems among women aged 15 to 44 are caused by sexual and reproductive health issues; approximately 830 women worldwide die every day from complications related to pregnancy or childbirth, and most of these deaths are preventable if high-quality care is accessible during pregnancy, delivery, and the postpartum period. In addition, some conditions are more prevalent in women; for instance, women are more prone than men to anxiety, depression, and other mental health disorders, particularly during pregnancy and after childbirth.

In the white paper “Equality, Development, and Sharing: The Development and Progress of Women’s Undertakings in the 70 Years of New China,” released by the State Council in 2019, the health of women and children is described as the “cornerstone of national health.” China has more than 688 million women, accounting for 48.7% of the total population. They play increasingly multifaceted roles in social and economic activities—as professionals, mothers, and primary caregivers for household chores and elderly care. Women’s health is of significant importance to individuals, families, and society alike.

As social and economic status improves, women are placing increasing emphasis on their own health. According to the "2020 White Paper on Chinese Women's Health" jointly released by Mob Research Institute and Meiyou, women are the primary users of health-related apps, accounting for nearly 60%. Furthermore, the user base for mobile apps focused on women's physiological health has been growing year by year, reaching 250 million in April 2020.

What are the current development trends in the women’s health market, and how much capital attention is it attracting? VCBeat offers the following observations.

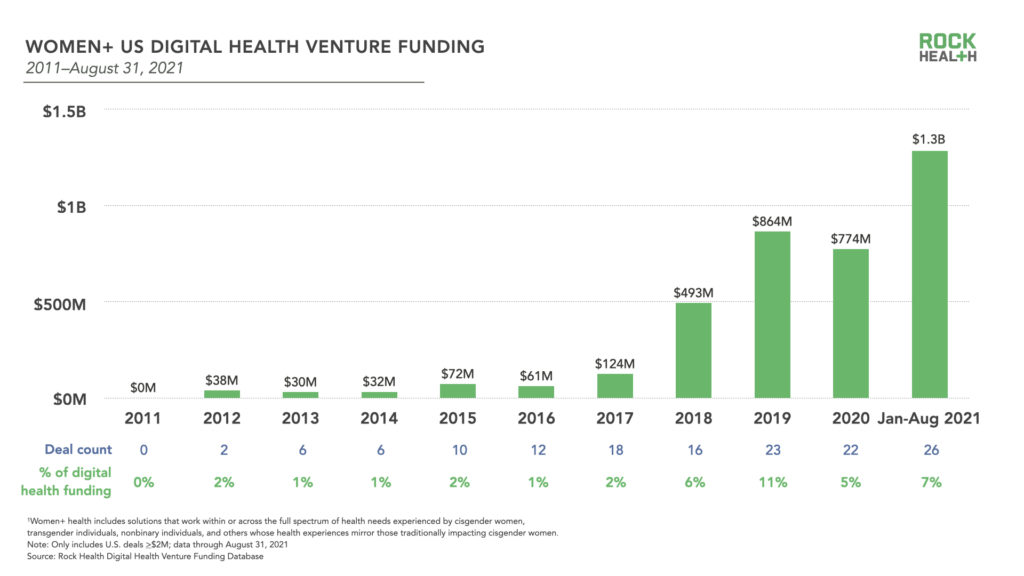

Rock Health, a venture capital fund dedicated to digital health, released an analysis of investment and financing in the U.S. “Women+” digital health market in September 2021. The concept of “Women+” here encompasses all women and all individuals who identify as having women’s health needs.

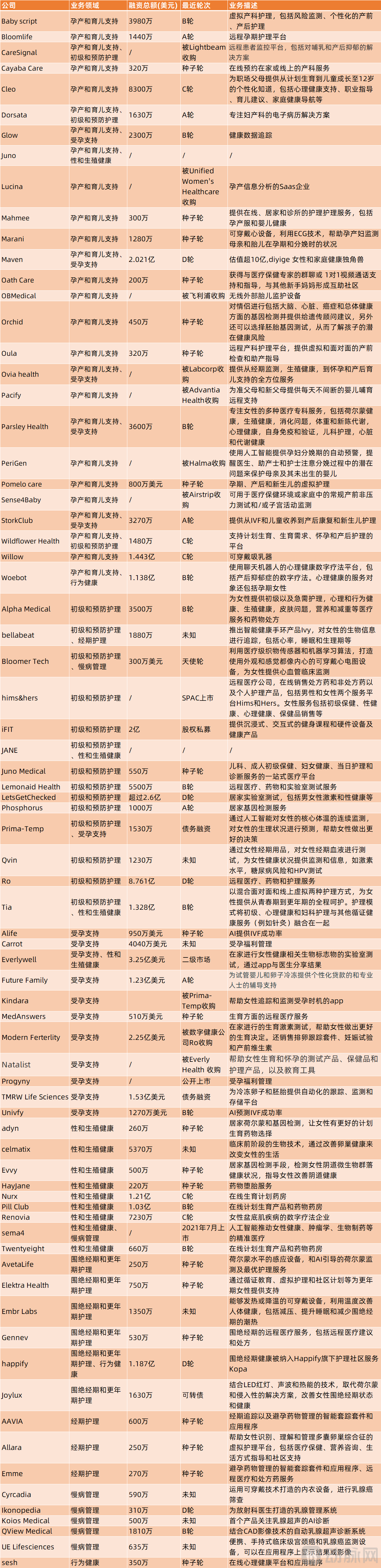

Rock Health segments the U.S. women’s health sector into eight categories: maternity and parenting support, primary and preventive care, conception support, sexual and reproductive health, chronic disease management, perimenopause and menopause care, menstrual care, and behavioral health. Analysis shows that maternity and parenting support has been the most popular area for startups over the past five years. In terms of financing, the subsector with the highest funding in the first eight months of 2021 was primary and preventive care ($668 million), followed by conception support ($330 million) and maternity and parenting support ($316 million). VCBeat has reviewed the business operations of nearly 80 women’s health companies compiled by Rock Health to provide interested readers with further insights; please refer to the infographic at the end of this article for details.

Since 2011, 74 U.S. women’s health companies have completed a total of 141 financing and investment transactions, raising $3.8 billion. 2021 marked the highest level of funding for women’s health enterprises in the past decade, with $1.3 billion raised in the first eight months alone. Compared with 2020, the average deal size in the first eight months of 2021 surged from $35.2 million to $49.4 million.

Historical Investment and Financing in the U.S. “Women+” Digital Health Sector from 2011 to August 2020 (Source: Rock Health)

Financing in the U.S. women’s health sector began to rise significantly in 2018, gradually showing signs of maturation. In 2017, the average age of companies in this sector was four years, and none had secured Series C financing. By 2021, the average age of women’s health startups had increased to six years. From January to August of that year, 31% of financing rounds were at Series C or later, while seed-stage deals accounted for 50% of the total. Both new enterprises and those in later funding stages are receiving support.

Funding Rounds and Scale in the U.S. “Women+” Digital Health Sector from 2017 to August 2020 (Source: Rock Health)

Although the U.S. women’s health sector is generally moving in a positive direction, it has failed to generate significant momentum. In terms of proportion, since 2011, financing for U.S. women’s health companies has accounted for only 5% of total digital health funding. Even at its peak in 2019, this share reached only 11%. The proportion in 2021 was the second highest in the past decade, at 7%. Additionally, regarding market size growth, financing in the women’s health sector increased by 2.2 times year-on-year during the first eight months of 2021, compared with a 2.3-fold increase across the entire digital health field, indicating broadly similar growth rates.

In contrast, in China. The nascent stage of China’s digital women’s health market closely paralleled that of the United States. The successive launches of the menstrual tracking apps Dayima and Meiyou in 2012 and 2013, respectively, can be regarded as a hallmark of the entry of Chinese women’s health awareness into the mobile era.

How is this market currently developing in China? VCBeat has analyzed the financing and investment activities of women’s health and maternal-and-child companies in its database since 2019, excluding enterprises whose sole business is infant care and products. According to VCBeat’s database, there have been only 33 financing rounds in the women’s health sector from 2019 to the present, with nine of these exceeding RMB 100 million. Over the past three years, the total financing amount in this sector has been approximately RMB 2.61 billion. Nearly two-thirds of the financing activities occurred before Series C, with companies focused on pregnancy, childbirth, parenting care, and related products dominating the landscape. Overall, the total financing volume in this sector remains relatively low.

In June 2021, Meiyou, which billed itself as the leading player in the niche segment of women’s health, withdrew its initial public offering (IPO) application from the Shenzhen Stock Exchange. This move was widely regarded by external observers as its closest brush with a public listing among its three IPO attempts. Although we do not judge a company’s success solely by its ability to go public, the subdued and rational investment sentiment prevailing in the capital markets suggests that the domestic women’s health sector may face an even more challenging path forward.

The long-standing lukewarm state of the women’s health sector is unlikely to change in the short term; however, the U.S. market has seen encouraging developments from women’s health companies in recent years. Progyny, a fertility benefits management company founded over a decade ago, went public via an IPO in 2019, making it the only publicly traded company exclusively focused on women’s care. In 2021, Hims & Hers, a comprehensive large-scale telehealth provider, and Sema4, a precision medicine company leveraging artificial intelligence in women’s health, oncology, and biopharmaceuticals, both achieved public listings through SPAC mergers. Ro, another integrated telehealth and care company, is also poised for a SPAC listing. In the private equity market, Maven Clinic, a virtual clinic offering comprehensive fertility and maternity services, became the first unicorn among companies dedicated solely to women’s health.

In our review of nearly 80 U.S. women’s health companies summarized by Rock Health, we identified three startups for a brief business analysis from a pool of approximately 60 independent companies focused exclusively on women’s health services. Selection was based on their leadership in IPOs and financing activities, aiming to help readers gain deeper insights into the strategic positioning and business logic of leading enterprises in the U.S. women’s health market.

Amid a funding winter and low market attention across the sector, how did they earn market trust?

Progyny is an employer-focused provider of employee fertility benefits, primarily serving individuals with needs for assisted reproductive technology (ART). In the United States, infertility is a high-prevalence condition that is either poorly covered or entirely excluded from traditional health insurance plans. Patients often face annual or lifetime reimbursement caps, are required to undergo step therapy, or encounter restrictions on access to more advanced treatments. Through its two core solutions—the Smart Cycle fertility benefit and the Progyny Rx pharmacy benefit—Progyny empowers users to make more flexible spending decisions throughout their fertility journey, reduces out-of-pocket costs, and improves the likelihood of successful conception in a cost-effective manner.

Smart Cycle is a comprehensive fertility benefit that provides users with access to all necessary diagnostics and cutting-edge technologies, such as egg freezing, embryo transfer, and preimplantation genetic diagnosis. Smart Cycle offers 17 different treatment options, which can be used individually or in combination based on user needs. Each treatment option is assigned a specific unit value (some are fractional, while others are whole numbers). Employers purchase a total Smart Cycle allowance for each eligible employee upon contract signing. Employees can select their preferred clinics within the Progyny network, undergo treatments deemed necessary by themselves and their fertility specialists throughout the conception journey, and pay for these services using their Smart Cycles.

Progyny Rx provides members with the medications required during fertility treatment, reducing dispensing and delivery time to two days to eliminate the risk of missing a treatment cycle. Progyny Rx offers clinical education and support via phone seven days a week to ensure members understand necessary medication storage requirements and administration techniques, including injection training. Additionally, the pharmacy benefit includes a video library to provide support for members who require extra guidance.

Maven Clinic is currently the first unicorn among pure-play digital women’s health companies in the U.S. private market and has raised the highest total funding, amounting to $202.1 million to date. Maven is a digital clinic that provides comprehensive services covering all stages of women’s health, including fertility, pregnancy and childbirth, newborn care, and even return-to-work support.

It boasts a robust women’s health care team, including obstetrician-gynecologists, specialists in conception, pregnancy, and postpartum care, nurse practitioners, midwives, doulas (from the Greek word “doula,” referring to trained and experienced individuals who provide physical, emotional, and informational support to pregnant women during the prenatal and postpartum periods; they are not necessarily medical professionals), prenatal dietitians, mental health providers, developmental psychologists, physical therapists, lactation consultants, sleep coaches, parenting experts, and career counselors. Whether it involves issues related to trying to conceive, egg freezing, prenatal care, postpartum and newborn care, postpartum depression, miscarriage, or even returning to the workplace, Maven can provide corresponding services.

Maven assigns a dedicated care advocate to each user, who helps connect them with the most suitable professionals for video and text consultations, recommends top-tier local providers for in-person care, and assists with issues related to employee benefits or insurance. Users can access personalized content and virtual courses through Maven. The company operates under two business models, catering to both individuals and employers.

Unlike Progyny and Maven, TMRW is a high-tech enterprise that provides an automated tracking, monitoring, and storage platform for the cryopreservation of oocytes and embryos during the IVF process, ensuring their secure management. Currently, oocyte and embryo cryopreservation relies on vitrification; however, TMRW argues that the backend infrastructure for this technology has lagged behind, with samples being manually labeled and customer data inadequately secured. TMRW’s platform integrates software and robotics, 24/7 remote monitoring, and a complete digital chain of custody for all cryopreserved oocytes and embryos in IVF laboratories. Key features of TMRW include:

● Embed radio-frequency identification (RFID) chips into vials used for storing oocytes and embryos. Each patient is assigned an RFID tag with a unique identifier, enabling the clinic to identify and track each reproductive cell, thereby significantly reducing the risk of sample mislabeling or loss.

● Subsequently, these vials are stored in liquid nitrogen within “cryogenic robotic” tanks equipped with sensors capable of detecting subtle changes, such as fluctuations in temperature and power consumption.

● Utilizes state-of-the-art cloud-based monitoring systems to perform thousands of health checks daily on stored samples without interruption. Predictive analytics are conducted via on-site and remote communication systems to proactively identify and address any security and storage trends, preventing them from escalating into issues.

● In severe emergencies such as natural disasters, TMRW’s storage tanks maintain safe cryogenic temperatures to protect oocytes and embryos, remaining operational for over two weeks without electricity or human intervention.

● HIPAA-compliant encrypted software system, providing the highest level of data privacy and security

According to CNN, TMRW operates on a subscription-based business model, offering the platform free of charge to clinics while charging patients an additional $25–$30 per month. To date, TMRW has raised a total of $153 million in funding.

The digital women’s health markets in China and the United States emerged around the same time. However, due to differences in healthcare systems, social attitudes, consumer habits, and insurance frameworks, the business and profitability models of U.S. companies may not necessarily offer applicable lessons for the Chinese market. We hope our observations will provide valuable insights for domestic enterprises and help foster growth in this sector.

First, regarding the nature of the business, the vast majority of digital women’s health enterprises in the United States maintain a strong medical character throughout their development. Whether through telemedicine consultations, online pharmacies, employee health benefits, genetic testing, or wearable devices, their operations and profit models remain centered on the fundamental provision of healthcare services, with the ultimate goal of improving health outcomes and reducing medical costs. Targeted professional medical advice and diagnoses from licensed physicians and nursing staff constitute a critical component of many companies’ business models. In China, specialized internet hospitals capable of delivering targeted medical services have not yet been able to support the blue-ocean market of women’s health. Instead, a more common path taken by many companies is one that anchors itself in women’s health while deeply cultivating the consumer-oriented attributes of this demographic. Although the consumption potential of women is enormous—with greater socioeconomic participation, improved status, and shifting mindsets making them more willing to pay for a healthy, comfortable, and high-quality life—the challenge of capturing a larger share of this highly competitive consumer market will likely remain a bottleneck for domestic enterprises for a considerable period to come.

Let us now examine the service landscape. Maternity care is a significant sector shared by the female health markets in both China and the United States. Given that childbirth represents a crucial phase in a woman’s life, this is not surprising; however, it should not be regarded as the sole purpose of a woman’s existence. Furthermore, it is noteworthy that in 2020, the average life expectancy for women in China reached 80.88 years. Meanwhile, at a press conference held on January 20, the National Health Commission pointed out that during the 13th Five-Year Plan period, the annual number of women aged 20–34—the peak childbearing age group—decreased by 3.4 million, with a further decline of 4.73 million in 2021 compared to 2020.It is evident that both fertility rates and the motivation to have children in China are in a continuous decline. If service providers in the market focus solely on meeting this critical demand for childbirth, such an approach may prove short-sighted, potentially causing them to miss greater opportunities to enhance women’s overall healthcare experience.This is also why we have observed that participants in the U.S. market have broadened their focus to encompass women’s entire lifecycle. Financing for U.S. startups specializing in female perimenopause doubled from 2019 to 2021, and numerous other emerging companies have entered fields such as breast cancer, cervical cancer, cardiovascular disease in women, and polycystic ovary syndrome (PCOS). These market gaps in China need to be filled by more enterprises.

Third, in the process of digitizing women’s health solutions, Chinese enterprises should strengthen the application of technology in women’s health scenarios, allowing technology to transcend its role as merely a platform carrier. In reviewing U.S. companies, VCBeat has identified numerous enterprises leveraging wearable or artificial intelligence technologies to support women’s health. Examples include Marani (which uses ECG technology to create wearable cardiac devices that help expectant mothers monitor both maternal and fetal conditions during pregnancy and childbirth), Qview Medical (an automated breast ultrasound diagnostic system integrated with CAD imaging technology), and Univfy (an AI-driven platform for predicting IVF success rates). Additionally, there are more conceptually innovative companies such as Bloomer Tech (which utilizes medical-grade fabric sensors and machine learning algorithms to develop wearable ECG devices that look and feel like underwear, providing clinical cardiovascular monitoring for women) and Qvin (which tests menstrual blood through feminine hygiene products to provide health monitoring and information for women, including hormone levels, diabetes risk, and HPV testing).

Finally, the development of the women’s health sector is inseparable from progress in societal perceptions. Due to physiological differences, many conditions unique to women are often viewed by outsiders as mysterious or stigmatized, and their impact on women may go unrecognized or misunderstood. Among U.S. women’s health companies that secured financing in the first eight months of 2021, 69% were led by women. This not only demonstrates that women are better positioned to identify their own genuine healthcare needs, but also highlights the need for broader societal engagement in raising awareness about women’s health, so as to develop products and services that truly address women’s needs. In this regard, entrepreneurs and investors should adopt a female-centric perspective when founding and investing in related businesses, carefully considering user needs and the resulting impact.

As part of the broader health and wellness industry, the field of women’s health in China holds immense potential for growth. As China’s first menstrual health management platform, the Dayima App has served over 100 million female users to date, building a comprehensive service ecosystem that covers the entire maternal journey, including menstruation, preconception care, pregnancy, and postpartum parenting.

Da Yi Ma allows users to track their menstrual cycles, ovulation, and other conditions via its app, helping women better understand their body’s cyclical changes and identify optimal times for conception and pregnancy. Through community sharing and science-based health education, Da Yi Ma addresses user needs for content on gynecological care, preconception planning, and sexual health by leveraging both peer experiences and expert advice, thereby enhancing women’s awareness of their physiological status. Additionally, Da Yi Ma offers specialized vertical services through dedicated columns, providing information on HPV vaccination and online medical consultations to precisely meet women’s specific healthcare demands.

At the current stage, leveraging its massive user base, Dayima (Menstruation Tracker) is continuously exploring how to perfectly match women’s needs with other participants in the industry chain. For instance, it provides marketing services for pharmaceutical companies such as Beijing Tongrentang and Good Doctor, as well as for preconception health and reproductive medical enterprises like Jinxin Fertility, Elevit, and Jinxiuer, thereby achieving product exposure and sales conversion. In addition to operating and developing on-platform traffic, the Dayima App aggregates other small and medium-sized vertical internet platforms for women and has launched a vertical female advertising traffic ecosystem alliance called “Yi Ma Miao.” This alliance is estimated to cover 400 million women and connect with over 200 media partners, helping brand owners identify precise female customer segments, adjust advertising delivery strategies, and drive long-term growth in advertising effectiveness. Based on its professional community platform and strong big data mining capabilities, the Dayima App also possesses the ability to export industry data. Over the past eight years, it has consecutively released annual Big Data Reports on Women’s Health, offering insights into new demands and trends in the women’s health industry by examining contemporary women’s attitudes, concepts, behaviors, and consumption trends regarding health, marriage and relationships, childbirth, child-rearing, and careers.

While strengthening its core business capabilities, Dayima is also incubating new brands. Haoyunma, a maternal health management platform incubated by Dayima and operating independently since August 2017, announced on January 4, 2022, that it had secured RMB 30 million in Series B1 financing, marking the first major funding event in the women’s health market for the new year. Designed for women across the preconception, pregnancy, and parenting stages, Haoyunma offers comprehensive features including access to medical knowledge, services, and products for preconception and prenatal care; monitoring of pregnancy health indicators; dietary guidance; infant care tips and product recommendations; and community sharing functionalities. Looking ahead, Haoyunma plans to launch a parent-child membership program to connect individual consumers (C-end) with business merchants (B-end), thereby expanding business opportunities within the childcare ecosystem. Currently, Haoyunma’s revenue model primarily consists of digital marketing advertising and maternal-and-infant insurance data services, with the latter contributing the larger share of income.

Although this sector is niche, there remains significant room for further exploration of specialized segments and innovation. According to Global Market Insights, the Femtech market—encompassing technologies, software, products, and diagnostics that leverage technology to enhance women’s health and well-being—exceeded USD 22.5 billion in 2020 and is projected to grow at a compound annual growth rate (CAGR) of 16.2% from 2021 to 2027. Currently, the women’s health sector remains a tranquil blue ocean, awaiting greater investment to create more substantial ripples.

VCBeat hopes to accompany and witness the growth of emerging enterprises. If you are a company or investor in the women’s health sector, we welcome you to share your industry insights with us.

Appendix: Business Overview of Nearly 80 U.S. Women’s Health Companies (Source: Rock Health, Crunchbase)