Can Online Fitness Apps Like Peloton and Keep Be the Future of Health Insurance?

Health insurers’ “health management” services have long revolved around reactive, post-event measures—such as green-channel access, online consultations, and medication discounts—while paying scant attention to proactive, pre-event prevention, such as fitness and nutritional diet. Although there have been some attempts, such as light-touch applications that offer increased coverage limits for walking 10,000 steps a day, these initiatives have largely remained at this superficial level.

Since “proactive prevention” is the ultimate goal of insurance, then:

1) Will China's Keep and the U.S.'s Peloton develop their own health insurance businesses?

2) Are the fitness industry and the health insurance industry in a zero-sum relationship?

3) Could a fitness app be the way forward for health insurance companies?

Recently, I read the prospectus and annual reports of Peloton (a U.S.-based online fitness app regarded as the pioneer of China’s Keep). On one hand, I was impressed by its successful business model; on the other, it prompted considerable reflection on its cross-industry implications for healthcare and insurance.

Peloton was founded in 2012 and went public in 2019. Initially, it sold high-end stationary bikes, later expanding to other fitness equipment such as treadmills. These machines are equipped with screens that stream proprietary workout videos, forming a highly comprehensive product and business ecosystem today.

Source: Peloton Prospectus, Mu Zhe Shuo

Source: Peloton Prospectus, Mu Zhe Shuo

Peloton adopted a hardware-driven software business model from the outset, which differs from the approach taken by China’s Keep.

The company sells fitness equipment such as stationary bikes, with each unit priced at approximately $3,000. Additionally, users are required to pay a monthly subscription fee of RMB 39 to access live video coaching during their workouts. This is a classic example of the Razor-Blade business model.

Sources: Peloton Prospectus/Annual Reports, Mu Zhe Shuo

If we look at the business model alone, it can be evaluated from three aspects:

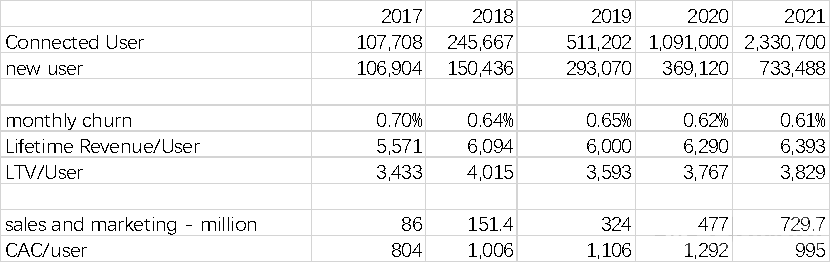

1. Attrition RatePeloton has managed to keep its monthly churn rate at 0.6–0.7%, demonstrating the success of its product and business model. What does this mean? It means that out of 1,000 people who purchased a bike and subscribed to the membership, 993 renewed their subscriptions in the second month.

Second, unit economics.Peloton’s customer acquisition cost (CAC) is approximately RMB 1,000–1,200, while its lifetime revenue, calculated based on monthly churn rate, is around RMB 6,000. According to the company’s prospectus, when subscription-related costs are taken into account, the lifetime value (LTV) amounts to approximately RMB 3,500–4,000. This figure does not even include the initial hardware fee paid by users (around RMB 3,000, with a gross margin of 40–50%). In short, Peloton’s business model is clear and highly attractive.

Source: Peloton Prospectus/Annual Report, Muzhe Shuo

Third, replicability.Scaling was a challenge for the company before 2017, as it had only acquired 10,000 users after four to five years of operation. However, post-2017, the company demonstrated significant momentum. After validating its unit economics, it achieved a rapid breakthrough through aggressive advertising campaigns, sustaining a 100% year-over-year growth rate for four consecutive years and reaching 2.33 million paying users by the end of 2021.

Source: Peloton Prospectus/Annual Report, Mu Zhe Shuo

Source: Peloton Prospectus/Annual Report, Mu Zhe Shuo

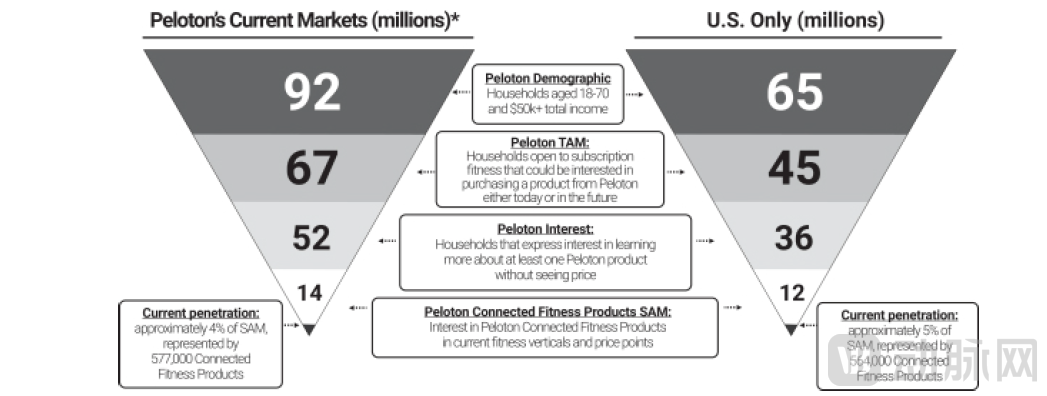

According to the company's IPO prospectus, the total addressable market (TAM) in target markets (such as the United States, the United Kingdom, and Canada) is approximately 67 million households, while the serviceable addressable market (SAM), representing the potential paying customer base, is around 14 million households. This indicates a growth potential of more than sixfold.

Peloton has long served as the benchmark for China’s Keep. Although cultural differences lead to variations in fitness habits, their overall strategic approaches are similar. Keep now also relies on a bundled sales model combining physical products with software, where the physical offerings include fitness equipment and nutritional supplements.

From the Servitization of Insurance to the Tangibilization of Services

We have observed that insurance companies have introduced health management services, but most of these are “virtual services.” Ping An Property & Casualty Insurance’s “Ping An Good Life” app has evolved from simple step-counting check-ins to featuring Olympic champion Lü Xiaojun leading calisthenics sessions and recording fitness videos. Thus, the foray of insurance providers into the fitness app sector has already begun.

Clearly, such fitness videos are relatively lightweight. The Peloton case demonstrates that software services should be driven by fitness equipment. What is displayed within an app is less impactful than what is physically present in the home. Even in the healthcare sector, Livongo successfully secured contracts with insurers and won over Teladoc by leveraging a model where smart hardware (glucometers and unlimited test strips) drives its app-based services.

Why Patients Keep Coming Back—“Joy” Outweighs “Fear”

In Peloton’s IPO prospectus, the founder articulated a most compelling and straightforward principle for attracting customers and sustaining their fitness engagement:Exercise generates dopamine, and dopamine makes people happy.

To amplify the “joy” element, the company spent over $100 million in 2021 on “music production and licensing” for its video content creation, accounting for approximately 15% of its subscription revenue. (You can imagine the instructor’s shouts syncing with the rhythm while you’re pedaling on a stationary bike.)

Insurers often struggle with low renewal rates. In addition to improving the quality of new policies, should they also consider how to stimulate long-term stickiness among existing customers by appealing to “happiness” rather than “peace of mind” or “anxiety”? Can buying “insurance” be “happy”? This is a question worth considering.

Additionally, Shukang, a domestic company specializing in sports rehabilitation, has obtained an NMPA medical device certification. Positioned as the “Keep of the medical circle,” could it also consider breaking into the “entertainment circle”?

"Either spend money on exercise, or spend money on medical care."

From a personal perspective, spending money on exercise and buying insurance (saving for medical care) are the same type of investment: either used for proactive prevention (fitness expenditure) or for post-illness treatment (insurance expenditure). Therefore, this is often cited as a reason for not purchasing insurance.

From a corporate operational perspective, it is common knowledge that regular exercise can reduce the incidence of disease, requiring no further proof. However, whether insurance companies are willing to lower premiums for those who engage in fitness activities is another matter entirely. This presents a contradiction, which also exists in healthcare: should the market aim for expansion or for “reduction”?

Imagine a product model where a fitness app charges a monthly membership fee of 30 yuan, requiring users to check in twice a week. If they fail to meet this requirement, half of the fee is automatically transferred to an insurance pool (mutual aid or commercial insurance) to cover medical insurance costs for this group.

There are two layers of logic here: First, individuals may feel that even if they do not utilize the fitness services, their money is not wasted, as it contributes to their insurance premiums. Second, rather than letting the premiums go to waste, it is better to promptly engage with one’s online personal trainer (male or female) and start lifting weights to boost dopamine production.

This morphology can be referred to as"Absolute Uniformity of Personal Health Expectations"。

A prediction:

1) Life and health insurance companies will increasingly enter the “online fitness” sector (either through in-house development or partnerships), potentially making it a standard feature of their mobile apps, and then begin selling products such as exercise equipment and nutritional meals, similar to Keep’s e-commerce model.

2) In certain single-disease insurance products (such as those covering cardiovascular conditions), “fitness” services (including both online and offline options) are integrated into policy benefits or claims reimbursement. This creates a dual-cycle ecosystem: insurance policies drive App usage, App services promote product sales, and together they drive further policy acquisitions. Especially in the current era of booming “digital therapeutics,” this process is being accelerated.

3) Internet healthcare platforms will not remain idle either; online fitness services (including weight training, cycling, and even cognitive training) will be integrated into their service ecosystems. If they fail to meet medical qualification standards, they can simply market these offerings as health supplements.

P.S. The analysis in this article is based on public information, reasonable assumptions, and business projections, and does not constitute any investment advice.