Riding the 'Guochao' Wave: Domestic Players in Biopharma Upstream Tools Face Critical Challenges on the Path to Localization

BIOENFINE

Supplier of Animal Cell Suspension Culture Products and Services

In the pharmaceutical sector, China has gradually transitioned from the era of generic drugs two decades ago to the current era of innovative drugs.

Data shows that the global biologics market is projected to grow from $286 billion in 2019 to $768 billion by 2030, while China’s biologics market is expected to expand from RMB 312 billion in 2019 to RMB 1.303 trillion by 2030. As the “water sellers” in this trillion-dollar golden track, the biopharmaceutical support industry has also developed rapidly alongside the boom in biopharmaceuticals. In the past two years, spurred by the COVID-19 pandemic, the localization of upstream equipment and consumables has accelerated and gained significant attention.

However, for a long time, the vast majority of upstream biopharmaceutical support products—including culture media, chromatography resins, single-use consumables and their accessories, instruments and equipment, as well as filters and filter membranes—have been monopolized by imported products. VCBeat, as an observer of the healthcare industry, has also been closely monitoring developments in this field.This article examines the current landscape, merits, strategies for overcoming bottlenecks, and future prospects of raw materials, equipment, and consumables in China’s biopharmaceutical sector following several years of localization efforts, aiming to provide insights and perspectives for industry development.

According to Emergen Research, the market size of industries related to biopharmaceutical production was approximately USD 18.3 billion in 2020, primarily comprising equipment, raw materials, and consumables. Based on Frost & Sullivan’s estimates, China’s biopharmaceutical market accounted for approximately 20% of the global share in 2020. Accordingly, the market size of China’s biopharmaceutical production-related industries in 2020 is estimated to be approximately RMB 24 billion.

Furthermore, according to Frost & Sullivan’s estimates, the market size of China’s life science research reagent industry was approximately RMB 16 billion in 2020, while the market for IVD raw materials stood at around RMB 10 billion. Overall, the total market size of China’s life science support industry reached approximately RMB 50 billion in 2020 and is projected to grow to about RMB 80 billion by 2024.

Yet, the lion’s share of this lucrative market has long been captured by foreign giants. Industry leaders such as Merck, Sartorius, Thermo Fisher Scientific, Agilent Technologies, Cytiva, Tosoh, Bio-Rad, and Osaka Soda have established a near-monopoly over biopharmaceutical raw materials, instruments, equipment, and consumables.

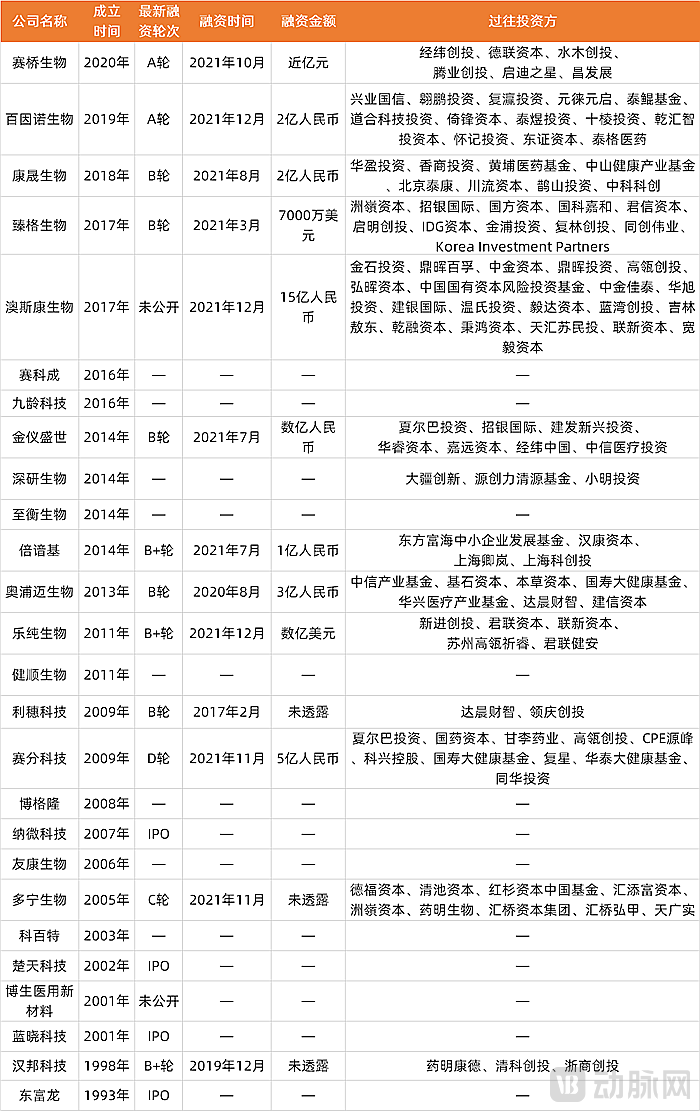

With the advent of an innovation boom in China’s life sciences sector, coupled with challenges posed by the COVID-19 pandemic—such as disruptions to overseas supply chains and concerns over product safety—the localization of biopharmaceutical support industries has become imperative. Dozens of emerging enterprises have subsequently emerged in China, including LePure Biotech, Lishui Technology, Cobetter, Shenyan Biotech, Baiyinuo, BIOENFINE, and Saiqiao Biotech.According to incomplete statistics, the domestic companies currently operating in areas related to biopharmaceutical consumables, raw materials, equipment, and instruments are as follows:

Compiled from public sources; listed in no particular order.

It is evident that the number of companies established before and after 2010, which serves as a dividing line, is roughly equal.

A number of biopharmaceutical equipment, consumables, and raw material companies established before 2010 have successfully completed their initial public offerings (IPOs).Through the gradual accumulation of production experience and client resources, these enterprises have established a solid foundation in technology, reputation, and market presence. Building on this base, breakthroughs in R&D technology and iterative improvements in products and services are key to their continued advancement.

Most enterprises established in 2010 and thereafter have been relatively active in financing., particularly in 2021, when multiple innovative companies completed new rounds of financing.Prominent investment firms such as Matrix Partners China, Qiming Venture Partners, IDG Capital, and Sequoia Capital, along with pharmaceutical companies like Tigermed and WuXi Biologics, have all become active in this sector.

The performance of listed companies offers a glimpse into the rapid development of the upstream biopharmaceutical industry over the past two years. Truking Technology achieved revenue of RMB 3.68 billion in the first three quarters of 2021, representing a year-on-year increase of 67.2%; East China Pharmaceutical Engineering and Technology Co., Ltd. (Tofflon) recorded revenue of RMB 2.88 billion during the same period, up 54.6% year on year. Other domestic pharmaceutical equipment manufacturers, such as Canaan Technology, Shinva Medical, and Chengyitong, have also benefited to varying degrees from the improved market sentiment.

It has been two to three years since the concept of localizing upstream raw materials, equipment, and consumables for the biopharmaceutical industry was first proposed. In addition to the impressive stock performance and reported revenue figures of listed companies, domestic startups have recently achieved frequent breakthroughs.

LePure Biotech, a leading domestic enterprise in biomedical consumables, recently achieved breakthrough milestones with the launch of its independently developed LePhinix™ single-use bioreactor and LeKrius™ biopharmaceutical process films. These innovations address two critical bottlenecks in China’s biomedical supply chain. Notably, LeKrius™ biopharmaceutical process films feature proprietary formulations and co-extrusion manufacturing processes, resolving supply constraints at the source. This marks a pioneering step toward the localization of single-use technologies across the entire production workflow for advanced therapies, including antibodies, vaccines, cell therapies, and RNA-based treatments.

Shenzhen Shenyan Biological Technology Co. LTD, a supplier of equipment and consumables in the cell and gene therapy (CGT) sector, has also achieved phased milestones in recent years. The number of CGT products approved globally remains limited, and the research and development of related equipment and consumables is still in its infancy worldwide. As one of the first companies in China to venture into the CGT consumables and equipment market, Shenzhen Shenyan Biological Technology has successfully launched the CellSep PRO, a fully closed automated cell processing system, and the EuLV, a lentiviral vector production system based on stable cell lines. These innovations have played a positive role in breaking the import monopoly on domestic CGT equipment, reducing high costs, and advancing viral vector production technologies.

Similar examples abound in today’s rapidly booming biopharmaceutical industry, yet there are also companies that have run aground in these “uncharted waters.” So, what did those startups that successfully achieved phased milestones do right?

First, the rise of the biopharmaceutical support industry is undoubtedly rooted in the emergence of the foundational biopharmaceutical industry.By examining and comparing the founding dates of companies in these two sectors, it becomes evident that those established before 2010 have remained resilient primarily because they had already achieved a certain scale in their respective domestic markets and continued to expand their business portfolios. In contrast, many companies that have attained phased achievements in innovative fields were mostly founded between 2010 and 2015, coinciding with the nascent stage of monoclonal antibody biologics in China. Following nearly a decade of rapid development, accumulation, industry coordination, and feedback in the biologics sector, its supporting industries have recently witnessed breakthroughs and substantial gains after this period of consolidation.

Furthermore, the entire biopharmaceutical sector, including its supporting industries, is characterized by high barriers to entry. Consequently, nearly all founders hold dual roles as both scientists and entrepreneurs. The technical expertise and experience of these scientists serve as a guarantee for the company’s research and development capabilities.

Third, the COVID-19 pandemic in recent years has also accelerated the localization of biopharmaceutical raw materials, equipment, and consumables.Due to the sudden onset of the COVID-19 pandemic, global biopharmaceutical supply chains have been strained and characterized by unstable supplies. Furthermore, safety concerns regarding many imported equipment and consumables during the pandemic warrant significant attention. In this context, the advantage of stable supply offered by domestic enterprises has rapidly come to the fore.Many enterprises have shifted from initially “having no choice but to use” domestic products to “actively adopting” them after trial, leading to a rapid increase in the brand influence and market share of domestically produced goods.

For any sector aiming to build itself up from scratch and achieve significant scale, various challenges are inevitable along the growth path, and the journey toward domestic substitution is no exception. Given the imperative nature of domestic substitution, what critical challenges do these startups face?

The fundamental challenge is the lack of relevant laws and regulations to standardize and regulate the industry.Although the upstream equipment, consumables, and raw materials sector for biopharmaceuticals serves as a supporting industry for biomedicine, its R&D standards and production quality control are not as detailed and stringent as those governing pharmaceutical products. High-quality startups often adopt the management systems of established industry leaders and refer to existing international regulations for their operations and control measures from inception.

Although the overall development of the biopharmaceutical industry shows a positive trend, occasional unscrupulous businesses lacking ethical conscience have tarnished the image of the nascent domestic industry. Clear laws and regulations can help identify and exclude such outlier enterprises, thereby raising the overall standard of the industry and fostering a healthy professional ethos. The establishment of relevant standards and legal frameworks not only provides companies with benchmarks and guidance during research and development and industrialization but also raises the entry barrier for the industry as a whole.

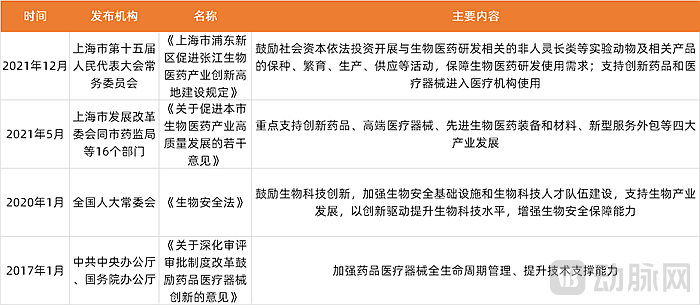

In response, relevant institutions have been sending positive signals in recent years, with various regulations being introduced successively. Going forward, the continuous introduction and updating of regulations related to biopharmaceutical equipment, consumables, and raw materials will require collaboration across the entire industry. Active cooperation and feedback between upstream and downstream sectors, along with frequent communication and collaboration among various institutions and enterprises, are essential to clarify these regulations through an iterative process of adjustment.

According to incomplete statistics, the relevant regulations issued in recent years

Other issues, such as technological barriers and brand influence, require companies to make long-term investments of time and effort based on a solid foundation and strict quality standards.

First, in terms of technical barriers,Take the raw materials used in cell culture media as an example. Standard culture media may involve 70 to 80 different raw materials, while high-end formulations can require over a hundred. “Beyond the high-barrier technologies related to manufacturing processes, even the seemingly simplest aspects—such as the proportion of trace elements and the sequence of ingredient addition—can affect batch-to-batch consistency and uniformity. Therefore, every detail warrants dedicated effort to master and accumulate experience.”BIOENFINE President Liu Xuping introduced.

Then there is the issue of how to break the brand influence of foreign giants.In this regard,Baiyinuo CEO Zhao Xiaojian told VCBeat New Medicine:“The so-called brand effect has a significant impact on the scientific research market. For the industrial sector, however, greater emphasis is placed on product quality and supply stability. International giants in the cell culture media industry, such as Thermo Fisher, Merck, and HyClone, have achieved mature scale and volume, established robust quality systems, and developed extensive formulation portfolios—all of which require considerable time to accumulate. There are no shortcuts for us either; we must prove ourselves through time and quality. Nevertheless, we can stand on the ‘shoulders of giants’ by synthesizing and summarizing years of prior experience. This approach enabled Bioinno to achieve rapid growth in its early stages.”

Since the research, development, and manufacturing of upstream equipment, consumables, and raw materials in the biopharmaceutical industry involve the interdisciplinary integration of bioengineering, chemical engineering, computer science, electronic engineering, and life sciences, sectors such as biopharmaceutical consumables and equipment have high entry barriers, requiring long-term efforts to achieve breakthrough innovations and build brand reputation. Due to a later start in China, there is indeed a certain gap in technological proficiency and patent holdings.

Although there is indeed a certain gap between domestic companies and industry giants, many niche segments across the upstream and downstream of the biopharmaceutical industry are still in their early stages of development. As supporting industries for biopharmaceuticals, sectors such as consumables and equipment require greater synergy between upstream and downstream players: suppliers should participate in and assist with process development in emerging fields, while customers should provide continuous feedback to help optimize product usage. Only through the concerted efforts of all stakeholders—including suppliers, end-users, and regulatory agencies—can the entire biopharmaceutical industry chain achieve increasingly robust growth.

“An egg, when broken from within, signifies life; when broken from without, it becomes food.” Stakeholders across the industry chain must work in concert to break monopolies from within and iterate upon previous technologies with more tangible advantages, thereby fostering a genuine trend toward domestication. Only by achieving full-industry-chain import substitution can we secure autonomy in key areas directly impacting patient benefits, such as cost and pricing.

However, the path to domestication does not equate to a domestic monopoly.Under the development trend of a global community with a shared future and the values of healthy industry competition, domestic substitution does not constitute moral coercion against Chinese biopharmaceutical companies. Robust in-house R&D capabilities and superior product quality are the cornerstones for Chinese enterprises to compete head-on with international giants.

On the other hand, many biopharmaceutical support industries embraced the development philosophy of “In China for Global” from their inception. Many startups often pursue global expansion by collaborating with pharmaceutical companies that have overseas operations, leveraging a “borrowing a ship to go to sea” strategy to establish a global presence and compete in the international market.

Thus, the tailwind driving the localization of upstream biopharmaceutical tools has blown from China to the international stage. We look forward to upstream biopharma tool providers offering higher-quality options for China’s biopharmaceutical industry, sparking a wave of “China Chic” across the country and around the globe.

Special Acknowledgments:

Shanghai LePure Biotechnology Co., Ltd. (hereinafter referred to as "LePure Biotech");

Shenzhen Shenyan Biological Technology Co. LTD (hereinafter referred to as "Shenyan Biotech");

Beijing Baiyinuo Biotechnology Co., Ltd. (hereinafter referred to as "Baiyinuo");

Shanghai Beitongji Biotechnology Co., Ltd. (hereinafter referred to as "Beitongji")...