Medical IPOs Lose Nearly RMB 400 Billion in Market Value in 2021 as Break-Issue Becomes the Norm

“Is it winning the lottery or getting shot?” After suffering consecutive setbacks in IPO subscriptions at the end of 2021, one investor appeared somewhat resigned.

In China’s capital markets, the distorted pattern of “new stocks never fail,” which lacks fundamental logical underpinnings, has persisted for a long time. Thus, when Cofoe Medical Technology dropped 4.43% on its first day of listing, it cracked open this illusion. Subsequently, Chengda Biologics, Hualan Pharmaceutical, Dizal Pharmaceutical, and Nanjing Model Biology all broke their issue prices, with declines deepening further. Market sentiment turned abruptly pessimistic, as each instance of breaking the issue price seemed to foreshadow the bursting of a bubble in a particular sector. From low-value consumables to innovative drugs, growth narratives have come under scrutiny, and even model organisms, once at the forefront of market enthusiasm, are now facing intense questioning.

Indeed, in 2021, as various internal and external dividends approached their end and capital became more market-oriented, market capitalization growth was no longer easily attainable. In 2021, 98 medical companies from China listed on global capital markets, with 25 breaking their issue price and 75 experiencing negative growth in their first year of trading post-IPO. Both fundraising amounts and market capitalizations were compressed compared to the previous year. However, the IPOs of medical stocks in 2021 were not merely sensational.

Wealth-creation myths persist. In late June, Nanomicro Tech listed on the STAR Market of the Shanghai Stock Exchange, with its share price surging by as much as 1,400%, temporarily triggering trading halts and making it the second-strongest new listing in the history of China’s A-share market to more than decuple on its first day of trading in the past two decades. In August, Sino Biological Inc. debuted on the ChiNext board, with an issue price of RMB 292.92 per share and a closing gain of 81.27%. Investors who were allocated shares in the initial public offering and sold them at high prices on the first trading day could net approximately RMB 150,000 per winning lottery unit, marking the most lucrative IPO allocation (“meaty ticket”) in the history of the A-share market.

Still a Paradise for Innovators. At the beginning of the year, New Horizon Health listed on the Hong Kong Stock Exchange, with its market capitalization surging to nearly HK$30 billion, pushing the hype around early cancer screening to its peak. Starting in April, star internet healthcare projects such as WeDoctor, LinkDoc Technology, Zhiyun Health, Simpai Health, and Yuanxin Technology successively filed their prospectuses. Under their respective innovation frameworks, they have validated business models, demonstrating the potential for sustained and rapid revenue growth. Meanwhile, medical AI vendors, having sequentially obtained product registration certificates, have embarked on intensive IPO journeys. In March, June, and September, Keya Medical, Infervision, and Shukun Technology filed their prospectuses, respectively. In November, Airdoc rang the opening bell on the Hong Kong Stock Exchange, becoming the first publicly traded medical AI company. Although this enthusiasm appears somewhat inverted compared to the fervor seen in the primary market, it nevertheless marks a significant milestone in the arduous progress of medical AI.

Our original aspiration remains unchanged. While the ups and downs of details are worth savoring, moving forward requires a deeper investigation into the underlying causal relationships.

It must be acknowledged that in 2021, the macroeconomic environment for initial public offerings (IPOs) of healthcare companies had been irreversibly altered compared to 2020.

First, the range of options in capital markets has narrowed. On one hand, economic uncertainty stemming from the global spread of the COVID-19 pandemic, coupled with policy red lines imposed by increasingly stringent data regulations, has led most healthcare companies to temporarily abandon plans for U.S. listings. On the other hand, market conditions on the Hong Kong Stock Exchange (HKEX) are deteriorating and may continue to worsen. In 2021, the Hang Seng Index and the Hang Seng TECH Index, which represent the overall performance of Hong Kong stocks and Hong Kong tech stocks respectively, fell by 13.7% and 32.7%, making them the worst-performing major indices globally that year. Against this backdrop, 14 out of the 35 healthcare companies newly listed on the HKEX saw their share prices fall below the IPO price on the first day of trading, resulting in a break-issue rate as high as 40%. Throughout the year, 30 companies experienced a shrinkage in market capitalization. Even firms that had established strong competitive positions, such as Kindstar Globalgene, Broncus Holding, MicroPort NeuroTech, and CARsgen Therapeutics, were unable to escape the fate of breaking their issue prices.

In fact, prior to the pricing mechanism reform on the Shanghai Stock Exchange’s STAR Market in September, all newly listed stocks that fell below their IPO price originated from the Hong Kong Stock Exchange. However, the performance of the Hong Kong stock market is relatively weakly correlated with the intrinsic value of companies and is more heavily influenced by monetary liquidity. To elaborate, as a typical offshore financial center, the Hong Kong Stock Exchange exhibits a high degree of globalization in capital allocation. Statistics show that in 2021, mainland Chinese capital accounted for no more than 20% of the funds traded on the Hong Kong Stock Exchange. This implies that pricing power in the Hong Kong market is held by the remaining 80% of capital, which flows freely across global capital markets. These profit-seeking, risk-averse liquid funds are primarily based in the two major U.S. stock exchanges; amid the uncertainty created by the COVID-19 pandemic, it is easy to imagine the challenges they faced in maintaining long-term positions.

Therefore, the downturn in the Hong Kong stock market in 2021 is highly likely to extend into 2022. This may also be one of the reasons why a large number of internet healthcare and medical AI companies that had already filed with the Hong Kong Stock Exchange have delayed their IPO progress; indeed, it is not an opportune time for IPOs in the Hong Kong market at present.

Intraday Price Movement of a Hong Kong-Listed Healthcare Stock on Its IPO Day

In other words, healthcare companies pursuing initial public offerings (IPOs) will most likely need to choose from the A-share market. Data from 2021 shows that the majority opted for the STAR Market; however, the most profound changes are now unfolding within the STAR Market itself.

First, it will become the norm for a certain proportion of new listings on the STAR Market to break their issue price. In September 2021, with the introduction of new regulations such as the Implementation Measures for the Issuance and Underwriting of Stocks on the Shanghai Stock Exchange STAR Market and the Guideline No. 1 on the Application of Issuance and Underwriting Rules of the Shanghai Stock Exchange STAR Market—Initial Public Offerings, the pricing mechanism for new STAR Market listings was liberalized. Previously, bids falling within the highest 10% were excluded as invalid prices. To secure allocations in new share offerings, institutional investors often submitted lower bids or engaged in coordinated bidding, thereby leaving room for post-listing price appreciation. Under the latest inquiry rules, the exclusion rate for the highest bids has been reduced to 3%. This change has disrupted the former “buyer’s market” dominated by offline investors, empowering lead underwriters (i.e., investment banks) to better exercise their autonomous pricing authority. As a result, investment banks are now more emboldened to set higher offer prices and earn greater underwriting fees.

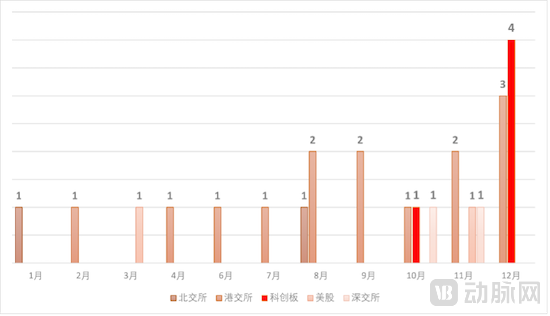

Number of Healthcare IPOs Trading Below Issue Price Across Capital Markets in 2021

In fact, the five instances of medical IPOs on the STAR Market breaking their issue price in 2021 all occurred after the introduction of new inquiry regulations. For example, Chengda Biology, the first medical stock newly listed on the STAR Market, raised its per-share offering price from RMB 50 to RMB 110 during its initial listing in October, increasing the funds raised from RMB 2.04 billion to RMB 4.582 billion, and closed with a 27.27% decline. This pattern was identical to the subsequent breakage of issue prices by Nanmo Biology and Hualan Biology.

Prior to this, upstream biotechnology “picks-and-shovels” providers such as Vazyme, Sino Biological, Aladdin, and Titan had all become star stocks highly sought after by investors. Among them, Sino Biological and Vazyme saw their share prices rise by 68% and 55%, respectively, on their debut trading days, setting the tone for valuation increases in this year’s hottest sector. However, Shanghai Model Organisms Center priced its IPO at a price-to-earnings (P/E) ratio of 100 times, significantly higher than the industry average, laying the groundwork for its subsequent break below the issue price. Meanwhile, Hualan Pharmaceutical, a leading domestic provider of pharmaceutical rubber stoppers for high-end injectable drugs and one of the earliest entrants in this field in China, delivered strong financial performance. According to its prospectus, Hualan Pharmaceutical projected revenue of approximately RMB 570 million to RMB 700 million for the first three quarters of 2021, representing a year-on-year increase of 88% to 130%; net profit attributable to shareholders was expected to range from RMB 160 million to RMB 200 million, up 217% to 288% year on year. As the second most lucrative IPO subscription (“big meat ticket”) of the year, its post-IPO drop below the offering price was likewise driven by an elevated P/E ratio of 101.4 times.

Second, the bar for listing on the STAR Market has been raised. In February 2021, the China Securities Regulatory Commission (CSRC) issued the *Regulatory Rules Application Guidelines—Disclosure of Shareholder Information for Companies Applying for Initial Public Offerings*, which explicitly required an extension of the lock-up period for new shareholders and emphasized the completeness and accuracy of information disclosure. This has dampened the enthusiasm of private equity investors who entered at the pre-IPO stage for short-term gains, increasing the difficulty of IPO preparations in the short term. However, it ensures the stability of companies’ shareholding structures, which is more conducive to long-term operations.

In April, the China Securities Regulatory Commission (CSRC) released the revised “Guidelines for Evaluating Sci-Tech Innovation Attributes (Trial),” changing the evaluation metrics to a “4+5” framework. This move further strengthened and quantified the technological and innovative requirements for the STAR Market, causing companies that failed to meet the standards to either withdraw their applications or face outright rejection. According to incomplete statistics from VCBeat, nearly 20 healthcare companies terminated their STAR Market listing processes in 2021, with nearly half being unprofitable innovative drug developers. The number of companies applying for listings on the STAR Market dropped by more than half compared to 2020.

In fact, even if unprofitable innovative pharmaceutical companies successfully go public, they may face the risk of delisting if they lack subsequent industrialization capabilities. The “strictest” new delisting rules for the STAR Market, released in December 2020, clearly stipulate that a company must achieve annual revenue of RMB 100 million within four years from its listing date; otherwise, it will be delisted.

For most enterprises aspiring to build enduring legacies, an initial public offering (IPO) is an inevitable milestone in their growth trajectory. However, amid the current landscape—where overseas listings face uncertain prospects, scrutiny on the STAR Market intensifies, the Beijing Stock Exchange remains nascent, activity on the ChiNext Board lacks vigor, and main board listing thresholds remain high—medical companies are being compelled to strengthen their core competencies. This pressure may well prove to be a blessing in disguise.

Having discussed the more abstract topics of liquidity and pricing, we now return to the core issue of corporate value.

An investor once candidly stated in a media interview that a common characteristic among companies experiencing severe post-IPO price declines is deteriorating financial performance. In his view, underwhelming fundamental performance is another key factor contributing to stocks trading below their IPO offering prices. According to China Merchants Securities’ interpretation of the third-quarter reports, overall earnings growth in industries represented by these broken-issue stocks has slowed, with corporate third-quarter results falling short of expectations. Taking Cofoe Medical, one of the earliest A-share companies to trade below its IPO price in 2021, as an example, its operating revenue in the first half and third quarter of 2021 decreased by 10.50% and 2.51% year-on-year, respectively, while net profit attributable to shareholders of the parent company declined by 20.97% and 8.13%, respectively.

As the dividends from innovation narratives near their end, profitability has become a Damocles’ sword hanging over newly listed healthcare stocks. Among healthcare companies that went public in 2021, innovative drug developers (15 IPOs), high-value consumables manufacturers (15 IPOs), and biopharmaceutical firms (including generic drugs and active pharmaceutical ingredients, 14 IPOs) were the hottest sectors. Similar to the previous year, innovative drug IPOs continued to command the highest average market capitalization, followed by IPOs of high-value consumables companies, represented by vascular intervention and orthopedic products. Biopharmaceutical companies, whose average market capitalization was only one-quarter that of innovative drug firms and half that of high-value consumables companies, saw a surge in IPO activity in 2021, with their market capitalization change slightly better than the average (-24.75%).

Overview of the Top 3 Subsectors by Number of Healthcare IPOs Across Capital Markets in 2021

Among the 15 innovative pharmaceutical companies that went public in 2021, eight were not yet profitable. Six high-value medical consumables companies were unprofitable, while only one biopharmaceutical company was unprofitable. These unprofitable biotech enterprises accounted for the vast majority of the RMB 400 billion in market capitalization lost by newly listed healthcare stocks throughout the year.

Taking Broncus Medical, known as the “first stock in pulmonary intervention,” as an example. By sales volume, Broncus Medical holds a 43.2% market share, ranking first; by sales revenue, it ranks second with a 37.5% market share but has yet to achieve profitability. On its IPO debut, the company’s share price dropped by 19.7%, and as of press time, its market capitalization had shrunk by 43.4%, reflecting a representative performance in the capital markets.

Concerns in the capital market regarding Broncus Medical may also stem from its less-than-optimistic growth prospects. According to the prospectus, in 2019, Broncus Medical’s average selling price per navigation system was $127,900, with 49 units sold; in 2020, it dropped to $119,900, with only 18 units sold; and from January to April 2021, it further declined to $84,900, with merely 10 units sold. The interventional pulmonology market targeted by Broncus Medical remains largely undeveloped and small in scale, albeit with a high growth rate. Regarding navigation systems, Frost & Sullivan data indicate that in 2020, the market size for interventional pulmonology navigation devices in China was only $6.9 million (approximately RMB 44.6 million), with sales of just 27 interventional pulmonology navigation platforms. The market grew at a compound annual growth rate (CAGR) of 68.9% from 2016 to 2020 and is projected to reach $189 million by 2025, suggesting a relatively limited ceiling.

A similar scenario is unfolding in the initial public offerings (IPOs) of innovative drug companies. Zhaoko Ophthalmology, spun off from Lee’s Pharmaceutical, has a product pipeline that is largely in the early stages of research and development and clinical testing. Among its candidates, only one product—Cyclosporine A Ocular Gel, an innovative therapy for dry eye disease—is expected to achieve commercialization by the end of 2021. However, the competitive landscape for this drug is challenging. Its benchmark product, Restasis, was launched globally in 2003, while Shenyang Xingqi Pharmaceutical’s comparable product, “Zirun,” entered the Chinese market in 2020. Additionally, there are other competitors in the market, including Harbour BioMed, Hengrui Medicine, and Beijing Vigenere Biotechnology. In comparison, Zhaoko Ophthalmology’s progress has been relatively slow. On its IPO day, Zhaoko Ophthalmology’s share price fell by 14.76%, and as of press time, its market capitalization had shrunk by 63.6%.

The other side of the coin is represented by biopharmaceutical companies that went public in 2021. A common characteristic among these enterprises is their possession of production capacity for one or more active pharmaceutical ingredients (APIs). Empowered by the Marketing Authorization Holder (MAH) system and centralized drug procurement, these companies—once minor players with little bargaining power in the industry chain—have gradually strengthened their position and extended downstream. Their sustained profitability and stable operational style have made them highly favored in a capital market characterized by continuously decreasing risk appetite.

Take Huiyu Pharmaceutical as an example. In November 2018, the Chinese government launched the "4+7" centralized volume-based procurement program for pharmaceuticals. Huiyu’s pemetrexed disodium, being the only product that had passed the consistency evaluation, won the exclusive bid by undercutting the originator manufacturer, Eli Lilly, with a 65% price reduction. It subsequently secured another winning bid in the centralized procurement for alliance regions. Since then, Huiyu Pharmaceutical has experienced explosive growth in its performance.

According to the prospectus, Huiyu Pharmaceutical’s total revenue was only RMB 50.8975 million in 2018. In 2019, however, its performance surged dramatically, with total revenue reaching RMB 655 million, representing a 22.6-fold increase. By 2020, revenue grew by another 1.89 times year-on-year, hitting RMB 1.236 billion. Within just three years, the company rose from being a minor player in the pharmaceutical industry to a mid-sized enterprise. The single product pemetrexed disodium served as the core engine behind Huiyu Pharmaceutical’s explosive growth, accounting for over 90% of revenue from 2019 to 2020. In 2020, sales of this product reached RMB 1.236 billion, constituting 91.02% of total revenue. On its listing day, Huiyu Pharmaceutical’s stock price rose by 1.9%.

From concept to practice, the downward shift of market trends has brought occasional growing pains, but for enterprises themselves, it also serves as a form of tempering.

In October 2021, Sun Piaoyang, who returned to the spotlight after Hengrui Medicine’s market capitalization plummeted by nearly half, stated at an R&D Day event, “I develop drugs purely out of interest and pay little attention to the capital markets.” Although this remark was sharp, it somewhat echoed the sentiments of many entrepreneurs. In late December, Kintor Pharmaceutical’s stock price experienced a cliff-like decline following the failure of the U.S. Phase III clinical trial of its COVID-19 drug, proxalutamide, and as peers rushed to distance themselves from the company. On the day the stock price fell back to its level from one year prior, Tong Youzhi, Chairman of Kintor Pharmaceutical, posted on his WeChat Moments, stating that “Kintor will remain Kintor,” and emphasizing that the company was vigorously advancing two international multicenter clinical trials targeting non-hospitalized and hospitalized patients, respectively, projecting firmness and confidence.

If one must identify the highlight of healthcare IPOs in 2021, it undoubtedly centers on the upstream segment of the biotechnology supply chain that has been subject to critical bottlenecks.

IPOs and Market Performance in the Upstream Biotech Industry Chain in 2021

In late June, NanoMicro Tech went public, marking the debut of China’s first listed company specializing in nanospheres. Its stock price surged as much as 12-fold at one point, instantly igniting investment enthusiasm for upstream raw materials in the biotechnology sector. Sino Biological, which focuses on providing a diverse portfolio of recombinant proteins, held its IPO in August; Biopss, also specializing in recombinant proteins, listed in October; and Vazyme, a leading Chinese manufacturer of enzymes, completed its IPO in November. All these companies achieved strong initial performances in the capital market despite adverse conditions.

Behind the rush of capital are abundant commercial orders that necessitate continuous capacity expansion, and technological breakthroughs finally achieved after years of being constrained by bottlenecks.

Taking the microspheres provided by Nanomicro Tech as an example, this essential raw material for reagents has a diameter smaller than that of a human hair. Nanospheres typically refer to microspheres with particle sizes ranging from 1 to 100 nm, at which scale their properties undergo significant changes. The precise fabrication of microspheres, along with the accurate control of particle size, pore size, and surface properties, requires highly sophisticated technologies. Once precision reaches the nanometer and micrometer levels, the manufacturing of high-performance microspheres becomes as challenging as chip fabrication, making technological breakthroughs difficult to achieve in a short period. The long-term technological monopoly held by overseas companies has resulted in a highly concentrated supply market. Previously, microspheres required by domestic biopharmaceutical companies and nuclear power plant water treatment systems were largely dependent on imports. Nanomicro Tech specializes in the localized provision of high-performance microspheres that rival imported products in quality, indicating substantial market demand.

Sino Biological and Vazyme provide precisely what downstream innovative drug developers and IVD companies urgently need. For instance, Sino Biological currently produces and sells over 47,000 types of off-the-shelf products, including more than 6,000 recombinant proteins—of which over 3,800 are expressed in human cells—and approximately 13,000 antibodies, including around 4,600 monoclonal antibodies. Its product portfolio spans multiple areas of life science research, offering a “one-stop” procurement channel for biological reagents and related technical services to support basic scientific research in molecular biology, cell biology, immunology, developmental biology, and stem cell research, as well as innovative drug development.

If we were to return to the starting point of 2021, while some might have anticipated the cooling enthusiasm for innovative drugs and high-value consumables that were once in the spotlight, the rapid rise of upstream companies such as Nanomicro Tech, Sino Biological, and Vazyme—becoming bright spots amidst an otherwise dismal year for healthcare IPOs—came as a surprise. The nearly RMB 400 billion erosion in market capitalization among healthcare IPOs in 2021 sent a clear signal: the industry needed to delve deeper into genuine demand and strengthen its capabilities in product and service supply.