2021 Global Biopharmaceutical Investment and Financing Report: Insights from 4,000+ Deals and Top 10 Hot Segments

In early 2022, VCBeat New Medicine decided to resume the statistical analysis of investment and financing data in the biopharmaceutical sector, providing industry professionals with timely insights2021 Biopharmaceutical Investment and Financing Report.

By mining and cleaning over 30,000 investment and financing records from the VCBeat database, we obtained more than 4,000 data points specific to the biopharmaceutical sector. Focusing on subsectors within the 2021 biopharmaceutical investment landscape, we use actual investment and financing data to substantiate the evolving development trends of the biopharmaceutical industry since 2013, thereby launching the “2021 Global Biopharmaceutical Investment and Financing Report.”

Global Trends

In 2021, there were a total of 1,274 financing and investment events in the global biopharmaceutical sector, representing a 34.1% increase from 2020; the total amount involved reached RMB 377.43 billion, a 34.4% increase from 2020.

Domestic Trends

In 2021, there were a total of 523 financing and investment events in China's biopharmaceutical sector, representing a 57.1% increase from 2020; the total amount involved reached RMB 118.875 billion, a 34.5% increase from 2020.

Innovative Biotechnologies Emerge as Growth Drivers in China’s Biopharmaceutical Sector

Small-molecule and large-molecule drug sectors gradually entered a bottleneck period in 2021. The primary drivers ensuring continued growth in biopharmaceutical investment and financing in 2021 stemmed from frontier biotechnology tracks such as cell therapy, gene therapy, and nucleic acid therapeutics.

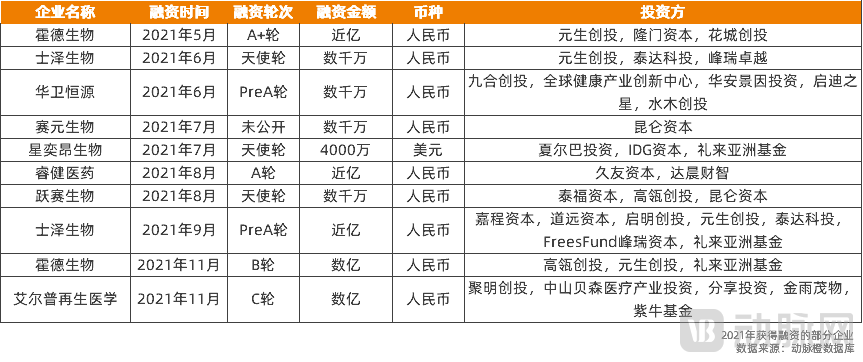

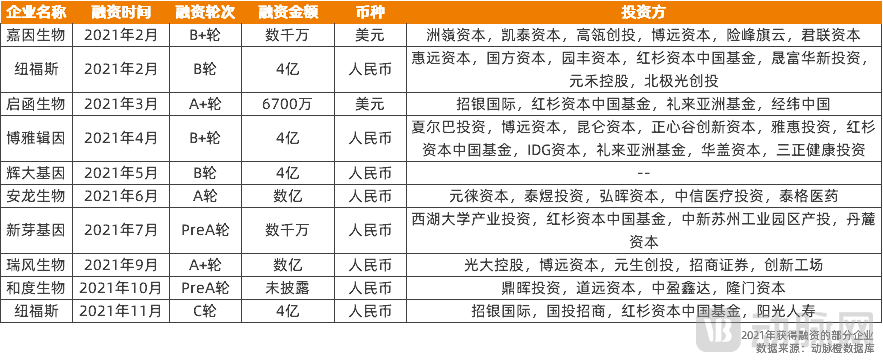

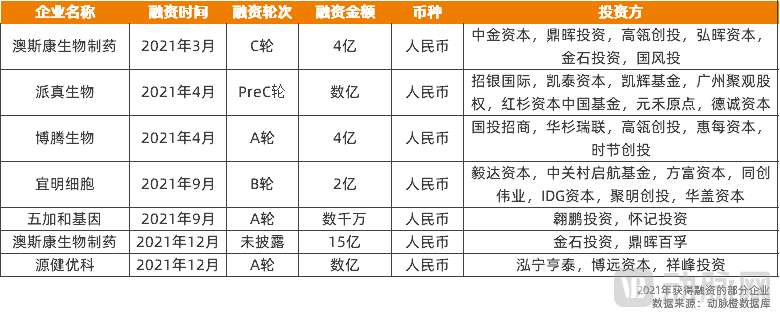

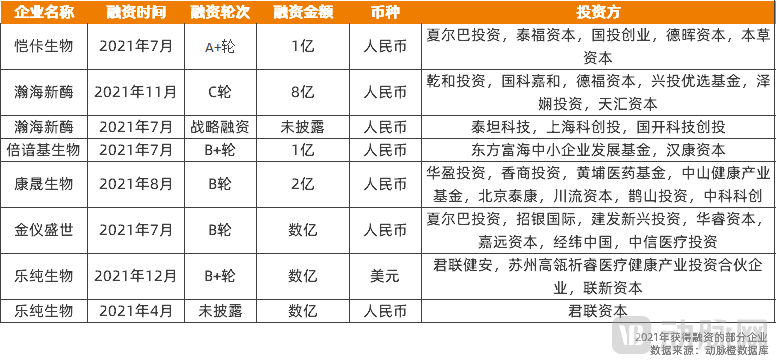

Top 10 Hot Sectors in China's Biopharmaceutical Industry in 2021

Nucleic Acid Drugs: mRNA

Cell Therapy: TIL, TCR-T, iPSC

Gene Therapy: Gene Therapy, Oncolytic Viruses

Macromolecular Drugs: ADC

Upstream Industry: Upstream Tools for Biopharmaceuticals, CGT CDMO, and Biologic Drug CDMO

Data Definition Rules

*To facilitate statistical analysis, we adhere to the following principles when processing investment and financing data:

1. The financing events covered in this report include only those from the angel round up to, but excluding, the initial public offering (IPO); they do not include IPOs, private placements, donations, mergers and acquisitions, or other such events.

2. Consolidate angel round, seed round, and seed VC into Seed/Angel Round; consolidate all Series A rounds into Series A; consolidate all Series B rounds into Series B; consolidate all Series C rounds into Series C; and consolidate all rounds after Series C but before IPO into Series D and beyond.

3. All monetary amounts in the charts and tables of this report are denominated in RMB, with foreign currencies uniformly converted into RMB based on the average exchange rate for the year in which the event occurred (the USD/CNY exchange rate for 2021 was 6.4512).

4. The data for 2021 in this report are cut off as of December 31, 2021. Any data released after December 31 will not be included in the statistical scope of this report but will be dynamically updated on VCBeat’s Investment and Financing channel.

5. Standardize financing amounts in the millions, tens of millions, or hundreds of millions to 1 million, 10 million, or 100 million, respectively; apply the same logic for amounts exceeding these thresholds.

6. The financing events/amounts presented in the chart include only those that have been publicly disclosed, excluding undisclosed events.

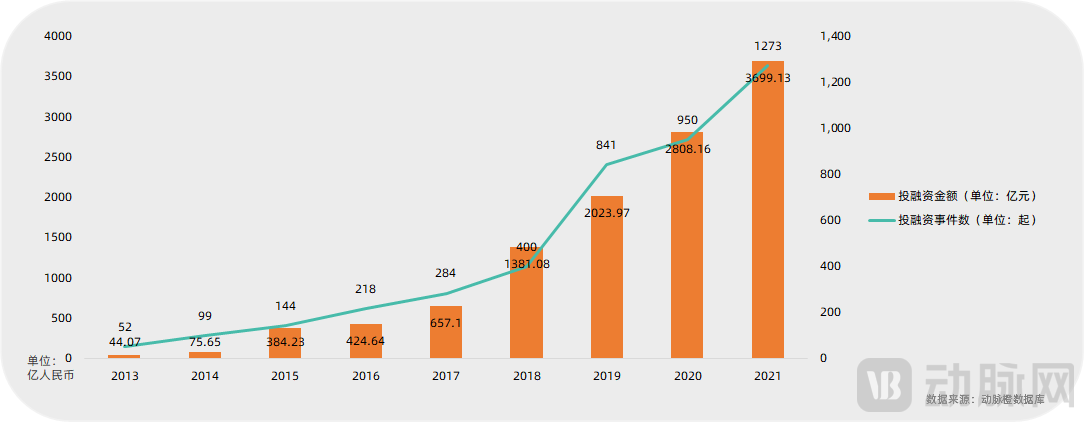

Global Trends in Investment and Financing in the Biopharmaceutical Sector

We recorded a total of 1,273 financing and investment events in the global biopharmaceutical sector in 2021, representing a 34.0% increase from 2020; the total amount involved reached RMB 369.913 billion, a 31.7% year-on-year increase. Overall, the global biopharmaceutical sector continues to witness robust growth in financing and investment activity, with both transaction volume and growth rate remaining strong. Further growth is expected in 2022.

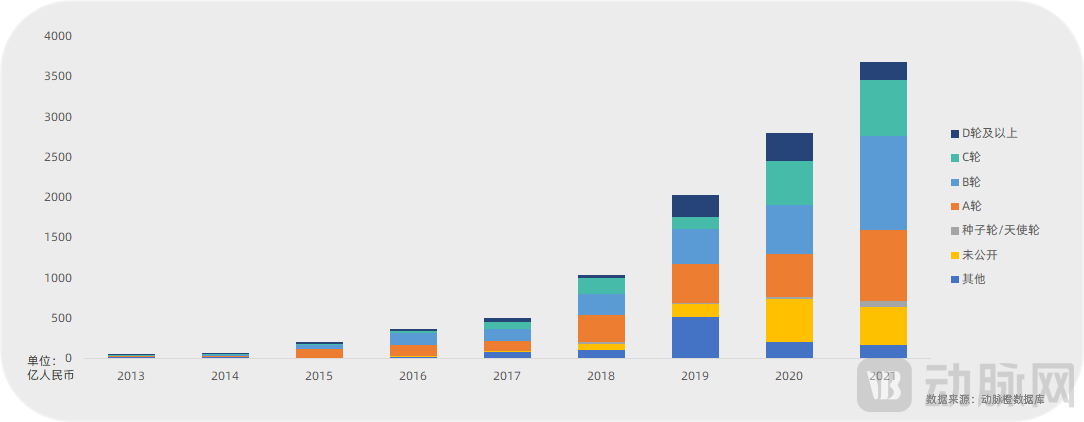

Over the past few years, the trend of investment and financing in the biopharmaceutical sector concentrating on companies at Series B and later stages has become increasingly pronounced. In 2020 and 2021, the proportion of total financing amounts raised by companies at Series B and beyond reached 53.2% and 55.4%, respectively. This indicates that leading global biopharmaceutical companies are gradually maturing, transitioning from early-stage proof-of-concept and exploration phases to the stage of establishing viable business models.

In terms of investment and financing activities, the global biopharmaceutical sector has long been dominated by Series A rounds. In 2020 and 2021, Series A deals accounted for 30.2% and 34.3% of the total, respectively. Most companies securing Series A funding are focused on cutting-edge biotechnology fields. Given the accelerating pace of technological translation in the biotech industry, Series A rounds are expected to remain the dominant form of investment and financing in the biopharmaceutical sector in the future.

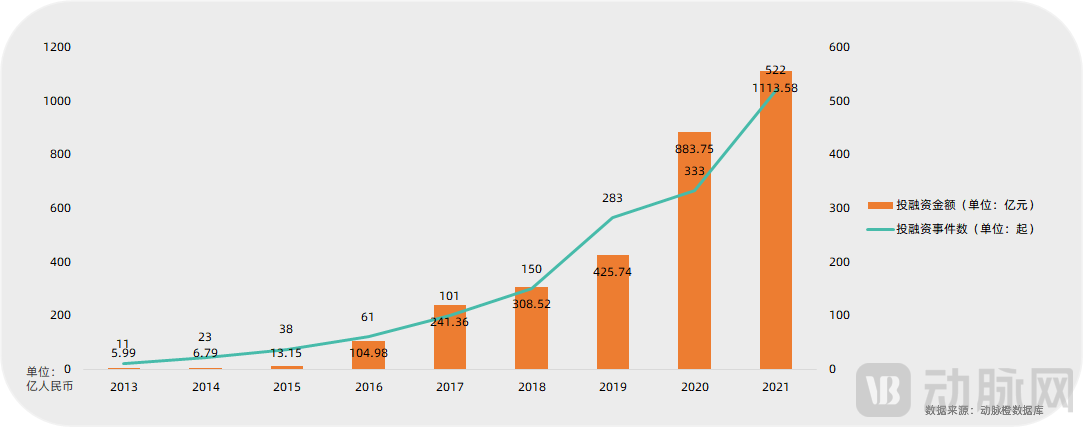

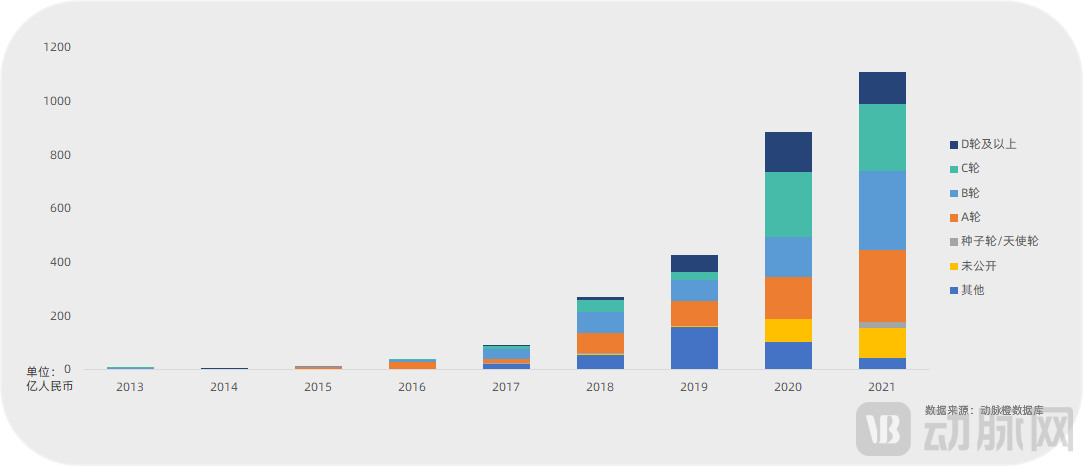

Investment and Financing Trends in China's Biopharmaceutical Sector

Driven by the pandemic, investment and financing in China’s biopharmaceutical sector experienced substantial growth in 2020. The total financing amount reached RMB 88.375 billion, representing a 107.6% increase compared to 2019. Investment and financing further increased in 2021 relative to 2020. The number of financing transactions reached 522, a 53.1% year-on-year increase from 2020, while the total financing amount amounted to RMB 111.358 billion, marking an additional 26.0% growth over 2020.

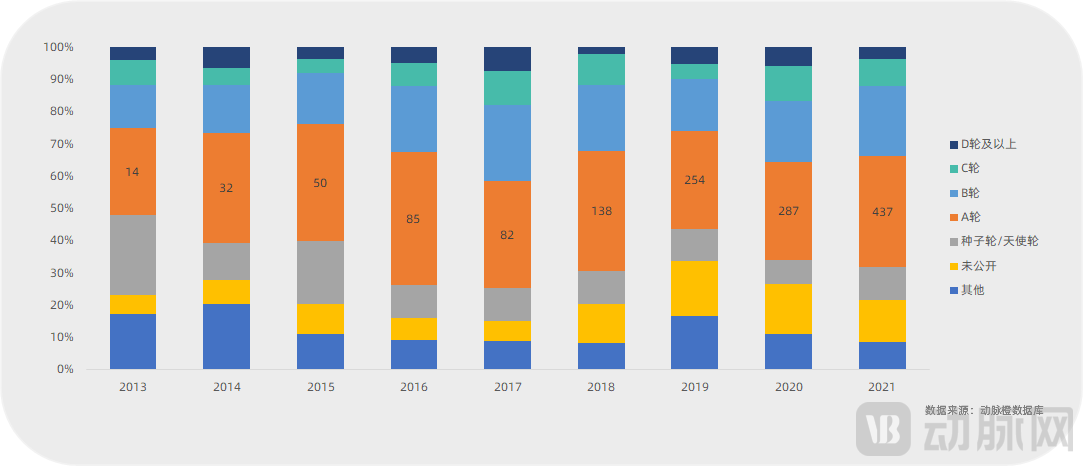

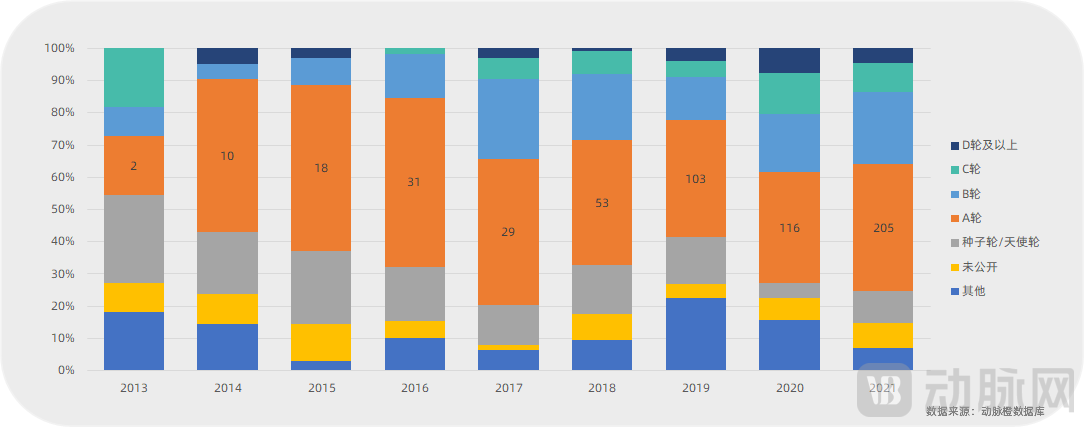

The distribution of funding amounts across various rounds in China aligns with global trends. In 2020 and 2021, the proportion of total funding accounted for by Series B and later rounds reached 60.9% and 59.6%, respectively. In fact, as recently as 2017, funding from Series B and subsequent rounds constituted only 21.5% of the total. It is speculated that the primary driver behind the growth in late-stage financing from 2018 to 2021 was the maturation of domestic IPO exit pathways.

Distribution of Financing Rounds by Stage In China, the distribution of financing rounds is largely consistent with global trends, with Series A financing events remaining dominant over the long term. In 2020 and 2021, Series A deals accounted for 34.8% and 39.3% of the total, respectively.

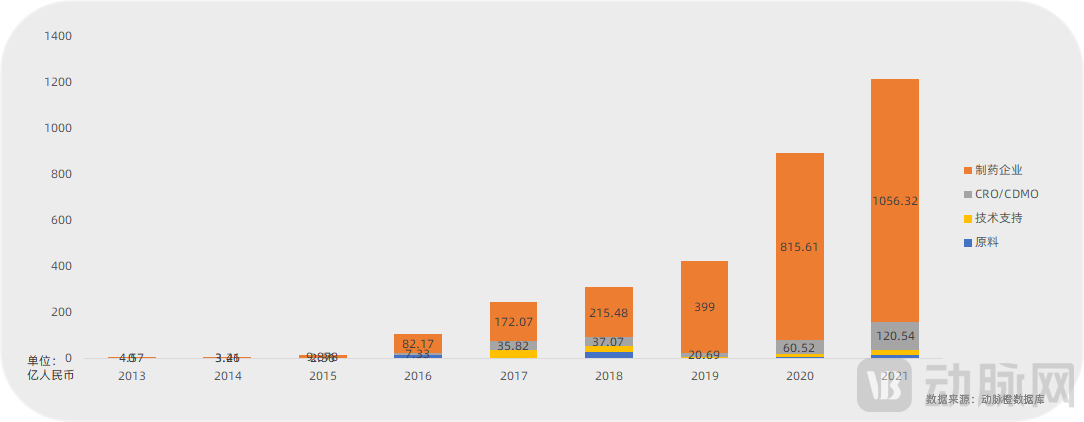

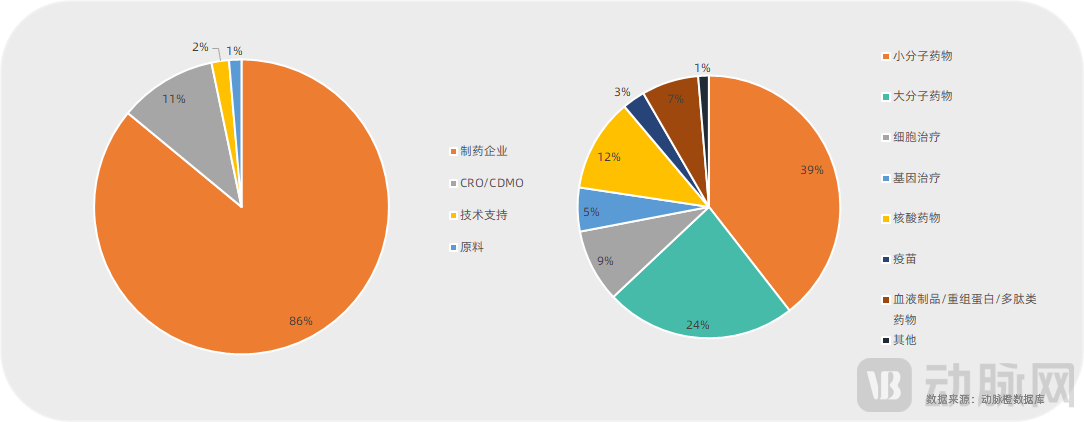

Investment and financing in China’s biopharmaceutical sector have long centered on the pharmaceutical industry. However, emerging trends indicate a significant surge in interest in CRO/CDMO from 2019 to 2021, with funding amounts increasing by 192.5% in 2020 compared to 2019, and by 99.17% in 2021 compared to 2020. The specific drivers of this growth will be further elaborated in the subsequent sector analysis.

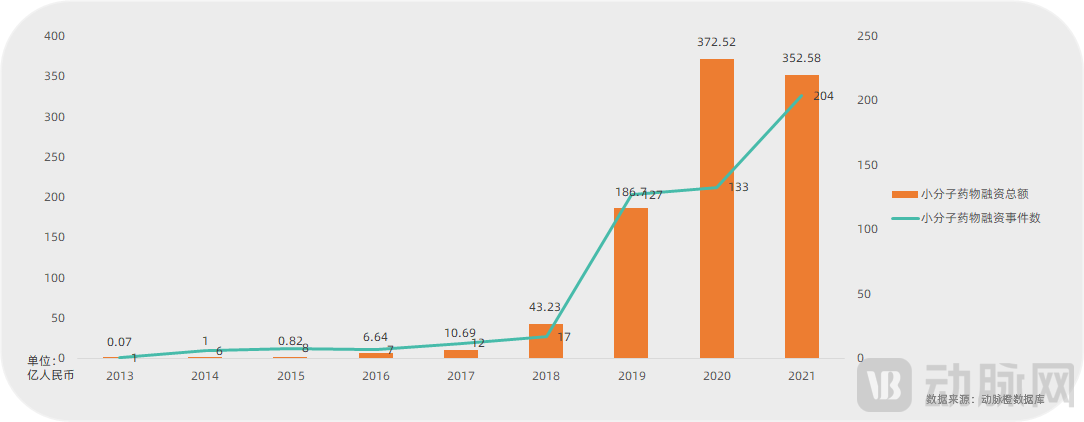

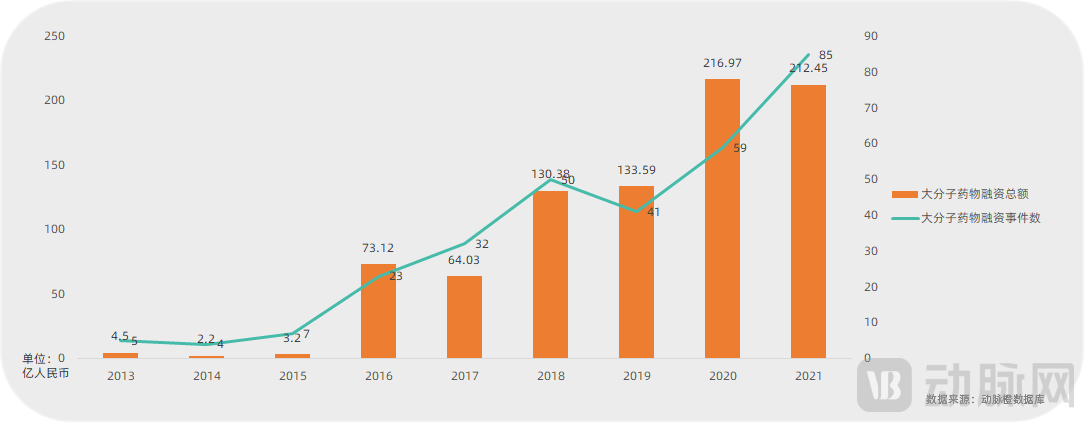

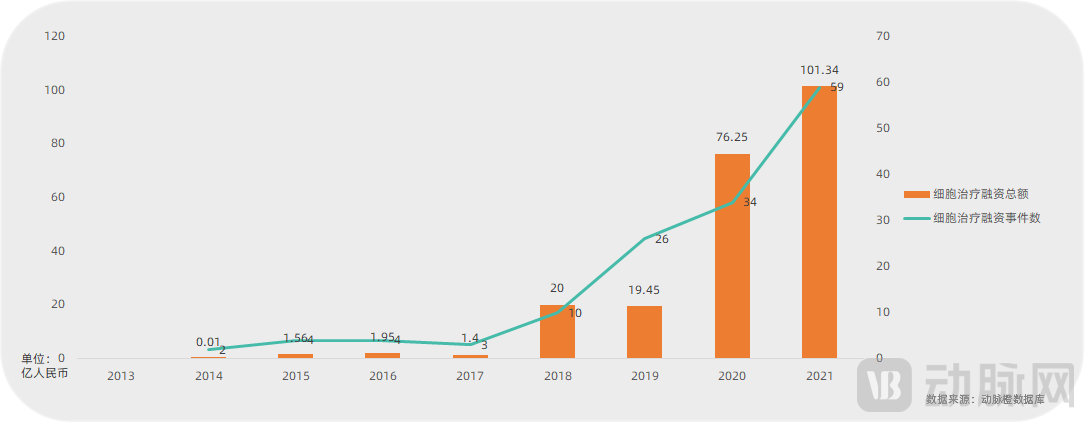

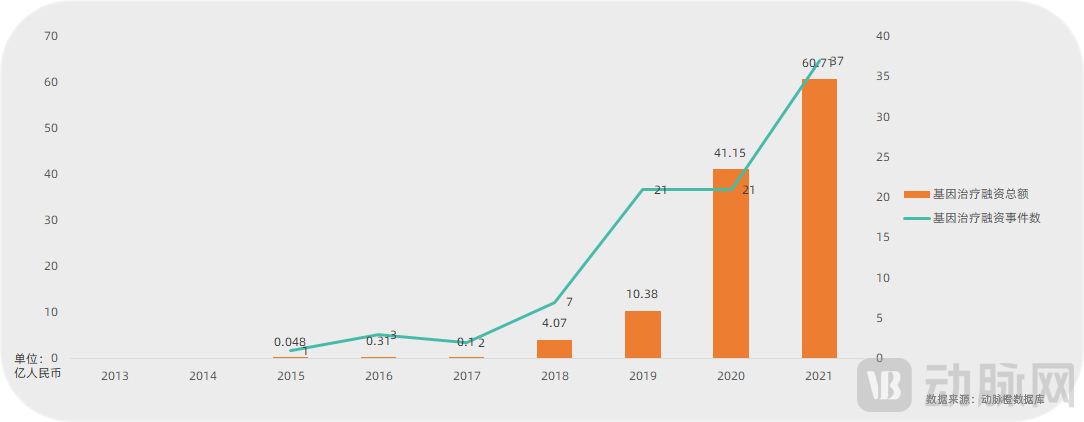

Small-molecule drugs and antibody-based therapeutics have long accounted for a significant share of China’s biopharmaceutical sector. In recent years, the emergence of novel technological platforms has further driven growth in small-molecule drugs. However, both categories hit a growth bottleneck in 2021. In contrast, innovative biotechnology fields—such as antibody–drug conjugates (ADCs), cell therapy, gene therapy, and nucleic acid-based drugs—experienced marked growth during 2020–2021, becoming the primary drivers of overall investment and financing growth in the biopharmaceutical sector at this stage.

In 2021, financing and investment in the CRO/CDMO sector accounted for approximately 10% of the total, with a trend of further increase. Among various sub-sectors, the three frontier technology fields—cell therapy, gene therapy, and nucleic acid drugs—saw significant growth in their shares in 2021, reaching 9%, 5%, and 12%, respectively.

Investment and Financing Trends in Subsectors of China's Biopharmaceutical Industry in 2021

The small-molecule drug sector has experienced significant growth in recent years, driven by the emergence of new technologies and the adoption of the license-in model. The application of artificial intelligence (AI) in small-molecule drug discovery is gradually maturing, while novel mechanisms of action such as PROTACs and molecular glues remain in relatively early stages. Furthermore, the capital-intensive nature of the license-in model has further enhanced the sector’s ability to attract investment.

The field of large-molecule drugs began to rise rapidly around 2016 and reached a new peak in 2020–2021, driven by the surge in investment and financing across the broader healthcare sector. The fact that 2021 levels were broadly on par with those of 2020 was partly attributable to the heightened activity in the antibody–drug conjugate (ADC) space in 2021. Given the accelerated pace at which leading companies are entering the secondary markets, primary-market interest in large-molecule drugs is unlikely to see further growth.

Financing in the cell therapy sector heated up further in 2021, with total funding surpassing the RMB 10 billion mark. The successful approval of two CAR-T products in 2021 provided a significant boost to industry development. Meanwhile, investment focus within the cell therapy field increasingly shifted toward broader application scenarios, particularly evident in cell therapies for solid tumors.

The gene therapy sector has witnessed a significant surge in interest over the past two years. Our analysis primarily covers three key areas: traditional gene therapy, gene editing therapies, and oncolytic virus therapies, all of which demonstrated robust growth momentum in 2021. In light of the multifaceted clinical advances achieved in gene therapy during 2021, the field is expected to maintain its upward trajectory in the foreseeable future.

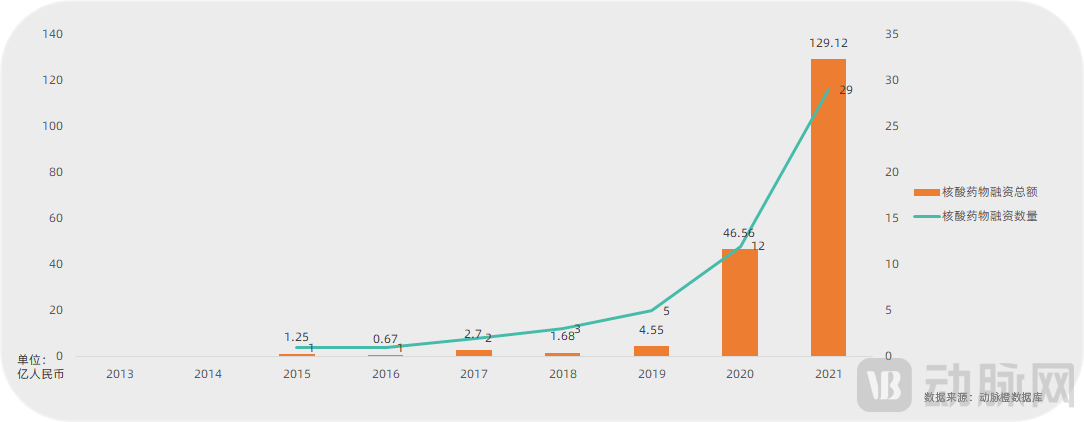

Nucleic acid therapeutics has been the fastest-growing subsector within biopharmaceuticals over the past two years. The outstanding performance of mRNA vaccines during the pandemic has attracted significant attention from investors, thereby driving increased financing across the entire subsector. The explosive growth in funding observed in 2021 was primarily attributable to two substantial financing rounds secured by Abogen Biosciences. In light of this, the nucleic acid therapeutics sector is expected to remain active in 2022, although further growth beyond the 2021 levels may not materialize.

Top 10 Hot Biopharmaceutical Sectors in China in 2021

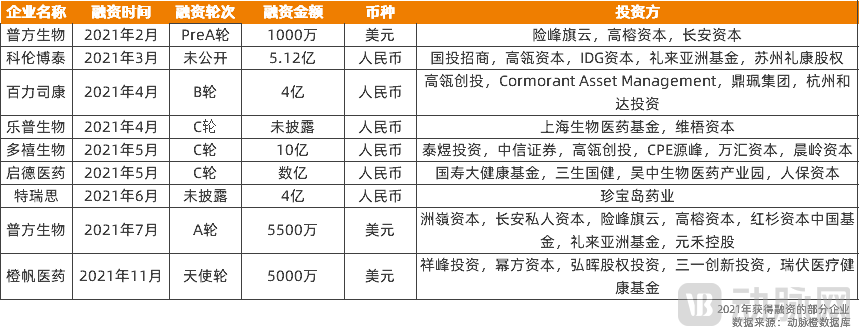

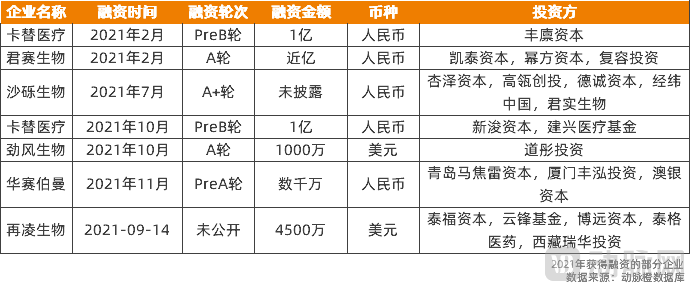

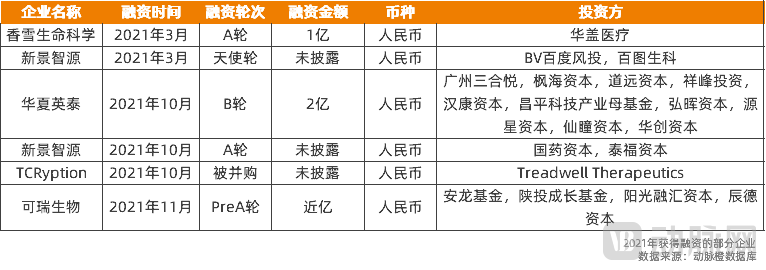

The mRNA sector was undoubtedly one of the hottest investment tracks during the pandemic. In 2021, Abogen Biosciences’ Series C financing round, exceeding $700 million, set a new record for fundraising in China’s biopharmaceutical industry—a milestone that may be difficult to surpass in the near term. That same year, leading companies in the mRNA field, including Abogen Biosciences, Stemirna Therapeutics, Xinhe Biotechnology, and Qichensheng Biotech, successively completed new rounds of financing. Given the diverse application scenarios of mRNA vaccine products and the emergence of numerous new enterprises, the mRNA sector is likely to remain a key focus of capital attention in 2022.

The approval of RemeGen’s Disitamab Vedotin (Aidixi) and its license-out deal worth up to $2.6 billion have sparked a surge of interest in the antibody-drug conjugate (ADC) field in China. The domestic ADC landscape is rich with innovative enterprises, and many traditional pharmaceutical giants are prioritizing ADCs as a key strategic segment during their transition toward innovation. The ADC sector is expected to maintain stable long-term growth.

Following the approval of two CAR-T products, immune cell therapy products for solid tumors have garnered increased attention. Due to their ability to infiltrate solid tumor tissues, Tumor-Infiltrating Lymphocytes (TILs) can penetrate the tumor microenvironment more readily than CAR-T cells, and are thus considered one of the key technological approaches for immune cell therapies to overcome the challenges of treating solid tumors.

Similar to TIL therapy, TCR-T therapy also witnessed multiple financing events in 2021, driven by the rising attention toward cell therapies for solid tumors. As an immunocellular therapy that emerged almost concurrently with CAR-T, TCR-T has maintained unique advantages in the treatment of solid tumors due to its ability to specifically recognize a wide range of tumor antigens.

The rapid rise of the iPSC sector in China is closely linked to industrial advancements abroad. Following the pivotal clinical progress achieved by Fate Therapeutics with its iPSC-derived CAR-NK product, the iPSC field has garnered widespread attention in China. Beyond oncology, iPSC technology is currently being applied to other areas, including neurodegenerative diseases and heart failure.

In early 2021, the gene therapy products of Nuofus (Visumab) and Boya Ji Yin (EdiGene) successively received implicit approval from the National Medical Products Administration (NMPA) and initiated registrational clinical trials, marking the formal entry of domestically produced gene therapy products into the clinical stage. Consequently, investment and financing in the gene therapy sector experienced significant growth in 2021, with multiple funding rounds occurring in both traditional gene therapy and gene editing therapies.

Following the entry of multiple products into clinical trials, the oncolytic virus sector has witnessed frequent large-scale financing rounds. Leading companies in the field, such as ImmuneOnco, Binhui Biopharma, and Fenuo Jian, are currently intensifying their efforts to advance clinical studies. It is anticipated that the disclosure of positive clinical results will likely spark a new wave of interest in the oncolytic virus sector.

The biological drug CDMO sector is primarily driven by positive signals from its downstream industries. An increasing number of large-molecule biopharmaceutical companies are entering late-stage clinical trials, generating substantial demand for outsourced process development and manufacturing. Consequently, the biological drug CDMO field attracted significant attention from investment institutions in 2021.

Driven by the rapid surge in popularity of the cell and gene therapy (CGT) sector, the upstream CGT industry has experienced concurrent growth, particularly within the CGT contract development and manufacturing organization (CDMO) segment, which focuses primarily on the industrial-scale production of viral vectors required for CGT products. The momentum in the CGT CDMO industry is expected to remain aligned with that of the broader CGT sector, ensuring it remains a key area of interest in the near term.

Upstream industries associated with the entire biopharmaceutical sector include reagents, consumables, and instruments and equipment such as culture media, enzymes, recombinant proteins, and single-use reaction systems. During the pandemic, disruptions to overseas supply chains severely restricted the availability of imported products, highlighting the importance of domestic substitution. Consequently, the localization of upstream biopharmaceutical industries garnered significant attention in 2021.

The above is an excerpt from the report. Scan the mini-program QR code to access the "2021 Global Biopharmaceutical Investment and Financing Report."