Global Healthcare Investment Report 2021: Digital Health Booms Abroad, Domestic Substitution Trend Strengthens in Medical Devices

Devoted Health

Healthcare Service Provider

Core Viewpoints

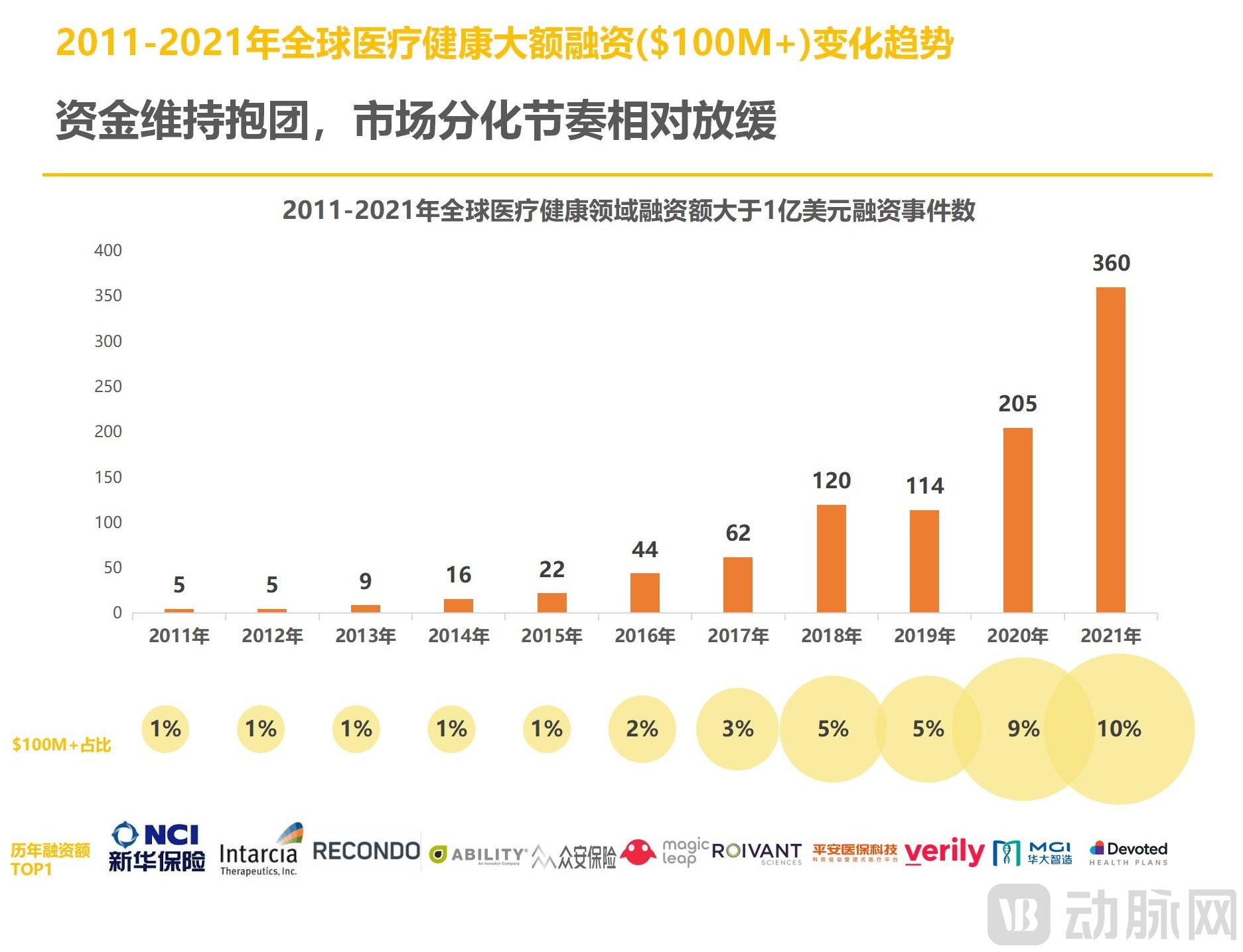

I. Buoyed by the 2020 IPO boom and large-scale M&A transactions, global healthcare financing in 2021 continued the previous year’s momentum: total funding reached a record high, marking the largest increase in nearly three years; there were 360 financing deals exceeding $100 million, accounting for as much as 10% of the total.

II. Strong Recovery Across Sub-sectors: Biopharmaceuticals Retains Top Spot; Digital Health Sees Surge in Major Funding Rounds, Leveraging Clear Advantages in Digitization Amid the Pandemic

3. The digital health sector abroad is experiencing robust growth. Driven by pandemic control measures and challenges associated with returning to work, companies in the mental health space continue to attract significant capital investment, while differentiated competition intensifies. In the medical device sector, the trend toward substitution with domestically produced products is pronounced, and centralized procurement of consumables has become fiercely competitive. Capital commitment to the medical robotics field remains strong, with surgical robotics companies securing multiple rounds of financing within a year. The approval of several first-in-class drugs has bolstered the valuation of biopharmaceutical companies, enabling this segment to lead in financing scale compared to other sub-sectors. The mRNA track remains hot and is likely to remain a key area of investor focus in 2022.

IV. Investment institutions worldwide remain highly enthusiastic about healthcare enterprises empowered by digital technology and innovative science; Sequoia Capital China has set a new global record, with cell therapy and small-molecule drugs attracting significant capital attention.

V. Asian and North American Capital Markets Show Comparable Performance, with Digitalization Becoming a Key Driver for the Development of Healthcare Industries Worldwide.

VI. The number and value of global IPOs hit new record highs, with the number of domestic listings increasing but the amount raised shrinking.

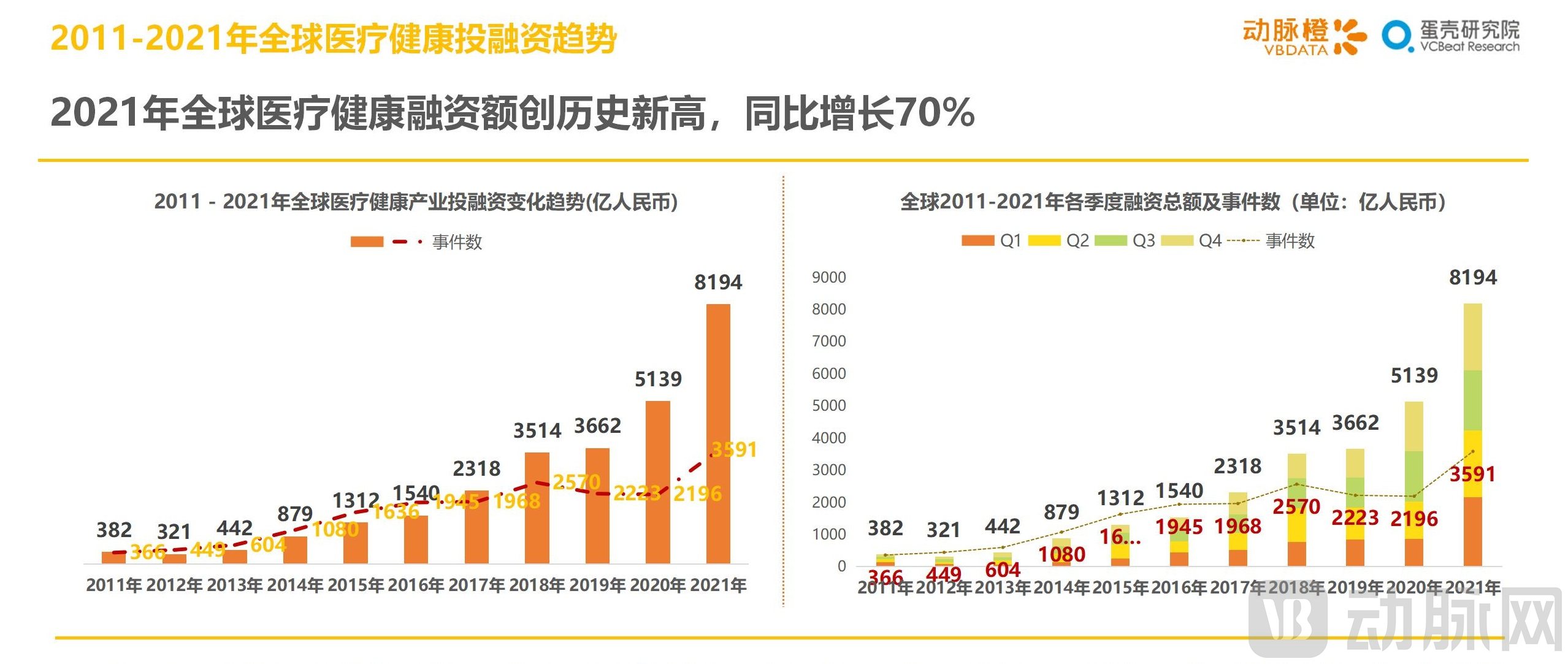

I. Global Healthcare Investment and Financing Trends from 2011 to 2021

In 2021, the global healthcare industry witnessed a total of 3,591 financing deals, with the total funding amount reaching a record high of $127.1 billion (approximately RMB 819.4 billion), representing a year-on-year increase of 70%. The number of financing deals also increased by 3,052, marking a year-on-year growth of approximately 63%. Meanwhile, Q1 2021 set a new quarterly financing record of approximately $33.7 billion (RMB 217.3 billion).

Considering multiple factors, we assess that the catalytic effect of the COVID-19 pandemic on the influx of capital into healthcare continues to be in force. Moreover, as epidemic prevention measures and the resumption of work and production have been progressively advanced, and as governments, industries, and the public have deepened their understanding of vaccines, online healthcare, and other fields since the outbreak began, investor enthusiasm for the healthcare industry remains undiminished. Furthermore, compared with the herd mentality in investment observed in 2020, capital has shown greater tolerance toward startups.

In 2021, the number of single financing rounds exceeding $100 million reached an unprecedented 360, a year-on-year increase of approximately 76%, surpassing the 2020 record of 205.

According to statistics, the total financing amount for these 360 companies exceeded $64.9 billion. This means that globally, approximately half of the funds invested in the healthcare industry are concentrated in less than 10% of enterprises. Among the top 10 companies by financing volume, four are digital health companies. The businesses of these four companies are primarily focused on internet insurance and chronic disease management.

It is worth noting that amid a sluggish global economy, the defensive nature of the healthcare sector has also driven capital to cluster in this area. However, the pace of market differentiation slowed down relatively in 2021, with a significant increase in the number of companies completing Series A and B financing rounds compared to 2020.

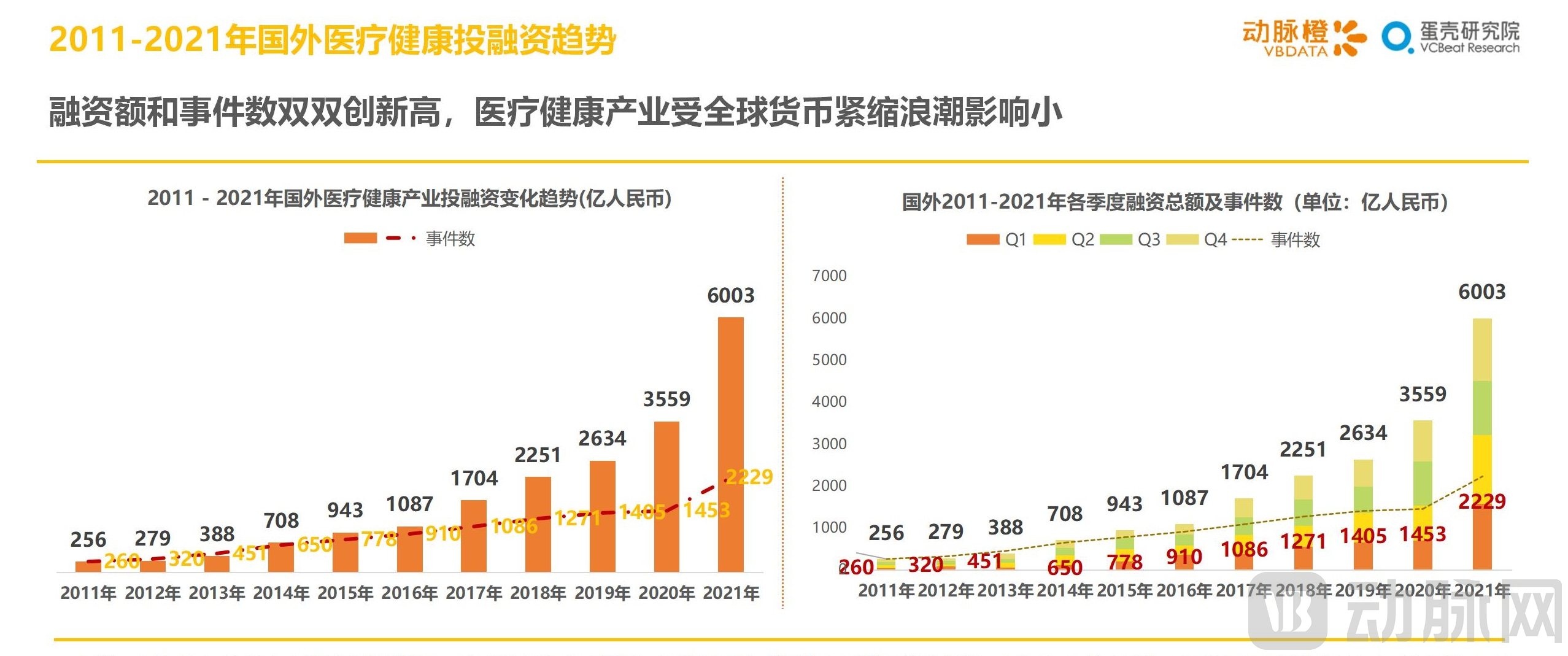

Abroad, the healthcare industry continued to thrive in 2021, marking its 11th consecutive year of steady growth. Although the growth rate in the number of financing deals slowed compared to 2020, 2021 saw higher growth rates in both the number of financing deals and the total financing amount.

In broad alignment with global financing trends, the COVID-19 pandemic has accelerated responses to many unmet medical needs. Sectors such as telemedicine, mental health, in vitro diagnostics (IVD), home care, and vaccines have continued to grow, building on the financing momentum gained in 2020.

Meanwhile, despite the global wave of monetary tightening, the healthcare industry has remained largely unaffected, with foreign venture capital investment in the sector continuing to increase.

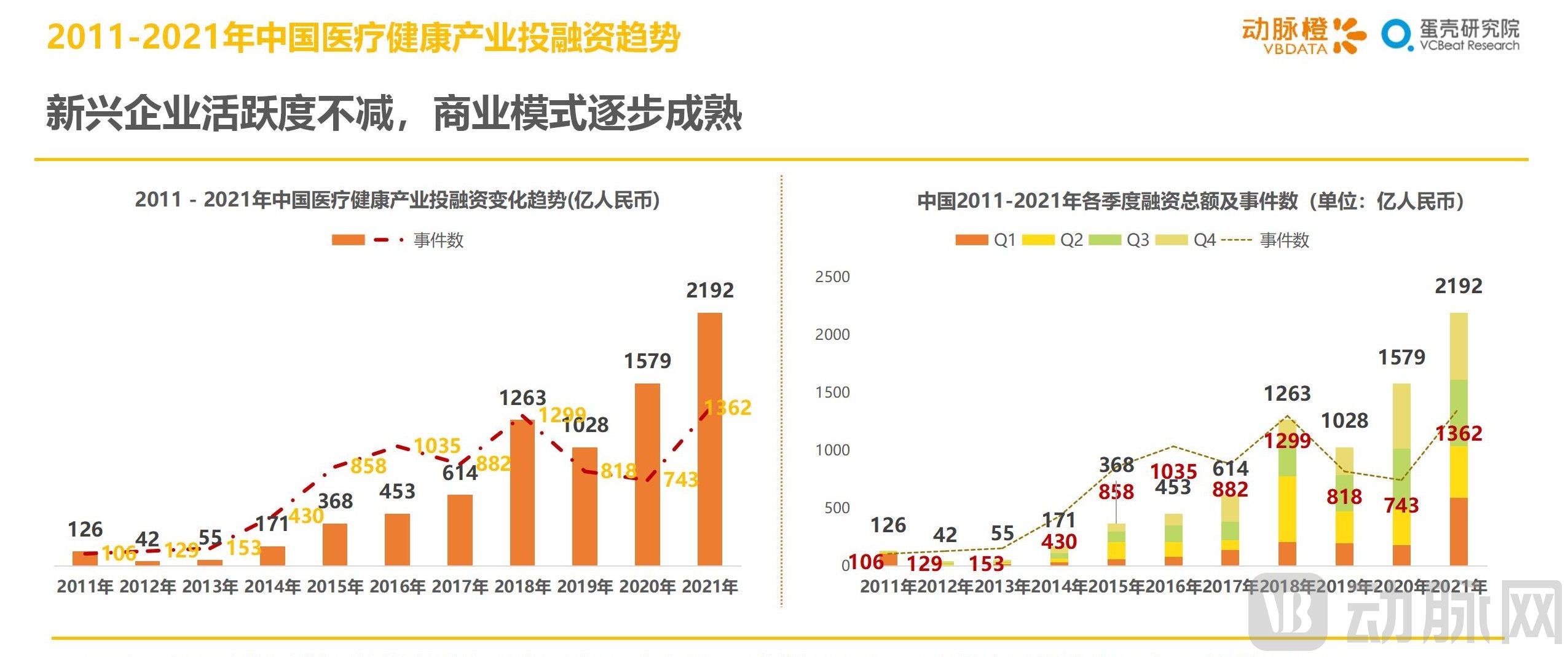

In 2021, the total investment and financing in China's healthcare industry reached a record high of RMB 219.2 billion, a year-on-year increase of 32.84%; meanwhile, the number of financing transactions reached 1,362, a year-on-year increase of 77.57%.

In the first half of 2021, China’s healthcare capital market continued the investment boom seen in the second half of 2020. Momentum further accelerated in the second half of the year, with a surge in large-scale financing rounds in the fourth quarter driving total funding for that quarter to nearly RMB 60 billion.

Notably, a cohort of Chinese startups with well-established business models and expanding operations delivered outstanding performance this year, including Anshi Biopharma, an innovator in anti-tumor drug development, and Yisi Biopharma, a developer of therapies for central nervous system disorders. More than half of these companies completed Series A and B financing rounds, raising a total of $15.1 billion (RMB 97.3 billion), which accounted for over 44% of the total annual healthcare financing in China.

II. Hot Sectors in Global Healthcare Investment and Financing in 2021

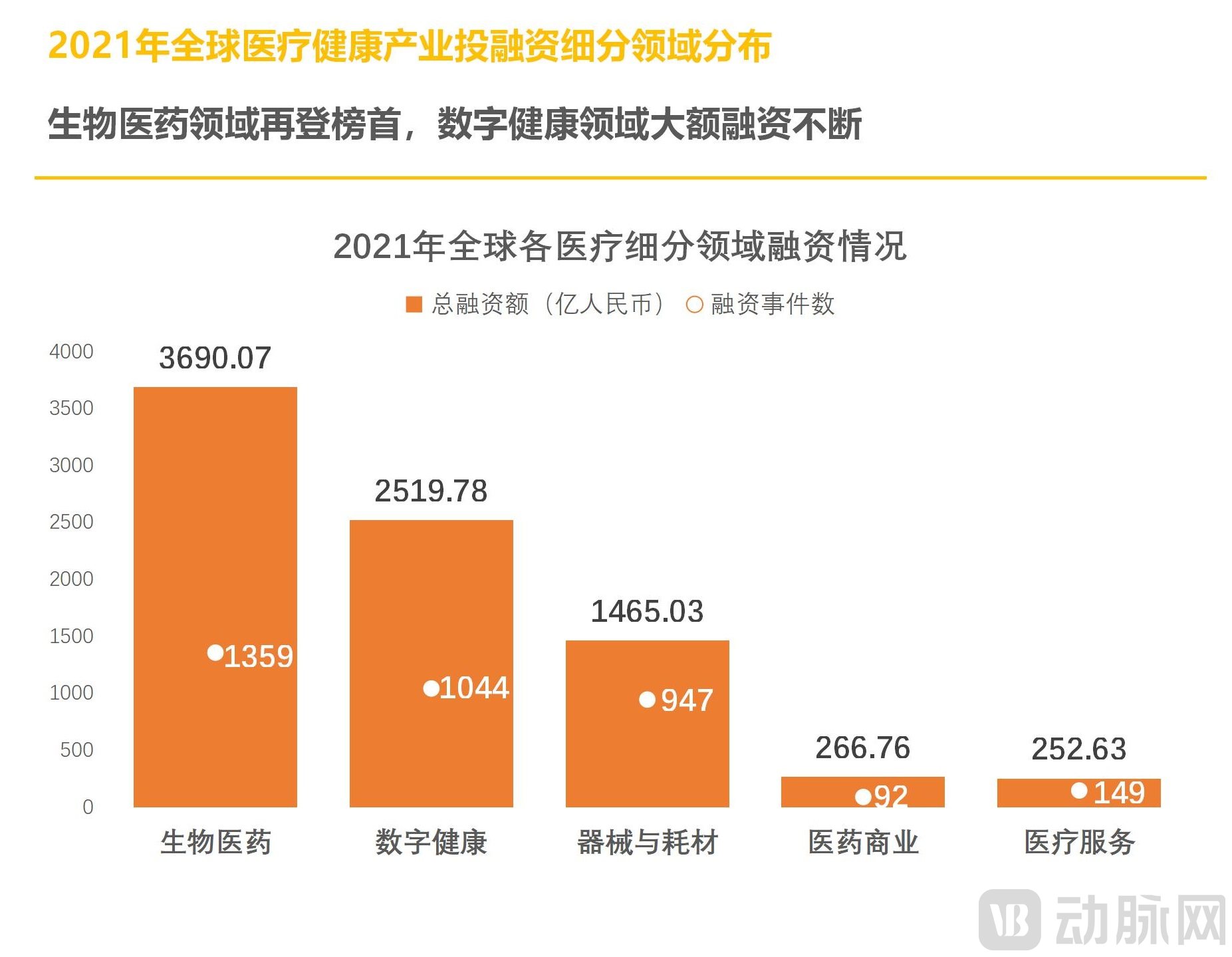

In 2021, the global biopharmaceutical sector led all other subsectors with 1,359 financing deals and a total funding amount of approximately RMB 369 billion, once again topping the financing rankings for the year. The digital health sector followed closely with nearly RMB 252 billion, while medical devices and consumables ranked third.

Among the 360 global financing rounds exceeding $100 million in 2021, nearly 78% occurred in the biopharmaceutical and digital health sectors, with these large-scale deals driving up the overall financing volume. In terms of specific distribution, biopharmaceuticals remained the sector most likely to secure substantial funding, similar to the previous year. The medical informatics and “Internet Plus Healthcare” sectors also demonstrated strong performance. Medical informatics ranked second with 52 deals, while “Internet Plus Healthcare” followed closely behind with 41 deals. Notably, against the backdrop of sustained enthusiasm for drug R&D and cost advantages, the contract research and manufacturing (CRMO) sector—capable of helping pharmaceutical companies reduce costs, improve R&D efficiency, and increase commercialization success rates—emerged as a dark horse in 2021, breaking into the top five sectors by number of large-scale financing events.

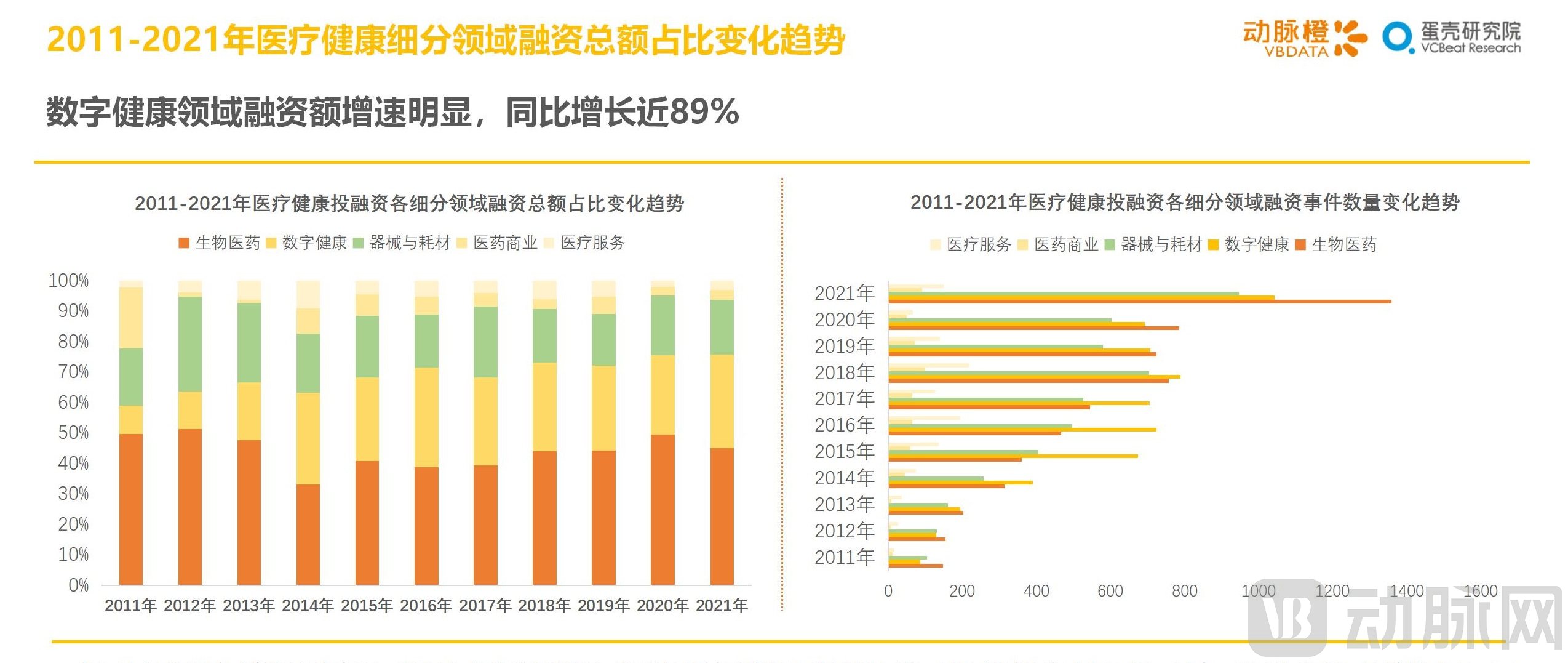

In terms of the proportion of financing amounts across five major sub-sectors, only digital health and medical services saw an increase in their share in 2021, while all other sectors experienced slight declines. Notably, driven by the COVID-19 pandemic over the past two years, industries such as telemedicine and internet-based healthcare have continued to expand their influence. In 2021, the total financing amount in the digital health sector increased by approximately RMB 118.5 billion compared to 2020, surpassing the full-year total of the previous year and representing a year-on-year growth of nearly 89%.

In terms of the number of financed projects across various sectors, the gap in financing volume among the three major sectors—biopharmaceuticals, digital health, and medical devices & consumables—was quite pronounced in 2021. Notably, while the number of new financing deals in digital health was nearly identical to that in medical devices & consumables in 2021, the total financing amount in digital health was almost double that of medical devices & consumables, indicating that the average financing size for digital health companies was significantly higher than that for companies in the medical devices & consumables sector.

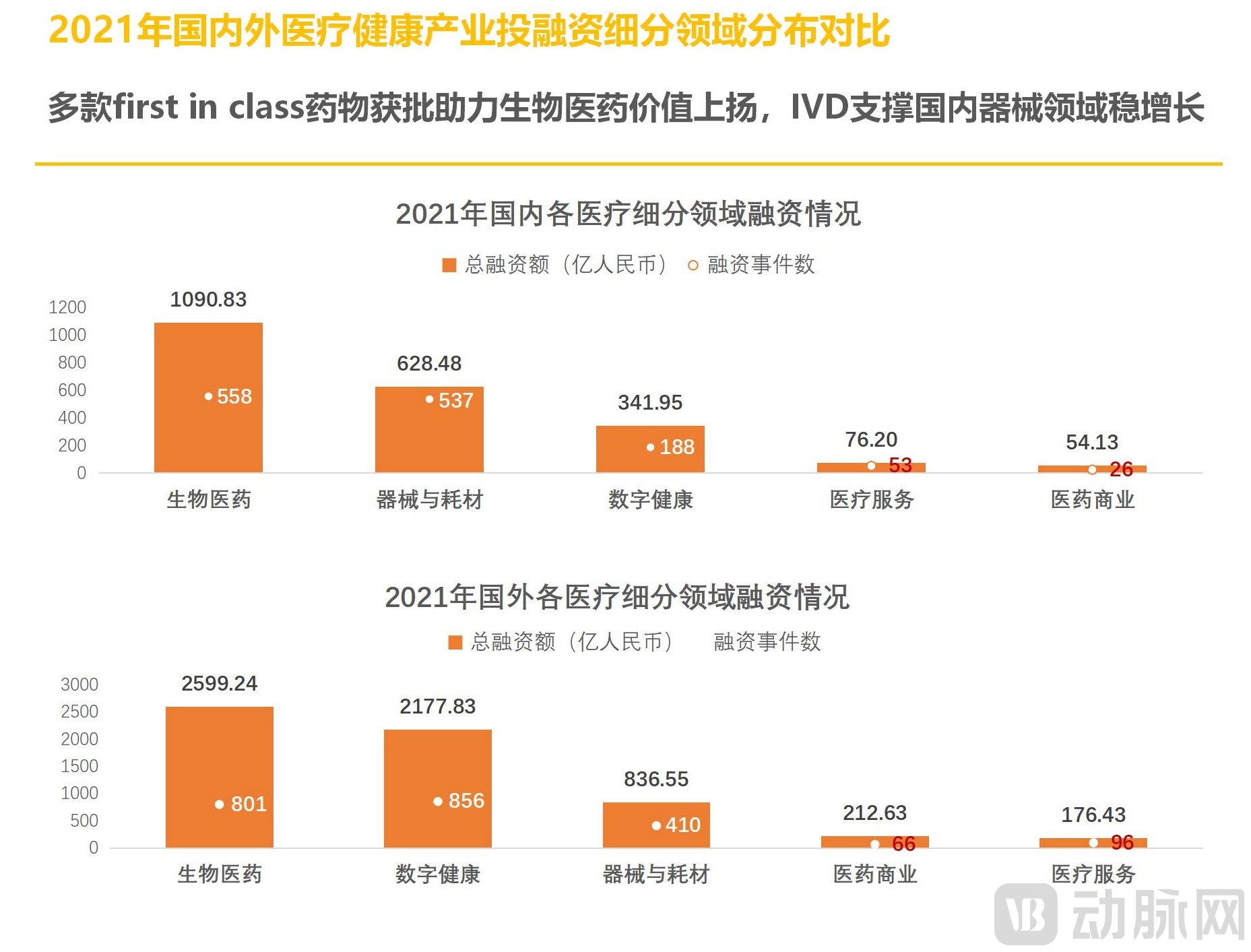

In 2021, the biopharmaceutical sector achieved impressive financing results in both domestic and international primary markets.

Driven by the combined effects of the pandemic and national policies supporting the biopharmaceutical sector, China continues to lead in both transaction volume and financing amount within the biopharmaceutical field. The global biopharmaceutical investment and financing market remains robust, with the sequential approval of multiple first-in-class drugs, nucleic acid therapeutics, antibody-drug conjugates (ADCs), and other innovative biotechnologies driving up valuations in the sector. Although the number of financing deals is slightly lower than that in the digital health sector, the total financing amount has surpassed it.

Meanwhile, the medical device and consumables sector, which has shown mediocre performance abroad, is more favored by capital in China, accounting for 46% of the total annual financing. Among these, POCT (Point-of-Care Testing) products in the IVD field—characterized by convenience, miniaturization, and suitability for various rapid diagnostics—played a significant role in epidemic prevention and control. Ustar Biotechnologies, which possesses multiple independent intellectual property rights and a rapid molecular detection technology platform, and Renmai Biology, which focuses on innovative platforms for quantitative immunoassay and the R&D of specialized reagent projects, both secured two rounds of financing in 2021.

In 2021, biopharmaceuticals, healthcare informatization, Internet Plus Healthcare, and the in vitro diagnostics (IVD) sector experienced high levels of interest.

In terms of funding round distribution, Series A financing deals occurred most frequently, with a cumulative total of 1,063 transactions. The number of Seed/Angel and Series B financing events both exceeded that of Series C, indicating that capital is more focused on early-stage startups with high growth potential, unwilling to miss any company that could become a unicorn. This trend is particularly evident in the biopharmaceutical sector.

III. Observations on Key Sectors in Global Healthcare Investment and Financing in 2021

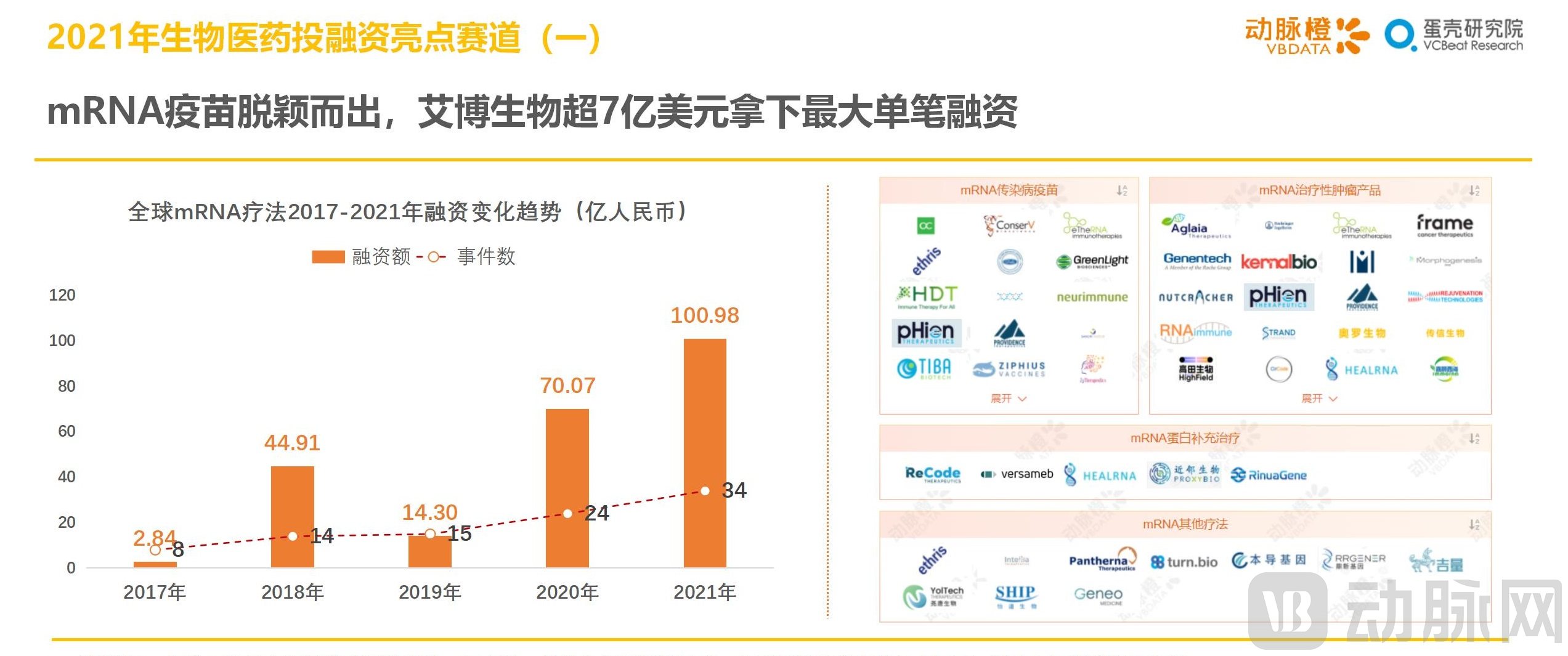

In 2021, investment and financing activity in the global mRNA market continued to heat up, with a total of 34 financing deals and cumulative funding of approximately RMB 10.1 billion, representing a year-on-year increase of nearly 44%.

The outbreak of the novel coronavirus in 2020 highlighted the urgent global demand for preventive vaccines. Leveraging advantages such as shorter development cycles and higher safety profiles, mRNA vaccines emerged as frontrunners among numerous COVID-19 vaccine candidates, becoming a highly sought-after sector for capital investment. Against the backdrop of the normalization of the pandemic and the sequential approval of booster doses, mRNA vaccines remained one of the hottest topics in the global biopharmaceutical industry in 2021. Furthermore, considering the diverse application scenarios of mRNA vaccine products and the emergence of numerous new enterprises, the momentum in the mRNA sector is expected to sustain through 2022.

Riding the wave of mRNA vaccine enthusiasm, star company Moderna saw its market capitalization surge in the past two years, briefly surpassing the $100 billion mark. Meanwhile, Abon Biopharm, which secured China’s first clinical trial approval for an mRNA vaccine, refreshed the financing record in China’s biopharmaceutical sector in 2021 by raising over $700 million in Series C funding—the largest single financing round in the mRNA field in the past five years.

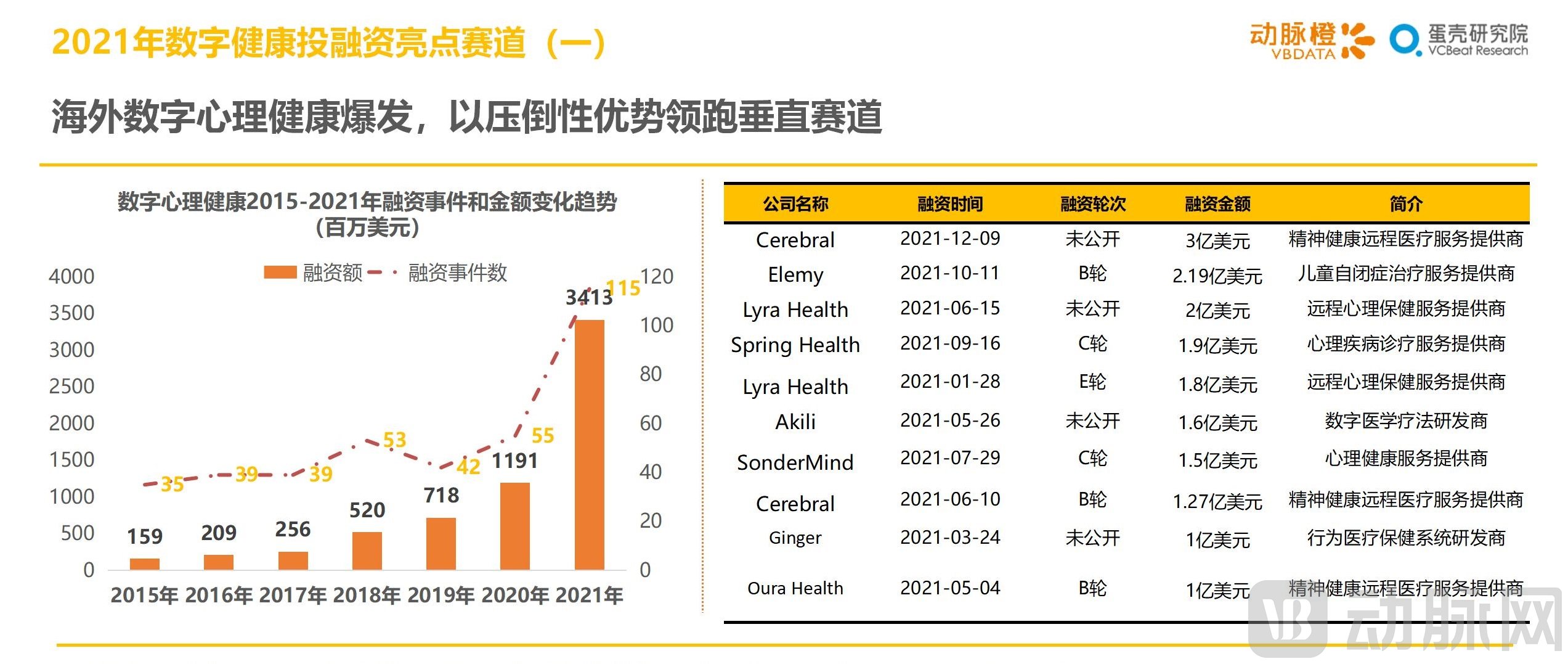

In 2021, global investment and financing activity in the digital mental health sector surged, with 115 funding deals completed throughout the year and total financing exceeding USD 3.4 billion (approximately RMB 21.9 billion).

Since 2015, the global digital mental health sector has maintained a growth trajectory. Particularly during the nearly two years following the outbreak of the COVID-19 pandemic, demand for mental health services surged amid instability driven by changes in work patterns and healthcare processes. This trend, coupled with accelerated development of digital healthcare infrastructure—exemplified by the United States—has, to some extent, stimulated the growth of the digital mental health market.

Moreover, within the overseas digital health sector segmented by indication, digital health startups focused on mental health services have maintained their leading position since 2018, further widening the gap with other clinical indications by at least $2 billion.

By the end of 2020, the platform war in digital health had intensified, with major healthcare and life sciences companies experiencing firsthand the challenges of integrating disparate data silos during collaborations or acquisitions. In 2021, as regulators pushed for greater patient transparency, health systems and payers were compelled to make their data more user-friendly, which further fueled the growth of the medical big data capital market in 2021.

In 2021, nearly 50 transactions related to big data in healthcare secured over $3.6 billion in financing, more than triple the amount raised in 2020.

These companies share common traits: their businesses help lower the entry barriers for new digital health startups, enabling entrepreneurs to focus on non-technical differentiators—paving the way for future patient-centric approaches in digital health; secondly, they reduce the friction and costs associated with integration and mergers and acquisitions (M&A) in the digital health sector, accelerating platform competition and industry consolidation; thirdly, they contribute to a unified industry data ecosystem, opening up new possibilities for population health.

According to the prospectus data from VentureMed, there were 36.3 million patients with heart valve disease in China in 2019, and this number is projected to rise to 40.2 million by 2025. It is undeniable that the heart valve market holds immense potential.

In 2021, the cardiac valve sector saw a total of 16 financing events, with amounts exceeding $400 million.

From a product perspective, companies developing mitral valve products are more likely to secure financing. According to an analysis by VCBeat, the mitral valve sector is so hot for three main reasons. First, there is strong unmet medical need: the one-year mortality rate for severe mitral regurgitation is as high as 57%. Second, approximately 7 million patients in China require mitral valve surgery, yet only 40,000 surgical procedures are performed annually nationwide, resulting in a severe supply shortage and urgent demand, which underscores the huge potential of the mitral valve market. Third, transcatheter mitral valve intervention involves extremely high technical difficulty and significant challenges; to date, the FDA has approved only one repair product, MitraClip, and no replacement products (while the CE mark has been granted to only one replacement product, Tendyne). These three characteristics have made mitral valve companies highly sought-after investment targets for capital markets.

In 2021, the global medical robotics sector witnessed a total of 72 financing rounds, with the total funding amount exceeding US$3.4 billion. This included 10 deals valued at over US$100 million each.

In terms of funding rounds, the financing completed in the medical robotics sector in 2021 was primarily concentrated in Series A rounds, with a majority involving surgical robotics companies.

Surgical robots represent the most technologically challenging segment within the broader robotics field and have attracted significant capital attention, with six surgical robot companies receiving multiple rounds of investment within a single year. Notably, Lancet Robot’s hip replacement, knee replacement, and dental implant surgical robots have all entered the clinical registration phase in China and demonstrated excellent clinical performance. ShuRui Robot has filed more than 340 patent applications worldwide, securing 16 authorized patents in countries including the United States and 120 authorized patents in China.

Three medical robotics companies saw their valuations rise after securing financing in 2021, making their debut on the 2021 Hurun Global Unicorn Index.

IV. Analysis of Active Healthcare Investment Firms in 2021

In 2021, Sequoia Capital China was the most active investor in the global healthcare sector, making a record-breaking total of 92 investments throughout the year, with its portfolio primarily focused on biopharmaceutical companies.

From the perspective of IPO exits, Sequoia China surpassed its 2020 record of 10 healthcare IPOs in 2021. The successful IPO of Dizal Pharmaceutical on the STAR Market in December 2021 also marked Sequoia China’s 12th healthcare IPO project in 2021 across multiple capital markets, including the A-share, Hong Kong, and U.S. stock exchanges.

Alexandria Venture Investments and Yuansheng Capital, both new entrants to the list, ramped up their investment activities in 2021. Unlike other investment firms that adopt a multi-sector diversification strategy, Alexandria Venture Investments focused exclusively on the biopharmaceutical sector in 2021, with particular emphasis on gene therapy and immuno-oncology.

Among the top ten healthcare investment institutions by number of investments in 2021, ten companies received support from four or more of these institutions. Notably, New Vision Medical, which is engaged in the research, development, and production of original endoscopy-related products, garnered joint favor from six active investors.

Overall, in 2021, financing rounds backed by multiple active investors were predominantly concentrated at Series B, with cell therapy companies and small-molecule oncology drug developers in the biopharmaceutical sector demonstrating particularly strong performance.

V. Review of Healthcare IPOs Listed in 2021

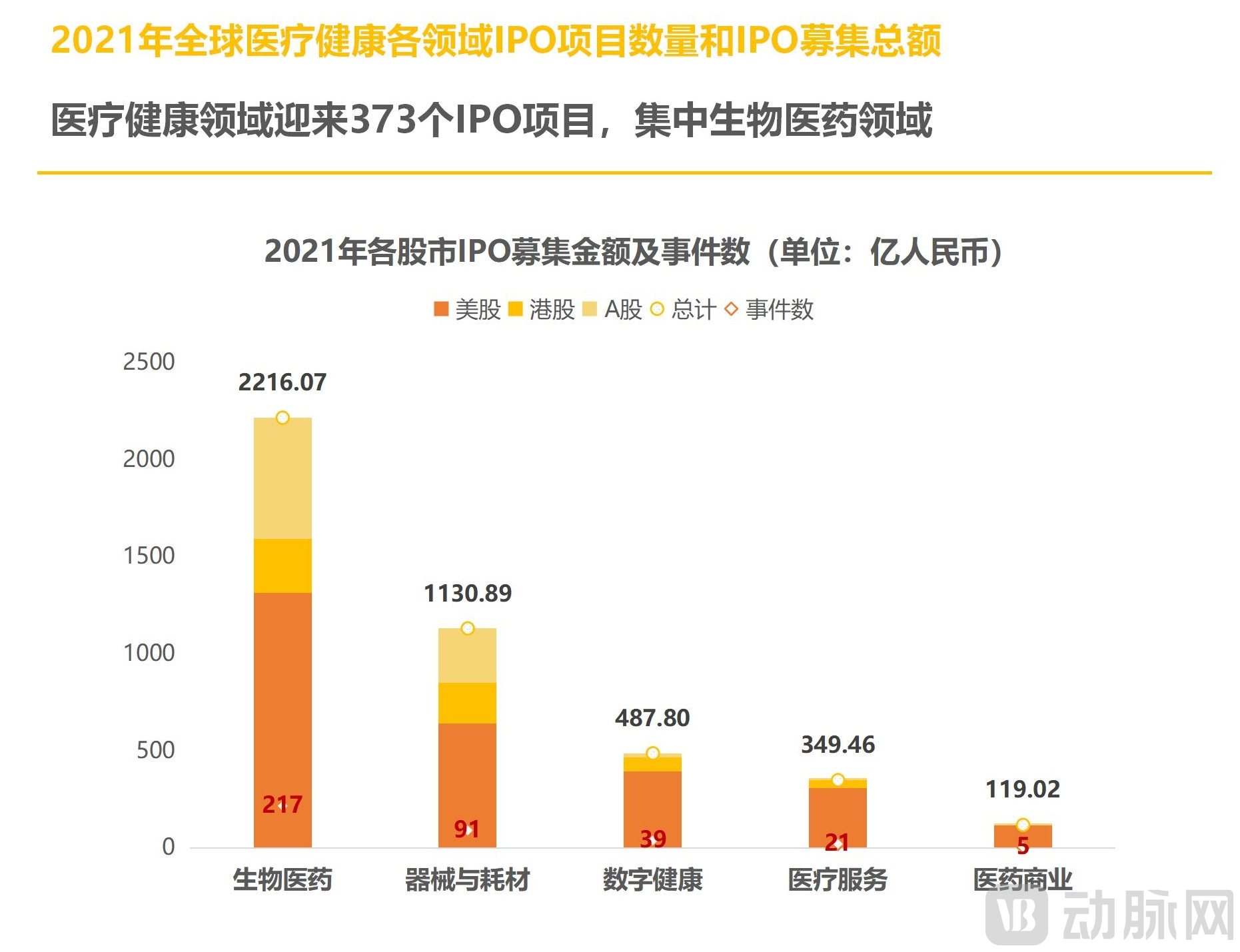

According to the VCBeat database, a total of 373 companies were listed on the A-share, U.S., and Hong Kong stock markets in 2021, raising a total of RMB 430.3 billion, a year-on-year increase of 31%, with both the number of listings and the amount raised reaching new historical highs.

Companies listed in the United States accounted for 70% of the total, with 272 firms raising a combined RMB 277 billion, a 62% year-on-year increase, surpassing the combined totals of the other two stock exchanges.

In 2021, a total of 217 companies in the biopharmaceutical sector went public, doubling the number of listings compared to 2020, while the amount of capital raised increased by 12% month-on-month.

Even amid the recurring domestic outbreaks, the healthcare capital market still witnessed record-breaking numbers of IPOs and fundraising amounts. In 2021, 111 Chinese companies went public, raising a total of RMB 162 billion, representing an increase of 35 IPOs compared to the previous year. Among the listed healthcare companies, the A-share market performed prominently, with 64 companies going public and raising RMB 93.3 billion in initial offerings. The Hong Kong stock market and the U.S. stock market saw 36 and 11 listings, respectively.

In 2021, the number of initial public offerings (IPOs) in China increased, but the total amount raised declined quarter-on-quarter, with Hong Kong-listed stocks experiencing a 40% quarter-on-quarter drop. For Chinese companies listing on the secondary market in 2021, it became common for new shares to break their issue price, with continuous declines primarily affecting unprofitable innovative drug and high-value consumables companies. Despite these challenges, there were still highlights in the secondary market. Upstream companies in the biotechnology industry chain performed exceptionally well. For example, NanoMicro Technology, the first company specializing in nanospheres in China, saw its stock rise more than tenfold on the first day of trading; Sino Biological, which focuses on providing a wide range of recombinant proteins, closed up by 81.27%.

VI. Global Distribution of Hotspots in Healthcare Investment and Financing in 2021

In 2021, the five countries with the highest number of global healthcare financing events were the United States, China, the United Kingdom, India, and Canada.

The United States led globally with 1,570 financing deals totaling $70.956 billion (RMB 451.59 billion), followed closely by China; together, the two countries accounted for over 80% of the total financing amount and number of deals worldwide.

Asia and North America performed on par in 2021. The proliferation of smartphones and the internet in India has spurred a surge of innovation in “Internet + Healthcare.”

In North America, aside from the United States, Canada also delivered impressive performance in 2021, with its number of financing events closely trailing that of India. Similar to India, digitalization has been a significant driver for Canada’s healthcare sector, with health information technology emerging as the fastest-growing subsector.

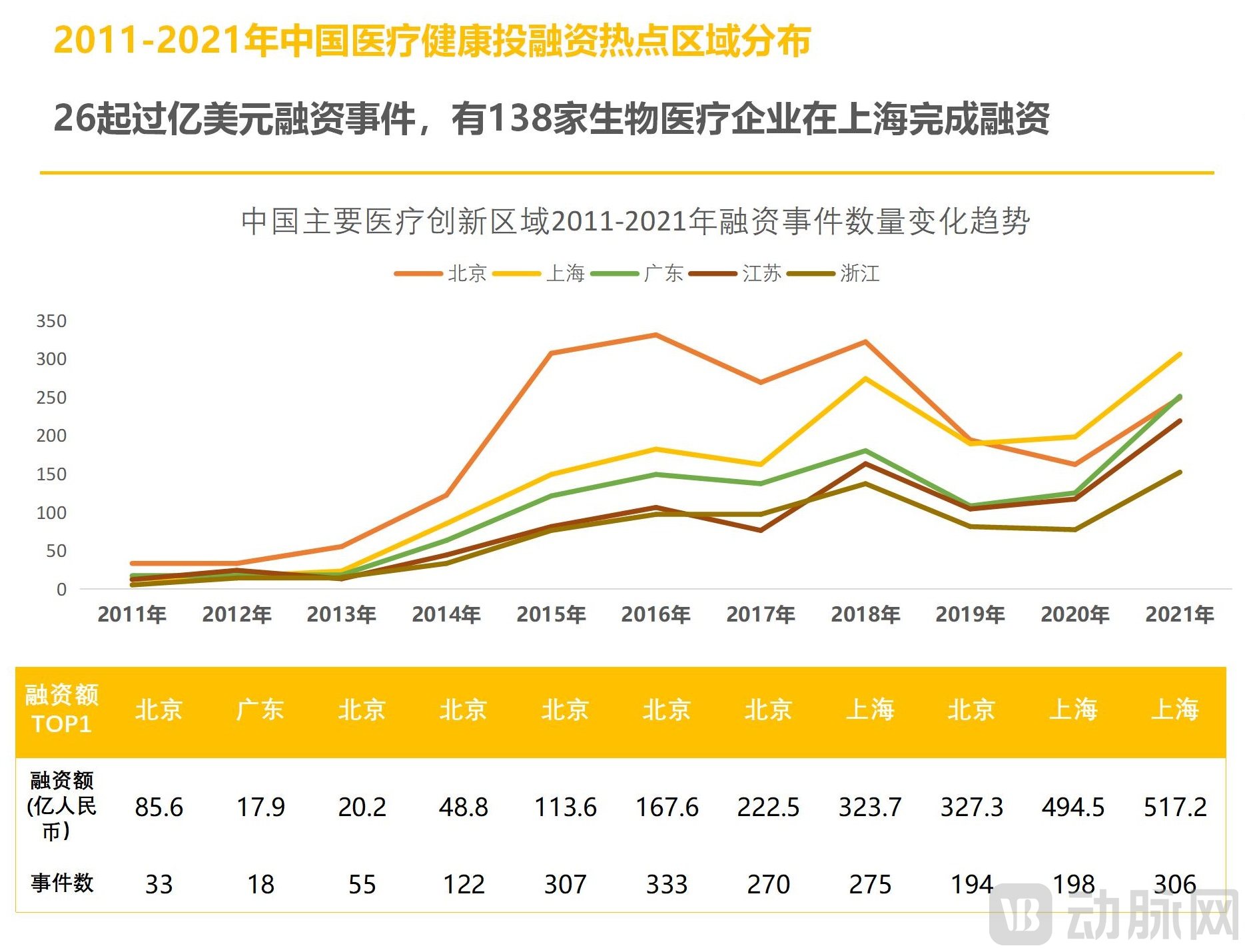

In 2021, the five regions in China with the highest concentration of healthcare and medical investment and financing activities were, in order, Shanghai, Guangdong, Beijing, Jiangsu, and Zhejiang.

Shanghai recorded a cumulative total of 306 financing events, an increase of 108 from the previous year, raising over RMB 51.7 billion and surpassing second-ranked Beijing by nearly RMB 6.6 billion.

Overall, the spatial distribution of healthcare financing transactions in 2021 remained largely unchanged, continuing to concentrate in Beijing, Shanghai, and Guangzhou—regions characterized by a solid foundation in the healthcare industry and a high aggregation of innovation resources. These areas accounted for 59% of all financing deals nationwide. Meanwhile, Jiangsu and Zhejiang provinces followed closely with 371 financing transactions, reflecting their rising investment热度.

Geographic Distribution Trends in Healthcare Investment and Financing Over the Past Decade: Beijing Has Long Maintained Its Dominant Position as China’s Primary Hub for Medical and Health Innovation

Specifically, Shanghai recorded 306 financing deals in 2021, with a total amount reaching RMB 51.7 billion, nearly RMB 6.6 billion more than Beijing. Among these, there were 26 deals exceeding USD 100 million, and 138 biomedical companies completed financing in Shanghai.

VII. Top Financing Records of Healthcare Companies in 2021

VIII. Appendix

Scan the mini-program QR code to download the full report