U.S. Digital Health Market Raises $29.1 Billion in Record-Breaking 2021

How long does it take to break the annual record for total investment and financing? For the U.S. digital health market, the answer is six months.

As early as six months ago, data from the digital health fund Rock Health showed that the U.S. digital health sector saw 372 financing and investment deals totaling $14.7 billion in the first half of 2021, breaking the total funding record for any previous year.

The outbreak of the COVID-19 pandemic has, on one hand, posed significant challenges to healthcare services, while on the other, it has presented unprecedented opportunities. In 2020, investment and financing in the U.S. digital health market surpassed $10 billion for the first time. Some argue that the development of digital health in 2020 was largely driven by physical distancing measures imposed due to the pandemic, and that as epidemic prevention becomes normalized, people will increasingly return to in-person treatment. In this view, digital health services may ultimately serve as a value-added supplement rather than a direct substitute. However, certain indicators suggest that the U.S. digital health market may establish a “new normal” characterized by sustained acceleration. According to Rock Health’s 2021 Digital Health Consumer Adoption Survey, 73% of telehealth users expect to continue using telehealth at the same or higher frequency in the future. Among respondents who have a primary care provider (PCP), 80% reported that their PCP offered telehealth services in 2021, up from 44% before the pandemic. Additionally, research by EY indicates that 60% of physicians plan to continue providing care via telehealth after the pandemic ends.

On January 10, Rock Health released the latest data for 2021. That year, the U.S. digital health sector surged forward like an arrow loosed from a bow, showing no signs of slowing down. This article distills, translates, and synthesizes the key insights from the Rock Health report.

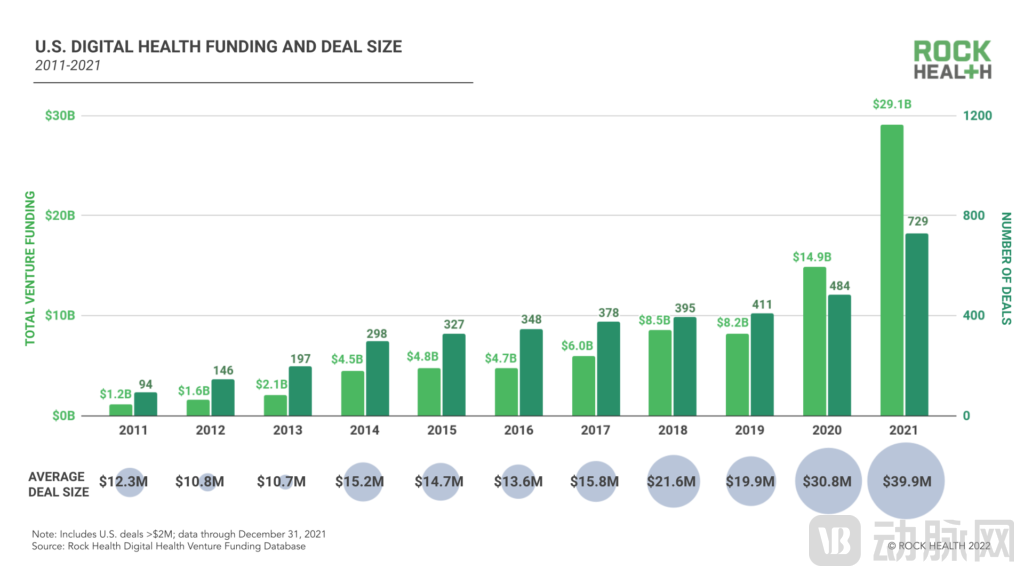

U.S. digital health startups raised a total of $29.1 billion across 729 deals in 2021, with an average deal size of $39.9 million, bringing the total funding to nearly double that of 2020.

Total Funding Amount and Number of Transactions in the U.S. Digital Health Market, 2011–2021 (Source: Rock Health)

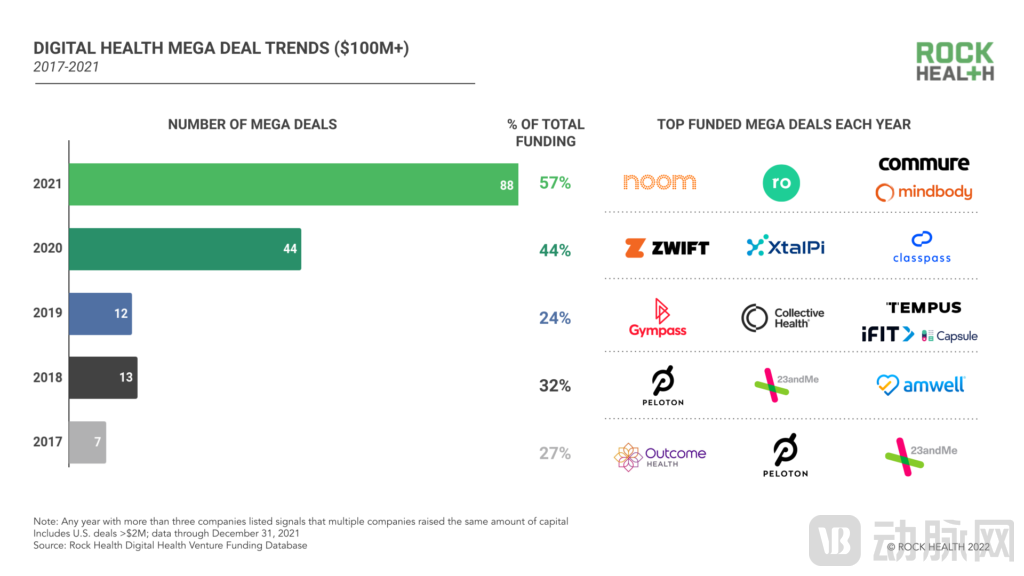

The number of mega-deals valued at over $100 million also doubled in 2021, serving as the primary driver of investment and financing growth that year. A total of 88 such mega-deals were completed in 2021, amounting to $16.6 billion and accounting for 57% of the total investment and financing volume for the year.

Number of Mega Deals in the U.S. Digital Health Market, 2017–2021 (Source: Rock Health)

Moreover, among the top five investment and financing deals from 2011 to present, four occurred in 2021, including Noom ($540 million), Ro ($500 million), Mindbody ($500 million), and Commure ($500 million).

Top Four Mega-Funding Deals in the U.S. Digital Health Market in 2021

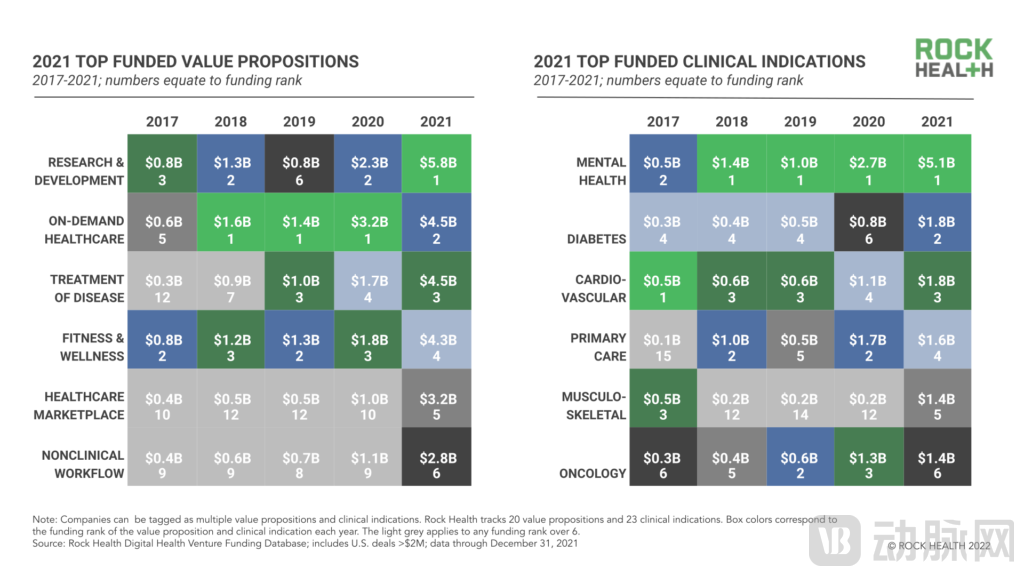

From the perspective of corporate value propositions, biopharmaceuticals and medical technology R&D topped the list of digital health investments in 2021, with $5.8 billion in funding. As the coverage of prescription digital therapeutics expanded, investment in disease treatment reached $4.5 billion in 2021, 2.6 times the $1.7 billion recorded in 2020.

Categorized by clinical indications, digital health startups providing mental healthcare services have not only maintained their leading position since 2018—raising a total of $5.1 billion in 2021—but have also widened the gap with other clinical indications by at least $3.3 billion. Drivers of this growth include the integration of mental health services into more comprehensive telecare platforms (such as K Health’s acquisition of Trusst) and the rise of virtual services addressing a wide range of psychological and behavioral health needs. Notable examples include Lyra Health, a comprehensive provider of psychological and behavioral health services ($200 million); NOCD, an obsessive-compulsive disorder (OCD) treatment platform ($33 million); and Equip Health, which treats eating disorders ($13 million). Investors are also increasing their investments in conditions that are increasingly manageable via telecare, such as diabetes care and musculoskeletal (MSK) care. In 2021, MSK-related funding reached $1.4 billion, six times the amount raised in the previous year. During this period, digital MSK clinics Hinge Health ($300 million and $400 million) and Sword Health ($25 million, $85 million, and $163 million) completed multiple rounds of financing.

Sector Performance of the 2021 U.S. Digital Health Market by Corporate Value Proposition and Clinical Indication (Source: Rock Health)

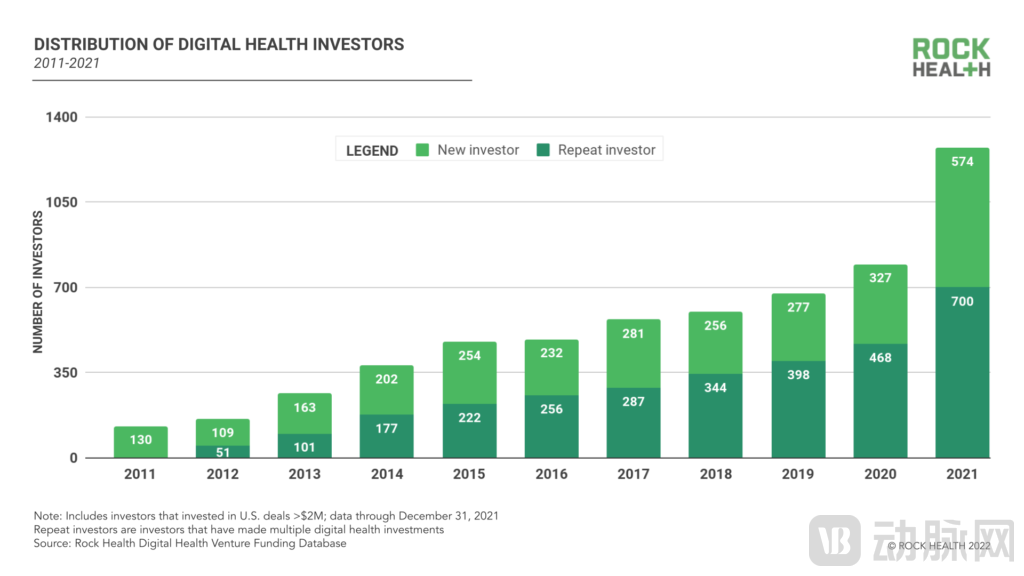

In 2021, the venture capital landscape in the digital health sector heated up, with new funds and growth-stage companies entering the market. New investors (45%) and repeat investors maintained a relatively healthy balance, accounting for 45% and 55%, respectively. Many startups saw opportunities under these market conditions and closely conducted multiple rounds of financing, with 60 companies completing two rounds of financing in 2021 and 2 companies completing three rounds within the year.

Changes in Investor Participation in the U.S. Digital Health Market, 2011–2021 (Source: Rock Health)

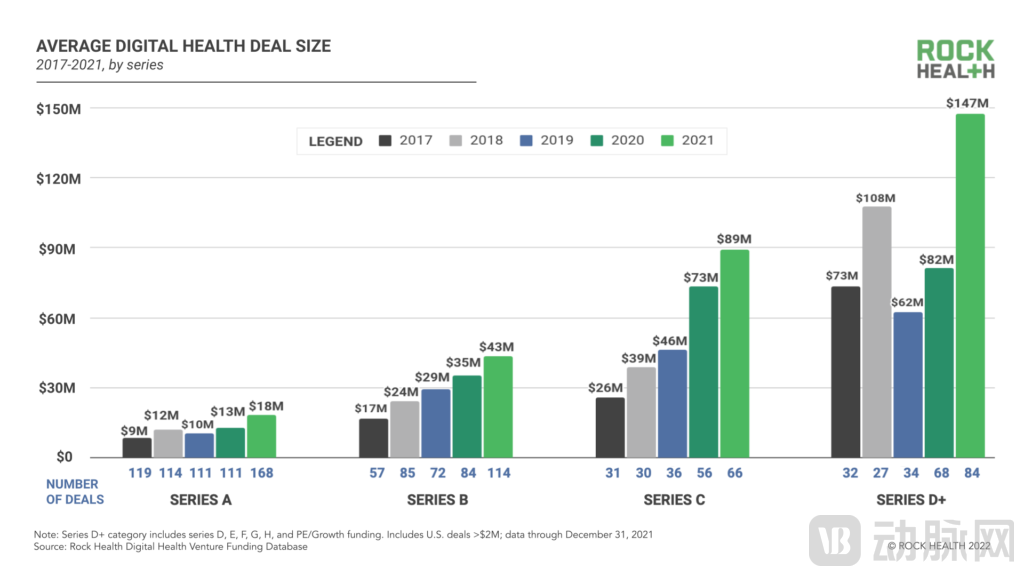

Competition among investors for early-stage deals is also intensifying. In 2021, the largest growth in the number of startup financing transactions occurred in Series A and Series B rounds, with increases of 51.5% and 35.7%, respectively. The average funding amount rose by 38% year-on-year to $18 million for Series A and by 23% to $43 million for Series B. Furthermore, among large early-stage transactions, there were 10 Series B financings and 1 Series A financing. By comparison, there were 6 large Series B financings in 2020, and prior to 2021, only one large Series A financing had occurred, back in 2018.

2017–2021 U.S. Digital Health Market: Financing Rounds and Deal Sizes (Source: Rock Health)

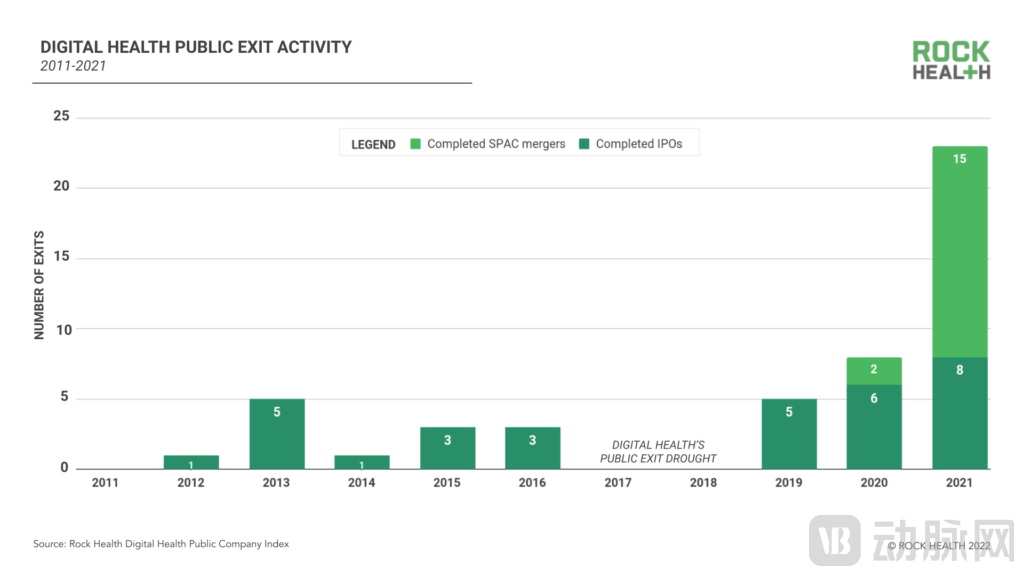

Prior to 2021, the pace of venture capital investment in digital health did not always align with exit activity. Over the past decade, approximately one-quarter (23%) of funding flowed to companies that ultimately exited; of this capital, 13% went to companies that merged or were acquired, while 10% went to those entering the public markets. However, in 2021, a surge in exit activity coincided with substantial capital inflows. In 2021, an average of nearly 23 digital health companies exited each month through mergers or acquisitions, almost double the 2020 monthly average of 12. Regarding public listings, although some anticipated SPAC transactions failed to materialize in 2021, 23 digital health companies still exited via SPACs or IPOs, nearly triple the number recorded in 2020.

Capital Exits in the U.S. Digital Health Market on Public Markets, 2011–2021 (Source: Rock Health)

Rock Health’s observations on the U.S. digital health sector reveal that three forces are fundamentally reshaping the American digital healthcare market from the ground up: improved infrastructure, flexible business models, and a war for talent. These factors not only constituted significant changes in the U.S. digital health landscape in 2021 but will also influence its development in 2022.

(I) Infrastructure Development

Historically, the fragmentation of the U.S. healthcare system has made it nearly impossible for stakeholders to share data in areas such as care coordination, billing, or research. Enterprises have had to build and manage their own technology infrastructures from scratch or adapt to existing electronic medical record (EMR) models.

However, by the end of 2020, the platform war in digital health had intensified, with major healthcare and life sciences companies experiencing firsthand the challenges of integrating disparate data silos during collaborations or acquisitions. As regulators push for greater patient transparency, health systems and payers need to make their data more user-friendly. Furthermore, the declining costs of data storage and algorithmic capabilities have created favorable conditions for equipping digital health businesses with a new set of “pipelines.”

In 2021, startups in the fields of digital health infrastructure and interoperability secured $2.2 billion in funding across 40 deals, nearly triple the investment in this category in 2020. Key players in this space include Innovaccer ($105 million), Redox ($45 million), and Ribbon Health ($43.5 million), which integrate data flows into unified API ecosystems; TripleBlind ($8.2 million and $24 million) and Truveta ($95 million and $100 million), which provide cross-company data analytics; ScienceIO ($8 million) and Centaur Labs ($15.9 million), which streamline data structuring and labeling; and Commure, Truepill ($142 million), Wheel ($50 million), and Zus Health ($34 million), which offer “Lego kits” or building blocks for other companies’ digital health solutions.

A growing number of infrastructure participants are driving market development across three key areas. First, they have lowered the barriers to entry for new digital health startups, enabling entrepreneurs to focus on non-technical differentiators—paving the way for future patient-centric approaches in digital health. Second, they have reduced the friction and costs associated with integration and mergers and acquisitions (M&A) in the digital health sector, thereby accelerating platform competition and industry consolidation. Third, they have contributed to a unified industry data ecosystem, unlocking new possibilities for population health.

(2) More Flexible Business Models

For a long time, the primary go-to-market strategy for healthcare companies has been selling to employers, insurance plans, and healthcare providers. However, in 2021, direct-to-consumer (D2C) digital health reached a new peak. Companies operating exclusively under the D2C business model accounted for 24% of total funding in the digital health sector. Additionally, 43% of all companies that raised financing in 2021 included individual consumers as part of their customer base—setting two new records. Meanwhile, some D2C players have begun leveraging their consumer bases to negotiate enterprise contracts and subsidize consumer costs, a approach regarded as an innovative B2C2B model.

In 2021, healthcare startups continued to expand their product categories and venture into the realm of complex care services. For instance, Ro entered the weight management and fertility sectors, while Headspace expanded beyond mindfulness services to include talk therapy. This expansion mindset also drove digital health companies toward physical establishments: Thirty Madison opened its first brick-and-mortar hair transplant clinic; Tia raised $100 million to expand its offline clinics; and Kaia Health, a digital musculoskeletal care provider, established partnerships for in-person physical therapy. The omnichannel shift also occurred in the opposite direction, as major insurers and other payers such as UnitedHealthcare, Cigna, and CVS/Aetna launched virtual-first products, while Amazon’s Alexa made inroads into hospitals and senior living facilities. Thus, digital healthcare is not destined to remain purely virtual. Instead, it can integrate digital and face-to-face interactions to achieve an appropriate balance in delivering accessible, high-value care.

Furthermore, a cohort of leading digital health companies has abandoned the fee-for-service model in favor of value-based care. This model incentivizes providers to deliver high-quality care and reduce costs by leveraging a broad spectrum of physical and digital interventions. In this space, service providers Spring Health ($190 million) and Omada Health both launched outcomes data initiatives in 2021 to demonstrate the clinical and commercial returns of the value-based care model.

(III) The War for Talent

In addition to capital, business models, and infrastructure, talent is another critical component for the healthy operation of businesses. Digital health companies require robust software engineering and product teams, as well as professional guidance from clinical healthcare professionals. In 2021, the United States faced a severe shortage of talent in clinical roles. The COVID-19 pandemic exacerbated occupational stress within the healthcare industry, prompting more clinicians to consider leaving the medical profession, while non-traditional healthcare employers began hiring physicians and expanding their clinical talent pools.

In 2021, several digital health startups emerged offering innovative approaches as clinical staffing platforms, including Prolucent Health ($11.5 million), connectRN ($76 million), Nomad Health ($63 million), and ShiftMed ($45 million). Wheel, an infrastructure player, proposes that virtual clinics need to adopt dynamic staffing models to manage fluctuating demand. Some virtual care providers, such as Seven Starling ($2.9 million), employ a one-to-many care model to maximize provider capacity, while Omada, Noom, and Robin ($2 million) advocate for care programs led by health coaches or peer support rather than relying on licensed clinicians—and are beginning to demonstrate evidence-based outcomes for this approach.