Comprehensive 100-Page Report on the Largest Cardiovascular Segment: Pathway to a $10 Billion Transcatheter Mitral Valve Market

The Transcatheter Mitral Valve (TMV) Sector Report is the second sector valuation report launched by VCBeat. The full text exceeds 60,000 words and spans more than 100 pages, making it currently the only in-depth report dedicated exclusively to mitral valves that exceeds 100 pages in the market.VCBeat has devoted extensive space and effort to analyzing the transcatheter mitral valve (TMV) sector because TMV is widely regarded as the “crown jewel” of interventional valve therapy. Strong unmet clinical needs have driven its rapid, sustained growth; its vast market potential makes it highly attractive; and its technical complexity has erected formidable barriers to entry. However, the technological pathways for TMV are intricate and diverse, encompassing more than 100 product candidates. How can we conduct a systematic assessment? What conclusions can be drawn? These are the key questions this report aims to address. In addition, what does the current competitive landscape look like? Where do future innovation opportunities lie? Is competition in the TMV arena a “blitzkrieg” or a “war of attrition”? And what is the true market value of the TMV sector? In this report, we will explore these issues in depth and strive to provide the most robust answers.

Due to space constraints, this article presents selected excerpts of text and images from the report. To read the full version, please scan the mini-program QR code at the end of the article to download it.

Zuo Hui, the late founder and chairman of Beike Zhaofang, once said, “Do the difficult but right thing.” This statement has resonated with many people. TMV is precisely such an endeavor—“extraordinarily difficult” yet “profoundly right.”

1Strong Inelastic Demand: Limited Surgical Service Supply Falls Far Short of Hundredfold Demand in the Long Term

The strong, inelastic demand for TMV primarily stems from the contradiction between the extremely limited supply of surgical procedures and the massive treatment demand—hundreds of times greater—that remains unmet in terms of both volume and indication coverage.

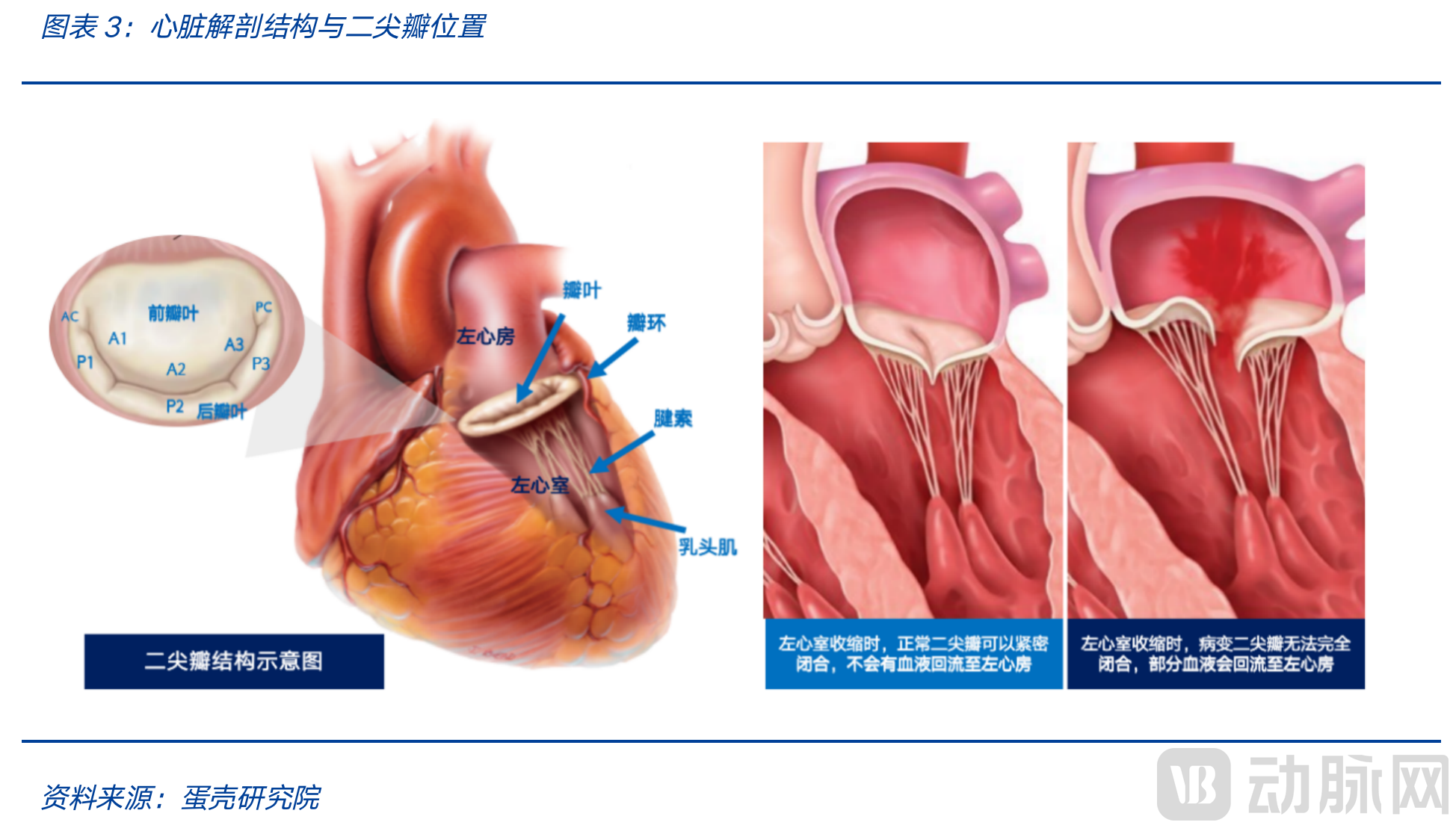

Severe Mitral Regurgitation Is Extremely Debilitating, Has a High Mortality Rate, and Creates an Urgent Need for Treatment

Mitral regurgitation is the most common valvular heart disease. Severe mitral regurgitation causes significant suffering, with typical symptoms including dyspnea, lower extremity edema, and paroxysmal nocturnal dyspnea, leading to a strong and urgent need for medical care. Delayed treatment of mitral regurgitation poses a serious threat to patients' life and health, progressively leading to heart failure and death as the condition worsens; the one-year mortality rate for severe mitral regurgitation is as high as 57%. Currently, surgical intervention is the gold standard for treating mitral regurgitation; however, more than 50% of patients with moderate-to-severe mitral regurgitation are ineligible for surgery due to advanced age and comorbidities. The overall one-year and five-year mortality rates for untreated patients are 20% and 50%, respectively.

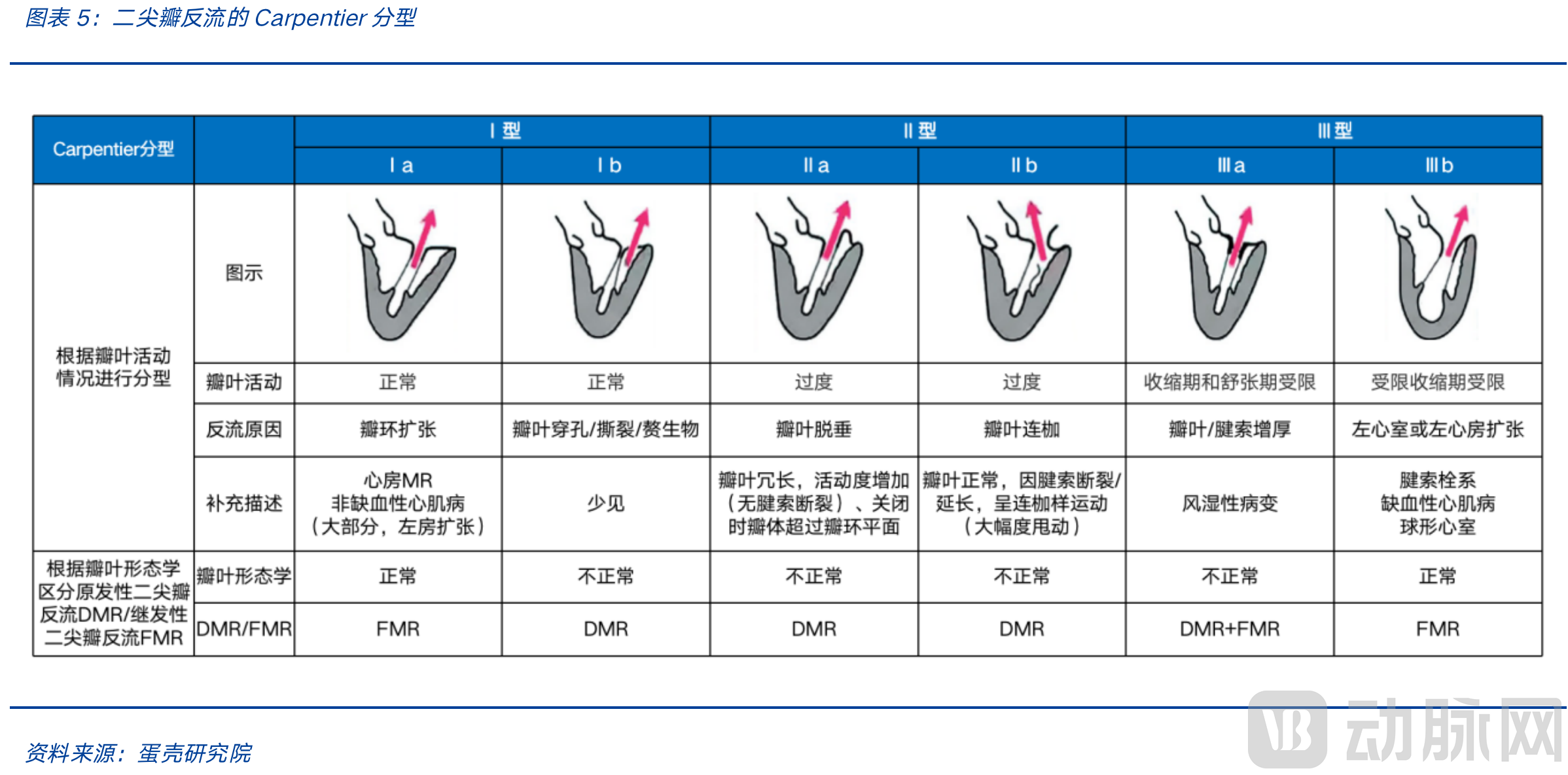

The etiologies of mitral regurgitation can be categorized into two types: primary and secondary. Primary mitral regurgitation results from alterations in the physiological structure and function of the mitral valve apparatus itself (including the leaflets, chordae tendineae, annulus, and papillary muscles). In most cases, favorable therapeutic outcomes can be achieved by surgically correcting the pathological lesions at an early stage. Secondary mitral regurgitation, on the other hand, is caused by dilation or functional abnormalities of the left ventricle and left atrium, leading to mitral annular dilation and subsequent regurgitation; merely correcting the anatomical structure of the mitral valve alone often fails to yield ideal therapeutic results. To better characterize the pathological type of mitral regurgitation, Professor Carpentier of Harvard Medical School proposed a more detailed classification system for mitral regurgitation (the Carpentier classification).

Mitral valve surgery currently fails to meet the hundredfold treatment demand and will remain insufficient in the future.

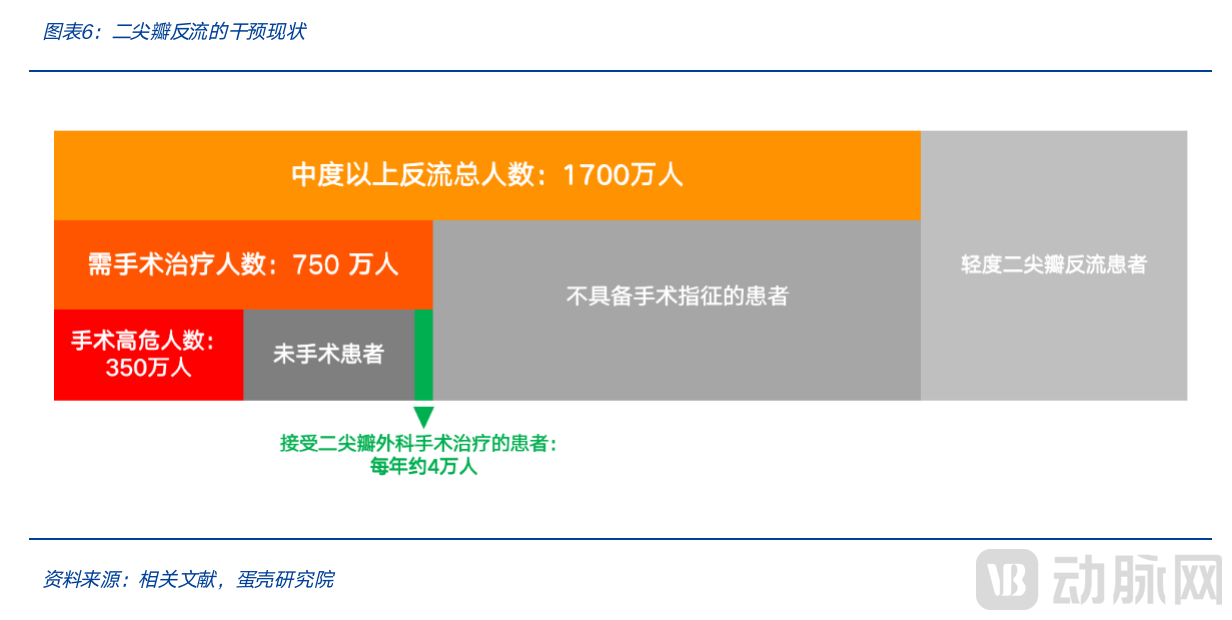

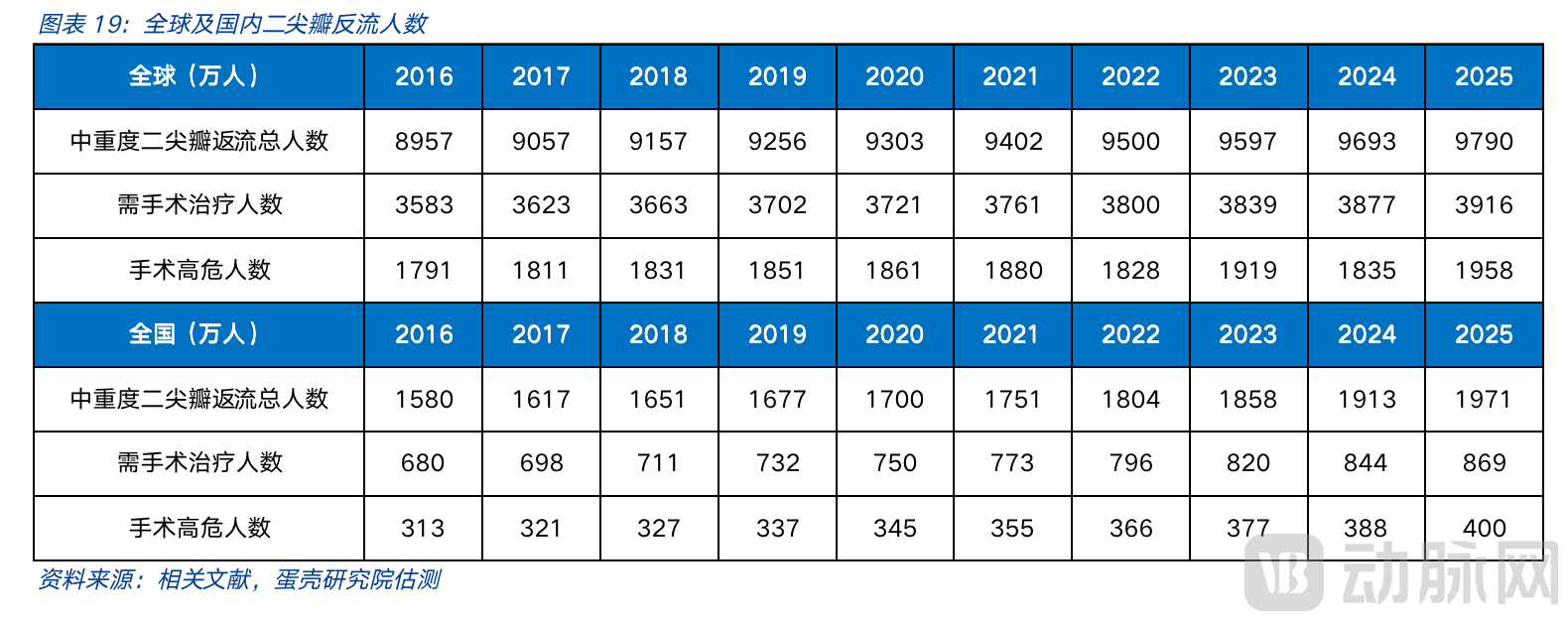

First, in terms of the quantitative gap, relevant guidelines and epidemiological projections indicate that nearly 7 million patients with moderate-to-severe mitral valve disease in China require interventional treatment. However, only 38,000 surgical procedures for mitral regurgitation were performed in China in 2019, resulting in a treatment rate of merely 0.5%. The gap between supply and demand exceeds 100-fold.

Second, from a long-term perspective, whether viewed domestically or globally, the supply of surgical procedures is unlikely to grow rapidly. In 2018, only nine hospitals performed more than 1,000 valve surgeries each, collectively accounting for approximately 25% of the national volume of valve surgeries in China. One major reason for the severe shortage in surgical capacity is the high complexity of these procedures and the prolonged learning curve for surgeons. Since surgical skills are primarily accumulated at the individual physician level, whereas transcatheter mitral valve (TMV) technology mainly embeds technological iterations and experiential knowledge into the device itself, the use of interventional devices will become increasingly simplified. This trend will accelerate the training of interventional operators, thereby breaking through the supply bottleneck.

Third, in addition to the quantitative shortfall, the limited coverage of indications results in a significant gap between surgical interventions and clinical needs. Approximately 50% of patients are considered high-risk for surgery due to age and comorbidities, rendering them ineligible for surgical procedures (the prevalence of mitral regurgitation shows a clear trend of increasing with age).

2Vast Market Potential: Leading Prevalence Among Valvular Heart Diseases, with a Potential Market Size at Least Five Times That of TAVR

Among the four cardiac valves, the mitral valve has the highest disease incidence. In 2020, there were approximately 17 million patients with isolated mitral regurgitation and about 6 million patients with mitral stenosis in China. Epidemiological statistics indicate that the mitral valve has the highest prevalence globally among the four heart valves, particularly for mitral regurgitation. Located at the junction between the left atrium and left ventricle, the mitral valve is responsible for systemic circulation and withstands greater hemodynamic pressure, making it more susceptible to pathology. Furthermore, the mitral valve is the only bicuspid structure among the four cardiac valves; dysfunction of either leaflet can significantly impair its normal physiological function.

Neil Moat, Chief Medical Officer of Abbott’s Structural Heart business, has pointed out that “the growth opportunity for mitral valve interventions lies not only in the fact that the number of patients with mitral valve disease exceeds those with aortic stenosis and regurgitation, but also in that patients with mitral valve disease often do not receive effective treatment.” As the most common valvular heart disease in clinical practice, moderate-to-severe mitral regurgitation affects nearly 10% of individuals aged 75 and older, a proportion likely to increase further with population aging. The large and rapidly growing population of patients with moderate-to-severe mitral regurgitation, coupled with the fact that more than half of these patients are intolerant to surgery, provides substantial room for development in transcatheter mitral valve therapies. Based solely on the potential patient base, the market potential for the transcatheter mitral valve (TMV) sector is at least five times larger than that of the transcatheter aortic valve replacement (TAVR) sector, which has been the hottest area in recent years.

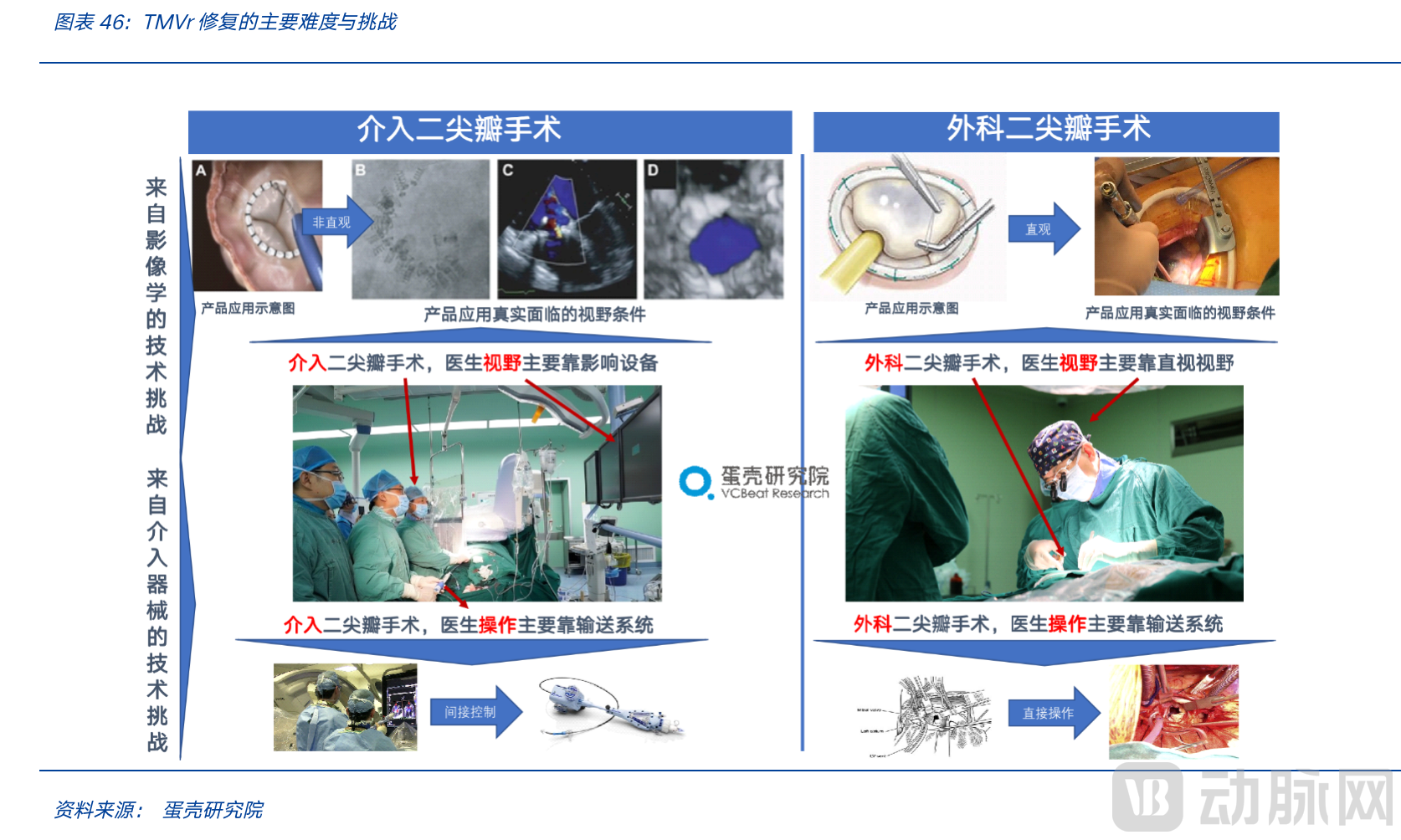

3Technical Challenges: Interventional Procedures Are Difficult, Mitral Valve Interventions Are Particularly Challenging, and Transfemoral Mitral Valve Interventions Are Even More So

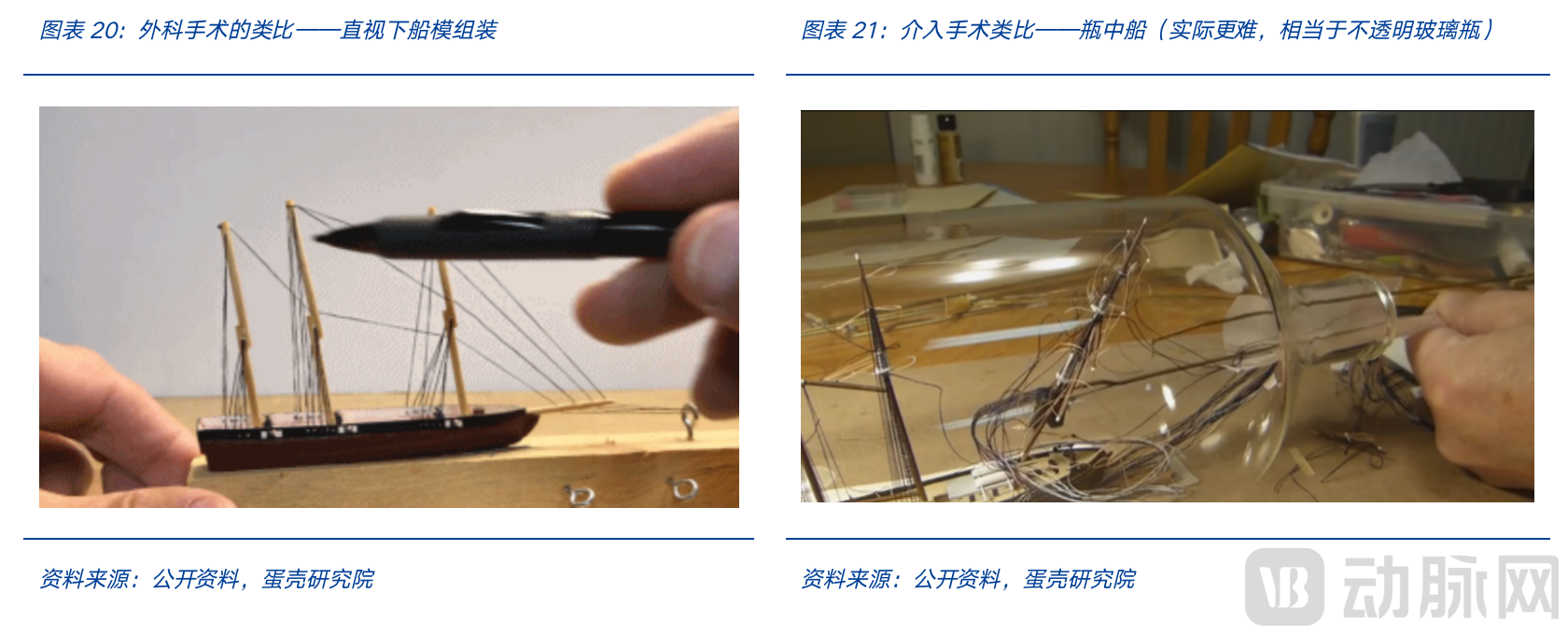

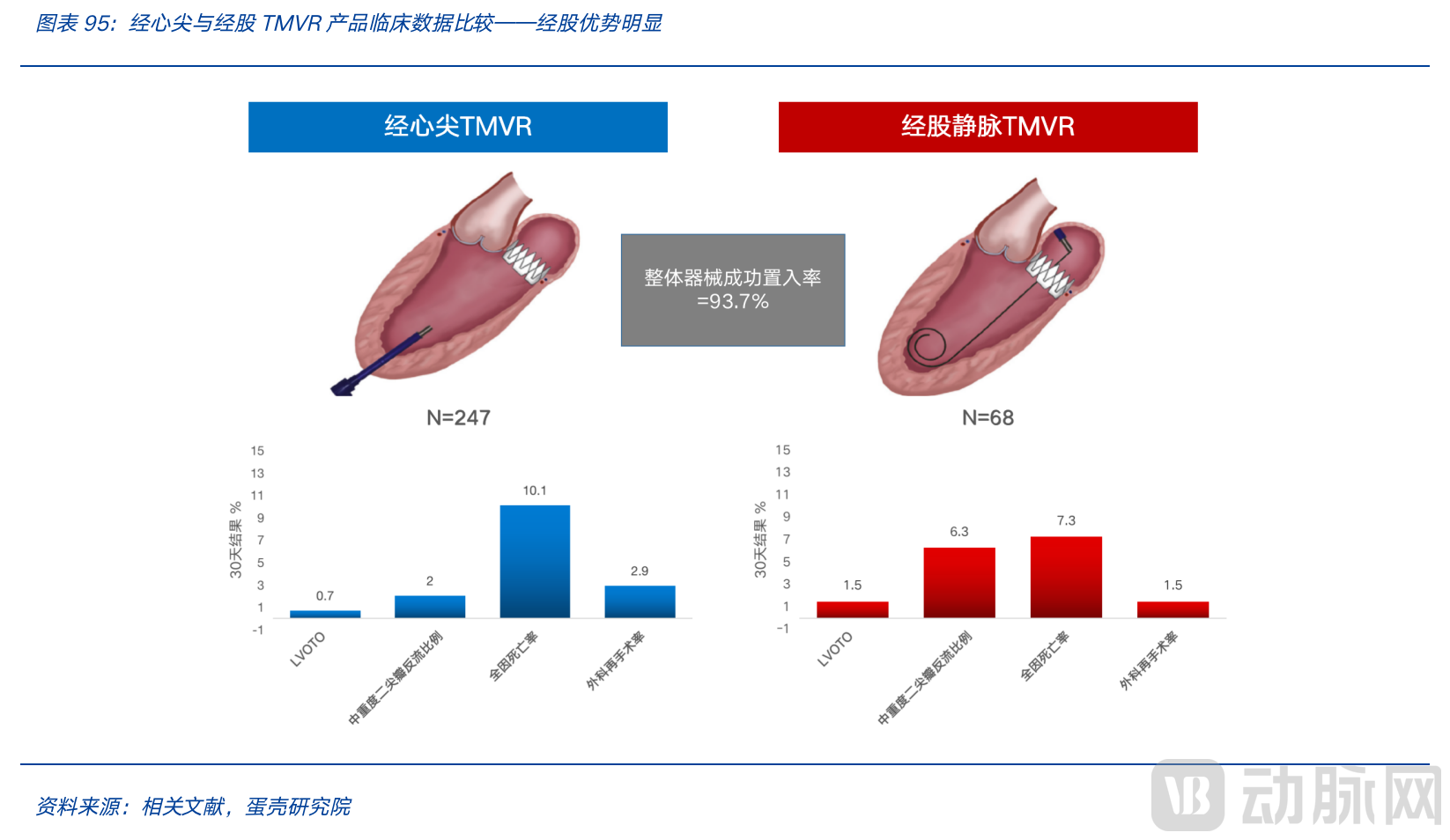

The immense technical challenges of transcatheter mitral valve (TMV) replacement stem from three aspects. First, the intervention itself is highly difficult; due to the lack of direct visualization, it relies heavily on ultrasound and fluoroscopy for imaging guidance, requiring precise maneuvers via long-catheter devices. Second, mitral valve interventions are particularly challenging because the mitral valve has a more complex anatomy than the aortic valve, is difficult to anchor, and carries a higher risk of complications or adverse events. Third, the transfemoral approach presents even greater difficulties. While the transapical approach inherently causes myocardial trauma and still depends on surgical procedures, the transfemoral approach truly minimizes invasiveness. However, this approach faces the superlative engineering challenge of miniaturizing both the valve and the delivery system while simultaneously navigating the 90-degree bend required for transseptal crossing.

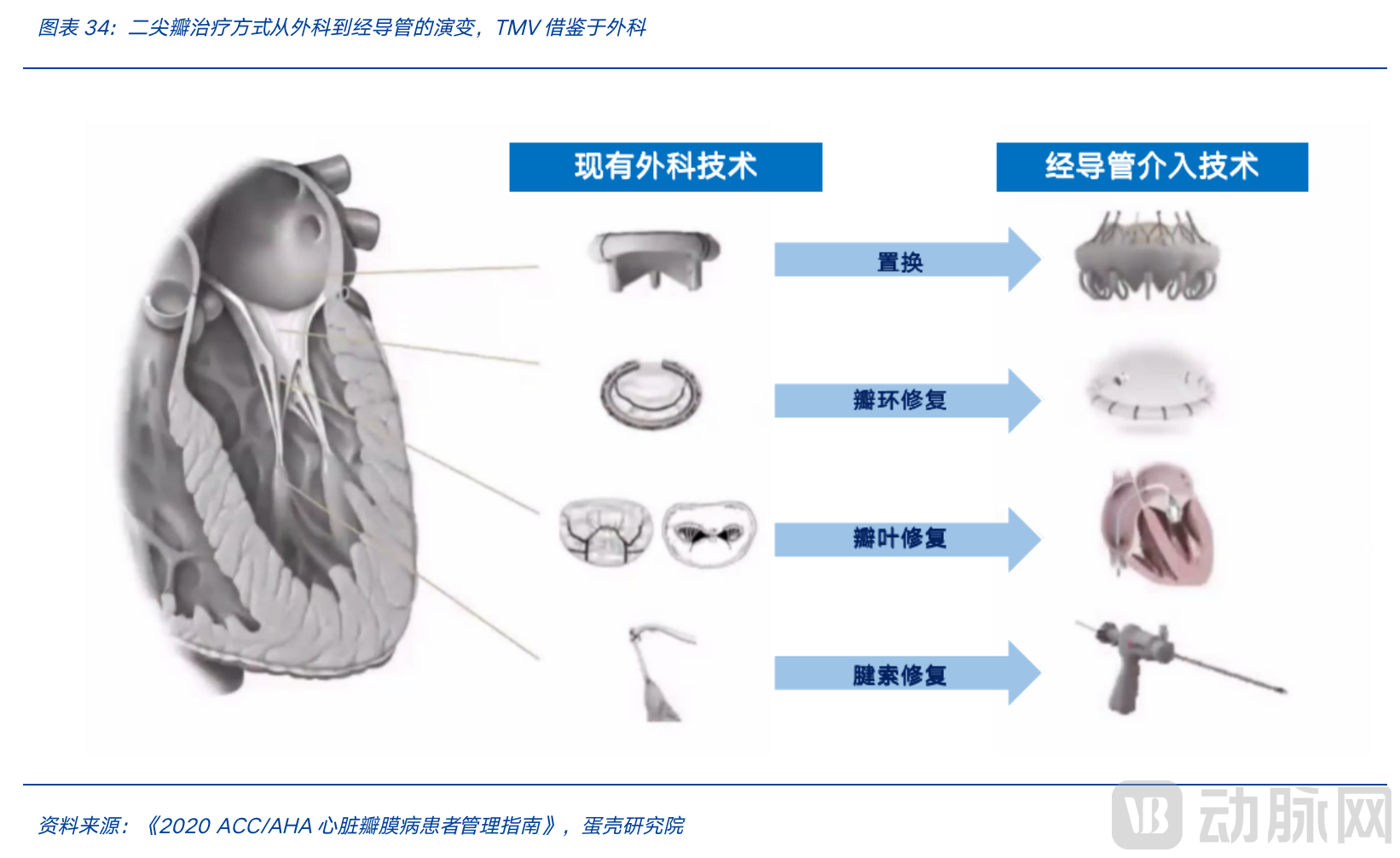

Unlike the standardized profile of TAVR, mitral valve intervention devices resemble an arsenal, presenting a dazzling array. This diversity stems partly from the anatomical complexity of the mitral valve and the diseases themselves, and partly reflects that current technological pathways are still in a pre-mature stage.

For clinical surgeons, medical device R&D and manufacturing enterprises, and investment institutions alike, the accurate assessment and selection of medical devices are of paramount importance. For companies and investors, the cost of a wrong choice can amount to hundreds of millions in financial losses, whereas for clinical surgeons, the consequence of an incorrect selection is the precious life of a patient.

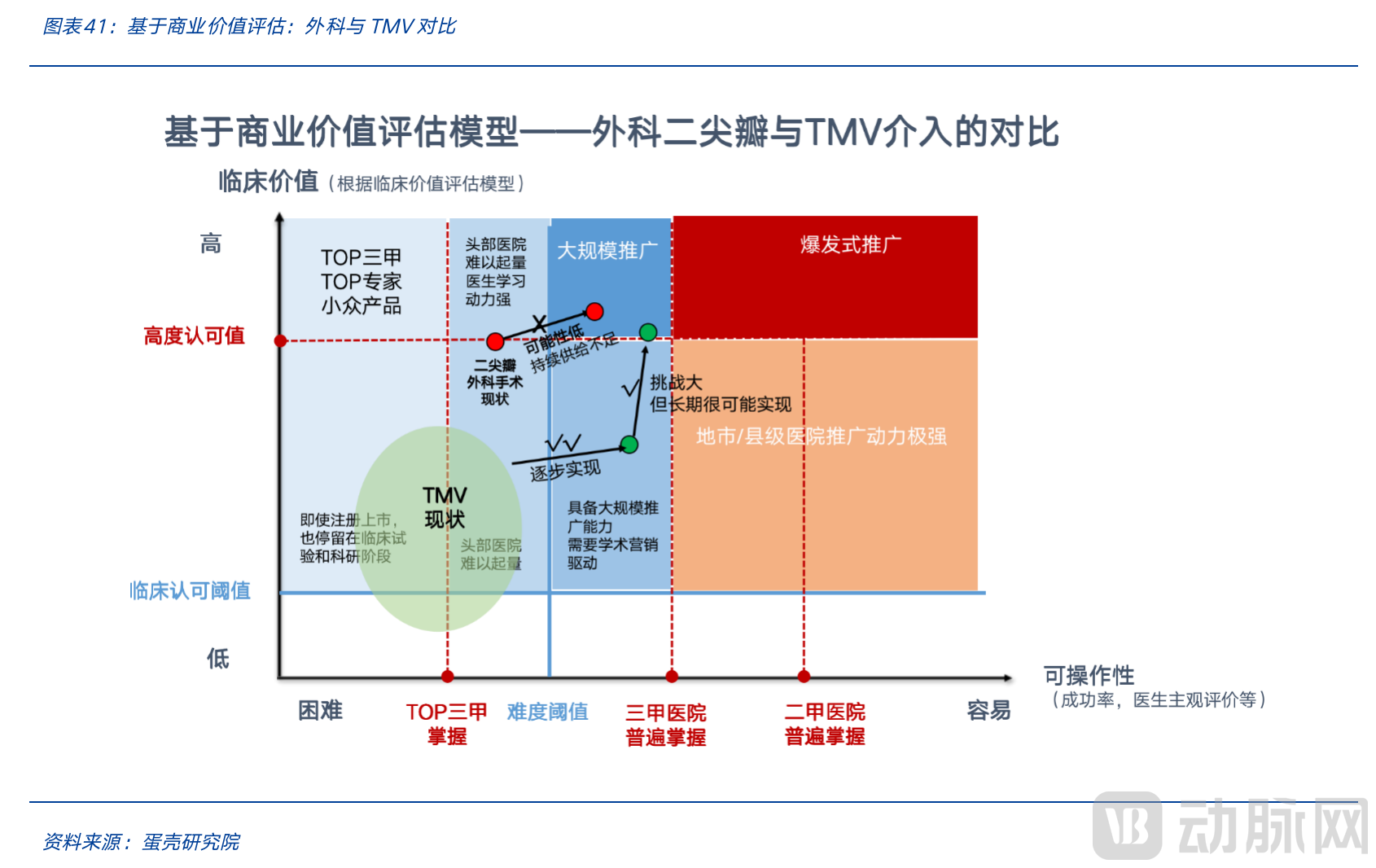

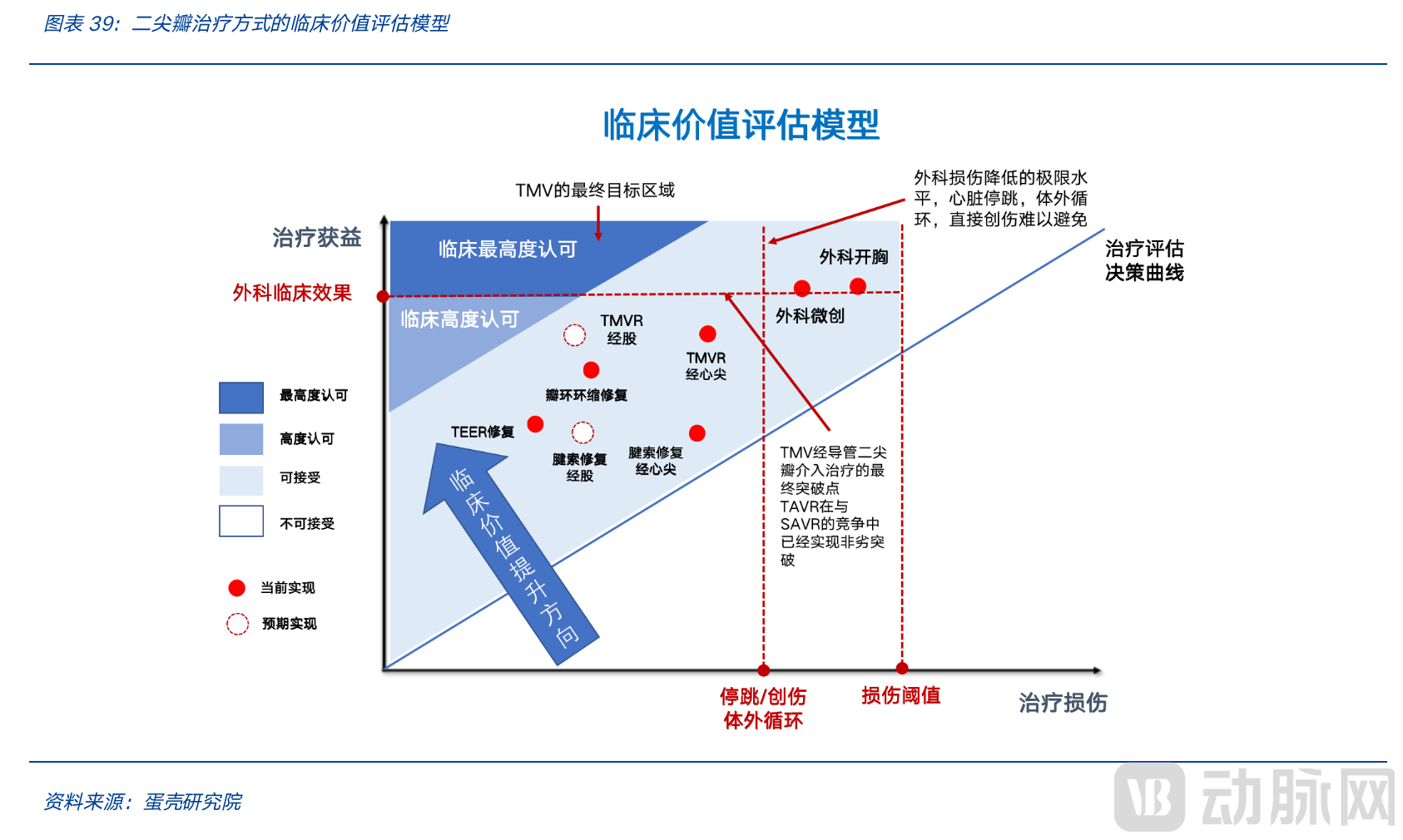

Faced with numerous technological pathways, we must have an analytical framework that acts as a sieve or funnel to derive the most accurate judgments possible based on existing information.In this report, we employ the “Triple Gate” framework for analysis and construct a matrix model to evaluate the commercial value of mitral valve intervention products, thereby assessing the development potential of various technological pathways.

1A Holistic Understanding of the Three Barriers to TMV: An Analytical Model Framework

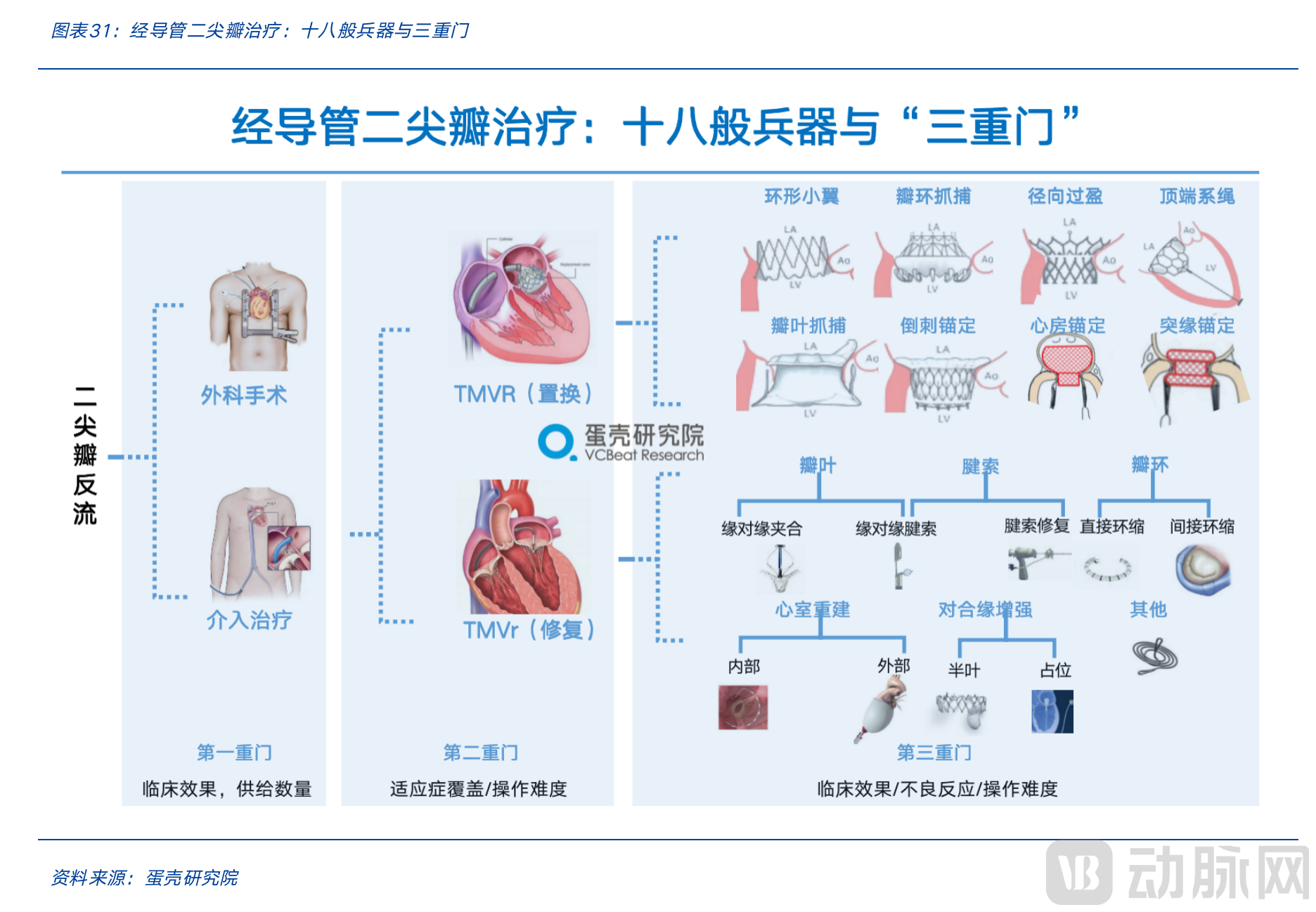

The so-called "Triple Gate" of TMV refers to three sequential choices that must be analyzed when evaluating TMV products: the first choice is surgical versus transcatheter intervention; the second is TMVr (repair) versus TMVR (replacement); and the third is the selection of specific technical pathways within TMVr and TMVR, respectively.

The three-tiered structure provides a framework for analysis, while our constructed commercial value assessment model enables the evaluation of the commercial potential of medical devices across different technological pathways. Our model is built upon two critical dimensions: clinical value and product operability, both of which are key variables influencing the ultimate commercial realization of a product.

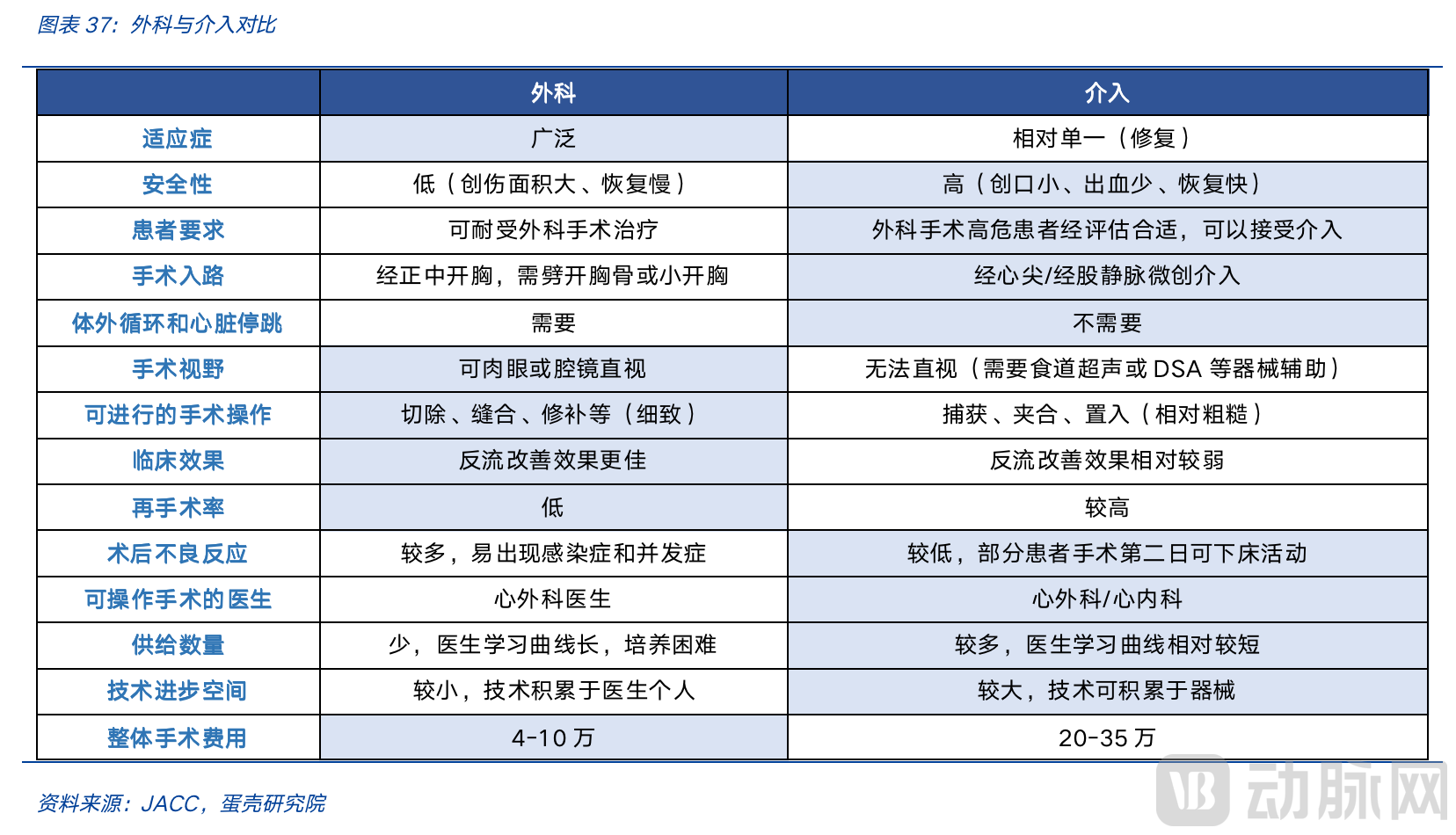

2Surgical Procedures vs. Interventional Procedures: The Stronghold of Surgery as the Gold Standard Does Not Hinder TMV from Unlocking Tens of Times More Growth Potential

The competition between surgical and interventional procedures is the first of the “three gateways.” This is the prerequisite for the large-scale adoption and promotion of transcatheter mitral valve (TMV) replacement, as well as the determining principle for the singularity point of its explosive growth.

From the current perspective, all transcatheter mitral valve (TMV) procedures are derived from their surgical counterparts, and surgical intervention remains the gold standard for treating mitral regurgitation. At present, there is still a certain gap between TMV and surgery in terms of overall clinical outcomes (both short- and long-term), safety, and adverse events. However, although TMV techniques draw on surgical methods, this does not mean that the underlying treatment philosophy is directly copied from surgery. With the evolution of interventional therapy concepts and continuous advancements in TMV technology, widespread adoption is expected once its clinical outcomes approach those of surgery. If TMV demonstrates non-inferiority to surgery, it may experience explosive growth; if it surpasses surgical outcomes, it is likely to exert a substitution effect on the existing surgical market.

From a conservative and prudent perspective, even if transcatheter mitral valve (TMV) intervention struggles to demonstrate non-inferiority to surgical treatment in short-term clinical outcomes, it does not preclude TMV from capturing an incremental market opportunity ten times the size of the existing stock—provided it delivers significant patient benefits. Currently, there are 7.5 million patients with mitral regurgitation in China who require interventional treatment. Among them, 3.5 million are at high surgical risk and have virtually no access to surgical intervention. Of the remaining 4 million patients eligible for surgery, fewer than 40,000 actually undergo surgical repair or replacement. This unmet need represents the initial growth avenue for TMV, offering an annual market potential dozens of times larger than the current stock of surgical procedures.

In terms of safety, although both types of procedures carry a certain risk of failure, transcatheter interventions are generally safer than surgical approaches. Regarding clinical outcomes, however, the overall efficacy of current transcatheter mitral valve interventions remains inferior to that of surgical treatment, due to the lack of direct visual field and the limited repair capabilities of existing transcatheter devices (e.g., MitraClip, which only enables edge-to-edge mitral valve repair). From the perspective of physician supply, transcatheter mitral valve therapies have significantly increased the number of qualified physicians by continuously optimizing and iterating interventional devices, thereby reducing procedural complexity and shortening the learning curve.

According to current guidelines, surgical intervention remains the preferred treatment for mitral regurgitation (particularly degenerative mitral regurgitation [DMR]) in patients at high surgical risk. Based on a comprehensive review of extensive literature, VCBeat Institute attributes the continued dominance of surgery to its broader capability in managing complex and combined lesions, superior efficacy in reducing regurgitation, and lower rates of reoperation. However, surgical approaches also face significant challenges that are difficult to overcome, such as concerns regarding procedural safety and the limited availability of experienced surgeons.

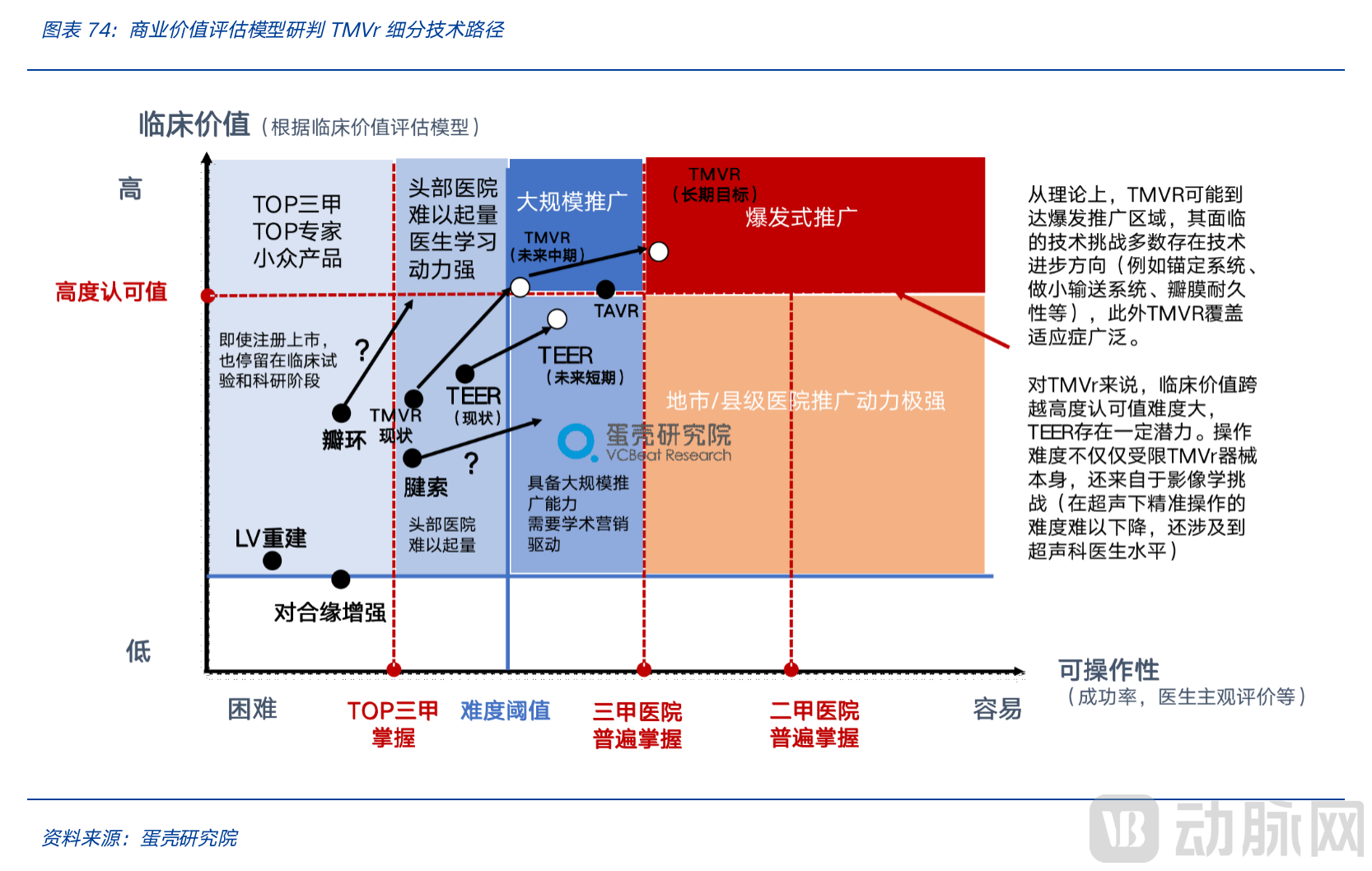

Finally, our analysis using a commercial value assessment model indicates that the development of TMV is an inevitable trend, with the potential to generate incremental volume many times over that of the existing stock of surgical procedures.

3Interventional Repair vs. Interventional Replacement: Each Has Its Merits, Coexisting in the Long Term; Transfemoral Replacement Holds the Most Promise as the Ultimate Solution for TMV

In the field of mitral valve interventional therapy, it is necessary to determine whether repair or replacement offers greater growth potential. The essence of this business question lies in assessing which approach can reach its “boiling point” more rapidly: (1) the rate at which the technical difficulty of repair procedures decreases (facilitating broader adoption), and (2) the rate at which the safety profile of replacement improves (enabling confident clinical application).

We believe that although both approaches face significant challenges, improving the safety and efficacy of transcatheter mitral valve replacement (TMVR) is theoretically more achievable than reducing the technical complexity of transcatheter mitral valve repair (TMVr). We anticipate that both modalities will coexist in the long term, as repair preserves the native subvalvular apparatus and allows for more targeted treatment, thus not being completely replaced by replacement. Nevertheless, transfemoral mitral valve replacement holds greater promise as an all-in-one ultimate solution, theoretically addressing the majority of regurgitation cases. A comparison of the cumulative sum (CUSUM) learning curves for surgical mitral valve repair versus replacement also clearly demonstrates that physicians find it easier to master mitral valve replacement procedures.

Overall, there is no statistically significant difference in safety between surgical mitral valve repair and replacement. However, repair allows for more precise, targeted treatment of the diseased mitral valve tissue, thereby ensuring better postoperative quality of life for patients. Consequently, it is considered the preferred option for treating moderate-to-severe primary mitral regurgitation. The exponential increase in technical complexity associated with transcatheter procedures has created greater potential for transcatheter mitral valve replacement. As a result, patients with mitral regurgitation who would typically be prioritized for surgical repair may opt directly for valve replacement when undergoing transcatheter therapy, as achieving optimal outcomes with transcatheter repair can be challenging.

However, in terms of safety, current transcatheter mitral valve repair (TMVr) products generally demonstrate a better safety profile than transcatheter mitral valve replacement (TMVR) products, primarily due to differences in product design and technology. Regarding the potential for device optimization in the near to medium term, transcatheter repair products require a significant reduction in the complexity of delicate maneuvers and an expansion of the scope of repairable cases per procedure, whereas transcatheter replacement products mainly need to reduce device size and mitigate valve degeneration to enhance safety.

Finally, our analysis using a commercial value assessment model suggests that transcatheter mitral valve repair (TMVr) is poised to overcome technical barriers and achieve high clinical acceptance for certain indications, thereby entering a phase of large-scale adoption. Although the development trajectory for transcatheter mitral valve replacement (TMVR) may be protracted, from a long-term perspective, TMVR holds greater potential and is more likely to experience explosive market penetration compared with TMVr.

4Transcatheter Valve Replacement: Tendyne Poised for Launch, Intrepid Shows Early Promise, and “Three Major Hurdles” Lie Ahead

The First Major Challenge: Anchoring Technology—High Stability, Minimal Trauma, and Ease of Operation

Currently, mitral valve replacement products employ a wide variety of anchoring mechanisms. Despite this diversity, the core objectives of these anchoring strategies remain relatively consistent: to ensure stable implantation and minimize trauma to the mitral valve while reducing the complexity of the implantation procedure as much as possible. The anchoring methods used in investigational mitral valve implantation devices can be categorized into seven types: radial oversizing, annular barbs, annulus grasping, leaflet grasping, apical tethering, atrial anchoring, and subannular anchoring.

The Second Major Hurdle: Delivery Approach—Transapical First, Then Transfemoral; Size Reduction Is Key

The access routes for TMVR products are primarily categorized into two types: transapical and transfemoral venous approach with transseptal puncture. Among TMVR products, the transapical approach is the main focus of research and development. This is because the large valve size results in a bulky TMVR delivery system, making it difficult to enter the left atrium without causing any damage to the femoral vein. Furthermore, the development of long-distance, flexible steerable systems poses additional challenges for the delivery system. VCBeat believes that although the transfemoral venous route is the optimal path for TMVR, the transapical approach is likely to remain the mainstream access route until breakthroughs are achieved in prosthetic valve compression technology.

The Third Major Challenge: Valve Design—Dual Stents, D-Shaped Rings, Quadra-Leaflet Valves, and Retrievability; TMVR Products Employ Diverse Innovative Strategies

In the design of prosthetic heart valves, differences among various products are primarily concentrated in aspects such as shape, material, and retrievability. First, regarding shape, since the mitral valve is not a regular circle but rather D-shaped (saddle-shaped), companies such as Abbott and Medtronic have adopted a dual-stent structure—featuring an outer saddle-shaped stent and an inner circular stent—to reduce the risk of paravalvular leakage while meeting hemodynamic requirements. In terms of valve material, transcatheter mitral valve replacement (TMVR) products all utilize bioprosthetic valves, with bovine pericardium being the predominant material currently used. To lower the technical difficulty for physicians during surgical procedures, the retrievability of the valve before it is fully deployed has also become a key aspect of technological competition among products.

Unknown Peaks: Clinical Manifestations Are the Guiding Light for Product Improvement

The vast majority of surgical medical devices are born out of clinical needs and evolve in response to clinical challenges, with most innovations driven by well-defined problems. The iteration of transcatheter mitral valve replacement (TMVR) products is no exception. VCBeat Research Institute believes that, given the complex anatomy of the mitral valve, future TMVR products will continue to encounter numerous unpredictable clinical challenges. This, in turn, drives continuous innovation and iteration among TMVR-related companies. Competition in the TMVR sector has yet to enter an era of “incremental innovation”; new designs have the potential to bring about transformative changes to the competitive landscape. In the current phase, where challenges and opportunities coexist, clinical outcomes serve not only as the cornerstone for product commercialization but also as a guiding light for future innovation directions.

5Interventional Repair: MitraClip Leads the Pack, While Annuloplasty, Chordae Tendineae Repair, and Left Ventricular Reconstruction Remain Highly Challenging

The technological landscape for transcatheter mitral valve repair (TMVr) is highly diverse. Established techniques include Transcatheter Edge-to-Edge Repair (TEER), annuloplasty, and chordal repair, while emerging technologies under development include left ventricular reconstruction and coaptation enhancement.

TEER: Simple and Effective, Bringing Edge-to-Edge Repair Back into the Spotlight

As of November 2021, there were two transcatheter edge-to-edge repair (TEER) products for the mitral valve available on the global market: Abbott’s MitraClip (approved in Europe, the United States, and China) and Edwards’ PASCAL (approved only in Europe). The design of both medical devices evolved from surgical edge-to-edge repair techniques. The core principle involves performing edge-to-edge approximation of the mitral valve leaflets, either by creating a double-orifice configuration through coaptation of the A2/P2 segments or by approximating the A1/P1 or A3/P3 segments, thereby reducing the mitral valve orifice area to treat regurgitation.

Transcatheter Chordae Tendineae Implantation: Constrained by Access Routes and Indication Scope

Since the launch of NeoChord, the first transcatheter mitral valve chordae tendineae implantation device, in Europe in 2012, commercialization in the field of transcatheter chordae implantation has remained largely stagnant. Few chordae implantation products are currently under development in China. We believe this is primarily due to the relative rigidity of access approaches and the difficulty in expanding the breadth of indications.

Transcatheter Annuloplasty: Direct Remodeling Is Challenged by Technical Complexity, and Indirect Remodeling by Adverse Effects

Transcatheter mitral valve annuloplasty presents the highest technical difficulty and is primarily indicated for patients with mitral annular dilation who are unsuitable for open-heart surgical intervention. Transcatheter mitral valve annuloplasty can be further categorized into ring-based annuloplasty (direct annuloplasty) and suture-based annuloplasty (indirect annuloplasty). Despite the significant challenges in product development and the demanding requirements for procedural execution, multiple manufacturers are actively strategizing and advancing clinical validation, including VitaFlow Medical’s Amend, Boston Scientific’s IRIS, and MVRx’s Arto. There are substantial differences in design philosophies among various annuloplasty devices, with variations in access routes, anchoring mechanisms, and principles of annular reduction. As a mainstream direction for product iteration has not yet emerged, this niche sector offers opportunities for latecomers to achieve rapid advancement and competitive parity.

Enhanced Coaptation: A Highly Promising Innovative Repair Technology

Although transcatheter edge-to-edge repair (TEER) is currently the most successful reparative approach, it still has certain technical limitations; the “double-orifice” configuration of the mitral valve may lead to valvular stenosis. As an optimized solution, coaptation augmentation technologies, represented by HalfMoon, offer an innovative alternative—by restoring physiological coaptation of the diseased mitral valve, they reduce regurgitation without compromising the valve orifice area. In October 2020, Medtronic announced a strategic agreement with Foundry and ultimately acquired the HalfMoon device, which has completed its first-in-human trial. The HalfMoon system is delivered via the transfemoral venous approach and improves regurgitation by increasing the posterior leaflet area of the mitral valve while preserving the normal physiological function of the anterior leaflet. Additionally, products from POLARES (Polares Medical) and Sutra (Dura Biotech, the second-largest shareholder of Peijia Medical) are also under development.

Finally, we employ a commercial value assessment model to analyze the commercial potential of sub-segments within Transcatheter Mitral Valve Repair (TMVr). It is evident that Transcatheter Edge-to-Edge Repair (TEER) technology will likely cross the complexity threshold from top-tier hospitals to achieve large-scale adoption. Whether it can subsequently enter a phase of explosive growth depends on whether its procedural complexity can be further reduced to a level manageable by most Grade 3A hospitals. From the perspective of current domestic practice, innovative clipping mechanisms such as Dejin Medical’s Dragonfly and Hanyu Medical’s ValveClamp have further optimized ease of use; therefore, we remain optimistic about a continued reduction in the complexity of TEER procedures. However, annuloplasty techniques remain at a stage where even top-tier Grade 3A hospitals have not yet mastered them, posing a significant barrier to future adoption. Without emerging innovations in device design, annuloplasty will face substantial challenges. The primary issue with chordae tendineae repair is that the transapical approach requires the participation of cardiac surgeons. If the transfemoral approach can maintain low operational complexity, chordae repair is likely to cross the complexity threshold and enter a phase of scaled promotion driven by academic marketing. Nevertheless, its relatively narrow indications limit its long-term growth potential to some extent.

6Path Summary: TMV is the prevailing trend, with a primary focus on three key elements: clinical outcomes, indication coverage, and procedural complexity.

Based on the above analysis, we can summarize the following three major conclusions:

(1) Transcatheter Mitral Valve (TMV) intervention is a challenging yet correct endeavor and represents an inevitable trend. Although surgical repair remains the gold standard, this does not hinder TMV from rapidly expanding its market potential tenfold;

(2) TMVR and TMVr are essentially competing to see which can reach the “singularity” of explosive growth more rapidly along its respective development path. The primary threshold for TMVR is safety, requiring the overcoming of three major hurdles: anchoring, delivery systems, and durability; whereas the main threshold for TMVr lies in procedural complexity. From the current perspective, once transfemoral implantation technology for TMVR matures, it holds promise as the ultimate solution.

(3) Regarding repair pathways, it is currently certain that Transcatheter Edge-to-Edge Repair (TEER) will experience the most rapid growth, primarily due to its superior clinical efficacy, broad indication coverage, and relatively simple procedural operation. In contrast, clinical evidence for Transcatheter Mitral Valve Replacement (TMVR) remains generally limited. Currently, Tendyne has obtained CE marking first, owing to its exceptional safety profile. Meanwhile, Intrepid’s transfemoral delivery system is the most anticipated; with excellent 30-day data already reported, Intrepid is poised to become the benchmark product for transfemoral approaches if it maintains high levels of clinical performance.

Compared with the relatively clear tiered landscape in the TAVR field, the TMV sector is witnessing more intense competition. Over 20 domestic companies have entered the TMV space, rapidly catching up in pipeline progress. Particularly in the TEER segment, more than half of TMV companies have established a presence, suggesting that competition in this area will become extremely fierce (by contrast, only two products, MitraClip and PASCAL, currently remain in the overseas market). Given the inherent technical characteristics of the mitral valve field, we anticipate that the entire TMV sector will evolve into a protracted battle. From a long-term perspective, standing out will depend on original innovation, with patents serving as a critical barrier.

1Current Landscape: Over 20 Companies in Fierce Competition, TEER Takes the Spotlight, TMVR Poised for Breakthrough

Mitral Valve Sector Heats Up in China, with More Companies Participating than in TAVR

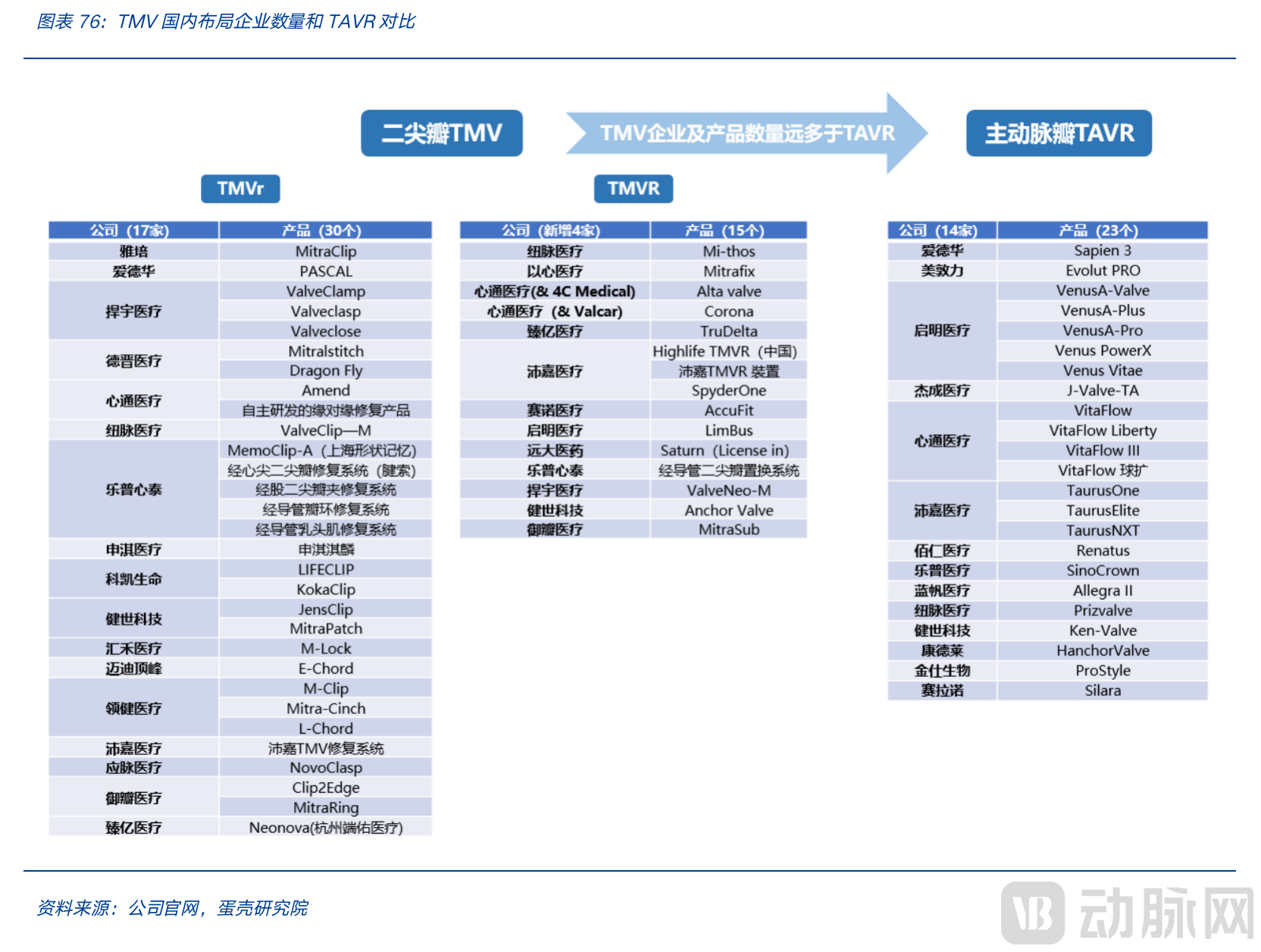

The domestic mitral valve sector is experiencing significant momentum, with the number of participants and product pipelines in transcatheter mitral valve (TMV) far exceeding those in transcatheter aortic valve replacement (TAVR). According to statistics from VCBeat Research Institute, a total of 21 companies (including two foreign enterprises: Abbott and Edwards Lifesciences) are active in the TMV field in China, with 45 TMV products in development. Of these, 30 are for transcatheter mitral valve repair (TMVr), and 15 are for transcatheter mitral valve replacement (TMVR). In contrast, only 14 companies (including two foreign enterprises: Edwards Lifesciences and Medtronic) are engaged in the TAVR sector, with a total of 23 TAVR products.

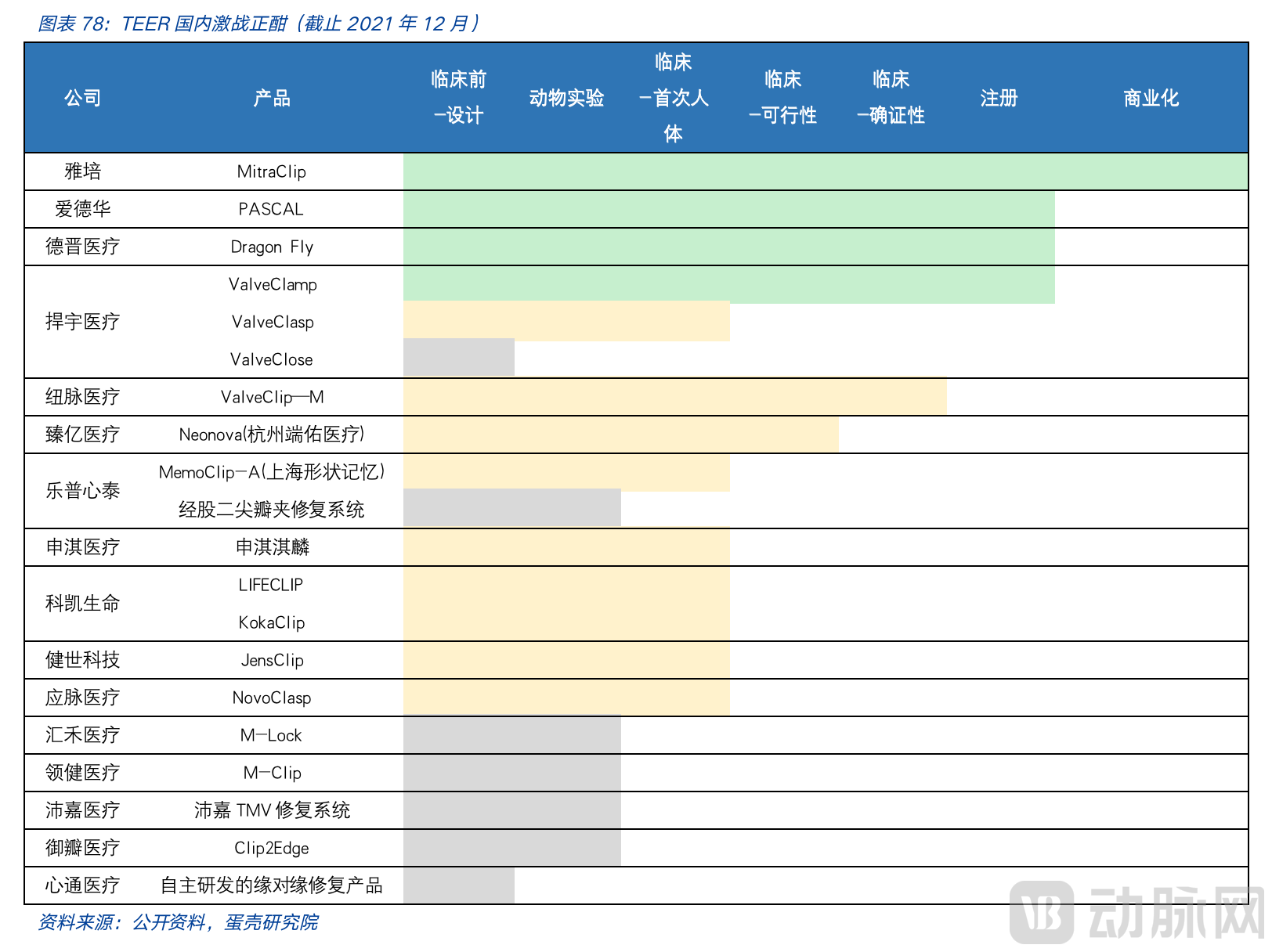

Domestic TMVr Repair Sector: TEER Track Becomes Crowded, Poised to Heat Up

Overseas, the TEER pathway was pioneered by Abbott’s MitraClip, which has accumulated over 140,000 implants, followed by Edwards Lifesciences, which reported a doubling of growth in 2021 with cumulative implants exceeding 4,500 cases. Currently, there are as many as 20 products (18 of which are domestically produced in China) competing in the TEER space in China, making the sector highly crowded. The core design philosophy of these products is largely derived from the surgical “double-orifice” technique, resulting in relatively low differentiation. The most advanced candidates are DragonFly by Dejin Medical and ValveClamp by Hanyu Medical.

MitraClip Secures First Approval in China; Domestic TEER Devices Poised for Rapid Growth and Potential Breakout

Unlike the TAVR market in China, where domestic companies have taken the lead, MitraClip was the first to achieve commercialization in the TMVr field. In 2021 alone, over 100 cases were implanted in China, marking a strong start for its initial promotion. MitraClip has already taken the lead in training skilled operators in China, which not only promotes its own adoption but also lays a solid foundation for similar products from domestic manufacturers. Once domestic products begin commercialization, their initial volume growth may be even faster, especially for DragonFly by Dejin Medical and ValveClamp by Hanyu Medical, both of which are currently leading in development progress. With strong support from top physicians, rapid post-launch promotion is expected.

TEER technology is relatively mature, and the preliminary efficacy of domestically produced products is non-inferior to that of MitraClip. After more than two decades of exploration, transcatheter edge-to-edge repair (TEER) has basically established a product iteration pathway dominated by clip-based devices, reaching a considerable level of maturity. Several TEER products awaiting market launch in China are already comparable to MitraClip in terms of detailed design and results from small-scale clinical trials. Although subsequent generations of MitraClip (e.g., G4) continue to undergo optimization, they have not yet obtained regulatory approval in China.

We can anticipate that starting in 2022, domestically produced edge-to-edge repair products will successively receive regulatory approval and enter the market. Leveraging strong promotion by leading physicians (Principal Investigators, PIs), sales volumes are expected to surge. Currently, Chinese manufacturers are jointly developing these products with multiple leading physicians, with collaborations spanning from R&D to commercialization. For instance, ValveClamp was co-developed by Shanghai Hanyu Medical and the team of Academician Ge Junbo from Zhongshan Hospital affiliated with Fudan University. The clinical studies for DragonFly were conducted by Dejin Medical in collaboration with several experts, including Professor Wang Jian’an from the Second Affiliated Hospital of Zhejiang University School of Medicine, Professor Chen Mao from West China Hospital, Academician Han Yaling from the General Hospital of Northern Theater Command, and Professor Zhou Shenghua from the Second Xiangya Hospital of Central South University. Furthermore, on May 6, 2021, Venus Medtech announced its investment in Dejin Medical. Venus Medtech holds a high market share and extensive hospital coverage in China’s TAVR market. Given current clinical study trends, physicians proficient in TAVR techniques will be the primary target group for the clinical promotion of TMVr products.

The R&D progress of domestic replacement products is on par with overseas counterparts, and they are expected to rank among the global leaders in the long term.

Currently, two domestically developed transcatheter mitral valve replacement (TMVR) products are leading the industry in R&D progress: MitraFix by MicroPort CardioFlow Medtech and Mithos by Nuomai Medical. Both have entered the product registration application stage. The two most advanced products both adopt a tri-leaflet bovine pericardial valve design. MicroPort’s MitraFix offers both transapical and transfemoral venous access routes, whereas Nuomai’s Mithos utilizes the transapical approach. Globally, among TMVR products under development, only Abbott’s Tendyne received CE Mark approval in Europe in February 2020; the U.S. FDA has not yet approved any such product for market launch. However, Chinese manufacturers’ products—MicroPort’s MitraFix and Nuomai’s Mithos—are on par with Edwards Lifesciences’ EVOQUE in terms of development progress, positioning them at the forefront globally. Their commercial launch is anticipated within the next one to two years.

2Strategic Landscape Analysis: TAVR Is a Blitzkrieg, TMV Is a Protracted War, and the Most Mature Technology, TEER, Remains in Its Prime After 18 Years of Growth

The competitive landscape of TMV differs from that of TAVR. If TAVR was a quick battle, the competition in the TMV sector is inevitably a large-scale “protracted war.” First, the overall design difficulty of TAVR is lower than that of TMV, allowing for faster iterative improvements and smooth, rapid clinical progress. In contrast, TMV has a higher failure rate than TAVR and slower iteration cycles. Second, along its development path, TAVR quickly achieved clinical outcomes non-inferior to those of surgical intervention. Coupled with its relatively simple operation, it rapidly entered a phase of large-scale adoption. Subsequently, growth became more dependent on platform and channel promotion capabilities. Once market leaders emerged, the industry quickly entered a “winner-takes-all” flywheel effect. Therefore, the TAVR competition resembled a swift campaign (as evidenced by Edwards’ significant lead in overseas markets), while opportunities for latecomers in the TAVR space stem more from differentiated positioning (e.g., targeting indications such as aortic regurgitation).

Compared with the relatively mature technology of TAVR, TMV cannot yet be compared with surgical outcomes. Various technical approaches are still competing for market share, and there are limited mature overseas models to reference (in fact, the global competition for original TMV technologies has been ongoing for nearly 20 years).

Global Perspective: Higher Failure Rate in Original R&D and Slower Iteration Than TAVR

The overall design complexity of TAVR is lower than that of TMV, with faster iterative improvements, smooth clinical progress, and rapid market adoption. However, the development history of TMV teaches us that long-term efforts are the norm, and R&D failures are commonplace. MitraClip, the only commercially available repair device, was approved in Europe as early as 2008. After 12 years of commercialization, its cumulative global implantations have just exceeded 140,000 cases—less than the annual implant volume of TAVR. Meanwhile, annuloplasty products under the repair approach, including Carillon, Cardioband, and Mitralign, were launched in Europe in 2009, 2015, and 2016, respectively, and the chordae tendineae technology product NeoChord was launched in Europe in 2013; none of these has achieved large-scale commercial application to date. The development of replacement devices has spanned many years, but most products failed midway due to high mortality rates observed in early clinical trials. Currently, only Abbott’s Tendyne system received European approval in February 2020. In short, the nearly 20-year arduous journey of TMV globally demonstrates that TMV is a protracted battle.

A Chinese Perspective on the Protracted War in TMV—While Technical Borrowing Shortens R&D Cycles, Fundamental Advancements Stem from Underlying Technology Iteration

Whether for transcatheter mitral valve repair (TMVr) or transcatheter mitral valve replacement (TMVR), the progress of product development relies on advancements in external sciences. The core objective of transcatheter repair products is to reduce operational difficulty for clinicians. In addition to considerations of the product’s own design mechanisms, the limited exposure of the surgical field (invisible to the naked eye) remains the most significant obstacle hindering transcatheter procedures. Only with qualitative leaps in imaging technologies, such as echocardiography, will the operational complexity of transcatheter procedures be reduced, thereby providing a stronger foundation for broader adoption. Although transcatheter replacement products involve less operational complexity compared to repair, the large size of prosthetic valves—particularly via the transfemoral approach—requires the delivery system to be minimized in size while maintaining multi-directional steerable flexibility. With future support from advances in engineering and materials science, the design of transfemoral replacement devices can become more “refined.”

Furthermore, regardless of whether the transapical or transfemoral approach is used, the pace of adoption remains constrained by external factors, ensuring that the competition will be protracted. With the transapical approach still serving as the primary battleground, interventional procedures rely on surgical assistance and cannot be performed independently by cardiologists, thereby slowing the clinical promotion of interventional devices. Although the transfemoral venous approach does not require surgical involvement and can be completed independently by cardiologists, the significant challenges in device R&D mean that overcoming these bottlenecks demands substantial long-term investment from manufacturers.

3Industry Trends: The Key Lies in Technological Innovation, with a Focus on Three Major Trends

The key to the development of transcatheter mitral valve (TMV) devices lies in technological innovation, which is primarily evolving along three major trends. First, surgical access is gradually shifting from transapical to transfemoral venous approaches. This transition significantly reduces the area of trauma, effectively lowering the incidence of severe postoperative adverse events and enabling more elderly, high-risk patients to receive treatment. Second, devices are evolving from complex to user-friendly designs; enhancing operational ease facilitates commercial adoption. Third, the field is moving from standalone procedures to combined interventions. The use of combination devices offers diversified solutions for patients with complex mitral valve pathologies while significantly improving therapeutic outcomes. Furthermore, original R&D innovation coupled with strategic M&A may be an essential pathway for companies to become international giants.

Transfemoral Vein Will Become the Ultimate Access Route

Access Route: From Transapical to Transfemoral. The transapical approach was the first to be applied in the field of transcatheter mitral valve (TMV) replacement, owing to its short target distance, lower procedural difficulty, ease of achieving coaxiality, and relatively simpler device development requirements. However, the two major drawbacks of the transapical approach are the continued need for surgeon involvement and the larger trauma area, which often leads to numerous postoperative complications. In contrast, the transfemoral approach can be performed independently by interventional cardiologists, significantly reducing trauma and enhancing safety, making it undoubtedly the optimal choice for patients. Nevertheless, the transfemoral approach imposes higher demands on device development, requiring not only a smaller delivery system but also multi-directional steerability. Therefore, the transapical approach is not an “active choice” but rather a “necessary compromise” at this stage. Once technological bottlenecks in transfemoral access are overcome, it will rapidly dominate the market.

Ease of Use Is the Key Determinant of Promotional Value

Procedure: From Complex to User-Friendly. When clinical efficacy and safety are comparable, ease of use becomes a key determinant of success. In the field of transcatheter interventions, transcatheter mitral valve replacement (TMVR) is more likely than transcatheter mitral valve repair (TMVr) to emerge as the ultimate solution, precisely due to its procedural convenience. Among the diverse array of TMVr interventional repair devices, only the MitraClip, which utilizes the transcatheter edge-to-edge repair (TEER) approach, has achieved commercialization. One of the primary reasons for this is that the “clip” procedure offers the greatest ease of use within the repair domain. Practice has proven that user-friendliness is the core element driving adoption value.

By comparing the approaches previously used in interventional repair, it is evident that non-edge-to-edge TEER (Transcatheter Edge-to-Edge Repair) procedures present significantly higher surgical difficulty, with transcatheter annuloplasty being the most technically challenging. Taking Edwards’ Cardioband system for direct annuloplasty as an example, the transcatheter approach lacks direct visual exposure of the surgical field, relying solely on echocardiographic guidance. The operator must advance a catheter-delivered band and densely deploy individual anchors along the annulus to achieve annular reduction through cinching of the band.

From the current landscape of interventional devices, the only mainstream technology commercially validated—"edge-to-edge"—has gradually been supplanted in the surgical field due to the dilemma of "double-orifice" formation. In contrast, within the transcatheter intervention domain, the "edge-to-edge" technique has made a comeback and emerged as the dominant approach, sufficiently demonstrating that the operational complexity of interventional devices has become the core bottleneck hindering product adoption.

Combined Device Application Is King; “Toolkit” Development Is the Prevailing Trend

Efficacy: From Monotherapy to Combination Therapy. The combined use of multiple transcatheter devices is a prevailing trend, with the “toolkit” approach offering diversified solutions for a broader range of patients with indications. Academic evidence has demonstrated that combination strategies yield superior outcomes compared to single-modality repairs—whether through pairwise combinations of the three mainstream repair techniques (edge-to-edge leaflet repair, annuloplasty, and chordal implantation) or through the combined application of transcatheter mitral valve replacement (TMVR) and LAMPOON (Laceration of the Anterior Leaflet of the Mitral Valve to Prevent Outflow Obstruction) to effectively prevent left ventricular outflow tract obstruction (LVOTO) and significantly improve survival rates. Given the unique complexity of the mitral valve, it is unrealistic to expect a single device to provide an all-in-one solution for all patient types; therefore, combination therapy will emerge as a more practical option.

(1) Annuloplasty plus edge-to-edge leaflet repair: Surgical studies have demonstrated that the combined approach yields superior outcomes compared to annuloplasty or edge-to-edge repair alone. In surgical clinical practice, 3-year follow-up data show that the recurrence rate of mitral regurgitation (MR) was as high as 21.7% in patients undergoing annuloplasty alone, whereas it decreased to 3.7% in those receiving combined annuloplasty and edge-to-edge repair. Furthermore, annuloplasty serves as the foundational technique for surgical repair. Surgical studies have also confirmed that the combined repair of edge-to-edge approximation plus annuloplasty is superior to edge-to-edge repair alone, as evidenced by lower rates of MR recurrence and reoperation—20% for the combined procedure versus 57% for edge-to-edge repair alone.

(2) Annuloplasty plus chordae tendineae implantation. For instance, the successful combined use of the Edwards Cardioband and NeoChord systems in the United States has demonstrated proven efficacy. The patient presented with severe mitral regurgitation due to chordal rupture in the P2 segment and annular dilation (anteroposterior diameter of 42 mm), with a left atrial index (LAI) of 1.02. Cardioband annuloplasty was performed first, followed by the implantation of three NeoChord artificial chordae into the P2 segment. Repair using NeoChord alone only reduced mitral regurgitation (MR) to a moderate level, whereas the combined use of both interventional devices resulted in near-complete resolution of regurgitation.

(3) Leaflet edge-to-edge repair combined with chordae tendineae implantation. For instance, the efficacy of combining edge-to-edge repair with transapical NeoChord chordae tendineae implantation has been confirmed. Furthermore, domestic manufacturers have introduced innovative devices for combined procedures; Dejin Medical’s Mitralstitch integrates both edge-to-edge repair and chordae tendineae implantation into a single system. This significantly expands the range of indications and patient populations covered, not only sparing patients the distress of multiple surgeries but also better preserving the native physiological structure of the mitral valve, thereby achieving superior clinical outcomes.

(4) TMVR + LAMPOON. Additionally, transcatheter valve replacement manufacturers can integrate complementary auxiliary technologies to mitigate severe postoperative adverse events associated with valve replacement, thereby providing patients with more optimized bundled solutions. Comparative results from multiple academic studies have confirmed that LAMPOON enables patients at risk of left ventricular outflow tract obstruction (LVOTO) to undergo transcatheter mitral valve replacement (TMVR). Postoperative outcomes in this group were not only superior to those in the non-LAMPOON group but also exceeded those in the surgical control group: the 30-day survival rate for patients receiving LAMPOON was 93%, representing a substantial improvement over the 38% 30-day survival rate observed in LVOTO patients who did not receive LAMPOON, and significantly higher than the 73% 30-day survival rate associated with surgical leaflet resection.

Original Innovation + Inorganic Growth Through M&A: The Inevitable Path for Global Giants

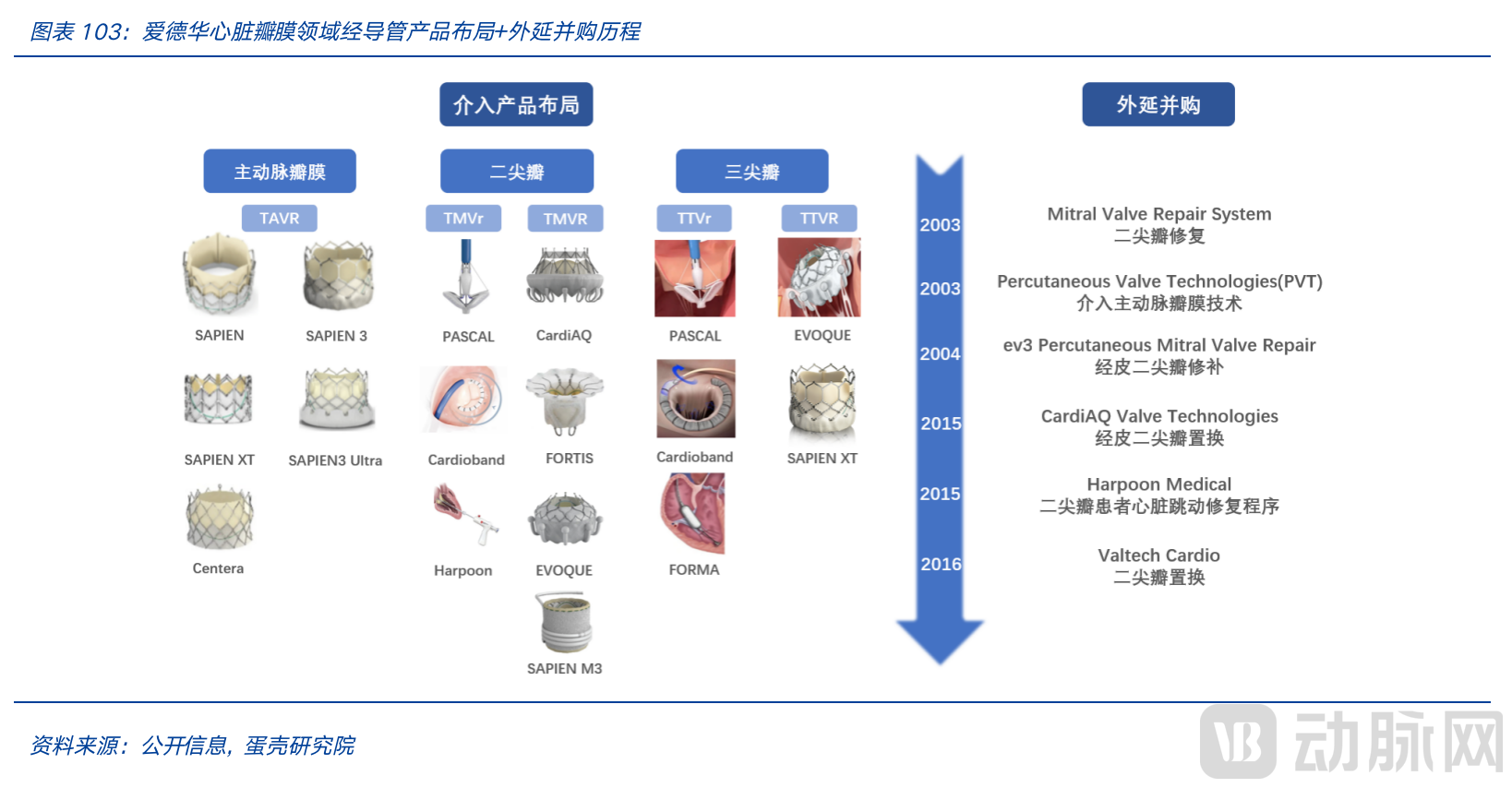

Original R&D innovation plus inorganic growth through M&A is the inevitable path to becoming a global giant. Most innovations by Chinese TMV companies are incremental in nature, with an overall lack of original concepts and related patent portfolios. From a long-term perspective, original innovation or global R&D and acquisitions may be essential for securing a foothold in the international market. Edwards Lifesciences, a leader in the heart valve sector, serves as a classic example. In this report, we provide only a brief overview without extensive analysis, as Edwards’ growth trajectory warrants a dedicated in-depth report.

1Methodology: DCF Valuation by Technical Pathway

We continue to employ the discounted cash flow (DCF) method for valuing companies in this industry sector. For the transcatheter mitral valve (TMV) industry, the primary challenge in applying DCF lies in the potentially divergent future trajectories of different technological approaches. Consequently, it is inappropriate to make broad, generalized forecasts of future revenue scale, net profit margin, and discount rate for TMV as a whole; instead, analysis should be conducted separately for each specific technological pathway.

First, the landscapes facing TMVR and TMVr differ, necessitating separate consideration. Second, within TMVr, TEER demonstrates the highest development certainty and strong predictive reliability. In contrast, areas such as chordae tendineae repair, annuloplasty, left ventricular (LV) reconstruction, and leaflet edge repair exhibit extremely high uncertainty. Logically, we are more optimistic about annuloplasty (provided that procedural complexity is significantly reduced). Although leaflet edge repair holds the greatest promise, it lacks sufficient clinical evidence at present and is therefore unsuitable for direct valuation using discounted cash flow (DCF) analysis. We believe a reasonable approach is to categorize TMVr into TEER and non-TEER modalities, and to roughly assume that one technology pathway among the non-TEER options may emerge to rival TEER. Consequently, the aggregate valuation of all non-TEER pathways is assumed to be approximately equivalent to that of TEER. This assumption represents our best estimate based on current understanding, although it inevitably has limitations.

2Valuation: TEER, TMVR, and Others

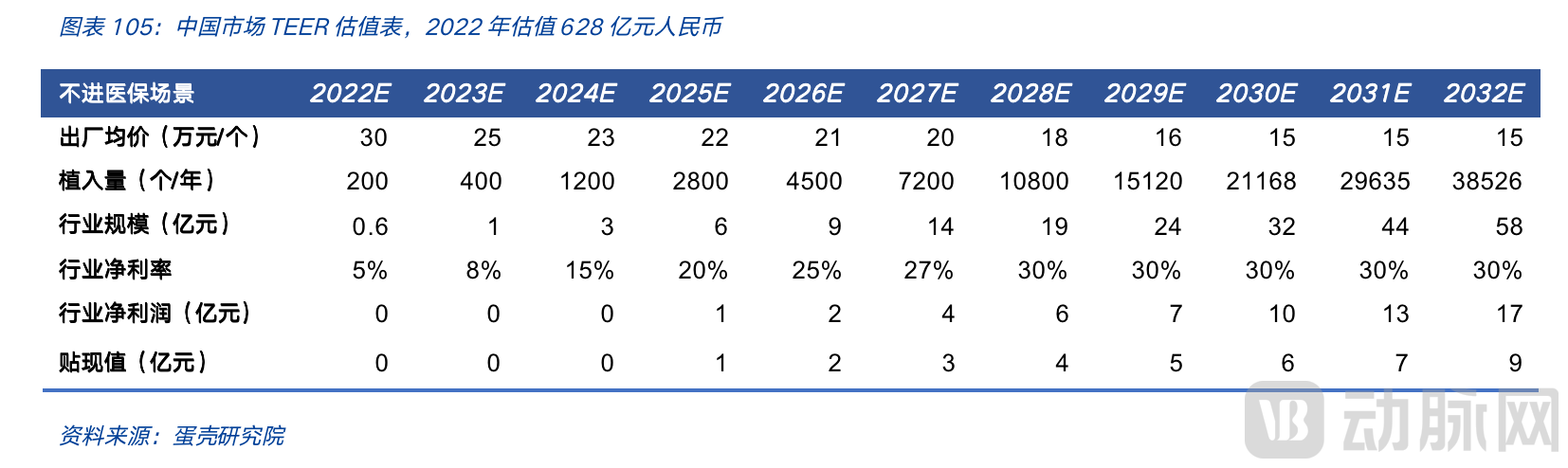

Currently, only TEER can provide a relatively accurate valuation range, and data from MitraClip and Edwards PASCAL can offer reliable references for predicting future development progress.

Based on U.S. MitraClip sales data and current domestic conditions, we have provided corresponding forecasts for pricing and implantation volume, projecting that the industry’s overall net profit margin will stabilize at approximately 30% by 2028. Transcatheter Edge-to-Edge Repair (TEER) is currently not considered under the scenario of centralized volume-based procurement by national medical insurance; its 2022 discounted cash flow (DCF) valuation stands at RMB 62.8 billion, approaching the valuation level of the transcatheter aortic valve replacement (TAVR) industry.

Based on the current progress of transcatheter mitral valve replacement (TMVR) in China, we anticipate that commercial promotion of TMVR will most likely commence in 2023. Our first-year forecast is relatively conservative; however, if clinical outcomes remain favorable, subsequent growth is expected to accelerate. We believe that due to the high technical barriers associated with TMVR products, the market landscape will remain an oligopoly. Pricing is expected to be higher than that of transcatheter aortic valve replacement (TAVR) and transcatheter edge-to-edge repair (TEER), with relatively smaller price reductions. The industry’s net profit margin is projected to be slightly higher than that of TEER, at 35%. Based on these assumptions, the estimated valuation of the TMVR sector in 2022 is RMB 91.3 billion (the valuation table only displays forecasts for the next 10 years; subsequent data are not presented in this report).

For the valuation of other technological pathways, we make a simple assumption in this report: that these alternative approaches will yield products comparable in excellence to TEER. Accordingly, the aggregate valuation of these other pathways is assumed to equal that of TEER, i.e., approximately RMB 63 billion. In subsequent studies in this series, should more precise valuation data become available, we will conduct separate valuations for specific sub-segments, including annuloplasty, chordae tendineae repair, left ventricular (LV) reconstruction, and coaptation enhancement.

3Key Drivers: Registration Time, Promotion Speed, Duration, Price Reduction Magnitude

DCF valuation for TMV is highly challenging, with significant uncertainty and numerous factors that could substantially impact the valuation outcome.

First, the timing of product registration and commercialization.With the imminent launch of domestic transcatheter edge-to-edge repair (TEER) products in China, characterized by high certainty, relatively mature technology, and stable expected clinical outcomes. In contrast, only Tendyne has received CE certification for transcatheter mitral valve replacement (TMVR) globally, with no products yet approved by the FDA. The timeline for true commercialization remains highly uncertain; overseas, the first transfemoral TMVR device is not expected to gain approval until after 2026. Domestically, however, CardiacCare Medical and Nuomai Medical have already entered the registration phase for their TMVR products. Therefore, we predict that commercialized TMVR products will emerge in China in 2023. Naturally, any acceleration or delay in registration and commercialization timelines will impact the discounted cash flow (DCF) valuation of the TMVR sector (each one-year delay results in a 6% loss in DCF valuation).

Second, the speed of product promotion.Currently, the adoption trajectory of Transcatheter Edge-to-Edge Repair (TEER) can be broadly assessed given the precedents set by MitraClip and PASCAL. In contrast, Transcatheter Mitral Valve Replacement (TMVR) currently lacks comparable benchmark products. Considering that TMVR is more technically challenging than Transcatheter Aortic Valve Replacement (TAVR), we project its future growth rate to be lower than that of TAVR. However, as the patient population eligible for TMVR is more than five times larger than that for TAVR, its peak sales and duration of growth are expected to exceed those of TAVR.

Third, the increasing duration of growth.We believe that the overall market for the TMV sector will continue to grow and surpass that of TAVR, primarily because its target patient population is more than five times larger than that of TAVR, which will be reflected in peak implantation volumes and sales figures far exceeding those of TAVR.

Fourth, the magnitude of future price reductions will also impact sector valuations.Given the significant uncertainties in the transcatheter mitral valve (TMV) sector, we will not consider the potential impact of national centralized volume-based procurement for now. Instead, we will assess the price reductions driven by competition solely from the perspective of the industry landscape. The magnitude of these price cuts will significantly affect the valuation levels within this sector.

Due to space constraints, this report does not present the full text. To read the complete article, please scan the mini-program code below.

Disclaimer: The intellectual property rights of the content published by VCBeat are exclusively owned or held by VCBeat and the relevant rightsholders. For reprinting, please contact tg@vcbeat.net.