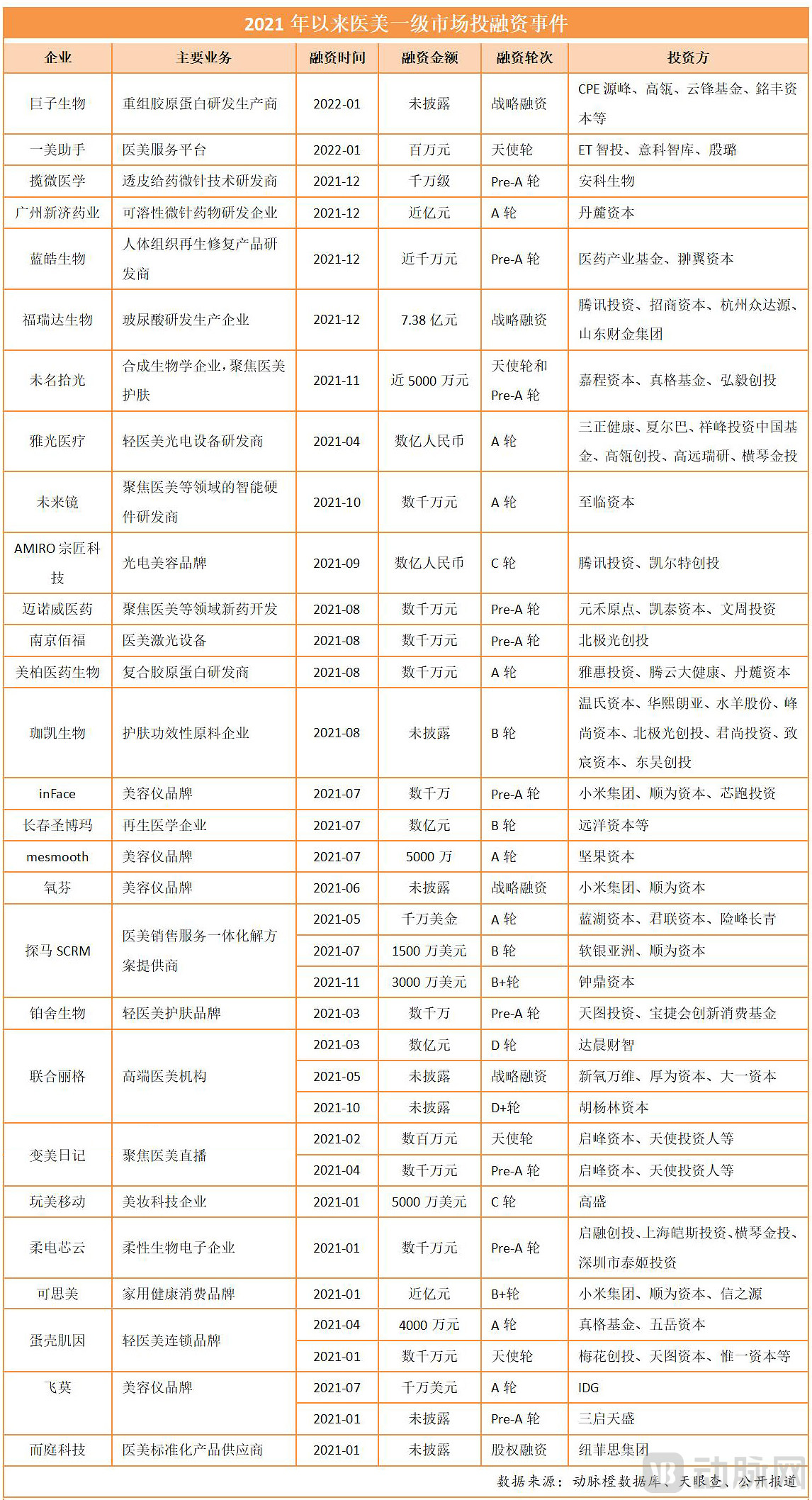

28 Upstream Aesthetic Medicine Companies Secure Funding in 2021, Attracting Nearly 100 Investors: Who Reigns Supreme?

From the beginning of last year to the present, the upstream sector of the medical aesthetics industry has remained consistently hot.

How should this be interpreted? Judging by the stock prices of companies listed on the secondary market, including Ha Sanlian, Imeik, Bloomage Biotech, Haohai Biological Technology, Huadong Medicine, and Aoyuan Meigu, among others.The share prices of leading upstream enterprises all rose last year., with increases of 125.5%, 49.7%, 7.2%, 9.6%, 55.6%, and 40.6%, respectively (comparing stock prices as of December 31, 2021, with the same period in 2020). During the peak of market activity in the first half of last year, the stock price surges for Ha Sanlian and Aoyuan Meigu even exceeded 200%.

Turning to the primary market, data from the VCBeat Orange Database shows that from 2021 to the present, a total of 28 companies in China’s medical aesthetics industry have completed financing rounds, with total funds raised exceeding RMB 3 billion, setting a new historical record.

Among them, 23 are upstream enterprises, accounting for as high as 82%. More importantly, they are backed by an impressive lineup of investors.From tech giants such as Tencent and Xiaomi to top-tier investment institutions including SoftBank, IDG Capital, Northern Light Venture Capital, Goldman Sachs, Hillhouse Capital, ZhenFund, and Yunfeng Capital, their names have frequently appeared in financing news involving upstream companies in the medical aesthetics industry. Furthermore, multiple companies have seen investors increase their funding commitments after initial investments.

“After securing tens of millions in financing, an early-stage medical aesthetics company specializing in bioactive ingredients immediately attracted interest from more than ten institutions seeking to visit,” Wang Han, an investor focusing on the pharmaceutical industry, told VCBeat. “As of now,”The project is so sought-after that one must rely on insider connections, such as existing shareholders, to even get in touch with the company’s founders., it is not easy to integrate through third parties or media.”

What’s more intriguing is that Aoyuan Meigu, whose core business was originally property operations, began its foray into the medical aesthetics sector after completing its name change in late 2020. Last year, it signed multiple strategic cooperation agreements with companies such as Jiyuan Pharmaceutical and KDMedical concerning high-end medical aesthetic skincare products, therebyOfficially entering the upstream segment of the medical aesthetics industry, its stock price achieved several consecutive jumps in 2021.

The industry’s exceptionally high level of interest actually stems from changes in its underlying logic.

“Over the next 5 to 10 years, the driving force behind industry development will not be demand, but rather the upstream sector. The core drivers are materials and technology.“Jin Xuekun, Founding Partner of Mingfeng Capital, stated.”

“Consumer spending patterns have undergone significant changes in recent years. Coupled with the pioneering influence of industry leaders like Imeik and Bloomage Biotech, this demonstrates that giant enterprises can emerge in the upstream segment of the medical aesthetics industry, which is a key factor attracting institutional investors to place their bets,” Song Gaoguang, Partner at Northern Light Venture Capital, told VCBeat. The growing number of investors specializing in healthcare, along with the aggregation of professional talent, has further fueled investment activity in the upstream medical aesthetics sector.

As can be seen, since 2021, the upstream segment of the medical aesthetics industry has become a fiercely contested battleground.

Why Is the Upstream Aesthetic Medicine Sector So Hot? What Major Changes Have Occurred Since 2021? What New Trends Are Emerging? What Challenges Remain to Be Addressed? In response to these questions, VCBeat has conducted a comprehensive review and interviewed numerous industry experts and investors to shed light on the answers.

In 2021, the upstream segment of the medical aesthetics industry attracted the highest frequency of financing rounds and the largest total capital inflow, surpassing the midstream medical aesthetics service providers that had consistently led in previous years.

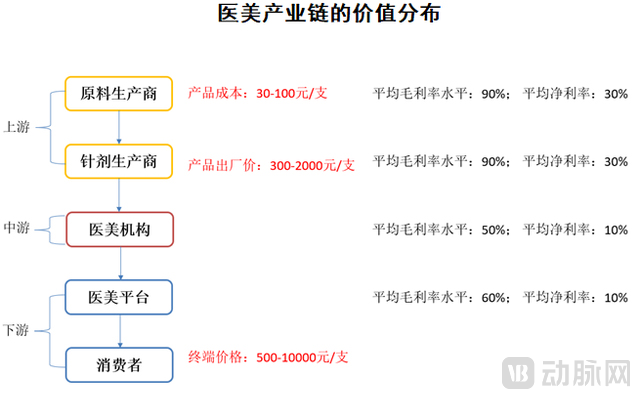

Investment institutions are shifting their focus to different sectors, a move that is closely tied to the current state of the industry:A typical characteristic of China’s medical aesthetics industry chain at present is the uneven distribution of value: upstream enterprises demonstrate strong profitability, while midstream and downstream players show relatively weak earnings performance, with an intensifying head effect.

How so? VCBeat reviewed the financial reports of six upstream medical aesthetics companies—Harbin Sanlian, Imeik, Bloomage Biotech, Haohai Biological Technology, Huadong Medicine, and Aoyuan Beauty Valley—and found that their net profits for the first three quarters of 2021 were RMB 539.8 million, RMB 708.9 million, RMB 555.3 million, RMB 310.5 million, RMB 1.895 billion, and RMB 211 million, respectively, with net profit margins of 76.17%, 69.25%, 18.39%, 24.65%, 7.49%, and 14.79%, respectively.

Such a level of net profit generally ranks among the highest across more than 4,000 companies listed on China’s A-share market.

Within the entire medical aesthetics industry chain, mid- and downstream enterprises, such as medical aesthetics service providers and traffic platforms, report average gross profit margins of 50%–70%, yet their average net profit margins stand at merely 5%–15%. Consequently, upstream companies capable of sustaining average net profit margins of 20%–40% have naturally become highly sought-after targets for investment institutions.

(Image source: Suning Finance Research Institute, Mingfeng Capital)

On the other hand, the penetration rate of China’s medical aesthetics industry stands at only 3.6%. In comparison, developed markets exhibit a penetration rate of approximately 10% (according to iiMedia Research data). Consequently, the number of medical aesthetics consumers in China is projected to exceed 150 million in the future. This indicates that demand for medical aesthetics services will remain robust over an extended period, andUpstream materials and technologies can turn potential demand into reality.

This is corroborated by the market data from 2021.For instance, the financial performance of the three major hyaluronic acid players—Bloomage Biotech, Imeik, and Haohai Biological Technology—has continued to rise, with their combined revenue reaching RMB 3.5 billion in the first half of the year alone. The core reason lies in consumers’ sustained preference for hyaluronic acid products.

In the view of Jin Xuekun, Founding Partner of Mingfeng Capital,Materials and technologies can turn potential demand into reality, yet they are predominantly controlled by upstream enterprises.“Much like the iPhone in its early days, there was no clear awareness of such a demand at the time; it was only after the iPhone’s emergence that people realized this need. Materials and technology can drive transformative change within an industry.”

In a nutshell, by virtue of its exceptional capital-raising capabilities and competitive barriers, as well as the immense potential to foster industry-leading enterprises,China’s medical aesthetics industry has truly entered a phase of business growth driven by technological and product innovation.

Against this backdrop, innovative enterprises that identify new materials and technologies to meet the demands of emerging consumer segments, and leverage digital technologies to expand service boundaries and enhance efficiency, will become the mainstream in the medical aesthetics industry.

In 2021, upstream companies in the medical aesthetics industry accelerated their efforts in the field of non-surgical aesthetic products, triggering a wave of new product launches.

The most closely watched development has been the successive approvals of regenerative injectable products.In April 2021, Ellansé (“Girl Needle”), a product of Sinclair, a wholly-owned subsidiary of Huadong Medicine, received the Medical Device Registration Certificate issued by the National Medical Products Administration (NMPA). In the same month, Changchun Shengboma’s “poly-L-lactic acid facial filler” was approved, becoming China’s first “Youth Needle” to obtain Class III medical device certification. In June, Imeik’s “cross-linked sodium hyaluronate gel containing poly(L-lactic acid-co-glycolic acid) microspheres” (the second Class III “Youth Needle”) was approved for market launch.

As collagen-stimulating agents, “Tongyan Zhen” (Baby Face Injection) and “Shaonv Zhen” (Girl’s Face Injection) share the same indications and can both be used to improve wrinkles, enhance elasticity, tighten skin, and provide lifting effects. The primary difference between the two lies in their composition: Tongyan Zhen consists of poly-L-lactic acid (PLLA), whereas Shaonv Zhen is composed of 70% carboxymethylcellulose (CMC), a biodegradable material, and 30% polycaprolactone (PCL) microspheres. To some extent, Shaonv Zhen offers superior contouring capabilities, earning it the reputation as the second-generation version of Tongyan Zhen.

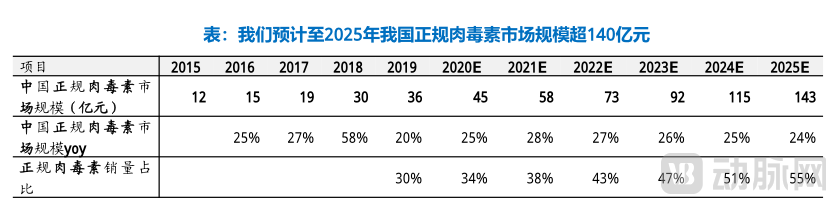

According to data from Founder Securities, China’s market for “Girl Needle” and “Youth Needle” aesthetic treatments is projected to reach nearly RMB 3 billion in 2025, maintaining an annual growth rate of over 20%.

As blockbuster cash-cow products, competition for PLLA-based “baby face” fillers and CaHA-based “girl” fillers will intensify during their market scale-up in 2022.

In June last year, Shanxi Jinbo Bio’s “Recombinant Humanized Type III Collagen Lyophilized Fiber” was approved for market launch. The product can be used for facial dermal tissue filling to correct dynamic forehead wrinkles (including glabellar lines, forehead lines, and crow's feet), becoming China’s first independently developed medical device prepared using a novel biomaterial—recombinant humanized collagen.

Meanwhile, brands such as Sihuan Pharmaceutical, Shangli, Galderma, and South Korea’s Regen are also conducting clinical trials and submitting NMPA registration applications for injectable products.The “injection war” among leading enterprises has undoubtedly officially begun.

As one of the sectors with the highest upstream barriers, botulinum toxin officially entered a “Big Four” competitive landscape in 2021.: The National Medical Products Administration has approved four botulinum toxin products, namely Allergan’s Botox, Ipsen’s Dysport, Hugel Inc.’s Letybo, and Lanzhou Institute of Biological Products’ Hengli, three of which are imported.

From the perspective of competitive differentiation among the four brands, Botox and Dysport are primarily positioned for affluent women, with high price points; Letybo mainly targets fashion-conscious young adults, with mid-range pricing; while Hengli focuses primarily on students, offering affordable prices.

“Botulinum toxin represents a seller’s market; as long as product positioning is clear, it can rapidly capture market share upon approval and launch.“Wang Han stated that, taking Letybo as an example, shipments approached 200,000 vials in the first half of 2021 following its approval.”

(Image source: Soochow Securities’ “Striking Gold in Botulinum Toxin: Upstream Aesthetic Medicine Injectable Products with High Barriers and Strong Growth”)

Data provides a glimpse into the popularity of botulinum toxin. According to a report by iResearch, botulinum toxin accounted for 52.9% of the market for injectable medical aesthetic treatments in 2021, indicating substantial room for growth in penetration rate. Data from the Chinese Association of Plastics and Aesthetics shows that approximately 70% of hyaluronic acid and botulinum toxin products on the Chinese market are counterfeit or smuggled goods. In 2020, legally approved botulinum toxin products accounted for only 34% of sales in China.

Substantial market returns have also intensified potential competition in the botulinum toxin market. Currently, at least five companies worldwide are developing botulinum toxin products, with Xeomin, jointly developed by Germany’s Merz and PPD (Pharmaceutical Product Development), showing the most rapid commercialization progress and expected to launch within the next two years.

Wang Han stated that due to the unique status of botulinum toxin as a controlled narcotic and psychotropic substance, domestic companies generally opt for agency models to accelerate market entry, turning competition in the botulinum toxin product sector into a race against time. “The trends observed last year will continue in 2022, andBotulinum toxin brands with precise positioning, unique advantages, or outstanding marketing capabilities are poised to capture a larger market share.”

As one of the most mature products in the medical aesthetics industry, hyaluronic acid began to expand into sectors such as functional foods in 2021.Driven by the strong performance of three industry leaders—Imeik, Bloomage Biotech, and Haohai Biological Technology—in the secondary market, hyaluronic acid gained significant popularity last year. According to Frost & Sullivan’s projections, the hyaluronic acid market is expected to reach RMB 12 billion in 2024, with continued expansion anticipated.

In terms of the competitive landscape, numerous hyaluronic acid manufacturers have received approval in China. Nearly all foreign brands have entered the Chinese market, with 18 domestic brands having obtained regulatory approval.However, the market is primarily dominated by four imported products and three domestic brands, including Imeik.

In terms of imports, LG Yvoire from South Korea (distributed by Huadong Medicine), Allergan’s Juvederm from the United States, and Galderma’s Restylane rank as the top three in sales volume. Among them, Yvoire holds the leading position with a 22% market share, driven by its high cost-performance ratio. Regarding domestically produced brands, Imeik, Bloomage Biotech, and Haohai Biological Technology are positioned in the mid-to-low-end segments. Notably, Imeik’s HiBody has emerged as the leading domestic product due to its differentiated positioning targeting neck wrinkles and the scarcity of regulatory approvals for such indications.

“In the future, the ‘medical’ attribute of hyaluronic acid will gradually diminish, while its usage scenarios and frequency will increasingly align with those of skincare products, reflecting its ‘aesthetic’ attribute. This shift will drive a steady expansion of its market share in sectors such as cosmetics and functional foods.” said Wang Han.

In early 2021, the National Health Commission officially approved hyaluronic acid as a new food raw material., a multitude of companies have flocked to enter the market, vying to capture a share of the oral hyaluronic acid sector. For instance, Bloomage Biotech launched the “Shuijiquan” hyaluronic acid beverage, while the popular brand Hankou Erchang introduced its hyaluronic acid sparkling water, “Ha Shui.”

In the beauty and skincare sector, take Freda Biopharm, backed by Tencent, as an example. In addition to its core businesses of research and development, production, and sales of raw materials, the company currently owns 11 brands, including “Rellet,” which specializes in hyaluronic acid-based skincare, and “Dr. Alva,” which focuses on microbiome science-driven skincare.

Meiye Biotechnology, a hyaluronic acid enterprise invested in by Fortune Capital, also focuses on beauty and skincare, primarily operating three brands: Dr. Ling (skincare), FMFM (body care), and Natural Melody (skincare and personal care). Among them, Dr. Ling’s core ingredient is full-molecular-weight hyaluronic acid, GaussianHA, which was launched to the market in 2021 and achieved sales of nearly RMB 200 million within five months of its launch.

Bloomage Biotech’s financial report shows that in its revenue structure, the income from “functional skincare” reached RMB 1.346 billion, surpassing for the first time the RMB 703 million from product raw materials and the RMB 576 million from medical terminal products. This indicates that hyaluronic acid still holds considerable market potential to be tapped.

It is foreseeable that in 2022, hyaluronic acid will continue to extend into sectors such as functional skincare and cosmetics, thereby expanding its market boundaries.

In addition to the three major sectors of regenerative injectables, botulinum toxin, and hyaluronic acid, which are fiercely contested by industry leaders, niche segments such as medical dressings, functional skincare products, chemical peeling agents, and microneedling also attracted intensive attention from primary and secondary market investors in 2021.

In 2021, Voolga and Chuanger Biotech, which pursued initial public offerings, as well as Boshe Biotech, Weiming Shiguang, Jiakai Biotech, Mainuo Wei Pharmaceutical, and Guangzhou Xinji Pharmaceutical, which secured financing, all focused on this sector.

Both Fu'erjia and Chuanger Biology are leading enterprises in the medical dressing industry (commonly referred to online as “medical aesthetic masks”).Voolga’s product portfolio includes medical dressings, patches, and masks (including leave-on mask formulations). Trauer Biotech’s products encompass the Chuangfukang series and the Chuangermei series; the former is primarily used for adjunctive treatment of wounds, while the latter is mainly indicated for skin barrier care.

According to the prospectus, Trauer Bio’s operating revenue from 2018 to 2020 was RMB 214 million, RMB 303 million, and RMB 303 million, respectively, while its net profit attributable to shareholders of the parent company was RMB 67.08 million, RMB 73.2278 million, and RMB 92.4981 million, respectively. However, in the first half of 2021, Trauer Bio experienced a significant decline in performance, with operating revenue of only RMB 108 million, a year-on-year decrease of 17.74%, and net profit attributable to shareholders of the parent company of RMB 21.2272 million, a year-on-year decline of 45.1%.

The underlying reason lies in the tightening of policies. Last year, the National Medical Products Administration (NMPA) strengthened regulatory oversight over so-called “medical aesthetic masks” and “Class II medical device masks,” bringing an end to the era when the medical dressing market could achieve substantial revenue growth driven primarily by marketing efforts.

More importantly,The R&D barriers for medical dressings are not yet very high.According to Voolga’s prospectus, its R&D expenditures from 2018 to the first quarter of 2021 were approximately RMB 300,000, RMB 600,000, RMB 1.48 million, and RMB 130,000, respectively, accounting for 0.08%, 0.04%, 0.09%, and 0.04% of its operating revenue. As of March 31 last year, Voolga had a total of 291 employees, including 2 R&D personnel, representing 0.69% of its total workforce.

From this perspective, the medical dressing industry still has a long way to go before true industry giants can emerge. To date, the IPOs of both Voolga and Chuanger Biology have failed, and their subsequent market performance remains to be tested.

Even so, as a key segment of the upstream medical aesthetics industry, medical dressings continue to attract strong investor interest in the primary market. Recently, one company secured a financing round worth billions of yuan, with investors reportedly including several leading venture capital firms.

Boshe Biotech, Weiming Shiguang, and Jiakai Biotech, which all completed financing in 2021, are focused on the skincare brand and skincare ingredient sectors.

Boshe Biotech primarily focuses on anti-aging solutions for the skin, having developed an integrated approach combining devices with consumable serums. The brand’s current product lineup is mainly divided into light medical aesthetic skincare products designed for home use, such as at-home hydration and oxygen infusion devices and freeze-dried essence serums, as well as daily functional products like repair masks and cleansing gels. In 2021, the brand’s average online transaction value was approximately RMB 800.

Weiming Shiguang is a synthetic biology company focused on skincare ingredients. It has established a database of natural bioactive molecules derived from plants and humans, and based on this, it has designed and delivered a collagen-derived skincare ingredient with anti-aging properties.

Jiakai Biotech also focuses on the field of skincare ingredients, specializing in active substances. Leveraging technologies such as skin microbiome modulation, cellular autophagy, and 3D reconstructed skin models, the company provides nearly 100 product solutions—including soothing, comprehensive repair, anti-wrinkle, whitening, scalp care, hydration, oil control and acne prevention, antioxidant, and anti-blue light protection—to skincare brands. It directly or indirectly supplies products and services to over a thousand domestic and international cosmetic brands, including Shiseido, Bloomage Biotechnology, and Shanghai Jahwa.

“Our investment thesis for Jiakai Bio rests on four pillars. First, Jiakai Bio has been deeply engaged in the skincare ingredients sector for over a decade and enjoys an excellent reputation within the industry. Second, from a market demand perspective, cosmetic companies have sustained and stable demand for functional ingredients. Third, regarding competitive dynamics, since the procurement volume of raw materials by individual enterprises is relatively small (approximately RMB 1–5 million), downstream brands have little incentive to establish in-house production capabilities. Fourth, Jiakai Bio currently serves 5,000–6,000 purchasers annually and is still accelerating its growth, demonstrating the potential to become a leading player in this niche segment,” stated Song Gaoguang, Partner at Northern Light Venture Capital.

In fields such as microneedle technology and innovative drugs related to medical aesthetics, Guangzhou Xinji Pharmaceutical, Lanwei Medical, and Mainuowei Pharmaceutical have all secured financing.

Microneedles play a crucial role in enhancing drug delivery efficiency and improving patient compliance, representing a new technological growth driver for the medical aesthetics industry. Guangzhou Xinji Pharmaceutical possesses six core formulation technologies, one of which is the industrialized formulation technology for soluble microneedles; however, no products based on this technology have yet been launched on the market.

Minovate Pharma, established in February 2021, focuses on the development of novel drugs in fields such as medical aesthetics. Currently, one product in the medical aesthetics sector is undergoing clinical trials, while several other products in medical aesthetics and related fields are in preclinical development. The company expects to complete Investigational New Drug (IND) applications for 3–4 products in China and the United States by 2022.

Lanwei Medical, which recently secured tens of millions in financing from Anke Biotechnology, was established in 2016 with a core team of Ph.D. graduates from Shanghai Jiao Tong University. The company has successfully overcome two major challenges in the GMP-compliant mass production of pharmaceutical-grade microneedles: high-precision microneedle mold design and fabrication, and automated, modular manufacturing processes. Its capabilities fully meet the consistency, automation, and cleanliness requirements for pharmaceutical-grade microneedle production.

“The upstream segment of the medical aesthetics industry generally sees innovations in existing materials or advancements in production methods, both of which undergo gradual iteration. A breakout moment is still some time away,” said Wang Han.

Beauty devices were arguably the most sought-after sector for upstream medical aesthetics financing in 2021, with brands such as Feimo, Yangfen, mesmooth, inFace, and AMIRO (Zongjiang Technology) all falling into this category.

Behind this lies the gradual rise of domestic brands, propelled by the tailwinds of new consumption. Historically, imported beauty devices have dominated the Chinese market. These include Clarisonic, a U.S. brand that entered the Chinese market in 2012, as well as later entrants such as Yaman, ReFa, Philips, Dr. Arrivo, Tripollar, Ulike, Notime, FOREO, and Smoothskin.

“The maturation of related technologies in recent years has enabled compact, portable home-use beauty devices to deliver professional-grade aesthetic treatments, thereby rapidly gaining popularity among younger consumers.“An investment director at a financial advisory (FA) firm told VCBeat that radiofrequency (RF) beauty devices, for example, rapidly gained popularity because they leverage the principle that collagen fibers in the dermis contract when heated to a certain temperature, thereby delivering skin-tightening and wrinkle-reducing effects. Coupled with the rising trend of ‘Guochao’ (national chic), it was only natural for capital to flock into the beauty device sector.”

VCBeat conducted a search for major beauty device brands on the JD.com platform and found that some domestic brands are already selling well, such as Xiaomi, Jin Dao, Landai Meiyan, Qucotang, Bear Electric, COSBEAUTY, AMIRO, and Femooi.

According to multiple investors, the industry holds a relatively optimistic view on the scale of China’s beauty device market, with projections reaching RMB 30 billion within three years. Additionally, China’s current share of the global market remains below 10%, indicating substantial domestic demand. According to the “2020–2026 Research Report on Market Size and Development Trends of China’s Beauty Device Industry” by Zhiyan Consulting, the production volume of beauty devices in China is currently growing at a rate exceeding 20%.

From the perspective of market landscape, mainstream beauty devices are primarily categorized into five types: ultrasound, microcurrent, radiofrequency (RF), light spectrum, and oxygen infusion. In terms of efficacy, ultrasound devices mainly provide facial cleansing and nourishment; microcurrent technology enhances muscle fiber tension to achieve a lifting effect; radiofrequency devices stimulate fibroblasts in the dermis to promote collagen regeneration; light spectrum therapy helps smooth fine lines and maintain skin vitality; and oxygen infusion stimulates stem cell growth and division, accelerating wound healing and inflammation recovery.

“Ultrasound-based, spectroscopy-based, radiofrequency-based, and microcurrent-based devices already have relatively mature products on the market, whereas oxygen-infusion devices are an emerging category in recent years that still requires market validation,” said the above-mentioned FA Investment Director.

Of course,Due to low entry barriers and intense, uneven competition, the market has been flooded with a large number of beauty devices that offer mediocre or even substandard performance.In October 2020, CCTV News’ “Weekly Quality Report” conducted an investigation into beauty devices, revealing that six out of ten best-selling models failed to meet relevant standards for nickel release, posing a heightened risk of allergic reactions and other issues. Additionally, two other products were found to carry a risk of low-temperature burns.

In early 2021, the National Medical Products Administration (NMPA) began soliciting public comments on the “Guiding Principles for the Classification and Definition of Radiofrequency Aesthetic Products,” which classify radiofrequency aesthetic medical products as Class II or Class III medical devices. This move indicated that the regulatory classification of radiofrequency aesthetic devices might be subject to adjustment.Once industry norms and standards are introduced, the beauty device market may usher in healthy development.

Small home-use beauty devices are primarily sold to the consumer (C-end) market and, in terms of product nature, are more akin to cosmetics. In contrast, large-scale medical aesthetic equipment for the business-to-business (B-end) sector is still in its early stages of development in China.

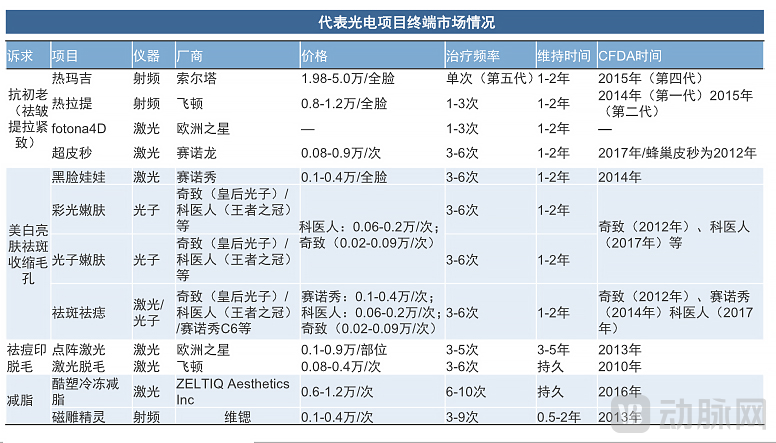

“Star aesthetic procedures on the market, such as Thermage and Fotona 4D, also fall under the category of photoelectric treatments, characterized by minimal invasiveness and rapid results. The overall market size exceeds RMB 10 billion, while the upstream sector for medical aesthetic photoelectric devices has long been polarized,” Xiong Zhe, Vice President of Investment at Qingtong Capital, told VCBeat. The top five global manufacturers are all European, American, or Korean brands, with annual sales ranging from USD 200 million to USD 600 million. Their devices, often priced at over RMB 1 million each, are in short supply and boast gross margins as high as 90%. In contrast, Chinese manufacturers still primarily engage in assembling and producing counterfeit machines, with selling prices less than one-tenth of those of imported products. Due to a lack of industry regulation, these devices pose significant safety risks. Furthermore, domestic products lack competitiveness in core technologies, such as energy stability and the structural design of optical and circuit systems.A small number of manufacturers with R&D and production capabilities have also shifted toward distribution, resulting in a chaotic competitive landscape characterized by resource and channel scrambling.

“The high-end product market is characterized by insufficient competition. As the medical aesthetics industry becomes more regulated, downstream demand will further expand. Meanwhile, imported products are iterating slowly, and their high prices make them unaffordable for most downstream institutions. ‘We believe that the inadequate adaptation of functional parameters to Asian populations presents an opportunity for domestic manufacturers to overtake competitors on the curve. After a long period of absence in the high-end market, the market prospects and returns have been continuously validated. Relying on China’s robust supply chain system and strong foundational research capabilities, Chinese manufacturers that achieve world-leading standards and scale will inevitably emerge in the future,’ stated Xiong Zhe.”

For instance, among high-end laser-based aesthetic medical devices, erbium lasers present the highest technical complexity, followed by alexandrite lasers, ruby lasers, picosecond lasers, and dye lasers. In skin management, different types of lasers are required for various anatomical areas and distinct treatment and care needs, which has led to a wide variety of laser device categories.

Nanjing Baifu, which secured financing in 2021, has been deeply engaged in the research and development and localization of high-end medical aesthetic laser technologies, achieving breakthroughs in the domestic production of certain devices. Nanjing Baifu has independently developed a series of laser products, including Q-switched Nd:YAG lasers, 1064nm long-pulse lasers, 755nm alexandrite long-pulse lasers, 2940nm erbium lasers, and 1064/532nm picosecond lasers. The relevant technical indicators have reached a leading level in China.

In the realm of light medical aesthetics devices, Yaguang Medical has launched the “Shuiyingji” (Water Baby Skin) series. This device is a non-invasive, transdermal drug delivery medical device classified as a Class II medical device. It is also a non-invasive transdermal drug delivery system that has obtained registration certification from the National Medical Products Administration (NMPA). Specifically, it applies medium-frequency pulses to the skin, causing temporary disruption of the stratum corneum structure and generating reversible “electropores” to facilitate drug penetration. The electric field applied to the cells increases cell membrane permeability, allowing nutritional ingredients to penetrate into the dermis.

“Domestic optoelectronic products, riding the major trend of import substitution, still present considerable opportunities; however, the key to success ultimately hinges on pricing and the product itself,” said Song Gaoguang.

(Image source: Cinda Securities’ “Robust Supply and Demand: Welcoming the Golden Age of Medical Aesthetics”)

(Image source: Cinda Securities’ “Robust Supply and Demand: Welcoming the Golden Age of Medical Aesthetics”)

In summary, due to relatively standardized industry regulations and a relatively concentrated industrial landscape, companies offering hyaluronic acid, botulinum toxin, and regenerative injectable products will serve as the cornerstone of the non-surgical aesthetic medicine market., which has also established them as industry leaders. They will continue to expand their product portfolios and indications in the future, driving industry development through technological innovation.

For large-scale equipment enterprises in the acoustic, optical, and electronic sectors, core competitiveness hinges on pricing and product quality, with domestic substitution presenting a significant opportunity. For consumer-facing companies such as skincare brands and beauty device manufacturers, the key to standing out lies in continuously enhancing product capabilities and strengthening brand equity.

Jin Xuekun believes that, from the demand side, the trend in the medical aesthetics industry is shifting from facial contouring to a combination of contour enhancement and overall aesthetic vitality.

“In the earliest days of medical aesthetics, consumers sought to spend money to immediately enhance features such as the nose and eyes. Thus, early-stage, basic medical aesthetic procedures were those that could rapidly address facial contouring concerns. However, this type of aesthetic improvement is the most rudimentary,”In the next stage, consumers seek a combination of contour aesthetics and overall condition—a more sophisticated form of beauty.”

Data reflect this trend. The 2021 So-Young Medical Aesthetics Industry White Paper shows that the proportion of surgical consumers primarily focused on contour aesthetics decreased from 34.2% in 2019 to 21.3% in 2021, while the proportion of non-surgical consumers mainly concerned with overall appearance and skin condition rose from 72.% in 2019 to 83.1% in 2021.

For instance, skin tightening and anti-aging treatments primarily involving photoelectric devices became the category with the highest total consumer spending in 2021; meanwhile, wrinkle reduction and facial slimming procedures primarily involving botulinum toxin injections became the category with the highest number of orders in 2021.This indicates that high-quality upstream products face no shortage of market demand, with substantial unmet needs still remaining.

Therefore, over the extended period ahead, investment institutions will continue to focus on foundational technologies, targeting high-quality assets across areas such as injectables, medical devices, material synthesis technologies, microbial fermentation technologies, and tool platforms.

However, the upstream segment of the medical aesthetics industry faces technical and process-related barriers, making it unrealistic to achieve rapid overtaking in the short term.Taking hyaluronic acid as an example, although China is the largest producer of raw hyaluronic acid materials, there is still a certain gap compared with international peers in high-end products. This is because the production of hyaluronic acid requires not only mastery of bio-fermentation technologies such as strain selection, fermentation formula conditions, and process control, but also expertise in materials science and synthesis related to cross-linking, necessitating continuous iteration and accumulation.

Where exactly do the breakthroughs in materials lie?

Jin Xuekun believes that there are mainly three aspects:First, combination therapy regimens. “Treatment regimens will inevitably be combinational in the future; for example, topical therapies can be combined with injectable treatments.” Second, whole-course management. Third, strengthening interdisciplinary application.

First, the material must have cross-lifecycle appeal, meaning it is not a short-lived trend but remains popular for a decade or even longer. Second, the material should be interdisciplinary; for instance, hyaluronic acid, one of the most well-known examples, is an interdisciplinary material. Third, the material must span multiple industries. “A major category of materials must be cross-industry; otherwise, it cannot become a mainstream material and may fall out of favor after a brief period of popularity.” Fourth, the material should have expandable indications; for example, botulinum toxin can be used not only to remove wrinkles but also to treat hemifacial spasm.

From this perspective, collagen and botulinum toxin will be the next investment hotspots.As collagen technology advances, human-like and other types of collagen offer superior regenerative and filling effects, gradually ushering injectable fillers into the era of regeneration. Botulinum toxin remains an irreplaceable category, with newly approved products and novel botulinum toxins based on bioengineering presenting attractive investment opportunities.

Additionally,Mingfeng Capital believes that major-dimensional innovations in the fields of materials and technology may also occur in the following areas:

1. Gene-edited biomaterials may reshape the current landscape of dermal filler products.

2. Synthetic biology will significantly transform the cosmetics ingredients market.

3. Application of Protein Technologies from the Innovative Drug Industry in the Medical Aesthetics Sector.

Certainly, different application scenarios and demands impose varying requirements on materials and their associated technologies, necessitating that medical aesthetics innovators continuously explore, accumulate experience, and even face the risk of failure.

For leading enterprises that have already established themselves in the industry, such as Bloomage Biotech, Imeik, and Huadong Medicine, in addition to continuously prioritizing R&D and internal innovation, it is also essential to follow the path of global aesthetic medicine giants like Allergan by pursuing in-industry acquisitions and consolidation to achieve sustained growth and scale, thereby creating greater potential for their own development.

Moving forward, substantial investment in the medical aesthetics industry will continue to concentrate on the upstream sector. Furthermore, as regulatory policies become increasingly stringent, the midstream and downstream segments of the industry will become more standardized, which will inevitably drive the expansion of the upstream market.

As technology continues to advance and high-quality products emerge, the medical aesthetics industry will benefit a broader population with lower prices and better outcomes.As the renowned science fiction writer Arthur C. Clarke once stated, any sufficiently advanced technology is akin to magic in transforming this world.

Aesthetic Medicine: The Magic That Makes People More Beautiful.

Special Thanks:

Jin Xuekun, Founding Partner of Mingfeng Capital

Partner, Mingfeng Capital Wang Zhen

Partner at Northern Light Venture Capital, Song Gaoguang

Vice President of Investment, Qingtong Capital Xiong Zhe

(The above list is in no particular order; “Wang Han” is a pseudonym, used at the interviewee’s request.)