Genesis MedTech Acquires JieCheng Medical, a Leading Chinese TAVR Innovator, Ahead of IPO Filing

Recently, emerging medical technology company Genesis MedTech announced the completion of its acquisition of Jiecheng Medical.

Jiecheng Medical is a leading enterprise in China’s transcatheter heart valve sector. Its flagship product, the “J-Valve Precise Positioning Heart Valve Implantation System” (hereinafter referred to as the J-Valve or J-Valve prosthesis), has driven source-level technological innovation in China’s TAVR field, breaking international monopolies.

As a "pioneer" in technological innovation for heart valves, Jiecheng has a 13-year development history, and its founder, Zhang Ji, was formerly a cardiac surgeon. The J-Valve, independently developed by Jiecheng, boasts globally leading technology and worldwide independent intellectual property rights.

Since its official commercial launch in July 2017, the J-Valve has been adopted by nearly 200 hospitals worldwide, with an annual TAVR implantation volume approaching 1,000 cases. It has secured a top-three market share in China and successfully exported dozens of units to developed Western countries, including Canada and the United States.

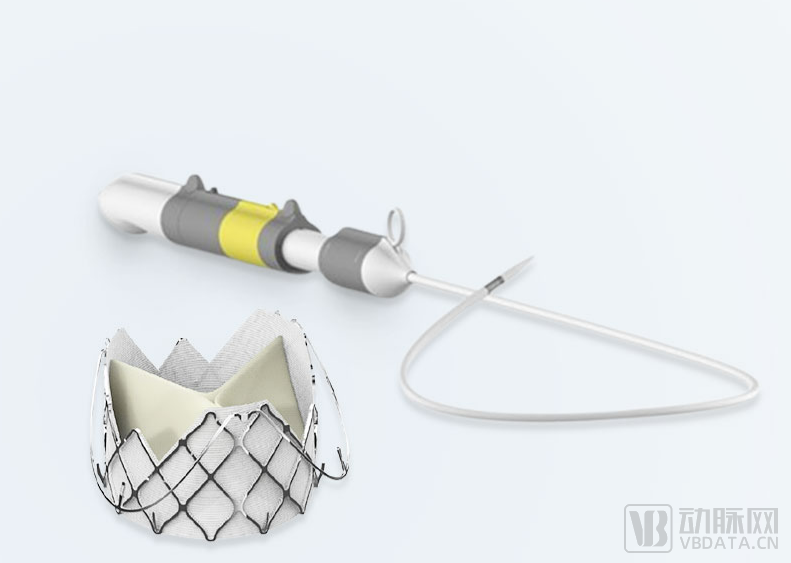

J-Valve-TF Transvascular Interventional Biological Heart Valve Replacement System

What Makes the J-Valve Unique? What Are the Growth Prospects for Jiecheng Medical Following Its Acquisition? VCBeat (WeChat ID: vcbeat) Conducted a Comprehensive Analysis.

Valvular heart disease is a type of structural heart disease, clinically characterized by morphological and structural abnormalities of one or more heart valves. The human heart has four valves: the mitral valve, aortic valve, tricuspid valve, and pulmonary valve. These valves regulate the flow of arterial blood (oxygenated) and venous blood (deoxygenated) through their normal opening and closing actions.

However, if valvular stenosis or regurgitation occurs, it will impede normal blood flow, thereby causing functional cardiac impairment; the most common conditions are mitral and aortic valve diseases.

Taking aortic valve disease as an example, if patients do not receive prosthetic valve replacement surgery in a timely manner, the one-year mortality rate exceeds 30%, the five-year mortality rate approaches 70%, and the risk of sudden cardiac death is extremely high.

Currently, the clinically effective valve replacement procedures mainly include traditional open-heart surgery and interventional therapy.

Traditional open-heart surgery requires thoracotomy for prosthetic valve replacement under general anesthesia and cardiopulmonary bypass. The vast majority of elderly patients (defined as those aged 80 years or older) cannot tolerate this invasive procedure.

Other patients, such as those with poor cardiac function, severe comorbidities, or multiple organ dysfunction, are also unable to tolerate the procedure; these patients account for 30%–50% of all patients with aortic valve disease. In addition, 25%–30% of patients reluctantly forgo treatment due to high hospitalization/readmission rates and substantial medical costs.

Overall, more than half of patients are not candidates for surgical intervention. Therefore, a minimally invasive solution for valvular heart disease—Transcatheter Aortic Valve Replacement (TAVR)—has emerged.

During TAVR, the physician advances a guidewire via a transvascular or transapical approach to deliver the crimped prosthetic valve to the site of the diseased native valve, thereby replacing its function. The entire procedure is performed without thoracotomy, resulting in minimal trauma to the patient.

Since the first TAVR procedure was performed in 2002, the annual number of TAVR cases worldwide has risen exponentially. Although TAVR technology is now widely and maturely applied globally, unlike open-heart surgical valve replacement under direct vision, TAVR relies on imaging guidance for valve implantation, posing technical challenges such as precise positioning and achieving in-situ fixation without sutures.

To address these challenges, Genesis has developed the “J-Valve Precision Positioning Heart Valve Implantation System.” J-Valve is a next-generation transcatheter heart valve capable of treating both aortic stenosis and aortic regurgitation. It features a 30-day pacemaker implantation rate of less than 5%, significantly outperforming other TAVR products, and offers the following technical advantages:

First, the J-Valve can achieve rapid positioning solely through its own anchoring system, significantly reducing paravalvular leakage and minimizing reliance on imaging technology, thereby substantially lowering the procedural difficulty for physicians. Meanwhile, the design of the J-Valve’s anchoring system provides coronary protection, offering an optimal solution for the challenge of low coronary ostia.

Currently, only JenaValve has developed an interventional valve with a positioning element design abroad; however, its positioning elements are fixed to the stent and cannot fully expand, thereby limiting their functionality. In contrast, the J-Valve achieves self-positioning through a movable connection-based positioning system, offering significant advantages.

The J-Valve prosthesis locates the aortic sinuses via its positioning elements, self-adjusts to align with the valve implantation site, and completes the entire valve replacement procedure.

Second, in addition to treating aortic stenosis, the J-Valve prosthesis can also effectively treat aortic regurgitation., while other TAVR products on the market are indicated only for “stenosis.”

The unique design of the J-Valve prosthesis allows the native valve leaflets to be sandwiched between the positioning elements and the stent frame after deployment. This clamping configuration provides additional anchoring support, reducing reliance on radial force alone. This approach not only prevents native leaflet obstruction of the coronary ostia but also addresses the international challenge of performing TAVR in patients with pure regurgitation and non-calcified valves.

Common access routes for TAVR procedures are further divided into transfemoral (TF) and transapical (TA) approaches. In 2017,Jiecheng’s “J-Valve TA Transapical Interventional Heart Valve Replacement System” has received NMPA approval, remaining the only approved interventional valve product capable of simultaneously treating both severe aortic stenosis and aortic regurgitation.As a result, Genesis became one of the earliest companies in China to develop TAVR products, and together with Qiming Medical, Peijia Medical, and MicroPort CardioFlow, it is hailed as one of the “Four Little Dragons” of the TAVR industry.

Shortly after the market launch of the J-Valve TA, Genesis initiated the research and development of the J-Valve TF transcatheter interventional biological heart valve replacement system. This product utilizes a transfemoral approach and can be performed in a catheterization laboratory, attracting widespread attention from the medical community both domestically and internationally.

In 2018, the J-Valve TF transcatheter interventional biological heart valve successfully completed human implantations in Canada and the United States. Subsequently, due to its superior clinical efficacy, the product has been approved through special access pathways by the U.S. FDA and Health Canada, saving more than 20 patients in both countries. Among these patients, some suffered from severe aortic regurgitation, while others had aortic stenosis that could not be treated with existing valve prostheses.

To date, leveraging its high-barrier technological advantages, Jiecheng has developed a one-stop TAVR solution for aortic valve disease via both TA and TF approaches.

According to statistics, there were 36.3 million patients with heart valve disease in China in 2019, and the number is projected to increase to 40.2 million by 2025, with a market size exceeding RMB 100 billion.

Based on heart valve anatomy, the therapeutic market can be preliminarily segmented into aortic, mitral, and tricuspid valves. Among these, transcatheter aortic valve replacement (TAVR) represents the primary battlefield.

Given that TAVR technology encompasses both valve-related and delivery system-related technologies, it presents extremely high barriers to entry. Consequently, the major overseas players are limited to four industry giants: Edwards, Medtronic, Abbott, and Boston Scientific.

In the Chinese TAVR market, due to racial and morphological differences between Chinese patients and those in Europe and the United States, Abbott and Boston Scientific currently have no TAVR products launched in China. Edwards Lifesciences has only one product available in the Chinese market, while Medtronic’s product was just approved by the China National Medical Products Administration (NMPA) at the end of 2021.

The domestic TAVR market currently features a “4 domestic + 2 imported” landscape—comprising four local medical device companies (Venus Medtech, Jiecheng Medical, MicroPort CardioFlow, and Peijia Medical) and two foreign giants (Edwards Lifesciences and Medtronic).

As of the market close on February 3, 2022. Data source: Tiger Brokers

VenusA-Valve from Venus MedTech, J-Valve from Jiancheng Medical, VitaFlow from MicroPort CardioFlow, TaurusOne from Peijia Medical, and SAPIEN 3 from Edwards Lifesciences are the five TAVR products currently successfully commercialized in China. Medtronic’s CoreValve Evolut PRO has recently obtained NMPA approval, with commercialization yet to be launched. It is worth noting, however, that these six products differ significantly in many aspects.

First,From the perspective of indications, only Jiecheng’s J-Valve can simultaneously cover both severe aortic stenosis and aortic regurgitation., and it does not require sufficient calcification of the patient’s aortic valve. In contrast, other TAVR products are indicated only for symptomatic patients with severe calcific aortic stenosis and are contraindicated in cases of aortic regurgitation.

In terms of valve expansion mechanism, only Edwards Lifesciences’ SAPIEN 3 is a balloon-expandable valve, while the other five products are self-expanding valves. Regarding interventional procedural approaches, although balloon-expandable valves offer greater radial support force and thus certain clinical advantages,The Jiecheng J-Valve also adopts a short stent, and its unique “positioning element” design can nearly perfectly address the issue of radial force.

Regarding access routes, among the TAVR products currently approved by the NMPA, Jiecheng’s J-Valve utilizes a transapical approach, while all others employ a transfemoral approach.

However, data from the “Annual Report of the Structural Heart Disease Group of the Chinese Medical Doctor Association” show that in 2021, the number of TAVR procedures performed in China (including transfemoral and transapical approaches, but excluding those conducted as part of clinical studies) exceeded 6,500, with a penetration rate of less than 1%.Jiecheng’s transfemoral transcatheter aortic valve replacement system technology is fully mature and is about to enter the clinical trial phase,Should it gain approval in the future, the domestic TAVR market will witness even greater disruption.

In addition to the aforementioned factors, physicians also place significant emphasis on key outcomes when selecting TAVR devices, including the incidence of paravalvular leak, pacemaker implantation rate, and valve durability. In July 2021, Jiecheng released its five-year follow-up data:The 5-year cardiac mortality rate for J-Valve was only 15.2%, the pacemaker implantation rate was only 7.4%, and the structural valve deterioration rate was only 3.7%.This set of data is at the forefront both domestically and internationally.

Furthermore, the J-Valve features a short stent frame, expanding the applicability of TAVR to patients with coronary ostium heights as low as 2 mm (whereas other TAVR systems require heights of 10–15 mm or more), thereby significantly reducing the risk of coronary obstruction. The optimized valve frame structure preserves coronary access, facilitating future valve-in-valve implantation for patients.

From the perspective of public listings, although Venus Medtech, VitaFlow Medical, and Peijia Medical have gone public in succession in China, their financial reports indicate that all these companies are operating at a loss. Their stock prices have all fallen below their IPO offering prices, with market capitalizations shrinking by 70% in less than a year.

The underlying reason is that TAVR product sales for Venus Medtech, VitaFlow, and Peijia Medical have fallen short of expectations. High pricing has hindered rapid market penetration, leaving the industry far from the stage of rapid volume growth. Furthermore, the domestic TAVR landscape is becoming increasingly competitive. In the future, more than 10 Chinese companies are expected to commercialize TAVR products in the Chinese market (with an additional 2–3 overseas companies potentially completing product registration and launch in China).

In contrast to the grim landscape in China’s TAVR market, which is characterized by low penetration and intense competition, the global market—particularly in Europe and the United States—boasts mature technological systems, high levels of market education, and a substantial market size. Therefore, for Chinese TAVR companies,Expanding into the global market is a way to break through.

However, due to the high technical barriers associated with TAVR, it remains a critical bottleneck product in most countries. Consequently, the pinnacle of this market is characterized by limited competition and attractive prospects—currently, the globally commercialized TAVR systems are predominantly supplied by Edwards Lifesciences and Medtronic, which together command a 90% market share.

According to Frost & Sullivan data, the global TAVR market has experienced rapid growth, increasing from $2 billion in 2015 to $4.8 billion in 2019, and is projected to continue expanding, reaching $10 billion by 2025.

VCBeat, in its special report “How Much Is the TAVR Sector Really Worth? Valuation Report on the TAVR Sector,” stated that “the overseas market is a hidden bonus, with the global market rapidly expanding to over 200,000 procedures annually, representing a $6.5 billion market.” If domestic brands could capture 5%–10% of this market, they would achieve an additional RMB 2–4 billion in global sales. However,Chinese Enterprises Face a Major Disadvantage in Entering the International TAVR Market—Lack of Global Patent Layout.

In this regard, Jiecheng is a low-key powerhouse. Since its inception, Jiecheng has targeted the global market for interventional cardiac valves. Currently,Jiecheng holds over 200 international patents and patent applications, of which more than 100 patents have been granted., established a robust global intellectual property protection system.

In 2018, with special authorization from the U.S. FDA and Health Canada, physicians in both countries successfully performed minimally invasive heart valve implantation procedures on two local patients each, using the Chinese J-Valve transcatheter heart valve system for the first time.

In addition to holding global intellectual property rights, the J-Valve prosthesis can simultaneously treat both aortic stenosis and aortic regurgitation.Indications Reach Areas Not Covered by Edwards and Medtronic, possesses differentiated competitive advantages. If it can secure FDA approval and successfully enter the U.S. market, it is poised to gradually leverage J-Valve to penetrate the global TAVR market.

To date, nearly ten leading international physicians have highly praised the J-Valve, including Professor Dean Kereiakes of Christ Hospital in the United States and Professor John Webb of St. Paul’s Hospital at the University of British Columbia in Canada, among others.

In China, J-Valve’s partner hospitals include nearly 200 institutions such as Fuwai Hospital of the Chinese Academy of Medical Sciences, Beijing Anzhen Hospital affiliated with Capital Medical University, West China Hospital of Sichuan University, the Second Affiliated Hospital of Zhejiang University School of Medicine, and Zhongshan Hospital affiliated with Fudan University. The annual number of TAVR implantations is approximately 1,000 cases. The cumulative number of implantations in mainland China stands at 3,000, with 10 cases in Taiwan, China, and 20 cases in Hong Kong, China.

According to Genesis,Following the acquisition, Genesis will establish a Structural Heart Disease Division, with Zhang Ji, founder of Jiecheng Medical, serving as Chief Technology Officer (CTO) of the division and President of Jiecheng.

Genesis boasts strong capabilities in building a global innovation platform and expanding market resources, while Jiecheng stands out in product research and development; their merger represents a powerful alliance between two industry leaders.

For Genesis, the acquisition of Jiecheng not only expands its business scope but also helps propel domestic innovative products into broader markets. With years of deep expertise and a rich reserve of innovative technologies, Jiecheng’s core R&D team is poised to accelerate its expansion in both domestic and international markets, bolstered by Genesis’s resources.