From IPO to Widespread Profitability, Medical AI May Still Need Five Years

It is not easy to find an appropriate word to describe medical AI in 2021.

The saga of IBM Watson’s distant quest for financial backing cast a somewhat shadowed pall over the industry’s early days. Yet before the sighs had fully subsided, Keya Medical filed its prospectus. In the ensuing months, regulatory reviews and approvals, financing and M&A activities, and supportive policies surged in succession, suggesting that AI was gaining increasing recognition from hospitals, investors, and government entities alike.

Medical imaging and healthcare informatics are the two fastest-growing sectors within AI. In 2021, disclosures from prospectuses, bidding documents, and contract transactions provided us with key data to assess the future development of AI.Imaging: From “0” to “1”; Informatics: From “1” to “10”。

As we usher in a new year, standing at the juncture of the old and the new, VCBeat has engaged in discussions with nearly ten industry experts to review 2021 and look ahead to 2022.

On January 15, 2021, Yidu Tech rang the opening bell on the Hong Kong Stock Exchange, followed closely by LinkDoc Technology, which filed its prospectus with NASDAQ in June. The successive listings of these two industry leaders mark the transition of next-generation healthcare IT companies from the primary to the secondary market, and highlight several commercialization models for medical AI.

Not coincidentally, 2021 also witnessed a surge in IPO filings within the medical imaging AI sector, with Keya Medical, Airdoc, Infervision, and Shukun Technology successively submitting their prospectuses. Multi-fold year-on-year revenue growth in 2020 has become the norm for medical imaging AI companies.

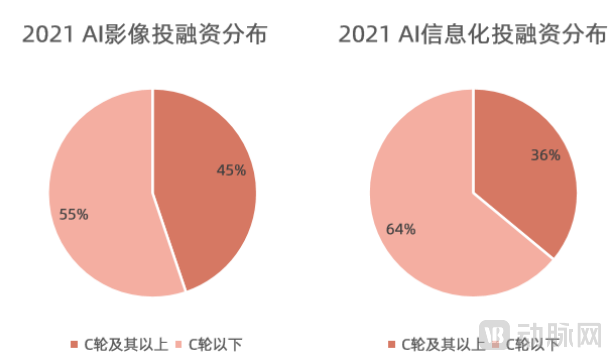

Correspondingly, the primary market has shown weakness, with data from VCBeat Research indicating thatIn 2022, there were 28 financing deals in the primary market for imaging AI, and 25 deals in the healthcare IT AI sector., in addition to the relatively low number of financing rounds, the vast majority of funds flowed to mid-to-late stage enterprises at Series C and beyond.

From a data perspective, IPOs were undoubtedly the “key” to medical AI in 2021, but when it comes to their significance, do IPOs truly deserve this title?

Over the past few years, in VCBeat’s research on medical AI, we have placed particular emphasis on investment and financing data. Since the surge in medical artificial intelligence began in 2015, companies in this sector have been continuously engaged in product development and hospital market expansion, with most generating annual revenues of less than RMB 10 million. During this phase, “fundraising” served as a relatively intuitive indicator of industry热度, reflecting to some extent the pace of AI companies’ product line development and hospital partnership progress. However, today, “profitability” has become a key consideration for leading AI firms.

What Determines Profitability? In the Short Term, It Is Product Quality and Genuine Demand.

“The root cause of weak commercialization is the lack of product quality, which fails to gain recognition from physicians.”A practitioner with years of experience in the AI field told VCBeat, “Some products suffer from poor quality, while others fail to meet clinical needs.”

“The rigorous screening of market needs has eliminated a large number of companies. To date, the remaining enterprises are almost all conducting stepwise R&D aligned with clinicians’ practical needs. After all, the AI in this context is ‘Healthcare + AI,’ not ‘AI + Healthcare.’”

Several AI companies that have filed prospectuses clearly meet the requirements. Since the registration and approval process was streamlined, Airdoc’s full-year revenue in 2020 increased by 50% year over year; Infervision achieved a year-on-year growth of 318%; and Shukun Technology saw its revenue surge 32-fold, exceeding RMB 50 million in just half a year. Although other companies did not disclose specific figures, they all reported substantial growth.

However, the current profitability of medical AI largely stems from the successful commercialization of products accumulated over the past few years. Dividends will inevitably fade one day; when that time comes, what will medical AI companies rely on for development?

The completeness of solutions is key to building long-term impact and expanding market reach for medical AI. Judging from the AI products currently approved by the NMPA,AI can only address specific, limited issues; however, radiologists are required to report all pathologies identified during image interpretation, including chronic obstructive pulmonary disease (COPD), pleural effusion, extra-pulmonary fractures, and cardiac-related conditions.Therefore, AI with single-point functionality may not necessarily reduce physicians’ workload; instead, it could prove counterproductive. In other words,, for AI enterprises to achieve long-term survival, they must adopt a comprehensive approach, initiating all-around upgrades.

Leading enterprises have mostly been building their own AI closed loops for the past 2–3 years.

For example, Keya Medical started with fractional flow reserve (FFR), an area with strong potential demand for AI applications, and gradually expanded from a single product to cover the entire diagnostic and therapeutic workflow for coronary artery disease. By strengthening its pipeline in cardiac treatment-oriented products such as balloons, the company has established a closed-loop in-hospital business model for the diagnosis and treatment of heart disease. With recognition from tertiary hospitals and a comprehensive suite of technologies, Keya Medical is likely to further expand across the full spectrum of cardiovascular diagnosis and treatment, leveraging its advanced technologies to reach a broader customer base.

Zhiyuan Huitu, Airdoc, and Tisu Technology have all made in-depth strategic moves in ophthalmology, attempting to expand from eye care into diabetes management. Zhiyuan Huitu and Tisu Technology have achieved remarkable success in their overseas endeavors. By partnering with optometry centers, Zhiyuan Huitu equips their fundus imaging devices with multi-disease AI-assisted diagnostic software for fundus images. Powered by AI, patients can gain comprehensive insights into their ocular health through a single fundus photograph. This examination can either serve as a supplement to myopia screening or be established as an independent ophthalmic testing service, helping residents detect ocular lesions more promptly and effectively, thereby enabling early intervention for eye diseases.

Both Huiyi Huiying and Deepwise Medical have established closed-loop systems built on the synergy between medical IT infrastructure and technical/clinical departments, emphasizing a closed loop of data and application flow, with a strategic bet on the future digitalization of clinical workflows. Huiyi Huiying’s product portfolio includes a big data cloud platform, a data middle-end, and AI-assisted diagnostic tools for the aorta, bones, breast, and other areas, with its entire closed-loop system already operational. Deepwise, meanwhile, holds a strong position in assisted diagnosis, having secured multiple Class III medical device certificates and published numerous medical AI papers in authoritative journals. Following its acquisition of Yitu Healthcare last July, Deepwise Medical has achieved a highly mature layout in the medical IT sector.

Beyond the aforementioned cases, companies such as LinkDoc Technology, Keya Medical, and Yizhun AI have also established their own closed-loop ecosystems. It thus appears that the previous practice of labeling enterprises simply as “AI + Imaging,” “AI + Informatics,” or “AI + Health Management” has become somewhat outdated. Most leading players now possess capabilities across multiple segments mentioned above. As competition in the medical AI sector intensifies and consolidates, it is also shifting toward new healthcare domains.

This trend has both advantages and disadvantages.On one hand, AI’s broader market options point to more efficient, clinically aligned solutions; on the other hand, today’s “breadth” largely stems from yesterday’s “points.”, but now we rarely see companies entering new “points.”

Sun Yuhui, CEO of Zhiyuan Huitu, explained in an interview: “The development of every medical AI product must undergo a process that includes data collection, algorithm development, clinical validation, and regulatory submission. Between 2019 and 2020, products accumulated from the past in the medical AI industry were launched intensively and obtained approvals one after another, thus creating the impression of a continuous stream of new products.”

However, from the perspective of a company’s R&D strategy, it is normal for initial products to have relatively high technical feasibility, while subsequent new product development involves greater challenges and requires more time. Additionally,There are few niche segments in the medical AI field that remain untapped., is also one of the reasons for this phenomenon.”

Some business leaders also believe that,The lack of new “highlights” is only temporary. Sales will be the most critical priority in the coming years.“Over the past few years, tens of billions in capital have been poured into medical AI. The seeds sown in the past are finally entering a harvest season as regulatory approvals are granted. The immediate priority, therefore, is to capitalize on this momentum and secure gains while the opportunity lasts. At this stage, the amount raised through IPOs or market capitalization is less critical, as is product diversity. What truly matters is leveraging Class III medical device certifications and the national performance evaluations of tertiary hospitals to rapidly capture market share. After all, only with profitability and sustainable development can companies explore new growth avenues.”

Between 2020 and 2021, medical AI achieved a transition from “novice to proficient” in regulatory approval. Within 24 months, the National Medical Products Administration (NMPA) issued a total of 23 Class III medical device registrations. Medical AI software for various anatomical regions received approval, including even clinical decision support systems (CDSS) centered on natural language processing (NLP).Senyi Intelligence also obtained the Class II medical device certification in October 2021.

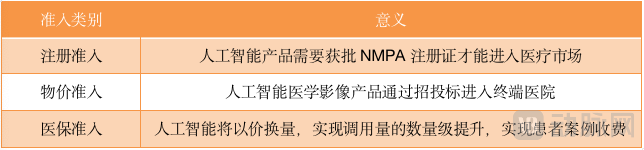

However, obtaining regulatory approval for market entry merely signifies that AI products are permitted to enter the healthcare market and be sold outside the hospital system. To embed closed-loop AI into comprehensive solutions within hospitals and secure a broader customer base willing to pay for them, medical AI companies must subsequently obtain approval for pricing inclusion and reimbursement under the national health insurance scheme.

Three Regulatory Hurdles for Medical AI

After obtaining NMPA approval for its CT-FFR DeepVessel FFR, Keya Medical took the lead in applying for pricing reimbursement approval, aiming to provide AI-driven medical services directly to patients through hospitals. Within one year, it secured market access for DeepVessel FFR in several provinces and municipalities, including Hebei, Anhui, Shandong, and Jiangsu. However, from an industry-wide perspective,The pricing approval for medical AI remains in its early stages, with fewer than 10 products approved nationwide.

"Broader health insurance reimbursement access is key for medical AI companies to achieve profitable scale, yet it remains a future that is harder for them to reach."

Looking abroad, the United States is a country where medical AI has achieved relatively successful commercialization, with many AI products gaining insurance reimbursement approval. This success is largely attributable to the separation of equipment costs and diagnostic fees for radiological examinations in the U.S., where labor costs are particularly high. In contrast, in China, radiological examination fees are low, not itemized separately, and primarily consist of equipment costs. This explains why AI applications can be billed and reimbursed independently in the U.S. at this stage, whereas a certain gap still exists in China.

Examples of AI Products Covered by Some U.S. Insurance Plans (Data Source: Medicare.gov)

Examples of AI Products Covered by Some U.S. Insurance Plans (Data Source: Medicare.gov)

Therefore, although revenue is important, it may still take several years for medical AI to complete both approval processes and realize every concept in its product pipeline.

In response, Sun Yuhui, CEO of Zhiyuan Huitu, stated, “The state strongly encourages the application of artificial intelligence in the healthcare industry. We believe that the next one to two years will witness a peak period for price approval; however, regarding inclusion in the national medical insurance reimbursement list, further policy-level support and promotion from the government are still required.”

Huiyi Huiying also expressed a similar view: “We have been striving to advance the inclusion of our services in the official pricing catalog, but this endeavor is contingent upon several prerequisites.First, the enterprise must hold the necessary certifications. Second, the frequency and timing of price approval applications vary by province each year. Third, in many provinces, even after price approval is granted, patients are still required to pay out-of-pocket for the product, and it typically takes at least one to two years of market operation before it can be included in the medical insurance reimbursement scheme.“Therefore, it will take enterprises another 4–5 years to accomplish these three tasks.”

Fortunately, policy support for medical AI continues to deepen. From “Healthy China 2025” and single-disease quality control to Diagnosis-Related Groups (DRG) and the high-quality development of public hospitals, the role of medical AI within hospitals is becoming increasingly significant, even influencing the smart hospital ratings and performance assessments of tertiary public hospitals.

Individual companies such as Huiyi Huiying and Shukun Technology are expected to turn a profit within the next two years, but it may take another five years for the medical AI industry to achieve widespread profitability.

Compared to the previous five years of uncertainty, we now have a clear plan, steady revenue, and multi-faceted support from hospitals, the government, and investors. The commercialization of AI is more than halfway through; from going it alone to walking side by side with partners, the first light of dawn is beginning to break.