Noom, Ro, and Commure: The Playbook Behind Record-Breaking Digital Health Fundraising

Noom

Health Service Provider

Commure

Healthcare System Developer

Record-breaking total investment and financing amounts, coupled with a doubling in the number of transactions, made 2021 the most vibrant year for the U.S. digital health market in nearly a decade (for details, see VCBeat’s previous report, “$29.1 Billion! The US Digital Health Market in 2021》). The U.S. digital health market raised a total of $29.1 billion in financing in 2021, representing a year-over-year increase of more than 95%, with the primary growth driver being 88 large financing rounds each exceeding $100 million.

Among them, a weight and stress management service provider (Noom), a digital clinic (Ro), and an informatics platform (Commure) drew the most attention, emerging as the leaders in large-scale financing for the year with single-round funding amounts of $540 million, $500 million, and $500 million, respectively. In fact, such scales were not only outstanding in 2021 but also ranked among the top five largest single-round financings in the U.S. digital health sector over the past decade.

The surge in large-scale financing driving overall funding growth is not unique to the United States. According to the "2021 Global Healthcare Industry Capital Report" released by VCBeat and Eggshell Research Institute, there were an unprecedented 362 global healthcare deals exceeding $100 million in 2021, representing a year-on-year increase of approximately 76% and surpassing the previous record of 205 deals set in 2020. The total funding raised by these 362 companies exceeded $64.932 billion, indicating that nearly half of all capital invested in the global healthcare industry was concentrated in less than 10% of enterprises. Notably, nearly 78% of these transactions occurred in the biopharmaceutical and digital health sectors. In China, the digital health segment completed 188 financing rounds in 2021, totaling RMB 34.196 billion. This performance ranked third among all healthcare subsectors for the year, trailing behind biopharmaceuticals and medical devices & consumables. However, digital health companies dominated the top ten list of healthcare financing amounts in China with a significant margin. The three leading companies—Medlinker, Yuanxin Medical, and WeDoctor—raised funding amounts comparable to those of their U.S. counterparts.

VCBeat and VBInsight’s “2021 Global Healthcare Industry Capital Report”

US-based companies Noom, Ro, and Commure were all established before 2018. In terms of financing, Noom, with over a decade of history, has progressed beyond its Series F round and is poised for an IPO this year, while the relatively younger Ro and Commure have both completed their Series D funding rounds. They respectively represent three dimensions of the digital health market: disease prevention, disease treatment, and healthcare data interoperability, demonstrating relative maturity in their respective niche sectors. What core competencies have enabled Noom, Ro, and Commure to achieve the highest annual transaction volumes? What are the differences between China and other countries in these three areas? VCBeat attempts to outline the following analysis.

For Noom co-founder Saeju Jeong, the quest has long been for an ultimate answer: how to transform healthcare into true “health care” rather than merely “sick care.” This was also the question left for Jeong to ponder by his father, a physician who passed away at the age of 51 from advanced gastric cancer. Noom generated $400 million in revenue in 2020 and secured a $540 million Series F funding round in May 2021, led by Silver Lake. According to PitchBook, this marked the largest venture capital deal ever in the global mobile and digital health sector. Yet its success was far from overnight; it is the story of a 13-year journey of repeated exploration and validation of its business model.

Noom's Historical Financing

Noom’s core business is weight management. However, unlike most companies in the market that primarily rely on exercise, medication, and dieting to achieve weight control, Noom has taken a highly unique path—psychology—after more than a decade of continuous product refinement.

Noom was founded in early 2007 under the name WorkSmart Labs. Co-founders Saeju Jeong and Artem Petakov developed a prototype for the company’s first product: a computer touchscreen mounted on stationary bikes in gyms. As users pedaled, the screen displayed an animation of them riding a rainbow and catching butterflies, making exercise more engaging. However, since gym members represented only a small fraction of potential users, this business model failed to deliver sustainable profitability. Jeong and Petakov began exploring new product prototypes. With the launch of iOS in 2007 and Android in 2008, they recognized the emerging market for mobile applications and subsequently released CardioTrainer, a running and cycling tracking app built for the Android platform. Within eight months, it became one of the most downloaded fitness apps on the Android Market. At that point, the founders faced several commercial challenges: users were unwilling to pay for premium versions, engagement was inconsistent, and usage tended to be passive. However, through analysis of user data, Jeong and Petakov made a key discovery: the majority of users treated the app primarily as a pedometer rather than a tool for tracking runs. Further user research revealed that many individuals suffered from underlying health conditions and needed to lose weight; their reliance on step counting stemmed from their inability to run. This insight paved the way for Noom’s subsequent growth and provided Jeong with an answer to a question left by his father: weight loss can serve as a form of preventive care in which people actively participate, and achieving a healthy weight is a fundamental driver of transformative, long-term health outcomes.

In 2010, Noom launched Calorific, a color-coded calorie-counting app, marking the company’s first step in pivoting its business toward weight loss. However, Noom’s ultimate mission was not merely to help people lose weight, but to help them sustain a healthy state. From this perspective, the effects of any popular weight-control regimen—whether based on diet, nutrition, medication, or exercise—tend to rebound quickly after goals are achieved. In the field of psychology, it is widely recognized that cognitive behavioral therapy (CBT) can help individuals proactively understand and manage thoughts and behaviors that may interfere with their weight-loss efforts, thereby enabling self-management of body weight. Although its potential as a primary approach to weight loss has often been overlooked, CBT may offer a more sustainable path to long-term health. Consequently, in 2011, Noom underwent its first substantial product iteration, launching the Noom Weight Loss Coach, which featured AI-driven coaching grounded in psychological principles and cognitive behavioral therapy. At this stage, science and technology appeared to form an ideal synergy, yet the actual results were underwhelming. The key issue lay in the positioning of the AI technology: when losing weight, people seek empathetic, emotionally engaged human coaching and interaction, rather than interfaces with machines. In 2014, Andreas Michaelides, a clinician from New York, joined Noom as Chief Psychologist, bringing additional coaches into the company. It was not until the launch of Noom Healthy Weight in 2017 that Noom finally identified its most accurate market positioning. In the current version, Noom’s weight-management program consists of three core components: tracking dietary calorie intake, participating in psychology-based behavior-change courses, and maintaining ongoing communication with coaches.

Psychology and behavior change form the foundation for a series of transformations. Noom leverages psychology and cognitive behavioral therapy, focusing extensively on reshaping individuals’ thought processes and mental patterns to help them modify behaviors that contribute to weight gain, such as binge eating, poor food choices, sedentary lifestyles, inability to adhere to dietary regimens, and maladaptive responses to stress. As individuals begin to examine the psychological underpinnings of these behaviors, they develop greater self-awareness in weight management and cultivate a healthier relationship with food.

In tracking food calories, Noom sets daily calorie intake targets for users based on the information provided during registration and their health goals. The Noom system color-codes foods according to their caloric density. However, unlike other products that focus on calorie restriction to achieve weight loss, Noom only informs users about their nutrient distribution through dietary logs, without prescribing what they should or should not eat each day. All motivation for dietary restrictions stems from the users themselves. This is where psychology and cognitive behavioral therapy come into play: as users begin to examine their own behaviors, changes in their eating habits no longer depend on a paradigm dictated by any specific product. For individuals with obesity or prediabetes, Noom may directly recommend participation in its Diabetes Prevention Program—the first virtual type 2 diabetes prevention provider recognized by the U.S. Centers for Disease Control and Prevention (CDC).

Coaching is equally important. Users are matched with coaches on the Noom platform, who provide guidance and support to help them achieve their goals throughout their health journey. These coaches can view users’ dietary and exercise data, offering personalized one-on-one coaching, support, and encouragement based on this information. Additionally, coaches initiate group chats to connect users with others willing to share weight-loss tips and tricks for collaborative discussion. All coaches are trained by Noom and hold at least a bachelor’s degree in a health-related field, with four or more years of relevant education.

Following Noom’s shift from AI coaching to human coaching, AI has not disappeared from its underlying framework. It is used to deliver personalized quizzes, workouts, and reading materials tailored to each user’s specific circumstances, while also optimizing coach allocation to eliminate repetitive tasks and maximize meaningful communication between users and coaches.

After validating its business logic, Noom’s next step was to withstand market scrutiny. According to Forbes, Noom generated revenues of $12 million, $61 million, and $237 million in 2017, 2018, and 2019, respectively, with app downloads surpassing 50 million in 2019. In 2020, Noom’s weight management business reached new heights amid the COVID-19 pandemic—according to a survey by the American Psychological Association, approximately 42% of U.S. adults gained unwanted weight during the first year of the pandemic—driving annual revenue to $400 million. The pandemic not only contributed to weight gain but also intensified the urgent need for addressing psychological issues such as anxiety and stress. Following user research, Noom launched its stress management service, Noom Mood, in October 2021.

Both China and the United States have large populations of obese individuals, and there is no shortage of weight loss and fitness programs available on the market. However, very few companies in either market have managed to find a resonance point between weight loss and psychology. When Noom emerged, it inevitably attracted capital attention as an innovator. Meanwhile, its technology foundation rooted in psychology means that Noom can extend this approach to other fields. This potential is also recognized by investors. “Noom’s combination of technology and human coaching is compelling,” said Ravi Gupta, who led Sequoia Capital’s Series F investment in Noom. “In our experience, the best AI companies are not about artificial intelligence, but augmented intelligence. Moreover, in Noom’s case, their success in weight loss has the potential to be applied elsewhere. We believe it is evolving into a digital health platform, rather than just a point solution.”

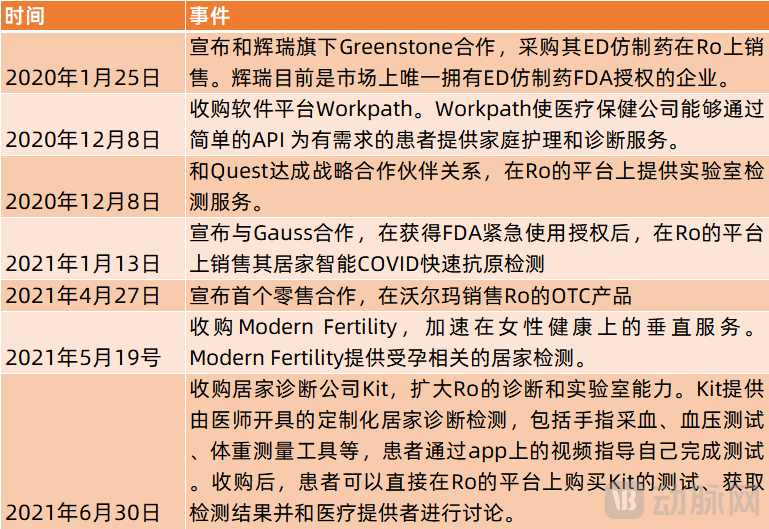

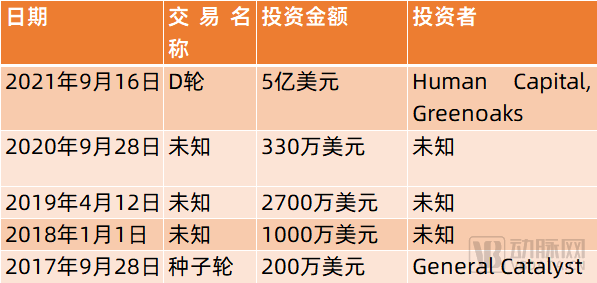

Noom has driven innovation in healthcare through preventive care, while Ro’s success lies in building a large, patient-centric digital clinic using a direct-to-consumer (D2C) model. Ro has raised a total of $876 million in funding to date.

Ro's Historical Financing

Ro was founded in 2017, starting as a digital health clinic for men. It currently offers telemedicine services for more than 20 categories of conditions, covering multiple verticals such as Roman (men’s health), Rory (women’s health), Zero (smoking cessation), and Ro Mind (mental health). The company has also built its own pharmacy, Ro Pharmacy, and an electronic medical record (EMR) platform. Ro is committed to creating a “Digital Clinic-as-a-Service” model, believing that U.S. healthcare is shifting toward a digital-first paradigm. Online channels will become the first step for patients to determine whether they can access safe, high-quality care remotely; if telemedicine cannot meet their needs, patients can then seek in-person care.

To win over investors, Ro has achieved the following in its business operations:

1. Many telehealth companies tend to rely on employers and insurance providers as their primary, or even exclusive, service channels. For individuals, however, this effectively cedes the choice and decision-making power over reducing their own medical expenses to third parties. Ro has chosen to take the opposite approach by accepting only direct-to-consumer payments, offering lower and more transparent pricing for telehealth services and medications to directly reduce healthcare spending. On the clinical side, patients pay just $15 per visit to receive remote consultations and medical advice from physicians, who can issue prescriptions when deemed necessary. On the pharmacy side, Ro offers more than 500 generic medication options for a wide range of common conditions, with refill cycles ranging from one to twelve months. These medications are priced lower than typical insurance copays and can be delivered within two days.

2. Bridged the gap in medical resources with primary care deserts in the United States (areas lacking sufficient physicians to meet local demand). According to a report released by the Association of American Medical Colleges (AAMC) in June 2020, the U.S. will face a shortage of nearly 139,000 physicians across all specialties and practice types by 2032. The shortfall in primary care physicians is estimated to be between 21,400 and 55,200. Based on an analysis by Ro, there were approximately 1,884 primary care deserts in the U.S. in 2020, and Ro achieved coverage in 95% of rural deserts and 98% of urban deserts.

3. Continuously enhance business capabilities through collaborations, acquisitions, and other activities. Over the past two years, Ro has completed four collaborations and three acquisitions, as summarized by VCBeat below.

Notably, the acquisitions of Workpath and Kit have equipped Ro with the capability to integrate remote care services, in-person face-to-face care services, and related data. Laboratory testing typically underpins 70% of medical care decisions. Kit’s at-home testing capabilities complement Workpath’s home care services API, enabling both self-administered at-home tests and provider-conducted home visits to be seamlessly managed through Ro’s platform, thereby facilitating the efficient collection of patients’ clinical data.

As technological capabilities advance, virtual care is increasingly regarded as a critical component of healthcare. An article by McKinsey points out that telehealth utilization has currently stabilized at 38 times its pre-pandemic level, and future models of virtual care are likely to evolve toward optimized hybrid service models that integrate both virtual and in-person care. Evidently, Ro’s current strategy aligns precisely with this approach, strengthening both fronts simultaneously.

In 2021, digital health maintained a positive growth trajectory both in China and globally. In China, the digital health sector even dominated the top ten largest financing deals in the healthcare industry by a significant margin. The two leading companies, Medlinker and Yuanxin Medical, are nearly on par with Ro in providing remote consultation and prescription services, though they lag slightly in their online/offline hybrid care models. The home testing market in the United States is relatively mature, with services already covering blood tests, hormone assays, and monitoring of various chronic disease indicators. In contrast, this market in China is still in its early stages, and there are limited home testing products with consumer-oriented attributes that have obtained certification from the National Medical Products Administration (NMPA). If Chinese telemedicine companies can expand into home testing and the associated offline services, they may be able to bridge the “last mile” gap, enabling seamless patient connectivity for the medical management of certain diseases.

In 2021, three forces were reshaping the U.S. digital health market, one of which was infrastructure improvements centered on informatization.

The United States began its healthcare information technology development in the 1970s. Historically, the U.S. healthcare system has been fragmented, making it nearly impossible for stakeholders to share data for coordinated care, billing, or research purposes. Healthcare organizations have had to build and manage their own technology infrastructure from scratch or adapt to existing electronic medical record (EMR) models.

The enactment of the HITECH Act in 2009 had a landmark impact on the development of Electronic Health Record (EHR) systems and healthcare payment reform in the United States. Currently, healthcare informatization in the U.S. has evolved from departmental applications and financial system implementations, through clinical information infrastructure construction and hospital-wide EHR system integration, to the stage of healthcare information interoperability.

The 21st Century Cures Act, passed at the end of 2016, further advanced medical information interoperability by requiring developers of health IT services to provide APIs. This mandate aims to eliminate procedural barriers in the access, exchange, and use of medical information and to complete interoperability testing under real-world conditions. Due to privacy concerns and restrictions imposed by the HIPAA regulations, the healthcare industry has lagged behind most other sectors in advancing connectivity. The 21st Century Cures Act standardizes medical information interoperability, mandates that health information be disclosed and shareable as required by law, and imposes penalties on entities engaged in information blocking. The Office of the National Coordinator for Health Information Technology (ONC) has set a goal to establish nationwide medical information interoperability by 2024. It can be said that the United States has entered the final sprint toward achieving full medical information interoperability.

Commure emerged in 2017, starting with the development of healthcare IT software services themselves, aiming to use open technology to address the information silo effect arising during the evolution of healthcare informatization. Commure’s founder, Hemant Taneja, is an executive partner at the investment firm General Catalyst and also co-founded Livongo, a well-known digital chronic disease management company. In February 2020, Commure launched a full-stack developer platform based on the FHIR standard, offering REST APIs, SDKs, and cloud services that enable developers to build required applications more quickly and securely without having to start from the underlying infrastructure.

Commure's Historical Financing

Moreover, companies and investors represented by Commure and its seed-round investor Catalyst have created a new model for cross-sector collaboration.

On October 18, 2021, General Catalyst and Jefferson Health, a multi-state healthcare system in the United States, announced the establishment of an innovative partnership known as “Health Assurance.” This network comprises technology innovation companies dedicated to delivering best-in-class products within their respective domains, working collaboratively to help healthcare systems undergo self-transformation. Commure is also a member of this network. This collaborative model reimagines the role of venture capital firms, shifting them from being merely sources of funding for startups to actively engaging in how these companies are built, nurtured, and interconnected.

This collaborative approach will address the significant challenge facing healthcare systems like Jefferson Health: the proliferation of isolated, fragmented technical solutions. Each healthcare system has its own market region and unique needs, leading it to develop proprietary technical processes and systems. However, the absence of a universal standard or delivery platform, coupled with hundreds of technology solutions vying for the ever-growing IT budgets of hospital systems, has resulted in further fragmentation of healthcare informatics.

In contrast, China’s healthcare informatization initiative began in 2009. The release of the “Opinions on Deepening the Reform of the Medical and Healthcare System” (hereinafter referred to as the “Opinions”) by the Central Committee of the Communist Party of China and the State Council marked the launch of a new round of healthcare reforms. The “Opinions” called for “vigorously advancing the informatization of medical and healthcare services” and “establishing practical and shared medical and healthcare information systems.” Currently, China is still in a phase that emphasizes the establishment and promotion of enterprise-wide electronic medical records (EMRs). A report published by Orient Securities in 2019 pointed out that there were as many as 500–600 domestic healthcare IT companies, with the market shares of the five major listed healthcare IT firms—Winning Health, B-Soft, Thinkive Medical, Heren Technology, and Jiuyuan Yinhai—ranging from 0.6% to 3%, indicating a highly fragmented market overall. This suggests that, from the perspective of interoperability, China’s healthcare informatization landscape faces an even more fragmented environment. Leveraging open standards to accelerate innovation in informational interoperability will require both enterprises and investors to adopt more forward-thinking strategies and allow sufficient time for strategic positioning.

The digital health sector is a red ocean. While it is not difficult to find a niche to dive into, becoming a true market leader is far from easy. Over its 13 years of development, Noom has repeatedly faced pressure from investors to accelerate commercial monetization, yet it has remained true to its original mission and found the positioning best suited to itself. Meanwhile, Ro and Commure have set their sights on the other side of the horizon, riding the next wave of the era. As competition intensifies, entrepreneurs must continuously seek sustainable competitive models to truly dance on the crest of the wave.