Multiple Companies Enter with Innovative Technologies, Challenging the Duopoly in China's Radiopharmaceutical Sector

In 1901, Henri Alexandre Danlos and Eugene Bloch used radium to treat cutaneous tuberculosis. In 1905, Marie Curie developed radium needles and performed the first case of brachytherapy using radioactive isotopes, marking the beginning of the application of radiopharmaceuticals in the medical field.

For over a century, radiopharmaceuticals have played a pivotal role, occupying an irreplaceable position in the global disease treatment market. According to data from medraysintell, the global radiopharmaceutical market was valued at approximately USD 6 billion in 2019, with diagnostic agents accounting for the majority of the market. The increasing number of therapeutic radiopharmaceuticals reaching the market is expected to drive the global radiopharmaceutical market to around USD 30 billion by 2030.

In recent years, with increasing public acceptance of nuclear medicine, technological advancements, and active R&D efforts by enterprises, China’s radiopharmaceutical industry has developed rapidly, drawing significant attention to this once-niche sector.

According to Frost & Sullivan data, the market size of nuclear medicine in China was RMB 4 billion in 2018, with a growth rate of 20%. With the continuous improvement of domestic nuclear medicine research, the Chinese nuclear medicine market is expected to continue expanding, and sales are projected to exceed RMB 20 billion by 2028.

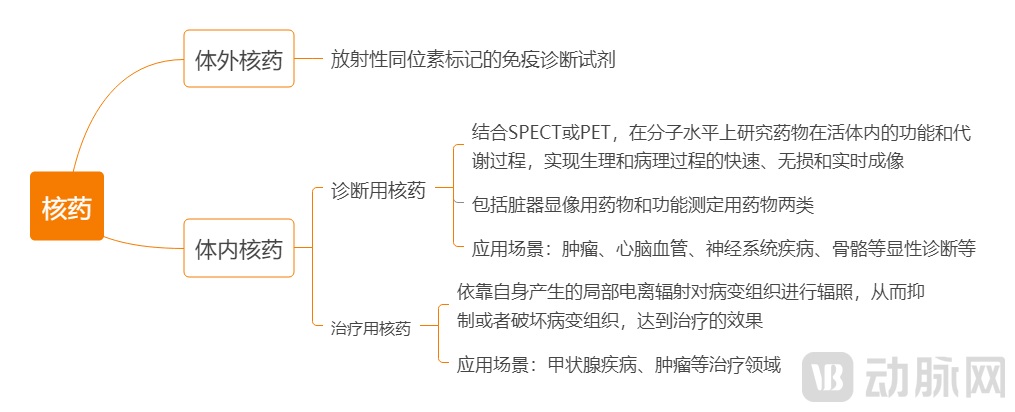

Nuclear medicine drugs (also known as radiopharmaceuticals) are a class of special preparations containing radioactive isotopes, used for medical diagnosis and treatment. According to their applications in clinical nuclear medicine, they can be divided into in vitro nuclear medicine drugs and in vivo nuclear medicine drugs.

Among them, in vitro radiopharmaceuticals mainly refer to radioisotope-labeled immunodiagnostic reagents, while in vivo radiopharmaceuticals are further divided intoDiagnostic RadiopharmaceuticalsandTherapeutic Radiopharmaceuticals。

Diagnostic radiopharmaceuticals comprise two categories: agents for organ imaging and agents for functional assessment. In conjunction with SPECT or PET, they enable the study of drug function and metabolic processes in vivo at the molecular level, facilitating rapid, non-invasive, and real-time imaging of physiological and pathological processes, thereby providing a means for true early diagnosis and timely treatment.

Therapeutic radiopharmaceuticals are a class of in vivo radiopharmaceuticals that can highly selectively accumulate in diseased tissues, generating localized ionizing radiation-induced biological effects to inhibit or destroy the diseased tissues, thereby exerting therapeutic effects. They are used for the treatment of thyroid diseases, tumor therapy, targeted therapy, and other applications.

Classification of Radiopharmaceuticals (Compiled from Public Information)

The overseas radiopharmaceutical market started early, with a history of over 100 years. In 1951, the FDA approved the first radiopharmaceutical, iodine [131[I], including it in the medication regimen for thyroid patients. Currently, several leading radiopharmaceutical companies have emerged globally, such as Novartis, GE, Cardinal Health, UPPI, RadioMedix, and Lantheus. The U.S. FDA has approved more than 50 radiopharmaceuticals, with star products including Xofigo for the treatment of prostate cancer and Lutathera, a radiolabeled somatostatin analog.

China initiated the development of radioactive isotopes in 1956. The nuclear medicine market started relatively late, resulting in a significant gap compared with European and American countries. The 2019 publication “Current Status and Prospects of Radiopharmaceutical Preparation in China” pointed out that China lags considerably behind developed countries in Europe and America, both in terms of the variety of medical radionuclides and the number of approved products. In 2017, global sales of radiopharmaceuticals reached USD 4.5 billion, with the United States accounting for 38%, Europe for 24%, and China for less than 8%.

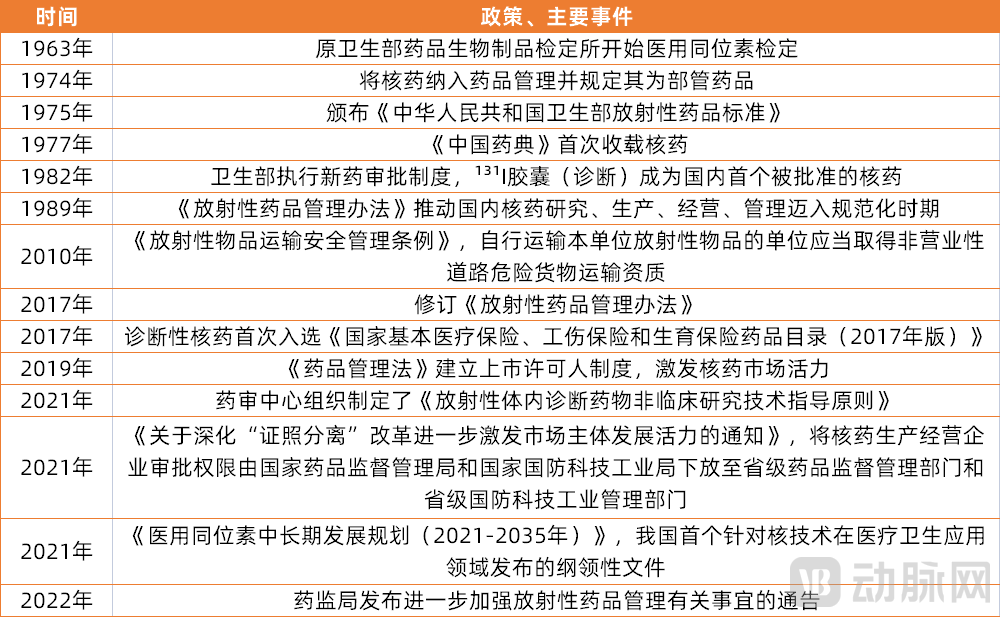

Since the inclusion of radiopharmaceuticals under drug administration in 1974, China has successively issued multiple policy documents to promote the standardized and rapid development of radiopharmaceuticals.

China’s Nuclear Medicine Industry Policies (Compiled from Public Information)

In 1989, China promulgated the Administrative Measures for Radiopharmaceuticals, ushering in a standardized era for the research, production, application, and management of nuclear medicines domestically. Nearly 30 years later, in 2017, China revised the Administrative Measures for Radiopharmaceuticals, updating institutional names and the scope of administration, and consolidating regulatory responsibilities under the drug regulatory authorities.

The revised Drug Administration Law, implemented in August 2019, established the Marketing Authorization Holder (MAH) system, adopting a management model that separates marketing authorization from manufacturing licensure. Under this framework, the MAH bears responsibility for drug safety throughout the entire product lifecycle, while manufacturers are accountable for the production process, thereby significantly stimulating vitality in the radiopharmaceutical market.

In 2021, the China Atomic Energy Authority, in conjunction with the Ministry of Science and Technology and seven other ministries, jointly issued"Medium- and Long-Term Development Plan for Medical Isotopes (2021-2035)", this isChina’s First Guideline Document on the Application of Nuclear Technology in Healthcare and Medical Services, pointing out that by 2025, breakthroughs will be achieved in a number of key core technologies for the development of medical isotopes; the construction of one to two dedicated production reactors for medical isotopes will be initiated at an appropriate time, thereby achieving stable and independent supply of commonly used medical isotopes. By 2035, efforts will be actively made to promote the global expansion of China’s medical isotope industry.

In January 2022, the National Medical Products Administration issued a Notice on Further Strengthening the Management of Radiopharmaceuticals, stating that quality testing of three consecutive batches of samples for immediate-labeling radiopharmaceuticals shall be conducted after obtaining the Production License; for drug products containing short-half-life radionuclides, release from the factory may proceed concurrently with testing.

Overall, policy support for the radiopharmaceutical industry has been increasing year by year, helping to address the shortcomings in the development of China’s radiopharmaceutical sector. Zhang Jianhua, Deputy Director of the China Atomic Energy Authority, stated in an interview that by the end of 2020, the total number of nuclear medicine examinations in China had exceeded 2.5 million, representing an increase of nearly one-fifth compared with 2017; moreover, the radiopharmaceutical market had achieved a growth rate of over 15% in the preceding five years.

However, at the level of policy guidance and standardization, there are stillThe approval process for innovative radiopharmaceuticals is relatively slow, as China’s regulatory framework for radiopharmaceuticals has not yet been fully aligned with international standards, leading to discrepancies in requirements for research and development, regulatory submissions, and other aspects compared to overseas markets.. For example, after 2017, China only had diagnostic radiopharmaceutical myocardial perfusion imaging agents99mTc-Tetrofosmin and Therapeutic Iodine [131[I] Sodium iodide capsules have been approved; radioimmunoassay diagnostic reagents are classified as radiopharmaceuticals in China, but not in some European and American countries; Iodine-125 sealed seed sources are regulated as pharmaceuticals in China, whereas the United States regulates them as medical devices.

With technological advancements, diagnostic and therapeutic services related to radiopharmaceuticals have become increasingly complex, involving a growing variety of products and expanding usage volumes. There is an urgent need to improve relevant laws and regulations to better align with the requirements of radiopharmaceutical production, distribution, and application. Only by establishing a regulatory framework that ensures effective oversight of radioactive pharmaceuticals while accommodating practical realities in production and use can the rapid development of the radiopharmaceutical industry be promoted.

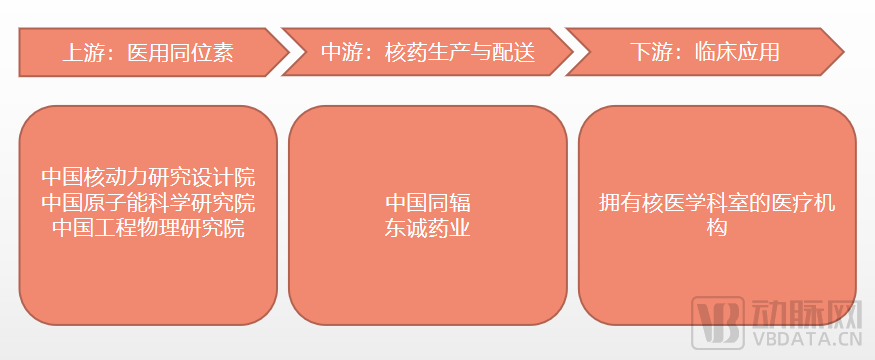

The nuclear medicine industry chain encompasses upstream raw materials (medical isotopes), midstream drug manufacturing and distribution, and downstream clinical applications.

Nuclear Medicine Industry Chain (Compiled from Public Information)

Upstream: Severe Import Monopoly of Medical Isotopes

Medical isotopes serve as raw materials for radiopharmaceuticals. There are four primary production methods: reactor irradiation, accelerator irradiation, isotope generator preparation, and extraction from high-level radioactive waste. Reactor irradiation is the most commonly used method, accounting for over 80% of medical isotope production.

Types of Medical Isotopes Include99mTc、125I、131I、14C、68Ga、177Lu、18F、90Y、89Sr, etc. Currently, there are five research reactors in China available for the preparation and production of medical isotopes; however, no dedicated commercial reactors are employed for the production of medical isotopes, and domestically produced131I and89Sr can only meet 20% of the domestic demand,177Lu can only meet 5% of domestic demand. The majority of high-volume medical isotopes produced via reactor irradiation are heavily reliant on countries such as Canada, the Netherlands, Belgium, and Australia, resulting in high costs, untimely supply, and risks of supply disruptions.

Unlike most industries, the import monopoly on medical isotopes is not due to technological limitations; in fact, several domestic nuclear industry research institutes have already established a solid technological foundation.The high cost of dedicated reactors is not the primary issue; rather, the insufficient demand for medical isotopes is the main reason.

The costs associated with reactor construction, production, and waste disposal are extremely high. Given the limited domestic demand from Chinese radiopharmaceutical companies, building a dedicated medical isotope reactor would inevitably lead to oversupply. Consequently, many domestic nuclear industry enterprises have demonstrated insufficient attention, enthusiasm, and investment in medical isotopes, resulting in an inadequate supply of commercially produced medical isotopes in China.

In this context, expanding into the global market to absorb excess capacity represents a viable strategic pathway. Beyond serving domestic enterprises, foreign reactors have also integrated into the global supply chain. Furthermore, some overseas companies have adopted a reactor leasing model, wherein businesses pay a fee to lease irradiation channels within reactors for production purposes.

As the market for radiopharmaceuticals expands, demand for medical isotopes rises, the international landscape becomes increasingly complex, and major foreign production reactors for medical isotopes successively reach the end of their service lives, the issue of import monopoly on medical isotopes has garnered significant attention. The Medium- and Long-Term Development Plan for Medical Isotopes (2021–2035) proposes thatBy 2025, initiate the construction of one to two medical isotope production reactors to achieve stable and independent supply of commonly used medical isotopes; by 2035, completely reverse the situation where the research, development, and production of medical isotopes are constrained by external dependencies.

In April 2020, the first batch of domestically produced reactor-irradiated Strontium-89 (Sr-89) medical isotopes, developed and manufactured by the Nuclear Power Institute of China, was officially delivered to Chengdu CNNC Gaotong Isotope Co., Ltd. This milestone marked a significant breakthrough in achieving domestic substitution of medical isotopes, successfully mastering the key technologies across the entire process chain, including Sr-89 R&D, reactor operation, irradiation, and product manufacturing.

In addition to the Nuclear Power Institute of China, the China Institute of Atomic Energy and the China Academy of Engineering Physics are also key players in the production of medical isotopes.

Data show that the annual demand for medical isotopes is growing at a rate of 5%–30%, and the total demand is projected to increase more than tenfold by 2030. Currently, domestic reactor production capacity remains very limited and is unable to meet the continuously rising market demand.

In the future, China needs toPrioritize research on the production of commonly used medical isotopes, upgrade and retrofit existing reactors to enhance automation, intelligence, and radiation resistance in high-radiation fields, and establish environmentally friendly, large-scale production lines.Efforts should also be made to encourage relevant enterprises to initiate the construction of dedicated reactors for medical isotopes., achieving self-sufficiency. Meanwhile, China still needs toOn Original Innovation Capabilities in Medical IsotopesMake efforts.

Pharmaceutical Production and Distribution: High Barriers to Entry, Resulting in a Duopoly

Given that radiopharmaceuticals involve radioactive isotopes, the safety barriers are exceptionally high in addition to technical thresholds. China imposes stringent administrative regulations on radiopharmaceutical companies.

According to relevant regulations, nuclear medicine manufacturers must obtain review and approval from the competent department of national defense science, technology, and industry under the State Council, followed by examination and approval by the drug regulatory authority under the State Council. Upon such approvals, the corresponding provincial-level drug regulatory authorities shall issue the “License for Manufacturing Radioactive Pharmaceuticals.” Nuclear medicine distributors must undergo examination by the drug regulatory authority under the State Council and obtain approval from the competent department of national defense science, technology, and industry under the State Council before they can be granted the “License for Distributing Radioactive Pharmaceuticals.” For both manufacturing and distribution enterprises, the validity period of the license is only five years, and a renewal application must be submitted prior to expiration.

Due to stringent regulations, China’s radiopharmaceutical market has failed to achieve full marketization. Currently, the major players in the market are almost exclusively state-backed enterprises, with China Isotope & Radiation Corporation and Dongcheng Pharmaceutical Group—two industry giants—dominating the majority of the market share.

China Isotope & Radiation Corporation was listed in Hong Kong in 2018, with a market capitalization approaching HK$10 billion. It operates seven major business segments: radiopharmaceuticals, nuclear medicine equipment, radioactive sources, radionuclide production, medical diagnostics, irradiation applications, and import-export trade. Its listed products include iodine [125I] Sealed Seed Sources, Strontium Chloride [89Sr], Iodine [131I] Oral solution, flu[18F]Deoxyglucose Injection, Technetium [99mTc]Tc-labeled injection, urea [C-14] capsule, urea [C-13] capsule.

In 2020, China Isotope & Radiation Corporation reported full-year revenue of RMB 4.274 billion, a year-on-year increase of 7.15%, and net profit attributable to shareholders of the parent company of RMB 214 million, a year-on-year decrease of 35.09%. In terms of revenue structure, pharmaceuticals accounted for 69.7%, radioactive sources for 10.6%, irradiation services for 2.4%, radiotherapy equipment and related services for 5.4%, and medical laboratory testing services and other businesses for 11.9%.

Dongcheng Pharmaceutical was listed on the Shenzhen Stock Exchange in 2012, with a market capitalization exceeding RMB 12 billion. Its marketed products include Technetium [99Tc] Methylene Diphosphonate Injection (the company's exclusive product), Technetium [99mTc]Tc-labeled imaging agents, fluorine[18F] Deoxyglucose Injection, Iodine [131I] Oral solution, iodine [125I] Sealed seed sources, carbon [14C] Urea Capsules.

In 2020, Dongcheng Pharmaceutical achieved a full-year revenue of RMB 3.419 billion, representing a year-on-year increase of 14.24%. The net profit attributable to shareholders of the parent company was RMB 418 million, up by 170.02% year on year. In terms of revenue structure, active pharmaceutical ingredient (API)-related products accounted for 50.48%, formulated products for 18.61%, radiopharmaceutical products for 27.21%, and other businesses for 3.7%.

Furthermore, unlike conventional pharmaceuticals, radiopharmaceuticals have short half-lives, with some lasting only a few hours, making them unsuitable for advance mass production and long-distance transportation.Relying on nuclear pharmacies or compounding centers for timely production and distribution,Therefore, radiopharmaceutical developers and manufacturers also assume the responsibilities of distributors. Furthermore, for certain drugs with extremely short half-lives, there is a phenomenon of medical institutions producing radiopharmaceuticals in-house.

The construction standards for radiopharmacies are stringent, with a lengthy approval process and an investment requirement of approximately RMB 50 million. It is understood that environmental impact assessment and construction take one and a half years, while obtaining the necessary licenses requires another one and a half years, creating significant barriers to entry. China Isotope & Radiation Corporation operates 17 radiopharmacies, primarily focused on technetium-labeled products, with eight facilities handling fluorine-labeled products. Dongcheng Pharmaceutical has 14 radiopharmacies, all dedicated to technetium-labeled products.

Currently, both China Isotope & Radiation Corporation and Dongcheng Pharmaceutical are accelerating their deployment of nuclear pharmacies. In the future, as the “tiered diagnosis and treatment” policy continues to advance and radiopharmaceuticals expand into primary care settings, ensuring the timely delivery of these drugs to the vast primary care market will pose a significant challenge.

New Entrants Enter the Market, but Cannot Disrupt the Existing Landscape in the Short Term

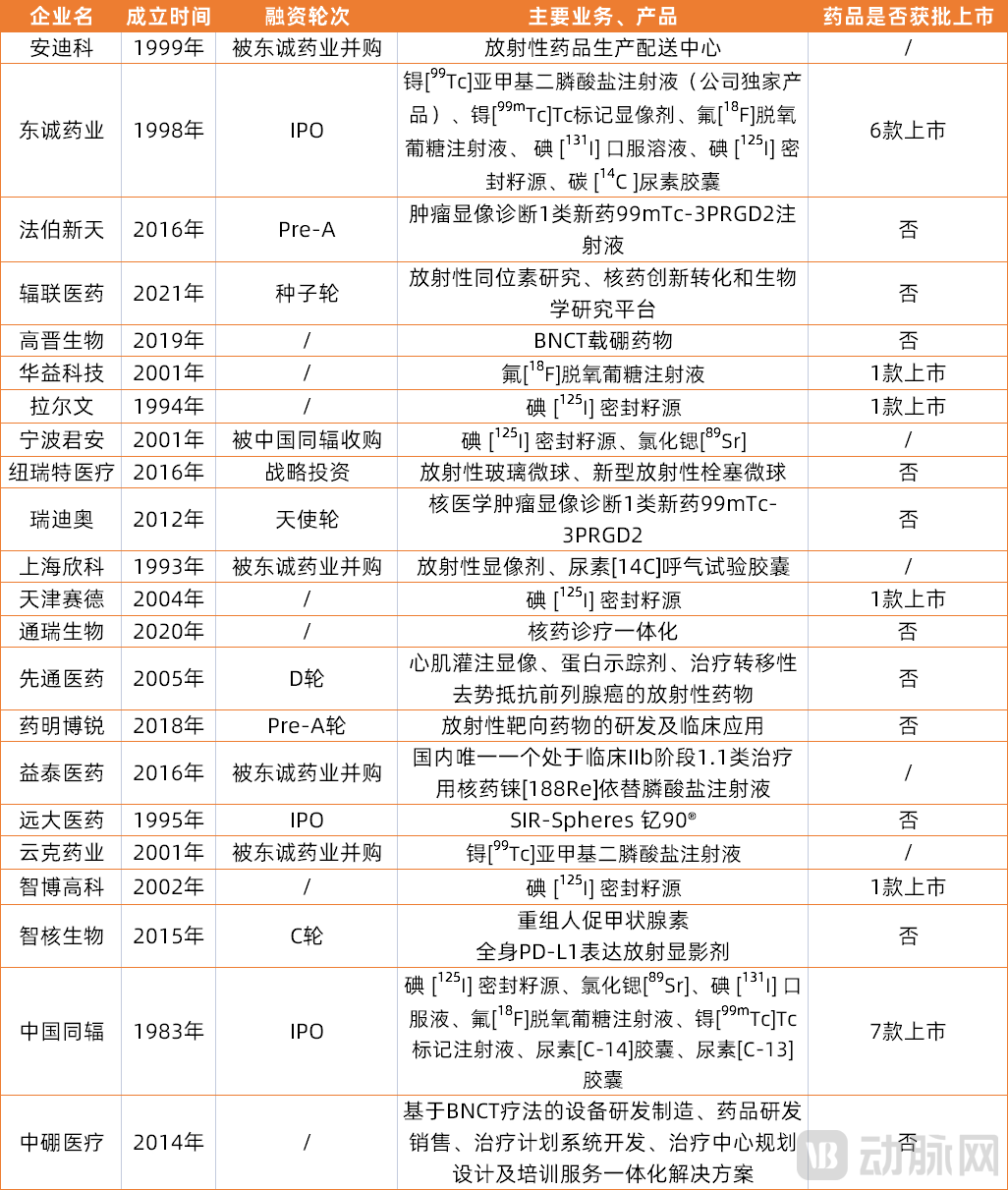

Overview of Chinese Nuclear Medicine Companies (Compiled from Public Information)

Companies operating in the radiopharmaceutical sector can be categorized into two groups: those dedicated exclusively to radiopharmaceuticals, such as China Isotope & Radiation Corporation, Zhihe Biotechnology, Zhongbo Medical, and Fulian Medical; and those that entered the field laterally, such as Dongcheng Pharmaceutical, which acquired Yunke Pharmaceutical in 2015, and Grand Pharma, which acquired Sirtex in 2018 to enter the radiopharmaceutical market.

For a long time, China Isotope & Radiation Corporation (CIR) and Dongcheng Pharmaceutical have dominated the market, with numerous approved products and significant market share. In contrast, companies such as Huayi Technology, Tianjin Saide, and Lalwen have only one product approved for marketing, resulting in limited industry influence. In recent years, however, the Chinese nuclear medicine market has attracted substantial investment and strategic deployment from new entrants like Grand Pharma and Zhongbo Pharmaceutical. These companies are focusing on highly innovative products with differentiated advantages, which may reshape the industry landscape in the future.

In 2018, Grand Pharma partnered with CDH Investments to acquire Sirtex for $1.4 billion, entering the radiopharmaceutical market. Sirtex’s core product, SIR-Spheres® Y-90, delivers selective internal radiation therapy via beta radiation for the treatment of primary liver cancer and metastatic colorectal cancer, among other indications. The marketing authorization application for this product was accepted by the National Medical Products Administration (NMPA) in 2020. In the same year, Grand Pharma entered into a share subscription agreement with Telix Pharmaceuticals and reached an equity purchase agreement with Pure Way, a radiopharmaceutical manufacturing and distribution company, thereby establishing a comprehensive domestic and international presence in the radiopharmaceutical sector.

Zhongbo Medical relies on Boron Neutron Capture Therapy (BNCT) to provide an integrated solution encompassing equipment R&D and manufacturing, pharmaceutical R&D and sales, treatment planning system development, treatment center planning and design, and training services. The company has independently developed a novel synthesis process for the boronated amino acid drug BPA, enabling high-efficiency preparation, reducing production costs, and achieving domestic production of the drug through independent R&D.18F-BPA, a positron-emitting radiopharmaceutical, is combined with PET imaging to assess drug distribution and precisely screen patients eligible for BNCT, while various next-generation boron agents are currently under exploration and development.

Zhihe Bio is an innovative nuclear medicine pharmaceutical company focused on the research and development of radiopharmaceuticals. It possesses a radionuclide-protein conjugation platform and a single-domain antibody development platform, with multiple products in the pipeline, including recombinant human thyroid-stimulating hormone and whole-body PD-L1 expression radioimaging agents, covering therapeutic areas such as thyroid cancer, breast cancer, and tumor immunology.

The entry of new enterprises has brought fresh momentum to China’s radiopharmaceutical industry, butNew enterprises will require a considerable amount of time to obtain product approvals and establish a multi-site network of nuclear pharmacies, making it unlikely that they will disrupt the existing market landscape in the short term.

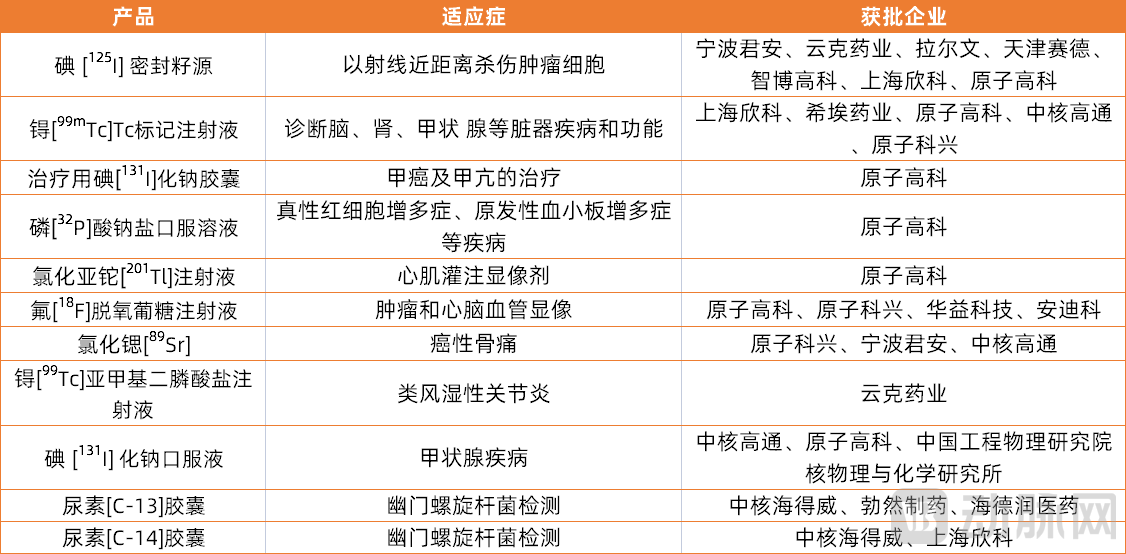

In China, the varieties with larger sales volumes are mainly fluorine[18F] Deoxyglucose Injection, Iodine [125I] Sealed Seed Source, Iodine [131I] Sodium Chloride Oral Solution, Technetium [99mTc]-labeled drugs, urea [C-13/14] breath test drugs/reagents, etc.

Domestic Nuclear Medicine Drugs Approved in China (Compiled Based on Public Information)

It is evident that China Isotope and Radiation Corporation (CIRC) and Dongcheng Pharmaceutical dominate the market for approved radiopharmaceuticals in China. It also becomes apparent that most domestic nuclear medicine products are generic versions of drugs that have been marketed abroad for many years.Product homogenization is severe, with a lack of differentiated and competitive innovative drugs.

For years, the research and development of innovative radiopharmaceuticals in China has been virtually stagnant, with no novel radiopharmaceuticals approved in recent years. Recognizing this gap, multiple companies, including China Isotope & Radiation Corporation and Dongcheng Pharmaceutical, are accelerating their efforts to seize market share.

In 2016, Dongcheng Pharmaceutical acquired Yitai Medicine and obtained the only Class 1.1 therapeutic radiopharmaceutical in China that was in Phase IIb clinical trials—Rhenium [188Re] Etidronate Injection. Rhenium [188Re] Etidronate Injection is currently the best medication for treating bone metastases. After administration, it rapidly concentrates in the affected bones, minimizing uptake by non-target tissues. The beta rays it emits provide significant analgesic effects.

Furthermore, Zhihe Bio and Faber New Sky are also focused on innovation in radiopharmaceuticals. However, these innovative enterprises are generally small in scale, with limited R&D capabilities and financial support. As the radiopharmaceutical sector is characterized by high investment requirements and significant barriers to entry, it is essential for these companies to identify clear development pathways and secure capital support.

With policy relaxation, increased capital investment, a growing talent pool, accelerated domestic substitution, and rising PET-CT installations, the development of nuclear medicine in China will continue to improve.

In terms of clinical adoption, the overall sales of radiopharmaceuticals in sample hospitals from 2012 to 2019 achieved a compound annual growth rate (CAGR) of 31%, with several key radiopharmaceutical products registering CAGRs exceeding 40%.

In terms of nuclear medicine department construction, as of December 31, 2019, the number of departments (sections) engaged in nuclear medicine-related specialties across China reached 1,148, representing a 23.8% increase compared to 2017; a total of 12,578 personnel were engaged in nuclear medicine-related work, marking a 38.4% increase compared to 2017.

In terms of the installed base of relevant medical equipment, positron emission tomography (PET) scanners reached 427 units by the end of 2019, representing a 39.1% increase compared to 2017; single-photon emission computed tomography (SPECT) scanners reached 903 units by the end of 2019, marking a 5.4% increase from 2017.

We believe that, under the current market landscape,Forge deep strategic partnerships with raw material suppliers, intensify R&D of innovative products, prioritize the development of long-half-life drugs, and accelerate the deployment of integrated theranostic services.It will be the breakthrough point for companies in the second tier to rapidly achieve a leap forward.

References:

Research Report on the Radiopharmaceutical Industry: High Barriers Forge a Duopoly, Illuminating the Vast Potential of Radiopharmaceuticals

Who Can Become the SpaceX of China’s Nuclear Medicine Industry?

China National Nuclear Corporation Magazine: "Radiopharmaceuticals: Breaking Through at the Source"

Pacific Securities "In-Depth Research Report on the Nuclear Medicine Industry"

Brief Report on the 2020 National Survey of Nuclear Medicine Practice in China