Digital CRO Emerges as Hottest Segment in Healthcare Digitization with 3x TAM Expansion and CAGR Over 15%

On January 24, Boji Medicine released its 2021 annual earnings forecast, stating that it expects to achieve a net profit of RMB 37 million to RMB 48 million for the period from January 1, 2021, to December 31, 2021, representing a year-on-year growth rate of 117.79% to 182.54%. The net profit for the same period in the previous year was RMB 16.9886 million.

This is not the first CRO company to disclose its 2021 annual report performance. To date, a large number of companies in the CRO industry, including WuXi AppTec and Tigermed, have released their 2021 earnings forecasts, with overall performance trending positively.In 2021, the CRO industry maintained robust momentum overall, driving significant performance growth for related companies.

Incomplete Statistics on 2021 Annual Earnings Previews of CRO Companies (Source: Compiled from Public Information)

Meanwhile, digital CROs have also seen significant growth in the past two years.

In fact, as early as 2018, Scott Gottlieb, then Commissioner of the U.S. Food and Drug Administration (FDA), publicly stated thatBetter leveraging digital tools to capture and audit data helps reduce R&D costs, urges the industry to abandon traditional manual research methods employed by contract research organizations (CROs), and drives the full integration of drug development and regulatory processes into the digital era.

On the international stage, digital CROs are no longer a novel concept. The industry features both clinical CRO giants like IQVIA and startups such as Science37. Although China entered this field relatively late, its digital CRO sector has begun to develop rapidly in recent years.

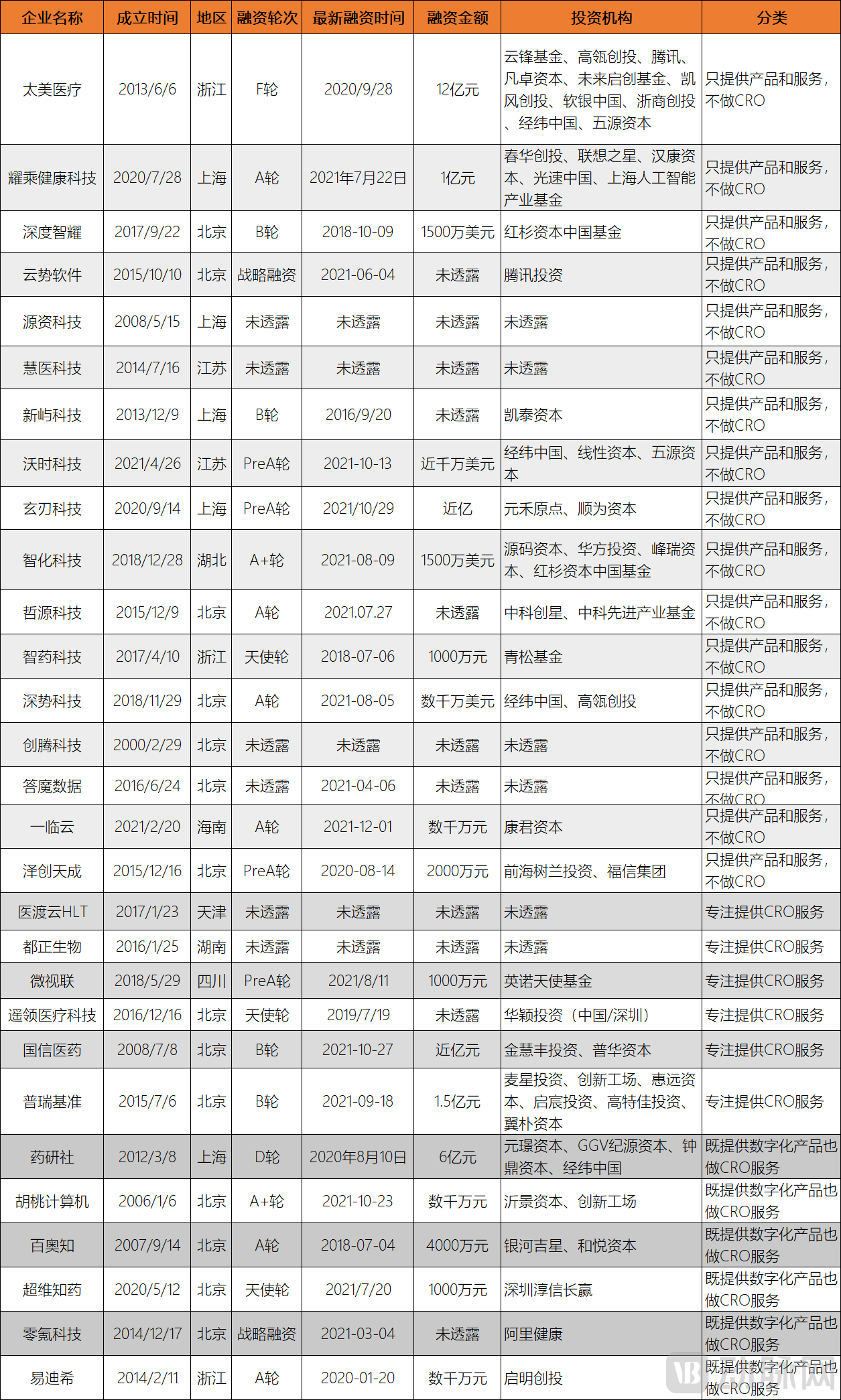

Where Does China’s Digital CRO Industry Stand Today? Which Companies Have Entered the Market? VCBeat Has Compiled a List of 29 Companies Related to Digital CROs, Primarily Covering Digital CRO Firms and Their Upstream Suppliers, Providing an Overview of the Development of China’s Digital CRO Industry from a Corporate Perspective.

In our inventory, we primarily focus on companies in the clinical stage, excluding those in stages such as drug discovery.Due to constraints on time and data volume, the data we have collected may not be exhaustive. Companies not included are encouraged to contact us.

"Digital CROs" primarily refer to contract research organizations that leverage innovative technologies such as big data, artificial intelligence (AI), and cloud computing to accelerate clinical trial processes, shorten drug development cycles, and reduce R&D costs. This term also encompasses upstream enterprises that provide digital clinical trial systems, services, or products built on tools including Clinical Trial Management Systems (CTMS), Electronic Data Capture (EDC), electronic Patient-Reported Outcomes (ePRO), and Pharmacovigilance (PV) platforms.

Digital CROs primarily leverage digital technologies to empower one or more stages of clinical trials, thereby enhancing the accessibility, accuracy, safety, and efficiency of these trials, and ultimately achieving a win-win outcome for multiple stakeholders, including patients, pharmaceutical companies, and clinical trial institutions.。

The majority of digital CRO companies and their upstream suppliers operate across both the software and information technology services sector and the biopharmaceutical industry. Digitalization in the pharmaceutical sector covers the entire lifecycle from drug development to marketing, and is currently commonly referred to collectively as “medical cloud.”

In its research report titled "Healthcare Cloud Computing—Global Market Trajectory and Analysis," the market research firm Global Industry Analysts pointed out that,The global healthcare cloud computing market is projected to grow at a compound annual growth rate (CAGR) of 19.6%, reaching a market size of $76.8 billion by 2026. Meanwhile, after accounting for the impact of the COVID-19 pandemic and the ensuing economic crisis on business, the report forecasts that the software segment within this industry will achieve a CAGR of 15.9% from 2020 to 2026.

The penetration rate of CROs is also continuously increasing.According to Frost & Sullivan’s previous forecasts, the penetration rate of the global CRO industry in the pharmaceutical market was in a phase of rapid growth, rising from 18% in 2006 to 44% in 2017, and is projected to reach 54% by 2020.This figure should have increased slightly by now.

As a critical link in the pharmaceutical R&D industry chain, Contract Research Organizations (CROs) play an increasingly significant role in shortening drug development cycles and reducing R&D costs. In terms of accelerating timelines, for comparable R&D projects, CROs typically reduce the required time by approximately 20%–30% compared to when pharmaceutical companies conduct the work in-house.

Ren Wei, co-founder of the digital CRO company Walnut Computer, told VCBeat that digitally enabled CROs capable of structural adjustments will see their efficiency increase exponentially. From this perspective, the industry generally believes that the incremental market for digital CROs will be more than three times the size of the existing market.

Ren further explained that institutional restructuring is not merely a partial improvement. In simple terms, project design must be evidence-based (leveraging the hospital’s historical data); during the execution phase, evidence should be automatically collected and quantified, with integrated data processing, analysis, and statistics; monitoring and traceability must rely on remote technologies and electronic information security technologies; the system must align with the CTD standards and interfaces already provided by drug regulatory authorities; and it must feature digital QA. “Only through platform collaboration of this nature can projects be implemented in an operable, high-efficiency, low-cost, and large-scale manner.”

Ren Wei emphasized that the primary issue addressed by all digital CROs is replacing low-productivity tasks through automation, thereby structurally transforming the entire industry.

Based on VCBeat’s analysis of 29 companies,Currently, there are two major product models in the digital CRO industry: one is providing platform-based digital products, and the other is offering digital clinical research services.

Two major product forms have given rise to three business models: the first type of enterprise provides only digital platforms, such as Taimei; the second type offers only digital CRO services, such as HLT; and the third type combines both, featuring a digital platform while also providing clinical research services based on that platform, such as Yaoyanshe.

Among the 29 companies included in our statistics, those offering only digital platforms were the most numerous, totaling 17 (58.62%), which accounts for more than half; six companies provided only digital CRO services; and another six offered both types of products.

Incomplete List of Digital CRO Companies (Not in Order of Ranking; Data Source: Compiled from VCBeat and Public Information)

HLT (Happy Life Technologies), a representative enterprise focused on providing digital CRO services, primarily offers big data technology and AI-enabled solutions for innovative pharmaceutical research. HLT boasts an EDC product line validated by the professional organization NNIT and an excellent team of clinical research professionals. It provides pharmaceutical companies with full-lifecycle product solutions, including clinical trials, drug launch strategies, and real-world studies to assess drug safety, efficacy, cost-effectiveness, and indication expansion, thereby accelerating new drug development and improving drug accessibility.

Since its inception, HLT has leveraged medical artificial intelligence technology to develop carriers and platforms featuring multiple innovative technical applications, serving numerous renowned hospitals, government agencies, and large multinational pharmaceutical companies.

Yaoyanshe is dedicated to providing innovative drug R&D services to pharmaceutical companies. It has established standardized and streamlined processes for pharmaceutical R&D, creating the “Yaoyanshe Model,” which balances quality, cost, and efficiency. Compared with traditional models, this approach reduces the overall R&D cycle by 20% and lowers average costs by 15%.

Starting with digital products designed to serve clinical research, its business has gradually expanded to encompass a one-stop suite of services, including CRO, SMO, rapid site initiation, patient recruitment, staffing outsourcing, and intelligent data services. Meanwhile, Drug Research Club leverages its clinical research entry platform, “Trial.Link,” to intelligently match all parties involved in drug development, breaking down information barriers and reducing communication costs.

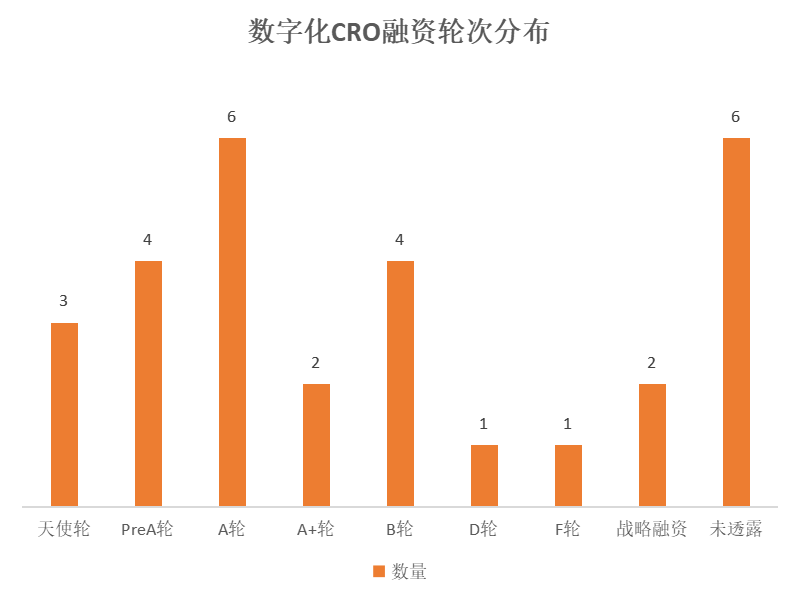

An Analysis of Digital CRO Companies: From the perspective of funding round distribution, financing in the digital CRO industry is primarily concentrated in rounds prior to Series A+. Excluding companies that have not disclosed their funding information, those in rounds prior to Series A+ account for more than 60%. In contrast, only one company each has reached Series D and Series F, namely Yaoyanshe and Taimei, respectively.

(Data source: Compiled based on VCBeat and publicly available information)

An analysis of the financing landscape reveals that the industry is relatively nascent and dominated by startups; however, leading companies have already emerged, having established successful business models.

Among them, the industry leader Taimei has secured seven rounds of financing totaling RMB 2.355 billion in the ten years since its inception. Notably, its Series F round in 2020 alone raised RMB 1.2 billion. The company has consistently ranked among unicorn enterprises for several consecutive years and disclosed its prospectus on December 29, 2021, as it geared up for an initial public offering (IPO).

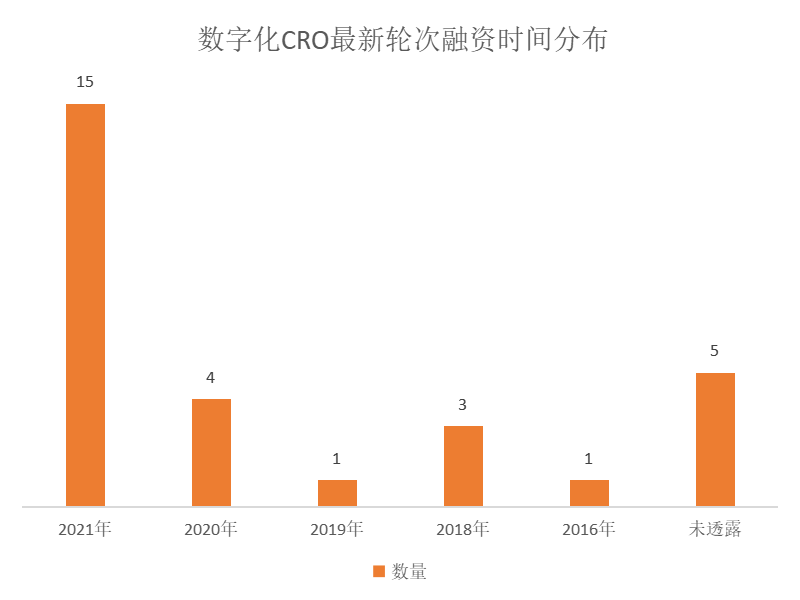

Based on the timing of the latest funding rounds, the digital CRO sector saw active investment and financing in 2021, with more than half of the companies securing their most recent round of funding that year.From the perspective of financing rounds, the industry is witnessing an upgrade in funding, with companies advancing to later-stage financing rounds, indicating that the sector’s development is accelerating.

(Data source: Compiled based on VCBeat and public information)

It can be said that the digital CRO industry is developing rapidly and holds immense potential; however, according to relevant investors, competition within the sector is intensifying, leading to heightened requirements for corporate operations, teams, funding, strategic positioning, and service quality.

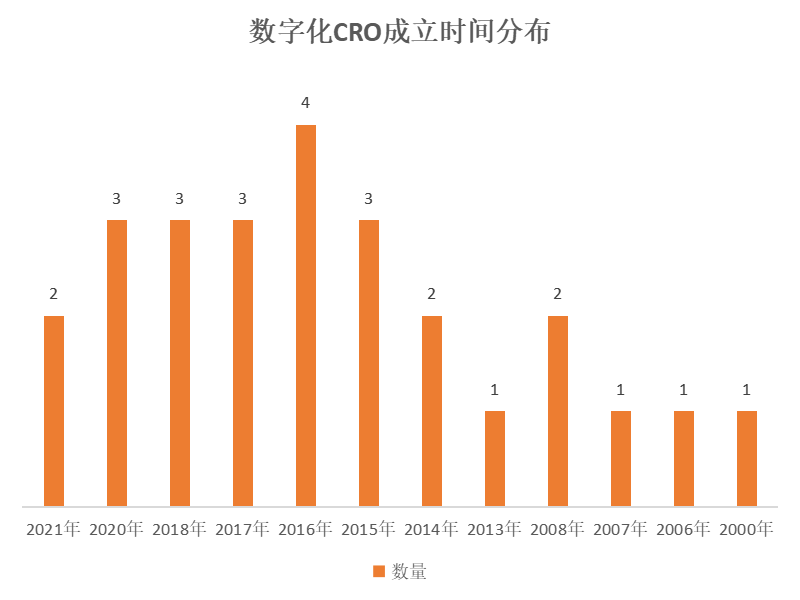

In terms of the distribution of establishment dates, more than 50% of the companies were founded in 2016 or later.This is inseparable from the fact that, starting in 2015, healthcare reform entered a critical phase, marked by the intensive rollout of various policies in the pharmaceutical and medical industries.

(Data source: Compiled based on VCBeat and public information)

The report “Quarterly Journal on Digital Healthcare Innovation: Framework for Digital Transformation in the Pharmaceutical Industry,” released by VCBeat and VBInsight, points out that over the past six years, the entities issuing policies in the pharmaceutical industry have shown a trend toward diversification, including multiple departments such as the State Council, the Ministry of Commerce, and the National Healthcare Security Administration. A large number of policies have been issued, with dozens of key national-level policies and hundreds of documents, while governments at all levels have successively released detailed implementation measures. These policies comprehensively cover four major areas: pharmaceutical R&D and manufacturing, commercial distribution, healthcare services, and pharmaceutical consumption.

Under such policy circumstances, on the one hand, the government has increased its support for digital healthcare infrastructure, improved the population health information service system, and promoted the application of big data in healthcare; on the other hand, with the establishment of the National Healthcare Security Administration and the introduction of a series of policies including the “Two-Invoice System,” consistency evaluation of generic drugs, and the “4+7” volume-based procurement program, cost containment and price reduction have become the central themes of pharmaceutical reform.This has compelled pharmaceutical companies to adopt digital technologies to improve efficiency and reduce costs. It has also created significant opportunities for digital CROs and their upstream partners, who are seizing the momentum driven by favorable policies.

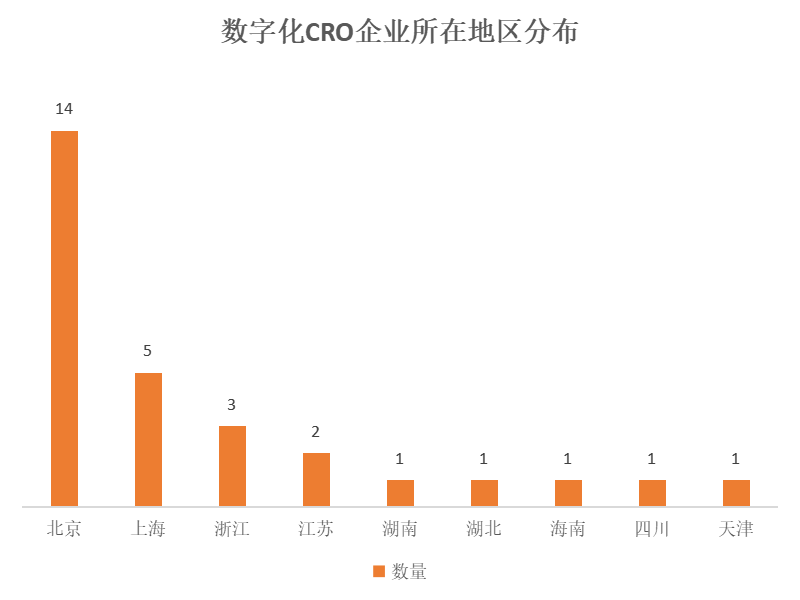

In terms of geographic distribution, Beijing and the Yangtze River Delta region far surpass other areas with a significant numerical advantage; notably, Beijing, with 14 companies accounting for nearly half of the total, greatly exceeds Shanghai, which ranks second.It is also evident that the eastern region holds a regional advantage in terms of resources. Other regions still lag significantly behind in areas such as technology and capital. For digital CROs, which span healthcare, software, and information technology—and require cutting-edge technologies, highly skilled talent, and substantial funding—the eastern region, particularly Beijing, the capital, is more attractive.

(Data source: compiled based on VCBeat and public information)

Taimei, Drug Research Club, Yaosheng Health Technology, Walnut Computer, Deepwise, EDCiX, and Yaoling Technology are all located in Beijing and the eastern region of China, while HLT is based in Tianjin, near Beijing.

The promulgation of policies and the aggregation of regional resources are driving the rise of digital CROs.

According to the industry analysis report “Quarterly Journal of Digital Healthcare Innovation: Five Major Scenarios for the Implementation of Digital Transformation in the Pharmaceutical Industry” released by VCBeat and VBInsight, it is predicted thatDigital-native enterprises will accelerate their integration with pharmaceutical companies.Digital-native enterprises that provide customized services to pharmaceutical companies may, through mergers and acquisitions, transition from providers of digital technology services to internal functional departments within pharmaceutical firms, thereby achieving mutual integration between the two.

Ren Wei stated,Digital CROs will enter this field by empowering traditional CROs with technology through methods such as mergers and acquisitions.Traditional CROs, constrained by their inherent corporate DNA, may lack the courage and capability to challenge their own values and pursue digital transformation independently.

For example, as a giant in the traditional CRO industry, one of WuXi AppTec’s development paths to achieve scale and strength has been through mergers and acquisitions: acquiring Pharmapace to enhance statistical data analysis capabilities during clinical trials; acquiring ResearchPoint Global to improve clinical research service capabilities; and investing in Engine Biosciences to advance the application of innovative technologies such as AI and big data in clinical settings.

As a representative example of digital CRO enterprises, HLT has achieved a perfect integration of its big data technology, AI capabilities, and technological strength in the medical field with PPD’s globally leading clinical research expertise through a strategic partnership with the international CRO giant PPD. This strong collaboration comprehensively empowers key stages including IND registration, clinical trial protocol design, clinical trial quality management, and patient enrollment efficiency.

Globally, developed countries such as the United States have achieved a mature stage in the digital CRO sector. Companies represented by Veeva and Medidata have established comprehensive SaaS product lines in areas including pharmaceutical clinical R&D and pharmaceutical marketing, offering cloud computing-based platform solutions for the pharmaceutical industry. In addition, Science37 is dedicated to developing innovative clinical trial models, along with its proprietary operating system and platform that enable patients to participate in clinical trials from home, reflecting the future trend toward decentralization in clinical trials.

Among them, Veeva has been operating in China since 2011 and currently maintains regional offices in Beijing, Shanghai, Dalian, and other cities. Medidata officially entered the Chinese market in 2015 and currently has branches in Beijing, Shanghai, and other locations.

For a long time, foreign pharmaceutical digitalization vendors have dominated the Chinese market, benefiting from years of experience and technological accumulation. In recent years, with the state’s increasing emphasis on new drug research and development, a number of emerging domestic providers of digital products and solutions for clinical research have entered the market. By leveraging their cost-effectiveness and closer alignment with local market needs, these companies have captured a certain share of the market, gradually breaking the previous dominance of foreign vendors and establishing advantages in user base, technology, and brand recognition.

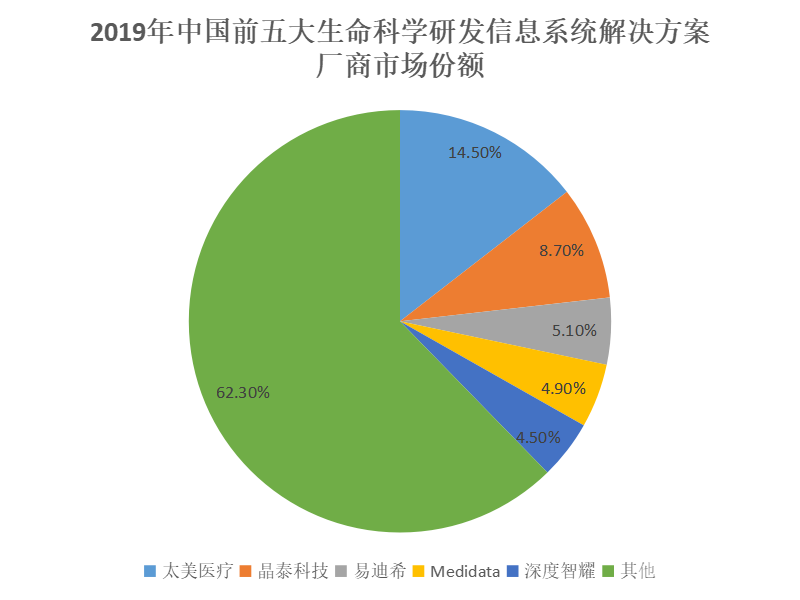

According to relevant data from the report “China Life Sciences R&D Information System Market Share, 2019: Emerging IT Technologies Accelerate New Drug Development,” released by IDC in November 2020,In 2019, the top five vendors of life sciences R&D information system solutions in China held a combined market share of 37.7%. Taimei Medical Technology ranked first with a 14.5% market share, followed closely by XtalPi with 8.7%. Yidixi and Medidata ranked third and fourth, with market shares of 5.1% and 4.9%, respectively. Deep Intelligence held a 4.5% market share.

(Data source: IDC, “Market Share of China’s Life Sciences R&D Information Systems, 2019: Emerging IT Technologies Accelerating New Drug Development”)

As previously mentioned, Taimei leverages digital technologies such as cloud computing, artificial intelligence, and big data to provide pharmaceutical digital solutions for the life sciences industry. Evolving from scattered, scenario-specific standalone solutions to the integrated TrialOS platform, Taimei has established its own pharmaceutical digital ecosystem.

XtalPi’s business is focused on the drug discovery phase. Since its inception, XtalPi has successively established collaborations with Pfizer and Singlera Genomics, dedicated to new drug discovery and target-based drug development.

Yidixi, a subsidiary of Tigermed, was established in 2014. Currently, in the field of innovative drugs, Yidixi has successfully completed multiple Phase III clinical trials utilizing the Clinflash EDC and Clinflash IRT systems, with several products successfully filing New Drug Applications (NDAs) and achieving market launch. Clinflash Safety is also adopted by renowned pharmaceutical and medical device companies both in China and abroad. Compliant with the E2B R3 standard, this system is widely used for the submission of individual case safety reports and signal monitoring in both clinical trials and post-marketing settings.

DeepGlow is dedicated to building an end-to-end AI-driven system platform, empowering and accelerating the comprehensive intelligent digital transformation of global pharmaceutical companies. In 2018, just one year after its establishment, DeepGlow secured four rounds of investment. Since its inception, DeepGlow has successively established collaborations with Medrio, Inc., China Pharmaceutical University, and Sinopharm.

Overview of the Top Four Domestic Companies by Market Share (Data Source: Compiled based on Artery Orange and public information)

Overview of the Top Four Domestic Companies by Market Share (Data Source: Compiled based on Artery Orange and public information)

Currently, although the four major domestic enterprises have captured over 30% of the market share, the development of domestic companies as a whole remains in its early stages.

At the Digital Pharmaceutical R&D Forum of the 2021 5th Future Healthcare Top 100 Conference, held on April 18, 2021, Ma Dong, Partner at Taimei Medical Technology, also mentioned in his speech that the complexity of new drug clinical development is continuously increasing, and regulatory policies are being strengthened.However, the digitalization of the pharmaceutical industry remains at a relatively low level. The digital transformation of pharmaceutical R&D has evolved through stages of localization, digitization, platformization, and ecosystem integration. In the future, the core value of R&D digitalization will lie in supporting the formulation, implementation, and adjustment of R&D strategies, while also enabling efficiency optimization and performance enhancement in R&D operations.

In 2021, the CRO industry maintained strong momentum, driving significant performance growth for related companies. To date, a large number of CRO firms, including WuXi AppTec and Tigermed, have disclosed their 2021 earnings forecasts, with overall results trending positively.

On January 24, Boji Medicine released its 2021 annual earnings forecast, stating thatThe company is expected to achieve a net profit of RMB 37 million to RMB 48 million from January 1, 2021 to December 31, 2021, with a growth rate of 117.79% to 182.54%., with a net profit of RMB 16.9886 million in the same period last year.

Regarding the primary reasons for the changes in its 2021 performance, Boji Medicine stated that during 2021, the company’s projects under development advanced steadily, and its main business revenue increased compared to the same period of the previous year, resulting in an increase in the net profit attributable to shareholders of the listed company for 2021 compared to the same period of the previous year.

On January 21, Pharmaron’s disclosure of its 2021 annual earnings forecast showed thatThe company expects to achieve full-year 2021 revenue of RMB 7.341 billion to RMB 7.495 billion, representing a year-on-year increase of 43%–46%.Regarding the changes in performance, Pharmaron stated that, in terms of its core business, the company’s operational plans were carried out in an orderly manner during the reporting period. In 2021, revenue from core operations grew steadily, with scale efficiencies and operational effectiveness of mature service lines gradually improving, leading to enhanced profitability.

Joinn Laboratories issued its earnings forecast on January 20. The forecast shows that,The net profit attributable to shareholders of the listed company in 2021 is expected to increase by approximately RMB 227 million to RMB 259 million compared with the same period of the previous year, representing a year-on-year increase of approximately 72.3% to 82.3%.During the reporting period, the company established and standardized an industry-leading innovative drug evaluation technology platform. The capacity utilization rate of the company’s laboratories continued to rise, ensuring efficient execution of orders on hand. Meanwhile, the supply side provided strong support for performance growth.

On January 18, the earnings forecast released by Medicilon showed that,It is estimated that the net profit attributable to shareholders of the parent company in 2021 will be between RMB 278 million and RMB 291 million, representing a year-on-year increase of 115% to 125%.It is reported that the company's newly signed orders in 2021 increased by approximately 88% year-on-year, and its operating revenue is expected to increase by approximately 78% year-on-year.

Furthermore, according to data from Choice,Over the past 30 days, MediciBio ranked third in the number of institutional surveys conducted in the secondary market, with a total of 21 visits., attracting significant attention from market institutions.

On January 12, Tigermed’s disclosed earnings forecast showed thatThe company expects to achieve a net profit of RMB 2.624 billion to RMB 3.027 billion in 2021, representing a year-on-year increase of 50%–73%.During the reporting period, the Company’s core business continued to grow, with both revenue and net profit attributable to shareholders of the listed company for the year 2021 expected to increase compared with the same period of the previous year.

WuXi AppTec’s 2021 earnings forecast shows that,For 2021, WuXi AppTec is expected to report a net profit of RMB 4.973 billion to RMB 5.032 billion, representing a year-on-year increase of approximately 70%.WuXi AppTec stated that both its chemistry and testing businesses achieved strong growth, which, combined with the impact of non-recurring gains and losses, resulted in a significant year-on-year increase in net profit.

In 2021, CRO companies experienced rapid performance growth, and the CRO industry as a whole developed swiftly. Digital CRO companies spanning two major fields, along with their upstream enterprises, also showed overall positive momentum. Digital CRO companies have not only provided software and computing platforms for the life sciences industry but are also driving transformation across the entire life sciences sector. Furthermore, they are fostering increasingly tight integration between technologies such as software and computing with drug development and clinical treatment, making research and development as well as therapeutic interventions more targeted.

Overall, the digital CRO industry is accelerating its development, and competition within the sector is intensifying. However, as clinical trials continue to expand, the overall market size of the clinical CRO industry is expected to grow further, thereby enhancing the market competitiveness of digital CROs.