Haoyue Capital In-Depth Analysis: Biopharmaceutical Industry Exits Bubble Phase and Returns to Fundamentals—Reassessing Core Drivers of Growth

In 2021, China’s biopharmaceutical industry witnessed remarkable achievements, setting all-time records for the number of clinical trial applications and ongoing clinical research projects reviewed by the Center for Drug Evaluation (CDE). With the implementation of a series of policies, including the Reform of the Review and Approval System for Drugs and Medical Devices and the Consistency Evaluation of Quality and Efficacy for Generic Drugs, domestic attention to clinical trials has continued to grow. Data from the CDE’s Drug Clinical Trial Registration Platform has also increased year by year; as of 2021, a total of 11,541 clinical trials with publicly disclosed Clinical Trial Registration (CTR) numbers were listed on the platform.While pursuing quantitative growth, domestic innovative enterprises have also achieved breakthroughs in multiple key technological areas. The COVID-19 pandemic has not hindered the robust development of China’s biopharmaceutical industry; on the contrary, effective epidemic control within the country has accelerated the rapid development and transformation of the entire biopharmaceutical technology sector. A wave of new technology companies has emerged across various niche segments. Interest in biologic macromolecule drugs continues to rise, with the number of newly marketed recombinant protein drugs and blood products more than doubling. In the field of cell and gene therapies, two CAR-T products were newly approved for marketing, achieving a breakthrough from zero. Additionally, significant progress has been made in the development of the world’s first inhalable vaccine. Capital markets have continued to increase their investment in the biopharmaceutical sector, with financing amounts multiplying, demonstrating the tremendous innovative vitality and growth potential of China’s biopharmaceutical industry.

We cannot help but ponder that the next decade may well be the period in which China’s biopharmaceutical industry transitions from catching up to surpassing its global counterparts. Accelerated regulatory reforms, increasingly robust government support, and the gradual opening of capital markets have all driven a significant transformation in China’s biologic drug market.

2021 also encountered a bottleneck, with a pronounced head effect in fundraising and frequent instances of innovative drugs breaking their issue price upon listing; in particular,, among Hong Kong-listed Chapter 18A companies positioned as innovative, nine have gone public since August 2021. As of today, eight of them have fallen below their IPO offering prices, with the sole exception being “MicroPort MedBot -B,” which is a medical device company. In comparison, last year saw four out of 22 Chapter 18A companies break their issue price on the first day of trading.The capital markets in 2021 appeared particularly harsh.A-share STAR Market listings in 2021: Cofool, Chengda, Hualan, Dizal, and BeiGene all broke their issue prices on the first day of trading.It has also served as a wake-up call to the industry, suggesting that the capital bubble may have already burst.FacingIncreasingly Rationalcapital markets, biopharmaceutical investors and entrepreneurs are all posing the same question,What Path Should the Future of Biomedicine Take?

Haoyue Capital believes that the biopharmaceutical capital market has experienced a short-term downturn,It does not alter the fundamental long-term bullish outlook for the entire industry.To answer these profound questions, it is necessary to examine the industry itself and the corresponding drivers in the capital market from three perspectives: the past, the present, and the future.

The Fifth Set of Listing Standards for the STAR Market and Chapter 18A of the Hong Kong Stock Exchange Listing Rules were introduced from the perspective of encouraging innovation, opening the door to public listing and financing for biopharmaceutical companies that are not yet profitable. Biopharmaceutical R&D involves long development cycles and substantial capital requirements. Without dedicated listing mechanisms tailored to such enterprises, Chinese innovative drug companies would have little chance of listing domestically. Over time, this would prevent outstanding local firms from receiving adequate support and deny domestic investors the opportunity to share in the industry’s growth dividends. However, due to historical reasons, both frameworks primarily rely on criteria such as “whether a specific clinical trial stage has been reached” and “whether valuation/market capitalization reaches a certain threshold in billions of yuan” as key evaluation metrics.

Although this design initially served as a useful aid for investment institutions in assessing project stages and quality, the rigid evaluation metric of “clinical stage + valuation” effectively turned the entire industry into an “open-book exam.” This inadvertently prompted numerous innovative drug companies and investors to pursue IPOs by, on one hand, aggressively licensing-in product pipelines that were close to meeting listing requirements, requiring only minimal additional clinical trials to qualify, and on the other hand, jointly inflating company valuations to meet listing thresholds sooner and facilitate rapid public offerings. This is not to deny the value of the license-in model; rather, it underscores the need for companies to thoroughly understand the mechanisms, targets, biomarkers, and competitive landscape of licensed-in drugs, clearly define their strategic positioning, and conduct in-depth secondary development based on this foundation. By way of analogy, if the IPO requirement is akin to running 100 meters, some companies either parachute athletes directly to the 90-meter mark or simply draw their own line and label it the “90-meter mark.” Such behavior, which creates price rather than value, is one of the key reasons behind the speculative capital frenzy and valuation inflation observed in the innovative drug industry in recent years.

“Price” is generated by the trading activities between two parties in the financial market, reflecting their consensus on the “value” of the same stock. When the two parties fail to reach a consensus on value, the price fluctuates in a specific direction to establish a new value consensus. In recent years, the perception that going public equates to sudden wealth and participating in IPO subscriptions guarantees profits has become deeply ingrained. This phenomenon is essentially the result of secondary market investors fully buying into the wealth-creation myths of the primary market and reaching an unconditional consensus on value.

As some innovative pharmaceutical companies burn through cash at an excessive pace, yet face either delays in product development or commercialization progress that falls far short of expectations, secondary market investors have come to realize, regarding certain individual stocks of these innovators, that the wealth-creation myth needs to be re-examined and that value recognition should not be overly hasty. This reflection in the secondary market has led to a reluctance to fully subscribe to initial public offerings (IPOs), resulting in two outcomes: either secondary market investors refuse to buy in, leading to frequent instances of stocks breaking their issue price (trading below IPO price) upon listing; or companies and investors anticipate such a break, making it impossible to offer shares at the current pricing, thereby leading to the withdrawal of the IPO. Both phenomena have occurred frequently over the past six months. As price expectations are transmitted backward through the chain, the equity valuation framework for innovative pharmaceutical companies is being reconstructed. This process will not be smooth, nor will it simply fluctuate in one direction; rather, it will involve a spiral and volatile adjustment.

The rapid development of China’s innovative drug industry in recent years has been driven by multiple factors. First, the domestic pharmaceutical supply, previously dominated by adjuvant therapies and low-end generic drugs, could no longer meet the demands generated by over two decades of economic growth, along with the corresponding levels of healthcare consumption and payment capacity. Second, multinational pharmaceutical companies have conducted clinical trials in China over the past decade, establishing Good Clinical Practice (GCP) capabilities and cultivating a pool of talent in clinical trial operations. Furthermore, contract research and manufacturing organizations (CXOs), represented by companies such as WuXi AppTec, Pharmaron, Joinn Laboratories, Asymchem, and Tigermed, built near-world-class infrastructure supporting drug development even before China had produced any world-class novel drugs. With demand, talent, and infrastructure in place, the only remaining constraint was the lagging regulatory approval policy for new drugs. The new drug reforms, introduced in response to the times, acted like a fire in winter, igniting the entire innovative drug sector. Nevertheless, we must remain aware that the industry still has significant shortcomings, and the “bucket effect” remains pronounced. While some “planks” may score 80 out of 100, others may still linger at 20–30.

For instance, within the innovative drug ecosystem, China’s foundational research remains relatively weak, resulting in a scarcity of fundamental innovation. Consequently, new drugs are still predominantly various types of “fast-follow” products. Furthermore, past clinical trials have focused mainly on mid-to-late stages, while early-stage clinical capabilities have lagged behind. This further limits China’s ability to conduct exploratory clinical trials when pursuing “First-in-Class” innovations. Additionally, in the sales segment, the large sales forces cultivated by traditional pharmaceutical companies during the era of generic drugs and adjunctive therapies may struggle to adapt to the new marketing model driven by medical education in the age of innovative drugs. Coupled with product portfolios that remain essentially fast-follow in nature, it becomes even more challenging to compete commercially with originator drugs that hold first-mover advantages. If domestic commercial capabilities are limited in this manner, competing effectively in developed country markets is even less feasible. Capabilities across all these links need to be strengthened one by one, which may take a considerable amount of time. However, there is no need for self-deprecation. Industries such as telecommunications, new energy, and aerospace in China have all undergone similar developmental trajectories, and the innovative drug industry will undoubtedly follow the same path in the future.

It is precisely for this reason that, over the coming extended phase of development, innovative pharmaceutical companies of all types must invest in foundational innovation and develop proprietary technologies, while also accurately defining their strategic positioning. Some teams can incubate products by building self-developed technology platforms and creating underlying technologies. Others can leverage licensed-in assets to capitalize on their strengths in efficient clinical execution, thereby accelerating clinical development in China and meeting the urgent needs of Chinese patients. Still other teams may find their competitive advantage not in developing their own pipelines, but in serving other pharmaceutical companies by outsourcing high-value-added activities such as R&D, manufacturing, and sales. In business strategy, we often observe that in niche sectors with relatively low levels of current development, rapidly establishing a competitive edge can facilitate quicker access to blue-ocean markets. By adopting differentiated positioning, companies can pave the way for rapid growth. The key lies in clearly recognizing one’s core capabilities, avoiding herd behavior in the selection of drug targets, development models, or valuation benchmarks, and instead precisely identifying one’s strategic position within a dynamically evolving industry.

We believe that from the past to the future, China’s biopharmaceutical industry has weathered many storms and gained valuable experience. We have witnessed both glorious eras and harsh challenges. As bubbles burst and superficiality fades, this journey—from inception and development to growth and maturity—is inevitable for any industry, sector, or ecosystem. A natural ecosystem primarily consists of four components: producers, consumers, decomposers, and the abiotic environment. Similarly, an innovative drug ecosystem should comprise researchers, developers, manufacturers, distributors, payers, users, and supporters across these segments. Only when various enterprises identify their precise roles can a healthy ecosystem be formed. A thriving innovative drug ecosystem will meet domestic clinical needs and make significant strides into the international market. Perhaps in 15 years, when we look back on the development of China’s innovative drug industry, we will find that the industry has become more robust after being tempered by trials, and that investors and entrepreneurs who have navigated economic cycles have grown stronger. The future of China’s innovative drug industry will be even brighter.

Main Text

2021 marked the beginning of the 14th Five-Year Plan period. To promote high-quality development during this period, it is essential to base efforts on the new stage of development, implement the new development philosophy, and construct a new development pattern. These several “new” elements permeate the entire Outline of the 14th Five-Year Plan. So, how are they specifically manifested? For instance, the release of the 14th Five-Year Plan for National Healthcare Security represents the first five-year plan in the field of healthcare security and serves as the overall blueprint for its development during the 14th Five-Year Plan period. The document proposes 15 key indicators and outlines requirements for building three major systems. Furthermore, developments in 2021—such as the Healthcare Security Law, the list-based system for healthcare security benefits, adjustments to the national reimbursement drug list, pilot reforms of medical service pricing, DRG/DIP payment reforms, national centralized procurement, and national price negotiations—demonstrate that China has adopted a comprehensive, multi-pronged approach to advancing its healthcare security system with distinct Chinese characteristics. Moreover, innovations in the pharmaceutical sector, consistency evaluations, and the definition of biomarkers have provided pharmaceutical companies with clear strategic directions. The issuance of important policies, including adjustments to the National Essential Medicines List, guidelines for rational drug use, and initiatives for the high-quality development of public hospitals, has also helped accelerate the integration of the R&D and commercialization chains for innovative drugs.

Under strong national policy support, 2021 was, overall, a year of remarkable achievements for domestically developed innovative drugs in China. The review and approval process for new drugs continued to accelerate. Supported by policies such as the National Major Special Project for New Drug Development and the National Key R&D Program, a batch of new drugs with significant clinical value that address urgent clinical needs were successfully launched, thereby meeting the public’s clinical demands. Currently, domestic pharmaceutical companies tend to adopt a dual-drive R&D model, namely “in-house R&D + external licensing,” to rapidly enrich their product pipelines. Statistics show that as of December 17, 2021, a total of 40 innovative drugs were approved for marketing in 2021, including 19 new anti-tumor drugs, 11 new traditional Chinese medicine (TCM) drugs, 3 new drugs for autoimmune diseases, 3 new antiviral drugs, and 4 new anti-infective drugs. Furthermore, with the rapid development of internet healthcare, pharmaceutical e-commerce, and other sectors, China’s biopharmaceutical industry is accelerating its efforts to advance the construction of medical informatization.

To better understand the direction of policy guidance for China’s biopharmaceutical industry in 2021, we have specifically selected several major guiding policies issued by various national ministries and commissions and conducted an in-depth analysis.

▶ Policy News:

In 2021, China successively issued policies such as the “14th Five-Year Plan for National Medical Security,” the “Medical Security Law (Draft for Comment),” the “Pilot Program for Deepening the Reform of Medical Service Pricing,” and the “Three-Year Action Plan for the Reform of DRG/DIP Payment Methods.”

VBInsight Viewpoint:

2021 was a critical period for healthcare reform. During this year, the Healthcare Security Law, the 14th Five-Year Plan for National Healthcare Security, and several related policies were gradually released. Domestically, a governance framework for healthcare security, comprising “three mechanisms and one system”—namely, the healthcare security payment mechanism, the medical price formation mechanism, the fund supervision system, and the pharmaceutical and medical service supply system—was basically established. We have observed several major dynamics:

1. Comprehensive implementation of centralized volume-based procurement (VBP) for pharmaceuticals and medical consumables. Multiple rounds of VBP documents issued at both the national and provincial/municipal levels have facilitated the accelerated market entry of domestically produced drugs and equipment from a policy perspective. For domestic companies, however, the long-term strategy lies in further strengthening the standardization of drug and device quality, accelerating the breakthrough of critical bottleneck technologies, and earning genuine market recognition through specialized, refined, and advanced technologies and products, thereby achieving the upgrade from “China to Global.”

2. Synchronize dynamic adjustments to medical service prices to create synergy with DRG/DIP payment system reforms. On one hand, the policy leverages price mechanisms to guide the allocation of medical resources toward underserved sectors, thereby better reflecting the value of technical and labor-intensive services. On the other hand, it aligns with the already piloted DRG/DIP systems to precisely define the supportive role of basic and essential medical care, while strictly controlling unreasonable diagnosis and treatment costs. Under this policy framework, the medical IT industry and third-party off-site clinical laboratories may benefit; meanwhile, domestic pharmaceutical companies face higher demands to continuously develop innovative therapies that meet disease management needs and demonstrate clear therapeutic efficacy.

▶ Policy News:

On October 26, the National Health Commission released the “Announcement on Soliciting Public Comments on the Detailed Rules for the Supervision of Internet-based Diagnosis and Treatment (Draft for Comment)” (hereinafter referred to as the “Draft”), which covers multiple aspects including supervision of medical institutions, personnel, business operations, quality and safety, and regulatory responsibilities in internet-based diagnosis and treatment.

VBInsight Viewpoint:

The Draft Opinion clearly defines the previously ambiguous and conflated concept of internet-based healthcare, delineating the boundaries between medical services, pharmaceuticals, and technological services. This establishes a framework where “medical practice remains medical, pharmaceuticals remain pharmaceutical, and AI remains technological,” thereby fostering the development of three distinct segments within the internet healthcare industry. First, we observe that the explicit requirements outlined in the Draft Opinion signal further standardization and normalization of online diagnosis and treatment. This will facilitate payers’ evaluation of the effectiveness of such services and support the broader and more timely inclusion of additional online diagnosis and treatment services within reimbursement coverage. Meanwhile, the requirement for online diagnosis and treatment to achieve maximum “homogeneity” with services provided by physical institutions, along with the value orientation of returning internet healthcare to “serious medical care,” will impact various platforms offering online diagnosis and treatment to differing degrees. We believe that compliant, leading internet healthcare platforms will possess greater potential for growth and expansion.

▶ Policy News:

On November 15, the Department of Drug Policy and Regulation of the National Health Commission released the "Administrative Measures for the National Essential Medicines List (Revised Draft)" for public comment.

VCBeat Insight:

Compared with the 2015 Measures for the Administration of the National Essential Medicines List, the Draft Revision released in 2021 specifically adds a pediatric drug catalog to the national essential medicines categories. Currently, China faces numerous challenges in pediatric medication, primarily manifested as a lack of drug varieties and dosage forms, as well as varying degrees of off-label use in clinical practice, all of which require timely improvement and enhancement. This revised Measures for the Administration of the National Essential Medicines List lists pediatric drugs separately, clarifying that they are mainly categorized based on drugs specifically indicated for children. In recent years, China has progressively intensified its efforts in “precision medicine.” Promoting the standardization of medication for typical diseases, systematically strengthening the layout of precision medicine research, and accelerating breakthroughs in prevention and control technologies for major diseases have become new driving forces for the development of China’s life and health industry.

▶ Policy News:

On December 3, 2021, the CDE released three major guidelines for gene therapy.

VBInsight Perspective:

Looking back at history, China embarked on gene therapy at an early stage. The first clinical trial of gene therapy in China dates back to 1991, only one year after the National Institutes of Health (NIH) in the United States conducted its first gene therapy treatment in 1990. Records indicate that as early as May 1993, the Ministry of Health had already issued the “Key Points for Quality Control in Clinical Research of Human Somatic Cell Therapy and Gene Therapy.” In 2003, China approved Gendicine, the world’s first gene therapy product. The first CRISPR clinical trial was also conducted in China. However, it was not until 2017 that the U.S. Food and Drug Administration (FDA) approved its first gene therapy. Although China started earlier, its progress compared with that of the United States and Europe during the same period was slow and quite limited, primarily constrained by issues such as the occurrence of specific adverse cases and inadequate regulatory oversight.

With the promulgation of the Technical Guidelines for Nonclinical Research and Evaluation of Gene Therapy Products (Trial) and the Technical Guidelines for Nonclinical Research of Genetically Modified Cell Therapy Products (Trial), a clear direction has been provided for pioneers in the field of gene therapy.

● We should draw lessons from history, place greater emphasis on the potential risks of gene therapy and the development of delivery technologies, and avoid severe adverse sequelae.

● Clinical protocols should place greater emphasis on long-term considerations; during the exploration of unknowns, more patient data should be collected and follow-up tracking conducted.

● Gene therapy is a future-oriented treatment and an untapped frontier for next-generation technologies, representing the cutting edge of medical advancement. It is essential to fully recognize the strategic significance of gene and cell therapies for China’s entire biopharmaceutical industry.

In 2016 and 2017, for the first time in history, multiple gene and cell therapy drugs were approved consecutively, ushering in a minor boom in the field. With the continuous optimization of delivery vectors, these technical hurdles have been gradually overcome, heralding the arrival of a new spring for gene therapy in China.

Appendix: Major Biopharmaceutical Policies in 2021

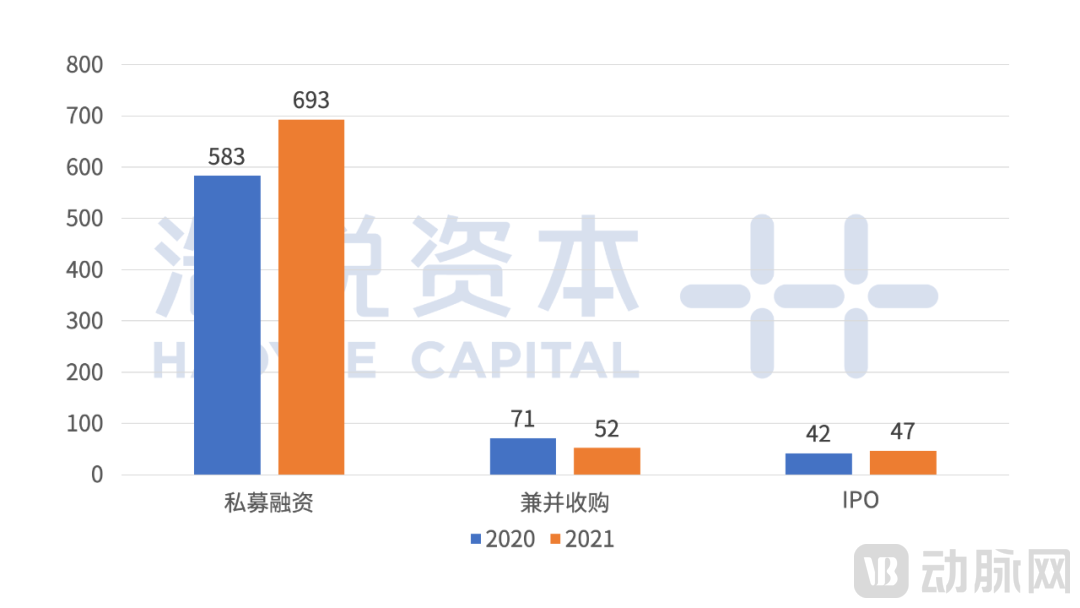

2021 passed in the blink of an eye. Looking back, the capital markets experienced another year of dramatic volatility. BeiGene achieved triple-listing status across three stock exchanges. Pfizer’s COVID-19 vaccine is projected to have generated over $36 billion in sales in 2021, equating to a profit of $1,000 per second, while China-made Sinovac vaccines challenged its leading position. The Beijing Stock Exchange commenced trading, and IPO activities remained robust, with SPAC listings suddenly becoming highly sought-after. Behind this seemingly prosperous facade, what reflections does it provoke? What insights can we draw from the vigorous development of the entire biopharmaceutical industry over the past year, as evidenced by the following data and events related to financing, mergers and acquisitions, and IPOs?

Private Equity Financing Market’s “Active Year”: Policy Support Accelerates Market Recovery

In 2021, venture capital activity in the global pharmaceutical and healthcare sector remained robust, with the total funding amount of the top 10 deals reaching a record high of over $8 billion. The biopharmaceutical sector, in particular, emerged as the primary battleground for major capital investments, characterized by a continuous stream of domestic and international financing events and heightened vitality in the capital markets.

The significant improvements in both technological standards and industry regulations in the domestic market are increasingly attracting entrepreneurs to choose China as the base for their technological innovation ventures. Our analysis suggests that, in addition to effective pandemic control, supportive policies implemented across various regions, and proactive monetary policies, the growing maturity of regulatory frameworks in the domestic biopharmaceutical industry, coupled with a standardized financial system, exerts a strong gravitational pull, thereby attracting and encouraging capital and enterprises to establish their presence in China.

Overall, as of December 31, private equity transactions in China’s biopharmaceutical sector saw a significant increase compared with previous years, while the number of M&A cases was slightly lower, and IPO activity rose. Publicly available data show that the financing landscape for “new drugs” in China was exceptionally active over the past year. As of December 31, a total of 693 financing deals were completed in the biopharmaceutical sector, with early-stage rounds (pre-Series B) accounting for more than 50% of all financed projects.

Table: Top Nine Domestic Events in 2021 Prior to Financing

We have taken particular note that in 2021, nearly all venture capital (VC) firms investing in healthcare were focused on one topic: vaccines. Undoubtedly, the vaccine sector, driven by the COVID-19 pandemic, continued to heat up in 2021. How vibrant was the vaccine landscape? In the second half of 2021 alone, four companies rushed toward initial public offerings (IPOs): Jindike Biotechnology, Aim Vaccine, Chengda Bio, and Clover Biopharmaceuticals. Significant financing also flowed into the vaccine sector. Yisheng Biopharma completed a Series B funding round exceeding RMB 800 million; Swire Microbes secured RMB 1.2 billion in financing; and Kangwei Weishi completed a Pre-IPO funding round of RMB 1.015 billion. Companies and investment institutions alike have actively moved to heavily “bet” on the coming golden decade for China’s vaccine industry.

The undisputed fundraising champion of 2021 was Abogen Biosciences, which set a record for the largest single pre-IPO financing round by a Chinese biopharmaceutical company, raising RMB 4.5 billion. Suzhou Abogen Biosciences is dedicated to the research and development of novel nucleic acid-based therapeutics (siRNA, mRNA, DNA), targeting indications such as oncology, infectious diseases, and personalized vaccines. With years of experience in nucleic acid drug development, the company has multiple candidates already in clinical trials in the United States, with several more projects expected to enter clinical trials and seek regulatory approval within the next three to five years. As a domestic pioneer in mRNA therapeutics, this is not its first appearance on the list. In 2021 alone, leveraging its strong R&D capabilities, it emerged as a major winner sought after by investment firms. Within just one year, through three rounds of financing, it attracted over RMB 14.5 billion in market capital, truly earning the title of “Fundraising Champion of the Year” and reflecting the market’s recognition of and enthusiasm for this sector.

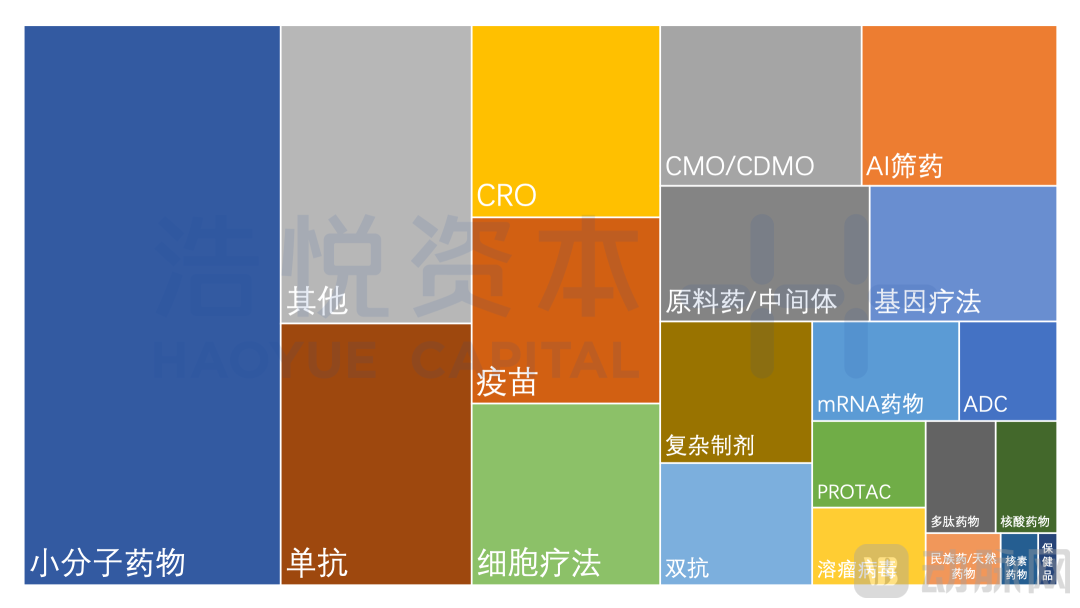

Beyond the booming vaccine sector, which specific sub-sectors attracted the attention of investment institutions in 2021? We found that the top three areas were small-molecule drugs, monoclonal antibody drugs, and AI-driven drug screening. Meanwhile, several other fields, including cell therapy, gene therapy, and CRO/CDMO/CMO services, witnessed multiple financing rounds. In terms of therapeutic indications, areas such as CNS disorders and infectious diseases also gained favor in 2021.

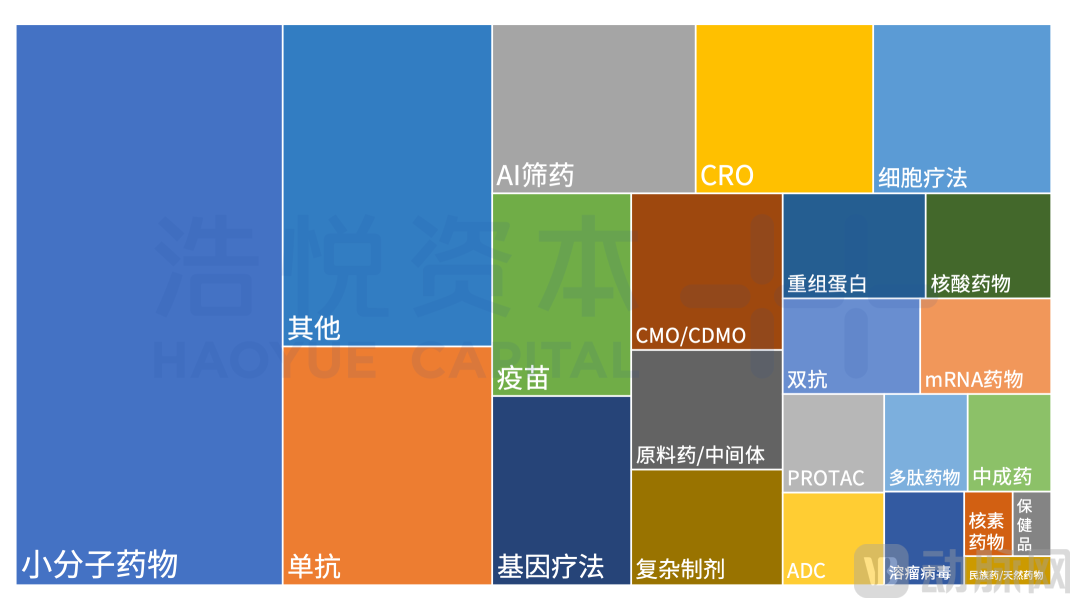

Although financing activities have been frequent, investment preferences between China and abroad are not entirely aligned. Using the United States as a benchmark, key investment areas pursued by domestic and international investors over the past year included small-molecule drugs, antibody-based therapeutics, gene therapy, cell therapy, and AI-driven drug discovery.

Top: China Bottom: United States

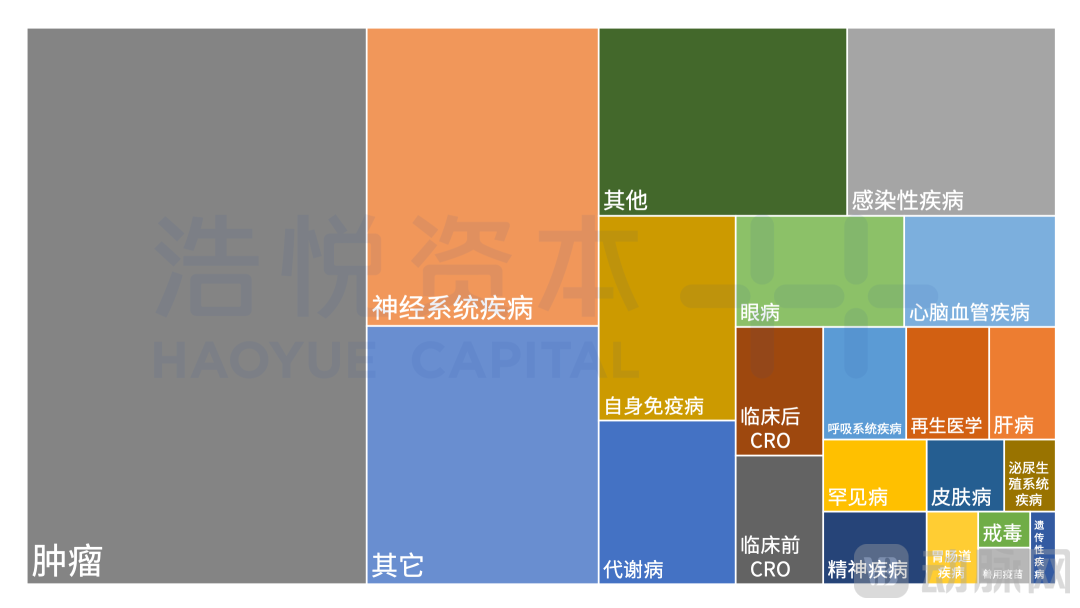

In 2021, it was noteworthy that beyond traditional innovative drugs, R&D in the oncology segment remained particularly vigorous. Leading biotechnology and biopharmaceutical companies also attracted significant attention. Meanwhile, cell therapy and gene therapy emerged as prominent fields, becoming highly sought-after investment opportunities.

Figure: Number of Financing Deals by Sub-sector

Surge in AI Drug Discovery Funding Fuels Demand for New Drug Development

In recent years, AI-driven new drug development has gradually gained market recognition. Its technologies are primarily applied in target discovery, virtual screening, compound design and synthesis, prediction of ADME-T and physicochemical properties, clinical trial design, management, and patient recruitment, as well as pharmacovigilance applications and real-world evidence generation. As the AI drug discovery boom continues unabated, substantial capital continues to flow into this sector. It is well known that new drug development faces challenges such as high risks, long cycles, and exorbitant R&D costs, coupled with a limited number of druggable targets. Overcoming these challenges has become a key focus in the pharmaceutical industry. Due to its ability to increase the probability of successful drug development, reduce potential costs, and improve R&D efficiency, artificial intelligence (AI) technology surged in popularity from 2020 through the end of 2021 and continues to attract significant market attention.

We note that Insilico Medicine recently announced the initiation of first-in-human trials for its ISM001-055 pipeline, rapidly advancing the clinical validation of novel drugs discovered through its end-to-end AI platform, marking a significant milestone in the AI-driven drug development sector this year.

Top 5 AI Drug Discovery Private Equity Financing Deals of 2021 (Domestic and International)

Data Source: Qimingpian

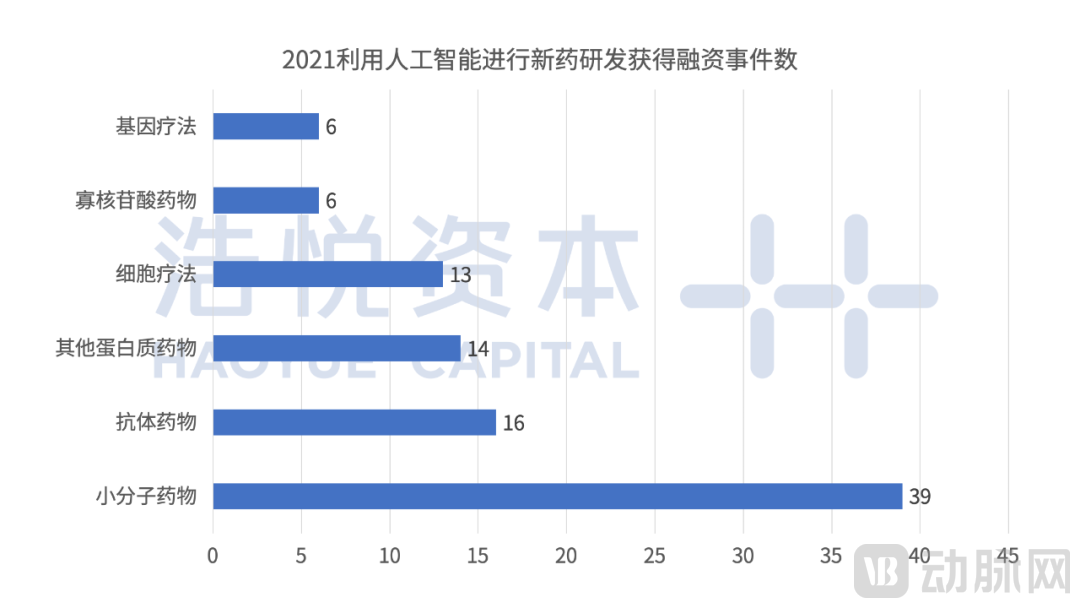

Based on incomplete statistics from publicly available information, the top five financing rounds raised a total of over $1.4 billion. In 2021, among companies applying AI technology to new drug development, small-molecule drug companies secured the highest number of financing deals, totaling 39. Antibody drugs and other protein-based drugs ranked second and third, respectively.

In summary, AI applications in new drug development continued to attract significant attention from the capital market in 2021. Among these, companies leveraging AI for small-molecule drug development secured the highest number of financing rounds, totaling 39. These companies have sustained investor interest by using AI to discover and validate novel drug targets, design lead compounds, or apply AI technologies to the development of proteolysis-targeting chimeras (PROTACs) and other novel small-molecule degraders.

Gene Therapy: Accumulated Strength Leads to Breakthroughs, Bringing New Hope for Disease Cures

Gene therapy has seen tremendous momentum both domestically and internationally in recent years, with a surge in financing activities making it a highly sought-after sector in the capital market. According to incomplete statistics, at least 42 gene therapy R&D companies worldwide disclosed financing events in 2021. A report by Grand View Research, Inc. projects that the global gene therapy market size will reach $10 billion by 2028, with a compound annual growth rate (CAGR) of 20.4%. Currently, more than 20 gene therapy drugs have been approved globally, and industry experts predict that approximately 40 gene therapy products will be approved for marketing by 2022. The CAGR of China’s gene therapy market has reached 12%. To date, there have been approximately 50 gene therapy financing events in China, with a total amount exceeding RMB 10 billion. Currently, the number of gene therapy clinical trials in China surpasses the combined total in Europe and ranks second only to the United States, with its growth rate leading the world. In addition to targeting cancer and various rare diseases with no existing cures, domestic gene therapy clinical trials also cover other conditions, such as cardiovascular and cerebrovascular diseases, diabetes, and HIV/AIDS.

In fact, gene therapy is hardly a novel concept. As early as 1963, Joshua Lederberg, an American molecular biologist and Nobel Laureate in Physiology or Medicine, proposed the concepts of genetic exchange and genetic optimization. Why, then, has it remained largely confined to the research stage? This is primarily due to the limitations of vectors required for gene therapy. Although currently used vectors have been optimized and engineered, they still suffer from various issues, such as immunogenicity, insertional mutagenesis potential, limited gene cargo capacity, and targeting specificity. These shortcomings fall far short of meeting the diverse requirements for vectors in gene therapy. However, with the increasing maturity of technologies such as CRISPR, the biological study and optimization of existing vectors, as well as the development of more diverse viral and non-viral vectors, will become key—and achievable—focus areas in gene therapy R&D for the foreseeable future. It is believed that this investment fervor will persist alongside successive technological breakthroughs into the next calendar year.

CNS Disease Drugs: An Unmet Market in Urgent Need of Capital Support

With the rapid development of society, central nervous system (CNS) disorders have garnered widespread attention in recent years, creating an urgent need for innovative and effective therapeutic approaches. There is a substantial unmet clinical demand for CNS drugs both domestically and internationally, and the market size is exhibiting a trend of rapid growth. In recent years, continuous technological advancements have enabled pharmaceutical companies and biotechnology firms to deliver impressive achievements, thereby revitalizing overall investment and financing enthusiasm in this field.

However, due to the complex etiology of central nervous system (CNS) diseases and the significant challenges in new drug development, few highly effective therapies have been introduced. Meanwhile, compared with their counterparts in developed Western countries, domestic pharmaceutical companies face substantial challenges in the R&D of CNS drugs. Only a small number of scientists, biotechnology firms, and pharmaceutical companies in China are dedicated to research in this field, while venture capital remains hesitant and adopts a wait-and-see approach toward biotechnology companies engaged in such research.

Drug development for neurological disorders remains a formidable challenge. Clinical diagnosis is highly complex, with a wide variety of disease types (including psychiatric disorders). Diagnostic classification criteria are frequently updated and subject to significant changes, entailing high specificity requirements. Although pharmaceutical companies face soaring R&D costs, scientists have not been deterred, and encouraging breakthroughs have emerged. For instance, Novartis’s flagship product, Zolgensma, the world’s first one-time gene therapy for spinal muscular atrophy (SMA), has been approved in more than 40 countries, achieving sales of $920 million in 2020. IONIS-MAPTRx is an antisense drug that selectively reduces the production of microtubule-associated protein tau (MAPT), or tau protein, in the brain for the treatment of Alzheimer’s disease (AD). Additionally, pediatric prolonged-release melatonin formulation (“PedPRM”) employs prolonged-release melatonin, a hormone involved in regulating the circadian clock and sleep, to treat conditions such as insomnia and anxiety.

Nucleic Acid Therapeutics Are Booming, Poised to Lead the Third Wave of Biopharmaceutical Innovation

The global COVID-19 pandemic has propelled the mRNA vaccine industry to unprecedented heights. The applications of mRNA vaccines extend beyond infectious disease prevention, holding significant potential in areas such as cancer therapy and immunological disorders. According to projections by Market Study Report LLC, a foreign institution, the global market for preventive and therapeutic mRNA vaccines is expected to grow at a compound annual growth rate (CAGR) of 32.0% from 2020 to 2025, reaching $5.98 billion by 2025.

The barriers to early-stage sequence design of oligonucleotide drugs are relatively low; however, the development of these therapeutics has been constrained by drawbacks such as instability and low delivery efficiency. The emergence of technologies like the GalNAc delivery system and chemical modifications has initially addressed issues related to drug delivery and stability. Following the approval of the first RNAi therapeutic in the United States in 2018, the field has witnessed a resurgence in research and development enthusiasm. In December 2021, the U.S. FDA approved Leqvio (inclisiran) for lowering low-density lipoprotein cholesterol (LDL-C). This medication enables long-term control with only two injections per year. Its approval marks the entry of nucleic acid therapeutics into the era of treating common diseases.

It is precisely because nucleic acid drugs can specifically upregulate or downregulate the expression of target genes, thereby controlling protein expression levels, that they demonstrate immense potential for development. Domestic companies are emerging continuously; in 2021 alone, there were 33 private financing events and one initial public offering (IPO) in China. The sustained recognition and increased investment from the capital market, coupled with the accumulation and consolidation of technology, talent, and supporting infrastructure, will inevitably drive the vigorous growth of China’s nucleic acid drug industry.

Synthetic Biology Focuses on the Cell Factory Track, with Long-Term Optimism for Biomanufacturing

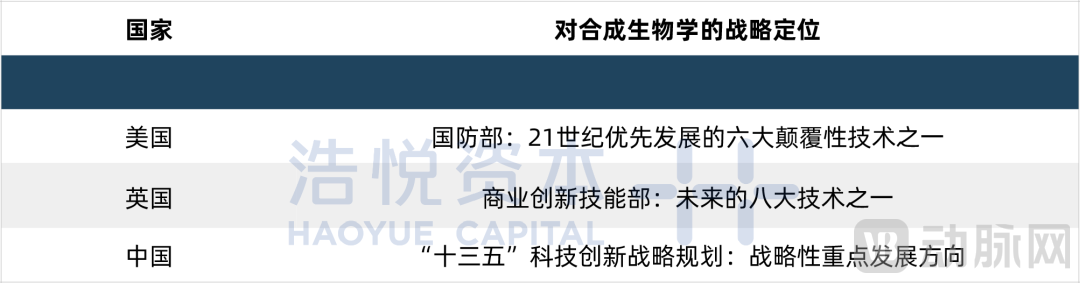

The essence of synthetic biology is to harness cells to produce desired substances for human benefit. Against the policy backdrop of “carbon neutrality,” with green manufacturing at its core, synthetic biology serves as a crucial cornerstone for achieving sustainable development. Compared with traditional chemical synthesis, synthetic biology offers miniaturization, recyclability, and enhanced safety; compared with conventional fermentation, it enables targeted intervention in cellular processes. Investment in synthetic biology has accelerated since 2015. In 2020, global financing for synthetic biology companies reached $7.8 billion (broadly defined), and in the first half of 2021 alone, funding amounted to $8.9 billion, surpassing the full-year total of the previous year and setting a new record. In recent years, capital market enthusiasm for the synthetic biology sector has continued to grow, and it has now become a key strategic development priority for countries worldwide.

After years of development, the field of synthetic biology has gradually shifted from screening based on extensive random mutagenesis to rational and semi-rational engineering. This design approach has significantly improved the efficiency of strain development. It is evident that by advancing data science, leveraging gene sequencing technologies, and integrating breakthroughs in AI-driven macromolecular prediction, it is possible to establish platform companies capable of building sequence-to-function correlation models. Such platforms can rapidly enable whole-genome cell factory engineering design, thereby enhancing microbial strain performance.

In the future, cell factory companies may focus on building capabilities in the following four areas:

(1)Efficiency.The three key metrics of primary concern to companies involved in cell factory operations are conversion rate, production rate, and product separation difficulty. These three metrics directly determine production costs and product competitiveness.

(2)Raw Materials.Currently, the cell factory industry primarily relies on food crops, such as corn, as raw materials. Utilizing biological waste, including crop straw and livestock manure, as feedstock is a critical challenge that must be addressed. A key direction involves employing novel waste pretreatment technologies to overcome the structural complexities of these materials and enhance the efficiency of converting waste feedstocks into monosaccharides. Furthermore, biotechnologies utilizing CO₂ and other compounds as primary raw materials have opened new avenues for exploring carbon utilization pathways.

(3)Standards.The industrialization of cell factories in China is still in its nascent stage. As production methods evolve, including the use of cell factories to produce novel substances, it is imperative to address the establishment of standards. The development of relevant standards and specifications will facilitate product promotion and certification, while also enhancing ease of use for customers. Companies that actively drive the establishment of industry standards will create the necessary conditions for large-scale technology adoption and will assume a leading position within the sector.

(4)Comprehensive capabilities.The cell factory industry spans multiple disciplines, requiring experienced technical teams in fields such as synthetic biology, cellular engineering, biochemical engineering, molecular materials, and pharmaceuticals. Meanwhile, companies in this sector face stringent demands for comprehensive R&D and management capabilities.

Amidst the Washout, the Value of Innovative Cell Therapies Begins to Emerge

In 2021, there were 36 private financing deals in the cell therapy sector. Among these, 25 involved immune cell therapies, 16 involved stem cell therapies (with some overlap due to companies developing stem cell-derived immune cell therapies), and 1 involved red blood cell therapy.

By analyzing the trends in related financing events, several key trends in immune cell therapy can be identified:

(1) Early signs of a "winner-takes-all" effect emerge in autologous CAR-T therapy, making it increasingly difficult for companies with early-stage autologous CAR-T pipelines to break through

(2) Trends in Indication Portfolio Strategy: A Gradual Shift from Hematologic Malignancies to Solid Tumors. Only 8 companies have pipelines focused exclusively on hematologic malignancies, while all 25 companies have portfolios covering solid tumors.

(3) Universal types are gradually taking center stage, becoming a key direction for future R&D, with over 60% of manufacturers positioning themselves in the universal-type segment.

(4) Financing events related to γδT, NK, TCR-T, and TIL therapies accounted for over 40%, indicating that novel immune cell therapies are gradually taking center stage.

The following changes have occurred in the field of stem cells:

(1) Stem cell therapy was once plagued by numerous irregularities, leading to a temporary halt in stem cell research. However, over the past two years, national regulatory authorities have frequently introduced policies to standardize the stem cell industry, gradually clarifying its development pathway.

(2) Research on stem cells is primarily focused on their differentiation into immune cells or into various other specific tissue-type cells to exert therapeutic effects.

Cell therapy is a rapidly evolving therapeutic modality that has already demonstrated transformative potential in the treatment of certain malignant hematologic tumors, and is poised to play an increasingly significant role in addressing solid tumors and other diseases in the future. As the potential of diverse cell therapy strategies continues to be unlocked, and complex bioengineering technologies such as gene editing undergo continuous iteration and breakthroughs, existing limitations are being progressively addressed. It is believed that next-generation cell therapies will ultimately be developed to improve the treatment of a wide range of human diseases, making the future of cell therapy highly promising.

The Market for Infectious Disease Drugs Spawned by COVID-19

The number of innovative drugs launched globally each year has remained relatively stable at around 50–60, with few new entries in the field of infectious disease treatment. However, the onset of the COVID-19 pandemic has spurred drug development in this area and garnered widespread recognition from investors. Most infectious diseases are typically short-term and non-fatal, while the application scenarios for drugs targeting resistant infections are very limited. This has made it difficult to achieve high returns on investment for anti-infective drugs, thereby dampening R&D enthusiasm. The global pandemic has reversed this trend, renewing the industry’s focus on the development of anti-infective agents. Capital infusion has also accelerated the market launch of new drugs in this field. Zai Lab announced that the National Medical Products Administration (NMPA) has approved the new drug application for Nuzyra® (omadacycline tosylate). Nuzyra is a novel antibiotic approved for the treatment of community-acquired bacterial pneumonia (CABP) and acute bacterial skin and skin structure infections (ABSSSI). As one of the world’s largest consumers of conventional antibiotics, China faces increasingly severe clinical resistance problems due to antibiotic overuse. The development of “super antibiotics” by domestic Chinese companies to combat drug-resistant bacteria represents an urgent strategic need in China. Furthermore, MicuRx Pharmaceuticals, which focuses on the treatment of infectious diseases, saw its Class I innovative drug, contezolid tablets (Youxitai), approved for marketing by the China National Medical Products Administration (NMPA) on June 1, 2021. Contezolid is a global first-in-class innovative drug designed to treat drug-resistant bacterial infections.

Stock Exchanges Across Regions Shine in Their Own Ways, with Uneven Listing Performances

Biopharmaceuticals is an emerging industry that has received significant attention in China’s 13th and 14th Five-Year Plans. Whether from the perspective of strengthening the national public health system or safeguarding public health and safety, the biopharmaceutical sector has always held a strategic position. Currently, there is a large number of listed companies in China’s biopharmaceutical industry, with active listing activities.

Since 2021, domestic biopharmaceutical companies have seen frequent initial public offering (IPO) activities, with numerous enterprises having sequentially submitted and gained approval for their IPO applications. These companies primarily span various niche sectors, including innovative drug research and development, innovative drug services, and proprietary pharmaceuticals.

Historically, the U.S. NASDAQ has been the securities market with the highest concentration of listed pharmaceutical and healthcare companies worldwide. As of November 2021, there were 953 listed pharmaceutical and healthcare companies on NASDAQ. By country of incorporation, U.S. companies accounted for 796 firms (83.5%), Israeli companies for 38 firms (4.0%), UK companies for 25 firms (2.6%), Chinese companies for 15 firms (1.6%), French and German companies for 10 firms each (1.0% each), and companies from other countries for 59 firms (6.2%). China boasts the world’s second-largest pharmaceutical and healthcare market, and its pharmaceutical and healthcare industry has experienced rapid growth in recent years.

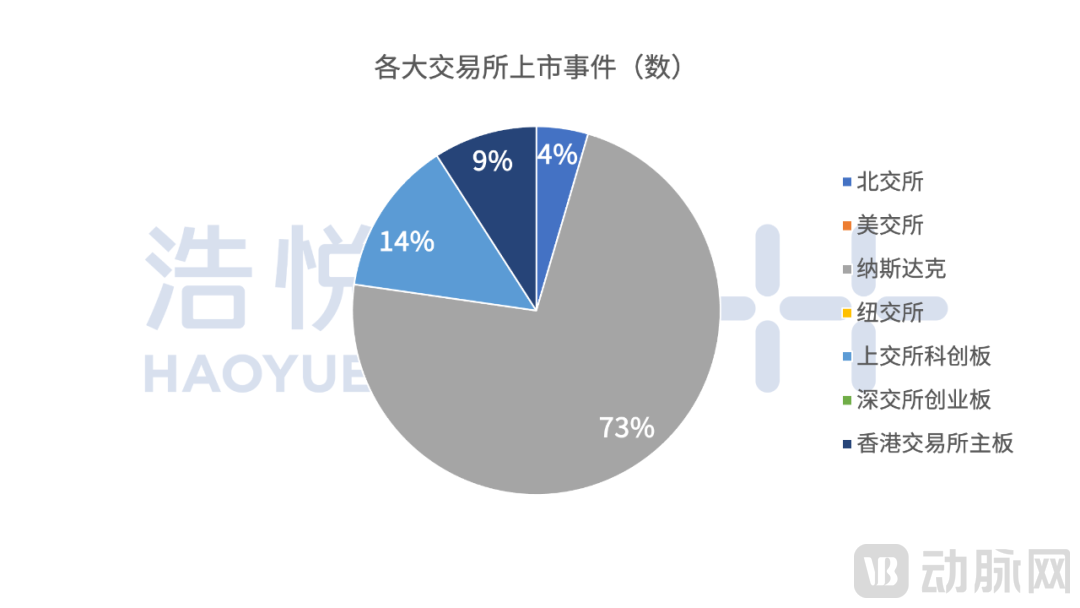

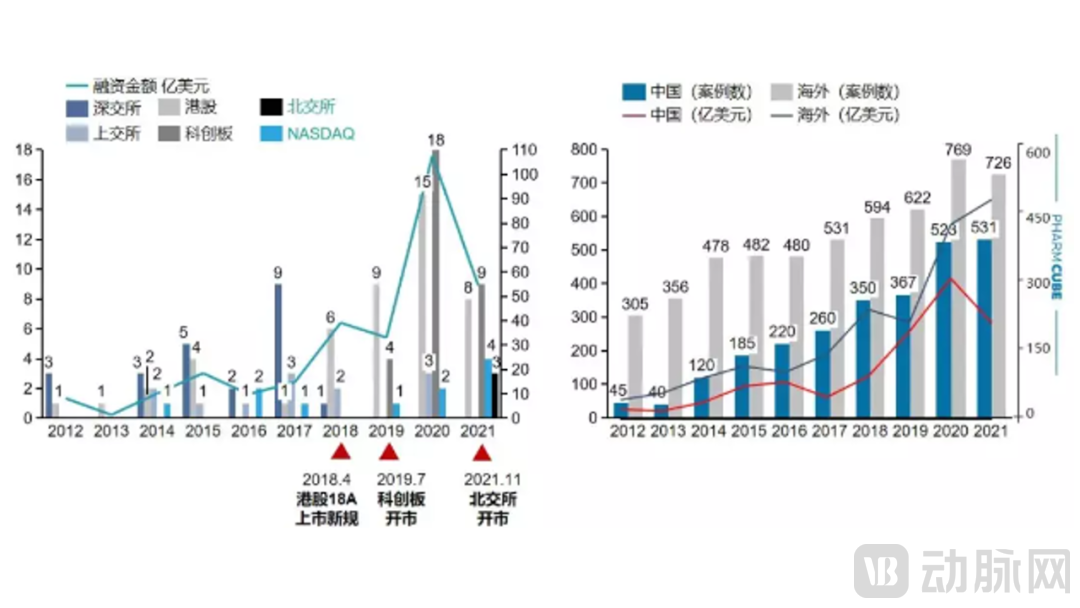

On the Hong Kong Stock Exchange, a total of 20 pre-revenue biotech companies successfully completed their initial public offerings (IPOs) in 2021. More than 20 healthcare companies have filed IPO applications, with over 90% originating from mainland China. In recent years, Chinese biopharmaceutical companies have intensively entered the capital markets. This trend has been driven both by the introduction of Chapter 18A of the HKEX Listing Rules in 2018 and the launch of the STAR Market on the Shanghai Stock Exchange in 2019, which opened an “IPO financing wave” for innovative, unprofitable biopharmaceutical enterprises; and by the continuous reform of China’s new drug review and approval system since 2015, which has injected strong momentum into the innovative development of China’s biopharmaceutical industry.

With the favorable domestic landscape and increasingly accessible pathways for biopharmaceutical companies, most Chinese biopharmaceutical firms have chosen the STAR Market as their listing destination in recent years. The advantages are self-evident, with its inclusiveness and openness becoming increasingly apparent. Against this backdrop, industry experts predict that the STAR Market’s significant industrial clustering effect, coupled with higher valuation levels, will continue to attract more small and medium-sized biopharmaceutical enterprises to list on the board. Notably, with the launch of the Beijing Stock Exchange, domestic companies now have an additional listing option.

Overall, the continued advancement of registration-based IPO reforms on the STAR Market and the ChiNext Board, coupled with stricter regulatory oversight, will facilitate the accelerated listing of biotechnology companies and may also enhance the quality of pharmaceutical firms listed on the STAR Market. As a strategic emerging industry, the biopharmaceutical sector has already entered a fast lane of development, driven by favorable policies such as the implementation of registration-based reforms on the ChiNext Board. With China’s epidemic prevention and control efforts showing sustained improvement and the market continuously recovering, industry insiders anticipate that 2022 will be another bumper year for initial public offerings (IPOs) among biopharmaceutical companies.

Data Source: PharmaCube PharmaInvest®

However, affected by factors such as the severe international situation and sluggish global economy, the performance of these biopharmaceutical companies listed in 2021 has been less than satisfactory, with the Hong Kong stock market showing the most concerning results.

Upon closer examination, unprofitable biopharmaceutical companies are facing increasing pressure in the secondary market due to a host of practical issues, including excessive valuations, a heavy reliance on license-in deals, and a lack of innovation. This necessitates a reevaluation of the IPO pathway for biopharmaceutical enterprises, placing greater emphasis on a professional assessment of their competitive positioning within their R&D tracks and their commercialization capabilities.

The essence of innovation lies in addressing patient needs. Any solution that effectively meets the substantial unmet needs of patients holds long-term value. This is precisely the underlying rationale behind the Center for Drug Evaluation (CDE)’s 2021 release of the “Guiding Principles for Clinical Development of Antineoplastic Drugs with a Focus on Clinical Value.” Taking PD-1/PD-L1 immune checkpoint inhibitors as an example, these therapies have emerged in recent years as novel anticancer treatments and offer new hope for saving the lives of cancer patients worldwide. Since the first monoclonal antibody was launched in China in June 2018, major pharmaceutical companies have intensified their efforts, resulting in the domestic approval of eight PD-1/PD-L1 monoclonal antibodies to date. However, skepticism has frequently arisen in the secondary market: Does the clustering of PD-1/PD-L1 developers in China risk causing overcapacity? Does it indicate a lack of genuine innovation? With twenty companies developing drugs targeting the same mechanism while thirty potential indications remain, do late entrants still have opportunities? We maintain that target innovation and technological advancement constitute the foundation for the sustainable development of pharmaceutical enterprises. Market launch is merely a process of validation. Beyond providing capital support, the market continually reminds entrepreneurs to return to the core of scientific research. Only by proceeding from practical realities can companies better earn market trust.

Rising Demand for Business Integration: Strategic M&A Facilitates Pharmaceutical Companies' Transformation

Since 2021, M&A, restructuring, and divestiture transactions in the pharmaceutical industry have continued unabated. Overall, large-scale M&A and restructuring activities are generally viewed positively by the market, as they aim to either accelerate drug development or strategically position companies within the pharmaceutical market. We analyze the integration logic behind M&A transactions in the biopharmaceutical sector in 2021: From a strategic perspective, it involves the integration between traditional pharmaceutical companies and innovative biotech firms; from a business perspective, it serves as an important channel for large enterprises to extend their operations, achieving complementary product portfolio integration or capacity supplementation, as well as combining R&D, manufacturing, and sales across the business chain.

According to incomplete statistics, as of November 29, 2021, a total of 52 merger and acquisition transactions occurred in China’s pharmaceutical sector, with a total transaction value of RMB 21.9 billion (excluding deals with undisclosed amounts). All these transactions reflected the aforementioned logic.

Surprisingly, companies in previously non-traditional hot sectors also garnered significant market interest in 2021. Taking Hengjuxing Pharmaceutical as an example, the acquirer was the listed pharmaceutical company Huaren Pharmaceutical (Stock Code: 300110), whose wholly-owned subsidiary acquired 100% equity of Hengjuxing Pharmaceutical for RMB 800 million using its own funds, thereby holding 100% equity of Hengxing Pharmaceutical. According to available information, Hengxing Pharmaceutical primarily focuses on the research and development of respiratory system drugs, psychotropic and narcotic tablets, and injectables. It holds approval numbers for 17 products, including Doxofylline Injection, and has completed Drug Master File (DMF) registrations for eight active pharmaceutical ingredients (APIs), including Doxofylline. This makes the primary objective of the acquisition easy to understand. Huaren Pharmaceutical operates in the large-volume parenteral (LVP) segment of the pharmaceutical industry, with four major production bases in Qingdao, Rizhao, Xiaogan, and Yuyuan, boasting a total capacity of 920 million bags/bottles. All its production lines have passed the certification under the new Good Manufacturing Practice (GMP) standards. Even so, competition in the LVP sector is fierce under healthcare reform policies such as volume-based procurement. The acquisition of Hengxing Pharmaceutical may provide certain support to Huaren Pharmaceutical. These are M&A cases driven by the need for business enhancement. However, the path ahead is challenging for pharmaceutical companies. How to strategically plan future development directions and expand their commercial footprints is now testing the leadership of major pharmaceutical enterprises.

As capital operations and project exit strategies become increasingly diversified, mergers and acquisitions (M&A) have gradually emerged as a central theme in the global development of the biopharmaceutical industry, with M&A investment in China’s health sector becoming increasingly active.

Based on the types of mergers and acquisitions (M&A) in 2021, domestic M&A trends are primarily categorized into two major groups:

First, listed traditional pharmaceutical companies acquire innovative technologies to pursue innovative transformation and achieve a breakthrough.

Transactions such as Huadong Medicine’s acquisition of Daol Biologics and Sinopharm’s acquisition of Kangming Bio reflect that acquiring innovative technologies and introducing external technology platforms have become the primary strategic choices for traditional pharmaceutical companies under China’s current policy environment, thereby supplementing and enriching their product pipelines. Furthermore, after being acquired, innovative biotech firms can leverage their parent companies’ mature manufacturing and commercialization capabilities to accelerate their entry into the revenue-generating phase of R&D.

Second, expand the business scope through M&A to continuously broaden the commercial footprint.

Take WuXi Biologics, a CDMO giant, as an example. In 2021, it spent RMB 1.437 billion and RMB 691 million to acquire Suqiao Bio and Pfizer Hangzhou, respectively, and completed the acquisition of Bayer’s drug substance manufacturing facility assets in Wuppertal, Germany, for EUR 150 million, continuously expanding the group’s global production capacity. For industry giants, continuous M&A of existing market capacity has become their primary strategy to consolidate their leading position and sustain expansion.

Furthermore, a review of M&A transactions over the past two years reveals that large-scale deals have been predominantly led by consortia or investment institutions. For instance, last year, Century Capital spearheaded the privatization of Taibang Biological Group, a plasma-derived biopharmaceutical company. In 2021, FountainVest Partners acquired 100% equity interest in Langdi Pharmaceutical for a total consideration of RMB 5.8 billion. It is foreseeable that there will be an increasing number of cases where investment institutions directly engage in managing corporate operations in the future.

According to incomplete statistics, in the first 11 months of 2021, there were a total of 52 mergers and acquisitions (M&A) transactions in China’s pharmaceutical sector, with publicly disclosed transaction amounts totaling RMB 21.9 billion. In the same period of the previous year, there were 72 publicly disclosed biopharmaceutical M&A transactions, with a total transaction value equivalent to nearly RMB 50 billion. Compared with the same period last year, both the number and value of transactions declined significantly, particularly in the number of large-ticket M&A deals. The largest M&A case last year was Taibang Life Science Group, with a total transaction value approaching RMB 10 billion, and there were more than 10 transactions exceeding RMB 1 billion in size. In contrast, only three such cases occurred in 2021. Both in terms of value and volume, it is evident that institutional investors are becoming increasingly cautious about mid-to-late-stage projects.

Table: Top 10 Disclosed M&A Transactions in China’s Biopharmaceutical Sector in 2021

First, the M&A activities and investment strategies of global pharmaceutical giants have gradually influenced the domestic market environment in China, stimulating transaction activity. Second, current policies such as volume-based procurement (VBP) and dynamic adjustments to the National Reimbursement Drug List (NRDL) have accelerated consolidation within the pharmaceutical industry, leading to a slight overall increase in M&A activity compared to the past five years. Frequent VBP effectively results in a “winner-takes-all” scenario, while demand for innovative drugs has kept China’s biopharmaceutical M&A market consistently active. Pharmaceutical companies are leveraging M&A to enhance the flexibility and innovative capacity of their product portfolios.

However, it is important to note that China is still in the process of innovation-driven transformation. Therefore, in the short term, M&A activity may be hindered by a scarcity of high-quality targets. Biopharmaceutical companies listed in Hong Kong are facing increasing pressure from the secondary market, which may instead lead to a polarization in M&A deals: high-quality targets will become more distinct and tend to pursue independent development and exit through IPOs; meanwhile, companies with mediocre quality may find it even more difficult to achieve an exit via either route in a tight market environment, resulting in an overall decline in M&A transactions.

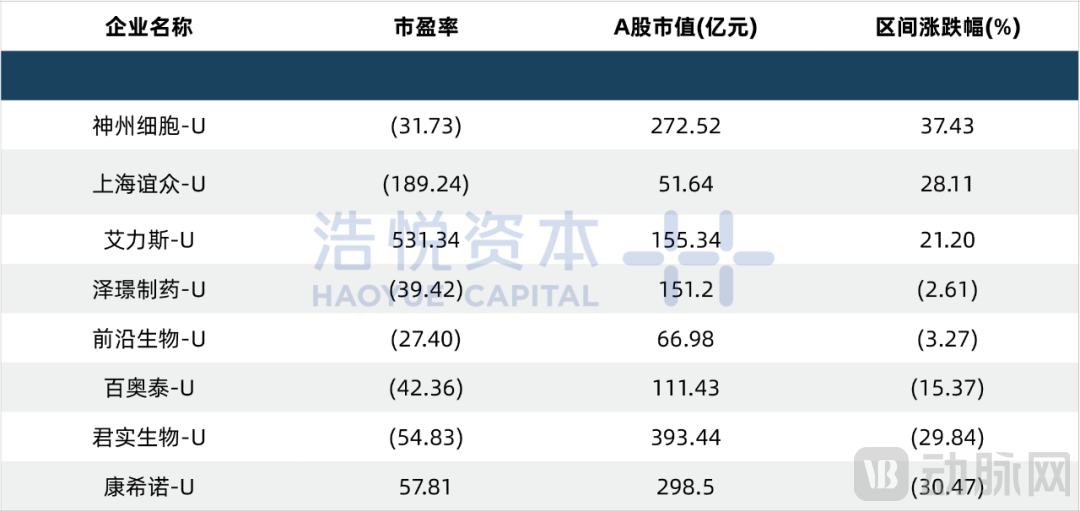

As of December 5, 2021, there were a total of 4,193 listed companies on the Nasdaq, including 1,088 in the biopharmaceutical sector. Among these more than 1,000 biopharmaceutical companies, only 291 exhibited positive stock price growth, while over 300 experienced declines exceeding 50%. The majority of biopharmaceutical firms saw their stock prices halved, with the Nasdaq Biotechnology Index (XBI) plunging by 60% compared to the beginning of the year. (Interestingly, Chinese concept stocks in the biopharmaceutical sector recorded an average decline of around 30%, which was lower than the overall index drop. Does this indirectly suggest that Chinese biopharmaceutical companies have gained recognition in the international market?)VCBeat Capital believes that the gap between Chinese and international biopharmaceutical companies in terms of talent and information has narrowed significantly. In recent years, supported by domestic pharmaceutical policies, an increasing number of outstanding Chinese scientists from multinational corporations (MNCs) have returned to China to start businesses. Given time, it is believed that Chinese biotech firms will deliver more surprises. Furthermore, the underperformance of Nasdaq-listed biotech stocks can be partly attributed to earlier substantial price increases driven by loose monetary policy, record-high U.S. inflation at a 40-year peak, and soaring U.S. Treasury yields. Additionally, the ongoing pandemic has severely disrupted supply chains. The primary challenge facing the U.S. government remains whether to prioritize inflation control and economic stability or maintain the status quo to support financial markets.

Table 1 Performance of Chinese Biopharmaceutical Stocks Listed Overseas (2021.01.01–2021.12.05)

Data Source: East Money Choice Data Terminal, compiled by Haoyue Capital

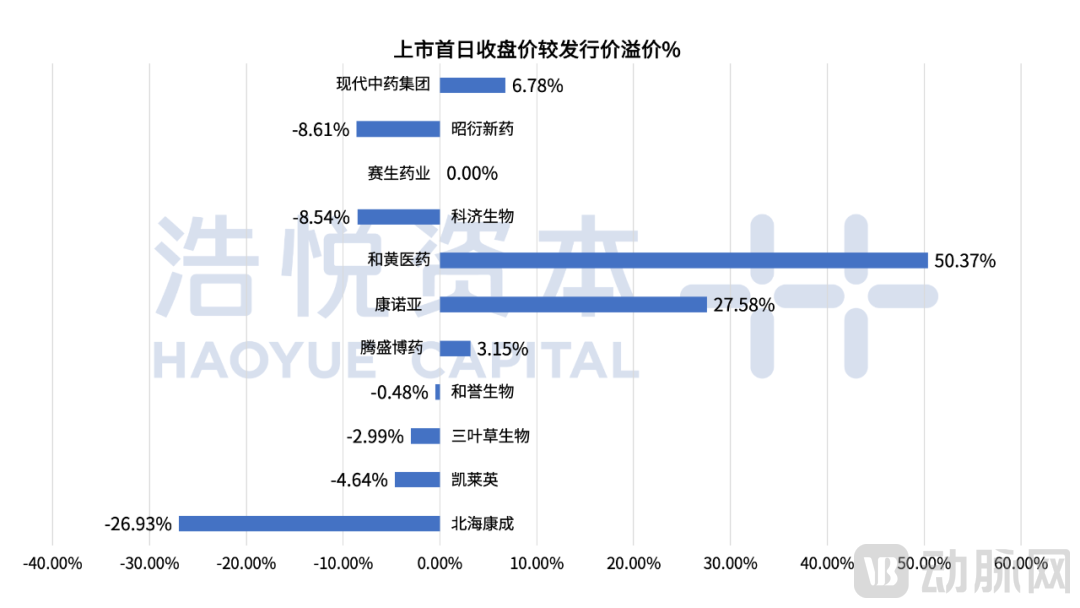

As of December 5, 2021, there were a total of 40 companies listed under Chapter 18A of the Hong Kong Stock Exchange. Two companies went public in 2018, eight in 2019, thirteen in 2020, and seventeen in 2021. The acceleration of the listing process fully reflects the vigorous development of China’s biopharmaceutical enterprises. However, stock price performance has been far from optimistic. Among the 17 companies that went public in 2021, eight experienced trading below their IPO prices (break-even failure). Moreover, only ten companies recorded positive stock price growth in 2021. The most outstanding performer was Kintor Pharmaceutical, with an interval gain of 435%, primarily driven by the promising potential efficacy of its core product, pyrotinib (an AR antagonist/androgen receptor antagonist), in treating COVID-19. High valuations of new listings, tightening market liquidity, and cooling investor sentiment were the direct triggers for the widespread break-even failures among new stocks. Nevertheless, the few companies that achieved positive stock price growth have made it clear to the industry that genuine source innovation and strategic market positioning are essential to enhancing core competitiveness and risk resilience.

Table 2. Biopharmaceutical Companies Listed Under Chapter 18A with Positive Stock Price Growth (January 1, 2021–December 5, 2021)

Table 3 Biotech Innovation Companies Listed Under Chapter 18A That Broke Their Issue Price on the First Day of Trading (2018–December 2021)

Data source: East Money Choice data terminal, compiled by Haoyue Capital

As of December 5, 2021, there were a total of 364 companies listed on the STAR Market. Since its launch in March 2019, the listing pace of biopharmaceutical technology companies on the STAR Market has gradually accelerated: 15 companies went public in 2019, 28 in 2020, and 31 in just the first 11 months of 2021. Currently, biopharmaceutical technology companies account for 20.3% of all companies on the STAR Market. In terms of the number of listed companies, the biopharmaceutical sector of the STAR Market is basically on par with those of NASDAQ and the Hong Kong Stock Exchange (HKEX).Among these biopharmaceutical technology companies, 24 experienced a decline of more than 10% during the period, while 41 saw an increase of more than 10%. Notably, 20 companies achieved gains exceeding 100%, indirectly reflecting secondary market investors’ recognition of biopharmaceutical enterprises. In terms of market capitalization, valuations on the first day of listing ranged from RMB 1 billion to RMB 20 billion, fully demonstrating the STAR Market’s inclusiveness toward biopharmaceutical companies.Since the STAR Market began allowing unprofitable companies to list, biopharmaceutical enterprises, especially innovative drug developers, have been flocking to the board, leveraging secondary market fundraising channels to accelerate the R&D of innovative drugs. The overall performance of STAR Market-listed biopharmaceutical companies in 2021 surpassed that of HKEX Chapter 18A-listed companies and NASDAQ-listed biopharmaceutical stocks. VCBeat Capital attributes this phenomenon to two main factors: First, A-share liquidity is significantly better than that of the Hong Kong and U.S. stock markets, and domestic investors show greater tolerance toward biotech companies. Second, domestic R&D investment in innovative drugs continues to increase, with innovative drug companies transitioning from previous fast-follow strategies to becoming truly innovative enterprises, as more Best-in-Class (BIC) or First-in-Class (FIC) drugs enter clinical stages.Additionally, amid current international instability, some companies are initiating the process of dismantling their red-chip structures to return to the A-share market. Does this mean that an increasing number of biopharmaceutical companies will choose to list on the STAR Market in the future? Only time will tell.

Table 4 Performance of Unprofitable Biopharmaceutical Companies on the STAR Market (January 1, 2021–December 5, 2021)

Data source: East Money Choice Data Terminal; compiled by Haoyue Capital

Overall, the secondary market performance of biopharmaceutical companies in 2021 was less than optimistic. Under the transmission effect from the secondary market, primary market investors also entered a period of investment uncertainty. Nevertheless, it is undeniable that the biopharmaceutical sector still holds significant growth potential. A brief valuation reset can help innovative drug companies achieve more sustainable and healthy development. Product differentiation and the pace of leadership are key indicators for evaluating such enterprises. Truly “specialized, refined, distinctive, and innovative” (SRDI) biopharmaceutical companies will continue to gain full market recognition. Investors need to cut through the fog and identify SRDI biopharmaceutical companies that are genuinely driven by clinical value.

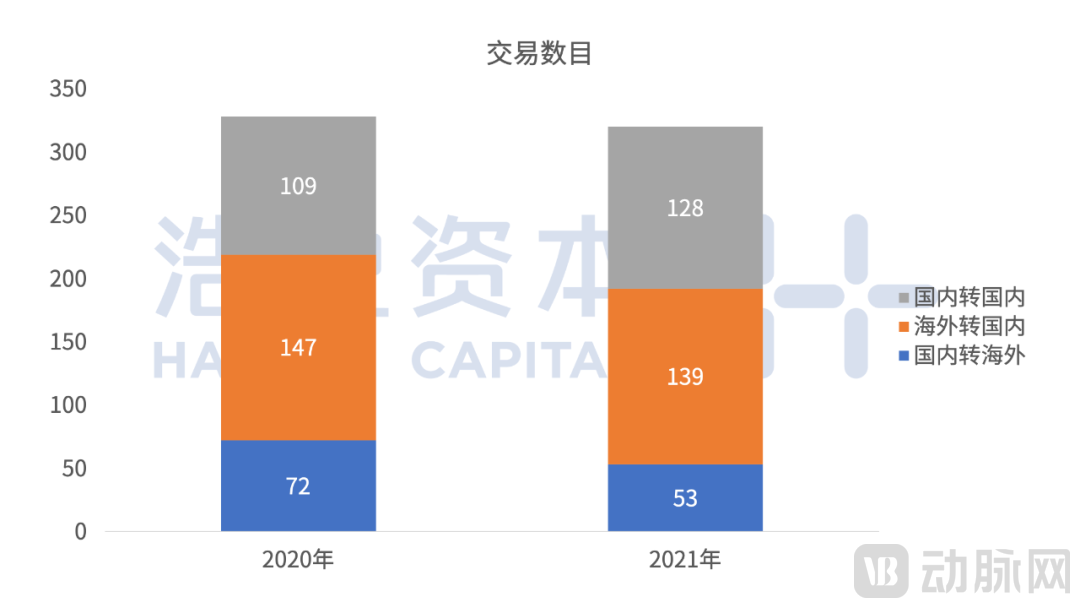

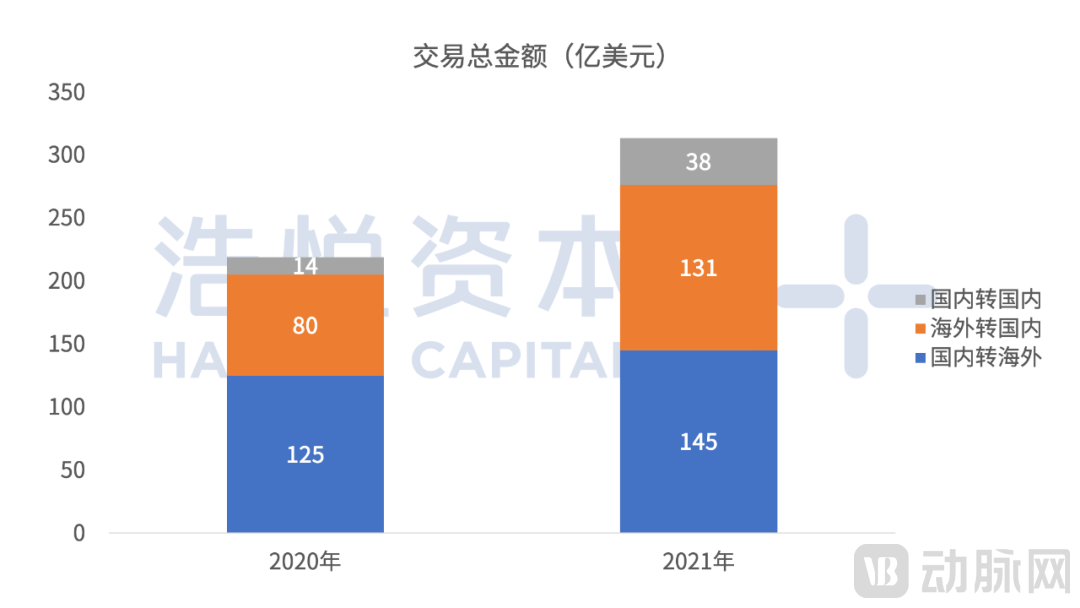

Big Pharma holds significant advantages in clinical drug trials and commercial market launch. Its long-term cultivation and substantial resource accumulation in terms of workforce size, capital volume, and organizational management capabilities create barriers that Biotech firms cannot effectively overcome in the short term. In contrast, due to their smaller scale, leaner staff, and more flexible R&D and management systems, Biotech companies are more adept at achieving continuous breakthroughs during the preclinical research stage. In mature pharmaceutical markets such as Europe and the United States, Big Pharma continuously licenses in innovative drug intellectual property (IP) from Biotech firms, forming robust commercialization models. As China’s pharmaceutical market further opens up, domestic enterprises are increasingly prioritizing transactional collaborations with pharmaceutical companies both domestically and internationally. In 2021, license-in and license-out transactions involving Chinese companies occurred frequently, with a total of 320 deals, basically comparable to the 328 transactions recorded in the previous year. However, statistics on the total disclosed transaction value reveal a different trend: while the amount stood at $21.9 billion in 2020, it surged far beyond that level in 2021, reaching $31.3 billion, indicating a growing scale of financial cooperation in the pharmaceutical sector. The same trend is evident in upfront payments: the total upfront payments amounted to only $1.3 billion in 2020, whereas in 2021, this figure increased by 2.4 times year-on-year, reaching $3.1 billion.

Figure: Statistics on the Number of Transactions in China’s Pharmaceutical Sector, 2020–2021

Data Source: PharmaCube Database

Figure: Statistics on Total Transaction Value in China’s Pharmaceutical Sector, 2020–2021

Data Source: PharmCube Database

Chinese pharmaceutical companies’ license-in deals for overseas projects are no longer limited to small molecules, antibody-drug conjugates (ADCs), and antibody-based therapies; they have also begun to explore and strategically position themselves in modalities such as nucleic acid therapeutics and gene therapy. Notably, Hansoh Pharmaceutical (03692.HK) secured exclusive rights to Silence Therapeutics’ mRNAiGOLD platform to develop siRNA drugs targeting three specific targets. Additionally, Hansoh licensed from OliX Pharmaceuticals (226950.KQ) the exclusive commercialization rights in China for drug candidates targeting liver-related cardiovascular, metabolic, and other diseases, leveraging OliX’s proprietary GalNAc-asiRNA platform technology. The total value of these two small nucleic acid drug transactions involving Hansoh Pharmaceutical (03692.HK) reached as high as $1.773 billion. Zai Lab (ZLAB.O) has licensed in four small-molecule oncology drugs from Blueprint Medicines (BPMC.O), Turning Point Therapeutics (TPTX.O), and Mirati Therapeutics (MRTX.O), actively expanding its oncology pipeline. Undoubtedly, Zai Lab (ZLAB.O) is one of the most mature players in China in terms of executing overseas license-in transactions.

Table: Top 15 License-in Deals of Overseas Projects by Chinese Pharmaceutical Companies in 2021

License-out deals from China to overseas markets are also significant. Novartis (NVS.N) partnered with BeiGene (BGNE.O, 06160.HK, 688235.SH), acquiring the primary overseas rights to Ociperlimab. This deal set another record for Chinese license-out transactions, following the PD-1 monoclonal antibody agreement reached by the two parties in January earlier this year. RemeGen (09995.HK) entered into an exclusive global license agreement with Seagen (SGEN.O) for the development and commercialization of its novel HER2-ADC drug, RC48 (disitamab vedotin). With a total value of up to $2.6 billion, this transaction marked both the first license-out of a domestically developed ADC drug and a new record for the highest value of a single innovative drug license-out deal from China at that time. Additionally, HighTide Biopharma, which utilizes single-cell technology for antibody discovery, partnered with FibroGen (FGEN.O) on innovative therapies for cancer and autoimmune diseases, with a deal value reaching $1.125 billion. The technological platforms, clinical development, and commercialization capabilities of China’s local innovative drug developers have garnered increasing attention and recognition internationally.

Table: Top 15 Overseas License-Out Deals by Chinese Pharmaceutical Companies in 2021

Furthermore, license-in and license-out transactions among domestic pharmaceutical companies have become increasingly active. Although the transaction volumes are not as large as those of cross-border collaborative projects, they reflect that Chinese pharmaceutical enterprises, in addition to focusing on the development and commercialization of their own products, are also adopting diversified cooperation models to appropriately mitigate high R&D risks, accelerate their commercialization processes, and strengthen competitive barriers. In 2021, there were nine deals with transaction amounts of no less than RMB 1 billion, predominantly involving oncology pipeline projects, including five small-molecule oncology collaborations and three oncology antibody partnerships. All licensees were domestically listed pharmaceutical companies, such as BeiGene (BGNE.O, 06160.HK, 688235.SH), Everest Medicines (01952.HK), Innovent Biologics (01801.HK), and Hengrui Medicine (600276.SH). This model is now emerging in China, signaling that major Chinese pharmaceutical companies are entering a transformation era aimed at benchmarking against multinational pharmaceutical corporations.

Table Top 15 License-in Deals of Domestic Projects by Chinese Pharmaceutical Companies in 2021