Teladoc and Livongo Merger Drives Doubling of Growth Within a Year Amid Pandemic and Policy Tailwinds

Livongo

Chronic Disease Management Service Provider

Driven by the synergy between pandemic-induced acceleration and favorable policy support, the internet healthcare industry has entered a golden period of growth. Among its various segments, appointment registration and online consultation platforms account for the largest share of cumulative users. However, these online consultation platforms face their own pain points: they are suitable only for minor ailments, unable to provide definitive diagnoses for complex or rare conditions, and thus do not engage with the core of medical services. Consequently, user stickiness remains low, hindering the delivery of continuous care.

Therefore, expanding service coverage has remained a key focus for online consultation platforms, with chronic disease management regarded as a critical area for growth. Because patients with chronic conditions require regular follow-up visits and long-term prescription renewals, these needs align perfectly with the capabilities of online consultation platforms. Consequently, many digital health companies are actively strategizing and investing in this sector.

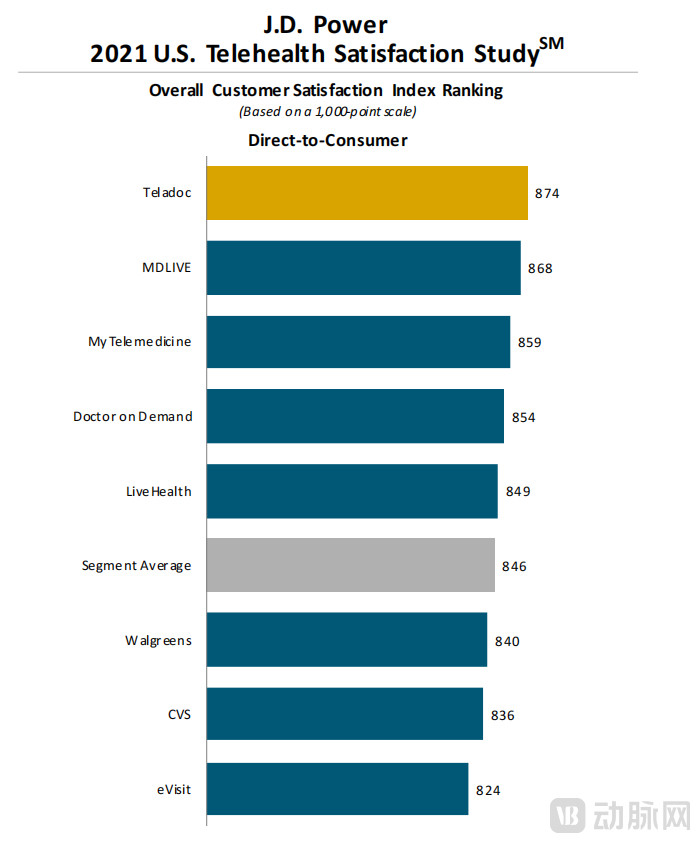

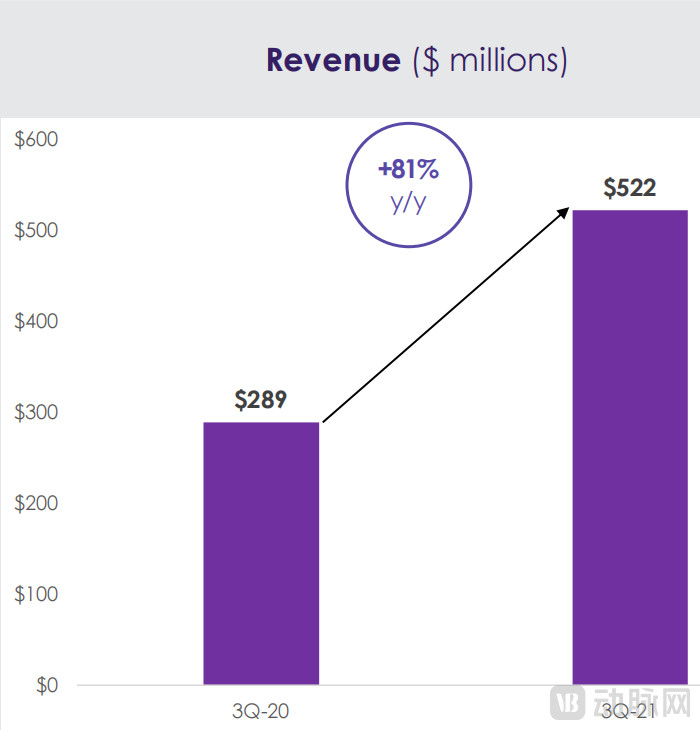

In the United States, there is a ready-made case in point. In August 2020, Livongo, a company specializing in chronic disease management, was acquired by Teladoc, a giant in internet healthcare, to expand Teladoc’s business segments. More than a year later, Teladoc reported an 81% year-over-year increase in third-quarter revenue, reaching $522 million; it projected full-year 2021 revenue of $2.015 billion to $2.025 billion, representing approximately 108% year-over-year growth; total visits in the third quarter exceeded 3.9 million, up 37% from the third quarter of 2020. In the J.D. Power 2021 U.S. Telehealth Satisfaction Study, Teladoc ranked first in consumer satisfaction. What exactly has this acquisition brought to Teladoc?

Overall, three factors determine Teladoc’s market growth: first, consumer demand and acceptance; second, providers’ willingness and capacity to deliver telemedicine services; and third, changes in reimbursement policies that enable U.S. healthcare spending to cover telemedicine.

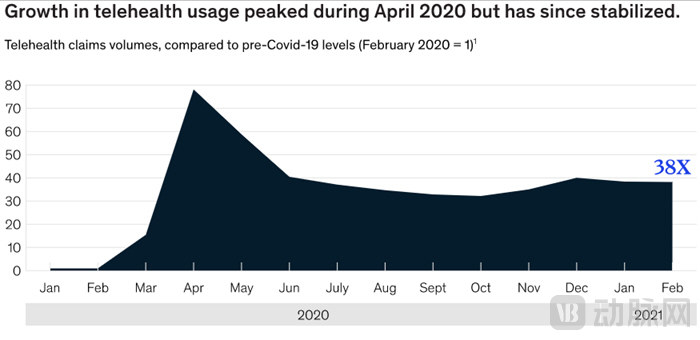

First, from the perspective of consumer demand, a McKinsey report indicates that just two months after the COVID-19 pandemic struck globally in April 2020, telehealth utilization was 78 times higher than in February 2020. Even at the current stage, where the epidemic situation is relatively stable, telehealth utilization has remained steady at 38 times the pre-pandemic level. Approximately 40% of consumers consider telehealth an important modality for their future care needs, a figure that stood at only 11% before the pandemic. Furthermore, some temporary policies conducive to expanding telehealth use have been formalized. For instance, the Centers for Medicare & Medicaid Services (CMS) expanded the list of reimbursable telehealth codes in its 2021 Physician Fee Schedule.

Undoubtedly, even as the pandemic is gradually brought under control in the future, telemedicine will remain a critical component of healthcare delivery, driven by evolving perceptions among patients and providers as well as shifts in regulatory attitudes. Telemedicine is currently a highly fragmented industry, and only through the integration of services across multiple specialties can comprehensive care solutions that deliver optimal patient experiences be provided. From an industry perspective, consolidation is inevitable to achieve the requisite level of service quality.

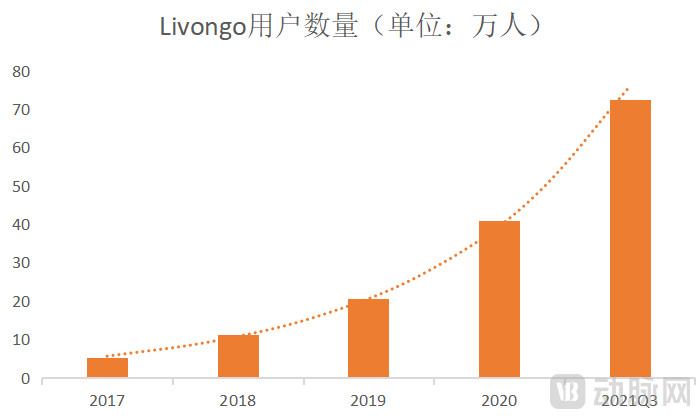

Following its acquisition of Livongo, Teladoc has positioned itself as a leader in the telehealth market, given that its services cover nearly every segment of the telehealth industry. Since being acquired by Teladoc, Livongo has experienced rapid growth, with its member base increasing from 553,000 in 2020 to 725,000 by the end of the third quarter of 2021, representing a 31% growth rate. Although this growth rate does not match the over-100% figures seen in previous years, this is attributable to the previously smaller base; in terms of absolute customer acquisition, the growth remains substantial. This surge is primarily driven by conversions from Teladoc’s extensive user base of 52.5 million, which was a key rationale behind the initial merger.

Examining Teladoc’s financial report for the second quarter of 2021, Livongo had 715,000 members in Q2 2021, representing a significant growth rate of 74.4% compared to 410,000 during the same period last year. However, the net increase in membership for the entire third quarter of 2021 was only 10,000. In fact, Livongo’s high growth rate peaked within nine months after the merger. Does this imply that the actual customer base for single-disease chronic disease management is not substantial? Let us refrain from jumping to conclusions and continue to examine the data.

From a market perspective, digital therapeutics focused on chronic disease management, particularly in the area of diabetes care, have a large potential patient base—for example, there are over 30 million people with diabetes in the United States. However, engagement rates among individuals with chronic conditions in health management programs remain low. Taking Livongo as an example, although the service is fully covered by employers, its actual enrollment rate among recruited diabetic patients has long hovered around 35%. This means that even when offered free of charge, only one-third of individuals with chronic diseases are willing to engage in long-term chronic disease management. Therefore, for Livongo to expand its membership, it must continuously broaden its pool of potential customers. Its sale to Teladoc, which boasts the largest domestic customer base, was aimed precisely at expanding membership numbers, and the growth observed in the year following the acquisition has validated this strategy. The slowdown in growth seen in the most recent quarter does not necessarily indicate any underlying issue, as Teladoc itself continues to experience rapid growth, and its customers will gradually transition to Livongo’s platform.

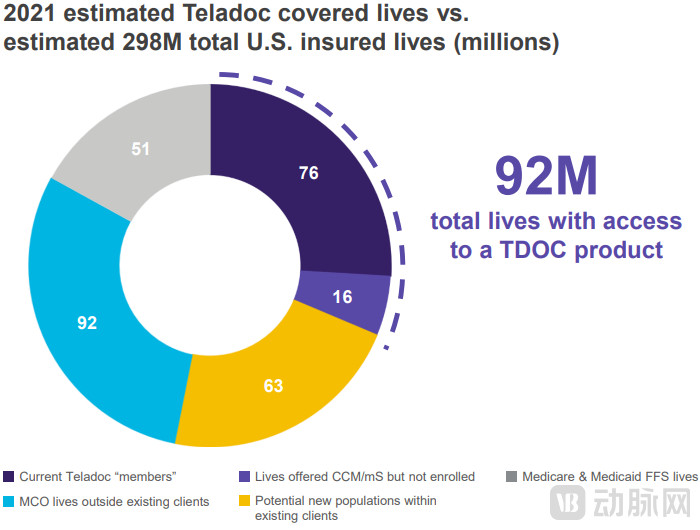

From Teladoc’s perspective, the acquisition was also highly cost-effective. As of 2021, approximately 298 million people in the United States were covered by health insurance. Teladoc already served 76 million of these individuals through insurers and various distributors, with an additional 16 million potentially convertible into customers for its chronic condition management services. This means that currently, 92 million people (accounting for about 31% of the insured population in the U.S.) have access to Teladoc’s products. Furthermore, there are approximately 63 million potential customers who could be reached through existing clients, managed care organizations, and Medicare and Medicaid fee-for-service programs. Therefore, the integration of Livongo has positively contributed to the growth of Teladoc’s membership base.

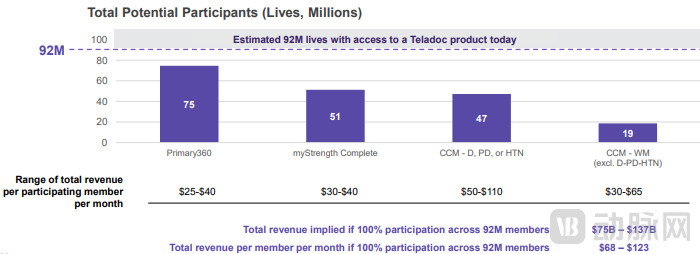

Furthermore, Teladoc believes that among its current 92 million users, there is an annual revenue opportunity of at least $75 billion. If customers choose to adopt multiple products within Teladoc’s service portfolio, revenues could rise significantly, with optimistic estimates reaching $137 billion. This is because 40% of Americans with chronic conditions suffer from two or more chronic diseases (such as diabetes and hypertension), all of whom can benefit from Livongo’s comprehensive care management solutions. According to Teladoc’s calculations, an employer with 10,000 members adopting a multi-product service portfolio would generate 4.1 times the revenue compared to single-condition services.

Teladoc’s revenue in the third quarter of 2021 increased by 81% year-over-year, reaching $522 million. Among this, enterprise-side revenue grew by 99% year-over-year, while pay-per-visit revenue rose by 18% year-over-year. The growth rate for domestic business in the United States was 89%, whereas international regions saw only a 17% increase, as Livongo’s operations are currently limited to the U.S. market. Total visits in the third quarter reached 3.9 million, representing a 37% year-over-year increase, which accelerated compared to the approximately 28% growth rate in the previous quarter. This was primarily driven by a 40% increase in domestic U.S. visits and a 19% rise in international visits.

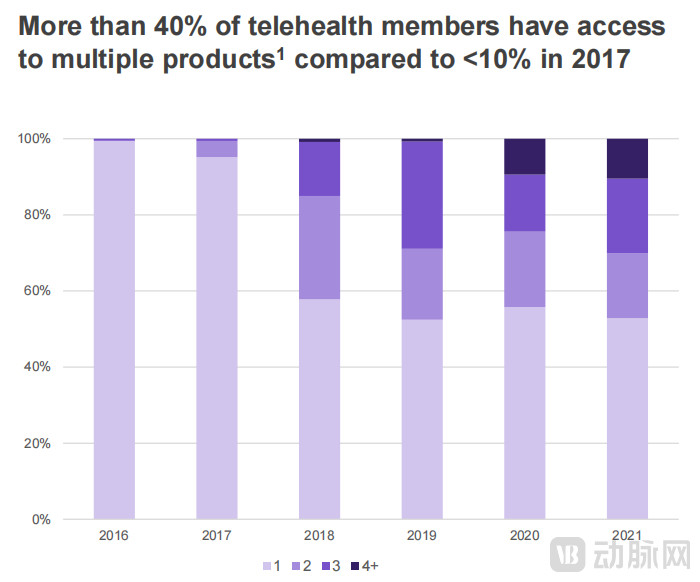

U.S. paying members increased by approximately 2% year-over-year in the third quarter, marking a slowdown from the previous year’s growth rate. However, the average monthly revenue per paying member and per pay-per-use customer showed a gradual upward trend, and these two metrics will drive future revenue growth. Most notably, the proportion of chronic disease management members enrolled in more than one program tripled year-over-year, reaching 24% in the third quarter of 2021. Over 40% of telehealth members had access to multiple product combinations, compared to less than 10% in 2017.

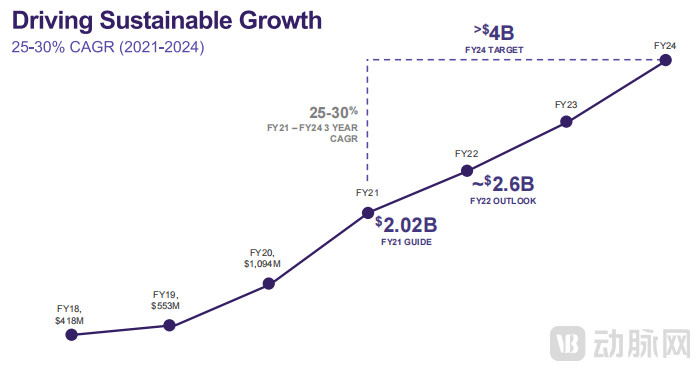

Finally, Teladoc raised its 2021 revenue guidance to between $2.015 billion and $2.025 billion, implying an annual growth rate of 85% for 2021, surpassing prior market expectations. During its Investor Day, management also provided a three-year performance outlook, projecting that fiscal year 2024 revenue would exceed $4 billion. This indicates a compound annual growth rate (CAGR) of 25%–30% over the next three years, effectively doubling its fiscal 2021 revenue scale within that period.

The confidence in setting such ambitious goals is closely tied to Teladoc’s successful market expansion. In the third quarter, Teladoc signed new agreements with CVS Health and Centene and was selected by Canada Health Infoway as its provider of virtual care services, which cover approximately 60% of Canada’s population. Teladoc established a strategic partnership with Philips to deliver online healthcare solutions in Australia and New Zealand. Additionally, Teladoc entered into an agreement with Latin American telecommunications giant Telefónica to expand their existing partnership, extending Teladoc’s services to over 60 million people in Brazil. Through collaboration with Microsoft, Teladoc integrated its health platform into Microsoft Teams to streamline clinicians’ workflows and enhance user experience. Notably, because these new enterprise clients require secondary enrollment of employees, the associated member counts have not yet been included in Teladoc’s current membership figures, nor have they been converted into Livongo users. The appeal of Livongo’s chronic condition management solutions has also been a significant factor contributing to Teladoc’s smooth expansion.

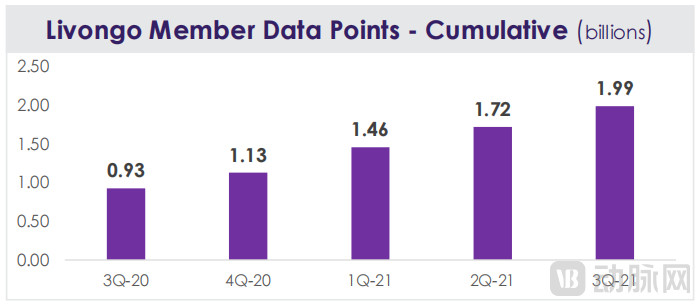

In addition to its own product solutions, Livongo has seen a substantial increase in the volume of data collected, thanks to the continuous growth in its membership. As of the third quarter of 2021, Livongo had accumulated 1.99 billion data points. This growing data repository will serve as a key competitive advantage for Teladoc in the future. Leveraging this strength, Teladoc ranked highest among direct-to-consumer providers in the J.D. Power 2021 U.S. Telehealth Satisfaction Study, scoring nearly 30 points above the category average. Incidentally, Teladoc is continuing to integrate acquired business units, including Livongo, and aims to build an internet healthcare platform centered on individual user health, integrating services such as online consultations, chronic disease management, and mental health support.

An analysis of Teladoc’s operational performance in the year following its acquisition of Livongo indicates that chronic disease management serves as a valuable complement to telehealth platforms, both in terms of revenue generation and customer acquisition. However, it is also evident that single-disease chronic care models face a revenue ceiling, even under the premise of full employer coverage in the United States. For chronic disease management to become a cornerstone of digital health, its scope must expand beyond diabetes to encompass a broader range of conditions. Furthermore, timely tracking and intervention by AI technologies and health management teams are effective means of helping patients achieve their health goals within chronic care programs. As data accumulates, the auxiliary diagnostic capabilities generated through AI’s learning and refinement of this data will constitute a key competitive advantage for service providers in the future.

According to data from Bida Consulting, online consultation currently accounts for the largest proportion of cumulative users in China’s internet healthcare sector, at 48.3%, with a penetration rate as high as 86%. As representatives of online consultation platforms, Ping An Health and WeDoctor have expanded their business into chronic disease management, similar to their foreign counterparts. For instance, Ping An Health’s family doctor product provides users with electronic health records, customized year-round health management services, 24/7 care, and second-level response times for physician services. Its core competitiveness lies in its proprietary team of physicians combined with an AI-assisted diagnostic system, which ensures controllable medical service quality and risk.

Members of WeDoctor’s digital chronic disease management service can access comprehensive care through its internet hospital, including personalized treatment and rehabilitation plans, ongoing follow-up consultations, prescription renewals and medication dispensing, monitoring of key health indicators, and professional guidance on diet, wellness, and exercise. For enterprise clients’ employees and end-users, WeDoctor provides integrated health management services covering online diagnosis and treatment, referrals, health monitoring, and health coaching.

From the user’s perspective, the services offered by such online platforms are functionally sound; the real barrier is payment. As evidenced by the earlier case of Teladoc in the United States, even with a mature commercial insurance payment system in place, a significant proportion of users remain reluctant to adopt these services. If payment issues are not resolved, the rollout of chronic disease management businesses will be exceptionally challenging.

Unlike the mature group-oriented corporate commercial health insurance market in the United States, commercial health insurance in China primarily targets individual customers. However, from a business model perspective, a market can be established as long as there are payers willing to cover the costs. Payers with willingness to pay in the healthcare market can be broadly categorized into consumer-side (C-end) and business-side (B-end) entities. Setting aside the C-end for now, enterprises on the B-end generally fall into two categories: those that offer healthcare services as value-added benefits to enhance customer stickiness, and those that aim to improve employee health and well-being.

Policy-level initiatives are also encouraging commercial insurers to enhance health management services. In 2019, the China Banking and Insurance Regulatory Commission (CBIRC) revised the “Measures for the Administration of Health Insurance,” adjusting the cap on health management service costs from no more than 12% of gross premiums under the previous version to 20% of net premiums. Based on the CBIRC’s target for the commercial health insurance market size to exceed RMB 2 trillion by 2025, this 20% share translates into a market scale of RMB 400 billion.

Building on these premises, Ping An Good Doctor has addressed the needs of B2B enterprise clients by offering its “Family Doctor Membership” product, helping insurers, banks, and other enterprises provide warmer, more personalized services to their customers, thereby enhancing customer stickiness and improving renewal conversion rates. Leveraging the empowerment of the Ping An Group, Ping An Good Doctor has launched a series of healthcare benefit products embedded within insurance policies, such as “Ping An Life Zhenxiang RUN.” The integration of Ping An Good Doctor’s medical service offerings broadens the scope of medical services covered by insurance products and enriches the overall service portfolio. The interconnection between medical provider networks and insurance technology platforms streamlines the payment process, while the proactive health management enabled by the inclusion of medical services generates valuable user data for health tracking and rational premium control. These initiatives represent Ping An Good Doctor’s efforts at the payment level.

Since 2019, WeDoctor, a digital healthcare service platform, has launched an innovative chronic disease management service in Tai’an City, Shandong Province, integrating “Internet + health insurance + medical care + pharmaceuticals.” This initiative represents WeDoctor’s practical implementation of building an Internet-based Chronic Disease Medical Consortium through its internet hospitals. Currently, among the 28 internet hospitals under WeDoctor, 18 have obtained health insurance accreditation and enabled online health insurance payment.

This model encompasses the entire online-to-offline workflow for chronic disease management, establishing a closed-loop, full-lifecycle management system covering “prevention, diagnosis, treatment, management, and health promotion.” It provides patients with services such as follow-up consultations, medication purchasing, insurance reimbursement, data management, and digital interventions. Furthermore, it strengthens health insurance supervision and cost containment through standardized, end-to-end digital management. Building a digital accountable care system centered on membership-based chronic disease management via internet hospitals constitutes a key future business segment for WeDoctor.

Of course, in addition to diabetes, chronic disease management in China is expanding to cover other conditions. For instance, the chronic disease management platform Medlinker has expanded its coverage from initially focusing on liver diseases to include cardiovascular diseases, diabetes, respiratory asthma, oncology, chronic kidney disease, HIV, pediatrics, gynecology, general practice, traditional Chinese medicine, and mental health. Medlinker aims to strengthen doctor-patient relationships through chronic disease management, thereby establishing deeper engagement for follow-up services.

Following the joint establishment of the Cardiology Center with Professor Hu Dayi, JD Health accelerated its entry into the health management sector by intensively launching 27 specialized centers, including a Chronic Disease Management Center. JD Health enhances user experience, cultivates health management habits, and boosts user stickiness. This approach creates a win-win scenario for all three parties: users adopt healthier lifestyles through health management; physicians generate income by guiding users to purchase appropriate products; and JD Health secures profits through increased sales volume.

Over the past two years, accelerated by the pandemic, individuals born after 1970—who have received systematic education, possess a profound understanding of technology, and are now approaching age 50, entering the stage where chronic disease management becomes critical—have demonstrated strong health awareness. They trust in science and recognize the importance of consistent, daily health maintenance. Building on this foundation, those born in the 1980s and 1990s place even greater emphasis on chronic disease management. As many of them are only children, they bear heavier familial burdens, rely heavily on the internet, and exhibit a willingness to pay for health services. Developing targeted solutions for these populations is a historical mission for the health and wellness industry.

This demographic aims to minimize disease incidence and prevent illness altogether, while seeking convenient access to medical care. They expect internet-based health services that are as healthy, swift, and user-friendly as ride-hailing or food-delivery apps. Therefore, chronic disease management and general health management should extend beyond hospital walls into community and home settings, offering solutions tailored to primary care and households; shift focus from treatment to prevention, providing lifelong health services; and transition from prioritizing traffic volume and rapid monetization to genuinely addressing the health needs of patients with chronic conditions. Internet healthcare platforms should develop corresponding products and services with substantial technological sophistication.

Based on the development trajectory of Teladoc (Livongo), chronic disease management is projected to evolve through three stages. The first stage is toolification, which involves transforming chronic disease management guidelines into SaaS tools provided to specialist physicians and general practitioners to enhance service capabilities. The second stage is digitalization, where IoT devices are utilized to collect data for creating personal health records; in collaboration with medical experts, this facilitates the development of digital solutions for out-of-hospital interventions and lays the data foundation for artificial intelligence research. The third stage is intelligentization, characterized by the emergence of health management robots, digital therapeutics, and smart terminals equipped with human-computer interaction and virtual reality capabilities, thereby enabling personalized intervention plans based on patient data matching driven by artificial intelligence.

For internet healthcare platforms, achieving a leap across these three stages is tantamount to delving into the essence of healthcare by starting with chronic disease management—focusing on individual health needs and transforming low-frequency, sporadic, and passive medical visits into high-frequency, proactive health behaviors. By effectively serving users at this level, internet healthcare platforms are poised to usher in a golden age for the broader health industry.