2022 Shifts in Medical Device Investment Trends: Ophthalmology and Upstream Sectors Emerge as Hotspots

“The downward revision of valuations for healthcare companies in the secondary market, which has driven a downturn in the primary market, is the trend we have felt most acutely,” an investor told VCBeat.

Over the past two years, this medical device investor has reviewed numerous high-profile projects of varying scales across China. He candidly admitted that although these projects commanded high valuations, they lacked sufficient quality in terms of market potential, global competitiveness, and technological originality. Subsequently, these companies secured financing and successfully went public; however, within less than a year on the secondary market, their market capitalizations declined, with many enterprises falling back to their IPO prices.

“Ultimately, the market will arrive at a reasonable price based on value. However, this recent downturn in the secondary market has still caused significant volatility.”

The most significant change in the medical device sector at the beginning of 2021 was a widespread rise in valuations, followed by successive funding rounds for domestic companies, which led to homogeneous competition among Chinese firms. As the market began to tighten in 2022, how would new trends emerge and shape the trajectory of the medical device industry? Based on data and insights from frontline investors, VCBeat (WeChat ID: vcbeat) has outlined the new investment trends in the medical device sector for 2022.

What was the biggest change in the healthcare investment industry at the beginning of 2022?

Domestic investors have clearly felt the downward pressure on the primary market driven by the secondary market, with a marked contraction in investment firms. This pessimistic sentiment is correlated with the performance of medical device companies in the secondary market.

According to Frost & Sullivan, as of December 31, 2021, there were a total of 20 companies in the medical device sector on the Hong Kong Stock Exchange (HKEX), with 12 already listed and 8 having filed listing applications. The combined total market capitalization of the 12 listed companies stood at HK$137.05 billion, with an average market capitalization of HK$11.42 billion. However, MicroPort Surgical Robot alone accounted for over HK$50 billion in market capitalization, indicating that the aggregate market capitalization of the remaining 11 companies was approximately HK$80 billion.

According to VCBeat’s statistics, in 2022, there were 15 initial public offerings (IPOs) of high-value medical consumables in China. The average market capitalization at IPO was RMB 15.38 billion, while the average year-end market capitalization stood at RMB 9.71 billion, representing an average decline of 36.82%.

This round of valuation correction in the secondary market has been influenced by multiple factors. From a macroeconomic perspective, geopolitical tensions, adjustments in industry policies, and the impact of the pandemic have all contributed to overall underperformance in the market.

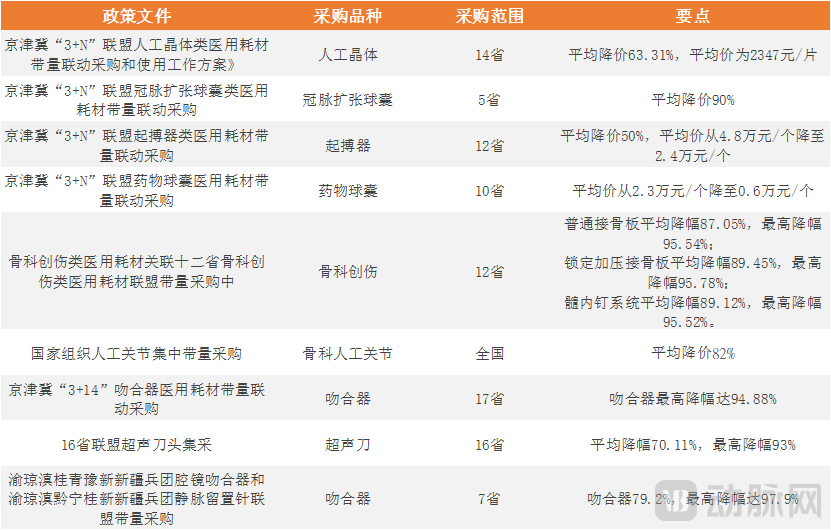

The most impactful policy has been the volume-based procurement (VBP) of high-value medical consumables. In 2021, more than ten VBP initiatives of varying scales were launched nationwide in China, covering products such as intraocular lenses, balloons, pacemakers, staplers, and ultrasonic scalpels. In terms of price reductions, VBP products saw maximum price cuts of 80%–90%, imposing significant cost-reduction pressures on domestic medical device manufacturers. Meanwhile, the market ceiling has been compressed, thereby limiting the valuation growth potential for listed companies in the secondary market.

Major Volume-Based Procurement Events in China in 2021

Meanwhile, biotech companies that went public earlier also face the issue of overvaluation.

Yi Hongxiang, Partner at the Shenzhen Capital Group’s Hongtu Medical Health Industry Fund, stated: “In the primary market, companies can secure financing based on their core technologies and market prospects; however, the secondary market places greater emphasis on financial performance and the realization of business results. Yet, many domestic medical device companies operate in markets that are still in the early stages of development, characterized by high product overlap and severe homogenization. Consequently, these sectors will undergo a process of clearing out inflated asset valuations.”

# Where Is Domestic Medical Device Financing Headed? Multiple Investors Believe the Market Will Gradually Rebound After Bottoming Out

Yang Zhenjun, a partner at Haoyue Capital, acknowledged, “China’s medical device industry still lags behind multinational giants in many segments. Domestically produced products require capital investment, market exposure, and feedback from physicians to gradually refine their offerings. The rapid influx of capital in recent years has been able to accelerate the development and upgrading of the medical device industry.”

The process of domestic substitution requires sufficient patience from the industry. The commercialization of medical devices is a lengthy endeavor, with a ten-year cycle not even considered long.

Yi Hongxiang stated, “From an industry perspective, obtaining a registration certificate for a product is merely the starting point; there remains a long road ahead for iteration and optimization. Looking at the development trajectory of Mindray Medical, China’s leading medical device manufacturer, it took more than three decades for Mindray to make its patient monitors competitive with imported alternatives. Therefore, regardless of how hot a sector may be, capital enthusiasm cannot obscure the challenges of commercialization.”

Markets are always changing, but value remains constant. The medical device sector continues to be dominated by several key segments: surgical robots, high-value consumables for vascular intervention, orthopedics, and medical imaging. Will the direction of these core segments shift in 2022? VCBeat has analyzed these major sectors by combining data with insights from investment interviews.

In the field of vascular intervention, 2021 saw the highest number of medical device companies go public. Multiple listed companies are present in the tracks of neurointervention, heart valves, peripheral intervention, and cardiac electrophysiology. In the primary market, the vascular intervention track also recorded the highest number of financing events. However, due to the impact of volume-based procurement (VBP), the market potential for vascular intervention has been viewed less favorably, leading to a gradual decline in the number of financing events in this sector.

The products directly impacted by centralized volume-based procurement (VBP) are primarily coronary drug-eluting stents and drug-coated balloons. Domestic products in these two categories are relatively mature, with high market shares but low market concentration; VBP has facilitated market consolidation. A review of the annual reports of MicroPort Scientific and Blue Sail Medical one year after the implementation of VBP for coronary stents reveals a significant increase in market concentration, with leading enterprises substantially expanding their market shares. In the long run, VBP has eliminated outdated production capacity and enhanced the competitiveness of leading domestic companies, thereby strengthening the global competitiveness of these industry leaders.

In other segments of the vascular intervention market, centralized procurement has also exerted significant disruptive effects. Due to the influx of numerous companies and severe product homogenization leading to market congestion—with at least five domestic enterprises developing the same product—there is also a strong possibility for the implementation of centralized procurement in these sub-sectors.

The investment rationale for the vascular interventional consumables sector is undergoing a shift.

Yi Hongxiang stated, “We conducted a comprehensive review of domestic manufacturers of high-value consumables for vascular intervention and identified an issue: while interventional consumables are valued in the market as high-value medical devices, the gross profit margins of major domestic players stand at only around 40%. In our view, a 40% gross margin does not characterize high-end manufacturing. This reveals that vascular intervention consumables are essentially manufacturing-driven, with relatively low technological barriers but stringent requirements for processing techniques. For the manufacturing sector, we place greater emphasis on corporate maturity, particularly a company’s operational capabilities in the global market.”

From the perspective of domestic financing, companies specializing in high-value consumables for vascular intervention continue to secure funding. Most of these firms are not early-stage startups; rather, those newly funded tend to focus more on overseas markets and are at later stages of growth. Investors place greater emphasis on their mature operational and commercial capabilities.

Take Acotec Medical, which secured $200 million in financing in 2021, as an example. Its vascular intervention product portfolio includes catheters, guidewires, balloon dilation catheters, scoring balloons, and innovative coated stents for coronary and peripheral vascular interventions. Although the balloon product segment faces a growth ceiling, Acotec Medical derives the majority of its revenue from overseas markets, with its balloon market share in Japan surpassing that of Terumo. The company’s strong competitiveness in international markets is the key reason it has garnered favor from multiple institutions.

Secondly, in the cardiovascular intervention sector, cardiac electrophysology has emerged as a standout field thanks to pulsed field ablation (PFA) technology.

The cardiac electrophysiology sector had previously maintained a relatively stable competitive landscape, with the domestic market dominated by multinational corporations such as Abbott, Johnson & Johnson, and Medtronic, while domestic participants primarily included Huitai Medical, Nuowei (Sinorhythm), and Jinjiang Electronics.

The Cardiac Electrophysiology Market Is Undergoing a Paradigm Shift Due to the Emergence of Pulsed Field Ablation Technology. Traditional catheter ablation for atrial fibrillation has been dominated by radiofrequency ablation and cryoablation, while PFA technology offers new hope for atrial fibrillation treatment thanks to its tissue selectivity during ablation.

More than 20 companies in China are developing pulsed field ablation (PFA) technology. The heated competition in this sector is driven, on one hand, by the rapid progress and favorable clinical outcomes of related products from overseas companies such as Boston Scientific. Boston Scientific’s PFA product, FARAPULSE, entered the “Green Channel” for Special Review of Innovative Medical Devices in late December 2021. On the other hand, the domestic electrophysiology market has historically grown at a relatively slow pace, and PFA technology presents an opportunity for Chinese firms to leapfrog competitors.

Yang Zhenjun told VCBeat: “We estimate that Johnson & Johnson’s market size in the electrophysiology field was around RMB 10 billion in 2021, with a patient population of tens of millions suffering from atrial fibrillation. This is a sector with enormous potential. In the past, traditional 3D mapping systems and catheter technologies had high barriers to entry, and domestically produced products did not stand out significantly; the main players were MicroPort, Jinjiang, and Huitai.”

Amid the new opportunities brought by pulsed field ablation (PFA) technology, whether more than 20 domestic companies in China can succeed remains questionable. Currently, the challenges facing PFA are twofold. On one hand, there are inherent technical barriers associated with PFA itself; only companies capable of rapidly overcoming these barriers will enjoy a first-mover advantage. On the other hand, Medtronic recently announced its acquisition of Afera, a three-dimensional (3D) mapping system company, for nearly $1 billion, suggesting that the integration of 3D mapping systems with PFA technology may represent a future direction. Other industry giants, such as Johnson & Johnson and Abbott, already possess both 3D mapping systems and PFA technology. Among Chinese companies, those equipped with both 3D mapping systems and PFA technology will hold stronger competitiveness and have a better chance of breaking through the competitive landscape.

Surgical robots have consistently remained the hottest segment within China’s medical device industry. In 2021, the most significant change in the surgical robotics field was the pronounced “head effect” (market concentration among top players), particularly in the laparoscopic surgical robotics segment.

“In the field of laparoscopic surgical robots, domestic companies primarily benchmark against the da Vinci Surgical System, which boasts the most mature commercialization prospects. More than 10 domestic companies have secured financing, and the leading players are relatively well-defined. In the field of orthopedic surgical robots, Stryker’s Mako joint surgery robot has demonstrated strong commercial performance, while a number of domestically developed joint surgical robots are also at advanced stages of clinical development. However, the domestic orthopedic robotics sector has not yet reached its endgame.”

As certain segments of the surgical robotics market enter maturity, multiple IPOs are expected to emerge in this sector. It is reported that several domestic surgical robotics companies are already preparing for initial public offerings.

However, some investors have pointed out that the valuation or market capitalization of surgical robotics companies does not equate to their true value. The current challenge for surgical robots lies in their persistently high costs. Although domestic surgical robotics firms are experiencing robust financing activity, they remain in the early stages of market expansion. Taking Stryker’s Mako orthopedic joint surgery robot as an example, while Mako has performed well overseas, China had only 17 such joint surgery robots installed in 2020, with approximately 250 procedures performed.

In addition to the increasingly entrenched market landscape in existing segments, a new development in the surgical robotics sector is the emergence of vascular interventional surgical robots.

An investor stated, “From a technical perspective, laparoscopic surgical robots pose the greatest development challenge, followed by orthopedic surgical robots, while vascular interventional robots have relatively lower barriers to entry. When evaluating interventional surgical robots, we place greater emphasis on their product synergy with other high-value vascular consumables and the overall layout of the industry chain.”

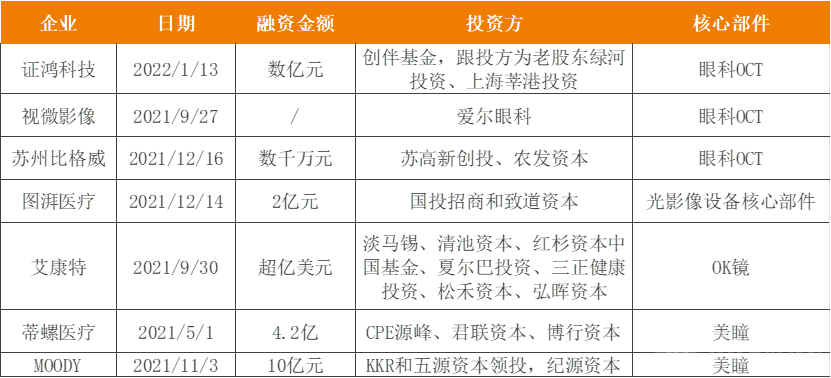

Sectors that saw a significant surge in popularity in 2021 also included ophthalmology. Within this sector, companies involved in optical diagnostic equipment such as OCT (Optical Coherence Tomography), intraocular lenses, orthokeratology lenses, and OK lenses all secured financing.

Major Financing Events in China's Ophthalmic Device Sector

The ophthalmology sector is driven by multiple factors, with strong growth in the ophthalmic device market being one of them., which can be seen from the performance growth of listed companies. OK lenses have become blockbuster products for Aikang Pushi and Eyebright Medical, demonstrating strong growth.

Aier Medical achieved revenue of RMB 325 million (+79%) in the first three quarters of 2021, demonstrating strong revenue growth. In terms of performance contribution, both Aier Medical’s intraocular lenses (IOLs) and its orthokeratology (OK) lenses, approved in 2019, experienced rapid growth. Sales of intraocular lenses reached RMB 154 million (+71.39%) in the first half of 2021, while sales of orthokeratology lenses amounted to RMB 44.22 million (+308%) during the same period.

Autek China’s operating revenue for the first three quarters reached RMB 996 million, a year-on-year increase of 64.22%. Its blockbuster product, orthokeratology lenses, generated RMB 426 million in revenue, representing a year-on-year growth of 37.61%.

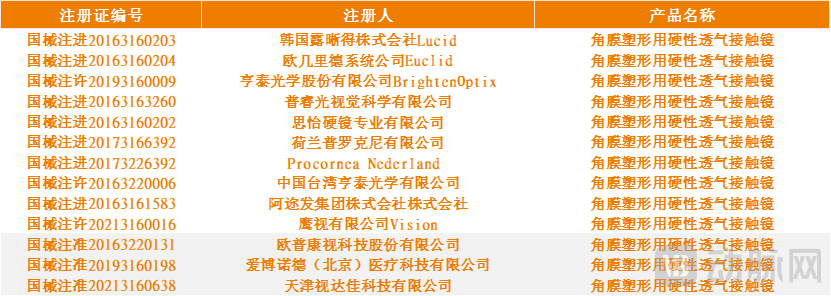

Second, the ophthalmology sector is also a market dominated by importers.Taking orthokeratology (OK) lenses as an example, there are currently 14 registration certificates in China, with only three held by domestic manufacturers.

In the intraocular lens (IOL) market, the domestic market size in China is projected to reach RMB 2.7 billion in 2023. Domestic companies dominate the low-end rigid IOL segment, while European and American enterprises essentially monopolize the soft IOL market. Key global players in the ophthalmic IOL sector include Alcon, Johnson & Johnson, Bausch + Lomb, and Zeiss. Major domestic companies include Haohai Biological Technology and Aier Eye Hospital Group’s subsidiary, Aibo Medical.

In the ophthalmology sector, colored contact lenses, with their consumer-oriented attributes, have attracted the highest amount of financing.In the first half of 2021, Aier Eye Hospital Group acquired a 55% equity stake in Tianyan Medicine for RMB 40 million. Tianyan Medicine is one of the few domestic manufacturers of colored contact lenses with independent proprietary technological capabilities.

In the colored contact lens industry chain, which is divided into upstream manufacturers and downstream brand owners, the entire sector attracted significant capital attention in 2021. Downstream consumer brands such as Moody and 4iNLOOK secured substantial financing, thereby driving a surge in popularity for upstream producers.

Moreover, high-end soft contact lenses present significant manufacturing barriers. Silicone hydrogel materials offer high oxygen permeability, which can substantially enhance the safety of lens wear and reduce the incidence of dry eye syndrome. Currently, colored contact lens products predominantly utilize hydrogel materials, and there are no mature production lines for silicone hydrogel soft contact lenses in China.

Meanwhile, colored contact lenses remain immune to volume-based procurement (VBP), unlike intraocular lenses, which are already included in VBP programs, and orthokeratology (OK) lenses, which face VBP risks. Currently, the domestic colored contact lens market features numerous brands and low concentration; following trends in consumer goods development, the head effect in the market is expected to strengthen in the future.

# Future Trends in Ophthalmology InvestmentYang Zhenjun, Partner at Haoyue Capital, stated, “Major ophthalmic conditions such as cataracts, glaucoma, macular degeneration, and dry eye disease all have substantial patient populations. Solutions for these diverse conditions continue to evolve, leaving ample opportunities for domestic enterprises.”

A significant portion of next year’s investment trends will be derived from this year’s developments, though new directions are also emerging. In 2022, focusing on the upstream sector began to become a key trend.

In fact, while upstream sectors have always been a key focus for domestic institutions, the scarcity of high-quality targets has resulted in fewer financing events for core upstream components.

In 2021, as the pandemic reshaped the global supply chain landscape, the upstream sector of the diagnostics industry experienced a surge. In both the diagnostics and pharmaceutical sectors, upstream life science reagents and tools have become the most prominent growth hotspots. In 2021, Mindray acquired HyTest, an upstream reagent manufacturer, for RMB 4 billion; Vazyme went public on the STAR Market; Nearshore Protein sought a listing on the STAR Market; and in the primary market, companies such as Biologix and Abclonal secured substantial financing rounds.

The upstream sector of the life sciences industry experienced a surge in 2021. On one hand, the COVID-19 pandemic generated substantial order demand for China’s diagnostics industry, leading to supply shortages of upstream raw materials. On the other hand, Chinese companies in certain niche segments of the life sciences industry have emerged as competitors capable of matching imported suppliers.

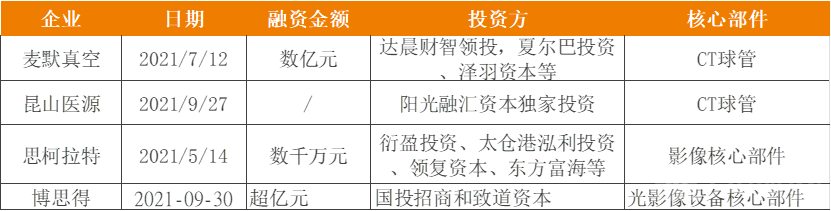

However, the upstream segment of the medical device sector still lacks high-quality investment targets, with financing activities primarily centered on core imaging components.

Yang Zhenjun, Partner at HaoYue Capital, stated, “The upstream core components sector, a key area of hard technology, has received substantial policy support. We believe that this sector will enter a period of developmental opportunity in the coming years, with its full market potential yet to be realized. Of course, the technological barriers in the upstream core components track are relatively high, requiring greater patience from investors to support companies through their growth journey.”

On December 28, 2021, ten departments—including the Ministry of Industry and Information Technology, the National Health Commission, the National Development and Reform Commission, the Ministry of Science and Technology, the Ministry of Finance, the State-owned Assets Supervision and Administration Commission of the State Council, the State Administration for Market Regulation, the National Healthcare Security Administration, the National Administration of Traditional Chinese Medicine, and the National Medical Products Administration—jointly issued the “14th Five-Year Plan” for the Development of the Medical Equipment Industry.

The Plan emphasizes strengthening industrial foundational capabilities and tackling key challenges in advanced basic materials, core components, and critical parts, specifically including hollow fiber membranes for Extracorporeal Membrane Oxygenation (ECMO) machines, medical AI chips, and proportional valves for ventilators. Regarding monitoring and life support equipment, the Plan indicates that it will promote the upgrading and performance enhancement of products such as dialysis machines and ventilators, while addressing technological challenges in new sensors, new materials, and microfluidic controllers.

In China’s medical device industry chain, numerous upstream core components still rely on imports. Against the backdrop of supportive policies, the upstream segment of China’s domestic medical device industry is poised for rapid development.

Hotspots in the medical device market constantly shift with changes in the industrial landscape. The long-cycle nature of the healthcare industry means that seeds sown this season will not blossom into full bloom in the next. As industry drivers increasingly revert to being propelled by genuine innovation, the only path to breakthrough lies in creating new value.