China Renaissance 2021 Annual Review: Diagnostics & Life Sciences Sector in Healthcare and Life Technology

2021 marked the second year of our coexistence with the COVID-19 pandemic, during which the healthcare sector witnessed continuous changes and emerging opportunities: frequent policy updates in the Chinese and U.S. capital markets; volatile market performance for companies focused on pandemic-related themes and diagnostics; deeper penetration of digital therapeutics and internet-based healthcare services; AI-driven enterprises obtaining regulatory approvals and entering the capital markets; and an increasing number of medical device companies listing on the Hong Kong Stock Exchange via IPOs.

As we embrace a season of renewal, the Huaxing Healthcare and Life Sciences team, with years of deep industry expertise, will present a four-part series to review the global healthcare trends of 2021 and look ahead to a broader future of innovation and upgrading in the medical field. The series will cover four key sectors: Diagnostics and Life Sciences, Pharmaceuticals and Biotechnology, Medical Devices, and Smart Healthcare. The first article will focus on the Diagnostics and Life Sciences sector; stay tuned for insights into the other areas.

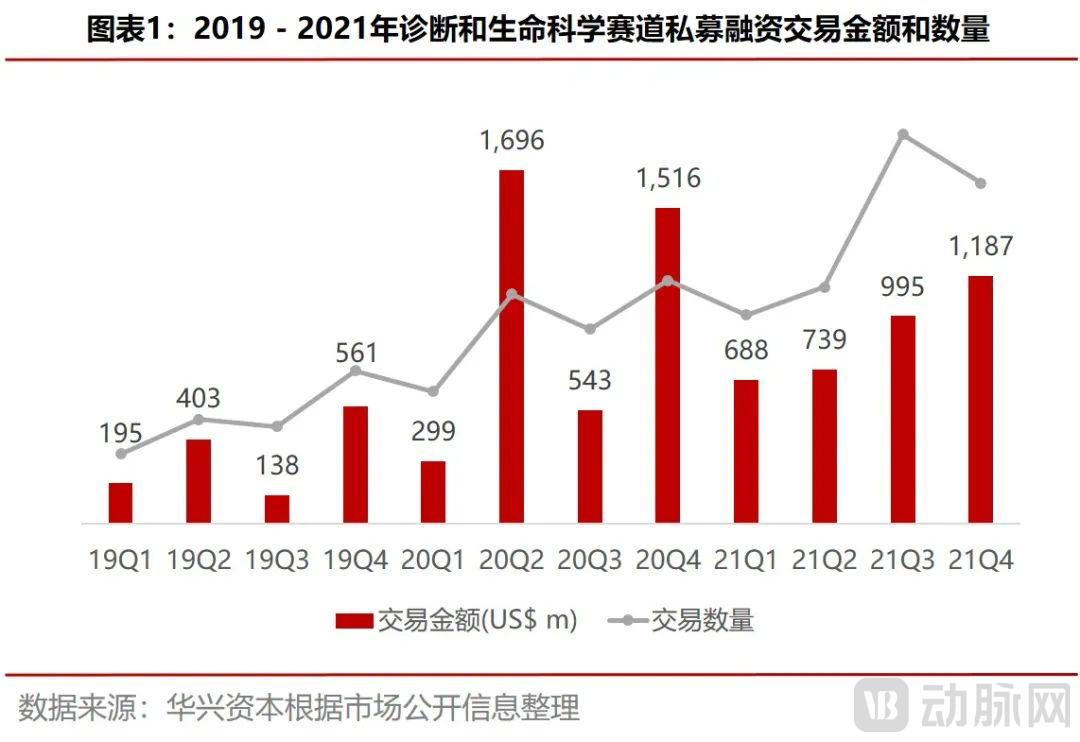

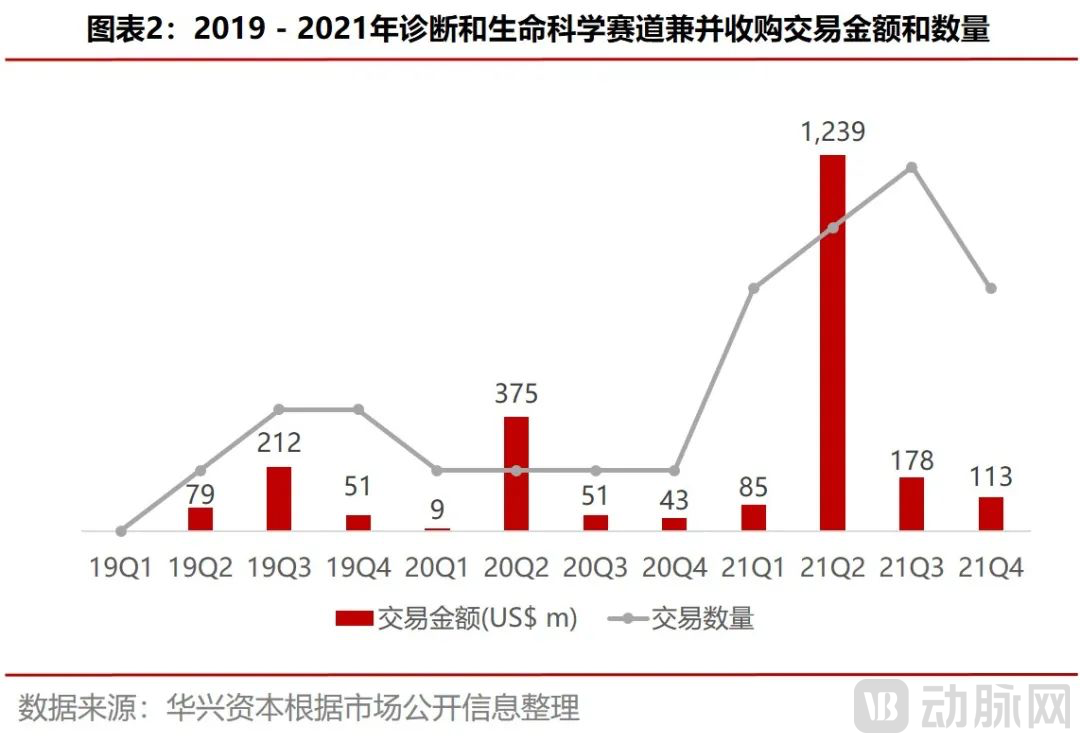

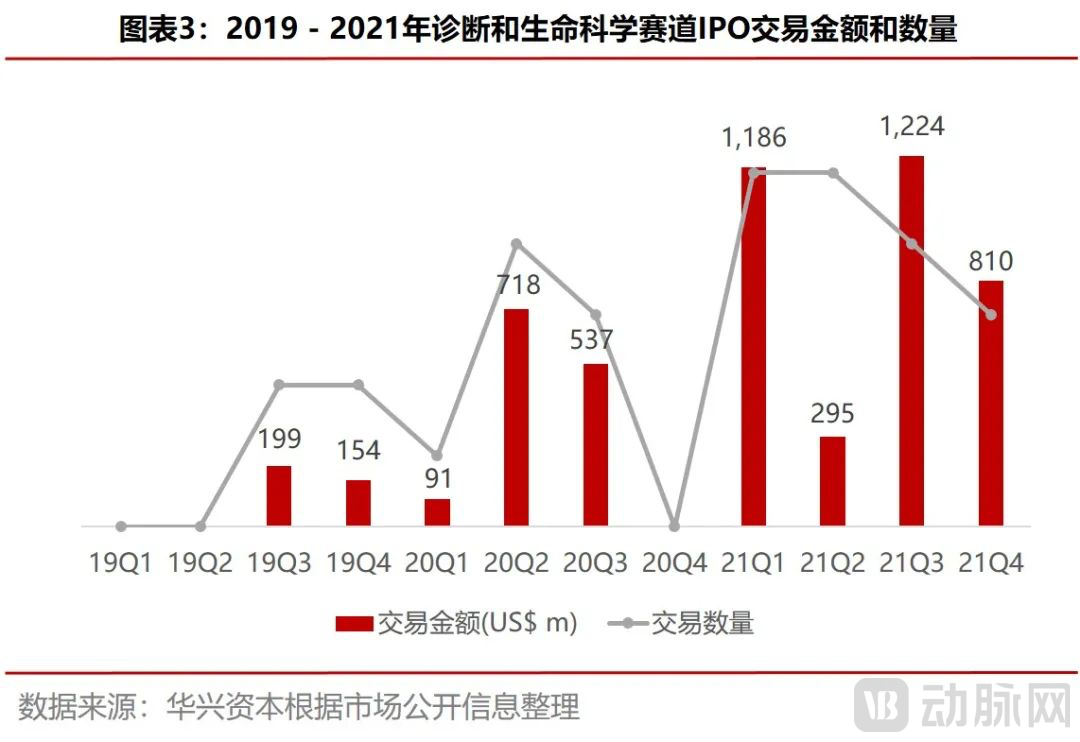

Overall, unlike the explosive growth seen in the diagnostics industry during the first year of the COVID-19 pandemic (2020), the sector entered a phase of adjustment in 2021. In terms of primary and secondary market transactions, private financing slowed down, and transaction volumes declined significantly. This was partly due to the temporary vacuum following the industry’s surge in 2020, and also directly related to the substantial volatility in domestic and overseas secondary markets. Nevertheless, the M&A and IPO markets remained highly active, with both transaction value and volume reaching record highs, as companies that capitalized on opportunities arising from the COVID-19 pandemic took the lead.

From the perspective of industry development, we summarize the following insights and outlooks: oncology remains the most favored sector; innovation driven by intense competition (“involution”); encouragement of domestic production for bottleneck technologies; industry consolidation in the post-pandemic era; and cross-sector integration under the digitalization of life sciences.

Disease: Oncology Remains the Most Favored Sector, with Integrated Diagnostics Built Through Full-Lifecycle Extension

Oncology remained the most sought-after therapeutic area by capital markets in 2021. Companion diagnostics and early diagnosis and screening for cancer continued their robust growth trajectory.

In the field of tumor companion diagnostics, companies such as Genetron Health, Simcere Diagnostics, TumorHunters, and ZhiBen Medical have successfully completed their latest rounds of financing. Meanwhile, other early-mover companies in the industry have begun initiating their final pre-IPO financing rounds. The competitive landscape of the first tier has largely been solidified, shifting from a period of intense competition among numerous players to one dominated by leading enterprises. Latecomers are now facing significant survival pressures, including difficulties in securing funding. The substantial decline in the secondary market stock prices of Burning Rock Biotech and Genetron Health has also placed considerable pressure on the IPO prospects of other first-tier players. How to escape the value depression and break through the industry’s predicament are questions being collectively contemplated by all stakeholders.Burning Rock Biotech was the earliest to lay out a pan-cancer early screening strategy to create a second growth curve, while Zenith Epigenetics has entered the fields of prognosis assessment and recurrence monitoring via minimal residual disease (MRD) testing, thereby building differentiated competitive barriers. The industry is undergoing reshaping. In the future, early screening companies will extend further along clinical pathways, and tumor diagnosis will evolve toward full-lifecycle management, encompassing early diagnosis and screening, precision medication and efficacy evaluation, postoperative prognosis assessment, and recurrence monitoring, ultimately achieving more precise diagnosis and treatment.

In the colorectal cancer segment, the most dynamic niche within the field of early cancer diagnosis and screening, New Horizon Health has completed its listing on the Hong Kong Stock Exchange, while companies such as ClearMed Biotech, Ameson, and MiRGenomics have secured new rounds of financing. Furthermore, early screening applications are expanding beyond colorectal cancer to other solid tumors, with liver cancer emerging as the next focal point. In addition to Genetron Health, which is already publicly listed, early-stage liver cancer pioneers such as HuiRui Gene and Aorui Gene have completed new financing rounds, and colorectal cancer screening players like New Horizon Health are also actively entering this space.

From the perspective of technical platforms, tumor detection has expanded from a sole focus on nucleic acids to include multi-omics biomarkers such as proteins. The field is evolving from technologies centered on NGS and PCR toward integrated, automated solutions that combine multiple platforms.

From a policy perspective, with the implementation of centralized procurement for in vitro diagnostic (IVD) reagents in Anhui Province and the national medical insurance price negotiations for oncology therapeutics, diagnostics—serving as the front end of clinical pathways—are also facing mounting pressure from the normalization of centralized procurement. In the area of early colorectal cancer screening, Beijing has taken the lead in including gene methylation testing in its medical insurance coverage. It is expected that this practice will be replicated in other regions, leading to increasingly fierce market competition. Meanwhile, payment-side pressures will inevitably drive continuous optimization of related tests in terms of both technology and business models.

As one of the largest and fastest-growing disease diagnosis and treatment markets in China, oncology will remain a sector of keen interest to capital markets for a considerable period. However, given the ever-changing nature of the market, cardiovascular and cerebrovascular diseases, neurological disorders, or other conditions may well emerge as subsequent therapeutic hotspots.

Technology: Innovation-Driven Growth Amid “Involution,” with Multi-Omics Coming to the Fore

Including non-invasive prenatal testing (NIPT), oncology, genetic disorders, and microbial detection, the industry has become increasingly mature and is beginning to show signs of intense internal competition. Innovative technologies are garnering significant attention, with multi-omics approaches—such as proteomics, metabolomics, single-cell analysis, and phenomics—leading the industry into the “post-genomic” 2.0 era.

With the public listings of U.S. multi-omics platform technology companies such as Seer, Olink, Somalogic, Quantum-Si, and Nautilus, China’s multi-omics sector has entered a period of heightened activity. Representative metabolomics firms, including Kaluipu, Metware, and Nuomi Metabolism, have successively completed financing rounds. Westlake Omics, an emerging player in proteomics, secured two rounds of funding within six months; its rapid valuation increase underscores capital markets’ strong interest in this burgeoning hot sector.

Proteomics and metabolomics more accurately reflect the current state of disease, holding significant importance for understanding biological processes and disease treatment. One of the core technological platforms for related omics research is mass spectrometry. Due to its superior high-throughput capability, sensitivity, specificity, analysis speed, and ability to simultaneously detect multiple indicators in complex samples, mass spectrometry is highly suitable for the discovery of novel biomarkers and their clinical translational applications.

In 2021, mass spectrometry testing experienced explosive growth, driven by successive breakthroughs in mass spectrometry instruments and supporting reagents, the launch of one-stop clinical mass spectrometry IVD solutions spanning from sample pretreatment to downstream data services, and the maturation of China’s LDT market. In the upstream sector, Chinese instrument developer Hexin Instrument listed on the STAR Market, while Rongzhi Biology and Ruilaipu completed financing rounds. In the midstream product and downstream service segments, companies such as Yingsheng, Baichen, and Haosi received strong support from leading investment firms. Amidst the sector’s fervor, homogeneous competition has intensified, and the clinical mass spectrometry landscape has become increasingly crowded. Companies are now seeking second growth curves; beyond pursuing breakthroughs in sample pretreatment and automation, multi-omics has emerged as a critical battleground for all players.

Currently, leading overseas companies such as Somalogic and Metabolon are primarily focused on scientific research and new drug development, with clinical applications and industrial translation just beginning to take off. China possesses the fertile ground necessary to nurture global leaders in multi-omics. Driven by the gradually opening policy support for Laboratory Developed Tests (LDTs), abundant domestic clinical cohorts, and increasingly robust capabilities in multi-omics data acquisition, mining, and bioinformatic interpretation, Chinese enterprises are poised to achieve leapfrog development in the source-innovation-driven translation of multi-omics applications, thereby leading global industry transformation.

With the explosion of the “post-genomic” era, continuous technological updates and iterations, and the expansion of application scenarios, multi-omics will break through the limitations of single-omics approaches, and integration across omics disciplines will become more frequent. Examples include collaborations between Kalu Pu (Kayla Biosciences) and Singleron (metabolomics and single-cell omics), as well as with Westlake Omics (metabolomics and proteomics). Furthermore, the continuous emergence of cutting-edge technologies such as spatial-temporal omics will enable more precise and personalized diagnosis and treatment in the future.

Industry Chain: Upstream Raw Materials and High-End Life Science Instruments Are in High Demand

Under the overarching industry trend of domestic substitution, Chinese brands have significant room for growth in the upstream raw materials and high-end equipment markets, which are currently dominated by international brands. Furthermore, as a critical link in the upstream segment of the diagnostics industry chain, strong bargaining power and a clear business model ensure more robust and stable profitability, rendering these companies highly attractive from an investment perspective.

At the policy and macroeconomic levels, the state has provided strong support for innovation and continued favorable conditions for the procurement of domestically produced products. Examples include the issuance of Presidential Order No. 103 at the end of the year (revising the “Law of the People’s Republic of China on Progress in Science and Technology”), reaffirmation of restrictions on foreign investment access, and the “14th Five-Year Plan for the Development of the Medical Equipment Industry,” which specifies key support for seven major areas, including diagnostic and laboratory equipment.

In the upstream raw materials sector, driven by favorable conditions stemming from the global pandemic and policy environments aimed at resolving “chokepoint” technologies, domestic primary and secondary markets have paid unprecedented attention to raw material companies. Sino Biological and Vazyme have successfully listed on the ChiNext and STAR Market, respectively, demonstrating strong market capitalization performance; the IPO applications of Fitogen and Conwiz have been accepted; Abclonal and Hanhai Enzyme have each completed private financing rounds of approximately RMB 1 billion; Hytest, a leading global legacy upstream raw material supplier, was acquired by Mindray for approximately EUR 545 million in cash, setting a new industry record. Raw materials significantly impact the quality and cost of diagnostic products. Currently, overseas giants still dominate the majority of the market share. However, with the trend of domestic substitution and the international expansion of Chinese enterprises, we anticipate that domestic upstream companies will gradually build comprehensive technical platforms, diversify their product portfolios, and break the market monopoly held by foreign giants. Furthermore, some upstream companies in the industry have begun to actively expand into equipment and diagnostic reagents, which is expected to reshape the industrial chain landscape.

In the field of high-end life science equipment, particularly in sequencing instruments and automation applications, the industry has received strong support from the capital market, driven by the benchmark effect of MGI Tech’s successful listing on the STAR Market. Internationally, Oxford Nanopore Technologies is listed on the London Stock Exchange; domestically, companies such as Qitan Technology, Annoroad, Jinshi Technology, and Zhenmai Biology have also gained recognition from the capital market alongside their rapid business growth. In specific application scenarios, such as CAR-T therapy, DNA reading/writing/storage, laboratory equipment, and integration, a trend toward full-chain domestic substitution has begun to emerge. It is believed that, bolstered by favorable policies, the high-end equipment sector will achieve faster and higher-quality development in the future.

Driven by unmet needs in scientific research and clinical practice, technologies, omics, and manipulation techniques at the single-cell and single-molecule levels have become the most sought-after breakthroughs in the market. This year, companies including Singleron Biotechnologies, Vanx Gene, Xunyin Biotechnology, Mozhuo Biotechnology, and Caike Biotechnology have emerged and successfully secured financing. Fueled by the strong momentum in upstream innovative life science equipment, this sector is poised to remain a key focus throughout 2022.

Landscape: “The Industry Enters a Consolidation Phase in the Post-Pandemic Era”

Since 2020, numerous companies have rapidly accumulated performance results and wealth through COVID-19 testing businesses, successfully going public. Meanwhile, industry leaders across various sectors in the primary market have raised substantial funds. These funds have not only supported organic corporate growth but also enabled companies to quickly supplement their business or product lines through external investments or mergers and acquisitions.

In 2021, early signs of mergers and acquisitions (M&A) began to emerge in the diagnostics and life sciences market. In China, traditional listed in vitro diagnostics (IVD) companies, whose performance surged during the pandemic, sought second growth curves by acquiring innovative technology platforms. Notable examples include Sansure Biotech’s attempted acquisition of Kehua Bioengineering (which led to the establishment of a joint venture after the deal fell through) and its investment in Genetron Biology; Mindray Bio-Medical’s investment in Nuoyin Biotechnology; Fapon Biotech’s acquisition of Sequlite; and ABclonal’s acquisition of Yurogen. Additionally, Mindray Medical acquired Hytest to address bottlenecks in upstream technologies, while simultaneously accelerating breakthroughs in product R&D capabilities and advancing its internationalization process. The overseas market also witnessed several large-scale M&A transactions, including Quidel’s unsuccessful attempt to acquire Qiagen followed by its successful acquisition of Ortho Clinical Diagnostics, Novo Holdings’ acquisition of BBI, and PerkinElmer’s acquisition of BioLegend.

As the dividends from COVID-19-related businesses continue, it is foreseeable that industry consolidation in 2022 will intensify, characterized by high frequency, large transaction volumes, and internationalization. Investment hotspots will increasingly focus on sectors with stronger business synergies with traditional diagnostic companies, such as molecular diagnostics and point-of-care testing (POCT).

Our 2022 Outlook

Looking ahead to 2022, under the industry themes of “post-pandemic” and “post-genomic” eras, oncology remains a key focus for capital markets. We anticipate the emergence of more testing technologies and products across various cancer types, particularly in early detection and screening, auxiliary diagnosis, prognosis guidance, and health management. We are focusing on industry game-changers that can deliver high-quality testing, ensure product accessibility, and achieve successful commercialization. The industry, characterized by intense “involution,” will undergo reshuffling and consolidation. Companies with strong innovation capabilities, high technical barriers, and sustainable long-term growth prospects will continue to attract capital favor, while those trapped in homogeneous competition may opt for mergers and acquisitions as an exit strategy. Data forms the foundation of multi-omics; when combined with single-cell and single-molecule technologies, it enables multi-dimensional, more precise personalized diagnosis and treatment, while significantly driving the systematic, digital, and intelligent development of life sciences. We believe that in 2022, the diagnostics industry will witness greater cross-sector integration and innovative transformations empowered by AI and big data.