The End of the High-Profit Era for Dental Implants: A Major Shift in China's Oral Healthcare Industry

“The era of ‘one dental implant costing as much as a house in a county-level city’ is coming to an end!”

Recently, the State Council Executive Meeting held in Beijing reiterated its decision to institutionalize and normalize centralized volume-based procurement (VBP) of drugs and high-value medical consumables. The meeting announced plans to gradually expand the coverage of VBP for high-value medical consumables, with centralized procurement of orthopedic consumables, drug-coated balloons, and dental implants—areas of significant public concern—to be carried out at both national and provincial levels.

Indeed, dental implants, long regarded by the industry as part of consumer-oriented healthcare and thus unlikely to be included in centralized volume-based procurement, have prominently appeared on the list.

Although various provinces and municipalities have previously conducted surveys and data collection on dental implants, significant challenges remain in implementing these initiatives. The national government’s first-ever emphasis on centralized volume-based procurement of dental implants across China undoubtedly sends a clear signal: to enable more Chinese citizens to access dental implant services and benefit patients.

“Last year, I took my 65-year-old father to the hospital for a dental check-up. The dentist told us that his current oral condition was no longer suitable for porcelain-fused-to-metal crowns, and recommended either dental implants or a combination of implants with removable dentures. However, when we calculated the costs, the treatment for four dental implants alone amounted to around RMB 50,000, not including the subsequent cost of bone grafting materials,” said Zhang Xianrong, a resident of Bishan District in Chongqing, in an interview with VCBeat. “As soon as the volume-based procurement program succeeds, we will proceed with the implant surgery immediately.”

On the other hand, the costs “slashed” by volume-based procurement (VBP) actually represent the profits along the supply chain from production to consumption for dental implants. Therefore, once VBP is implemented for dental implants, relevant stakeholders will face significant impacts, which will inevitably affect the current evolutionary trajectory of the oral care industry.

Based on the experience of previous national centralized procurement of high-value medical consumables, the price reduction for dental implants may range from 50% to 90%.In other words, following the volume-based procurement, patients may be able to achieve their dental implant goals at 50%, or even 10%, of current prices.

Undoubtedly, the era of exorbitant profits in dental implants is nearing its end.

In recent years, there have been strong calls to reduce the cost of dental implant treatment. Therefore, whenWhen dental implants became the target of centralized procurement, it immediately drew close attention from both the industry and consumers, for two reasons.

· On one hand, the high cost of a single dental implant, often exceeding RMB 10,000, imposes a significant financial burden on patients. According to statistics from China’s fiscal authorities, fewer than one-tenth of the Chinese population earns a monthly salary above RMB 5,000, making the threshold for dental implants prohibitively high for most people.

· On the other hand, with the acceleration of population aging, the market demand for dental implants is gradually increasing, becoming a significant livelihood issue. According to statistics from the China National Committee on Aging, 50% of elderly people aged 65 to 74 in China have lost more than 10 teeth due to various reasons; among those over 74, 26% have lost all their teeth, and this proportion continues to rise.

Where there is demand and a market, competition should logically be relatively intense.Why Are Dental Implants Still So Expensive?

This requires an analysis of the dental implant industry chain. Specifically, the dental implant sector is divided into the upstream segment, dominated by equipment and consumables manufacturers; the midstream segment, primarily composed of medical device distributors; and the downstream segment, mainly consisting of dental healthcare institutions.

(Image source: Guohai Securities' "In-depth Report on the Dental Implant Industry")

(Image source: Guohai Securities' "In-depth Report on the Dental Implant Industry")

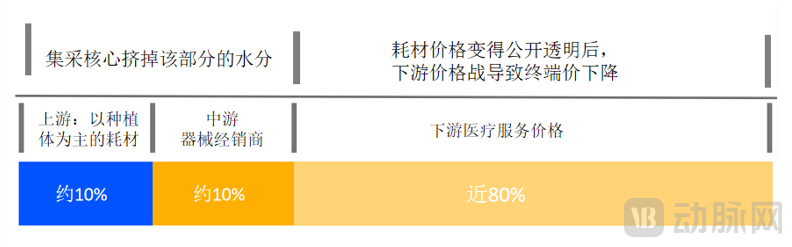

Looking at the upstream segment, dental implants, as a core consumable in dental implant procedures, currently account for approximately 10% of the total out-of-pocket expenses paid by consumers. The market is predominantly dominated by imported brands, with a very low rate of domestic production.Among these, Korean and Western brands are the mainstream. “The prices of domestically produced and Korean dental implants range from around 1,000 to 2,000 yuan, while Western brands generally cost 3,000 yuan or more,” Lv Sang, a seasoned oral healthcare investor, told VCBeat.

The midstream distribution segment, where medical device distributors operate, also accounts for a certain portion of costs.According to previous research by VCBeat, the downstream dental service sector is characterized by a fragmented landscape of small, independent operators, with tens of thousands of private dental clinics. Coupled with the wide variety of clinical SKUs at the upstream level, the midstream segment plays a critical “bridging” role, generating profits through economies of scale. In this process, the overall cost of dental implants accounts for approximately 10%.

Finally, there are downstream medical service prices.“The educational and time investment required to become a dentist is substantial, typically spanning 10 to 13 years from undergraduate medical studies through graduate and doctoral training. Additionally, implant dentists must dedicate significant time to patient care, including diagnosis, treatment planning, and follow-up therapy,” said an anonymous executive at a dental chain group, who noted that daily operational expenses for dental practices, such as equipment procurement and marketing costs, also contribute to overall expenditures.

In other words, the majority of the overall cost of dental implant treatment is concentrated in downstream oral healthcare service providers, covering expenses such as physician fees, marketing costs, related equipment costs, and facility leasing fees, which account for approximately 60% to 80% of the total cost.

After clarifying the pricing for each stage of dental implant procedures, how can we eliminate inflated costs to ensure patients benefit from affordable, inclusive pricing?

First, it is important to clarify that,Volume-based procurement targets upstream medical device manufacturers and midstream distributors, rather than physicians and healthcare institutions.

Based on the above analysis, consumables such as dental implants and midstream distribution channels together account for approximately 20% of the total cost of dental implant treatment. If a patient pays RMB 15,000 for a single dental implant, RMB 3,000 is spent on consumables and distribution. The cost reductions achieved through centralized volume-based procurement are deducted from this RMB 3,000 portion.

“However, it is important to recognize that the end-user prices for dental implants were previously highly fragmented due to a lack of regulatory oversight. Once volume-based procurement is implemented and the government provides guidance prices, making the cost of consumables open and transparent, it will also exert downward pressure on downstream pricing,” said Mr. Lv.Driven by market share considerations, dental service providers may even ignite a "price war," causing terminal prices to continue declining to reasonable levels.

(Impact of Volume-Based Procurement on All Links in the Dental Implant Chain; Graphic by VCBeat)

However, this has also raised concerns among oral healthcare practitioners. “From a long-term perspective, the policy can help standardize industry development. Nevertheless, we are concerned that consumers may focus solely on the final price while overlooking the quality of medical services. Given that each dentist’s time is limited and high-quality dental professionals are scarce, excessively low prices could dampen the motivation of skilled dentists,” a dentist at a Wuhan-based oral hospital told VCBeat. “Therefore, I hope that patient education efforts will keep pace in the future.”

From the above dimensions, centralized procurement of dental implants indeed has considerable room to squeeze out profit margins, thereby reducing overall treatment costs.However, the exact extent of the price reduction will ultimately depend on market reactions following the release of centralized procurement prices for implant-dominated consumables, particularly the future pricing strategies of downstream medical service providers.

“Since various regions across China began rolling out news about centralized procurement for dental implants last year, many industry insiders have started to worry about the significant impact on the oral care sector. This impact is certainly real and may severely compress profits for certain groups. However, it is also important to recognize the substantial industrial opportunities within this shift, such as domestic substitution or competing globally through premiumization,” said a fund manager who has long followed the oral care industry.

How will China’s dental implant market evolve in this process?

In the field of dental implants, domestically produced implants in China started relatively late, currently holding a market share of approximately 7%, which is relatively low.

This is because domestically produced dental implants have insufficient accumulation in technology and experience, their industrialization is relatively lagging, and they are still at the stage of technological following compared with foreign countries.

Taking surface treatment technology as an example, according to data from Gaohe Investment Research Center, the two leading dental implant manufacturers, Nobel Biocare and Straumann, employ fourth-generation technologies—TiUnite anodic oxidation treatment and SLActive (hydrophilic SLA) hydrophilic sandblasted and acid-etched treatment, respectively. These technologies offer superior biocompatibility, corrosion resistance, and bone integration strength. In contrast, most domestic Chinese dental implant brands remain at the second- or third-generation level, relying on simple coating and sandblasted and acid-etched treatments, which is relatively backward.

Specifically, the market shares of European and American brands and Korean brands are 35% and 58%, respectively. European and American dental implants offer superior performance and dominate the high-end market. Korean brands, with their lower prices, hold the largest share among end consumers. Chinese-made implants are priced similarly to Korean brands but entered the market later, facing competitive pressure from the cost-effectiveness of Korean products.

“The inclusion of dental implants in centralized procurement has promoted the development of domestically produced implants with price advantages.“From Lu Sang’s perspective, the market share of domestically produced dental implants and Korean brands will gradually increase through provincial and national centralized procurement initiatives. The reason lies in”The dental implant industry achieves scale through volume; once volume increases, corporate profitability will follow suit.

According to a research report by Guohai Securities, approximately 4 million dental implants were placed in China in 2020, equivalent to 28 implants per 10,000 people. In contrast, South Korea recorded 632 implants per 10,000 people, 22 times the figure in China, indicating substantial room for growth in China’s dental implant penetration rate. The volume-based procurement program has led to a decline in dental implant prices, which in turn has driven an increase in overall sales volume and accelerated the rise in market penetration.

“There is also a less noticeable trend. As far as I know, few domestic dental implant manufacturers have successfully registered for procurement in public hospitals, especially those in Beijing, Shanghai, and Guangzhou. In previous years, domestic brands had almost no opportunity to enter these institutions, with most concentrating on private hospitals or clinics that did not require such registration. However, the introduction of centralized volume-based procurement may open up this channel.”Once a company successfully opens an account with a public hospital, its natural channels will operate more smoothly across all aspects.“Lu Sang stated.

“At the same time, there are risks in this process. ‘Companies must be willing to invest in R&D as needed. If the price of dental implants drops and volume surges, but production capacity cannot be expanded and quality cannot be controlled, that would pose a significant problem.’”

Additionally, from the perspective of the pathway,For relatively low-end products, it is essential to actively participate in centralized volume-based procurement to expand market share, whileFor mid-to-high-end products, it is essential to target specific high-value customer segments and capture consumer mindshare through comprehensive solution offerings.

The value of the midstream segment is expected to persist in the short to medium term. Lu Sang believes that while ex-factory prices for consumables and end-user prices for dental implants may decline, the rapid annual expansion of the overall dental implant market—driven by increased penetration rates—will offset these pressures. As a core intermediary linking upstream and downstream players, the oral care midstream sector primarily generates revenue through supply chain services. Given the substantial growth in the total market size, the impact on overall profitability remains limited.

The downstream medical service sector is likely to follow two divergent trajectories. One scenario involves companies with weaker brands experiencing “revenue growth without corresponding profit growth,” or even suffering declining profitability in this segment due to industry-wide price wars. The other scenario features leading industry players leveraging their superior physician talent and service resources to siphon off the majority of patients within their regions. By offering comprehensive oral health solutions—such as family-oriented dental care services in addition to dental implants—these leaders can enhance patient stickiness and achieve higher premium pricing.

Beyond the changes across upstream, midstream, and downstream enterprises, another key issue is whether dental implants will be covered by medical insurance in the future.

In this regard, many industry experts have stated that the positioning of medical insurance is to "cover basic needs." In addition to dental implants, there are various other options for tooth restoration, such as removable dentures and porcelain-fused-to-metal crowns. Furthermore, the status of medical insurance funds varies across different regions. Therefore, it is unlikely that dental implants will be included in medical insurance coverage in the short term.

In summary, once the centralized procurement policy is implemented, the process of domestic substitution in China’s dental implant market will accelerate. Upstream brands that are the first to achieve volume growth will gain a competitive advantage, but they must pay attention to improving production capacity and quality. For mid- and downstream distributors and service providers, the market size will expand, and the Matthew effect will become more pronounced. Additionally, it is unlikely that dental implants will be included in the national medical insurance scheme in the short term.

It is well known that consumer healthcare has always been a sector heavily favored by capital investment.

The core logic lies in the fact that consumer healthcare primarily follows a B2C business model, with most products falling outside the scope of medical insurance coverage, such as medical aesthetics products, orthokeratology lenses (OK lenses), and health supplements. This positions consumer healthcare at the forefront of the medical industry in terms of gross margin and reflects a higher degree of marketization.

However, the national-level proposal to include dental implants in centralized procurement for the first time also signals a further step of centralized procurement into consumer healthcare.

It is important to recognize that volume-based procurement (VBP) has a significant impact on the development of specialized healthcare sectors. For instance, in terms of stock prices, the first round of drug VBP in October 2019, the coronary stent VBP in 2020, and the Anhui IVD VBP in 2021 all led to declines of 20% to 30% in the pharmaceutical industry index.

Does this mean that the consumer healthcare sector, long considered a highly coveted investment target by capital markets, will also face undervaluation in future investments?

“I believe the logic behind the policy is not aimed at consumer healthcare, but rather at livelihood issues. With dental implant prices being excessively high and demand substantial, this matter has garnered increasing social attention as our society rapidly ages,”Centralized procurement is an initiative to address public concerns.“An industry veteran stated, ‘In previous years, policymakers conducted research on clear aligner orthodontics but later discovered that over 70% of the market share was held by private hospitals, with consumption primarily driven by young adults aged 20 to 30. Consequently, they did not pursue the matter further. In the future, if a large population requires orthodontic treatment that impacts their quality of life, centralized procurement will likely intervene.’”

From this perspective, consumer healthcare will continue to remain highly active.Many industry experts believe that the greater the market penetration of dental implants, the more effectively the market can be educated, thereby encouraging consumers to place greater emphasis on the importance of preventive oral care and periodontal maintenance. This, in turn, can drive the growth of the broader dental industry, including emerging consumer healthcare segments such as oral care products and pediatric dentistry.

“People’s livelihood will always be a major concern for the nation, and the decline in dental implant prices will enhance the sense of well-being for hundreds of millions of Chinese people in the future.”Consumer healthcare sectors, represented by dentistry, must capitalize on this trend to unlock greater market demand and create value for users across the entire care continuum, from treatment to prevention.“The aforementioned investors stated.”

From this perspective, although the window for exorbitant profits from dental implants is closing, this aligns with the original intent of normalizing national volume-based procurement, thereby delivering tangible benefits to patients. In this process, companies that proactively seize the opportunities of the times are poised to enter a golden period of development.