IVD Raw Materials Sector Attracts Over ¥3.4 Billion in Funding, Evolving from Niche Market to a Hundred-Billion-Yuan Industry

In 2021, light and darkness intertwined in the IVD sector, driving the upstream raw materials industry to advance rapidly amidst turbulence.

The persistent outbreak has further highlighted the vulnerability of China’s IVD industry, which relies heavily on imported upstream raw materials. Centralized procurement has accelerated the substitution of domestic alternatives for these upstream inputs, leading to a sudden boom in the IVD raw material sector. A surge of IVD raw material companies has emerged to capitalize on this trend, triggering significant volatility and activity in the capital markets.

According to the VCBeat database,In 2021, a total of 12 companies in the IVD raw materials sector completed 15 financing rounds, with the total amount exceeding RMB 3.4 billion, among which 10 rounds exceeded RMB 100 million.

2021 IVD Raw Material Company Financing Events

Dr. Ren Hui, founder of Haili Biotech, stated, “Previously, the focus was predominantly on the clinical market, with little willingness to invest in the upstream raw materials sector. Impact by the pandemic, the raw materials industry has been rapidly thrust into the spotlight, leading to a sharp increase in capital investment interest. Raw material companies have successfully completed initial public offerings (IPOs), and financing and merger-and-acquisition activities have become frequent. Haili Biotech has also successfully completed its Series B financing round, raising tens of millions of yuan.”

The industry’s boom, fueled by capital influx, is driving the rapid expansion of China’s IVD raw materials market. The golden age has arrived; what turning points is the IVD raw materials sector facing? What development trends will emerge in the future? In this article, VCBeat examines a series of events and changes in the IVD raw materials field in 2021, seeking to explore the future landscape of the sector.

I. The Spring of Domestic IVD Raw Materials Has Arrived

From scarce capital interest to high demand, from a niche market to a scale of tens of billions, the IVD raw materials sector has taken more than a decade.

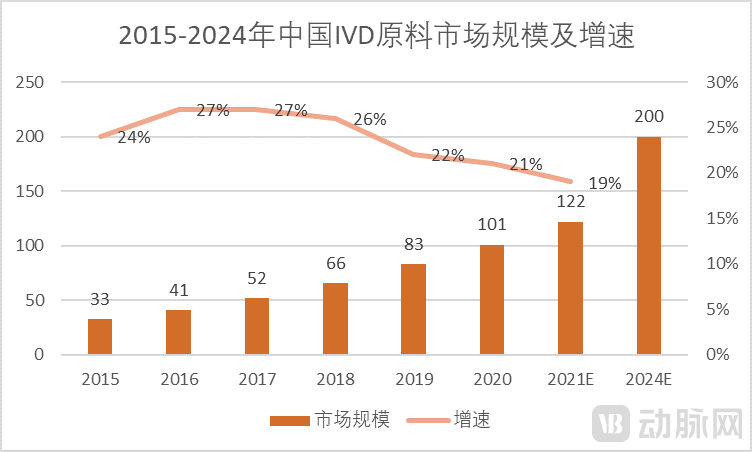

With the rapid development of China's in vitro diagnostics industry,The market demand for in vitro diagnostic (IVD) raw materials, as the upstream segment of the industry chain, has correspondingly expanded rapidly.The market size grew from RMB 3.3 billion in 2015 to RMB 8.2 billion in 2019,The compound annual growth rate (CAGR) from 2015 to 2019 was 25.8%;The market size is expected to reach RMB 20 billion in 2024., the compound annual growth rate from 2019 to 2024 will reach 19.4%.

Market Status of China's IVD Reagent Raw Materials Industry Data Source: Huajing Industry Research Institute

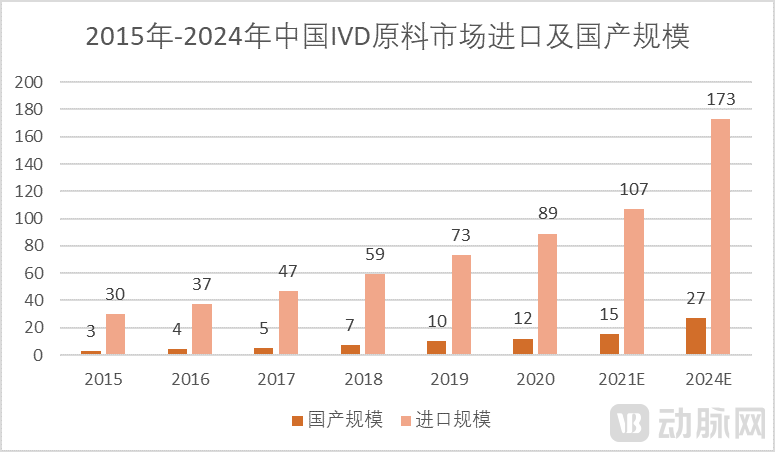

From the perspective of market landscape, imported products still dominate the IVD raw material market, while domestically produced alternatives are developing rapidly with significant potential for import substitution.

In 2019, the market size of imported products reached RMB 7.3 billion, accounting for 88% of the IVD raw material market; the market size of domestically produced products was RMB 1 billion, with a relatively small market share, but it demonstrated rapid growth, achieving a compound annual growth rate (CAGR) of 30.6% from 2015 to 2019, which was higher than that of imported products.

As domestic enterprises continuously enhance their technical capabilities and place greater emphasis on the localization of the biotechnology industry supply chain, the market size for domestically produced in vitro diagnostics (IVD) raw materials is projected to reach RMB 2.7 billion by 2024, with a compound annual growth rate (CAGR) of 23.3%, thereby gradually achieving import substitution.

Market Size of Imported and Domestically Produced Raw Materials for IVD Reagents in ChinaData Source: Huajing Industry Research Institute

Raw materials for in vitro diagnostic (IVD) reagents are substances used to manufacture IVD reagent products, primarily including antigens and antibodies, enzymes and coenzymes, probes, primers, microspheres, and others. Among these, antigens/antibodies and enzymes/coenzymes serve as the key active components in the reagents, determining the core performance of the products.

The production of raw materials for in vitro diagnostics (IVD) has long been a critical bottleneck in China’s IVD industry, as the quality of these materials significantly impacts the performance and accuracy of diagnostic reagents.To ensure consistent quality, although there are domestic manufacturers of IVD raw materials, approximately 90% of the market is still dominated by imported raw materials.

Although the upstream segment accounts for only 10% of the total output value in the IVD industry, it boasts gross profit margins exceeding 90%, making it a core profit center within the industrial chain. With substantial bargaining power, midstream players have no leverage in negotiations with upstream suppliers. Consequently, any supply disruptions or price hikes by imported brands would significantly impact domestic enterprises.

In recent years, the international landscape has shifted, and the outbreak of the COVID-19 pandemic has further exacerbated global supply chain tensions. Shortages, supply disruptions, and price hikes of core in vitro diagnostics (IVD) raw materials have exposed China’s long-standing vulnerability due to its heavy reliance on imported inputs. Domestic manufacturers are increasingly recognizing the importance of mastering core segments of the industry chain and are gradually cultivating Chinese suppliers to build a more resilient and secure supply chain.

Furthermore, the COVID-19 pandemic has generated massive testing demand, expanded the market for IVD products, and consequently driven growth in China’s domestic IVD raw materials market.

Major domestic IVD raw material manufacturers have experienced rapid performance growth over the past two years.For example, Fapon Biotech is one of the leading suppliers of raw materials for COVID-19 nucleic acid testing reagents and COVID-19 antigen immunoassay reagents. Benefiting from the COVID-19 pandemic, the company has experienced explosive growth in performance in recent years. From 2018 to 2020 and in the first half of 2021, Fapon Biotech’s operating revenues were RMB 221 million, RMB 289 million, RMB 1.067 billion, and RMB 1.13 billion, respectively, with a compound annual growth rate (CAGR) of 119.63% over the past three years.

Vazyme is one of the few R&D-driven innovative enterprises in China that possesses both independent and controllable upstream technology development capabilities and end-product manufacturing capabilities. In 2020, its operating revenue reached RMB 1.564 billion. From January to September 2021, the company reported operating revenue of RMB 1.289 billion, a year-on-year increase of 13.21%, with net profit attributable to shareholders of the parent company amounting to RMB 550 million.

In 2021, as vaccination became widespread, epidemic control in China entered a normalized phase. Coupled with the impact of centralized procurement on the IVD market, the capital market was also undergoing changes.

An investor specializing in the IVD sector noted that in early 2020, many individuals had an unclear assessment of the pandemic’s trajectory, leading numerous institutions to hesitate over whether to invest in IVD companies benefiting from the outbreak. As pandemic management became normalized, and influenced by international relations and centralized procurement policies, the underlying logic of the entire industry has shifted. “Previously, most market institutions paid relatively little attention to the upstream segment of the industry chain; now, they are increasingly increasing their investments in upstream enterprises.”

In 2021, upstream IVD raw material manufacturers became the darlings of capital, and Chinese IVD raw material companies began to accelerate their rise.

Since June, Nanomicro Technology, Abexa Biologics, and Vazyme have successively listed on the STAR Market. Starting in August, Sino Biological, Proteintech, and Univer Biotech have successively listed on the ChiNext Board, while Fapon Biotech launched its IPO on the ChiNext Board, raising RMB 2.5 billion. This year, Nearshore Protein is poised for an IPO on the STAR Market, aiming to raise RMB 1.5 billion. In the primary market, several IVD raw material companies have secured substantial financing; for instance, Hanhai New Enzyme raised RMB 800 million, and Abbkine raised RMB 1.2 billion.

IVD Raw Material Companies Listed in 2021

In recent years, China’s in vitro diagnostics (IVD) industry has experienced rapid growth, with the domestic market size approaching the RMB 100 billion mark. According to data from Fapon Biotech’s prospectus, the market size of China’s IVD industry grew from RMB 42.75 billion in 2015 to RMB 80.57 billion in 2019, representing a compound annual growth rate (CAGR) of 17.2% during this period. It is projected that by 2030, the market size will reach RMB 288.15 billion, with China’s share of the global market rising to 33.2%, making it the largest consumer of IVD products worldwide.

The market demand for IVD raw materials has consequently surged. However, the accumulation of core underlying technologies has not advanced at a comparable pace. Due to the high R&D complexity, intricate production technical routes, and sophisticated process flows associated with IVD raw materials, domestically produced in vitro diagnostic reagents still lag behind imported counterparts in terms of quality control, manufacturing processes, and purity.

Currently, approximately 90% of the market in China is dominated by companies such as Roche, HyTest, and Meridian. This has placed Chinese IVD manufacturers in an extremely weak position during price negotiations, resulting in a pronounced dependence on foreign suppliers.

The severe overseas epidemic situation has led to prolonged import cycles for raw materials among midstream reagent manufacturers, highlighting the necessity of domestic backup supplies.Companies represented by Mindray are moving upstream to directly address supply issues at the source.

In May 2021, Mindray Medical made a significant acquisition of Hytest, a globally renowned supplier of IVD raw materials, for €545 million (approximately RMB 4 billion), marking its substantial entry into the upstream IVD raw materials sector. Hytest is one of the four core global suppliers of raw materials in the IVD industry.

It is reported that in 2020, Mindray Medical’s in vitro diagnostics (IVD) business generated RMB 6.64 billion in revenue. Chemiluminescence immunoassay represents a key segment of Mindray’s IVD portfolio. Through this acquisition, Mindray has strengthened its core R&D capabilities for chemiluminescence products and raw materials, while optimizing the global layout of its upstream and downstream industrial chain.

"Stability and cost control of upstream raw materials are the top concerns for IVD companies at present. Many large domestic IVD enterprises are acquiring raw material suppliers or establishing their own raw material subsidiaries to address supply chain challenges in upstream raw materials," said an industry insider.

This will, to some extent, also compress the market space for raw material companies. Against this backdrop, a segment of upstream raw material suppliers has begun to actively expand their business into the downstream in vitro diagnostics (IVD) sector.

For instance, Fapon Biotech expanded its business to offer integrated reagent and instrument solutions, and further entered the booming field of next-generation sequencing (NGS) by acquiring the remaining equity interest in Sequlite Genomics, a high-throughput gene sequencing R&D company, in October 2021. Vazyme has also successfully established a POCT product portfolio covering eight series, including cardiovascular and cerebrovascular diseases, inflammation and infection, eugenics and prenatal care, and gastric function.

III. Pandemic and Centralized Procurement Accelerate the Pace of Domestic Substitution

Last August, Anhui Province fired the first shot by launching centralized procurement for in vitro diagnostic (IVD) reagents. With the official implementation of the procurement results in Anhui, the “Anhui Model” for volume-based procurement of laboratory reagents has taken shape, setting a precedent and providing a demonstration for other regions across China to carry out similar volume-based procurement initiatives.

In the past, due to high gross margins, most reagent manufacturers were not sensitive to costs. Now that prices have declined while quality must still be guaranteed, cost reduction has become an urgent priority.

Dr. Ren Hui stated, “Currently, many domestic IVD manufacturers are actively seeking Chinese-made alternatives to imported raw materials, and it is expected that the localization of IVD raw materials will be widely achieved within five years.”

Multiple companies have switched to domestic raw material suppliers to reduce reagent costs; for instance, YHLO and Meikang have collaborated by integrating chemiluminescence and biochemical reagents. Furthermore, in Anhui’s centralized procurement program, some mainstream foreign enterprises withdrew their bids, thereby accelerating the process of domestic substitution in the chemiluminescence sector.

On the other hand, the ongoing pandemic may break the long-standing monopoly of imported brands in China’s IVD raw material market, accelerating the substitution with domestically produced alternatives and becoming the main theme of industry development.

A PCR manufacturer once shared such an experience: after the outbreak of the COVID-19 pandemic, raw materials were either in short supply or saw price increases. Moreover, the price hike was not merely 10%, but a tenfold increase. In the post-pandemic era, most companies have begun to consider how to build more secure supply chains.

Since 2020, international logistics has been significantly impacted by the dual pressures of the COVID-19 pandemic and the China-US trade war. In 2020, the revenue growth rates of imported brands Thermo Fisher and Abcam in China declined substantially, reaching 1.64% and -1.76%, respectively. This trend not only reflects the supply chain risks faced by importers but also exposes the long-standing dominance of imports in China’s IVD raw material market. As a result, supply chain localization has garnered increasing attention from domestic research institutions and enterprises, bringing unprecedented development opportunities to the IVD raw material industry.

The biological reagent industry is characterized by high technical barriers. Downstream customers conduct lengthy evaluations and screening of upstream suppliers regarding product performance, supply chain stability, and other factors, resulting in strong customer stickiness. Consequently, imported brands with first-mover advantages have established significant brand barriers.

Zhu Qishan from the Ailingda IVD Industrialization Platform stated that, affected by the pandemic, the prices of imported IVD raw materials have multiplied, and transportation times have been significantly prolonged. In contrast, China offers cost advantages as well as logistical and market channel benefits, which will accelerate the pace of domestic substitution.

Furthermore, imported brands rarely engage in direct sales within China, predominantly relying on domestic distributors for sales. This results in longer procurement cycles and higher end-user prices. The pandemic exacerbated these issues, leading to a multiplicative increase in both prices and procurement lead times. Among domestic raw material manufacturers, Vazyme, Sino Biological, and ACROBiosystems primarily adopt a direct sales model supplemented by distribution. From 2018 to 2020, their direct sales proportions all exceeded 60%. This approach not only provides cost advantages but also ensures after-sales service, enabling timely and rapid responses to meet customers’ diverse needs.

IV. R&D Difficulties, Fragmented Competition, and Low Brand Recognition Hinder the Pace of Domestic Substitution

The in vitro diagnostic (IVD) reagent raw material industry in China started relatively late. Compared with overseas IVD reagent raw material companies,Achieving domestic substitution still faces numerous challenges, primarily manifested in the gaps in R&D capabilities and technological process levels, highly fragmented industry competition, and low brand trust.etc.

First, the research and development of raw materials for in vitro diagnostic reagents is highly challenging, with complex production technology routes and process flows., domestically produced in vitro diagnostic (IVD) raw materials still lag behind imported ones in terms of quality control, manufacturing processes, and purity.

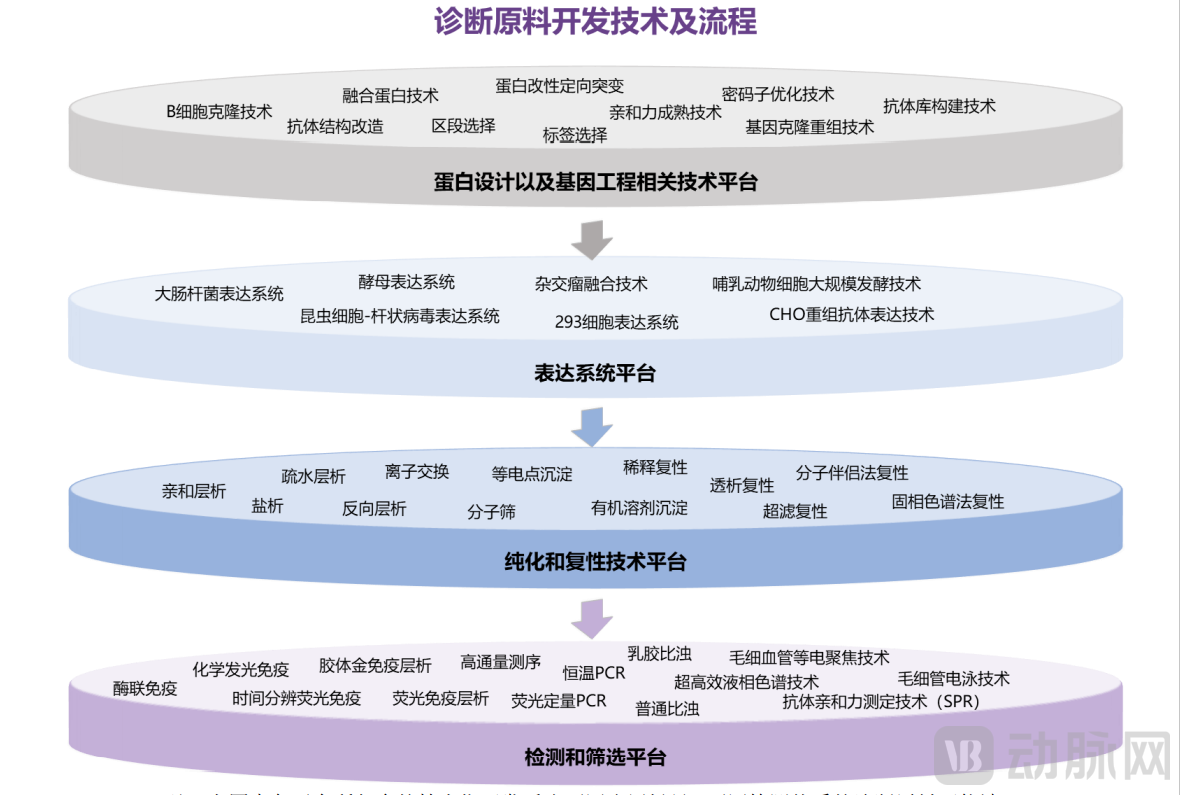

Technologies and Processes for the Development of Diagnostic Raw Materials. Image source: Fapon Biotech's prospectus

According to the prospectus of Fiton Biologics, the complete underlying technology platform for IVD raw materials involves numerous technical pathways and stages, making it difficult for small and medium-sized laboratories to establish a comprehensive underlying technology platform. Furthermore, in vitro diagnostics encompasses various diagnostic methodologies, each involving multiple diagnostic assays. This results in a wide variety of core reagent raw materials, reagents, and instruments required, with differing technical systems needed for mastery. The industry is predominantly composed of small and medium-sized enterprises, and few companies are able to invest substantial capital and time into foundational research, which is characterized by long cycles and high levels of difficulty.

Enhancing innovation capabilities and product quality serves as the core driver for the development of in vitro diagnostics (IVD) enterprises. It is essential to establish a more robust technical framework and implement more systematic and rigorous quality control. Strict oversight must be maintained throughout the entire process, including raw materials, research and development, production processes, and quality control, to ensure the quality of core raw materials. This will further enhance innovation capabilities and product quality, thereby continuously strengthening core competitiveness.

Second, the global IVD raw material market features numerous participants, small individual company sizes, and a highly fragmented industry.Even leading enterprises such as Fitop Biological, HyTest, BBI Solutions, and Meridian hold only around 5% of the global market share each, while numerous small and medium-sized laboratories have carved out a niche in the industry by supplying several specialized products. The IVD raw materials industry encompasses a wide range of fields and technological platforms, making it extremely challenging for any single company to achieve comprehensive product line coverage. Product portfolio “breadth” and “depth” constitute the core competitiveness of bioreagent manufacturers. By adopting an “organic growth + mergers and acquisitions” strategy, these companies can establish a complete and diverse product matrix that covers multiple application scenarios, thereby meeting the varied needs of downstream customers.

Third, the industry has high brand barriers.During the R&D phase, in vitro diagnostic (IVD) reagent manufacturers must invest significant time and capital to verify the reliability of raw materials in order to ensure product quality. Consequently, many midstream companies prefer core raw material suppliers with long operating histories and high brand recognition. Once these products are adopted and validated, they generate strong customer stickiness, creating substantial brand barriers within the industry. IVD reagent manufacturers have traditionally favored imported core raw materials. Furthermore, for an extended period, most domestic IVD manufacturers in China discriminated against domestically produced raw materials due to various factors, leaving Chinese raw material suppliers in a disadvantaged position.

In fact, with continuous investment in technology and R&D by domestic brands, some have already broken through key technical barriers, with product performance on par with imported counterparts. Meanwhile, they hold greater advantages in logistics supply, technical services, and meeting special project requirements within China. While continuously enhancing technology and optimizing process quality, persisting in reputation-based marketing and customer service to gradually build a brand image with market influence is also a pathway to achieving further breakthroughs.

Moreover, domestic IVD raw material manufacturers possess significant localization advantages, including more controllable production cycles and logistics processes, shorter lead times, and lower communication costs with customers compared to multinational corporations.

V. Four Major Development Trends in the Future

The IVD raw materials industry is in an era of major transformation. Driven by the rapid growth and demonstrative effects of leading enterprises, the swift expansion of specialized small and micro enterprises in niche markets, and increased attention from financial capital, the industry has entered a phase of rapid development. What trends will characterize the industry’s future evolution?

First, integrating instruments and reagents to provide an integrated solution is a major development trend.Providing comprehensive solutions that span raw materials and semi-finished reagents to supporting equipment can reduce redundant R&D investments for downstream customers, facilitate rapid reagent development, and accelerate industrialization. This approach aligns with the development trends of leading global IVD raw material manufacturers. Represented by Fapon Biotech, approximately RMB 880 million—the largest portion of its RMB 2.5 billion in substantial fundraising—will be invested in integrated equipment-reagent solutions, offering downstream customers a full range of upstream products, including raw materials, semi-finished reagents, and compatible instrument platforms.

Second, the highly fragmented market offers participants ample room for growth and consolidation, with mergers and acquisitions expected to become more frequent in the future.Most domestic IVD raw material companies have relatively single business directions and are prone to hitting a growth ceiling. By expanding operational scale through mergers and acquisitions, especially overseas M&A, building a comprehensive technical system, establishing strong product development and iterative update capabilities, and constructing a robust sales network, these companies will find it easier to stand out in global competition.

Third, leveraging its advantages in raw materials, the company independently obtains certifications and builds a platform to expand downstream.Representative companies such as Vazyme have leveraged their R&D and manufacturing capabilities in the field of IVD raw materials to independently obtain regulatory approvals for supporting instruments and test kits, thereby entering the downstream market. This expansion has diversified their business models and increased their market potential. Once new technologies or rare biomarkers gain clinical recognition, they can further drive demand for their raw material business. However, disadvantages include the risk that existing customers may switch to other raw material suppliers due to competitive conflicts, as well as uncertainties associated with downstream market development.

Finally, focus on the core technologies of the raw material industry to expand brand influence.The raw material industry features high barriers across multiple dimensions, including technology, processes, production, sales, and branding. Top-tier raw material suppliers do not merely follow technological trends; instead, they are deeply committed to R&D with the aim of setting those trends. Such enterprises can provide comprehensive coverage from scientific research to IVD (In Vitro Diagnostic) raw materials, focusing on refining R&D technologies and manufacturing processes to establish their brand as a premium provider of high-quality raw materials.

2021 was destined to be an extraordinary year for the IVD raw materials sector, and we will wait and see whether the industry can sustain existing trends in 2022.

References:

Comprehensive Assessment of China’s IVD Testing Equipment Industry (2021–2026) and Investment Planning Recommendations — Huajing Industry Research Institute

Soaring IVD: The 3 Most Anticipated Sub-Sectors! — Haoyue Capital

In-Depth Report on the Biological Reagents Industry: Domestic Substitution Is Gaining Momentum, and "Hidden Champions" Are Poised for Rise – Guoyuan Securities