Can the Six Major Payers Alleviate Profitability Concerns? Internet Healthcare's Make-or-Break Battle | 2021 Annual Review

After experiencing a surge in concentrated traffic and user growth, internet healthcare has had to confront the challenge of monetization. The industry’s overarching theme in 2020 was the former, while in 2021 it shifted to the latter.

The development of internet healthcare has demonstrated that single, low-frequency consultation services are insufficient to fully meet user needs and are even less capable of supporting enterprises in achieving scalable revenue. Meanwhile, the monetization logic of internet healthcare differs significantly from that of other internet sectors; after all, even with a substantial user base, it is not feasible to continually incentivize users to seek medical care.

Reviewing the industry’s development status in 2021, apart from well-established models such as pharmaceutical sales, companies have primarily explored monetization pathways through integrated medical services, aiming to generate revenue by creating tangible value for multiple stakeholders within a unified system.

Internet healthcare emerged as the “top-tier” online service during the pandemic. However, in the aftermath, years of experimentation and validation of business models within the industry reached a critical juncture, making the challenge of revenue growth even more pressing for sector participants in 2021.

Based on the operating data disclosed by companies, it is evident that pharmaceutical sales remain the most direct pathway to achieving scaled revenue and even profitability. Nevertheless, enterprises have never ceased exploring alternative payment models. Given that pharmaceutical sales and out-of-pocket payments for medical services are well-established within the industry, this article focuses on monetization models beyond these conventional approaches, categorized by payer.

Healthcare Insurance Payment: Exploring Outcome-Oriented, Capitated Bundled Payment Models

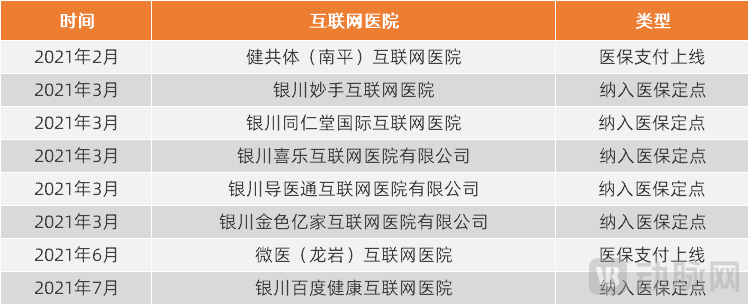

Previously, some internet hospitals under companies such as WeDoctor, Ping An Health, and Medlinker enabled payments via the medical insurance pooled fund accounts or personal accounts. In 2021, there was limited growth in medical insurance payment coverage among newly added internet hospitals affiliated with these enterprises, with the expansion primarily driven by leading industry players.

In March 2021, Yinchuan Miaoshou Internet Hospital, under the Yuanxin Technology Group, was officially included in the list of designated medical insurance payment institutions. By the end of 2021, a total of 18 internet hospitals operated by WeDoctor had been connected to the medical insurance payment system.

Some Internet Hospitals Included in or Launched with Medical Insurance Payment Coverage in 2021; Source: Official Website of the Yinchuan Municipal People's Government, Public Reports

Unlike public internet hospitals in cities such as Beijing and Shanghai, which have rapidly enabled medical insurance payments, medical insurance has not achieved large-scale coverage for enterprise-owned internet hospitals, nor is rapid integration likely in the short term. The aforementioned medical insurance payments primarily cover consultation fees and medication costs for follow-up visits for chronic diseases, all reimbursed on a fee-for-service basis. Consequently, medical insurance authorities place significant emphasis on fund security and the risk of insurance fraud. Furthermore, medical insurance payments for internet healthcare are applied for through the affiliated physical medical institutions; essentially, this represents a shift of certain offline reimbursements to online channels. From a holistic perspective, this constitutes “existing capacity” within medical insurance reimbursement rather than “incremental growth.” Therefore, for internet healthcare enterprises, the significance of enabling medical insurance reimbursement for chronic disease follow-ups lies more in attracting patients to use their platforms with greater frequency, thereby generating revenue from disease management services.

In 2021, WeDoctor piloted a value-based payment model in Tianjin. The Tianjin Primary Care Digital Health Consortium, led by the Tianjin WeDoctor Internet Hospital, deployed digital chronic disease management services to provide care for nearly 400,000 diabetic patients across the city. It explored payment methods such as diagnosis-related group (DRG) bundling and capitation, and implemented an incentive and constraint mechanism of “retaining surpluses and covering no deficits” based on assessments of healthcare quality and management performance.

Currently, several months after the implementation of capitation payment, the medical insurance surplus rate at primary healthcare institutions that have adopted this model has reached 16%-31%.

Under this model, internet healthcare companies bear the pressure of controlling health insurance expenditures, giving them the incentive to manage medical and pharmaceutical costs while ensuring effective patient management. Judging from the published surplus rates of health insurance funds, this approach has proven effective; however, questions remain regarding the exact amount of savings achieved and whether these savings are sufficient to cover corporate operational costs. Longer-term practical experience and more extensive data are needed to provide definitive answers.

Commercial Insurance Payment: Expansion of Direct Claim Settlement and Health Management Coverage

Just like medical insurance payments, commercial insurance payments are also highly anticipated within the internet healthcare industry.

In 2020, VCBeat published an article titled “Four Possibilities for Internet Healthcare + Commercial Insurance: Will Commercial Insurance Claims Account for 10% of Online Medical Payments?” which outlined the landscape of commercial insurers paying for patient-side services in internet healthcare, a sector that involved relatively few companies at the time.

By 2021, leading companies were refining commercial insurance payment channels, primarily through two models: first, internet outpatient insurance, which provides direct reimbursement for online consultation fees and medication costs; and second, health management services within medical insurance, which incorporate internet-based medical services.

Overview of Commercial Insurance Products Related to Internet Healthcare Services in 2021, Source: Public Reports

In the area of outpatient insurance, companies such as JD Health and Chunyu Doctor have partnered with external entities to launch outpatient insurance products that cover the entire process of medical care, pharmaceuticals, and insurance services, providing reimbursement for online consultations and medication purchases within specified formularies and coverage limits.

Since internet-based outpatient insurance products are almost exclusively co-developed by multiple parties, including internet healthcare companies, insurers, and insurtech firms, their product design and operations simultaneously account for factors such as data interoperability and claims processing. As a result, direct reimbursement during online consultations is nearly always achievable. In contrast, in offline care settings, the low level of information exchange between insurers and medical institutions often necessitates complex documentation collection and reimbursement procedures. In this regard, internet-based outpatient insurance demonstrates significant advantages.

In 2021, Ping An Health also collaborated with Ping An Health Insurance to launch a new feature for direct billing of commercial insurance on its internet hospital platform, establishing a connection between commercial insurance and online healthcare. Users insured under relevant insurance products can not only consult doctors and purchase medications through the Ping An Health APP but also enjoy zero out-of-pocket settlement convenience. Consultation services and medication costs covered under the policy are settled directly between the platform and the insurance company, enabling direct reimbursement from commercial insurance.

In the field of health management, companies such as Ping An Health, Alibaba Health, and JD Health have all established their presence.

In 2021, Ping An Health added the “Zhenxiang RUN” series of services to Ping An Life Insurance’s critical illness insurance policies. Policyholders who purchase flagship critical illness products are entitled to corresponding value-added health services.

Alibaba Health, in partnership with ZhongAn Insurance, has launched the “Family Care” million-yuan medical insurance plan for families, integrating internet-based medical services. It has also introduced a million-yuan medical insurance product tailored for hepatitis B patients, establishing a comprehensive health management framework that covers the entire care continuum for liver disease patients, including screening, diagnosis, therapeutic medication, and insurance claims settlement.

JD Health, together with Fosun United Health, JD Allianz Insurance, and other insurance companies, has jointly launched the “Family Medical Insurance” managed health insurance service, integrating health insurance with JD Health’s medical services and health management capabilities. Building on the disease-risk protection products provided by insurance companies, “Family Medical Insurance” incorporates the stewardship-style health management services of “JD Family Doctor,” intervening before family members develop illnesses. Through health promotion, health management services, and medical intervention plans, it aims to reduce the risk of disease onset and slow disease progression, thereby safeguarding the health of the entire family.

All of the aforementioned products were launched in 2021. VCBeat has not yet obtained comprehensive sales data from the companies. However, historical data reveals certain trends.

In 2020, ZhongAn Online P&C Insurance piloted the internet-based outpatient insurance product “ZhongAn Zunxiang e-Sheng 2020 (Outpatient and Emergency Edition)” and the digital healthcare management service “ZhongAn Yi Guanjia.” In 2021, the company further integrated its internet hospital services with a broader range of medical insurance products. According to ZhongAn Online’s 2021 interim report, by June 2021, over 6 million users in its health ecosystem held policies that included internet hospital benefits, representing a penetration rate of approximately 42%. This development is believed to reflect the positive impact of integrating internet healthcare with commercial health insurance, suggesting that commercial insurance payment may be a promising direction for growth.

Pharmaceutical Companies Pay: Digital Marketing Becomes a High-Margin Business

Internet healthcare directly connects doctors and patients, and under the influence of policies such as centralized drug procurement and national medical insurance negotiations, it has become a channel for pharmaceutical companies to reach doctors and patients and conduct digital marketing. Currently, apart from companies like Haodf Online that fully redirect medication purchase demands to third-party platforms, most leading internet healthcare enterprises are involved in digital marketing for pharmaceutical companies. In particular, companies that offer a comprehensive suite of services spanning from online consultations to pharmaceutical supply chains hold significant advantages.

In October 2021, Alibaba Health Pharmacy launched the “New Drug First-Release Support Program,” providing pharmaceutical companies with a breakthrough into the out-of-hospital market. In 2021, major pharmaceutical firms such as Roche and BeiGene debuted their original branded drugs on Alibaba Health’s self-operated pharmacy platform. Furthermore, Alibaba Health has established in-depth collaborations with over 100 renowned pharmaceutical companies, including Eisai China and Organon, leveraging its professional digital marketing capabilities to help these companies reach patients.

In its 2021 IPO prospectus, Yuanxin Technology disclosed that it could provide innovative marketing services to pharmaceutical companies. In 2021, DXY spun off its enterprise-facing digital marketing services as an independent brand named dmc (DXY Marketing Center), nicknamed “Damai Cha.”

In terms of revenue, JD Health’s 2021 semi-annual report showed that its online platform, digital marketing, and other services generated RMB 1.9 billion, a year-on-year increase of 73%. The growth in digital marketing service fees was primarily driven by an increase in the number of advertisers on the platform.

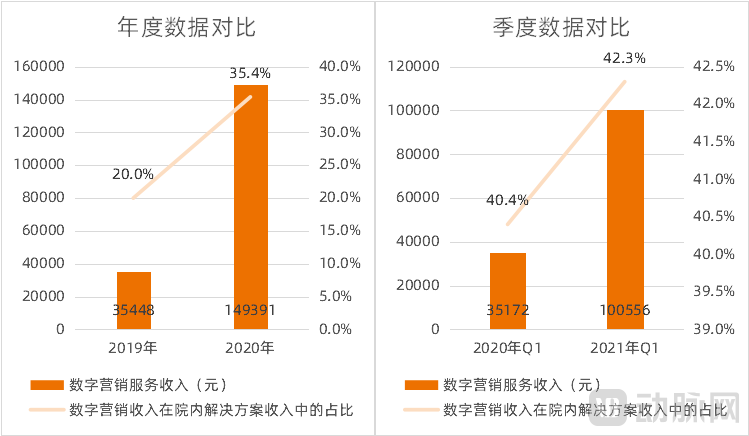

According to the prospectus of Zhiyun Health, the company provides digital marketing services to pharmaceutical companies for drugs related to chronic disease management, helping them promote their products to hospitals and physicians, and charges a service fee as a percentage of the pharmaceutical companies’ sales revenue. As of March 31, 2021, Zhiyun Health had signed contracts with 15 pharmaceutical companies, and its digital marketing revenue showed an upward trend.

Growth in Zhiyun Health’s Pharmaceutical Digital Marketing Revenue, Source: Prospectus

The prospectus further stated that from 2019 to 2020, Zhiyun Health’s gross profit margin increased from 11.7% to 27.7%, partly driven by the improvement in the gross profit margin of its in-hospital solutions. The rise in the gross profit margin of in-hospital solutions was “primarily due to a continuous shift in revenue mix, specifically an increasing proportion of revenue from digital marketing services, which carry relatively higher profit margins.”

Given that internet healthcare companies have already accumulated a certain number of physician and user resources, undertaking digital marketing for pharmaceutical companies is a relatively low-cost endeavor. The primary costs are associated with the development and utilization of online technical functionalities, eliminating the need for heavy offline asset investment. Consequently, this model offers higher profit margins and has been widely adopted within the internet healthcare industry.

However, it is worth noting that the 2021 “Measures for the Administration of Internet Diagnosis and Treatment (Draft for Comment)” was introduced, prohibiting prescription data aggregation (“tongfang”) and kickbacks on pharmaceuticals. In reaching physicians and driving drug sales, digital marketing must strictly adhere to regulatory boundaries.

Enterprise Payment: Insufficient Usage Habits, Currently in the Initial Trial Phase

Here, corporate payment refers to the model in which enterprises purchase internet medical services as benefits for their employees or customers.

Ping An Healthcare and Technology Company Limited’s financial report shows that, as of June 2021, its product packages had cumulatively served more than 3,800 corporate clients, covering nearly one million corporate employees, for whom customized health management solutions were provided.

In 2021, WeDoctor’s prospectus revealed that it partnered with large commercial banks to promote health management services to credit card holders, and collaborated with corporate clients to develop employee health management plans, for which companies paid annual membership fees. By the end of 2020, WeDoctor had served more than 200 corporate clients.

In addition, Haodf Online has also launched a membership-based service package, which is sold to banks and insurance companies as an employee benefit.

As widespread adoption of corporate health benefits has yet to take hold, and given the requirement for service providers to possess sufficient service capacity, the sector remains in its initial exploratory stage.

Individual Payment: Develop and sell health products, extending into the consumer sector

Internet healthcare services typically provide medical popular science information. Such content inevitably involves health advice and can be highly persuasive to users. Consequently, internet healthcare platforms inadvertently serve as product endorsers, with some even engaging in the development and sale of health-related products.

Dingxiang Yuan is a typical case. Dingxiang Yuan positions healthy lifestyles as the “upstream” of disease, focusing on addressing “upstream” needs. For example, it has partnered with Wugu Mofang to launch health food products and introduced nasal wipes designed to alleviate the “red nose” symptom for rhinitis patients. In 2021, it also launched a skincare brand called “Yanzhi Butie.”

In 2021, Chunyu Doctor also expanded its services in dermatology, pediatrics, nutrition, gynecology, and psychology: dermatologists collaborated with the Gene Drug Engineering Center of Jinan University to develop medical-grade skincare products, while nutritionists partnered with New Hope Group to jointly recommend a novel probiotic yogurt for gut health.

These health products are grounded in accumulated expertise from fields such as medicine and nutrition. They exhibit strong consumer-oriented attributes, boasting a user base far larger than the patient population alone, with higher usage frequency compared to medical services. However, this places greater demands on the consumer-facing (C-end) influence of internet healthcare platforms, and the products themselves must be more competitive than similar pure-consumer offerings.

Government Payment: Public Service Tendering and Procurement with Limited Participating Enterprises

This article primarily refers to the procurement of internet healthcare-related public services by government departments or medical institutions from enterprises. Additionally, there is a model in which governments or medical institutions procure internet healthcare systems from enterprises; this essentially constitutes the procurement of informatization projects, a model that is already relatively mature and thus will not be the focus of discussion in this article.

An example of the former is WeDoctor’s “Mobile Hospital,” which integrates public health examination vehicles, laboratory and diagnostic equipment, and an internet hospital platform. Procured by county-level health authorities or primary healthcare institutions, it is used to deliver primary healthcare services. Announcements on the China Government Procurement Network indicate that the price of a “Mobile Hospital” vehicle is approximately RMB 1 million. As of December 2020, the “Mobile Hospital” had covered 69 counties.

However, WeDoctor and its prospectus have not yet disclosed the specific number of “Mobile Hospital” vehicles, making it impossible to calculate the revenue generated from this business.

A search on the China Government Procurement Network also reveals that, apart from WeDoctor, few internet healthcare companies have ventured into government procurement services. For WeDoctor, the “Mobile Hospital” is not a primary revenue source; it also serves to deliver primary care services as part of WeDoctor’s Digital Health Community strategy.

It remains difficult to accurately grasp the comprehensive revenue situation for the aforementioned payers. However, it is certain that serving a single payer alone is insufficient to achieve scale; enterprises typically serve multiple payers and build systematic service frameworks behind this multi-payer model.

In 2021, internet-based healthcare primarily featured integrated medical services, emphasizing a systematic approach to support various payment models. Specifically, it integrates health promotion, disease prevention, diagnosis and treatment, nursing and rehabilitation, along with their management, based on the needs of patients or users. This integration coordinates healthcare institutions at all levels and of all types to provide lifelong, continuous care to patients or users. Based on the primary target population, these services can be categorized into three types.

HMO Services Targeting the General Public

In the early stages of internet healthcare development, the Health Maintenance Organization (HMO) model drew industry attention and was regarded as a target for innovation. However, the HMO model requires building a sufficient quantity and quality of medical, pharmaceutical, and insurance resources, attracting adequate user participation, and achieving data interoperability to form a mutually constraining closed loop. By 2021, on the foundation of earlier resource infrastructure deployment, the health maintenance models of some enterprises became more mature.

WeDoctor’s primary care digital health community in Tianjin, which adopts the HMO model, had achieved digital upgrades in over 230 primary healthcare institutions by November 2021, cumulatively serving more than 210,000 patients. The integration of medical, pharmaceutical, and insurance resources, along with large-scale user bases and data interoperability, has been realized; payment mechanisms have been established, making the essential elements required for the HMO model increasingly clear.

In 2021, Ping An Health announced its strategy to deliver high-value medical and health management services to users across various payer channels—including commercial insurance, public medical insurance, enterprises, and individuals—based on the HMO (Health Maintenance Organization) model. Leveraging the resources of its parent company, Ping An Group, as a commercial insurance payer, Ping An Health had, by September 2021, built an in-house medical team of 2,000 professionals and contracted with 46,500 external physicians. These two groups were integrated into a collaborative healthcare service system featuring coordination between internal and external providers, as well as between specialists and general practitioners. Additionally, the company established a comprehensive pharmaceutical supply network, comprising an online pharmacy platform and a network of 189,000 offline partner pharmacies.

Internet-Based Chronic Disease Management Targeting Patients with Chronic Conditions

The large population of patients with chronic diseases, the long course of disease, and the heavy disease burden have made chronic disease management a fiercely contested arena for internet healthcare companies. In addition to WeDoctor and Ping An Health, which incorporate chronic disease management into their HMO service systems, there are other companies that focus primarily on chronic disease management or are accelerating their strategic layout in this area.

In 2021, Zhiyun Health submitted its IPO application, disclosing its chronic disease management model. Specifically, centered on chronic disease management, it provides medical products and SaaS solutions to hospitals and pharmacies, and offers digital marketing services to pharmaceutical companies. In its consumer-facing solutions, Zhiyun Health enables patients to undergo out-of-hospital monitoring, consultations, and prescription issuance.

In 2021, Fangzhou Jianke launched “Fangzhou MedTalk,” a specialized health education platform for chronic disease management, to cultivate branded physicians, provide patient education, address information asymmetry, and enrich the dimensions of its online chronic disease management services.

In 2021, Alibaba Health established 12 major health care centers focused on neurological, cardiovascular, oncological, and immune-related diseases, and expanded its internet-based chronic disease management services with a focus on primary care. As of September 2021, the number of chronic disease users had increased by 170% year-on-year. Patients can access chronic disease management services including medication supply, medication follow-up, patient education, and dedicated physicians.

Hardware and data are essential components of internet-based chronic disease management and serve as the foundation for improving management adherence. Miao Health is exploring digital therapeutics in the fields of diabetes, hypertension, and medical obesity. For instance, in 2021, it launched a digital lifestyle management platform for hypertension, which integrates with designated medical devices to collect, display, store, transmit, and analyze physiological data such as blood pressure and blood glucose, thereby providing patients with evidence-based hypertension intervention plans.

Meanwhile, the mental health sector, with a focus on chronic disease management, demonstrated strong growth momentum in 2021. Haixinqing and Zhaoyang Health both secured substantial financing to further expand their business scale. Internet-based mental health service platforms such as Jiandan Xinli (Simple Psychology) and Yidianling not only obtained funding but also established internet hospitals, thereby augmenting the medical service component of their overall offerings. In the field of mental health, the boundary between internet-based health services and internet-based medical services is becoming increasingly blurred.

Internet-Based Full-Course Disease Management Centered on Patient Admissions by Medical Institutions

This model is characterized by deep collaboration between internet companies and hospitals, with mutual patient referral between online and offline channels and complementary services, focusing on interventions for pre-hospital preparation and post-discharge rehabilitation.

Internet-based whole-course disease management was initiated by Xiangya Hospital of Central South University in 2015. The hospital continues to jointly operate the whole-course disease management service with the third-party company Zhiyi Online. According to publicly available information, as of 2021, the hospital had established more than 100 specialized disease management teams, participated in two research projects, published over 20 academic papers, and developed operational guidelines for individual diseases, whole-course disease management pathways for specific conditions, and case management training programs.

Weimai is one of the early pioneers in implementing internet-based full-course disease management. Since 2017, Weimai has collaborated with numerous hospitals across China to create innovative, specialty-specific full-course management platforms for key departments, including obstetrics, gynecology, pediatrics, oncology, and cardiology. By organizing multidisciplinary teams led by attending physicians and supported by case managers or treatment course managers, Weimai provides patients with higher-quality, more continuous care, comprehensively empowered by Nuoyiman AI technology. Developing managed care organizations (MCOs) with Chinese characteristics is the direction of Weimai’s innovation. Weimai continues to deepen its practice of digital therapeutics (DTx) based on EMR (Electronic Medical Records) and RWD (Real-World Data), conducting clinical validations in areas such as family-based interventions for autism, management of cancer complications, and interventions for Alzheimer’s disease. Currently, Weimai has partnered with hundreds of public hospitals across China, delivering internet-based full-course disease management services for over 1,000 specific disease subtypes.

Yuanxin Technology also launched its internet-based whole-course disease management services in 2021. According to its prospectus, the company collaborates with hospitals to provide patients with a wide variety of disease course management services tailored to individual diseases and patient conditions. Currently, the Yuanxin Whole-Course Disease Management Platform has developed and operationalized management pathways for over 200 disease types, which are being promoted across various departments in dozens of hospitals throughout China.

In 2021, Medlinker expanded its existing chronic disease management services into comprehensive full-cycle disease management and enhanced its cloud-based infrastructure capabilities, including cloud laboratory testing, cloud imaging, cloud pharmacy, and cloud medical insurance. In collaboration with several industry-leading partners, Medlinker co-developed integrated cloud laboratory service solutions and an out-of-hospital medical imaging ecosystem, thereby increasing resource supply and striving to build a closed-loop system for full-cycle disease management covering “prevention, diagnosis, treatment, and rehabilitation.” Meanwhile, following the integration of Future Doctor into Medlinker, its network of more than 70 general practice clinics, specialty clinics, and ambulatory surgery centers across 16 cities nationwide will provide stronger offline support for Medlinker’s online disease management system. Overall, Medlinker has further strengthened its characteristics as an internet-based provider of full-course disease management.

Although the three models described above differ in their target populations and service offerings, there is still considerable overlap among them. For instance, given the high prevalence of chronic diseases, health maintenance models also cater to patients with chronic conditions. Meanwhile, these patients may require hospitalization due to complications, thereby becoming beneficiaries of internet-based whole-course disease management services. Therefore, the distinctions among the three models are relative rather than absolute. The purpose of this classification lies in analyzing the strategic priorities of various enterprises, while also revealing their commonalities in building integrated medical services and implementing systematic layouts.

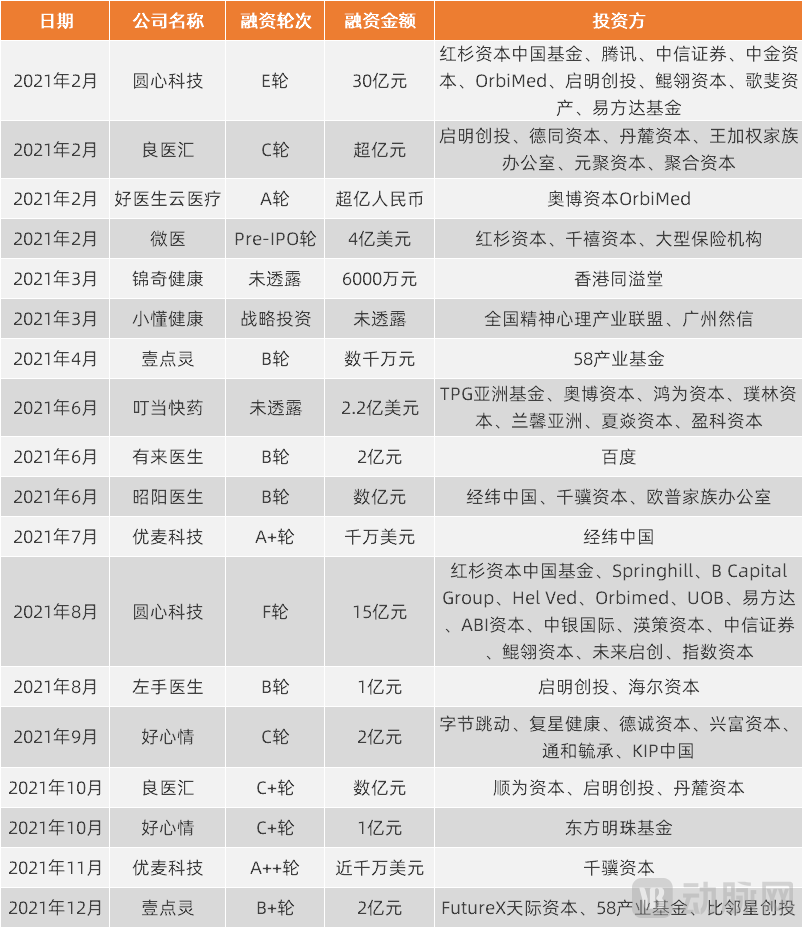

In terms of capital, there were 18 financing deals in the primary market for internet healthcare in 2021, with a total financing amount of RMB 9.7 billion; this shows a certain gap compared to the 16 deals and RMB 16.7 billion in 2020.

In 2021, four companies—WeDoctor, Zhiyun Health, Dingdang Kuaiyao, and Yuanxin Technology—filed prospectuses with the Hong Kong Stock Exchange to apply for listing, but as of now, there is no definitive news regarding their successful listings.

2021 Financing Landscape of Internet Healthcare Companies (Statistics Based on Platforms with Self-Built Internet Hospitals); Data Source: VCBeat

Furthermore, the lackluster performance and share price declines of three internet healthcare companies listed on the Hong Kong Stock Exchange pose significant challenges not only to these firms but also to the industry as a whole.

Industry insiders believe that investors have high expectations for digital health, anticipating that these companies will exert a disruptive influence in the future, thus granting them higher valuations. However, judging from the capital market situation in 2021, investor sentiment toward internet healthcare has gradually returned to rationality.

So, what should “disruptive impact” look like? There has been prior debate within the industry over whether the internet can “disrupt” healthcare services. Given that internet-based healthcare emphasizes the “medical” aspect, addressing this question requires examining the overall trajectory of the current healthcare system, rather than merely discussing from a technological perspective whether it can “disrupt.”

Currently, the heavy disease burden caused by population aging and chronic diseases has placed significant pressure on all payers. There is an overall shortage and uneven distribution of medical resources, yet the goal is to achieve equalization of public services, including healthcare services, in the future. The pathways to achieving this include: source prevention and control of diseases, ensuring relatively sufficient and accessible medical resources, and controlling costs for all stakeholders. Whether through technological or business model innovation, internet healthcare should discuss "disruption" only under the premise of alignment with macro trends.

As outlined in this article, internet healthcare has established a systematic layout in terms of service models and payers. Whether these elements can be integrated into a model aligned with major trends remains a challenge to be addressed.