China's Five-Year Healthcare IT Plan Unveiled: “Small but Beautiful” Million-Dollar Orders Emerge as the New Mainstream

In February 2009, President Obama signed the American Recovery and Reinvestment Act (ARRA), under which the HITECH Act allocated more than $20 billion to promote the adoption of health information technology across the United States. One year later, the Patient Protection and Affordable Care Act (PPACA) was enacted, introducing the “Medicare and Medicaid EHR Incentive Program.” This policy provides financial incentives to physicians and hospitals that adopt electronic health records (EHRs) while imposing penalties on those that do not.

Behind the massive investment in medical IT and the mandatory implementation of electronic health records (EHRs) lies the U.S. government’s determination to leverage digitalization to control healthcare costs amid the heavy burden of national healthcare expenditure. To genuinely reduce healthcare spending, it is essential to break down data barriers between insurance providers and healthcare institutions, enabling real-world clinical data to serve as the basis for insurance reimbursements—in this process, EHRs act as the key medium connecting the system.

Although there are fundamental differences between the Chinese and U.S. healthcare systems, electronic medical record (EMR) systems remain a cornerstone in driving healthcare IT reform in both countries.

In 2018, the issuance of the “Notice on Further Promoting the Construction of Information Systems in Medical Institutions with Electronic Medical Records (EMR) as the Core” ushered in the era of high-level EMR grading. In alignment with the EMR requirements embedded in the performance evaluation of tertiary public hospitals, hospitals launched vigorous initiatives to achieve Level 3 EMR certification by 2019 and Level 4 by 2020.

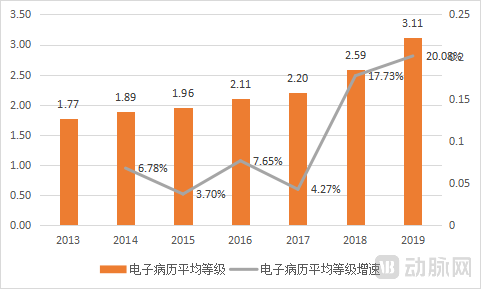

Between 2013 and 2017, the development of electronic medical records (EMR) in China remained sluggish, with an average annual increase in EMR maturity levels of less than 8%. However, following the release of the grading indicators in 2018, the EMR maturity level surged by approximately 20%, thereby achieving the national grading target set for 2019.

Electronic Medical Record (EMR) Grading Status from 2013 to 2019 (Data Source: CHIMA)

Data on electronic medical record (EMR) grading for 2020 and 2021 have not yet been released. However, assuming a continued growth rate of 20%, the overall EMR grading level would approach Level 4 in 2020, even if the predefined targets were not fully met. In other words, by the end of 2021, tertiary hospitals across China had nearly achieved comprehensive implementation of basic clinical decision support systems and hospital-wide information sharing.

Having reached this stage, medical IT construction has arrived at a critical turning point.

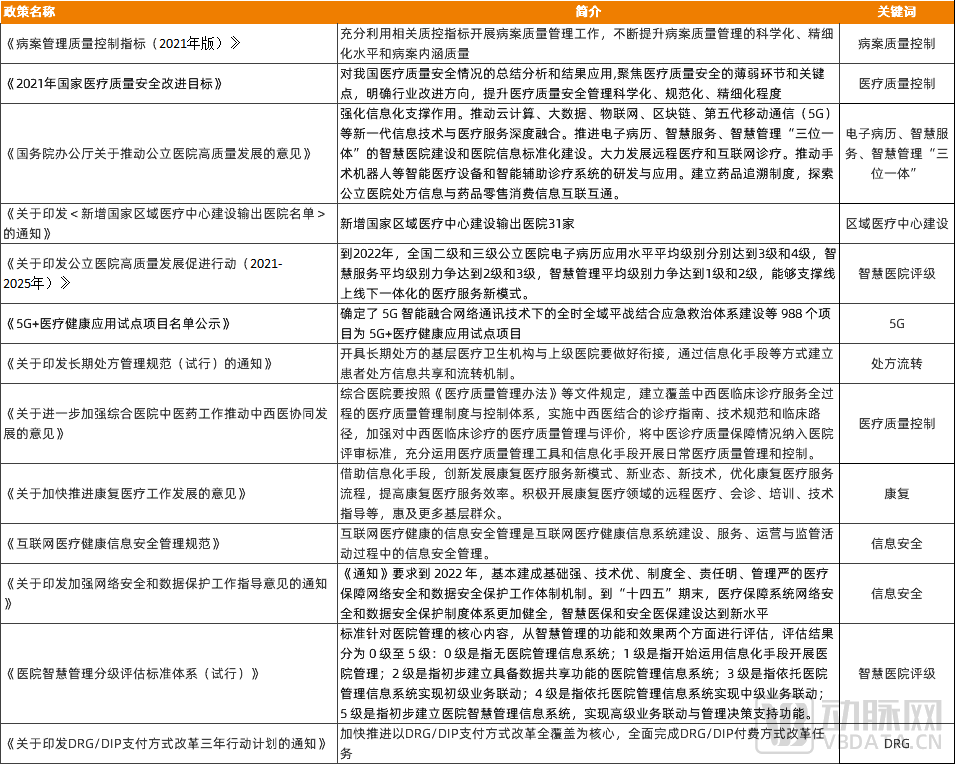

A review of the policies involving the National Health Commission in 2021 reveals a total of 13 items related to healthcare informatization. Extracted by keywords, these policies focus on several key areas: “quality control,” “smart hospitals,” “information security,” and “regional center development.”

However, to prioritize its importance, two policies—the “Action Plan for Promoting High-Quality Development of Public Hospitals (2021–2025)” and the “Notice of the National Healthcare Security Administration on Issuing the Three-Year Action Plan for DRG/DIP Payment Method Reform”—have established the main trajectory for healthcare informatization construction from 2021 onward.

Summary of Healthcare IT-Related Policies in 2021

Summary of Healthcare IT-Related Policies in 2021

“The Notice on Issuing the Action Plan for Promoting High-Quality Development of Public Hospitals (2021–2025)” outlines the development roadmap for public hospitals, covering their past, present, and future. Notably, the fourth key initiative under the priority construction actions—“Building a ‘Trinity’ Smart Hospital”—echoes the approach advocated three years ago for electronic medical record (EMR) system development. The document states:

By 2022, the average levels of electronic medical record (EMR) application in secondary and tertiary public hospitals across China reached Level 3 and Level 4, respectively. The average levels of smart services aimed to reach Level 2 and Level 3, while the average levels of smart management aimed to reach Level 1 and Level 2, thereby supporting a new model of integrated online and offline medical services.

Given the current landscape, a significant number of hospitals already meet the grading requirements for Electronic Medical Records (EMR) and smart management. Consequently, construction efforts in 2021 will focus more heavily on achieving higher ratings in smart services. This signifies that the focal point of healthcare informatization is gradually shifting from foundational IT infrastructure to the development of smart hospital applications, such as Clinical Decision Support Systems (CDSS), AI-assisted diagnosis, and internet hospitals. In the coming year, “intelligentization” will be the primary theme of development.

Another key focus of the policy lies in the capacity-building initiatives, which emphasize the “Implementation of Medical Quality Improvement Actions.” This aligns closely with the Quality Control Indicators for Medical Record Management (2021 Edition) issued in early 2021 and the Notice on Further Strengthening Quality Management and Control of Single Diseases released in mid-2020. The document states:

Improve the medical quality management and control system, strengthen the construction and management of quality control centers at all levels, further refine the medical quality control indicator system, and continuously consolidate the eighteen core systems for medical quality and safety. Guided by the annual “National Medical Quality and Safety Improvement Goals,” promote goal-oriented management. Implement special initiatives related to surgical quality and safety and the enhancement of medical record content. Promote the “four unifications” for secondary and above public hospitals in terms of medical record front pages, medical terminology, disease diagnosis coding, and surgical procedure coding.

The introduction of this policy aims to highlight “quality control” and “cost control.” In conjunction with the Notice on Issuing the Three-Year Action Plan for DRG/DIP Payment Method Reform released at the end of 2021, the development of information systems related to medical insurance cost containment will become the second major theme for construction in 2022.

The “impossible trinity” of healthcare describes the inherent contradiction in simultaneously achieving low cost, high efficiency, and high-quality services. However, it also demonstrates that technological advancements can alleviate the mutual constraints among these three factors, thereby raising the upper limits attainable for each “vertex.” This was precisely the objective of the policy goals set in 2021. The key lies in finding a balance point that controls health insurance expenditures while ensuring the provision of high-quality medical services, thereby leveraging these outcomes to alleviate pressure on the health insurance system. In this process, the synergy between smart hospital development and health insurance informatization is crucial to achieving this goal.

Zhang Qi, CEO of Huimei Technology, stated in an interview: “Since 2018, the state has successively introduced relevant policies, standards, and supporting documents to promote the development of this industry. For instance, in the area of smart hospital grading, we must first improve foundational capabilities such as electronic medical records and interoperability. Only then can digitalization in the smart hospital sector be fully leveraged, enabling higher-level applications of smart services. This is an indispensable process.”In 2021, the overall construction of electronic medical records (EMR) in China’s healthcare institutions was largely completed, naturally propelling the development of healthcare informatization into its next phase.”

“On Health Insurance Again.” The normative documents on the reform of DRG/DIP payment methods have clearly outlined the timeline and phased objectives. However, over the past five years, despite the rapid advancement in healthcare informatization, health insurance payment systems seem to have failed to leverage this momentum. The primary reason lies in the fact that current healthcare informatization efforts have focused more on patient services, providing clinical decision support tools for physicians, and assisting hospitals in managing medical quality.

"In the future, to achieve refined management and precise, rational cost control, hospitals must intensify their efforts in information technology infrastructure, particularly by striking a balance between medical quality and reasonable cost containment—a feat unattainable through manual labor and traditional methods. Therefore, medical AI enables real-time, automated, and intra-process multidimensional intelligent cost control and statistical analysis across DRG grouping, expense management, and health insurance settlement documentation, constituting a management system for hospitals aimed at cost containment and quality improvement."

From Zhang Qi’s perspective, once the foundational capabilities of electronic medical records meet the required standards, construction proceeds downward along the timeline, with one aspect followingSmart Hospital Applicationscontinue to move forward in this direction, leveraging information technology to optimize clinical and management processes. This approach offers numerous entry points, with individual order values in the millions but substantial demand, representing a fragmented yet vast market; on the other hand,Medical Insurance Information TechnologyConstruction is an urgent priority amid the pressure on medical insurance.

The concept of building smart hospitals has been discussed for many consecutive years.

For a large number of Grade A tertiary hospitals, the process of achieving Level 4 Electronic Medical Record (EMR) certification has already endowed them with a certain degree of intelligent capabilities. During the informatization upgrade, various departments have deployed numerous applications; however, these applications are largely isolated and non-standardized, resulting in a lack of data interoperability between them. To promote the development of smart hospitals at this stage, the primary task is to break down the data barriers across different hospital scenarios.

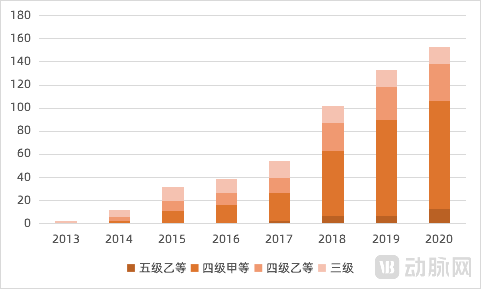

VCBeat conducted a survey in 2021 on the status of the Standardization Maturity Assessment for Interconnectivity of Medical and Health Information in China. The data showed that out of 13,400 secondary-and-above hospitals nationwide, only 503 had passed the Level 3 or higher interconnectivity assessment. This means that merely 3.75% of secondary-and-above hospitals in China achieved Level 3 or above in the Standardization Maturity Assessment for Interconnectivity of Medical and Health Information, indicating that the current level of medical and health information interconnectivity in China remains relatively low.

Historical Interconnectivity Assessment Results

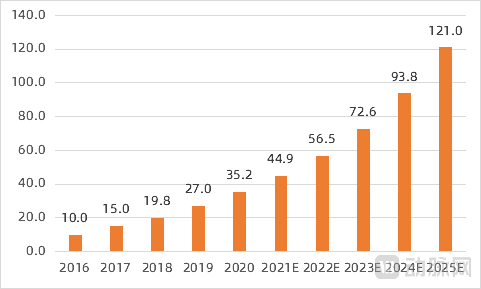

Consequently, with the development of smart hospitals as the central theme, businesses related to interoperability ratings, medical big data platforms, integration platforms, and data middlewares experienced rapid growth in 2021, a trend that is expected to continue. Many next-generation enterprises have risen to prominence by leveraging this wave. Taking the market size of medical data centers as an example, Frost & Sullivan, in the prospectus of Jiahua Meikang, reported a compound annual growth rate (CAGR) of 37.0% for the period from 2016 to 2020, and projects that the market will maintain a CAGR of 28.0% from 2021 to 2025.

Market Size of China’s Medical Data Center Industry (Unit: RMB 100 million; Source: Jiahua Meikang Prospectus)

Hospitals that have completed data governance can proceed with the application-layer development in accordance with the Smart Hospital Service Rating and Smart Hospital Management Rating systems. In 2022, the national requirements for smart hospital construction in tertiary public hospitals were not overly stringent, as data sharing and integrated smart services connecting internal and external hospital operations had already been partially implemented in many institutions. Consequently, in 2022, more hospitals will focus on addressing gaps in missing functionalities, such as enhancing follow-up capabilities in internet hospitals and optimizing the intelligent features of online consultation and triage services.

Smart Hospital Service/Management Rating Requirements (In 2022, tertiary public hospitals were required to reach Level 3/Level 2, respectively)

Smart Hospital Service/Management Rating Requirements (In 2022, tertiary public hospitals were required to reach Level 3/Level 2, respectively)

Where to Go Next After 2022? Under Policy Guidance, Companies Such as Huimei Technology, Senyi Intelligence, and Jiahe Meikang Have All Bet on the Development of Specialty-Specific Informatics.

Specialized information system development serves two primary objectives: first, to optimize service workflows, enhance quality and efficiency, and reduce operational costs; second, to enable specialty-generated data to integrate with hospital-wide information systems, meet DRG/DIP requirements, and support managers in making refined, data-driven decisions. This landscape encompasses many high-potential areas that remain underexploited by most enterprises, such as Goodwill’s oncology and obstetrics electronic medical records (EMR), and Huimei Technology’s single-disease quality control systems and venous thromboembolism (VTE) management solutions.

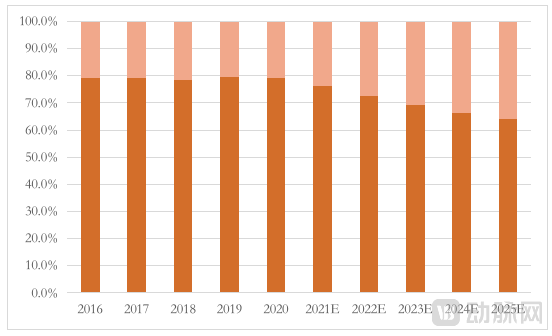

Changes in the EMR Market Structure from 2016 to 2025 (Source: Jiahua Meikang Prospectus; the upper section represents the specialized EMR market)

AI+CDSS systems that integrate clinical grading, data reporting, and medical quality control have become key strategic focuses for major health IT vendors, with companies such as Huimei Technology, Senyi Intelligence, and Jiahe Meikang prioritizing their development. According to statistics from VCBeat Research Institute, AI products related to quality control and CDSS ranked first and second in the number of AI-related bids, accounting for 29% and 28%, respectively. As smart hospitals strengthen their assessment of clinical decision support through the “three pillars” framework, specialty-specific CDSS solutions are expected to accelerate their deployment in tertiary hospitals in the coming year.

Overall, foundational IT infrastructure has begun to yield results, and the push for medical insurance cost containment is imminent. Under the combined influence of these factors, intelligent applications heavily invested in by next-generation healthcare informatics companies are finally poised for rapid development. In 2022 and the subsequent years, intelligent applications—primarily specialty-specific Clinical Decision Support Systems (CDSS), specialty-specific electronic medical records (EMR), and AI-assisted diagnosis—as well as customized services for smart hospital accreditation, are expected to be widely implemented across hospitals.

The construction of smart hospitals ensures the “medical quality” component of high-quality hospital development; the next step is to control costs while pursuing quality.

In November 2021, the National Healthcare Security Administration (NHSA) issued the *Notice on Printing and Distributing the Three-Year Action Plan for the Reform of DRG/DIP Payment Methods*, requiring that by the end of 2025, DRG/DIP payment methods cover all eligible medical institutions providing inpatient services, basically achieving full coverage of disease types and medical insurance funds. This document even provided specific implementation targets.

All medical insurance pooling areas shall implement DRG/DIP payment method reforms and make actual payments; expenditures from the pooled medical insurance fund under DRG/DIP payments shall account for 70% of total inpatient medical insurance fund expenditures within the pooling area; all medical institutions providing inpatient services within the pooling area that meet the conditions for DRG/DIP payment implementation shall achieve full coverage of DRG/DIP payments; for disease types/groups included in DRG/DIP-based payments, medical institutions shall fully implement DRG/DIP payments, with an encouraged case-mix grouping rate of over 90%.

During the three-year pilot implementation of CHS-DRG, medical practices in healthcare institutions across pilot cities have gradually become more standardized. The proportion of surgical and procedural groups, which reflect technical complexity, has shown an upward trend, while the proportion of internal medicine groups, representing conservative pharmacological treatment, has declined. Furthermore, unnecessary hospitalizations in pilot cities have decreased, alleviating the issue of “over-treatment for minor illnesses.” Taking Beijing as an example, the average proportion of pharmaceutical costs in healthcare institutions dropped from 38.8% to 24.2%, while the share of medical service fees increased from 30.6% to 36%. Nevertheless, despite these significant achievements, there remains a considerable gap before reaching the target set for the end of 2025.

To meet such challenges, the healthcare system requires a comprehensive set of information technology standards and infrastructure for support. The validity of DRG data imposes requirements on medical records, while the quality of these records demands robust information exchange and quality control capabilities across various departments. Therefore, only by establishing a solid foundation in electronic medical records (EMR) can we effectively advance the informatization of health insurance. With EMR systems universally achieving Level 4 certification, the synergistic operation of these two systems allowed the goals of smart hospital development and health insurance informatization to gradually unfold in 2021. In this regard, China and the United States have traversed a similar path.

However, the market for health insurance informatization is not particularly large, with companies such as Guoxin Health, Huoshu Technology, and Pingyi Medical Insurance already having secured a first-mover advantage in this field. Therefore, compared to its impact on enterprises, health insurance informatization has a greater influence on hospitals and physicians. Hospitals, long accustomed to the model of subsidizing medical services through drug markups, have begun—much like private hospitals—to focus on achieving optimal medical outcomes within the same level of expenditure over the past few years.

In reviewing the full-year development of 2021, VCBeat identified smart hospital construction and health insurance information system development as the highest-priority areas, though not those with the largest market size. In fact, competition in healthcare informatization has never been a simple shift from A to B; rather, it predominantly involves integrating B into ongoing A initiatives.

Therefore, an analysis of bidding data reveals that larger contracts continue to be secured by leading health IT companies such as Winning Health, B-Soft, and Yilianzhong, primarily for projects involving medical consortia and hospital accreditation. However, laying a solid foundation serves the purpose of constructing more prominent structures atop it; as time progresses, these advanced applications are gradually replacing foundational systems as the mainstream focus of healthcare IT.

Meanwhile, competition among public hospitals is also driving the overall development of healthcare informatization in China, with companies such as Kangbojia and Jiahe Meikang securing more orders. In particular, healthcare IT solution providers represented by Kangbojia have assisted numerous hospitals in completing their digital transformation in recent years, significantly advancing the intelligent evolution of the entire healthcare system.

From this perspective, healthcare IT development over the next five years will no longer resemble the patterns of the first two decades of this century; order, standardization, and efficiency will replace extensive growth models. In this process, hospitals, physicians, health insurance providers, patients, and enterprises will all benefit.